Abstract

In this article, we examine the effects of reforms to reduce administrative burden in a foreclosure prevention program by streamlining the application process and reducing applicant wait times. We find that the reforms are associated with a significant 23 percent increase in the rate of benefit receipt and a 7.5 percent decrease in the foreclosure rate. These effects are even larger for applicants with more difficult-to-document hardship situations. However, we also find evidence of congestion, where the elimination of documentation requirements increased processing times for applicants, undoing some of the positive benefits. These findings suggest that shifting the documentation burden to the state without sufficiently expanding state capacity may substitute one form of administrative burden for another.

The administrative burden of proving eligibility for government programs is shown to undermine program equity and effectiveness (Christensen et al. 2020; Heinrich 2018, 2016). Means-tested programs are often associated with compliance burdens, such as significant paperwork and documentation requirements to confirm that would-be recipients meet program eligibility requirements (Moynihan, Herd, and Ribgy 2016). The Hardest Hit Fund (HHF) is a multistate foreclosure prevention initiative launched in 2010 that provided mortgage assistance to homeowners with financial hardships. The means-tested program has been criticized for its onerous documentation requirements and long application processing times (Special Inspector General 2018). In this article, we examine the effects of reforms to reduce administrative burden in Ohio’s HHF program.

In an effort to get assistance more quickly to homeowners in need, the Ohio HHF program enacted reforms to, first, streamline the application process—including temporarily eliminating a requirement that applicants submit documentation to prove a financial hardship, and, second, improve internal processes for reviewing and approving applications, thereby reducing congestion and lengthy applicant wait times. Both types of reforms affect the compliance costs of application—but in theoretically distinct ways. Building from the literature on human capital and individual agency in the experience of burdens (Christensen et al. 2020; Peeters and Campos 2021; Masood and Azfar Nisar 2021), we define two sources of compliance costs, active and passive. Active compliance costs are incurred when the individual applicant is responsible for taking the next action, such as filling out paperwork or submitting documentation. Passive compliance costs are incurred when the applicant must wait for the organization to take the next action, such as processing or approving the application. Most application processes impose both active and passive compliance costs on individuals, but in varying degrees.

The distinction between active and passive compliance costs adds nuance to the notion of shifting burdens between the individual and the state. Limited organizational capacity and bureaucratic processes can lead to congestion and lengthy delays for applicants—as was the case in the HHF program studied here. In fact, congestion is common in emergency assistance programs that are ramped up quickly in response to a crisis, such as in the Emergency Rental Assistance program launched in the wake of the COVID pandemic (Aiken, Ellen, and Reina 2023, this issue). Thus, even if the intention is to get benefits out quickly to as many people as possible, congestion may unintentionally create burdens for applicants, negatively affecting those who may be most in need but are unable to persist through a lengthy process. This reinforces the need to think holistically about the regime of burdens experienced by individuals rather than narrowly focusing on a single burden (Herd et al. 2013; Moynihan, Gerzina, and Herd 2022; Rauscher and Burns 2023). State actions or inactions to alleviate one source of burden may unintentionally exacerbate other sources of burdens. Thus, shifting burdens from the individual to the state without adequate attention to state capacity may simply substitute active compliance costs, such as arduous application processes, for passive compliance costs, such as long wait times.

For this study, we leverage rich administrative data on 68,460 households that began the application process to Ohio’s HHF program between September 2011 and the end of 2014, of which 17,564 ultimately received assistance. We refer to the rate of transition from beginning the application to ultimate receipt of benefits as the program pull-through rate. Active and passive compliance costs are typically incurred after deciding to apply to a program and affect who persists through the process. Our data provide a unique lens on this stage of the process. The administrative data include detailed information on applicant characteristics, including race, income, and source of hardship, as well as information about whether an applicant eventually received assistance. We link these data to individual-level data on wage earnings, unemployment claims, and loan outcomes from 2009 to 2016.

Using these data, we estimate interrupted time-series analysis (ITSA) and linear probability models (LPM) to identify the association between the introduction—and subsequent removal—of reforms intended to reduce compliance costs on applicant processing times, pull-through rates, and subsequent program outcomes—regardless of whether applicants experienced foreclosure within three years of applying for assistance. The ITSA model allows us to examine changes in outcomes immediately after the introduction of the policies by aggregating individual data to the month level and identifying an interruption or discontinuity in the expected time trend. However, the ITSA model does not control for individual characteristics that may also vary with the introduction of the policy, which is a strength of the LPM. Comparing outcomes across the two specifications increases confidence in our results.

Our ITSA results indicate that administrative reforms enacted to reduce active and passive compliance costs were associated with an increased HHF pull-through rate of 4.1 percentage points—a 22.7 percent increase over the previous pull-through rate. These changes were also associated with a reduced three-year foreclosure rate of 1.6 percentage points, or 7.5 percent among all individuals who started the HHF application process, regardless of whether they ultimately received assistance. In our LPM specification, the reforms are associated with a 2.8 percentage point (19 percent) reduction in the probability of foreclosure. This is a substantive reduction in foreclosure: a prior study found that the receipt of HHF assistance was associated with a 40 percent reduction in the probability of mortgage default and foreclosure (Moulton et al. 2022). Reduced administrative burdens thus increased the probability that individual who started the application and who may have otherwise experienced foreclosure ultimately received HHF assistance, thereby reducing the probability of foreclosure for the entire applicant pool.

However, we also find evidence that some of the reduction in active compliance costs—the elimination of required documentation—was associated with increased passive compliance costs as measured by increased application processing times. Our ITSA model results show that application processing time increased by twenty-seven days (14 percent) after the initial policy changes, the increase being driven by the time it took the state agency to process the application after the participant submitted the application (passive compliance costs). When the documentation requirement was reinstated, we observe a significant reduction in processing times, a further increase in applicant pull-through rates, and a further decrease in foreclosure. Taken together, these findings suggest that shifting the documentation burden to the state without sufficiently expanding state capacity may simply substitute one form of administrative burden (active compliance costs) for another (passive compliance costs)—both of which have detrimental effects on applicants.

Our data allow us to observe differences in responsiveness to application compliance costs based on the complexity of an applicant’s situation (Herd and Moynihan 2018). In Ohio’s HHF program, the documentation process was easiest for applicants who were receiving unemployment benefits. Other hardships, such as loss of income associated with a medical hardship, divorce, or death of a spouse were more difficult to document. In our preferred specification, we find no significant association between reduced compliance costs and the pull-through rate for homeowners with easy-to-document unemployment claims, whereas the pull-through rate for homeowners without unemployment claims increased by more than 56 percent. Similarly, we find an 11.3 percent decrease in the foreclosure rate for homeowners without unemployment benefits, but no significant difference in foreclosure rates for homeowners with unemployment benefits.

We also examine heterogeneity in outcomes for groups that we expect to be more or less likely to be affected by administrative burden. Studies find that administrative burden disproportionately affects disadvantaged groups (Christensen et al. 2020; Herd and Moynihan 2018; Jilke, Van Dooren, and Rys 2018; Nisar 2018). We find that reduced compliance costs are associated with a higher probability of women receiving assistance, an association largely driven by women without unemployment benefits. Further, demographic differences in the composition of homeowners without unemployment benefits versus those with unemployment benefits are important. Homeowners without unemployment benefits were more likely to be Black, more likely to be female, and more likely to be older. Thus, the administrative reforms were associated with improved program equity for these disadvantaged groups.

