Abstract

The COVID-19 pandemic and resulting economic crisis exposed the U.S. rental housing market to extraordinary stress. Policymakers at the federal, state, and local levels established eviction moratoria and a number of additional direct and indirect renter-supportive measures in a bid to prevent a surge in evictions and associated public health risks. This article assesses the net efficacy of these interventions, analyzing changes in eviction filing patterns in 2020–2021 in thirty-one cities across the country. We find that eviction filings were dramatically reduced over this period. The largest reductions were in places that previously experienced highest eviction filing rates, particularly majority-Black and low-income neighborhoods. Although these changes did not ameliorate racial, gender, and income inequalities in relative risk of eviction, they did significantly reduce rates across the board, resulting in especially large absolute gains in previously high-risk communities.

The COVID-19 pandemic precipitated an economic collapse that threatened to spiral into a housing crisis, particularly among renters. Job losses in the early weeks of the pandemic were concentrated in industries and occupations—particularly in the retail, service, and tourism sectors—that disproportionately employ renters (Kneebone and Murray 2020). Because few jobs were available and savings with which to weather unemployment were limited (Pew Charitable Trusts 2018), these tenants were at imminent risk of eviction if they could not meet the next month’s rent. Evictions in turn raised the prospect of more households ending up homeless or doubled-up with friends or relatives, conditions that foster the spread of COVID-19. In responding to the unfolding economic emergency, policymakers at the federal, state, and local levels enacted a range of policies that offered income support and reduced housing instability. These included general benefits such as economic impact payments (EIPs) and expanded unemployment insurance (UI) as well as measures targeted at preventing evictions, most notably federal and state eviction moratoria and emergency rental assistance (ERA).

In this article we assess the cumulative effects of these policies, analyzing changes in eviction filing patterns over the first two years of the COVID-19 pandemic in thirty-one cities across the United States. We address four primary questions. First, did these policies prevent an increase in eviction cases? Second, were these cumulative effects felt equally across cities? Third, who benefited most from these policies? We describe the populations that saw most dramatic changes in eviction risk since the start of the pandemic, show where gains accrued, and assess how existing inequalities in rental housing precarity changed. Finally, fourth, which policies had most pronounced effects? Although we cannot estimate the effects of each policy separately given their temporal co-occurrence, we leverage variation in the timing of state and local eviction moratoria to estimate the effects of these measures in reducing eviction risk.

To answer these questions, we use administrative data on case filings collected through the Eviction Tracking System (ETS), a tool we developed in response to the pandemic (Hepburn, Louis, and Desmond 2020a). We find that eviction filings were dramatically reduced between March 15, 2020, and December 31, 2021: some 57.6 percent fewer eviction cases than normal were filed over this period. The largest reductions were in places that previously had the highest eviction filing rates, particularly majority-Black and low-income neighborhoods. Although these changes did not eliminate racial, gender, and income inequalities in the relative risk of eviction exposure, they did significantly reduce rates across the board, resulting in especially large absolute gains in previously high-risk communities. We find that eviction moratoria, particularly those that halted the earliest stages of the eviction process, resulted in significant and durable reductions in eviction filing rates.

Our findings highlight both the potential and the limitations of public policies aimed at reducing the prevalence of eviction. We show that an unprecedented combination of income supports, restrictions to the eviction process, and direct payments of rental arrearages to landlords resulted in a significant reduction in eviction caseloads for a prolonged period. This effect appears to have been achieved without fundamentally undermining the financial stability of landlords overall (ATTOM 2021; Choi, Pang, and Goodman 2022; Greig, Zhao, and Lefevre 2021). The full cost of these prevented eviction cases remains unclear, however, and variations in the efficacy of policies across jurisdictions are a reminder of the challenges that arise when attempting to reform established regulatory frameworks, especially in states with a history of pro-business landlord-tenant policies (Hatch 2017).

EXTRAORDINARY REACTIONS TO A MOMENT OF CRISIS

In response to the COVID-19 pandemic, the federal government established a range of policies that supported renters and, directly or indirectly, may have helped reduce the number of eviction cases filed during the pandemic. Many of these policies were not specifically developed to prevent evictions. For instance, although not framed as anti-eviction measures, EIPs and temporary expansion of both UI and the Child Tax Credit significantly improved household finances during the pandemic. These measures lifted millions of households out of poverty (Parolin et al. 2021), and likely helped keep rent paid for many families.

Policymakers pursued two sets of policies that were directly targeted at reducing eviction filing rates: eviction moratoria and ERA. The federal government established two eviction moratoria in the first year of the pandemic. The first, which Congress enacted in the CARES Act, restricted eviction filings between March 27 and August 23, 2020, from buildings that were financed, insured, subsidized, guaranteed, or otherwise supported by the federal government.1 Determining building-level eligibility under this policy proved complicated (Ernsthausen, Simani, and Shaw 2020); the best estimates suggest that between 28.1 and 45.6 percent of all rental housing was covered (Stein and Sutaria 2020). The second moratorium, established by the Centers for Disease Control and Prevention (CDC) on September 4, 2020, limited evictions when tenants provided a declaration attesting that they qualified for protections. The order was initially set to expire on December 31, 2020, but was repeatedly extended. The Supreme Court found the order unconstitutional and struck it down on August 26, 2021. In addition to these federal measures, forty-three states and the District of Columbia established their own eviction moratoria in the early weeks of the pandemic, as did a number of county and municipal governments.2 The vast majority of these orders were rescinded or allowed to expire by late summer of 2020 (Benfer et al. 2022). Neither federal nor any state eviction moratoria unilaterally halted all eviction cases, but in most cases the policies afforded protections to the majority of renters.

Recognizing that eviction moratoria delayed but did not remove rent obligations, Congress implemented a large-scale ERA program to repay rental arrears that accrued due to pandemic-related hardship. Between the Consolidated Appropriations Act of 2021 (December 2020) and the American Rescue Plan (March 2021), Congress appropriated $46.6 billion in ERA funds. These funds were distributed to more than four hundred state, county, local, and tribal grantees throughout the country; they, in turn, developed application and payment processes (Yae et al. 2020). The earliest ERA payments to landlords were made in the first quarter of 2021, distribution increasing rapidly as the year progressed. By the end of 2021, 3.8 million households had received assistance and the Treasury Department reported that between $25 and $30 billion was either spent or allocated (U.S. Department of the Treasury 2022).

This article explores the net efficacy of these interventions. Taken jointly, were eviction moratoria, ERA, and other policies enacted in response to the pandemic successful in reducing eviction filings? Were reductions in eviction filings evenly distributed across cities and, if not, what inequalities emerged between jurisdictions? If these policies worked, which neighborhoods and which renters saw largest reductions in filings?

We are particularly interested in analyzing what, if anything, these measures did to ameliorate socioeconomic, racial-ethnic, and gender disparities in eviction risk that predated COVID-19 (Hepburn, Louis, and Desmond 2020b; Desmond and Gershenson 2017). Many of the policies enacted to address the pandemic, including most eviction moratoria, offered universal or near-universal benefits.3 Universalistic policies, however, do not necessarily result in a progressive distribution of benefits and indeed are often more regressive than targeted or means-tested programs (Hoynes and Rothstein 2019). For example, research on clean energy tax credits finds that the top income quintile receives 60 percent of the benefits from the program relative to only 10 percent in the bottom three quintiles (Borenstein and Davis 2016). The pandemic presents a test case for understanding the effects of a much broader set of universalistic policies on existing inequalities across a range of domains (see Bitler, Hoynes, and Schanzenbach 2023, this issue; Bell et al. 2023, this issue). In the case of housing instability, did these policies help to close gaps in eviction risk between groups, leave them unchanged, or widen them?

