Abstract

This study considers socially stratified take-up of income-driven repayment plans among federal student loan borrowers with high-debt payment obligations. Qualitative analyses of borrower complaints from the Consumer Financial Protection Bureau are used to document borrowers’ experiences of administrative burden in the federal loan repayment system. The combined effects of burdens on access to payment relief programs are quantified using both administrative data from a national sample of consumer credit reports and restricted-use survey data from the Beginning Postsecondary Longitudinal Study (BPS). Socioeconomic and racial gaps in take-up of income-driven repayment (IDR) plans are estimated among the subset of borrowers who would face high loan payment-to-income ratios under a standard repayment plan. Regression models indicate that among these borrowers, those living in lower-income census blocks are less likely to be enrolled in IDR.

Total outstanding debt for federally backed student loans in the United States grew from $229 billion in 2000 to $1.04 trillion (in constant dollars) by 2020, making educational debt the second largest type of household debt holdings after home mortgages. Forty-three million households carry student debt, including 40 percent of those headed by adults under the age of forty (authors’ calculation from 2019 Survey of Consumer Finances [U.S. Federal Reserve Board of Governors 2019]). Among those adults with student loans who are in the bottom half of the national income distribution, average student debt loads had come to exceed average annual income by 2019 (Kopparam and Clemens 2020).

Even as scholars and policymakers have produced a growing body of research on the financial effects of student loan obligations and related inequality (Houle and Addo 2018; Haughwout et al. 2019), less attention has been paid to the accompanying administrative burdens that borrowers in the federal student loan repayment system face that may exacerbate the financial strains and disparate effects of student debt. Building on concepts of administrative burden in policy implementation (Herd and Moynihan 2018) and cultural capital as a mechanism of inequality (Lareau 2015), this article assesses the difficulties and inequalities that arise from a public-private loan servicing system that places the onus on individual borrowers to navigate complex terms and negotiate directly with private loan servicers (Brodkin and Majmundar 2010).

We focus specifically on take-up of federal income-driven repayment (IDR) plans on the basis of their role as the main policy mechanism for mitigating affordability strains on student borrowers. Although all nonparent federal student borrowers are theoretically entitled to participate in some type of income-based repayment program, these programs are widely understood to be characterized by underenrollment and to feature high practical barriers to access as a result of unresponsive loan servicers, involved documentation requirements, and a confusing patchwork of rules (Frotman and Gibbs 2017; Baum and Chingos 2017; Pearl 2021).

This article examines the relationship between high administrative burden and social stratification in IDR enrollment. We argue that by making access to repayment programs effectively conditional on individuals’ abilities to parse complex program terms and traverse bureaucratic hassles (Sunstein 2019), the loan servicing system disproportionately hinders access for those in more marginalized social positions, who bring comparatively fewer resources to these administrative encounters (Cherlin et al. 2002; Brodkin and Majmundar 2010; Goldstein and Wharam 2022). The result is that borrowers with lower socioeconomic status (SES) are disproportionately excluded from the very federal programs intended to help borrowers manage the costs and risks of debt-financed higher education.

After briefly discussing federal student loan repayment programs and administrative burdens as a mechanism of inequality, this analysis draws on qualitative text analyses of Consumer Financial Protection Board (CFPB) complaint testimonials to describe the burdens that student loan borrowers experience as they attempt to manage repayment, interact with loan servicers, and access payment relief programs. The analysis reveals the variety and pervasiveness of administrative burdens throughout the loan servicing system, and identifies key ways burdens hinder borrowers’ access to payment relief programs.

The analysis then quantifies disparate effects of high administrative burden on program participation. Using administrative data from a 1 percent national sample of consumer credit reports, we estimate socioeconomic and racial gaps in take-up of income-driven repayment among the subset of borrowers who would face high (> 0.2) monthly student loan payment-to-income ratio under a standard repayment plan, and who thus most clearly stand to benefit from participating in income-based repayment.

The analysis contributes to the student loan policy literature by adding new empirical evidence on how loan servicing operates as a mechanism of stratification within the financialized higher education funding system. For research on administrative burdens, we add new insights on the role of outsourced of privatized service contractors as a source of burdens in public programs—even in the context of universalistic programs that are not subject to eligibility targeting, and where policymakers have few incentives to ration provision.

FEDERAL STUDENT LOAN SERVICING AND REPAYMENT PROGRAMS

Since the mid-1990s, federal government policy has responded to concerns about the growth of student loan debt by instituting payment relief programs intended to mitigate the adverse effects of debt burdens on borrowers. Income-based repayment programs lengthen the loan amortization and peg monthly payment to a proportion of borrowers’ discretionary income (typically 10 percent), with cancellation of the remaining balances after some period of satisfactory payments (typically twenty or twenty-five years). IDR programs have seen several refinements and expansions since their initial introduction in 1995, resulting in various flavors with slight variations in repayment terms and eligibility. All nonparent federal loans are eligible for at least one version of IDR (see table 1). IDR plans all share the policy goals of making monthly payments more manageable, insuring against lower than expected returns to higher education, and providing protection against labor-market shocks by allowing payments to adjust dynamically if earnings decline. They thereby aim to limit the financial risks of individual investments in higher education within the United States’s prevailing high-tuition, high-debt funding system.

Summary of Income-Driven Repayment Plans for Federal Student Loans

Concerns about administrative barriers to accessing IDR have become more acute as student debt has ballooned and its impact on borrowers has become more apparent. Prior studies and policy reports suggest that confusing terms, noncooperative loan servicers, and onerous documentation requirements present frequent barriers to enrolling and remaining enrolled (Consumer Financial Protection Bureau 2015; Frotman and Gibbs 2017; Baum and Chingos 2017; Mueller and Yanellis 2019; Conkling and Gibbs 2019). According to a policy brief by the legal education advocacy group AccessLex (2021), “the . . . consensus among nearly all stakeholders is that IDR has, unfortunately, over time, evolved into a web of cryptic and opaque options that leave too many student borrowers behind.”

Although enrollment in IDR increased from less than one million prior to 2010 to nearly ten million in recent years (Karamcheva, Perry, and Yannelis 2020), around 50 percent of borrowers with low incomes and large loan balances still do not enroll. Thomas Conkling and Christa Gibbs (2019) report that every year, approximately 15 percent of enrolled borrowers fail to successfully reenroll within two months of annual plan expiration and end up either in forbearance or default, suggesting that the drop-out from IDR was not purposeful. Nongraduates who may be in the greatest need are more prone to fall through the cracks (Frotman and Gibbs 2017). Beyond this information, however, we have limited knowledge about patterns of IDR participation (Collier, Fitzpatrick, and Marsicano 2022). Even less is known about patterns of underenrollment among highly payment-burdened borrowers who would benefit from IDR but are not participating.

FEDERAL STUDENT LOAN SERVICING

An important feature of the federal student loan policy is that private servicers are the conduits through which borrowers access federal relief programs for federal loans. Although 92 percent of outstanding student loans are held and governed by the Department of Education, the federal government does not directly collect payments or interact with borrowers. Instead, loans are allocated to contracted servicing organizations, which are responsible for customer service and communication, payment collection, and—crucially—guiding and processing borrower enrollment in the various federal repayment programs. This means that administrative burdens in federal IDR programs must be understood in the organizational context of the contracted-out consumer creditor state (Quinn 2017). In this respect, federal student loan programs parallel federally backed mortgage and small business credit programs, many of which also rely on private firms as servicers and gatekeepers.

Until 2009, only one servicer for federal direct loans (ACS) was in operation.1 However, with the winding down of the FEFL program in 2008 and the massive expansion of federal direct loan holding following the 2010 Student Aid and Fiscal Responsibility Act, the Department of Education began contracting with a stable of multiple for-profit and nonprofit servicers. During our study period up to eight of these were in operation, including four for-profits and four smaller nonprofits. With few exceptions, borrowers cannot choose which servicer their loans are assigned (for background, see Postsecondary National Policy Institute 2019).

The Office of Federal Student Aid (FSA) oversees awarding and monitoring of servicing contracts. However, FSA has little direct oversight over servicing operations. Instead, incentives are managed using performance-based criteria. These criteria are incorporated into fee rate schedules and also used to determine servicers’ future loan allocations. Servicers are paid a monthly fee for all nondefaulted loans and a higher amount for performing loans, which includes loans in IDR ($2.85 per loan-month). Lesser amounts are paid for loans that are delinquent or in forbearance. Performance assessments are used to allocate future loans across servicers, giving them an incentive to meet criteria. The most important of these is loan default avoidance and delinquency avoidance, though other criteria include borrowers satisfaction surveys and FSA manager surveys of perceived servicer performance.