This article makes several unique contributions to the literature. First, we define and test two theoretically distinct sources of compliance costs—one that requires the applicant to take action (active compliance costs), and another that requires the applicant to wait on the state to take action (passive compliance costs). This distinction extends an understanding of how differences in human capital and behavioral factors may interact with different forms of burden to exacerbate inequities in the distribution of benefits (Christensen et al. 2020; Linos and Riesch 2020; Masood and Azfar Nisar 2021; Peeters and Campos 2021). Second, we call attention to regimes of burdens and the interplay between organizational factors and the experiences of administrative burdens by individuals. Although actions of the state and experiences of burden are distinct constructs (Baekgaard and Tankink 2022; Madsen, Mikkelsen, and Moynihan 2020), our findings demonstrate that slow or backlogged organizational processes can translate into an experience of passive compliance costs for individuals. When designing interventions to increase the flow of applicants into the system, such as streamlining application requirements, administrators should also consider agency capacity to process the flow of applicants through the system. Finally, our study is among a handful to examine the effects of administrative burden on the outcomes of individuals targeted for the program. In line with Mansai Deshpande and Yue Li (2019), we find evidence that reductions in compliance costs improve targeting efficiency, defined here as a reduced rate (and probability) of foreclosure among the pool of applicants.

THEORETICAL FRAMEWORK: COMPLIANCE COSTS, EQUITY, AND EFFECTIVENESS

In this study, we focus on persistence through the application process—from the initial expressed intent to apply to the ultimate receipt of benefits—and how this process affects who receives benefits and the subsequent program outcomes. The burdens experienced during this process are often referred to as compliance costs, defined as the “material burdens of following administrative rules and requirements,” including “time lost waiting in line, completing forms or providing documentation of status” (Herd and Moynihan 2018, 15). Numerous studies document the effects of arduous application processes, finding that more complex forms, larger amounts of required documentation, increases in the number of application steps, and long wait times are associated with reduced applicant persistence through the process (Deshpande and Li 2019; Herd et al. 2013; Foote, Grosz, and Rennane 2019; Godard, Koning, and Lindeboom 2019; Linos and Riesch 2020). Compliance costs may also interact with other forms of administrative burden, such as learning and psychological costs. For example, the process of completing application steps may contribute to learning about program eligibility (Linos and Riesch 2020), and categorizing oneself as unemployed or self-employed may be associated with stigma and impose psychological costs (Moynihan et al. 2022).

We propose two theoretically distinct sources of compliance costs based on the degree of agency an individual has over an experienced burden at a particular stage in the application process (Peeters and Campos 2021). At some stages of the process, much of the agency is on the individual to take the next step through a complicated maze of actions. Although the state establishes procedures, such as creation of forms or documentation requirements, it is up to the individual to complete the paperwork and submit documentation. Human capital and cognitive resources are critical at this stage of the process to navigate information and discern program requirements (Christensen et al. 2020). The more complicated an individual’s situation and the fewer resources available to them, including human capital, the less likely they are to persist. For example, more stringent documentation processes to verify eligibility for disability benefits reduced take-up among individuals with mental health impairments and more difficult-to-document conditions (Godard, Koning, and Lindeboom 2019). We refer to this stage as incurring active compliance costs.

In other stages, the applicant’s primary task is to wait on the state to take action—to process paperwork, determine eligibility, and allocate benefits. At this stage, organizational red tape and state capacity constraints can create congestion and long wait times that individuals experience as administrative burden (Ali and Altaf 2021; Deshpande and Li 2019; Heinrich et al. 2022). Long wait times may be particularly burdensome for those in a state of crisis and already emotionally taxed. For example, individuals in need may be present-biased and less willing and able to persist through a lengthy process in exchange for uncertain benefits (Frederick, Loewenstein, and O’Donoghue 2002). Although individuals still have agency at this stage in the process, it is more directed at navigating complex bureaucracies, and the extent of their agency depends in part on administrative capital, defined as applicants’ “explicit or tacit knowledge of bureaucratic rules, processes, and behaviors” (Masood and Azfar Nisar 2021). We refer to this stage as incurring passive compliance costs.

The delineation between active and passive compliance costs allows for a theoretically richer examination of how human capital and behavioral constraints may come into play at different stages of the application process, affecting who persists and receives benefits. Traditional economic models assume that administrative burdens (ordeal mechanisms) lead to targeting efficiency, where those truly in need of benefits are more likely to persist through a burdensome process (Finkelstein and Notowidigdo 2019; Nichols and Zeckhauser 1982). However, a growing body of empirical research finds the opposite—that those who are most in need of benefits are more likely to be negatively affected by burdens (Bhargava and Manoli 2015; Deshpande and Li 2019; Godard, Koning, and Lindeboom 2019; Heinrich 2016). One of the reasons for this discrepancy is the oversimplification of burdens in the economic literature—without specifying theoretically distinct effects based on different sources of burdens and varying individual experiences of the same burden (Heinrich et al. 2022; Madsen, Mikkelsen, and Moynihan 2020). Individuals may experience the same burden differently depending on underlying differences in human capital, administrative capital, motivation, and behavioral biases (Bertrand, Mullainathan, and Shafir 2004; Christensen et al. 2020; Masood and Azfar Nisar 2021).

This delineation between active and passive compliance costs serves pragmatic purposes. Much focus in the literature has been on reducing active compliance costs by simplifying forms, reducing paperwork requirements, and providing information and assistance to complete paperwork. Less focus has been on reducing passive compliance costs. Part of this may be due to ease of study—changes to forms or information are more amenable to experimental manipulation than changes to agency capacity. However, part may be the distinction between individual experiences of burdens and state actions that contribute to burdens (Baekgaard and Tankink 2022; Madsen, Mikkelsen, and Moynihan 2020). The study of burdens within government agencies is a separate literature, including research on organizational red tape (Bozeman and Feeney 2011; Bozeman, Reed, and Scott 1992; Pandey and Scott 2002) and managerial process reforms (Boyne and Walker 2002; Damanpour, Walker, and Avellaneda 2009). Thus some may argue that passive compliance costs are out of scope for studies of administrative burden. However, management reforms that streamline internal processes or simplify red tape may reduce congestion and be experienced as shorter wait times, thus increasing the likelihood of individuals persisting through the application process.

Rather than viewing active and passive compliance costs as independent, we expect that any application process has a combination of both at different stages. Also, burdens can shift between the individual and the state (Herd and Moynihan 2018), though shifting burdens to the state will not necessarily reduce administrative burdens for individuals. Certainly, states can intentionally impose costs on individuals in the application process as policymaking by other means (Agarwal et al. 2017; Herd and Moynihan 2018; Linos and Riesch 2020; Moynihan, Herd, and Ribgy 2016; Ali and Altaf 2021; Doughty and Baehler 2020). However, even well-intended efforts to reduce administrative burdens to individuals who do not sufficiently invest in internal capacity or address red tape may simply be exchanging one type of administrative burden for another—from active compliance costs of filling out complex paperwork to passive compliance and psychological costs to endure excessive delays.

POLICY BACKGROUND

This article examines outcomes associated with active and passive compliance costs in the context of a foreclosure prevention program. In times of economic crisis, such as the Great Recession that began in 2008 or the COVID-19 pandemic that began in early 2020, massive waves of unemployment and economic downturn result in people being unable to pay their bills. The largest bill for most households in the United States is housing, and for the 65 percent of U.S. households who own a home (U.S. Census Bureau 2022), this expense most often takes the form of a mortgage payment to a private lender. Failure to make mortgage payments results in the loan being in default. If nonpayment continues, the lender will foreclose on the property, a process during which the homeowner is evicted.