Disentangling the relative effects of these various policies is also critical, both in understanding what transpired during the pandemic and for future policymaking. Could we have achieved a significant reduction in eviction filing rates through income supports alone or were eviction moratoria necessary? How many eviction cases were avoided as a function of rental assistance and at what cost? As a function of policy co-occurrence and limited data availability, we are unable to address all of these questions or assess the relative contribution of each pandemic-era program, but we do offer multiple tests of the causal effects of strong state and local eviction moratoria in reducing filings.

DATA AND METHODS

We draw on the records of eviction case filings collected through the ETS (Hepburn, Louis, and Desmond 2020a), a tool we built to better understand real-time trends in eviction filings. The ETS relies primarily on web-scraping techniques to monitor the filing of new eviction cases in a set of jurisdictions across the country. It allows us to observe case numbers, filing dates, plaintiff and defendant names, and addresses associated with eviction filings.4 We clean the data, removing duplicate cases and filings against commercial defendants, geocode addresses, and associate them with census tracts. Using these data, we produce counts of new eviction cases that feed into the ETS website, where we make aggregate data publicly available for download.

The ETS currently collects data from thirty-six court systems: six at the state level (covering 338 counties or county-equivalents), twenty-seven at the county level, and three at the municipal level. This is a purposive sample of court systems that met two inclusion criteria.5 First, the court must make the necessary data available. In most sites these data were collected from public court websites, though in several jurisdictions the courts share data directly (such as Maricopa County, Arizona). Second, in each site we must have historical data, either taken from the Eviction Lab’s national database (Desmond et al. 2018) or collected directly from the court systems. These historical data allow us to establish a baseline against which pandemic-era eviction filings can be compared. Roughly one in every four renter households in the United States lives in a jurisdiction covered by the ETS.

To facilitate comparison across similar units, we limit analysis here to counties or cities in metropolitan areas. We list these thirty-one cities in table 1, detailing the exact jurisdictions covered, the historical eviction filing rate (EFR) in each, and the years of baseline comparison data. Using information about emergency landlord-tenant policies enacted in response to the pandemic (Benfer and Koehler 2022), we list the days, if any, when each site established weak or strong eviction protections. The eviction process generally consists of five steps. First, landlords give notice to tenants that they intend to evict them. Second, landlords file an eviction case with the courts. Third, a court hearing is held. Fourth, if the court finds in the landlord’s favor, an eviction judgment is issued against the tenant. Fifth and finally, the eviction is executed. We classified those moratoria that blocked eviction cases for nonpayment of rent at one of the first three stages without requiring tenant action as offering strong protections. All other moratoria—those that blocked only one of the last two stages or that required renters to submit an affirmative declaration of hardship—we classified as providing weak protection.

ETS Sample Characteristics

As table 1 shows, we draw on data from a wide variety of jurisdictions. We have coverage in five of the ten largest cities in the country—Dallas, Houston, New York City, Philadelphia, and Phoenix—but also include a number of smaller places, such as Gainesville, Florida, and Wilmington, Delaware. Cities such as Richmond, Virginia, and Charleston, South Carolina, had extremely high eviction filing rates before the pandemic; in others, however, such cases were relatively rare. All sites enacted moratoria at the start of the pandemic, often closing courts due to concerns over the spread of COVID-19. However, many state and local governments began rolling back these protections in mid-2020: roughly half of all cities (fifteen) had no meaningful emergency eviction protections in place after August 31, 2020; seven maintained strong protections.

Eviction Filing Patterns During the Pandemic

Using these data, we document the extent to which eviction filings were reduced from the start of the COVID-19 pandemic, measured as March 15, 2020, through the end of 2021. We show, first, how total caseloads fell, month by month, across this period. Second, we demonstrate heterogeneity across cities in the scale of these reductions. These analyses demonstrate the cumulative effects of pandemic-specific policies that reduced eviction risk and highlight the inequalities that emerged between cities as a function of both more or less robust local policy response and variations in local interpretation and implementation of federal policies.

Court filings are thin records; that is, they contain relatively little information about those facing the threat of eviction or the buildings or neighborhoods in which they live. Turning to intracity variations in eviction filing reductions, we augment these data in two ways, each of which in turn forms the basis for a set of analyses.

First, at the neighborhood level, we assign eviction filings to either census tracts or, in those sites in which exact addresses were not available, zip codes. This allows us to compare eviction filing rates over time within stable geographic units and to merge in tract- or zip-level data from five-year American Community Survey (ACS) estimates. We analyze changes in the distribution of filings, demonstrating the extent to which reductions in eviction cases were evenly or unevenly spread within jurisdictions. We pay particular attention to differences in reductions in eviction filings by neighborhood racial-ethnic composition and median income. These descriptive analyses allow us to show which neighborhoods experienced the largest and smallest reductions in case filings during the pandemic.

Second, we conduct a series of analyses at the individual level. Because defendant gender and race-ethnicity are not listed in eviction records, we imputed demographic characteristics on the basis of defendants’ names and addresses (Hepburn, Louis, and Desmond 2020b; Hepburn et al. 2021). We produced three predictions of defendant gender using the R packages gender (Mullen 2018) and genderizeR (Wais 2016), and the web service Gender API (2022). Drawing on first names, each method produces a prediction (0 to 1) that the defendant is female and the inverse probability they are male. We took the mean across available predictions. To impute defendants’ race-ethnicity, we used a Bayesian predictor algorithm—the wru package in R (Khanna, Imai, and Jin 2017)—that calculates race-ethnicity probabilities on the basis of two Census Bureau data sets: the Surname List and the 2010 Census. These data sets provide, respectively, the frequencies with which common surnames are associated with racial-ethnic groups and the racial-ethnic composition of each tract in the United States. Jointly, they enable us to estimate the conditional probability of a defendant’s race-ethnicity, given their surname and geolocation. This process produces counts of eviction filings disaggregated by gender and race-ethnicity. We divide these counts by the number of renters in the respective group to produce EFRs, which we in turn use to demonstrate differences by race-ethnicity and gender.6

Causal Effects of Eviction Prevention Policies

We leverage the staggered roll-out and repeal of state and local eviction moratoria to isolate the causal effects of these policies on eviction filings.7 To do so, we use a difference-in-differences (DID) framework, identifying the effect of strong moratoria on eviction filings relative to historical averages. We use ordinary least squares (OLS) regression to model eviction filings as a percent of historical average (Y) in a given site (s) and week (t) as follows:

In equation 1, Xst is a vector of time-varying covariates and λs and φt are site and week fixed effects, respectively. Covariates included are unweighted county-level monthly unemployment rates and the state’s percent of ERA disbursed from the December 2020 federal relief package. The m terms in this equation are binary indicators of moratoria status. We define a moratorium as an order that halted the eviction process for nonpayment of rent at any stage between the notice stage and the execution of an eviction.8 In the main results presented here, we focus on the effects of strong moratoria: those that halted the eviction process at either the notice, filing, or court hearing stage of the eviction process without requiring tenant action.9 The subscript y on these terms refers to event time, which are weekly intervals relative to the week when moratoria were enacted (for example, –2 refers to two weeks before moratoria were enacted). Thus the variable msy denotes a series of binary indicators equal to 1 if the moratoria for a given site had occurred during or before the week associated with event-time period y.