Servicers are responsible for enrolling borrowers in IDR following a request (typically via phone), and subsequent submission of application and income certification forms. In theory, compensation incentives and performance-based loan allocation criteria in federal servicing contracts should give servicers an incentive to ensure that struggling borrowers are able to access IDR programs in order to heighten their chances of remaining current and in repayment, rather than steering them into forbearance or allowing them to lapse into delinquency (see Darolia and Sullivan 2020). However, both government and private watchdog reports have consistently documented widespread servicer failures with respect to federal loan repayment programs, despite recurrent tweaks to the servicing contracts, and termination of some servicers (see Consumer Financial Protection Bureau 2015; GAO 2016; Student Borrower Protection Center and American Federation of Teachers 2020). As we document in the next section, borrowers experienced a litany of servicer-borne barriers to IDR enrollment across the study period.

ADMINISTRATIVE BURDEN AND SOCIAL STRATIFICATION

Administrative burdens represent the flipside of street-level bureaucracy from the perspective of recipients and claimants (Peeters 2019). Here the issue is how the informational requirements and bureaucratic procedures surrounding public programs can undermine equitable access to citizens by creating various hoops through which claimants must jump. Such burdens can arise intentionally as a rationing tactic on the part of either policymakers (Herd and Moynihan 2018) or street-level bureaucrats. Burdens also often emerge as unintentional consequences of policy design or organizational constraints. We adopt a broad conceptualization of burdens to include all formal programmatic rules, organizational hassles, and interactional stresses and miscommunications that borrowers experience in managing their loan repayment obligations and accessing available programs.

Research on administrative burdens has tended to focus on particular recipient-facing requirements or program elements, which can be classified in terms of learning costs, compliance costs, and psychological costs (Moynihan, Herd, and Harvey 2015). Examples include cognitive and informational barriers that make it difficult for claimants to learn about the availability of programs; complicated paperwork submissions and obtrusive documentation requirements that make enrollment more difficult; frequent recertification requirements with strict deadlines; and time and effort expended due to long wait times, understaffed agencies, and poor client services (Schanzenbach 2009; Soss, Fording, and Schram 2011; Bhargava and Manoli 2015; Mueller and Yanellis 2019; Pearl 2021). As we show, all of these elements are relevant in the IDR case.

Two additional features of the present case merit particular theoretical and empirical attention. First is that IDR is an amalgam of programs. Four types of income-pegged repayment programs were available during the study period, each with slightly varying provisions and eligibility. This patchwork of options adds to IDR’s complexity (Baum and Chingos 2017) and may thereby generate added learning costs, choice overload, and miscommunication between borrowers and servicing representatives. Second is the role of organizational fractures and perverse organizational incentives generated by a privatized servicing system (Wu and Meyer 2021). Organizational failures on the part of servicers such as lost documentation and misprocessing of forms may compound the effects of formal programmatic burdens, leading to problems that require redress and thus overcoming a secondary layer of burdens to rectify the initial error.

BURDENS AND STRATIFIED ACCESS TO PUBLIC PROGRAMS

The second goal of this article is to estimate the resulting effects of the high-burden servicing system on disparities in borrowers’ access to IDR. It is widely believed that administrative burdens tend to exacerbate inequality within a given population of potential recipients or claimants. As Julian Christensen and his colleagues (2020) point out, burdens create a Catch-22 insofar as the subpopulations most acutely in need programs are typically the least well equipped to navigate bureaucratic hoops (Cherlin et al. 2002; Greene et al. 2006), and hence face the greatest challenges in actually accessing programs. Administrative burdens will operate as a stratifying mechanism of exclusion insofar as they strengthen the association between sociocultural resources or status and program access.

We test this hypothesis in the context of student loan repayment by estimating socioeconomic and racial differences in take-up of IDR among those with high-debt payment burdens, who would presumably benefit from being IDR over a standard repayment plan. We argue that accumulated deficits of social- and cultural-capital resources among lower-SES and marginalized racial minority borrowers will leave them less well equipped to navigate the multifaceted knot of informational and administrative barriers. By contrast, higher-status actors will be better equipped to learn about IDR, navigate the documentation requirements, and make claims on servicer representatives. The high-burden process to enroll in IDR will thereby disproportionately limit access to payment relief programs for borrowers in more marginalized positions (Ray, Herd, and Moynihan 2022), even though they are often the borrowers most in need of payment relief.

Research using small samples from the Survey of Consumer Finances (SCF) offers suggestive evidence that IDR enrollment is indeed lower on average among low-income than middle-income borrowers, and lower among higher debt-to-income borrowers than among lower (Collier, Fitzpatrick, and Marsicano 2020). However, the SCF samples are too small to assess variation in enrollment by borrower traits among borrowers with high loan payment burdens. Meanwhile, Conkling and Gibbs (2019) use the CFPB’s large-N consumer credit panel to provide a detailed description of the characteristics and experiences of IDR-enrolled loans. Their analysis, however, does not include indicators of borrowers’ socioeconomic status. Finally, using Department of Education administrative data and imputed lifetime incomes, Nadua Karamcheva, Jeffrey Perry, and Constantine Yannelis (2020) report that take-up of IDR, which they define as ever being enrolled in IDR at any time, is greater among both lower-income and high-debt borrowers across the full population of borrowers. However, their analysis does not assess how participation rates vary by socioeconomic status or race among borrowers with high debt-payment-to-income ratios.

We consider this to be the key study population for assessing the extent to which high administrative burdens disparately impede program access, because this is the subset of borrowers for whom the financial benefits of participating in IDR are least ambiguous. In other words, our analysis shifts the focus away from the question of who participates in the IDR program to ask instead who participates among those who would benefit from participating.

We expect that those highly indebted federal loan borrowers in more marginal positions, indexed by income and race, will show lower rates of enrollment.

METHODS AND RESEARCH DESIGN

We use a mixed-method research design. The qualitative portion of the analysis describes obstacles that borrowers encounter as they traverse the organizational and programmatic terrain of federal loan repayment, with a particular focus on those that bear on repayment program enrollment. The quantitative analysis then tests the extent to which these barriers jointly produce social stratification in program participation.

QUALITATIVE DATA AND METHODS

The qualitative analysis draws on publicly available, full-text consumer complaint data from the Consumer Financial Protection Bureau. The growth of complaint databases worldwide has led to various efforts to leverage these data sources for both social scientific and regulatory policy purposes (OECD 2020). Although very little work has used consumer complaint data specifically to study administrative burdens, these data offer a large-scale source of information regarding the obstacles that federal student loan borrowers face in managing repayment. Although CFPB complainants necessarily represent a selective subpopulation of borrowers, given that filing a report is itself a form of claims-making, the content of the accounts allows us to understand in greater detail the range of hassles, negotiations, misunderstandings, and administrative disjuncts from which access-limiting administrative burdens tend to arise.2

The relevant population of complaints covers all servicing and repayment-related claims regarding federal students loans from July 2013 through February 2020, coinciding with the onset of the COVID-19 pandemic in the United States. Specifically, the complaint pool is defined by restricting the universe of all CFPB complaints to those self-classified by complainants via screening questions as meeting two categorical criteria. The first of these is related to federal student loans: subproduct type is loan or loan debt or loan servicing. The second is related to problems repaying student loan debts or problems with loan servicers, as opposed to problems getting a loan or ancillary problems with credit reports such as identity theft: issue type is a problem with paying debt or problem with a loan servicer or incorrect information or false statements.

These restrictions yielded a total of 15,512 complaints. We then selected an analytic subsample of 1,187 complaints for detailed qualitative coding based on calendar days of the month, of which 505 included a narrative description. This narrative field is our main source of textual data.3

We use a coding scheme (see appendix) to describe the administrative burdens reported in the text field along several dimensions. This coding was developed with the aim of understanding borrowers’ administrative challenges with loan repayment in general, not solely with respect to IDR. Although the built-in complaint type categories are useful for screening purposes and to understand how borrowers themselves classify issues, they are analytically limiting because many repayment problems are more multifaced than the CFPB’s exclusive issue categories can convey. Based on a recoded sample of 1,200 student loan servicing complaints, Jason Delisle and Lexi West (2019) claim that only 44 percent of ostensibly service-related complaints invoke a problem that is purely within the control of the servicer. Their results highlight the cross-cutting nature of burdens that often implicate both programmatic features and poor performance by administering organizations.

Capturing information about administrative burdens from the texts of consumer complaints carries certain methodological challenges. First, identifying administrative burdens from consumer complaint texts requires extracting information from documents collected for different purposes (Salganik 2016). The particular nature of complaint data means that the narrative description focuses on grievances. Although the complaint texts typically reference to certain types of burdens (such as those related to document processing errors or servicers’ failures to redress other problems), key background information about other types of burdens that precipitated the focal problem may be mentioned only in passing. Meanwhile, burdens that result from high informational costs and consequent borrower confusion about program requirements or loan terms might not be stated explicitly but must instead be inferred from the testimonial.

Second, relying on self-selected complaints to capture experienced burdens means that certain types of burdens will likely be underrepresented. Borrowers may be unfamiliar with terminology, lack programmatic awareness, or not have the organizational vantage to articulate the source of the problem. Understanding the bureaucratic categories through which to articulate claims is itself endogenous to the administrative burdens borrowers must overcome. We address this issue by coding the vague, or confused, or nonspecific complaints as their own substantive category rather than simply as sparse data cells. These are the people who are confused and do not know where to begin in terms of claims-making and resolving repayment problems.

