Abstract

Few existing studies of federal disaster aid examine the logics that govern assistance access. Applying the lens of administrative burdens, we identify four onerous aspects of the Federal Emergency Management Agency’s (FEMA) housing aid program—regulations regarding application unit, documentation, and damage sufficiency, and long processing times—that prompt assistance delay or denial for in-need households. Our empirical strategy pairs administrative records from FEMA on denied applications (N = 206,157) after Hurricanes Katrina and Rita with survey (N = 354) and in-depth interview data (N = 106) from a longitudinal study of low-income survivors of Katrina. Results show that applications from poor, communities of color were disproportionately denied or delayed due to burdensome program requirements and their implementation. Interviews and survey evidence elucidate the compliance costs and suggest a toll on post-disaster well-being.

Climate change and population settlement patterns are rendering more people vulnerable to disaster exposure (IPCC 2014). Over the past half century in the United States, populations have grown in counties bordering the Gulf and Atlantic coasts (NOAA 2013), and tropical cyclones have strengthened and become slower moving (Sobel et al. 2016). The result of these dual patterns is a dramatic increase in the number of billion-dollar hurricanes that upend the lives of many people, including the most vulnerable (Smith 2020). As federal disaster aid becomes increasingly costly in this context, social scientists must conceptualize it as an essential part of the fragmented social safety net. Yet scholars have historically paid limited attention to government assistance from the Federal Emergency Management Agency (FEMA)—the agency tasked with administering most disaster aid—relative to other government programs.

A nascent but growing body of scholarship documents racial and socioeconomic disparities in federal dollars from disaster aid programs (Domingue and Emrich 2019; Kamel 2012; Kousky 2013; Muñoz and Tate 2016). Differences in disaster aid correlate with unequal population recovery at a community level and economic trajectories at an individual level (Howell and Elliott 2019; Raker 2020). Examining disaster assistance across affected places or people using dollar amounts allows scholars to quantify relative differences in FEMA assistance and the effects on recovery outcomes. Yet, by focusing on dollar amounts, we argue that existing studies fail to consider how inequalities may emerge in the process of accessing aid, leading some in-need people to receive delayed assistance or none at all. A handful of studies have shown how problems with contact information and insufficient damage are frequent reasons for application denials and needs for appeals (García 2021; Kousky 2013). Others have conceptualized long processing times in disaster rental assistance programs as a form of “temporal domination” (Reid 2013, 743). What remains largely unanswered is how people navigate the bureaucracy of federal aid in a period of acute need for housing, and what the scale and consequences of denial are for well-being in the recovery stage (Abramson et al. 2010).

In this article, we address this gap using mixed-methods data from two sources: administrative data from FEMA on applications for housing and property damage after Hurricanes Katrina and Rita in New Orleans; and survey and in-depth interview data from the Resilience in Survivors of Katrina (RISK) Project, a longitudinal study of low-income mothers who lived in New Orleans at the time of Katrina. Denials for government assistance are a strategic site to investigate the scale and consequence of administrative burdens, but rarely do scholars have data to interrogate these processes. Drawing on Pamela Herd and Donald Moynihan’s (2018) framework, we examine denial disposition codes from administrative data to estimate the scale of burdens, and the survey and interview data from the RISK project to understand the experiences and effects of burdens on post-disaster well-being and recovery. Results from a tripartite analysis—a descriptive examination of administrative data, qualitative coding of in-depth interview data, and regression analyses on survey data—demonstrate three key findings.

First, regulations surrounding appropriate documentation; proof of homeownership, residency, and occupancy; and damage substantiation and sufficiency constituted a large share of denied applicants, contributing to an overall denial rate of 53 percent. Although we are unable to decipher true eligibility from the administrative data, both justified and unjustified denials contribute to burden, and the magnitude of denials suggests a level of burden whose costs borne by in-need people may be greater than the benefit of their function to prevent fraud. This trade-off imbalance is particularly striking given evidence of relatively little fraud in other disaster cases and the documented struggles of public officials to implement policies after Katrina given the unprecedented need for government assistance. Additionally, bivariate associations point to disproportionate denials due to documentation and duplicate applications in zip codes with higher poverty rates and more people of color, suggesting that these policies or their implementation may have exacerbated racial and socioeconomic inequalities. Second, qualitative data from the RISK project elucidate how in-need families experienced and navigated federal disaster assistance programs. In particular, the burdens of program compliance and the nature of interactions with FEMA bureaucrats were taxing on many of our respondents who had been denied assistance or experienced long waiting times for aid. Third, an analysis of survey data estimates the association between assistance denial and psychological distress. We find that being denied FEMA assistance, which interview data showed frequently occurred alongside burdensome experiences with policies or their implementation, correlated with greater psychological distress compared to receiving assistance, net of housing damage and pre-disaster mental well-being.

BACKGROUND

Despite the common refrain that disasters level the playing field, the consequences of disasters are not distributed equally across groups (Tierney 2019). Instead, marginalized people, such as low-income and people of color, bear a disproportionate share of disaster exposure and negative consequences (Fothergill and Peek 2004; Tierney 2019). During Hurricane Katrina, flood damage was concentrated in predominately poor and Black communities with low-quality housing (Donner and Rodríguez 2008). Because low-income households are less likely to be able to prepare for disasters or have enough insurance to buffer their adverse effects (Fothergill and Peek 2004), government assitance may be a vital lifeline. FEMA’s Individuals and Households Program (IHP), in particular, is an essential part of the post-disaster safety net for many marginalized people, and is often not their first encounter with government programs and bureacracies.

ACCESS TO FEMA POST-DISASTER ASSISTANCE

To date, most research on FEMA and other post-disaster government assistance focuses on variation in aid amount (Grube, Fike, and Storr 2018; Muñoz and Tate 2016). Our understanding of the process of applying for and receiving federal disaster assistance, as well as the consequences of aid denial, is more limited. A small number of studies explore these topics, documenting how applying for post-disaster federal aid is often slow, difficult, and complicated (Kamel 2012; Reid 2013; Texas Advisory Committee to the U.S. Commission on Civil Rights 2021), with eligibility requirements that result in increased aid denial (García 2021). Megan Reid (2013), for example, examined Hurricane Katrina survivors’ experiences with FEMA’s rental assistance program, drawing on in-depth interviews and field observations with displaced Katrina survivors. She finds that FEMA policies and practices were oriented toward a middle-class family structure and socioeconomic status, and that low-income people with complex family structures were forced to wait while the state investigated their applications, leading to negative psychological and material consequences.

More recently, scholars have examined the process of applying for FEMA aid after Hurricane Harvey in Texas and Hurricane Maria in Puerto Rico. In the case of the latter, approximately 60 percent of applications to FEMA’s IHP were denied in Puerto Rico after the storm (NLIHC 2018), which Ivis García (2021) finds to be typically based on inadequate proof of home ownership, inability to make contact for inspections, or duplicate applications. His study was a descriptive qualitative one, with a small sample size. Chenyi Ma and Tony Smith (2020), however, provide quantitative evidence that most of the homes in Puerto Rico that were deemed “not economically feasible to repair” by FEMA belonged to low-income households, emphasizing how access to disaster assistance can exacerbate economic inequalities. A recent report by the Texas Advisory Committee to the U.S. Commission on Civil Rights (2021) describes how inconsistent eligibility criteria and complicated applications led to challenges for vulnerable populations applying for aid after Hurricane Harvey, ranging from requirements to produce extensive documentation to lack of language access for a diverse, multicultural population. More anecdotally, journalistic accounts of federal assistance after Harvey suggest that FEMA aid is often difficult to access and varies in its utility (Young 2017), given that many households were denied aid for some reason or another, such as a missed inspection. Although these studies offer insight into the experiences of disaster survivors applying for and being denied disaster assistance, missing from the extant literature is a unifying theoretical framework to understand these isolated denial experiences in a broader social and political context.

ADMINISTRATIVE BURDENS IN DISASTER AID

To fill this gap, we apply the concept of administrative burdens (Herd and Moynihan 2018) to the case of federal disaster assistance for housing and property damage. Herd and Moynihan define administrative burden as “an individual’s experience of a policy’s implementation as onerous” (22), identifying three distinct types of costs that individuals experience in citizen-state interactions: learning costs, compliance costs, and psychological costs. Learning costs include the time and effort individuals exert to learn about a given program and determine eligibility requirements; compliance costs include the information and documentation needed to establish eligibility and the financial costs of accessing services; and psychological costs include the stigma that can arise from participation in unpopular programs, or the stresses associated with application or participation. This framework centers individuals’ experiences of state actions, rather than the state actions themselves. In the introduction to this issue, Herd and her colleagues (2023) offer a clear summary of administrative burdens and how they often function as a mechanism to reproduce inequalities.