This model estimates the difference in outcomes for leads  of moratoria enactment relative to a reference week (y = –1) and relative to all sites that did not enact moratoria during the study period (where msy = 0 for all event periods). These relative differences are captured by the coefficients βy. By allowing associations between exposure and the outcome to vary over time, our specification represents a generalization of the method of difference-in-differences, often referred to as the event study specification (Goodman-Bacon 2021; Venkataramani et al. 2020; Sandoval-Olascoaga, Venkataramani, and Arcaya 2021). In addition to allowing for time-varying exposure and treatment effects, the event study specification provides a more transparent test of violations of the parallel trends assumptions (by examining trends in the event time coefficients leading up to moratoria). For ease of visualization and to reduce week-to-week variation, we bin event-time y as follows: –3 (less than minus eight weeks), –2 (minus eight to minus five weeks), –1 (minus four to minus one weeks), 0, 1 (one to four weeks), 2 (five to eight weeks), 3 (nine to twelve weeks), and 4 (more than twelve weeks) (results with unbinned week-time are presented in the supplementary materials). Some sites enacted a second moratorium after the expiration of their first order, and we include both sets of moratoria in analyses.

of moratoria enactment relative to a reference week (y = –1) and relative to all sites that did not enact moratoria during the study period (where msy = 0 for all event periods). These relative differences are captured by the coefficients βy. By allowing associations between exposure and the outcome to vary over time, our specification represents a generalization of the method of difference-in-differences, often referred to as the event study specification (Goodman-Bacon 2021; Venkataramani et al. 2020; Sandoval-Olascoaga, Venkataramani, and Arcaya 2021). In addition to allowing for time-varying exposure and treatment effects, the event study specification provides a more transparent test of violations of the parallel trends assumptions (by examining trends in the event time coefficients leading up to moratoria). For ease of visualization and to reduce week-to-week variation, we bin event-time y as follows: –3 (less than minus eight weeks), –2 (minus eight to minus five weeks), –1 (minus four to minus one weeks), 0, 1 (one to four weeks), 2 (five to eight weeks), 3 (nine to twelve weeks), and 4 (more than twelve weeks) (results with unbinned week-time are presented in the supplementary materials). Some sites enacted a second moratorium after the expiration of their first order, and we include both sets of moratoria in analyses.

The majority of moratoria were enacted at around the same time at the start of the pandemic, which limits the power of our model. We therefore also present results from a period between April and November 2020 when initial state and local moratoria expired in staggered weeks. Because these analyses focus on the period when moratoria were being rolled back, treatment in these specifications is flipped from our earlier models: in this period, we define treatment as going from a strong moratorium to no strong moratorium.

Results are substantively similar across several alternative specifications (for example, testing count models in place of OLS, testing the effects of any moratoria rather than just strong moratoria, and using alternative estimators to two-way fixed effects).10