Likewise, selectivity in terms of the types of borrowers who lodge complaints could potentially skew conclusions about the types of burdens that are most prevalent within a given institutional context. Using community-level ecological data for several large consumer complaint databases including CFPB, Devesh Raval (2020) shows that higher education, more urban, and more heavily Black-populated zip codes lodge complaints at a higher rate per capita. Notably, these elevated rates of complaints are especially pronounced in the CFPB relative to the Federal Trade Commission and Better Business Bureau databases, though the same racial pattern appears for complaints related specifically to financial services across all databases. Given that Black borrowers are known to face higher rates of default and challenges repaying federal student loans (Haughwout et al. 2019), Raval’s findings provide some reassurance that this group is reasonably well represented within the corpus of complaints.

Finally, one interpretive caveat is that we are relying on narratives from the complainant. We cannot verify the facticity of each complaint—only how the situation is perceived. Some of these depictions could likely be debated by servicers, and some might not withstand a forensic accounting. Nonetheless, they do provide a vantage to understand how borrowers experience burdens in the loan servicing system.

QUANTITATIVE DATA AND METHODS

Having shown pervasive burdens surrounding IDR, the quantitative analysis then estimates the resulting social stratification in participation rates. It is important to emphasize here that our design does not directly measure individual-level exposure to learning, compliance, or psychological costs. Instead, based on the qualitative analysis, we presume that these burdens are a ubiquitous feature of the IDR program. We then indirectly capture their joint impact on disparate program exclusion by analyzing associations between income-race and IDR enrollment within the subpopulation of debt-burdened borrowers who would hypothetically face a high payment-to-income ratio under a standard repayment plan.

We define high loan-payment-to-income burden as greater than 20 percent of total monthly income, a subgroup that corresponds almost exactly to the top four debt-to-income deciles of the federal borrower population. These are borrowers whom we can reasonably assume would stand to benefit from participating in an income-based repayment plan, which reduces the monthly payment to a more affordable 10 percent of discretionary income.

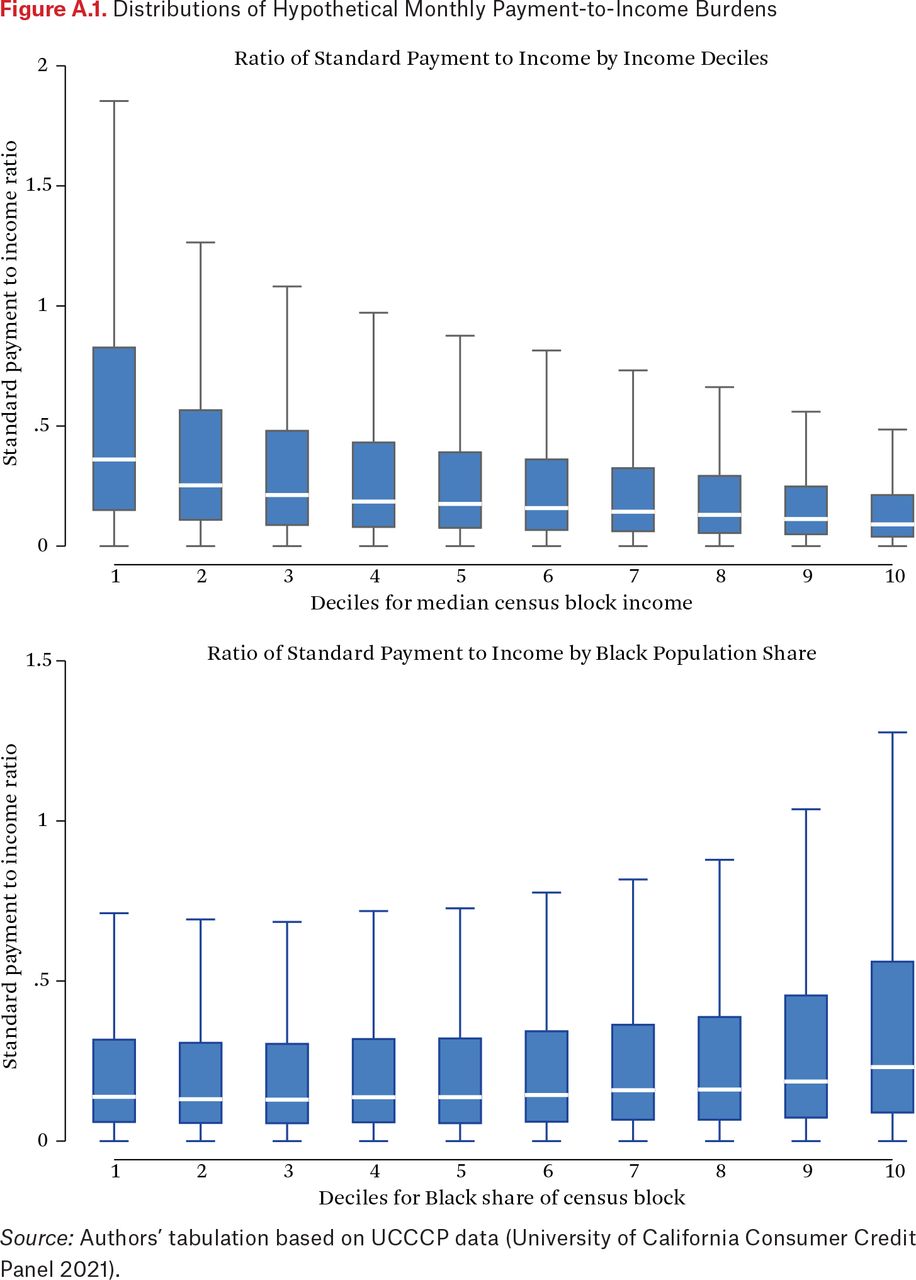

The logic of this approach rests on the fact that significant numbers of high payment-burdened borrowers exist across the income and race distributions (see figure A.1).4 This allows us to examine social stratification of program access within this highly debt-burdened population. This approach to defining the analytic sample population is necessarily assumption-laden insofar as we are presuming that borrowers with payments in excess of 20 percent of monthly income would be better off with lower monthly loan payments. However, we find substantively identical results when using more stringent cutoffs of 30 percent or 40 percent.

To maximize the robustness of our findings, our analysis draws on two separate restricted-use datasets. Each of these have mutually compensating strengths and limitations.

University of California Consumer Credit Panel Data

The first analysis draws on credit data from the University of California Consumer Credit Panel (UCCCP), which is based on a 1 percent national longitudinal sample of U.S. adults with credit records from 2004 to 2019. UCCCP reports tradeline-level (loan-level) records on a quarterly basis and includes the credit records of the household members of those sampled. The data originates from Experian, one of the three nationwide consumer reporting agencies.5 The UCCCP is similar to other consumer credit panels built by the Federal Reserve Bank of New York and the Consumer Financial Protection Bureau.

We follow an approach similar to that of Conkling and Gibbs (2019) in restricting the analytic sample to include only those student loans that are presumptively eligible for IDR enrollment. First, we removed all noneducation loans using the account type indicator. We then filtered nonfederal private loans and Parent Plus loans, neither of which are eligible for income-based repayment, by dropping any loans with cosigners or joint debtors using Equal Credit Opportunity Act fields. We also further filtered private loans by dropping loans for which the initial term duration is too short to be a federal loan. Finally, we drop loans that are in default, deferment, or otherwise not in repayment. Our analysis is confined to the period from 2010 to 2019 because we have that information on borrowers’ residential location. However, accrued debt from loans originated in earlier years are incorporated into the measures.

We treat a borrower as being enrolled in IDR in a given quarter if any of their eligible federal loans are in IDR. Because repayment plan status is not directly reported in the credit data, we identify IDR enrollment using the reported term duration for the loan. This figure should be set to 240 or 300 months for loans enrolled in the Repaye, Paye, income-based repayment (IBR), or IDR programs (Consumer Data Industry Association 2020), reflecting the longer repayment period for loans in these plans relative to those in the standard 120-month term. Because we suspect that some servicers fail to update the term duration field when borrowers enroll in IDR, we also recoded loans as being in IDR by using a simple amortization formula to identify those for which the scheduled monthly payment obligation is less than the amount that would be owed based on the loan balance, the remaining term period, and a conservative 3.4 percent interest rate.6

One downside of credit report data is the lack of direct household income measures. We proxy borrowers’ household income level by drawing on the UCCCP’s residential census block linkage. We applied census block-group medians, which we constructed by averaging across the 2015 and 2019 five-year ACS estimates. Census block groups are small subunits of tracts, typically comprising approximately a thousand persons. Proxying household status using census data on small area aggregates is a long-standing practice in fields such as health research. Although block-group medians are more precise proxies of actual household income than larger geographies such as zip codes or tracts, heterogeneity within block groups means that this procedure is still subject to a nontrivial degree of measurement error (Soobader et al. 2001; Moss et al. 2021). Such error will have an attenuating effect on our estimates of the association between borrower socioeconomic status and program participation, thereby rendering our hypothesis test conservatively biased against finding a relationship.7

Similarly, we use the proportion of Black residents in a census block group as a proxy for racial marginalization. Numerous studies have found that Black borrowers tend to experience significantly worse outcomes across most facets of student lending than other groups, making this a theoretically salient indicator of racial marginalization. Analyses based on this neighborhood racial composition metric should be interpreted cautiously, given the difficulties of predicting borrower categorical traits from credit report geolocations (Consumer Financial Protection Bureau 2015). Readers should also bear in mind that because Blacks are a racial minority, only those blocks groups in the top 24 percent of the Black distribution have majority Black populations.