Administrative burdens tend to disproportionately affect marginalized individuals. Herd and Moynihan (2018) discuss how burdens are distributive and reinforce existing inequalities and power relationships. Policies for means-tested public assistance programs, which are primarily oriented toward poor and low-income individuals and families, are typically more burdensome than universal programs. For example, accessing Temporary Assistance for Needy Families is more difficult than Social Security or Medicare. Administrative burdens are often the product of political choices designed to protect political values, such as limiting “undeserving” applicants from accessing aid (Christensen et al. 2020), given that politicians are generally less willing to impose burdens on those seen as more deserving (Baekgaard, Moynihan, and Thomsen 2021). However, burdens can also arise with less explicit negative intent, such as in the implementation (rather than the design) of policies.

Empirical evidence is beginning to mount on how administrative burdens function in specific programs, including burdens in the Supplemental Nutrition Assistance Program (SNAP), the Earned Income Tax Credit, and Social Security (Herd and Moynihan 2018). We extend this literature by examining administrative burdens to FEMA assistance for housing and property damage, illuminating the compliance and psychological costs that in-need disaster survivors experience when seeking FEMA aid and the resulting consequences for well-being. Despite little scholarly application of the administrative burden framework to disaster aid, administrative processes in federal disaster assistance are beginning to receive U.S. policymaker attention. In a recent executive order, the Biden administration pointed specifically to the case of disaster victims waiting months for benefits as an example of a “time tax,” calling for FEMA to make accessing disaster assistance easier and less burdensome. A focus on long wait times for disaster assistance complements other scholarly work on time and waiting as a burdensome element of public policy. For example, Jennifer Bouek (2023, this issue) analyzes wait lists for subsidized childcare as a venue where burdens play out, identifying the stresses and uncertainty associated with such waiting. More generally, the experience of waiting represents what Stephanie Pierce and Stephanie Moulton (2023, this issue) classify as a passive compliance cost that imposes delays and uncertainty on clients, distinct from paperwork, documentation requirements, or other more active compliance costs. Using the case of FEMA disaster assistance, we show how such passive compliance costs, in turn, exert psychological costs.

OVERVIEW OF ADMINISTRATIVE BURDENS IN FEMA’S IHP

Established by the 1984 Robert T. Stafford Disaster Relief and Emergency Assistance Act, FEMA’s Individuals and Households Program is the key federal program that provides direct assistance to households following a disaster. A state governor requests a disaster declaration and, if granted, the federal government provides direct assistance for underinsured or uninsured damaged property (Reese 2018). Disaster victims apply for assistance with FEMA (whether by telephone, online, or in person), providing personal information such as social security number, current and pre-disaster addresses, telephone number, insurance information, household income, and a description of losses (GAO 2006). After an initial assessment of eligibility, FEMA contacts victims to schedule an inspection, during which FEMA meets with victims in their homes to assess the verify damage, ownership, and occupancy. FEMA then approves or denies the application, within about ten days (FEMA 2005). If denied, applicants receive a letter detailing why they were denied and may appeal the decision within sixty days. Under IHP, at the time of Hurricane Katrina, the maximum aid per household was $26,200. Although IHP also includes other forms of assistance, most FEMA IHP grants go toward the Housing Assistance Program (financial assistance for rental housing and home repair and replacement). In this study, we focus on the Housing Assistance Program.

Unlike other government programs that are means tested and for which eligibility is determined by a set threshold, FEMA determines eligibility after application and is based on the extent of property damage.1 This shifts many learning costs—the search process of identifying programs, assessing eligibility and requirements—from an upfront barrier to program application to compliance burdens during and after application. One significant example is the mandate of one application per household, or the shared household rule, which prohibits multiple applications with the same residential address. This means that multigenerational families often struggle to access aid, disproportionately affecting low-income households with complex family structures (Reid 2013). It also ignores the realities of displacement during a major disaster such as Katrina, where many families provided the same contact information of a shelter (Young 2017), flagging applications as duplicates. However, documentation provided to applicants about IHP assistance does not explicitly state that only one application per household is allowed (FEMA 2005). Instead, survivors typically learned of this requirement after being sent a denial determination letter, initiating a lengthy, and potentially frustrating, process of appeals.

Applicants also incur compliance costs when proving occupancy, ownership (for homeowners), and identity. Until recently, only certain forms of documentation were accepted for homeownership, which marginalized many low-income Black homeowners who pass down deeds intergenerationally (Dreier 2021). Additionally, when an inspector comes to a property to assess damage, they must determine that the damage crosses a particular threshold for the homeowner to be eligible for aid. However, the inspector must be able to access the property and the applicant must be present for the inspection, both of which were often impossible when homes were still underwater, and families were still displaced from New Orleans. Further, whether damage warrants aid is partly a subjective assessment of what makes a home “unsafe” or “uninhabitable.” Finally, in a moment of crisis when housing needs for poor families were extremely acute, the processing time for FEMA was often long, resulting in problems with contacting the applicants.

FEMA IHP seeks to both provide necessary assistance to households after a disaster and to prevent fraud or improper access to program assistance (GAO 2006). FEMA Deputy Associate Administrator Zimmerman, in her testimony to the Senate Homeland Security and Governmental Affairs Committee, noted that “FEMA must balance the requirement to quickly distribute funds to meet the needs of disaster survivors with its responsibility to be good stewards of taxpayer funds” (Zimmerman 2011). Despite reports of fraud during Hurricane Katrina (GAO 2006; Zimmerman 2011), evidence indicates that the prevalence of fraud has been relatively low after recent disasters. According to a GAO report after Superstorm Sandy, less than 3 percent of assistance was determined to be fraudulent (GAO 2014). In instances where the state attempts to manage competing values of program integrity and program access, administrative burdens often arise and do so amorphously alongside notions of deservingness. This is particularly true of federal disaster assistance after Hurricane Katrina, where many survivors were both “deserving” because of their status as disaster victims and “undeserving” because of the association between accessing public assistance and their various identities, like race and gender (Reid 2013).

OVERVIEW OF THE CASE: HURRICANE KATRINA

Hurricane Katrina struck the Gulf Coast of the United States in August 2005 as a category 5 hurricane, wreaking havoc on an entire region, causing prolonged displacement, and resulting in billions of dollars in damage. The storm and its aftermath killed nearly two thousand people and displaced countless more (Picou and Marshall 2007); New Orleans was particularly hard hit. The most disastrous effects came not from wind damage or heavy rains, but instead from catastrophic flooding that resulted from the breach of several levees in New Orleans, compounded by gross government mismanagement (Brinkley 2006). Poor, people of color were especially vulnerable to Katrina, bearing a disproportionate brunt of the losses (Elliott and Pais 2006). Hurricane Katrina was an extraordinary disaster event that surpassed the conditions for which many FEMA policies were designed. The policies and practices of FEMA IHP were meant to respond to a typical disaster, but Hurricane Katrina was in no way typical, given the scale and extent of damage and displacement and its overwhelming concentration in vulnerable neighborhoods. As we show in this article, FEMA policies were unprepared for to meet the needs of survivors following such an extraordinary event. Indeed, Hurricane Katrina famously exposed the shortcomings of federal disaster assistance programs.

DATA AND METHODS

Our empirical analysis marshals three forms of data from two sources, all focused on survivors of Hurricane Katrina (or Rita) from the same forty-seven zip codes in the New Orleans area.

ADMINISTRATIVE FEMA DATA

First, we use administrative data from FEMA for the final dispositions of all federal disaster aid applications filed after Hurricanes Katrina and Rita. We acquired the data via a Freedom of Information Act request in 2018 (FOIA 2019-FEFO-00891). To assess the frequency of denials presumed to generate burdens, we conduct a descriptive analysis of the denial categorical outcomes. We use three pieces of information from each household-level application: the type of damage for assistance, denial disposition code, and zip code of residence. We restrict our descriptive analysis to the 438,365 applications that FEMA considered for either home repair or personal property replacement from forty-seven zip codes in New Orleans. Of those, 5.73 percent were appeals from first-round decisions and 5.92 percent were withdrawn by the applicant, resulting in 387,298 first-round nonwithdrawn applications (206,157 denied). To the forty-seven zip codes, we link data using the corresponding ZCTAs from the 2000 Census on two demographic measures: the proportion of adults (ages eighteen to sixty-five) living below the poverty line, and the proportion of the population that are people of color (except non-Hispanic White).

RESILIENCE IN SURVIVORS OF KATRINA PROJECT

The second data source is the Resilience in Survivors of Katrina Project, a mixed-methods, fifteen-year longitudinal study of Hurricane Katrina survivors from 2003 to 2018 (Waters 2016). Participants were enrolled in two community colleges in New Orleans before the disaster, and as a study requirement, were parenting a child younger than eighteen years old and living below 200 percent of the federal poverty line. Participants were primarily Black and single mothers. For this article, we rely on in-depth interview data from 2006 to 2010, and survey data from a pre-disaster baseline in 2003 and a one-year follow-up in 2006–2007.