RESULTS

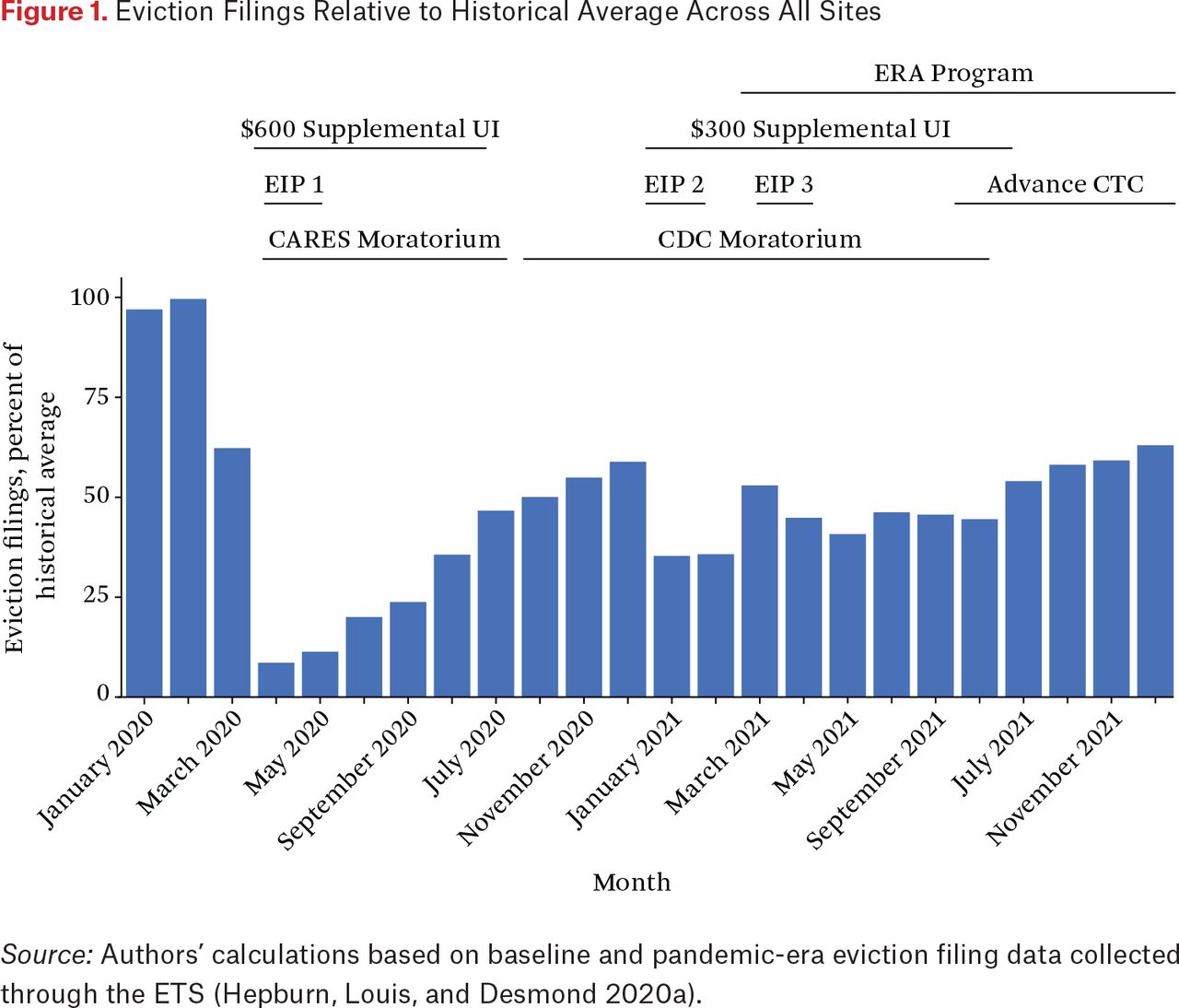

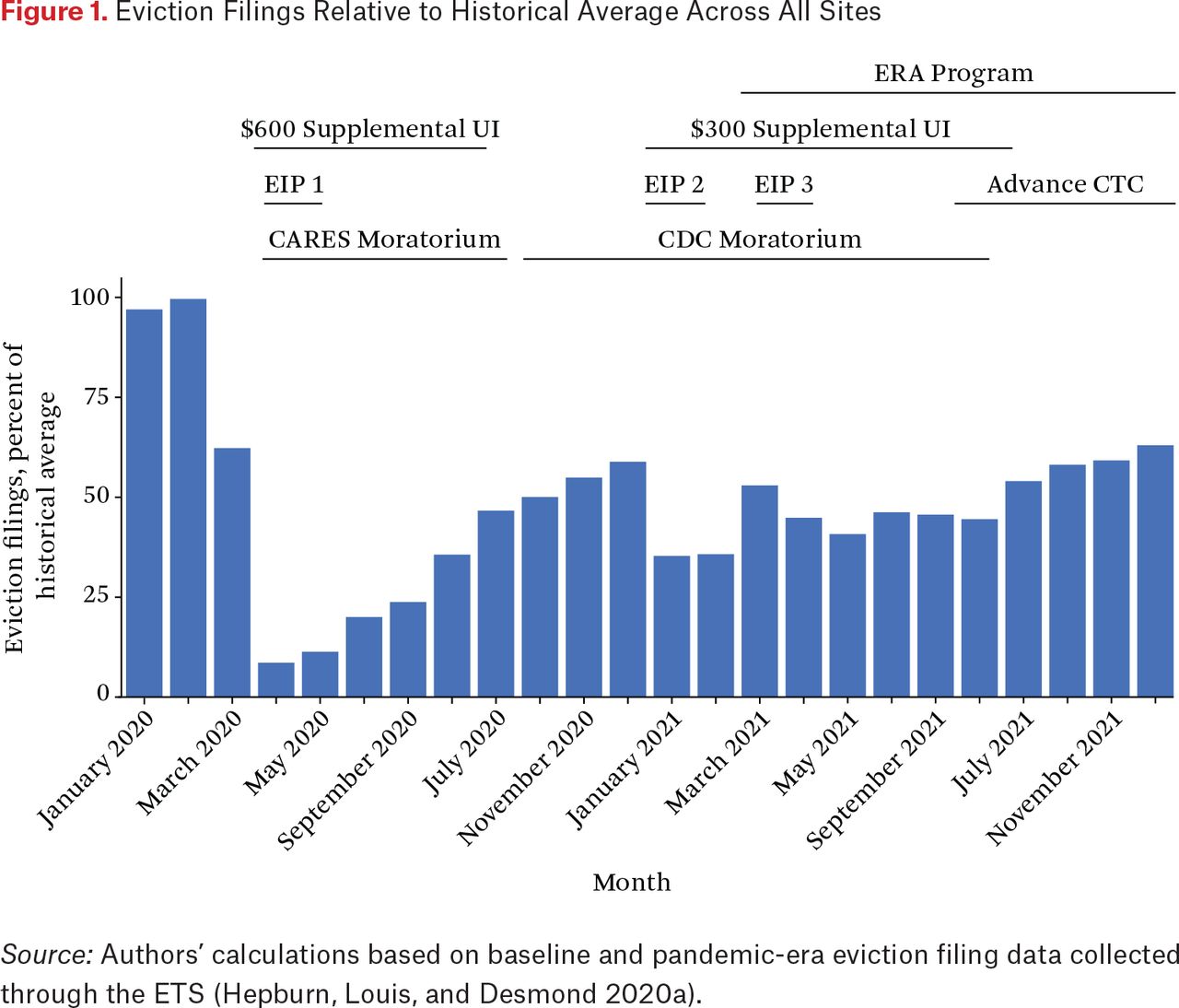

Between March 15, 2020, and December 31, 2021, we recorded the filing of 594,352 eviction cases in the thirty-one cities in our sample. Historical data from the same sites indicate that this was 57.6 percent lower than average for this period (42.4 percent of the 1,401,081 cases typically filed). In figure 1, we plot eviction filings relative to normal from January 2020 through December 2021. The figure also provides a timeline of when major federal policies that could have reduced eviction risk were implemented.

Eviction Filings Relative to Historical Average Across All Sites

Source: Authors’ calculations based on baseline and pandemic-era eviction filing data collected through the ETS (Hepburn, Louis, and Desmond 2020a).

Filings were reduced most dramatically in the early months of the pandemic, dropping as low as 8.6 percent of historical average in April 2020. By fall 2020—with the CDC eviction moratorium in place nationwide—this rate had increased to approximately 50 percent of historical average (Hepburn et al. 2021). Filings remained around this level throughout the duration of the CDC moratorium, and increased slightly after it was struck down by the Supreme Court in late August 2021 (Rangel et al. 2021).