The direct and indirect costs of foreclosures for households and communities (Diamond, Guren, and Tan 2020) motivate a variety of policy responses to help prevent mortgage defaults. During the Great Recession, the federal government allocated more than $45 billion to help distressed homeowners (U.S. Department of the Treasury 2017). Yet such policies often rely on the voluntary take-up of interventions by individual homeowners who are experiencing substantial distress as well by as the voluntary participation of private lending institutions. Not surprisingly, foreclosure prevention programs end up being underused by the people who may benefit the most, with programs being criticized for serving too few homeowners in a time of crisis (Agarwal et al. 2017; Special Inspector General 2015b, 2015a). A Special Inspector General report (2015b) indicates that the more than one million homeowners, a quarter of all denied requests, were denied assistance under the Home Affordable Mortgage Program (HAMP) because the homeowner failed to provide “the financial and/or hardship verification documentation required to complete the evaluation of their request in a timely manner”—not because the homeowner was ineligible for assistance.

Some of the administrative burdens in the foreclosure prevention process are intentional. As with other need-based benefit programs, such as unemployment or disability insurance programs, moral hazard and fraud are concerns. Ideally, mortgage assistance programs aim to help homeowners who would otherwise default on their mortgage absent the intervention, but with the intervention will be able to resume making timely payments. Yet the intervention could induce homeowners to default in order to qualify for assistance (moral hazard), crowding out limited subsidies for homeowners who truly need and would benefit from the assistance (Mayer et al. 2014). In an extreme case, fraud could also be possible when individuals or lending institutions falsify or withhold information to obtain—or prevent people from obtaining—benefits (Karikari 2013).

In light of these concerns, mortgage assistance programs historically include an onerous screening process to verify the presence of a hardship and to evaluate the likelihood of resuming payments when assistance ends. However, recent research suggests that appropriately designed streamlined processes can increase take-up among distressed homeowners without evidence of extensive moral hazard or fraud (Farrell, Greig, and Zhao 2020; Goodman, Scott, and Zhu 2018). For example, in response to the 2020 COVID-19 pandemic, the federal government announced that federally insured or securitized mortgages, about 80 percent of the market, could receive a temporary suspension of their mortgage payments for up to eighteen months if they experience a COVID-related financial hardship—with no documentation of hardship or lengthy application process.1 Despite more than 9 percent of U.S. homeowners taking advantage of forbearance in 2020, preliminary research does not find evidence of moral hazard or fraud (Farrell, Greig, and Zhao 2020).

STUDY CONTEXT

The study context for this article is the HHF foreclosure prevention program. HHF was administered through state housing finance agencies during the Great Recession, assisting more than 418,000 homeowners with total federal funding of $8.8 billion from 2010 through the end of the program in 2020 (U.S. Department of the Treasury 2021). Although some of the assisted homeowners received mortgage modifications, most received temporary mortgage payment assistance, under which government subsidies were used to pay mortgage payments during a spell of unemployment. Given the assistance was structured as a subsidy, federal guidelines required states to verify homeowner eligibility—including documentation of hardship. Eligibility criteria were similar across states but showed some variation in the maximum allowable household income and mortgage balance.2 Government reports on HHF describe difficulty getting money in the hands of homeowners in part because of excessive administrative burden. In 2015, the Special Inspector General for the Troubled Asset Relief Program (2015a) released a scathing report titled “Homeowners Have Struggled with Low Admission Rates and Lengthy Delays in Getting Help from TARP’s Second-Largest Housing Program—The Hardest Hit Fund,” finding that only 43 percent of homeowners who applied for HHF since 2010 had received assistance as of June 30, 2015, and that the median wait time was six months. Ohio’s program was singled out as a program with substantial delays. Research indicates that, despite lower than intended take-up rates and delays, those who did receive HHF assistance were 40 percent less likely to experience foreclosure on their homes three years after rolling off assistance (Moulton et al. 2022).

The Ohio Housing Finance Agency (OHFA) launched Ohio’s HHF program on September 27, 2010. Ohio was one of eighteen states along with the District of Columbia to receive federal funding under the Department of Treasury’s HHF program, receiving the third largest allocation of federal HHF dollars of any state. Ohio was selected for the program because of high unemployment, which resulted in thousands of homeowners being unable to afford their mortgage payments (U.S. Department of the Treasury 2010). Program administrators estimated that the state’s initial allocations would only be able to serve a small fraction of the homeowners at risk of foreclosure (OHFA 2011, 13). They therefore initially designed several rules to limit eligibility (OHFA 2010). Given the rapidly rising number of foreclosures in the state, agency administrators were under pressure to design and implement the program quickly, and thus the agency drew on eligibility, documentation, and capacity processes that were already in place for other mortgage assistance programs.