The in-depth interview sample includes 106 participants who completed a post-disaster interview between 2006 and 2010, selected for variation in their post-disaster mental health and residential location. We employed a flexible, iterative coding process (Deterding and Waters 2021). First, we applied a series of index codes that captured any experiences respondents had with FEMA or other government assistance. Next, we developed and applied analytic codes to the portions of the transcripts included in the FEMA index codes. These codes correspond with the administrative burdens and associated consequences we identified a priori (learning and compliance costs associated with documentation, sufficiency, application unit, and processing time). We also included an Other code, which we applied to experiences that did not fit neatly into one of the established buckets. Next, we read through the output of the Other code and developed new, emergent codes, which we then applied in another reread of this output.

The survey data come from an analytic sample of N = 354 respondents with complete data on all variables. We measured psychological distress one year before and one year after the disaster using the Kessler-6 (K-6) scale (Prochaska et al. 2012). The K-6 score is a construct of nonspecific psychological well-being and is estimated by a series of six questions to respondents whether they have had feelings of helplessness, hopelessness, restlessness, effort, sadness, and worthlessness in the last month. Response options are (0) none, a little, some, most, and (4) all of the time. For the main independent variable, we constructed a mutually exclusive categorical variable corresponding to the status of respondents’ FEMA housing aid at the time of the post-disaster survey, using several questions about application, inspections, and approval. We categorize respondents’ status with federal disaster aid as (1) no request (no application), (2) denied (applied and received denial), (3) pending (applied and awaiting either decision or for home appraisal), and (4) approved (applied and received aid).

To isolate the association between disaster aid status and psychological distress, we include several key variables. Each respondent was asked their level of housing damage on a 5-part scale from none to enormous. Time since the disaster is the number of days since Hurricane Katrina, given that the survey interview date is correlated with the probability of receiving a final determination on an aid application. We also include a parsimonious set of sociodemographic control variables measured one year before the disaster. Age is a continuous variable. A dummy variable differentiates Black respondents from non-Black respondents. A dummy variable indicating single and not cohabitating is used for marital status. Self-rated health is a variable ranging from one to five, corresponding with excellent to poor health. A dummy variable differentiates socioeconomic status indicating those who received no public benefits relative to those who received at least one, such as SNAP, Section 8 housing, or disability. We measure social support using the Social Provisions Scale (Cutrona and Russell 1987), which ranges from one to four.

Equation (1) shows the fullest model specification, regressing psychological distress (Y) at the post-disaster survey wave (t) as a function of (F), the status of respondents’ FEMA housing aid application:

β1 is the main coefficient of interest in our analysis. It is estimated conditional on a lagged measure of distress before the disaster (t-1), a variable capturing the level of housing damage (H) post-disaster, and the previously mentioned sociodemographic controls assessed before the disaster in vector X. We first assess a baseline model that excludes vector X. In text, we use the summary K-6 score (ranging from 0 to 24). In supplemental analyses, we estimate equivalent models on each of the six items, and we also examine dummy variables indicative of moderate mental distress (MMD)—K-6 score greater than 7, and serious mental illness (SMI)—K-6 score equal to or greater than 13. These regression models are intended to provide descriptive evidence of associations and are therefore not interpreted as causal estimates.

RESULTS

Our results section proceeds in three parts, relying on each source of data to uncover (1) the frequency and distribution of denials per FEMA administrative data; (2) the experiences of compliance and psychological costs from the RISK study interview data; and (3) the relationship between aid denial and well-being from the RISK study survey data.

FREQUENCY AND DISTRIBUTION OF DENIALS, FEMA DATA

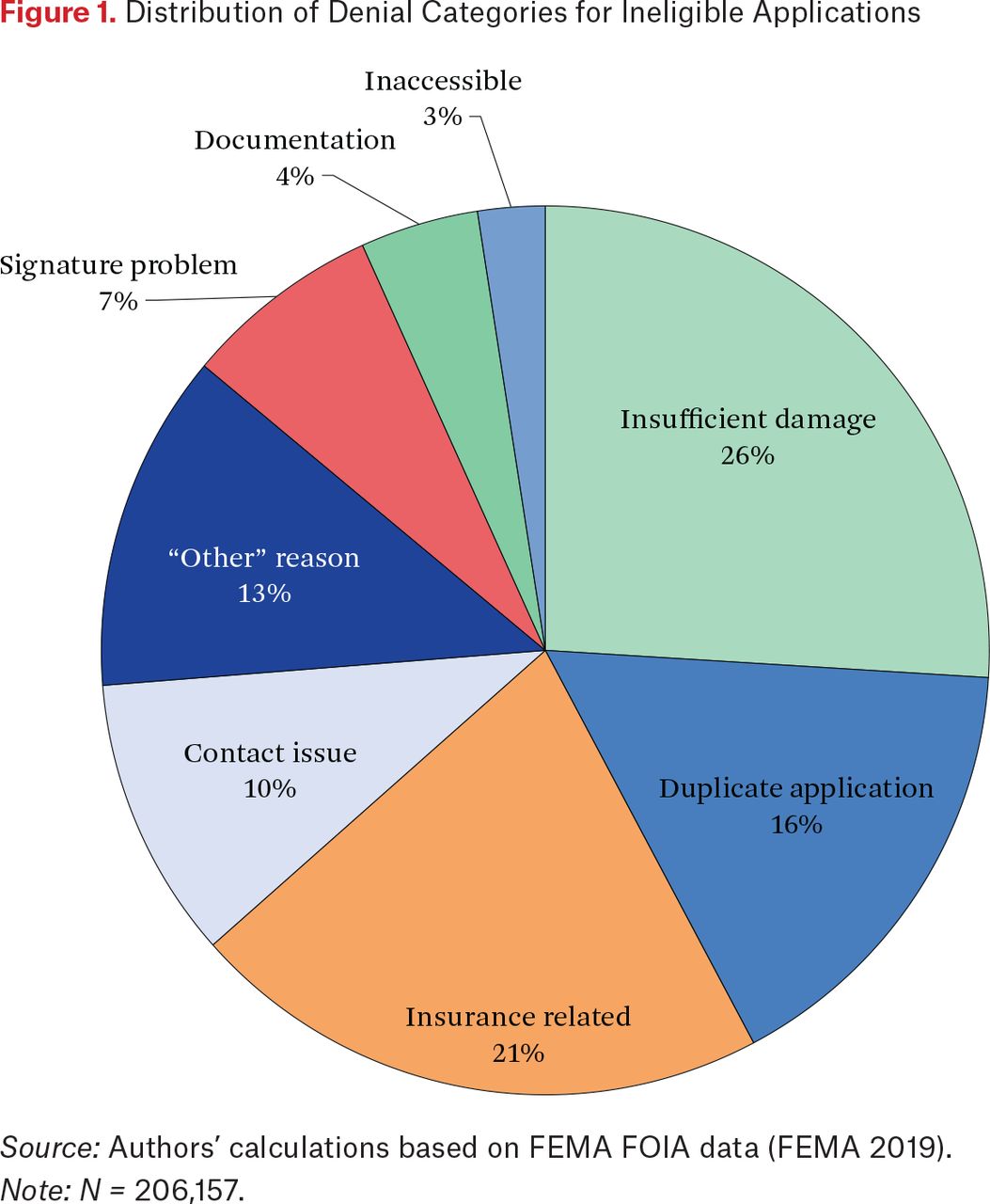

Of the 387,298 first-round nonwithdrawn applications for home repair and personal property replacement, FEMA approved 46.77 percent of applications for aid and denied 53.23 percent (206,157). Figure 1 shows the distribution of denial categories. What were the policy logics associated with assistance denial in hard-hit areas of New Orleans following Hurricane Katrina? The modal reason for denial was insufficient damage, which constituted just over a quarter of denied applications (26 percent). Reasons related to insurance coverage (insurance over the maximum payout) were also common (21 percent). Another 16 percent of applications were denied due to duplication from another applicant, and 10 percent to the inability of FEMA to contact the applicant. Problems with signatures (7 percent), documentation (4 percent), and inaccessibility (3 percent) constituted about 14 percent of denied applications together, corresponding to around twenty-eight thousand applications denied aid.

Distribution of Denial Categories for Ineligible Applications

Source: Authors’ calculations based on FEMA FOIA data (FEMA 2019).

Note: N = 206,157.