We measure actual monthly payment burdens using the account payment amount field. We measure borrowers’ hypothetical monthly payment burden under a standard repayment plan using an amortization formula with an assumed interest rate corresponding to the rate for unsubsidized federal direct Stafford loans in the relevant vintage of origination.8 For loans with less than 120 months remaining, the standard payment calculation is based on the actual remaining loan term. For loans in IDR, the counterfactual standard calculation is based on a 120-month remaining term. In cases where borrowers have multiple federal student loans, actual and hypothetical monthly payment measures are aggregated to the borrower-quarter level.

Figure A.1 shows boxplots of the (counterfactual) distributions of monthly loan payment-to-income ratios under a standard repayment plan by population deciles of block-group median income, and deciles of block-group percentage Black residents. The graphs show that, among all federal loan borrowers, a greater relative share of those in lower-income and more heavily Black census blocks would face unaffordable monthly payments in the absence of income-based repayment. Crucially, however, at least some borrowers have high hypothetical monthly payment obligations across the income and race distributions. For the main analysis, we focus on the subsample of borrowers who would face a monthly loan payment-to-income ratio greater than 0.2 under a standard repayment plan, but we also find similar results using more restrictive cutoffs.

Beginning Postsecondary Students Longitudinal Study Data

We also supplemented the UCCCP analysis with a parallel analysis of a sample drawn from the Department of Education’s Beginning Postsecondary Students Longitudinal Study (Dudley et al. 2020). Whereas the UCCCP provides information on a large nationally representative sample of federal borrowers on a quarterly basis over a ten-year span, the BPS is limited to a single cross-sectional observation for a single cohort of students who exited college quite recently. The one advantage of the BPS survey over the UCCCP data is that we can measure income and race directly rather than with census-based proxies, which significantly reduces measurement error.

The BPS cohort is composed of a national sample of students who began college in 2011–12 and were interviewed again six years later. The BPS data also contain administratively linked loan-level data for each respondent from the National Students Loan Data System. As with UCCCP, we remove borrowers who were still enrolled or otherwise not in repayment circa 2018. As with the UCCCP, we model the association between income and participation in the BPS using rank deciles in order to avoid linearity assumptions. Here, however, the deciles are based on the 2017 income distribution among federal borrowers from the 2011–12 entering cohort, rather than the national distribution of all census block groups.

QUALITATIVE ANALYSIS OF CFPB COMPLAINTS

In this section, we describe the nature and prevalence of burdens that borrowers experienced in the course of managing their student loan repayments. Examples drawn from the qualitative data focus primarily, but not exclusively, on testimonials that explicitly highlight the relevance of the burden for impeding enrollment in IDR plans.

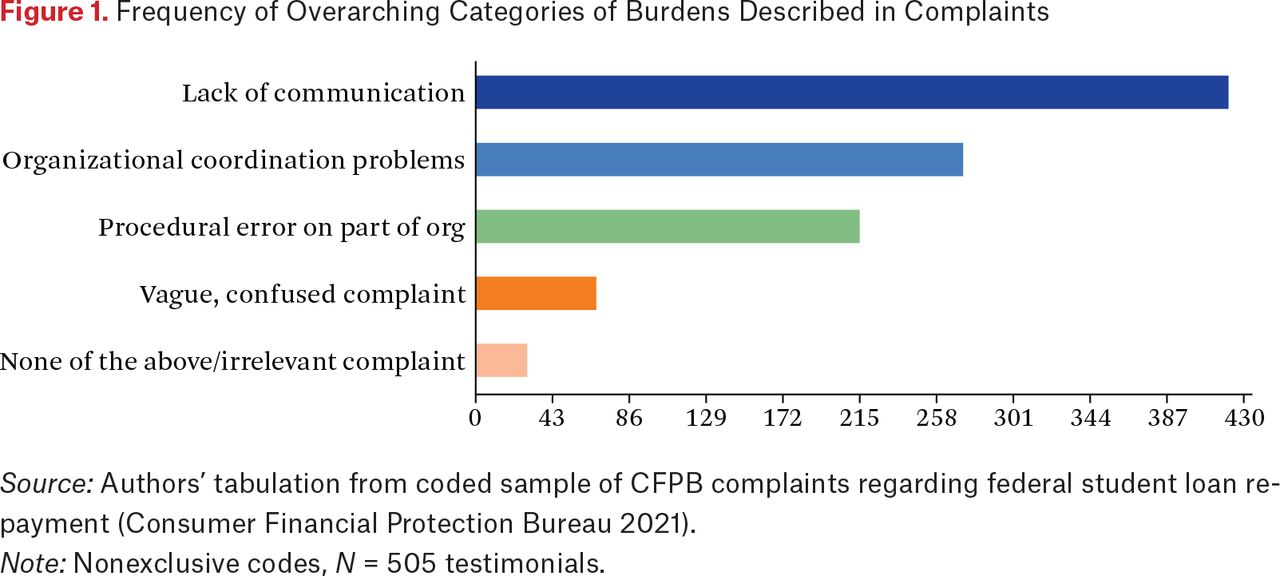

Figure 1 shows the overarching categories into which the coded complaints fall. The mean number of overarching burden types per complaint was 1.9. The most common source of reported burden involves miscommunication or noncommunication from servicers. The majority of all coded complaints indicate some sort of difficulty that arises from a communication failure. The next most prevalent types arise from organizational coordination failures and from servicer procedural errors. Although borrowers varied in their abilities to describe problems in the precise administrative jargon, relatively few complaints were simply vague missives or confused pleas.

Frequency of Overarching Categories of Burdens Described in Complaints

Source: Authors’ tabulation from coded sample of CFPB complaints regarding federal student loan repayment (Consumer Financial Protection Bureau 2021).

Note: Nonexclusive codes, N = 505 testimonials.