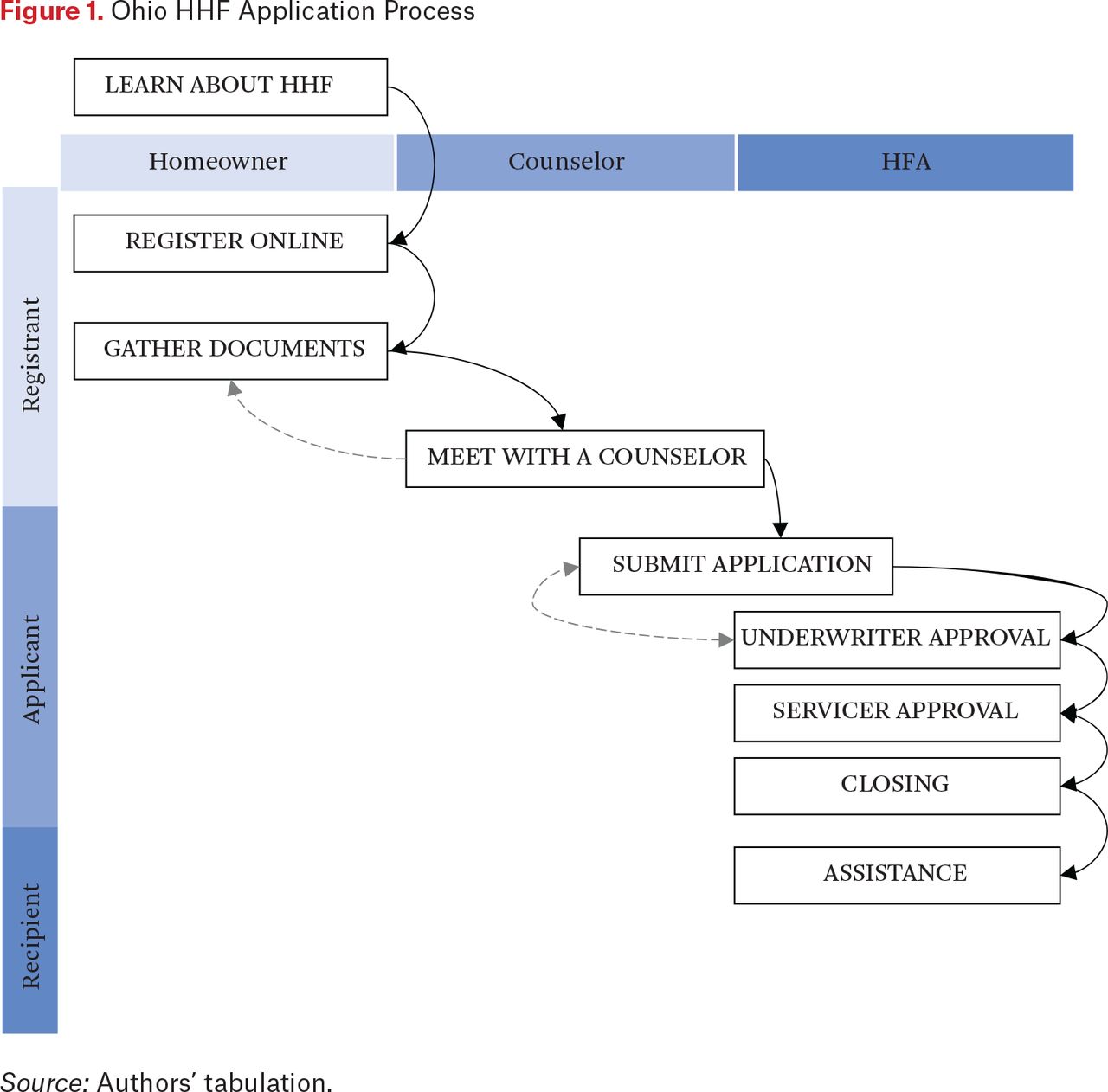

In practice, the program that launched in September 2010 involved several steps homeowners had to complete before receiving assistance from Ohio’s HHF program (see figure 1). First, homeowners became registrants by visiting the HHF website and entering their name, Social Security number, county, and email address. At this point, registrants continued their online registration, which involved seven pages of questions about their demographic characteristics, financial situation, mortgage, property, and hardship. Once the online registration was complete, registrants printed their registration packet and submitted it to a housing counselor along with additional documents to demonstrate their mortgage amount, proof of ownership, income, and financial hardship. Registrants were assigned to a housing counselor, typically at a local nonprofit organization, to verify eligibility and submit applications on homeowners’ behalf. Registrants could not submit their own applications to OHFA, which created additional delays when housing counselors were backlogged with cases.

Ohio HHF Application Process

Source: Authors’ tabulation.

Once a housing counselor submitted a registrant’s application, the registrant became an applicant. Underwriters at OHFA were tasked with reviewing applications and requesting additional documentation if applications were incomplete or if submitted documentation was deemed insufficient. After an applicant was determined eligible, OHFA contacted the applicant’s mortgage servicer to request servicer approval. If the servicer approved the applicant, OHFA arranged a closing with a third-party title company. After the closing, the applicant became a recipient when the first payment was sent to the homeowner’s mortgage servicer. The first part of the process, during which a registrant completed the required steps to become an applicant, was largely associated with active compliance costs; the second part, during which the applicant waited on OHFA and the servicer to process and approve the application, was mostly characterized by passive compliance costs.

By mid-2012, Ohio HHF administrators were concerned about the time it was taking HHF registrants to move through the process and the low percentage of registrants who ultimately received assistance. At the time, the registration to application pull-through rate was 29.7 percent, the application to assistance pull-through rate was 48.6 percent, and the average length of time from registration to funding was 173 days (LeanOhio 2012). HHF administrators consulted with LeanOhio, a state agency tasked with helping other state agencies improve program efficiency through analyzing work processes and identifying ways to make them simpler, faster, and less expensive (LeanOhio 2022). LeanOhio was based on the Lean Six Sigma model, a total process improvement model that began in the private business sector and permeated government by the early 2000s (Maleyeff 2007; Radnor 2010). By the end of a week-long LeanOhio event, HHF administrators decided to implement several process and policy changes to improve pull through, reduce processing times, and increase program generosity (LeanOhio 2012; Garver and Alston 2013). Table 1 describes the administrative reforms conceived at the 2012 LeanOhio event that were implemented on February 1, 2013. We classify changes by the associated sources of administrative burden they were designed to target.

Ohio HHF Program Administrative Reforms Introduced February 1, 2013

In this study, we are interested in the outcomes of administrative reforms to reduce active and passive compliance costs. We thus focus on the stage in the process after homeowners initially registered for HHF assistance. Changes to program marketing and pre-registration screening primarily targeted learning costs before beginning the registration and application process. In regard to active compliance costs, program administrators eliminated the requirement for homeowners to provide supporting documentation to demonstrate their financial hardship. Such documentation was particularly burdensome for people with hardships other than an Unemployment Insurance (UI) claim—such as wage loss, death, disability, divorce, or significant medical expenses, or who were involuntarily unemployed but did not for various reasons qualify for UI. Treasury approved Ohio’s elimination of hardship documentation but required OHFA to audit 10 percent of homeowners who received HHF assistance each month—verifying their stated hardship with documentation (OHFA 2013). By the end of 2013, there was concern that a high share of audited recipients had failed the documentation test, causing OHFA to reinstate hardship documentation for all registrants beginning in January 2014 (OHFA 2015a, 11).

OHFA implemented other changes to reduce active compliance costs, including revising the online application form and expanding its Consumer Advocacy Center to proactively help registrants complete their applications. It also reduced passive compliance costs by substantially reducing the number of internal steps required of OHFA underwriters to process applications. Finally, it expanded benefit generosity by adding new types of assistance, increasing the maximum benefit amount, and extending the duration of benefits. These changes remained in effect after the January 2014 reinstatement of the documentation requirements.

The introduction and subsequent rollback of administrative reforms resulted in three distinct regimes of burdens experienced by homeowners seeking assistance through Ohio’s HHF program. The pre-regime is the period before any of the administrative reforms listed in table 1, that is, before February 1, 2013. Post-regime 1 is the initial period after the introduction of most of the reforms in table 1, including the removal of hardship documentation, from February 1, 2013, until January 1, 2014. Post-regime 2 is the period after the reinstatement of the hardship documentation requirements while continuing the other administrative reforms and increasing the maximum benefit amount, on or after January 1, 2014. We expect both post-regimes to be associated with an increase in registrant pull-through rates and a decrease in foreclosure rates relative to the pre-regime. To the extent that removal of hardship documentation requirements creates congestion, we expect that post-regime 1 may be associated with longer processing times, lower pull-through rates, and higher foreclosure rates than post-regime 2. On the other hand, to the extent that applicant documentation requirements were the primary burden affecting pull through in the HHF program, we expect post-regime 1 to be associated with better outcomes than post-regime 2.

In line with the literature that finds applicants with complex cases are more negatively affected by compliance costs (Godard, Koning, and Lindeboom 2019), we hypothesize that the reduction in compliance costs associated with both post-regimes will affect registrants with complex hardships more than those with less complex hardships. In the HHF context, registrants with verified UI claims were able to prove their hardship more easily and with less documentation than homeowners with other types of hardships. Registrants with recently successful UI claims may also have more “administrative capital” to navigate complex bureaucratic processes than registrants without UI claims (Masood and Azfar Nisar 2021), and thus may be less affected by reforms to streamline the process or to provide applicant support.

DATA AND METHODS

The primary source of data for this analysis is Ohio HHF administrative records provided by the state agency. The records include self-reported demographic, financial, hardship, mortgage, and property information on everyone who started the registration process between 2010 and 2015. Our analysis focuses on the 68,460 households that registered for HHF between September 2011 and February 2015, when the program stopped accepting new registrations.3

The second source of data comes from the Ohio Department of Job and Family Services, which is the state agency that administers the UI program and collects wage and employment records on people who work in Ohio.4 The data, provided by the Ohio Longitudinal Data Archive (OLDA),5 includes information on total wages paid and hours worked by employer, UI wages, and UI claims by quarter from 2009 to 2016. The employment data was linked to OHFA administrative records using Social Security number and deidentified prior to being shared with the authors. The third source of data comes from CoreLogic. The CoreLogic data comprise public property tax records and recorded transactions associated with each borrower-property combination, such as mortgage liens, sales, and foreclosure activity. CoreLogic matched this data to the Ohio HHF administrative records using address and homeowner name prior to de-identifying and sharing with the authors.