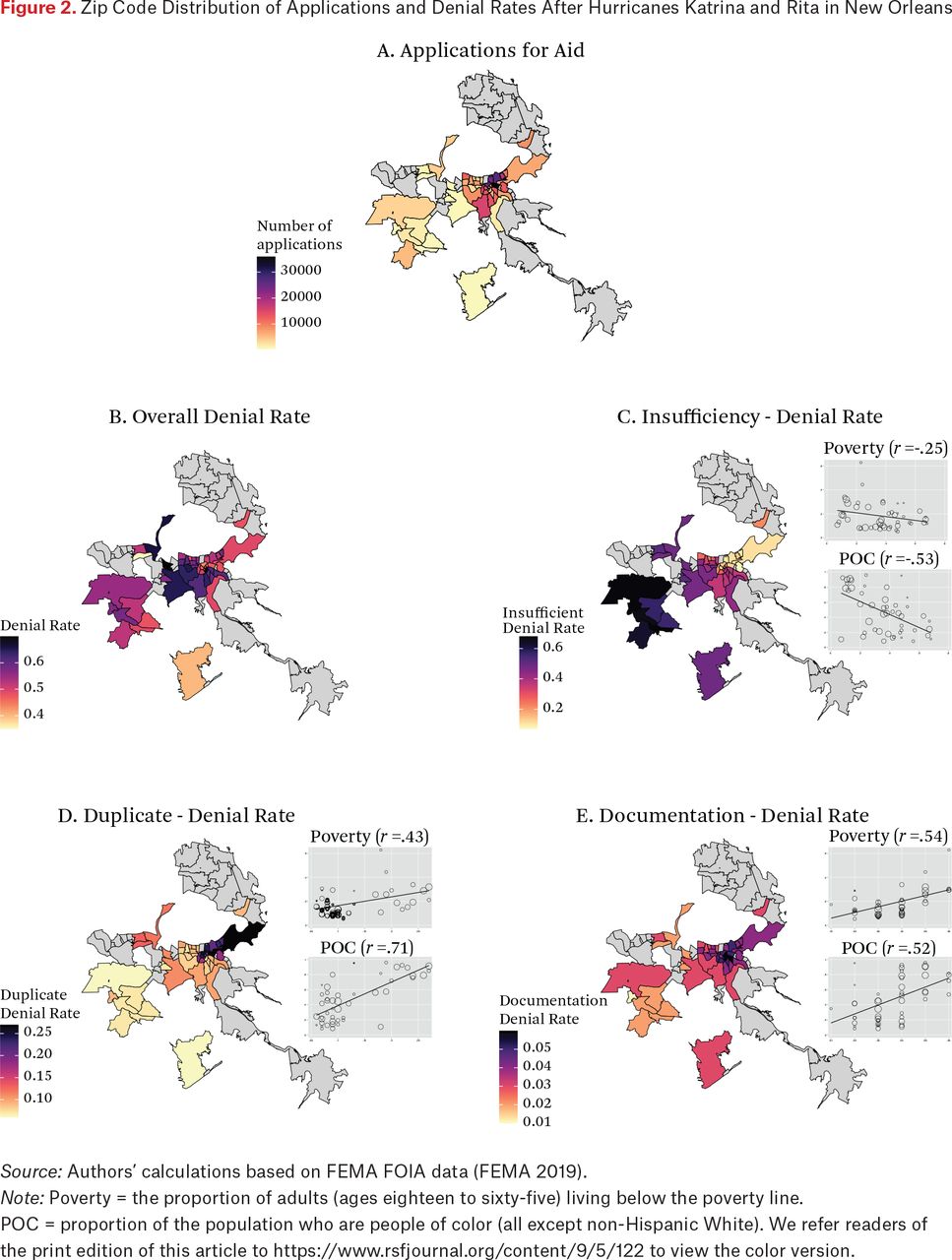

Figure 2 maps the spatial distribution across the forty-seven (and adjacent) zip codes in New Orleans of disaster assistance applications (panel A), overall rates of denial (panel B), and rates of denial for three specific categories discussed in previous research to be particularly consequential compliance regulations in vulnerable populations (panels C through E). The total number of applications ranged from 357 applications in 70343 to 35,964 in 70117 (Bywater and Lower 9th Ward). Despite an overall individual-level denial rate of 53 percent, the community-level denial rates ranged from 35 percent in 70049 to 70 percent in 70047—two zip codes on opposite banks of the Mississippi River. Panels C through E show stark divergent spatial patterns of denials due to insufficient damage, duplicate applications, and documentation across zip codes. The majority Black zip code 70129 in New Orleans East had the highest rate of denials due to duplicate applications at 27 percent.

Zip Code Distribution of Applications and Denial Rates After Hurricanes Katrina and Rita in New Orleans

Source: Authors’ calculations based on FEMA FOIA data (FEMA 2019).

Note: Poverty = the proportion of adults (ages eighteen to sixty-five) living below the poverty line.

POC = proportion of the population who are people of color (all except non-Hispanic White). We refer readers of the print edition of this article to https://www.rsfjournal.org/content/9/5/122 to view the color version.

Administrative data from FEMA did not include information about applicants. To understand if denial rates map onto local demographics, panels C through E provide two bivariate correlations between the denial rate (Y axis) and, first, the proportion of adults in poverty and, second, proportion of the population who are people of color. The local denial rate for insufficient damage was negatively associated with local poverty and racial composition. This makes sense as greater damage occurred in low-income, minority communities. In panels D and E, we find strong, positive relationships between both community-level poverty and racial composition, and the local concentration of denials for duplicate applications and documentation. The correlation between documentation denial rate and poverty and concentration of people of color was 0.53 and 0.54, respectively. The correlation between the local denial rate for duplicate applications and concentration of people of color was 0.71 and 0.42 for the poverty rate.

EXPERIENCES OF COMPLIANCE AND PSYCHOLOGICAL COSTS, THE RISK STUDY

The denial reasons documented in FEMA data were commonly experienced by RISK participants as burdensome, either as a function of policy design or the failure to implement them in the overwhelming disaster circumstance. We use in-depth interview data from RISK, in combination with documentation and reports on FEMA IHP policies during Katrina, to detail the compliance and psychological costs participants incurred when applying for disaster aid.

Application Unit

Many respondents experienced difficulties applying for and receiving FEMA assistance because of the prohibition against duplicate applications, which permits only one application per household. This shared household policy intended to prevent providing duplicate benefits. The program expects that everyone in a household will coordinate and submit one application. However, the documentation that FEMA provided potential IHP applicants (FEMA 2005) makes no mention of this restriction against multiple applications from a single address, which was ultimately confusing and frustrating for individuals who were denied under this rule.

For example, Victoria was a twenty-two-year-old Black woman with a young son at the time of Katrina.2 She had been living in her own apartment in New Orleans, but after her landlord raised the rent, she and her son moved in with her parents the month before Katrina. She lost everything when her parents’ home was flooded in the storm. She applied for FEMA assistance to replace her personal belongings, including her clothing, furniture, and car, but was denied when her mother claimed her as a resident on a different application. Despite being told by FEMA to appeal her case, she continued to be denied and ultimately gave up: “[FEMA] said I wasn’t eligible and that I was on my mom’s application and that made me ineligible. . . . They said that we should appeal it. So, we did that, and they still said I was ineligible, so I just left it alone.”

Victoria was unaware that the policy prohibited multiple applications from the same household when she applied for assistance. This lack of transparency from FEMA resulted in a frustrating interaction between Victoria and FEMA that could have been avoided by clearer delineations of eligibility requirements. Furthermore, Victoria’s family situation—a multigenerational household of adult children with families living with their parents—was not uncommon, but even though she likely maintained personal property and managed household finances separately from her parents, she did not receive assistance.

Other respondents were similarly denied assistance because they cohabitated with others, often parents. Samantha was twenty years old, had one child, and lived at home in New Orleans with her mother. Like Victoria, she noted that her mother received help from FEMA, but she did not: “My mother got help from FEMA. I didn’t get any assistance from FEMA because they were saying it was a duplicate [application], because they said I lived in the same household.” Despite living at the same residential address, many of these families functioned independently, with adult children paying rent (often informally) to parents. Families living together may have had their own personal property, but FEMA policy does not recognize the potential division of assets within a household. By immediately denying any application from an address used on an existing application, the implementation of the policy led to a difficult appeals process and often no assistance for in-need families.

Additionally, the realities of post-disaster displacement made the enforcement of the shared household rule difficult. Most of our sample was forced to evacuate New Orleans and many lived in community shelters across the Gulf Coast region. This meant that many survivors shared a telephone line for the shelter and listed the shelter as their contact information on their FEMA application, to ensure that they would be reachable (given that this was before cell phones were commonly used, especially among low-income people). As a result, some of these applicants were also flagged as submitting a duplicate application and denied. Nicole, who was twenty-six years old at the time of Katrina and had one child, told her experience: “[FEMA] was telling me that I have a duplicate application. . . . This happened to a lot of people—if you used the same telephone number as somebody else, that’s going to show that you have a duplicate application. . . . People in the Astrodome had duplicate applications because they used the same phone number.”

In addition, when families were displaced from New Orleans for an extended period, family members often separated. One component of IHP assistance for housing damage is rental assistance, but the restriction against duplicate applications precludes these separated family members from separately accessing rental assistance. According to the GAO (2006, 24), FEMA recognized this issue and adjusted the policy after the fact: “FEMA created new IHP procedures to allow multiple household members separated by the disaster to receive rental assistance. As a result of Hurricanes Katrina and Rita, thousands of families evacuated to locations across the country and in some circumstances required families to temporarily separate. As a result, providing assistance to multiple household members was warranted.”