Variation Between Cities

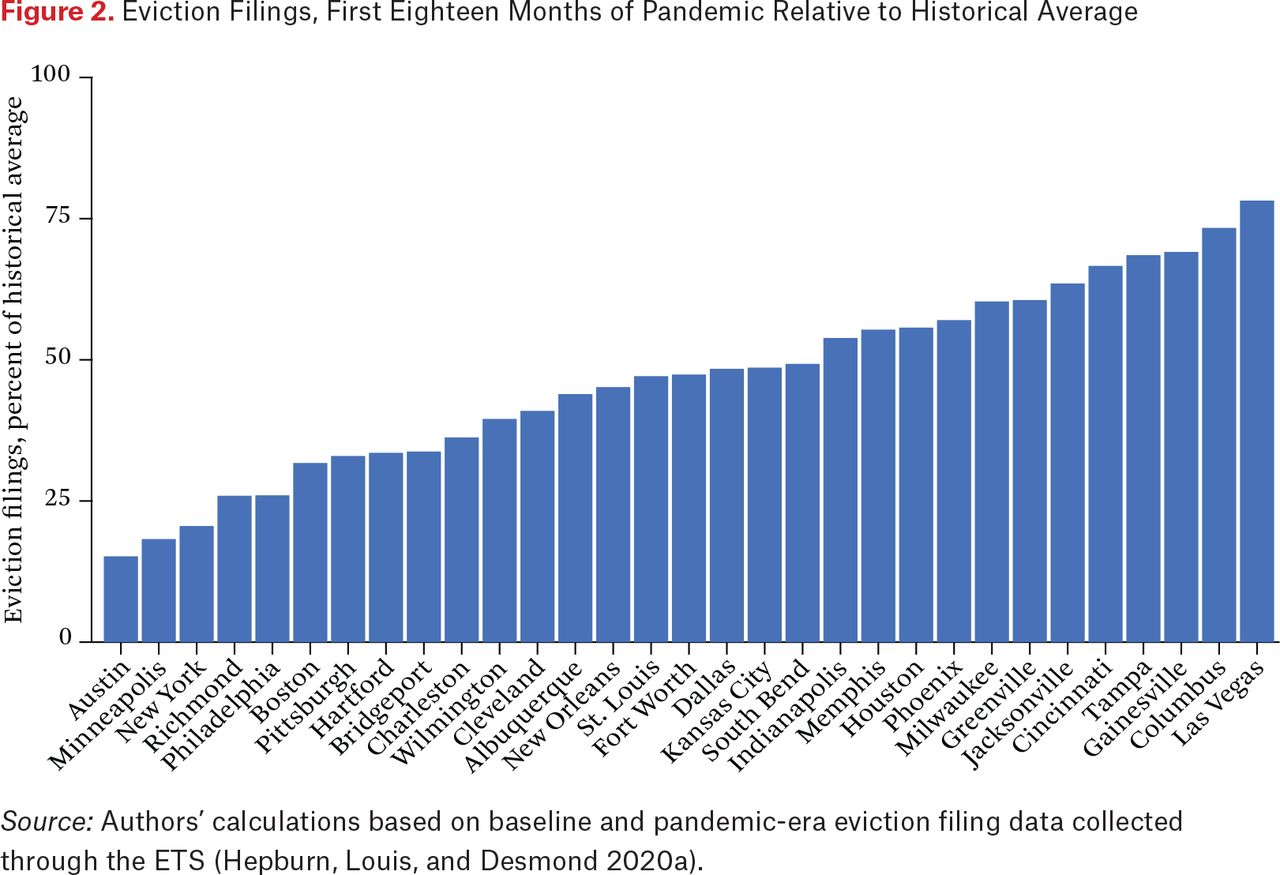

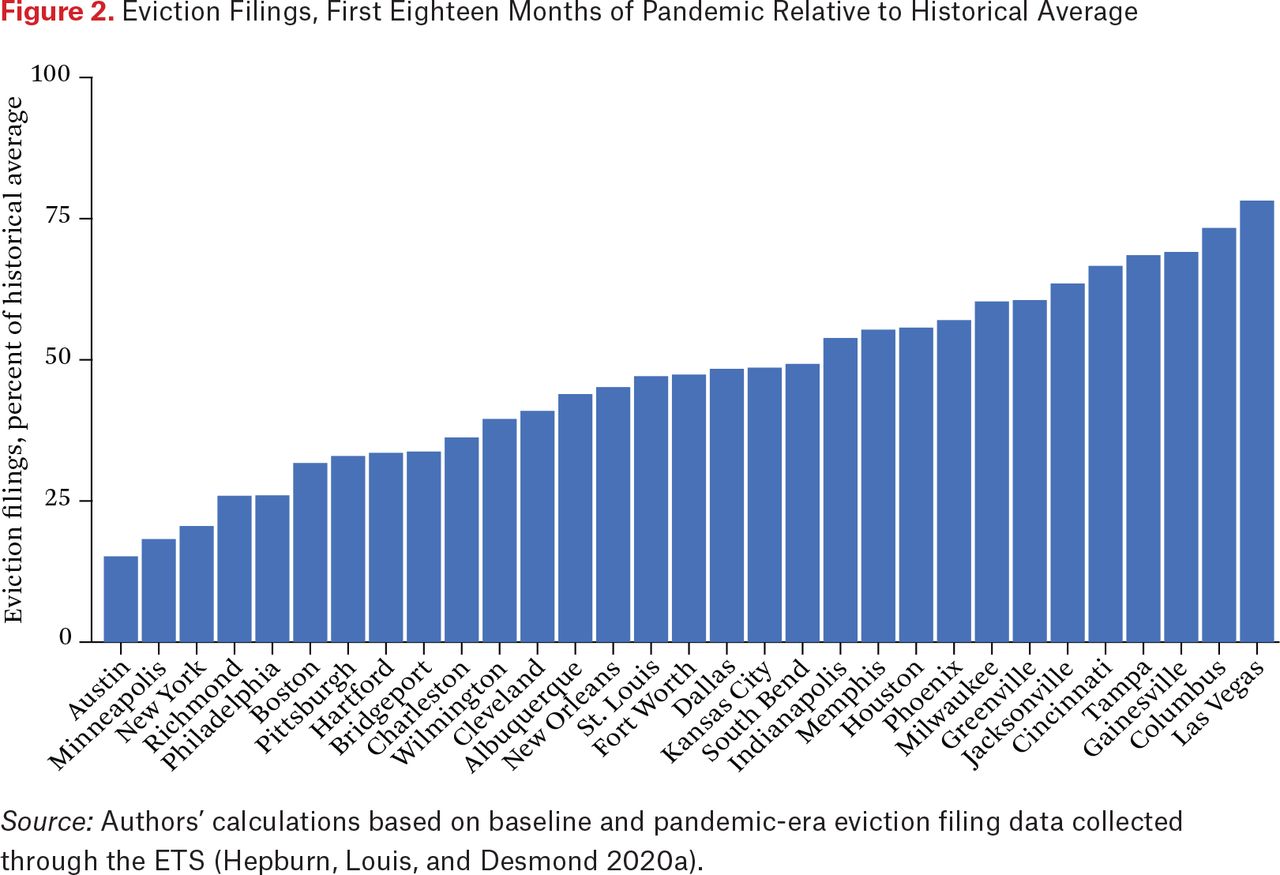

Just as cities’ eviction filing rates varied before the pandemic, we also observed differences between cities in the scale of eviction filing reductions during the pandemic. Variations in local interpretation and implementation of federal eviction moratoria—as well as establishment of additional state- or local-level eviction protections—led to considerable heterogeneity in eviction filing rates (Hepburn et al. 2021; Rangel et al. 2021). Simply as a function of where they lived, tenants struggling to pay rent were at much greater risk of receiving an eviction filing in some cities than in others. In figure 2, we plot cumulative eviction filings over the study period relative to historical average in each city. Case filings ranged from 15.2 percent of historical average in Austin to 78.2 percent in Las Vegas.

Eviction Filings, First Eighteen Months of Pandemic Relative to Historical Average

Source: Authors’ calculations based on baseline and pandemic-era eviction filing data collected through the ETS (Hepburn, Louis, and Desmond 2020a).

Cities that enacted the most stringent and longest-duration eviction moratoria cluster on the left side of figure 2. Of the ten cities with lowest filings relative to average, all were covered by strong eviction moratoria in the early days of the pandemic and eight maintained these protections through at least summer 2020. For example, apart from exceptional circumstances (such as tenants engaged in criminal activity or creating unsafe living conditions), landlords in Minneapolis-St. Paul could not start the eviction process between March 16, 2020, and June 30, 2021. Over the full study period, eviction filings fell by 81.7 percent in the Twin Cities. By comparison, of the ten cities with the highest filings relative to average, four ended all state and local protections by early June 2020, and only one (Las Vegas) had strong protections in place after August 2020. In Las Vegas, filings were generally below historical averages when Nevada had strong protections in place but skyrocketed well above average during periods when protections lifted.

Even among cities that enacted similar protections—or where protections were in place only for a relatively short period—variation in the rate of eviction filings relative to normal was considerable. For example, neither Greenville nor Columbus had eviction moratoria in place after June 1, 2020, but filings were reduced by two-thirds overall in the former compared to one-third in the latter. These inequalities played out within as well as between states: renters in Cleveland were far better insulated from the threat of eviction during the pandemic than their peers in Cincinnati and Columbus, even though none had a moratorium in place after June 15, 2020.