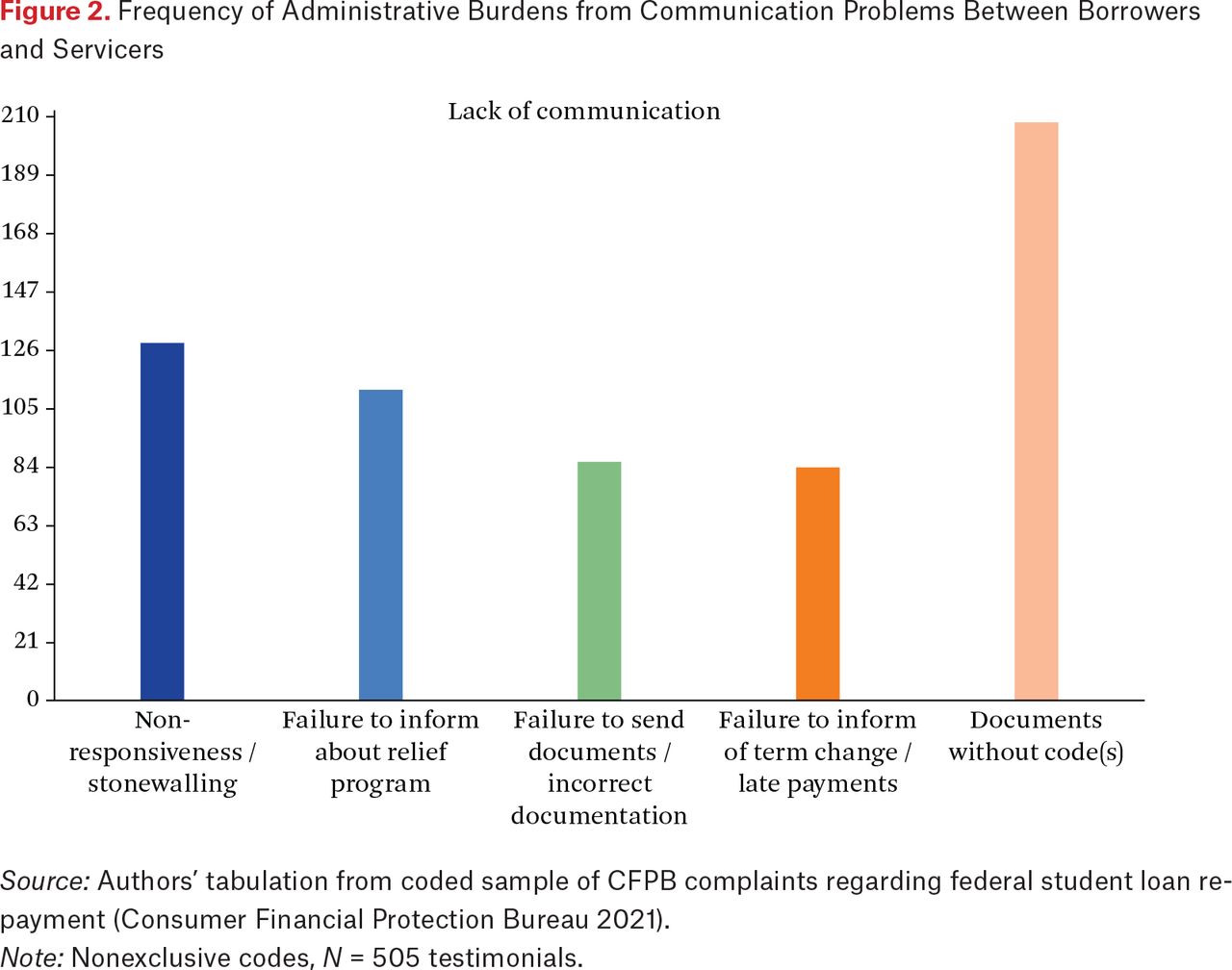

Figures 2 and 3 show the subtype breakdowns for communication failures and organizational failures, respectively. Communication problems between borrowers and servicers took several forms, each of which have some role or relevance in impeding borrowers’ access to IDR. As seen in figure 2, the most common subtype of communication problem was a perceived lack of responsiveness by servicers when borrowers sought information or assistance. Although servicer nonresponsiveness typically revolved around repayment problems not directly related to IDR, it did sometimes hinder IDR participation when borrowers sought confirmation from the servicer that their enrollment documents were in order, only to learn much later about a problem, costing the borrower several months of additional time in forbearance or making unaffordable payments.

Frequency of Administrative Burdens from Communication Problems Between Borrowers and Servicers

Source: Authors’ tabulation from coded sample of CFPB complaints regarding federal student loan repayment (Consumer Financial Protection Bureau 2021).

Note: Nonexclusive codes, N = 505 testimonials.

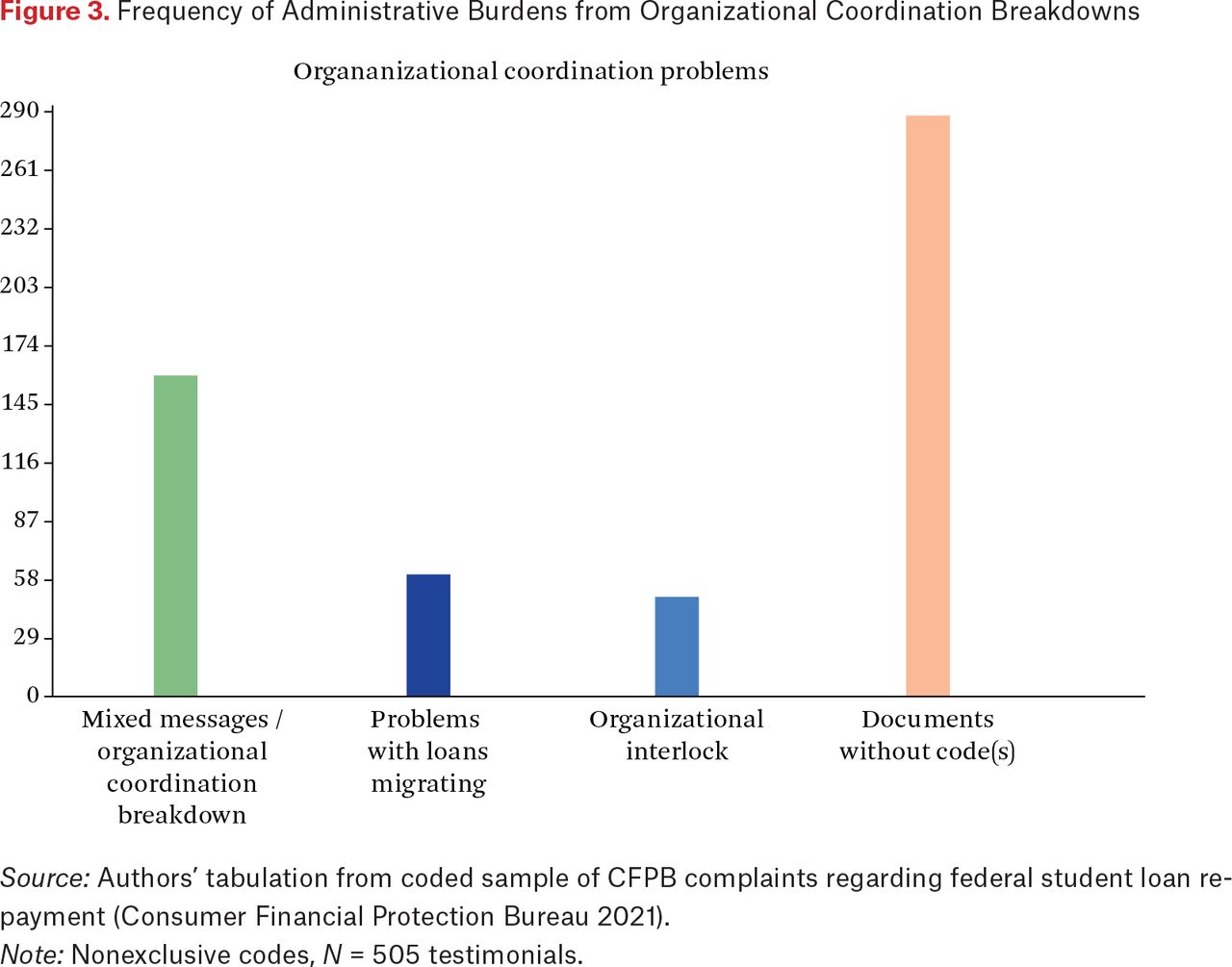

Frequency of Administrative Burdens from Organizational Coordination Breakdowns

Source: Authors’ tabulation from coded sample of CFPB complaints regarding federal student loan repayment (Consumer Financial Protection Bureau 2021).

Note: Nonexclusive codes, N = 505 testimonials.

More directly relevant are the second and third subtypes. Servicers’ failure to communicate IDR plans as an option was implicated in more than 20 percent of all the coded documents. In most of these cases, borrowers called to request a lower monthly payment amount, and were steered into interest-accruing forbearance instead of IDR. Forbearance-steering has been well documented and was the basis of a lawsuit by the CFPB and several state attorneys general against the loan servicer Navient (Lewis and Vanatko 2019). Given that servicers receive greater monthly fee revenue for loans in IDR than for those in forbearance, the forbearance-steering phenomenon more likely results from intraorganizational failures in which understaffed street-level bureaucrats in servicer organizations seek to avoid the more time-consuming processing of IDR enrollment. Either way, forbearance-steering effectively heightens the learning costs borrowers face. These cases typically appear in the complaint data ex post facto when frustrated borrowers later realize they would have been better off in an IDR plan. As one borrower bemoaned,

I sheepishly relinquished the ball to Navient and their predecessor Sallie Mae for more than sixteen years and as of today, my balance is nearly the same as it was on day one. If the executive leadership at Navient or their predecessor Sallie Mae had any ethics whatsoever, they would have informed me that an income-based repayment plan was my best option. This option was never discussed with me until all my deferments and forbearances had been exhausted! Why did you wait until 2018 when all my deferments and forbearances had been exhausted to tell me about the income-based repayment plan? Why did the company’s representative convince me that forbearance and deferments were my best option when in fact an income-based repayment plan would have resulted in my loans being paid in full more than five years ago? (emphasis added)

Even when borrowers are aware of IDR and explicitly request enrollment, additional communication breakdowns can arise that make it difficult for borrowers to acquire answers to questions or other necessary information.

I have been involved in a multimonth process for IDR to go in effect on both mine and my wife’s loan. I am required to take time off of work and go through a one-hour plus process waiting on call center representatives. Information is not consistent and already complicated processes are made more challenging by XXXX’s antiquated infrastructure. Their self serve options are nonexistent. They have no texting or mobile functionality I experience in every other financial services industry. Very simple notifications via text would have prevented 99 percent of my issues. As a citizen, I am troubled by the waste that confounds our already insurmountable student loan debt.