Our respondents were instead consistently denied when more than one household member applied. Note that in some cases, this policy did capture fraud as intended, but the original denial of the recipient led to burdensome and stressful processes of appeals. For example, Cynthia, a twenty-year-old mother, related that a relative in Florida claimed FEMA benefits using her address, and that she was denied assistance as a result: “[FEMA] didn’t give me anything because my uncle tried to claim our house. . . . They told us we couldn’t get it. . . . He tried to get FEMA [aid] for our house, and he was in Florida somewhere.” This story highlights the trade-offs in policy design and implementation between program integrity and access. The adjudication process between duplicate applications may lessen burden if the implementation of the shared household rule did not simply deny the additional application from a given address, as was the case with Cynthia, and set off a lengthy appeals process. Instead, it could be the role of FEMA to use administrative records to ensure that the rightful applicant is not mistakenly denied.

In sum, the restriction against duplicate applications that produced burdens for our respondents had three primary issues. First, the restriction itself was poorly communicated to applicants. Our respondents were unaware that they were prohibited from applying if they lived with their parents, and thus were confused when they were denied for this reason. The documentation that FEMA provided applicants in August 2005, titled “Help After a Disaster” (FEMA 2005), makes no mention of the requirement that only the head of household applies. This often resulted in unnecessary and burdensome interactions between applicants and bureaucrats. Second, the policy itself does not account for the complicated family situations of many low-income families, such as multigenerational households. Third, FEMA’s method for adjudicating between multiple applications by immediately denying second applications with a phone number or address, often leads in-need people to a lengthy appeals process.

INSUFFICIENT DAMAGE AND THE FEMA INSPECTION

Applicants must also meet a threshold of damage sufficiency when FEMA inspects the damage to their property. Following Hurricane Katrina, however, large swaths of New Orleans remained inaccessible for weeks or months. When FEMA inspectors were unable to access these homes, survivors’ applications were sometimes denied on grounds of insufficient damage. Rebecca, a twenty-nine-year-old Black mother of five, experienced this: “[FEMA] said that I didn’t have sufficient damage. But the same report that said I didn’t have sufficient damage said that the inspector couldn’t even get to my apartment because it was still underwater. Well, if you couldn’t get there and it was underwater . . . how could you say I had nonsufficient damages?”

This respondent then appealed the decision, after which FEMA noted that they would have to wait several weeks until the water receded. This experience sheds light on the burdens that applicants endured to meet a threshold of damage sufficiency during an inspection as set out by FEMA. The requirement for an inspector to assess property damage and for the applicant to be present for their inspection fails to consider the reality that many applicants are displaced and may not be able to return to their homes.

Although her property was accessible, Madison, a twenty-nine-year-old mother of one, was denied because she was displaced in Georgia. She said that an inspector attempted to schedule an inspection, but despite Madison’s being out-of-state and providing alternate contact information for a designated representative, the inspector never called: “The person who called me that was supposed to meet with you, I told him I was in Georgia. And he said, well I have to get somebody to come to verify that I came. The numbers that I gave her, she never called. . . . That house was not livable.” As a result, Madison was denied FEMA assistance. She made clear that the process of scheduling and communicating with the inspector was also burdensome in addition to her being displaced and unable to be present. FEMA likewise attempted to accommodate applicants in these types of situations (GAO 2006). For example, FEMA said that for applicants in areas that were inaccessible due to high flood waters, it used “remote sensing” (satellite technology) to assess damage and allowed applicants to designate a third-party representative to be present for inspections (GAO 2006). Again, however, our respondents were often still denied, suggesting potentially uneven implementation of these accommodations or a struggle on the part of implementation given the overwhelming need.

In some instances, respondents also reported unfair or mistaken characterizations by FEMA inspectors regarding the damage to their homes. For example, Julia explained that the inspector assigned to her case incorrectly determined the damage to her home: “I lived in a duplex and my house was downstairs and somebody lived up over me. But because the way the house looked, [the FEMA inspector] thought I had an upstairs and downstairs. She was like, ‘oh, you didn’t have any damage.’ And I fought tooth and nail, wrote back and forth, nothing.”

This represents a common trend: FEMA made an assessment considered incorrect by the respondent; the denied respondent attempted to appeal the decision; but the lengthy appeal and bureaucratic process led to people giving up and aid never materializing. In the face of unprecedented disaster, FEMA found itself overwhelmed by the sheer volume of affected individuals. FEMA inspectors are mostly a contract workforce, and in the case of Katrina were mobilized on short notice, cutting corners on typical training procedures for new inspectors (GAO 2006). Our respondents often bore the consequences of these policy and implementation issues, as seen in struggles with FEMA inspections.

DOCUMENTATION

To receive FEMA assistance, applicants must provide documentation that establishes home ownership, occupancy, and identity. However, given the rushed and chaotic conditions under which most families evacuated during Hurricane Katrina, it was common for people to not have any of this documentation with them while displaced. Many families assumed that they would be returning to New Orleans within a couple of days and left important documents at home. When it came time to apply for FEMA aid, those without proper documentation often ran into difficulties. Kristen was such a twenty-five-year-old mother of two. She noted that assistance was delayed because of issues she ran into trying to provide adequate documentation: “[FEMA] put us through so much to get [assistance]. Like we didn’t have any documents to send them showing them that we were affected by it. I had my ID because I had my purse. But most of the stuff I didn’t have.”

Like Kristen, Catherine was also initially denied on grounds of inadequate documentation. She was living in a house with her mother and her two children but had used a post office box address because of issues with postal delivery to her address. Despite providing a lease showing that she was her mother’s tenant, Catherine was denied assistance. Eventually, she appealed the decision, and her mother went to a recovery center in Houston to sign a letter attesting that this was all true, after which FEMA provided aid. However, these documentation requirements resulted in significant delays in receiving assistance as well as stress on Catherine and her family to appeal the decision and receive the aid for which they were eligible. This exemplifies how the burden of proof falls on individuals rather than the state, at a time when those individuals are in acute need for housing and stability.

Rebecca ran into similar problems with documentation while trying to secure assistance, but, unlike the previous two respondents, these problems prevented her from ever receiving assistance. Many of her important documents were in her parked cars, which were lost during Katrina. After months of fighting for assistance, she eventually gave up: “They [FEMA] kept saying one thing after another. They didn’t have the paperwork on my car. And I said, well, I have to get it. But everything was in the car. . . . When we came back, it was gone. Both our vehicles. . . . They were gone. So, it took us a while to get certain documents. But we fought with them up until maybe the end of 2006, beginning of 2007, when I just said, you know what, forget it.”

PROCESSING TIME

The extended processing time between applying for assistance and receiving that assistance from FEMA was often very long and thus costly for survivors. Indeed, both Angela and Lindsey explained that they waited between four and eight months for assistance, meaning that they were left without aid during the crucial weeks and months following the disaster. For example, Lindsey noted that “before I got my apartment, I think it was like about four months . . . and then it was maybe eight months before I got any actual financial reimbursement for personal property.” Angela applied for FEMA assistance at the beginning of September 2005 right after the storm hit but did not receive any aid until February 2006. For Cynthia, the wait was enough to give up: “And when I called FEMA to ask why they weren’t they helping, they told me they wrote out a check, but ‘we don’t know who to send it to.’ I’m like, I sent you everything. I sent you my new statement. I sent you my housing plan. I sent you where I work and everything and they were like, ‘oh well we’re still reviewing it.’ I’m like you know what? You can take this shit and stuff it.”

In addition to delays in receiving assistance, Cynthia received confusing and sometimes contradictory information when asking FEMA for updates on her application, suggesting that processes in place were overwhelmed by the magnitude of need after the disaster.

Kristen similarly pointed out that the reasons for delay were typically opaque. Recall that Kristen experienced difficulties providing adequate documentation to FEMA. She said it was almost impossible to know exactly why her assistance was delayed: “Because when you would talk to FEMA, you would get five to six different answers from people. So, you really don’t know what the reason for the hold up. Because they’ll tell you so many different things. You’ll call five times a day. They’ll give you five different stories.”

Investigations by the GAO provide support for our respondents’ experiences of long processing times. Despite explicitly providing estimates of ten days from application to inspection and ten days from inspection to decision (FEMA 2005), processing times were often two to five times longer (GAO 2006). This entailed significant costs for our respondents.

INTEGRITY, ACCESS, AND DESERVINGNESS IN DISASTER ASSISTANCE

A common theme across many of these individual experiences is that myriad FEMA policies made accessing disaster assistance onerous, lengthy, or even impossible for in-need families. As discussed, public assistance programs balance program integrity and program access (for a robust discussion of value trade-offs and error in administrative burdens research, see Bouek 2023, this issue). Our qualitative data suggest that the delay and denial that resulted was burdensome and stressful.