Variation Between Neighborhoods

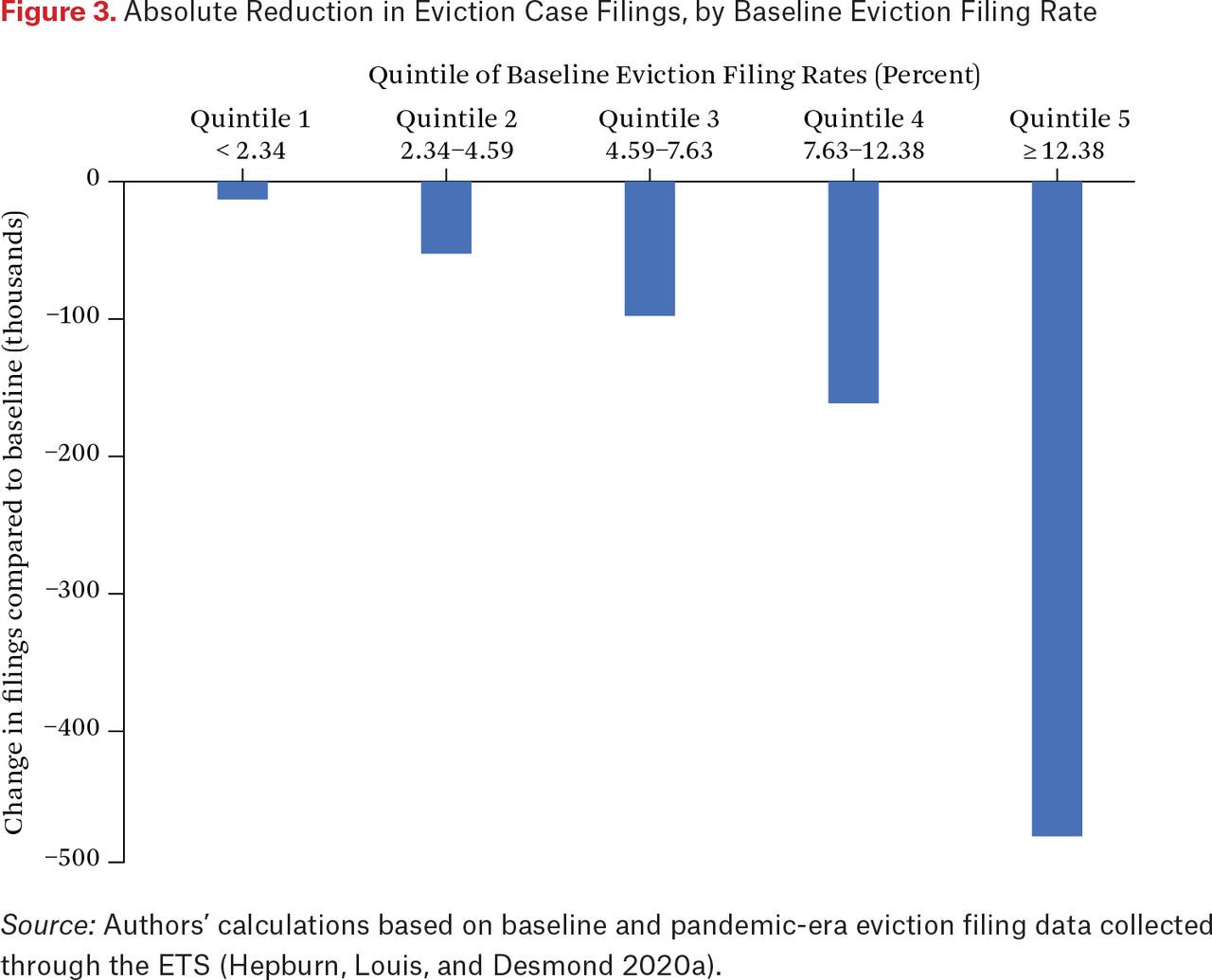

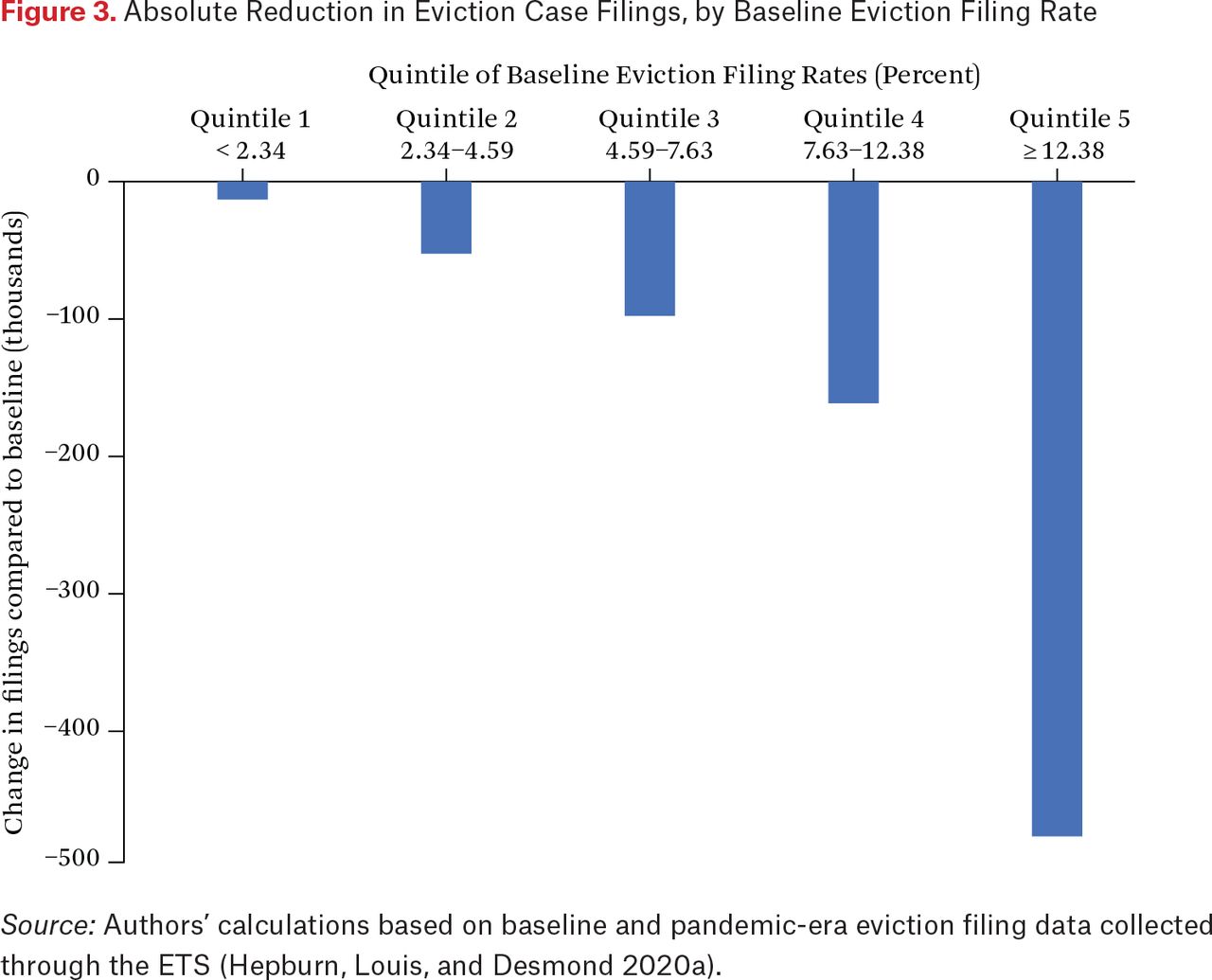

Reductions in eviction filings were far larger in areas that typically see very high EFRs. In neighborhoods that normally see the fewest eviction filings—those in the first quintile of historical baseline EFRs—filings fell 38.9 percent during the pandemic. By comparison, filings fell 62.4 percent in neighborhoods that normally see the highest filing rates (fifth quintile of baseline EFR). Because such neighborhoods experience far more filings under normal conditions, these larger proportional reductions translated into very large reductions in absolute caseloads. In figure 3, we categorize all neighborhoods by their pre-pandemic EFR and plot the total number of “missing” eviction filings (number of cases avoided) over this period.