We focus our analysis on homeowners who registered for Ohio’s HHF program. Recall that a registrant is anyone who started the online application process for Ohio’s HHF program. We exclude registrants who did not complete all seven pages of their online registration packet, which allows us to focus on policy changes that may affect applicant pull through rather than changes to streamline the online registration process. We also drop registrants whose registration data suggest they were not eligible for assistance due to property or mortgage requirements, and we exclude those who repaid all of their HHF assistance or who owed a repayment to OHFA.6

Just over 73 percent (N = 50,431) of registrant households remain after applying these exclusions. To align our final samples and isolate the effects of changes to compliance burdens rather than expanded eligibility or benefits, we apply pre-regime eligibility criteria to all registrants, ensuring that registrants in the post-regimes would have qualified for HHF under the pre-regime criteria. Eligibility criteria that became more generous in both post-regimes include percent area median income (AMI), and the Federal Housing Administration (FHA) lending limit. Post-regime 2 also included an increase in the maximum benefit amount, from $25,000 to $35,000. However, the benefit amount received was still a function of applicant need based on the size and amount of past-due mortgage payments. We thus run predictive models to estimate the maximum benefit required by a registrant and limit the analysis sample to those with predicted benefit amounts of $25,000. This and the other exclusions described here increase our confidence that observed changes in outcomes of interest relate to changes in compliance burdens rather than to changes in program generosity.7 Our final analysis sample comprises 44,140 people who registered for assistance in the pre-regime or post-regimes 1 and 2.

After constructing our main sample, we use information on UI claims to split our registrant sample into two groups: registrants with a verified UI claim (UI registrants) and registrants without a verified UI claim (non-UI registrants). To do this, we create an indicator for any adult in the household having a verifiable UI claim in the linked OLDA data. Table 2 provides summary statistics for our final samples. On average, 27 percent of registrants received HHF assistance within twelve months of completing registration, though just 20 percent of non-UI registrants received assistance versus 38 percent of UI registrants. Approximately 15 percent of registrants had foreclosure activity—defined as any foreclosure activity recorded in property records, including ninety-day default, foreclosure filing, judgment, or foreclosure sale—that occurred within three years after registration.8 The median processing time between registration and receipt of HHF assistance was 183 days for the full sample, 168 days for UI registrants, and 202 days for non-UI registrants. The median time between registration and application was shorter than that between application and receipt (sixty-three and 101 days, respectively), suggesting that HHF recipients spent about two-thirds of the application process experiencing passive compliance costs in the form of wait time.

Summary Statistics, HHF Registrant Sample

Differences between registrants with and without a UI claim are notable. Women made up fewer than 50 percent of UI registrants but more than 57 percent of non-UI registrants. Similarly, Black registrants made up 27 percent of non-UI registrants and just 19 percent of UI registrants. The percentage of UI registrants reporting that they were married was also higher than that of non-UI registrants (53 percent and 43 percent, respectively).

We conduct a series of simple regressions to identify whether any demographic and economic differences in new registrants across policy regimes are statistically significant. Table A.2 presents several differences. For instance, registrants were slightly older in post-regimes 1 and 2 than in the pre-regime, and the share of Black registrants decreased in later regimes. New registrants had slightly less income (measured as percent AMI) in the post-regimes and higher debt-to-income ratios but were less likely to report a prior bankruptcy or an active foreclosure. These differences likely reflect changes in the nature of the foreclosure crisis as the economy began to recover from the Great Recession (Chun, Pierce, and Van Leuven 2021; Immergluck 2015). The methods we describe in the next section attempt to address these evolving differences in two ways. Our first approach examines marginal differences in outcomes just before and after the introduction of a new policy regime. The second controls for a rich set of demographic and economic characteristics.

METHODS

We use two modeling approaches to examine the relationship between regimes and program outcomes. The first uses a single-group ITSA model, which accounts for the autoregressive nature of the data organized by time (Hartmann et al. 1980). For this analysis, we use a single-group model with three phases—pre-regime, post-regime 1, and post-regime 2—as Ariel Linden (2017, 2015) describes. The main ITSA model takes the following form:

where Yt represents the aggregated dependent variable at month t. We model five dependent variables: the HHF pull-through rate (receipt of HHF assistance within twelve months of initial registration), the foreclosure rate (foreclosure activity within three years of initial registration), the median processing time between registration and application, the median processing time between application and HHF receipt, and the median processing time between registration and HHF receipt. In alternative specifications, we model the application rate (the share of registrants who submit a complete application within six months). Tt denotes the time, in months, since the start of the study period. POST1t and POST2t are indicators representing post-regimes 1 and 2. POST1tT1t and POST2tT2t are interaction terms. β0 is the coefficient for the intercept or starting level for the dependent variable. β1 is the coefficient for the slope of the outcome variable until the introduction of the intervention. β2 and β4 denote the change that occurs in the month immediately following the introduction of the post-regimes 1 and 2, respectively, relative to the prior regime. β3 and β5 represent the difference between the pre-regime and post-regime 1 slopes of the dependent variable, and the post-regime 1 and post-regime 2 and slopes of the dependent variable, respectively. The random error term, et, follows a first-order autoregressive process, such that ρ is the coefficient between error terms at time ε t – 1 + u1t and are independent disturbances (Linden 2015). We use a general specification test of serial correlation to confirm the inclusion of a single autoregressive lag (AR1) (Baum and Schaffer 2013; Cumby and Huizinga 1992). Finally, for the ITSA model, we exclude the two months prior to the start of post-regime 1, given evidence of strategic behavior in the lead-up to the policy change (see figure 2). In addition to estimating the overall rate of the outcomes, we also estimate the pull-through and foreclosure rates separately for people with and without a verified UI claim.