Consider the respondents, such as Victoria and Samantha, who were denied FEMA assistance because of the duplicate application rule. Both were denied because they were claimed as dependents on their parents’ applications, despite being adults with families of their own. These denials represent the policy working as intended, but at issue was that the policy itself failed to recognize the complex family structures and living arrangements of many poor families, suggesting an issue in policy design. In contrast, other respondents were denied assistance because of issues with providing supporting documentation, such as Kristen and Rebecca, or because they were unable to meet the inspector, such as Madison, suggesting issues with implementation. One interpretation of the practices to prevent fraud or the duplication of benefits, mainly by shifting the burden of proof onto the individual, is that FEMA sets out disaster aid deservingness to those who were not displaced for extended periods, who did not lose their documents and paperwork, and who have the ability to meet with a FEMA inspector whenever necessary.

CONSEQUENCES OF DELAY AND DENIAL

The delays and denials associated with these policies are not innocuous. For a low-income, marginalized population recovering from a natural disaster, being denied FEMA assistance for all the reasons outlined has negative consequences for mental well-being. Within the administrative burden framework, being denied is a clear psychological cost of the burdens associated with navigating FEMA programs. Indeed, many of our respondents reported experiencing acute distress because of the difficulties they encountered applying. For example, Kelly was a twenty-nine-year-old mother of two who is unemployed and relying on her husband’s income to make ends meet. She said waiting for FEMA and ultimately being denied multiple times was difficult for her family: “The hardest thing is not receiving any [assistance]. . . . That’s the hardest thing because like I said, the little money that my husband is earning, we’re putting dime by dime to fixing our home for us. So, the hardest thing is not receiving any help. When you are applying for it [FEMA aid], you get turned down.”

For many, the link between experiences of financial hardships resulting from disaster-related expenses and psychological well-being was tight. For those who lost everything after Hurricane Katrina, many shared their experiences of psychological distress. Rebecca, whose story we told earlier, is one example: “I was really out of money. I was fighting with FEMA. . . . I was trying to get what I thought I should have gotten, and everybody just kept turning me down. And I would have to go through all this paperwork, and I’m like, I don’t want to have to ask anybody to help me, because everybody’s going through it. And I was wondering how we were going to survive, how we were going to pay these bills, and I just didn’t see a way out.”

Rebecca’s difficult experience applying for FEMA aid led her to feel like she was “having a breakdown.” Rather than being a vital safety net in a moment of acute crisis, the burdens associated with FEMA assistance led to further distress. Rebecca pointed out that, in addition to the time and effort she put into accessing assistance (such as standing in lines), she also felt the weight of psychological costs by having to ask for help. For some of our respondents, applying for FEMA assistance was associated with stigma because they were judged and made to feel inferior for seeking aid. For example, Erica, twenty-eight years old, described both the hassle and how she felt inferior: “I just didn’t feel like going through the hassle of standing in the lines, waiting on the phones and, you know. . . . I was like, you know what? I’m just sick of this. I’m tired of feeling like I’m begging people for something or, you know, like they call us so-called refugees. . . . That was just disgusting and aggravating. It was like, uh-uh, I’m not doing this.”

Being called a refugee, cast as an outsider jumping through hoops to access basic government assistance, and feeling inferior for seeking out assistance took its toll on Erica and many others.

DISASTER AID DENIAL AND WELL-BEING: SURVEY EVIDENCE FROM RISK

RISK respondents’ narratives clarify and underscore the costs incurred in accessing disaster assistance, which required difficult compliance processes, stringent requirements, and taxing procedures. Each denial generated some form of burden, stemming from factors that administrative data suggested were not unique to the RISK survey sample but generally experienced by applicants from low-income, communities of color. Qualitative data also suggested a link between denials or delay and well-being. We now turn to assess this association using survey data.

Table 1 provides the descriptive statistics of the RISK survey sample. The sample mean K-6 score increased from 5.59 to 6.81 from before to after Hurricane Katrina. The prevalence of moderate mental distress increased from 22.60 percent to 38.42 percent.

Descriptive Statistics of Survey Sample, Percentages, and Mean (SD)

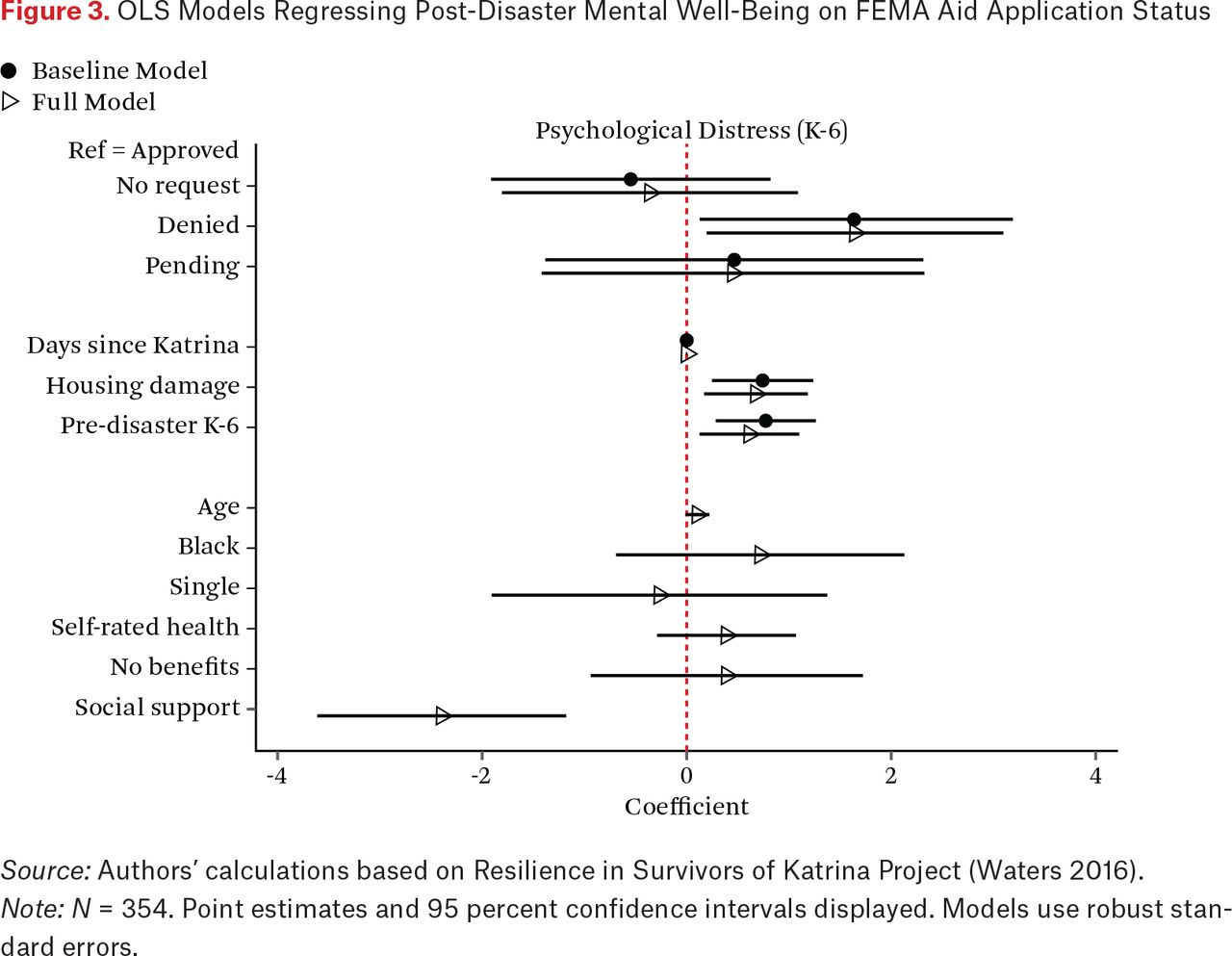

Figure 3 presents results from two nested multivariable OLS models regressing post-disaster K-6 on FEMA aid application status (for tabular presentation, see table A.1). Survey participants who were denied FEMA aid scored significantly higher on the K-6 scale of psychological distress relative to those approved for aid (β = 1.637, p < .05), controlling for level of damage and pre-disaster psychological distress. The effect was not attenuated by the inclusion of additional controls for sociodemographic indicators in model 2. We find no statistically significant difference in psychological distress between those with pending applications and those who had already been approved for aid. Among the controls, social support correlated with lower levels of distress, protecting against mental health adversity (p < .001). As expected, those with greater housing damage also experienced significantly greater psychological distress after the storm, net of other factors.

OLS Models Regressing Post-Disaster Mental Well-Being on FEMA Aid Application Status

Source: Authors’ calculations based on Resilience in Survivors of Katrina Project (Waters 2016).

Note: N = 354. Point estimates and 95 percent confidence intervals displayed. Models use robust standard errors.