Absolute Reduction in Eviction Case Filings, by Baseline Eviction Filing Rate

Source: Authors’ calculations based on baseline and pandemic-era eviction filing data collected through the ETS (Hepburn, Louis, and Desmond 2020a).

In total, about 476,000 eviction cases were likely averted in neighborhoods with baseline EFRs in the top quintile. Under normal circumstances, the median EFR among such neighborhoods was 17.4 percent. During the pandemic it fell to 8.3 percent.11 In other words, more than one in six residents of these neighborhoods typically faced an eviction filing each year, but only about one in twelve risked eviction during the pandemic. Approximately 325,000 cases were averted across the other four quintiles of the distribution. Each saw a relative reduction in filing rates, but the vast majority of cases prevented during the pandemic were from neighborhoods that normally saw very high filing rates.

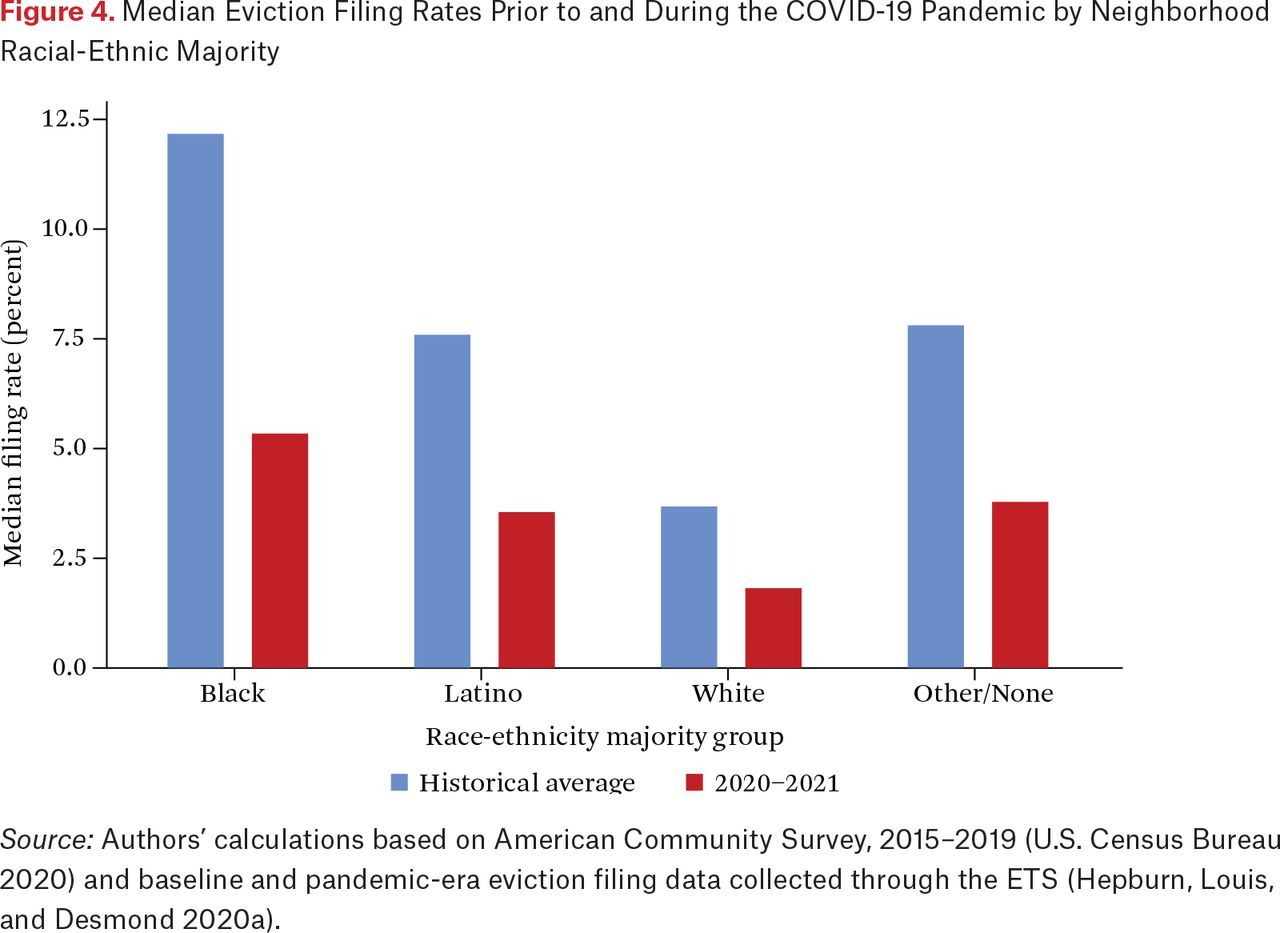

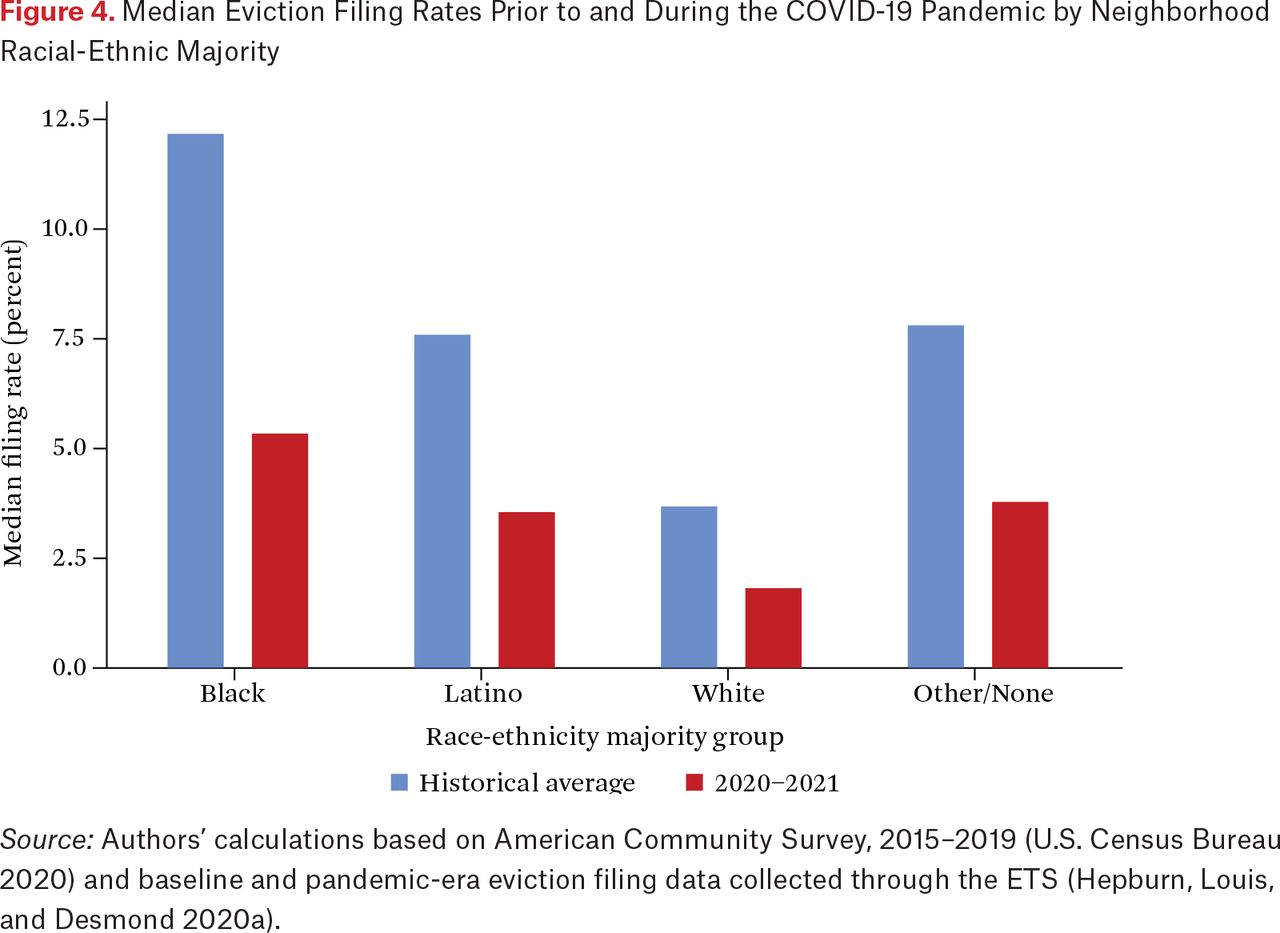

Were these changes evenly distributed depending on the racial-ethnic composition of neighborhoods? Again, the largest relative reductions accrued to areas that typically see highest eviction filing rates: majority-Black neighborhoods. Filings fell by 56.0 percent in the typical majority-Black neighborhood, relative to 51.2 percent in majority-White neighborhoods, 49.9 percent in majority-Latino neighborhoods, and 51.3 percent in neighborhoods with no racial-ethnic majority. Among majority-Black