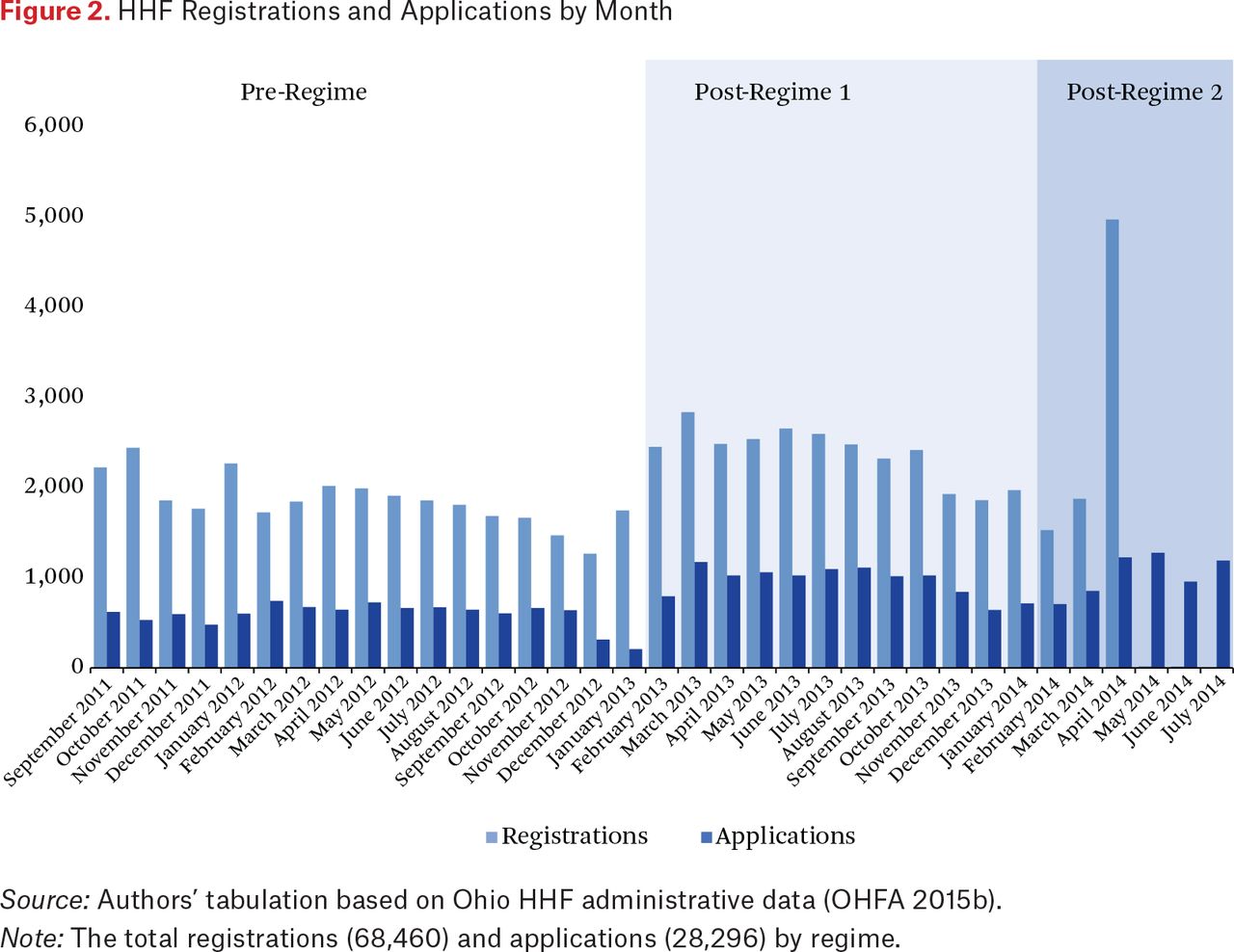

HHF Registrations and Applications by Month

Source: Authors’ tabulation based on Ohio HHF administrative data (OHFA 2015b).

Note: The total registrations (68,460) and applications (28,296) by regime.

Although the ITSA model allows us to isolate changes in outcomes associated with the introduction of each regime in short time increments, we are unable to control for registrant characteristics that may shift with each regime and affect program outcomes. To control for individual characteristics, we estimate a series of linear probability models. The main LPM is as follows:

where Yi represents the probability that a registrant receives HHF assistance within twelve months after starting the initial application and, alternatively, the probability that the registrant experiences foreclosure activity within three years after starting the initial application. In alternative specifications, we also examine the probability that a registrant submits a complete application within three, six, and nine months. In all specifications, we include dummy indicators for beginning the application (thus becoming a registrant) during post-regime 1 or post-regime 2 (omitted category is the pre-regime), where the coefficients (β1 or β2) represent the change in the probability of the outcome associated with a respective regime. We include a vector of covariates (χ1) at the time of initial application such as race, ethnicity, gender, age, education, household size, percent AMI, hardship, debt-to-income ratio, mortgage amount, year the home was built, square footage, and acreage. In alternative specifications, we add interaction terms between the regime indicators and the indicators for race, gender, and age to test for heterogeneous effects. We control for history of past mortgage delinquency or foreclosure actions found in property records, as well as having received a foreclosure notice, which was self-reported by registrants in their initial applications. We include controls for self-reported hardship type.9 Finally, we control for the county-level unemployment rate by month to account for macro-level trends over time and across counties. ei is the error term.

RESULTS

Figure 2 graphs the total number of households that began the registration process or submitted applications by month during our study period.10 The number of applications submitted in the two months before the start of post-regime 1 decreases significantly, corresponding to an announcement from OHFA that the administrative reforms were forthcoming—resulting in people delaying applications until after the changes took effect. Following the launch of post-regime 1, the number of submitted applications surged by 280 percent in February 2013. Post-regime 1 also coincided with a 42 percent increase in the monthly number of registrations, likely tied to increased advertising that accompanied the launch of the new policy regime (Garver and Alston 2013). We drop the two months before the post-reform regimes from our ITSA analysis given the strategic behavior of applicants following the reform announcement.

ITSA RESULTS

Table 3 displays the results of the ITSA specifications. We find a statistically significant relationship between post-regime 1 and each of the dependent variables of interest. The HHF pull-through rate increased by 4.1 percentage points, a 22.7 percent increase over the pre-regime pull-through rate (p < .01), and the foreclosure rate decreased by 1.6 percentage points during the three years following HHF registration (p < .05). The application pull-through rate increased by 3.4 percentage points, or 12 percent, (p < .05) at the beginning of post-regime 1 (for ITSA results on the application rate, table A.3). Following the introduction of post-regime 2, pull-through rates once again increased, and registrant foreclosure rates decreased.

Interrupted Time Series Results, HHF Registrants

When we split the registrant sample by whether or not they had a UI claim, we see that the post-regime indicators are only statistically significant for non-UI registrants. For this group, the pull-through rate increased by 5.1 percentage points, or 56.7 percent, following the introduction of post-regime 1. The application rate increased by 4.1 percentage points—20.5 percent, and the foreclosure rate decreased by 2.7 percentage points, or 11.3 percent, for non-UI registrants at the start of post-regime 1. Similarly, non-UI registrants saw a significant increase in the pull-through rate and a marginally significant decrease in the foreclosure rate following post-regime 2 after hardship documentation was reinstated. This finding indicates that it is not simply the removal of hardship documentation that is associated with improved outcomes for registrants without UI claims, but also the bundle of reforms to reduce both active and passive compliance costs more broadly.

Table 4 reports the results of the ITSA on processing times. The median overall processing time from registration to receipt increased with the introduction of post-regime 1 by 26.8 days, or 13.9 percent (p < .01). When we break out the overall processing time into two parts—registration to application versus application to receipt—we find that the effect appears to be driven by the latter. We find that the median time between application and receipt increased by 28.6 days, or 29.5 percent (p < .01). Recall that we also observed a 42 percent increase in the number of new registrants at the beginning of post-regime 1. The reinstatement of hardship documentation (post-regime 2) is associated with a reduction in overall processing time of 20.7 days—nearly offsetting the increase in processing time associated with post-regime 1. Taken together, these findings suggest that the influx of applications after the initial launch of the reforms (post-regime 1) may have overwhelmed agency capacity, leading to congestion despite the agency’s attempts to reduce applicant wait times. Interestingly, we observe little association between post-regime 1 and the time between registration and application, such that the median days decreases slightly, but the effect is not statistically significant.