One particularly common communication-related complaint involves alleged failure by servicers to transmit the necessary paper forms to complete IDR enrollment or to inform borrowers of problems with previously submitted documents. Borrowers’ formal requests to enroll in IDR thus often fail to result in actual enrollment. For instance, one borrower complained how it was a bureaucratic struggle to acquire the paperwork needed to complete enrollment:

Since consolidating my loans I have had a lot of difficulty in obtaining an affordable monthly payment. I have called and been left on hold for long periods of time. I have also actually spoken with representatives that may give me options on the phone, place my loans in forbearance, and then claim I will receive documents in the mail to complete to finalize the lower payment based on my income. However, I never get the revised documents nor can I locate them on the website. This is factoring into my debt-to-income ratio and has prevented me from qualifying for new credit and also makes it appear I can not afford very much. Based on my current loan payment, which is well over [$1,000], I can not afford anything. I need help. (emphasis added)

Organizational coordination problems are the second most common generic category after communication problems (see figure 3). Within this category, the most prevalent subtype involves intraorganizational breakdowns between subunits. This typically occurs when servicer representatives take actions or dispense advice at cross-purposes with one another, or when a servicer representative’s actions in response to one issue have unintended consequences, generating further knock-on burdens that must be overcome to keep the loan in good standing.

Figure 3 also highlights the high frequency of burdens that arise from interorganizational breakdowns. Loan migration problems are instances when transfers of loan servicing responsibility between organizations, typically as a result of contract changes with the Department of Education, unexpectedly upset borrowers’ repayment arrangements. Loan transfers are often accompanied by system integration errors that cause borrowers to be erroneously unenrolled from repayment plans, and thereby exposing borrowers to an array of new burdens in order to reenrolled. One borrower explained how they were ultimately unable to retain their prior payment plan:

The problems began when my balance was transferred from my original lender, [Servicer 1], to [Servicer 2]: I was not provided notice of this transfer until after the fact, and two of my monthly payments went to the original lender, which was very difficult to get corrected. More important, once it came time to recertify for the IDR, which I was enrolled in through [Servicer 1], I encountered one issue after another with [Servicer 2]. The deadline had passed due to issues on [Servicer 2]’s end, being unable to process requests due to high volume at that time. When the recertification request finally was processed, it was denied; the reason stated on the website was that certain documentation was missing. I submitted the documentation and the request was denied again. In attempting to resolve these issues, I had multiple calls with [Servicer 2] reps, all of whom were unhelpful. My IDR request was finally “approved,” but with an increased monthly payment [from $86.00 to $320.00], even though my total household income and dependent information hadn’t changed. . . . According to [Servicer 2], because the initial payment amount of $86.00 was set up through [Servicer 1], [Servicer 2] has no record of the original IDR calculation and no way of obtaining it. This left me with no choice but to request forbearance for the maximum time period, which has now passed and left me with an absurdly increased monthly bill that I cannot afford.

Although our tabulations focus on univariate frequencies, the majority (66 percent) of complaint testimonials with any type of burden involved a convergence or layering of multiple distinct burdens. In some cases, the effects of multiple burdens appear additive in that borrowers overcome one burden only to be stymied by another. In other cases, the effects are multiplicative in that they compound upon one another. One borrower recounted an especially Kafka-esque instance. This example does not concern IDR enrollment directly but does illustrate the cascading effects of a single coordination error. In this case, a Navient representative’s instructions about how to cancel an accidental extra payment inadvertently activated a fraud prevention system (an intraorganizational coordination error), which in turn made it impossible for the borrower to make any future loan payments from her bank. The process of resolution confronted her with the additional burden of having to liaise between her bank and the servicer, which we refer to as organizational interlock, and follow up with additional phone calls after Navient failed to process the initial letter from the bank, that is, a procedural error. Altogether, the borrower had to make at least eight phone calls and secure multiple bank validation letters in order to resume repayment and remain in good standing. As she concluded in at the end of a long and exasperated complaint to the CFPB, “It should not be difficult to make a payment for your student loans when you want to make a payment!! And I’m supposed to deal with them for the next thirty-plus years???? Not to mention they put me into a very unnecessary ‘administrative forbearance’ without my permission, trying to get more money from me! . . . I have done everything that has been asked of me. I am trying to make timely payments and should be able to do so without having to jump through a thousand hoops each time.”

Although somewhat unusual in its convolutions, this example illustrates the common phenomenon whereby multiple burdens co-occur and compound. A borrower with less tenacity and bureaucratic capability would likely have found herself either in a longer period of interest-accruing forbearance, or credit-undermining delinquency. More broadly, the case also highlights the degree to which federal loan repayment policies not only impose a disciplinary regime on borrowers (but see Soss, Fording, and Schram 2011) but also de facto require borrowers to take on the additional burden of monitoring servicers and resolving servicer-induced errors.

IMPLICATIONS FOR ADMINISTRATIVE EXCLUSION FROM IDR

The administrative burdens tabulated illustrate both the range and frequency of learning, compliance, and psychological-hassle costs throughout the loan repayment process. As the complaint testimonials articulate, these costs can substantially impede borrowers’ access to repayment programs.9 Specifically, accessing and remaining in IDR requires overcoming impediments at three junctures: learning about the program and requesting enrollment; successfully submitting application and income documentation forms and following up in cases of errors or lost documentation; successfully recertifying one’s income each year. At each stage, borrowers face a risk of being overwhelmed by complex terms, having to parse inconsistent information from servicer representatives; having to grapple with frequent errors; and having to devote significant time to overcoming the forgoing burdens.

In some cases, the cumulative effect of burdens clearly serves to exclude borrowers from IDR altogether. As one typical complainant notes,

I have been trying for YEARS to get Fedloan servicing to set up a income-based repayment. . . . For some reason it is always stalled out, or can’t be processed, or needs more documents, or a signature is missing, even though I am doing everything they ask or tell me. I keep having to put my loans in forbearance which accrues interest and nothing is ever resolved. I have spent hours on the phone, I’ve tried the website, it just never works. This is the most ridiculous process I have ever seen. I am certain I am not the only person having this problem. Please help.

Yet even as burdens operate as mechanisms of exclusion for some, other borrowers are able to surmount obstacles with minimal harm beyond some time and inconvenience. As one borrower complained on noticing an erroneous change in her IDR payment amount,

payment is much lower than I’ve ever paid, but my family size and income have remained the same XXXX—called to make sure XXXX payment amount is correct ; account rep said my family size was incorrectly input as XXXX. Account rep says that it was probably an input error. . . . Now, I have to resubmit my XXXX application with correct family size (which is nothing, because it’s just me), even though it was their fault, and I had to figure it out. (emphasis added)

Such cases illustrate variability in borrowers’ abilities to overcome burdens. All borrowers face an administrative gauntlet in the federal loan servicing system, but some manage to navigate these situations in a relatively low-cost way. Meanwhile, others find themselves unable to access relief programs or to resolve initially small problems before they compound into significant financial harms. The analysis in the next section examines whether the combined effect of these burdens disproportionately impedes program participation as a function of socioeconomic status and race.

COMBINED EFFECTS OF ADMINISTRATIVE BURDENS ON STRATIFIED ACCESS TO REPAYMENT PLANS

Table 2 shows the UCCCP results from logistic models of IDR enrollment among borrowers in the top 40 percent of monthly payment-to-income burden under a standard plan. These are pooled sample models, with year-fixed effects and borrower-clustered standard errors.