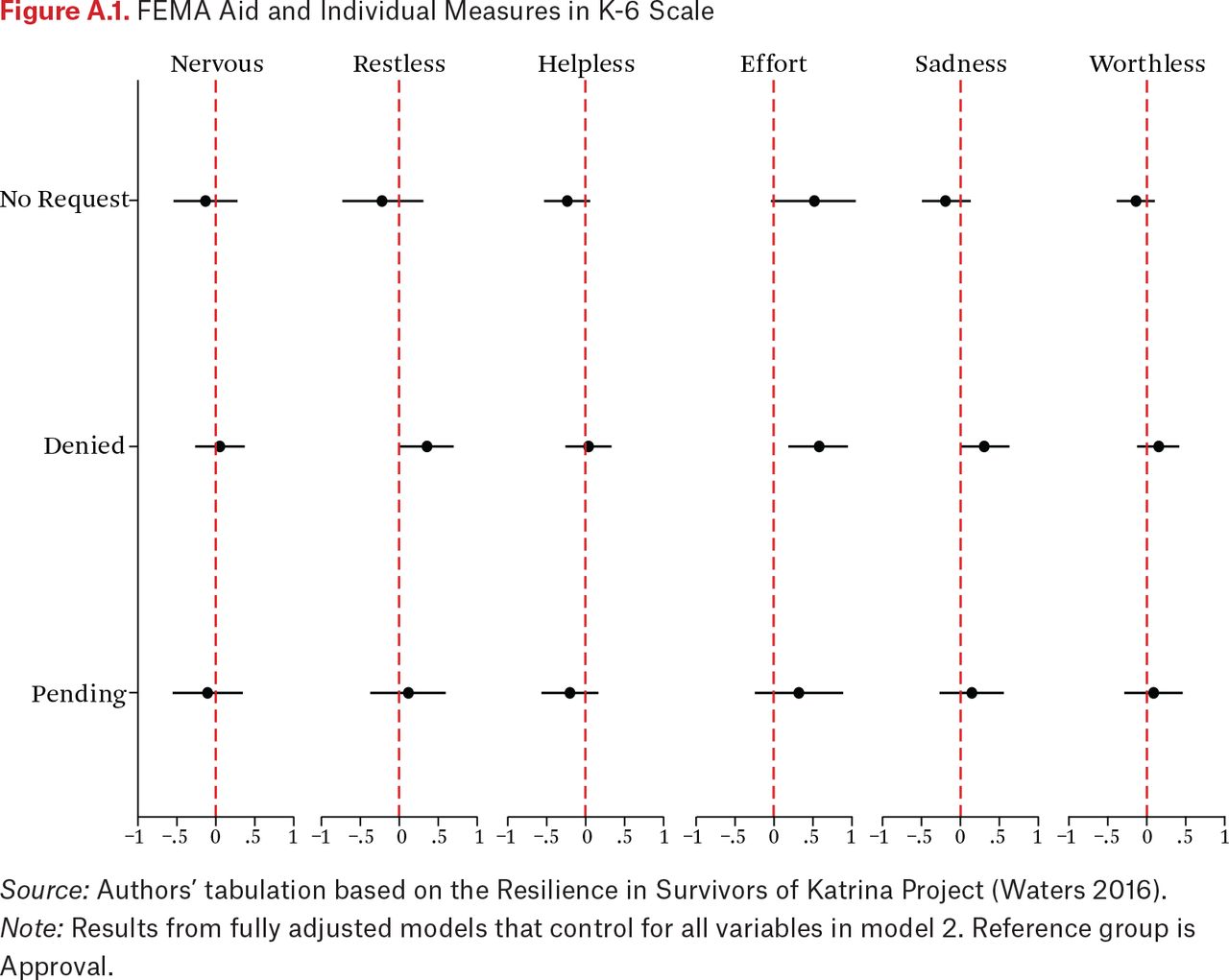

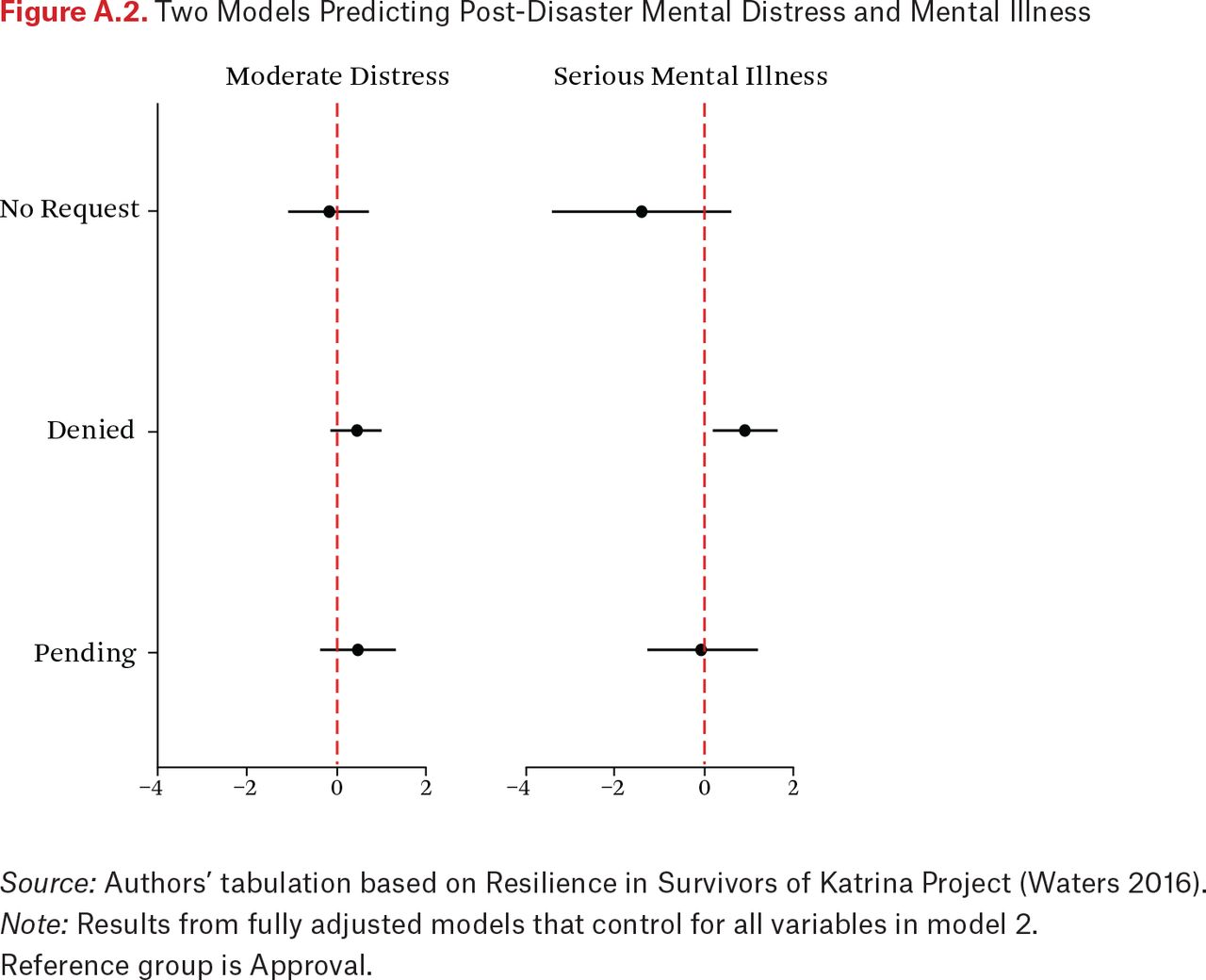

Holding all other variables at their means, the full model predicts that respondents who were denied aid had a K-6 score of 8.86, above the threshold used clinically to indicate moderate mental illness. Those who did not apply for aid had a predicted K-6 score of 6.06, whereas those who were approved had a predicted score of 6.42. Respondents with pending applications scored 6.87. In figure A.1, equivalent models to those presented in figure 3 but regressed on the individual K-6 measures demonstrate that aid denial was particularly consequential for three subquestions: experiences of restlessness, sadness, and effortfulness. We show that aid denial was significantly associated with a greater likelihood of experiencing serious mental illness, relative to no mental illness, indicated by a K-6 score of above 13. It did not significantly distinguish the likelihood of moderate mental distress, relative to no distress; however, the coefficient is in the expected direction (see figure A.2).

DISCUSSION

This article contributes to a growing body of scholarship documenting the contours and consequences of administrative burdens in public policy. Using data obtained from FEMA through a FOIA request, we first offer descriptive evidence that denials of FEMA assistance that generate burden are common and more likely to occur in disaster-affected areas with higher proportions of poor residents and people of color. Second, drawing on in-depth interview data with low-income mothers, we document how marginalized survivors experienced compliance and psychological costs associated with applying for FEMA aid, particularly stemming from duplicate applications, damage insufficiency, and failed documentation. Our respondents described the slow, complicated, frustrating process of applying for aid only to be denied or to have their assistance delayed in times of hardship. Survivors explained that these denials took a toll on their mental well-being. Survey evidence paints a similar picture. Our quantitative data suggest that aid denial was associated with greater psychological distress relative to those who were approved aid. The burdens our respondents encountered resulted from issues with design and with implementation, or in some combination. Our data cannot clarify the precise origin of these burdens. We focus instead on their scale and their impact.