Interrupted Time Series Results for Processing Times, HHF Registrants

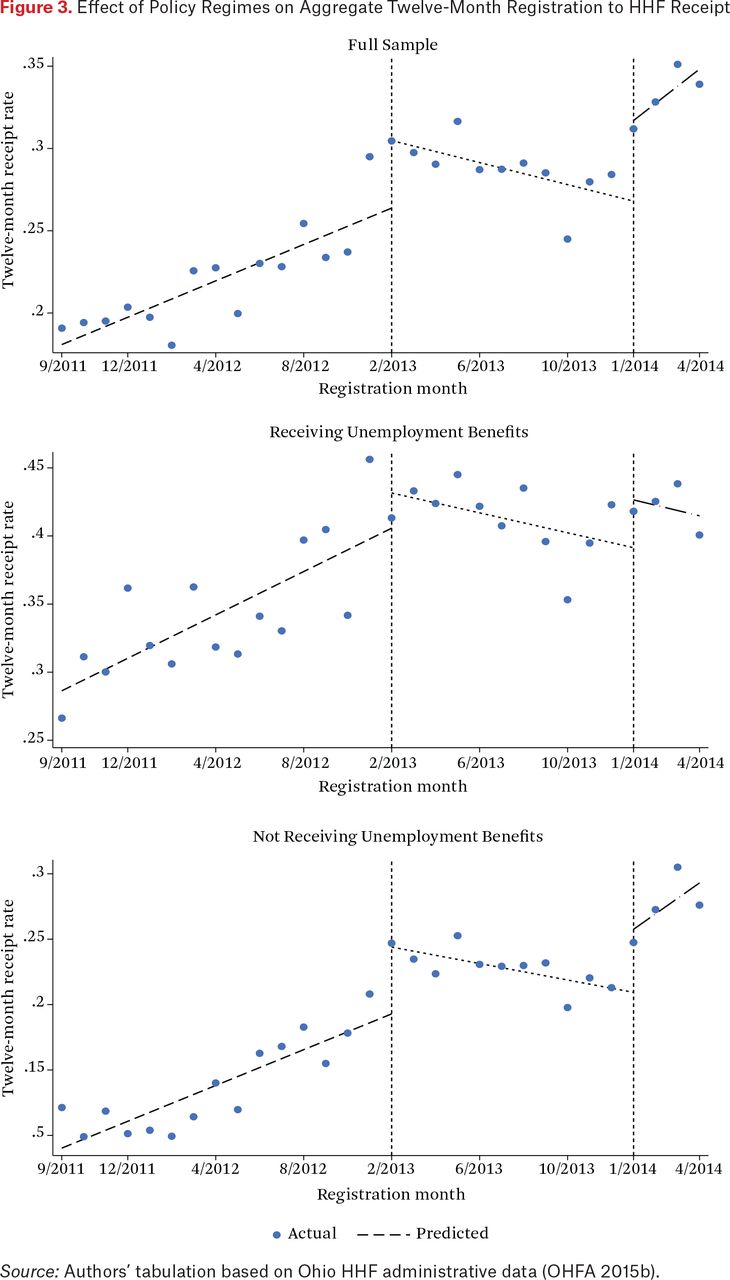

We visualize the effects of the administrative reforms on the aggregate outcomes in figure 3, which displays the ITSA results for the HHF pull-through rate for the full sample and for UI and non-UI registrants. We see a similar pattern for each, such that the pull-through rate increases during the months prior to the first reform, in February 2013. However, the pull-through rate declines for each sample during post-regime 1, an effect that may stem from the influx of new registrants and shifting documentation burden from the applicant to the state. Post-regime 2 marks another increase in the pull-through rate for each sample, followed by a statistically significant increase in pull through for the remaining months of the program. The change in slope following post-regime 2 is not statistically significant for UI registrants.

Effect of Policy Regimes on Aggregate Twelve-Month Registration to HHF Receipt

Source: Authors’ tabulation based on Ohio HHF administrative data (OHFA 2015b).

LPM REGRESSION RESULTS, INDIVIDUAL LEVEL

Table 6 presents the results from our individual-level LPM regressions that include controls for registrant characteristics as well as changes in unemployment rates in the macro-economy.11 The results from the LPM are substantively similar to the ITSA model results.12 We find that both post-regimes are associated with a significant increase in the probability of a registrant receiving HHF assistance within twelve months relative to the omitted baseline period. Specifically, post-regime 1 is associated with a 4.5 percentage point (p < .001) increase in the probability of a registrant receiving HHF assistance, whereas post-regime 2 is associated with a 9.1 percentage point increase (p < .001), all else constant. Turning to program outcomes, we find that post-regime 1 is associated with a 2.8 percentage point (19 percent) decrease in the probability of experiencing foreclosure activity (p < .001), and that post-regime 2 is associated with a 5.0 percentage point (33 percent) decline (p < .001). To put these effect sizes in context, reported wage loss at the time of registration is associated with a 2.0 percentage point increase in the probability of foreclosure (p < .001) and having a four-year college degree is associated with a 3.7 percentage point reduction (p < .001).

Like the ITSA model results, the LPM results differ when we split our registrant sample by whether they had a verified UI claim. Whereas the post-regimes are associated with a significant increase in the probability of registrant pull-through and reduction in the probability foreclosure for both the UI and non-UI registrant subsamples, the effect sizes are larger for the non-UI registrant sample. For non-UI registrants, post-regime 1 is associated with a 6.1 percentage point (30 percent) increase in the probability of receiving HHF assistance, relative to a 3.7 percentage point (10 percent) increase for the UI registrant sample. Post-regime 2 is associated with an even larger 11.8 percentage point (59 percent) increase in the probability of receiving HHF assistance for non-UI registrants, relative to a 5.3 percentage point (14 percent) increase for the UI registrant sample. Similar to the findings from the ITSA, non-UI registrants experienced an additional boost in their pull-through rate when the documentation requirement was reinstated, indicating that the no-documentation reform was not driving the effects for post-regime 1.

In regard to the probability of foreclosure, post-regime 1 is associated with a larger reduction for non-UI registrants than UI registrants (-3.4 versus -1.9 percentage points). Post-regime 2 is associated with an even larger decrease, the effect sizes being similar for non-UI and UI registrants (-4.7 versus -5.0 percentage points).

The LPM allows us to test for heterogeneous effects of the policy regimes on outcomes by gender, race, and age by running a second set of models that interact the regime indicators with dummy variables for these subgroups. The results are shown in table A.5. We find a significant interaction between the administrative reforms and being a female in the full sample, where post-regime 1 is associated with a 2.6 percentage point higher probability and post-regime 2 is associated with a 4.0 percentage point higher probability of receiving assistance for women than for men (p < .01). We find no differential effects for race and regime or age and regime on the probability of receiving assistance or on the probability of foreclosure.

Linear Probability Model Results, HHF Registrants

ALTERNATIVE SPECIFICATIONS

We examine the robustness of our results to several alternative specifications. First, we estimate sensitivity tests for different time periods of pull through from registration to receipt. In our main models, we define HHF recipients as registrants who receive HHF within twelve months of their initial registration—capturing most registrants who go on to receive assistance. Alternatively, we estimate models that predict receiving HHF assistance within three, six, and nine months of the initial registration, as well as ever receiving assistance. The ITSA and LPM results for post-regime 1 on registrant pull-through rates are statistically significant in a negative direction when HHF receipt is defined as three months following registration. In other words, immediately after the administrative reforms, the likelihood of receiving assistance within three months decreased, likely due to capacity limitations. The number of applications submitted to HHF increased by 280 percent, causing institutional congestion and making it less likely that applications received funding quickly. The LPM and ITSA results for the regimes do not differ substantially from our main specification results when defining HHF receipt using the nine-month, or “ever” pull-through rates.

For the ITSA models, we test alternate specifications limiting the window of time to six months before and after each policy regime change, still excluding the two-month window before the beginning of post-regime 1. Overall, the effects of the administrative reforms on HHF application rate, pull-through rate, and foreclosure rate are robust to this restricted sample period.

Finally, we conduct LPM analyses using a sample of only HHF applicants—registrants who submitted a complete application. In this set of models, our dependent variable represents the probability of pull through from application to HHF receipt, and the probability of foreclosure within three years of application. Our primary specification predicts the probability of receiving HHF within six months of application, but we also estimate sensitivity tests for three, nine, and twelve months. As with the full registrant sample, we split the applicant sample into UI applicants and non-UI applicants. We find that post-regime 1 is associated with an increased pull-through rate for the full sample (5.1 percentage points) and non-UI applicants (11.7 percentage points), but the effect is not statistically significant for UI applicants (for the results, see table A.6). Post-regime 1 is associated with a reduction in the foreclosure rate of 4.1, 3.5, and 4.6 percentage points for the full, UI, and non-UI applicant samples (p < .01). Post-regime 2 is also significantly associated with an increased pull-through rate of 11.2, 7.2, and 17.3 percentage points (p < .01) for the full, UI, and non-UI applicants, respectively. All samples saw a significant decrease in the foreclosure rate ranging from 4.3 to 4.6 percentage points following the introduction of post-regime 2. The applicant model results largely support our main findings.