Logistic Regression Estimates of Probability of Enrollment, UCCCP Sample

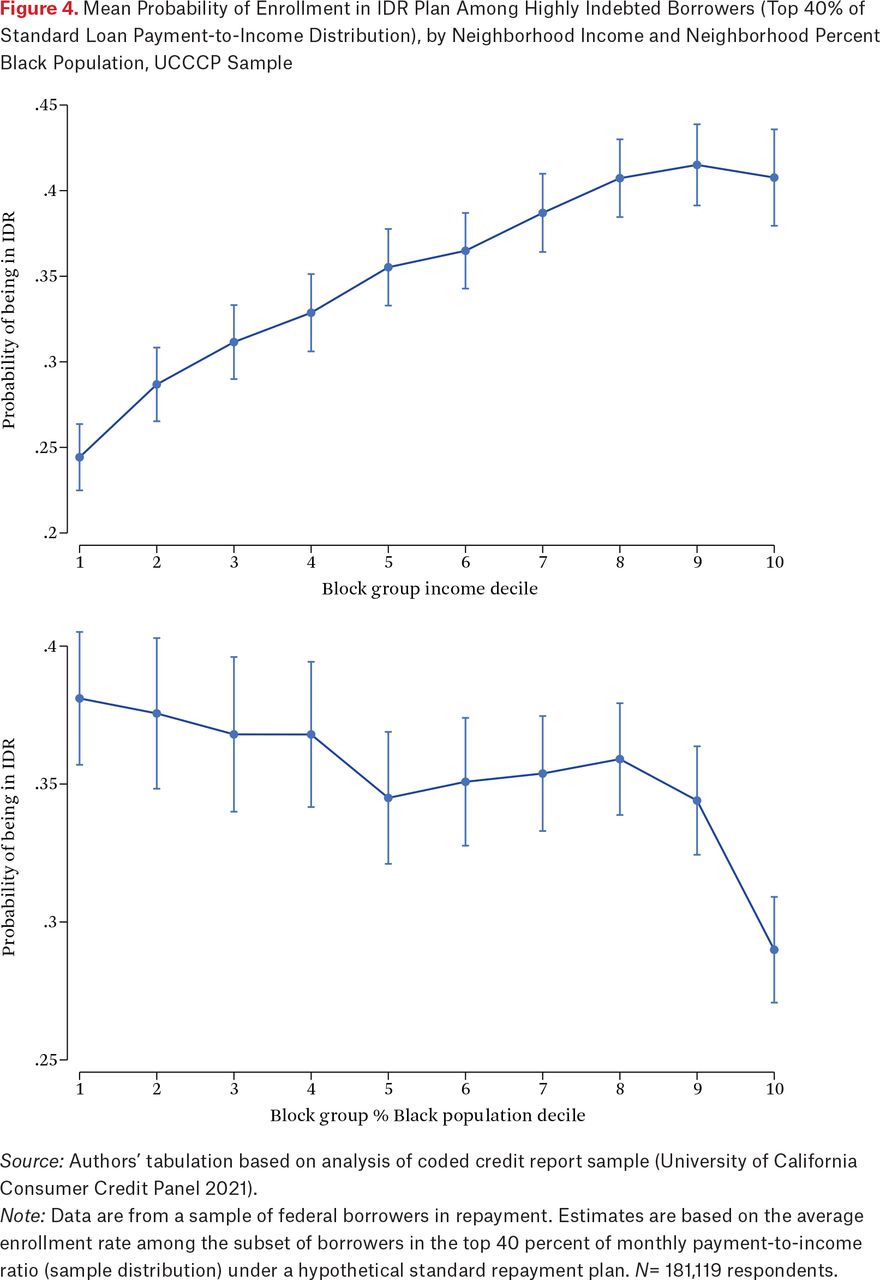

Consistent with these hypotheses, highly indebted borrowers residing in higher-income blocks are significantly more likely to be enrolled in IDR plans than those in lower-income blocks. The odds ratios in column one of table 2 indicate a positive, nearly linear relationship between income and the odds of being enrolled in IDR. For those in the top three income deciles, the odds of being enrolled are twice as great as for those in the bottom (baseline) income decile.

The top panel of figure 4 shows the estimated results from model 1, converted into estimated mean probabilities over the full sample period. In additional unreported specifications we further tracked the evolution of stratified take-up over time. These models show marked stability in the relative income differentials over the period from 2010 to 2020, even as overall participation in IDR increased.

Mean Probability of Enrollment in IDR Plan Among Highly Indebted Borrowers (Top 40% of Standard Loan Payment-to-Income Distribution), by Neighborhood Income and Neighborhood Percent Black Population, UCCCP Sample

Source: Authors’ tabulation based on analysis of coded credit report sample (University of California Consumer Credit Panel 2021).

Note: Data are from a sample of federal borrowers in repayment. Estimates are based on the average enrollment rate among the subset of borrowers in the top 40 percent of monthly payment-to-income ratio (sample distribution) under a hypothetical standard repayment plan. N= 181,119 respondents.

The results in table 2 also show evidence of a negative relationship between racial composition (percentage Black) and IDR participation. This relationship, however, is nonlinear. As seen in models 2 and 3, only within the top decile of percentage Black census block groups do high-debt borrowers show significantly reduced odds of being enrolled in IDR. As seen in model 2, those in the top decile have 34 percent lower odds of being enrolled in IDR than high-debt borrowers in the lowest percentage Black residential locations, although this estimate attenuates to an estimated 22 percent reduction in model 3. Notably, the persistence of both associations in model 3 suggests that the income and racial profiles of borrowers’ neighborhoods are each independently associated with the likelihood that borrowers can successfully surmount the obstacles to enrolling in IDR.

Table 3 shows the results from comparable specifications on the BPS data sample, which includes individual-level rather than census proxy measures of borrower income and race. These analyses confirm the strong positive relationship between borrower income and IDR take-up among highly indebted borrowers, the highest rates of take-up appearing in the upper-middle portions of the borrower income distribution. In fact, the income gradient in the BPS sample is much steeper, those in the eighth income decile exhibiting odds of IDR participation more than 3.8 times greater than in the bottom income decile. This larger differential likely reflects the effects of measurement error attenuation in the UCCCP, and also perhaps differences between the two sample populations.

Logistic Regression Estimates of Probability of Enrollment, BPS 12/17 Sample

The BPS analysis shows evidence of a significant relationship between race and IDR take-up. The point estimates for Blacks and Hispanics are positive relative to Whites, whereas those for Asians are negative in model 2 and model 3. The positive for Black borrowers in the BPS differs from the UCCCP results, which showed lower take-up among borrowers in high percentage Black block groups. These differing patterns across the two samples may reflect the limitations of the census-based racial proxy measure in the UCCCP, which would obscure systematic differences between those Black borrowers who live in high- versus low-percentage Black neighborhoods. The differing results could also reflect particularities of the younger cohort covered by the BPS sample.

Taken together, these results document clear evidence of social stratification in take-up of IDR among highly indebted borrowers. Disparities in access to repayment programs are structured primarily by borrowers’ socioeconomic status (indexed by income), such that highly indebted low-income borrowers are significantly less able to access these programs than highly indebted high-income borrowers. That this income differential is consistent across the two datasets make us more confident that the effect is real. By contrast, the relationship between racial marginalization and take-up of IDR is less clear cut and less consistent across the two data samples. We are thus unable to draw any firm conclusions about the degree of racial stratification in access to IDR.

DISCUSSION AND CONCLUSION

Income-driven repayment plans have developed as the primary policy mechanism to limit the costs of student loan payment burdens as more Americans face the individualized risks of debt-financed higher education. Whereas research has often conceptualized burdens as emerging as a result of targeting or rationing, the case of IDR highlights an instance in which universalist programs can also become mired in similar forms of “sludge” (Sunstein 2019). As our quantitative results show, this has pronounced distributional implications. Although a significant subset of borrowers across the social structure carry federal debt that would result in payments exceeding 20 percent of their monthly income under a standard repayment plan, high levels of learning, compliance, and psychological-hassle costs disproportionately suppress participation among those in lower socioeconomic positions.

A few limitations are important to emphasize. First, administrative burden is a broad category that can encompass a wide array of phenomena with respect to any given policy. This study focuses on describing the multiplicity of burdens that federal loan borrowers face as well as their combined effects on stratification in take-up. The downside of this design is that it is impossible to ascribe unequal administrative exclusion to any specific burden (Mueller and Yanellis 2019), or to parse their relative contributions to the total observed SES gaps. In other words, we cannot identify which of the numerous burdens observed in the present case—or which combinations of burdens—pack relatively greater punch as mechanisms of inequality. This remains a key issue for future research on policy domains where multiple forms of burden co-occur. Such work might focus in particular on unraveling the potentially additive or interactive effects of different types of burdens, as well as their potentially heterogenous effects across subpopulations. Such work might also seek to better distinguish burdens that arise from policy design, whether intentional or unintentional, and those that result from implementation failures.

A second limitation of the current analysis is its use of repeated snapshots. Future work might use panel analyses to capture social stratification across both take-up and drop-out (Wu and Meyer 2021). As this qualitative analysis and other quantitative analyses (Conkling and Gibbs 2019) suggest, remaining enrolled in IDR may be almost as difficult as accessing it in the first place. Because borrowers must confront recertification hassles anew every year, the inequality effects can be expected to cumulate over time.

Third, our analysis of inequality is limited to stratification in program participation. Future research on the effects of administrative burdens in this domain should trace the downstream consequences of disparate outcomes in the servicing system to other indicators of borrowers’ financial well-being. This can allow for an assessment of the degree to which administrative burdens contribute to the broader system of wealth stratification associated with student loan debts (Houle and Addo 2018).

BROADER IMPLICATIONS

Although this article’s primary focus is the consequences of high administrative burdens for social stratification of program access, our results also highlight two sources of administrative burden that have been less well studied. One is the privatization of street-level bureaucracies by outsourcing to private contractors. This is an increasingly common feature across numerous sites of policy delivery in the contracted U.S. social state (Soss, Fording, and Schram 2011; Weir and Schirmer 2018), but one whose implications for administrative burdens are only just now becoming a focus of study (Wu and Meyer 2021).