Applying the lens of administrative burdens and examining their consequences highlights how federal disaster aid programs can exacerbate inequality for poor and minority residents in disaster-prone areas and reinforce existing power structures. Wealthier households are less likely to experience major damage from disasters because they live in less disaster-prone areas and may also have the resources to navigate and manage complex aid programs (Fothergill and Peek 2004). Conversely, poorer households are more likely to live in disaster-prone areas and may need government assistance, such as FEMA, to buffer the negative socioeconomic impacts of disasters. We have documented how the compliance and psychological costs associated with FEMA’s IHP further disadvantage the poorest and minority households and inhibit their long-term recovery. Our findings suggest that residents of areas with greater proportions of poor and minority households are more likely to be denied aid because of duplicate applications and lack of documentation—burdens that may be alleviated by smart policymaking that shifts them to the federal government.

These distributive consequences can also point to notions of deservingness. On the one hand, making post-disaster assistance easier to access might mean that more people receive aid who otherwise would have been deemed ineligible, leading more individuals to receive aid who otherwise are seen by the state as undeserving (for example, those who miss inspections, those who do not have enough damage). On the other hand, prioritizing program integrity leads some individuals who are eligible to experience burdens, which arise from policies that limit access and ensure integrity (such as documentation requirements). Our analysis illuminates the burdens resulting from these policies or their implementation that disproportionately affect marginalized households after a disaster, and to point toward how integrity, access, and deservingness are state logics that combine in ways that may contribute to inequality.

Although the eligibility and compliance requirements may appear neutral at face value, their impacts are not. Our qualitative evidence suggests that families ran into issues proving sufficient damage, and the aggregated analysis of administrative data that denials due to insufficiency were less common in areas with higher poverty and more people of color. These bivariate relationships, however, do not control for damage severity, given the disasters’ greater impacts in marginalized neighborhoods in New Orleans (Donner and Rodríguez 2008). Thus the aggregated nature of this evidence may further mask underlying mechanisms, and future research should model relationships between burdens and outcomes conditioning on key individual-level attributes like more objective severity.

In terms of mental health and well-being, our finding that aid denial is associated with psychological distress highlights the need to consider government policies—and more suggestively, administrative burdens—as social determinants of health. We were unable to differentiate the cause of denials in the survey data, but our qualitative data suggest that many denials and their associated policy processes were burdensome for respondents. The qualitative data also support our interpretation of the direction of the association given that we did not find evidence that mental health problems led to greater difficulty with program navigation.

CONCLUSION

Reduced or delayed access to FEMA IHP assistance after disasters gave rise to significant administrative burdens, with negative consequences for disaster survivors. A recent summary of study evidence concludes that one key stage of promoting post-disaster health equity is that “social services should integrate and strive to reduce the administrative burden on survivors” (Raker et al. 2020, 2128). Identifying how to reduce burdens for citizens or shift them to the state is critical. This could be achieved several ways in FEMA’s IHP. First, FEMA should craft the IHP program to be more generous for disaster survivors. Since Hurricane Katrina, the program has not become more generous: $26,200 in August 2005 has the same buying power as $36,900 in October 2021 ($1,000 less than the October 2021 maximum grant). FEMA could integrate community-level social vulnerability indices in the calculation of awarded grants and relax the concern that some households may receive “too much” aid.

Second, FEMA should reconsider the trade-off of reducing fraud and promoting access. By focusing almost exclusively on reducing fraud and abuse of the program, at the expense of access for in-need survivors, the structure of disaster aid in its current configuration comes with costly trade-offs. Instead, increasing access through virtual assessments and wider documentation standards could help FEMA officials struggling to implement appropriate procedures. The Florida Automated Community Connection to Economic Self-Sufficiency (ACCESS), the state’s service delivery model for its public assistance programs, offers an innovative approach (Heflin, London, and Mueser 2013). Rather than filling out paper applications and visiting a state office for an interview, individuals apply for benefits via ACCESS, an internet-based system that determines eligibility simultaneously for multiple programs and does not require documentation to verify most expenses and assets. FEMA could look to ACCESS as an example of a service delivery model that prioritizes access in managing the application process, determining eligibility, and delivering benefits.

Beyond these potential changes in the near term, we believe now is the time to seriously reconsider the structure of disaster aid in the United States. Climate science suggests that even with large investments in greenhouse gas reduction, trends in disaster severity will continue. Creating a universal disaster assistance program is worthy of consideration. Some scholars argue for a universal, parametric-based flood insurance program (Sengupta and Kousky 2020), which would eliminate many administrative burdens. There would be no need to prove eligibility, schedule an inspection, or track down and submit required paperwork. Another site of potential overhaul would be the structural integration of FEMA processes with existing government structures, such as the Internal Revenue Service on property taxes, to reduce applicants’ need to prove their eligibility. If guided by scholarly evidence, decision-makers can reduce or shift administrative burdens to promote equity and recovery in the face of disaster.

Appendices

Tabular Form of Figure 3, OLS Models Predicting Post-Disaster Well-Being

FEMA Aid and Individual Measures in K-6 Scale

Source: Authors’ tabulation based on the Resilience in Survivors of Katrina Project (Waters 2016).

Note: Results from fully adjusted models that control for all variables in model 2.

Reference group is Approval.

Two Models Predicting Post-Disaster Mental Distress and Mental Illness

Source: Authors’ tabulation based on Resilience in Survivors of Katrina Project (Waters 2016).

Note: Results from fully adjusted models that control for all variables in model 2. Reference group is Approval.

FOOTNOTES

↵1. Although eligibility for IHP was mostly determined when an individual applied, eligibility requirements were in place, including that the individual must have experienced losses in a federally declared disaster area; had uninsured or underinsured needs; been a citizen, noncitizen national, or qualified alien in the United States or have a qualifying individual who lived with the disaster victim; have been living at the home at the time of disaster; and be unable to live in or return to their home or have a home that requires repairs because of disaster damage (GAO 2006).

↵2. All demographic information refers to respondent characteristics at the time of interview. Pseudonyms are used throughout.

- © 2023 Russell Sage Foundation. Raker, Ethan J., and Tyler Woods. 2023. “Disastrous Burdens: Hurricane Katrina, Federal Housing Assistance, and Well-Being.” RSF: The Russell Sage Foundation Journal of the Social Sciences 9(5): 122–43. DOI: 10.7758/RSF.2023.9.5.06. For comments on previous drafts and support, we thank Meghan Zacher, Sarah Lowe, Mary Waters, Lilly Yu, Saul Ramirez, Marie Claire Meadows, and Kate Burrows, as well as the participants of the “Administrative Burdens as a Mechanisms of Inequality in Policy Implementation” conference at the Russell Sage Foundation and three anonymous reviewers. The RISK Study was generously funded by Eunice Kennedy Shriver National Institute of Child Health and Human Development grants P01HD082032, R01HD057599, and R01HD046162, National Science Foundation grant BCS-0555240, MacArthur Foundation grant 04–80775–000-HCD, the Robert Wood Johnson Foundation grant 23029, the Center for Economic Policy Studies at Princeton University, and the Harvard Center for Population and Development Studies. The first author acknowledges support from the Peter Wall Institute for Advanced Studies. Direct correspondence to: Ethan J. Raker, ethan.raker{at}ubc.ca, 6303 NW Marine Drive #2318, Vancouver, BC V6T1Z1, Canada.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

- Article

- Abstract

- BACKGROUND

- ACCESS TO FEMA POST-DISASTER ASSISTANCE

- ADMINISTRATIVE BURDENS IN DISASTER AID

- OVERVIEW OF ADMINISTRATIVE BURDENS IN FEMA’S IHP

- OVERVIEW OF THE CASE: HURRICANE KATRINA

- DATA AND METHODS

- ADMINISTRATIVE FEMA DATA

- RESILIENCE IN SURVIVORS OF KATRINA PROJECT

- RESULTS

- FREQUENCY AND DISTRIBUTION OF DENIALS, FEMA DATA

- EXPERIENCES OF COMPLIANCE AND PSYCHOLOGICAL COSTS, THE RISK STUDY

- INSUFFICIENT DAMAGE AND THE FEMA INSPECTION

- DOCUMENTATION

- PROCESSING TIME

- INTEGRITY, ACCESS, AND DESERVINGNESS IN DISASTER ASSISTANCE

- CONSEQUENCES OF DELAY AND DENIAL

- DISASTER AID DENIAL AND WELL-BEING: SURVEY EVIDENCE FROM RISK

- DISCUSSION

- CONCLUSION

- Appendices

- FOOTNOTES

- REFERENCES

- Figures & Data

- Info & Metrics

- References

Related Articles

Cited By...

- No citing articles found.