STUDY LIMITATIONS

Although the Ohio HHF program is an interesting case to examine administrative burden, it is a single program within a single state at a specific time during the Great Recession. It is likely that some of the findings are context dependent—for example, the extent to which internal processes create costs for program applicants likely varies substantially based on the nature of the benefit being provided, the regulations governing its distribution, the needs of the target population, and the capacity of the administering agency. Second, the ITSA’s ability to isolate causal effects rests on the assumption that the administrative reforms to reduce application compliance costs are as good as random, and that no other temporal changes corresponded to the reforms that might explain the observed differences in outcomes. However, we observe some significant differences in registrant characteristics between regimes that may be related to improvements in the macro-economy following the Great Recession (see table A.2). In light of these differences, we estimate LPMs that control for individual registrant characteristics and find substantively similar, if not stronger, results to those from the ITSA model. This increases confidence that our results are due to the changing regimes and not simply differences in registrant characteristics over time. Third, like many other field studies of administrative burden, the administrative reforms analyzed here represent a bundle of mechanisms that may affect application pull through and subsequently program outcomes. Although our study design focuses on active and passive compliance costs, the results suggest the underlying mechanisms rather than a precise test.

DISCUSSION AND CONCLUSIONS

This study advances the literature on administrative burden in several ways. First, we theoretically distinguish compliance costs as active or passive based on the degree of agency required of an individual when confronting a particular step in the application process. We show that this distinction matters for the types of applicants affected by reforms to reduce compliance costs. Specifically, individuals with more complex cases—in this case, without a UI claim who have harder-to-document hardships—were more affected by administrative reforms to reduce compliance cost. Disparate impacts for more complex cases can compound inequities across social programs. For example, research documents racial differences in the take-up of UI benefits, where people who are Black are less likely to apply for and pull through the application process for UI benefits—differences that cannot be fully explained by observable characteristics (Kuka and Stuart 2021). Our research suggests that people who are Black not only disproportionately miss out on UI benefits, but also may slip through other social safety net programs because they subsequently have hardships that are more difficult to document.

Second, our study findings highlight the need to think holistically about the regime of burdens associated with a given policy or program (Moynihan, Gerzina, and Herd 2022), rather than a single burden, such as an application form, in isolation. Although prior studies find that the removal of documentation requirements increases program take-up (Graff and Pirog 2019; Moynihan, Herd, and Ribgy 2016), we find evidence that removing hardship documentation dampened the overall effects of internal process improvements. This offers nuance to the notion of shifting burdens between individuals and the state to think about the intersection of individual and organizational burdens. Well-intended efforts to reduce active compliance costs in the HHF program led to congestion, extending internal processing times and increasing passive compliance costs to applicants. There is a need to consider internal process reforms that reduce congestion and enhance state capacity alongside more direct reforms to reduce applicant compliance costs. This is particularly relevant in times of crisis, when the aim is to distribute benefits as quickly as possible to people in need, and sometimes this intent conflicts with existing administrative processes and red tape designed to reduce fraud (Aiken, Ellen, and Reina 2023, this issue).

Third, our study contributes to the nascent literature on the distributional effects of administrative burden on program outcomes—in this case, the longer-term foreclosure rate among all individuals who started the application process. Standard economic theory on ordeal mechanisms suggests that administrative burdens are an efficient sorting mechanism, under which people most in need of benefits (in this case, who are more likely to foreclose absent intervention) are more likely to persist through an arduous process. Our findings indicate the opposite—that reductions to active and passive compliance costs are associated with improved targeting efficiency, as measured by lower rates of foreclosure among the entire pool of people who begin the application process (registrants)—regardless of whether they complete the application and subsequently receive benefits.

Appendices

Complete Summary Statistics, HHF Registrant Sample

Summary of Sample Composition Differences by Regime

Interrupted Time Series Results, 6-Month HHF Application Rate

Linear Probability Model Results, HHF Registrants

Interaction Effects of Policy Regime on Registrants by Gender, Race, and Age

Linear Probability Model Results, HHF Applicants

FOOTNOTES

↵1. Coronavirus Aid, Relief, and Economic Security (CARES) Act, Pub. L. No 116-136 (2002).

↵2. Income limits ranged between 115 percent area median income (AMI) in Ohio to no income limits in New Jersey and North Carolina. Unpaid mortgage balance limits ranged from $275,000 in Tennessee to $729,750 (the government-sponsored enterprise conforming limit for a one-unit property) in several states. Eligibility criteria became more generous over time in most HHF states.

↵3. We exclude the first year of the program—September 2010 to August 2011—because OHFA implemented other programmatic changes during the first year of operations that are not the focus of this analysis.

↵4. Self-employed individuals and people employed by the federal government are excluded from the wage data.

↵5. The OLDA is a project of the Ohio Education Research Center and provides researchers with centralized access to administrative data. It is managed by CHRR at The Ohio State University in collaboration with Ohio’s state workforce and education agencies (ohioanalytics.gov), with those agencies providing oversight and funding. For more information, including on project sponsors, see the OLDA website (https://chrr.osu.edu/projects/ohio-longitudinal-data-archive).

↵6. Approximately 12 percent (N = 8,277) of households did not complete the entire online registration packet. Another 14 percent (N = 9,752) were excluded from the sample for missing data or for failing to meet eligibility criteria. These restrictions exclude 272 people who were overpaid and owed funds to OHFA, 781 people with ineligible property types, 12,175 who did not have an active mortgage at the time of registration. Some people were excluded for more than one reason. We dropped a total of 18,029 households at this stage.

↵7. Of registrants, 2,369 exceeded pre-reform AMI limits, 147 exceeded the pre-reform FHA limit, and 3,775 had predicted benefit amounts that exceeded $25,000.

↵8. We exclude the first six months after registration from our foreclosure rate calculation to exclude foreclosure activity that may have occurred while a registrant was completing the HHF application process.

↵9. Although we split our samples by those with an observed UI claim and those without, the self-reported hardship controls for those who are unemployed or who have an unemployed household member but are missing from the UI claim data, such as those who were unemployed from jobs in other states.

↵10. The spike in registrations in April 2014 is an artifact of the wind-down of Ohio’s HHF program. April 2014 was the last month the program accepted new registrations, which led to a surge in registrations as counseling agencies, housing advocates, and local media encouraged homeowners to register before the deadline.

↵11. Table 5 presents an abbreviated set of results. Table A.4 presents the same model with all control variables shown.

↵12. The post-regime 2 coefficients are larger for the LPM than the ITSA results in part because post-regime 2 is relative to the omitted pre-regime period in the LPM model, whereas the post-regime 2 indicator is relative to the intercept at the end of post-regime 1 in the ITSA specification.

- © 2023 Russell Sage Foundation. Pierce, Stephanie Casey, and Stephanie Moulton. 2023. “The Effects of Administrative Burden on Program Equity and Performance: Evidence from a Natural Experiment in a Foreclosure Prevention Program.” RSF: The Russell Sage Foundation Journal of the Social Sciences 9(5): 146–78. DOI: 10.7758/RSF.2023.9.5.07. We thank the Ohio Housing Finance Agency for research support. The views in this article are those of the researchers and do not represent the views of the Ohio Housing Finance Agency, The Ohio State University, or any other government agency. Direct correspondence to: Stephanie Casey Pierce, at spierce1{at}utk.edu, University of Tennessee, Department of Political Science, 1115 Volunteer Boulevard, Knoxville, TN 37996, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.