One key issue for future research on outsourcing and administrative burdens is to more systematically compare varieties of privatization across programs and jurisdictions. Studies should also try to disentangle how administrative burdens emerge from the interaction of public- and private-sector actors and organizations. In particular, to what extent do privatization-induced burdens reflect incentive misalignments, interorganizational coordination breakdowns, diffusion of responsibility, or simple managerial failures? To what extent do the street-level bureaucrats employed by servicing firms face their own administrative burdens and incentive misalignments? These issues are of great policy relevance as policymakers experiment with various reforms and proposed redesigns the of current loan servicing regimes. For instance, in 2021 the U.S. Department of Education announced new customer service accountability metrics that aim to make servicers more accountable to borrowers by incorporating additional customer satisfaction criteria into performance-based loan allocation formulas. However, research casts doubt on the utility of consumer satisfaction surveys as a way of disciplining providers (Young and Chen 2020). More fundamentally, it is unclear to what extent incentivizing servicers to tamp down on bureaucratically generated hassles costs will diminish social stratification in participation, absent a more fundamental program redesign that automates enrollment and diminishes the underlying compliance costs of participating.

This also points to a second, more intractable source of burdens in the IDR case, which is the tension between flexible, personalized, and adaptive policies on the one hand, and rigid, error-prone administrative systems on the other. IDR is intended to personalize debt payment to borrowers’ individual situations, and to do so dynamically in response to the reality that many Americans experience fluctuations in income. However, the complexity and frequent documentation that accompanies this adaptiveness—along with the multiplicity of program variations that create further choice burdens—together create confusion for borrowers and street-level bureaucrats alike. Policymakers need to be cognizant of how easily a policy that is intended to be responsive to everyone’s unique and changing circumstances can systematically undermine its own aims when implemented in practice.

APPENDIX. DESCRIPTION OF CODING SCHEME FOR QUALITATIVE ANALYSIS

CFPB complaints typically contain at least one of four elements, and frequently all four in combination: description of the problem, typically the focus of the complaint; mention of original precipitating problem if different from the focal problem; lack of resolution; consequential harms.

Sometimes complainants frame the original source of the problem as their own financial constraints (such as their inability to make payments on time), but frequently the problem is framed as organizational. Complaints usually go on to describe failed attempts to resolve the problem. Finally, most complaints give some indication of the harms, such as ruined credit score or inability to buy a house or harassing family members, but sometimes the harms are implicit.

CODING SCHEME FOR CLASSIFYING ADMINISTRATIVE BURDENS

Metacodes for presence of narrative elements (yes or no)

Description of focal problem

Mention of original precipitating problem, if different from focal or immediate problem

Efforts to resolve

Consequent harms

Metacodes for general types of underlying administrative complexity from which problems arise (nonexclusive)

Organizational coordination and bureaucratic problems with servicers

Problems with loans migrating between servicers

Inconsistent information from different customer service representatives

Failure of servicer to follow-through on promised actions

Steering borrowers to forbearance, lost paperwork

Policy complexity or patchwork problems

Multiple statuses or repayment programs

Confusion about forbearance versus IBR confusion about the necessity of being enrolled in IDR plan for Public Service Loan Forgiveness payments to count toward 120

Different terms and programs for different loans

Confusion arises because borrower has multiple loans, some of which do not qualify for certain repayment programs

Borrower thinks they are enrolled in X program but are for only a subset of loans

Problems that arise from the instability of borrowers’ lives in the face of bureaucratic rigidity

Change in borrower’s employment or life circumstances that alters program eligibility, upsets prior repayment arrangements, or leads to inexplicable or surprise increase in payment obligations such as job loss or health problems, divorce, marriage

Residential instability or change of address leads to missed correspondence

Falling into delinquency because of the time lag between income loss and adjustment to payment obligation for those already enrolled in IDR/IBR

Specific codes (nonexclusive)

Problems with loans migrating

Information is lost or who is accountable is unclear

Mixed messages or organizational coordination breakdowns

One person says one thing, a department does something else

One representative says something but something else happens

Website says one thing, representative says another

One arm of organization makes error, representatives say they cannot help

Organizational interlock

Credit bureaus only respond to reporting organization

Lack of communication, documentation, or opacity in communication

Lost proof of payments

Lost documentation or income forms

No documentation on changed terms of payment

Refusal to send documentation

Generally unresponsive when trying to resolve the problem

Borrower cannot get clear information on the types or terms of programs they are enrolled in

Procedural error on the part of the organization

Charged in excess

False reporting of debt

Misapplied payments

Payments accepted but still marked unpaid

Payments infrastructure not working, people end up with late or missing payments that are not their fault

Terms of repayment change unilaterally

Borrower inexplicably unenrolled from payment plan

Organization claims debtor agreed to change terms of payment

Debtor does not remember agreeing to terms

Organization claims agreement made by telephone but has no documentation

Servicers fails to inform borrower of payment relief programs when borrower complains of inability to pay (possibly not explicit in complaint)

Steering borrowers into forbearance rather than IDR/IBR

Failing to convey relief programs as option when borrowers complain about inability to pay balance

Processing repayment program enrollment request incorrectly or not crediting payments toward forgiveness threshold, such as payments not applied toward public service loan forgiveness despite borrower being ostensibly enrolled in program

Complaints about lack of information from college regarding repayment and loan terms

Vague, confused, or nonspecific complaints

Metacategory of cases where burden arises from borrowers not knowing about loan terms or bureaucratic categories and thus being unable to begin a claim

None of the above, that is, complaint is specific but outside scope of repayment-related administrative burden, such as solely about college being a rip-off

Harms

Hassle costs

Borrower complains of time trying to resolve problems

Mention of repeated efforts or phone calls

Additional accrued balance, capitalized interest

Loan deemed in default

Damaged credit score or report

Suspected financial irresponsibility

Inability to take out a loan

Poor credit score for seven years

Claims of added stress, mental health toll from administrative burdens

Distributions of Hypothetical Monthly Payment-to-Income Burdens

Source: Authors’ tabulation based on UCCCP data (University of California Consumer Credit Panel 2021).

FOOTNOTES

↵1. Before 2010, federally backed student loans were lent both directly and through private lenders (FEFL loans) with a federal guarantee. Both were governed by the same rules, but individual lenders serviced the FEFL loans. After 2010, all new federal loans were direct loans and private organizations were involved only as servicers.

↵2. The vast majority of complaints in the overall CFPB corpus are not about federal student loan serving. In fact, when adjusted for the relative shares of the population holding each type of debt holding the rate of complaints regarding federal student loan servicing is lower than that for mortgage loans, and only slightly higher than for auto loans.

↵3. After classifying their complaint using predefined menu choices, CFPB complainants are asked to describe, in a short narrative field, the nature of problem.

↵4. Our main analysis defines high loan-payment burdened borrowers as those who would be in the top 40 percent of monthly payment-to-income ratio under a standard repayment plan.

↵5. Before being provided to the UCCCP, records were stripped of any information that might reveal consumers’ identities, such as names, addresses, and Social Security numbers.

↵6. We use 3.4 percent because it is the lowest interest rate for any type of subsidized or unsubsidized federal student loan from any vintage prior to 2020.

↵7. Substantively identical results are obtained when using state-normalized block-group income deciles.

↵8. Fixed interest rates for federal loans differ by vintage of origination, and also by lending program. Unsubsidized rates for direct undergraduate loans ranged from 3.8 to 6.8 percent between 2006 and 2020.

↵9. More than 49 percent of all coded complaints concern issues related to IDR.

- © 2023 Russell Sage Foundation. Goldstein, Adam, Charlie Eaton, Amber Villalobos, Parijat Chakrabarti, Jeremy Cohen, and Katie Donnelly. 2023. “Administrative Burden in Federal Student Loan Repayment, and Socially Stratified Access to Income-Driven Repayment Plans.” RSF: The Russell Sage Foundation Journal of the Social Sciences 9(4): 86–111. DOI: 10.7758/RSF.2023.9.4.04. Direct correspondence to: Adam Goldstein, at amg5{at}princeton.edu, Princeton University, Dept. of Sociology, 114 Wallace Hall, Princeton, NJ 08540, United States; Charlie Eaton, at ceaton2{at}ucmerced.edu, University of California Merced, Dept. of Sociology, 5200 North Lake Rd. Merced, CA 95343, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

- Article

- Abstract

- FEDERAL STUDENT LOAN SERVICING AND REPAYMENT PROGRAMS

- FEDERAL STUDENT LOAN SERVICING

- ADMINISTRATIVE BURDEN AND SOCIAL STRATIFICATION

- BURDENS AND STRATIFIED ACCESS TO PUBLIC PROGRAMS

- METHODS AND RESEARCH DESIGN

- QUALITATIVE DATA AND METHODS

- QUANTITATIVE DATA AND METHODS

- QUALITATIVE ANALYSIS OF CFPB COMPLAINTS

- IMPLICATIONS FOR ADMINISTRATIVE EXCLUSION FROM IDR

- COMBINED EFFECTS OF ADMINISTRATIVE BURDENS ON STRATIFIED ACCESS TO REPAYMENT PLANS

- DISCUSSION AND CONCLUSION

- BROADER IMPLICATIONS

- APPENDIX. DESCRIPTION OF CODING SCHEME FOR QUALITATIVE ANALYSIS

- FOOTNOTES

- REFERENCES

- Figures & Data

- Info & Metrics

- References

Related Articles

Cited By...

- No citing articles found.