neighborhoods, around one in eight (12 percent) saw eviction filings exceed 75 percent of historical average during the pandemic, but this was true for more than one in four majority-White neighborhoods (26.1 percent). Although this did not eliminate racial-ethnic disparities in the risk of eviction, it reduced their scale considerably. In figure 4, we plot baseline and pandemic-era median EFRs in majority-Black, majority-Latino, and majority-White neighborhoods, as well as those neighborhoods with no racial-ethnic majority.12

Median Eviction Filing Rates Prior to and During the COVID-19 Pandemic by Neighborhood Racial-Ethnic Majority

Source: Authors’ calculations based on American Community Survey, 2015–2019 (U.S. Census Bureau 2020) and baseline and pandemic-era eviction filing data collected through the ETS (Hepburn, Louis, and Desmond 2020a).

Under normal circumstances, the typical majority-Black neighborhood in our sample had an EFR of 12.2 percent, 8.5 percentage points higher than that in a majority-White neighborhood (3.7 percent). That gap narrowed to 3.5 percentage points during the pandemic. Still, the typical majority-Black neighborhood had an EFR during the pandemic that was higher than the typical White neighborhood pre-pandemic (5.3 percent versus 3.7 percent). Even with filing rates cut by more than half, the risk of eviction in majority-Black neighborhoods was greater than equivalent risk in majority-White spaces before the pandemic.

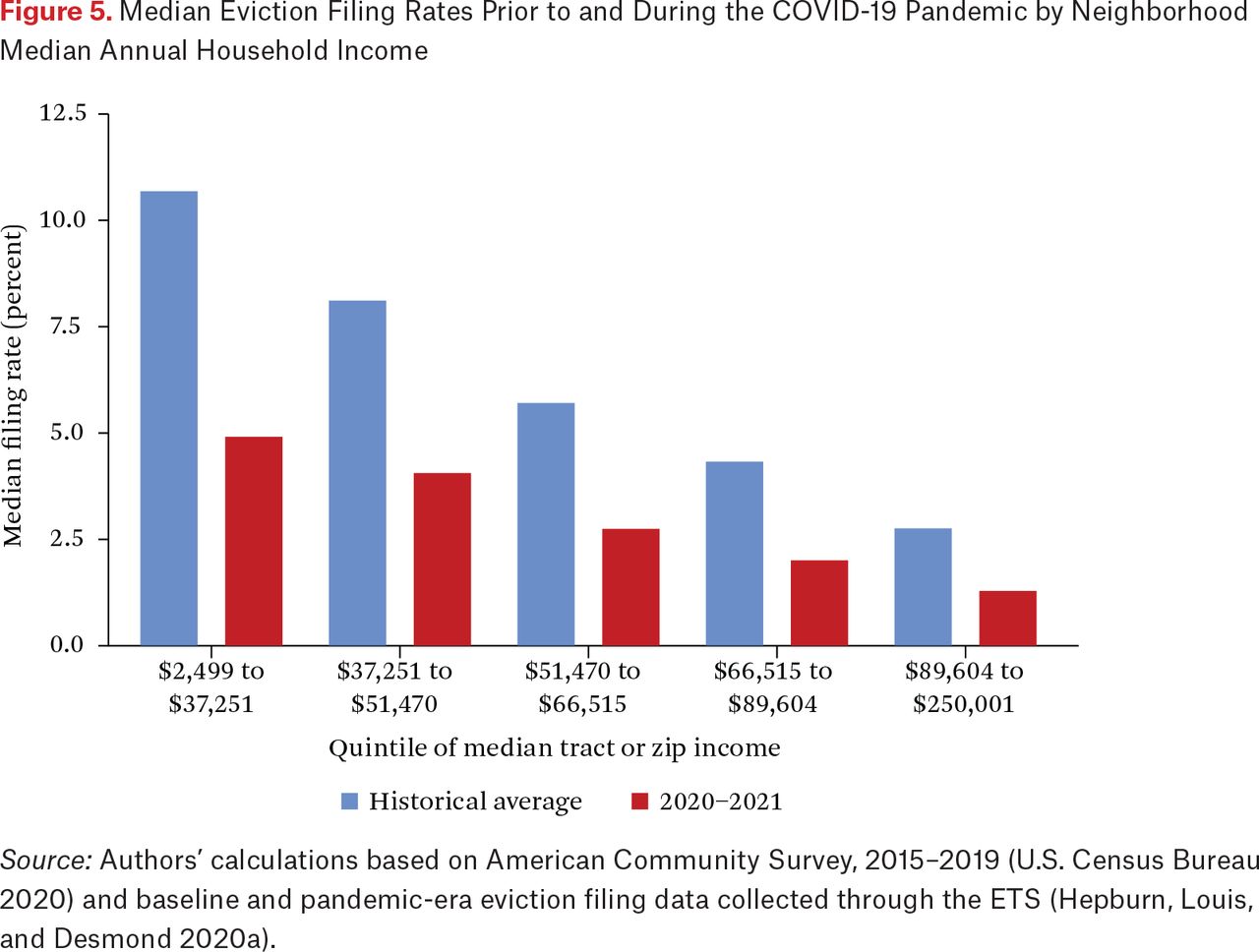

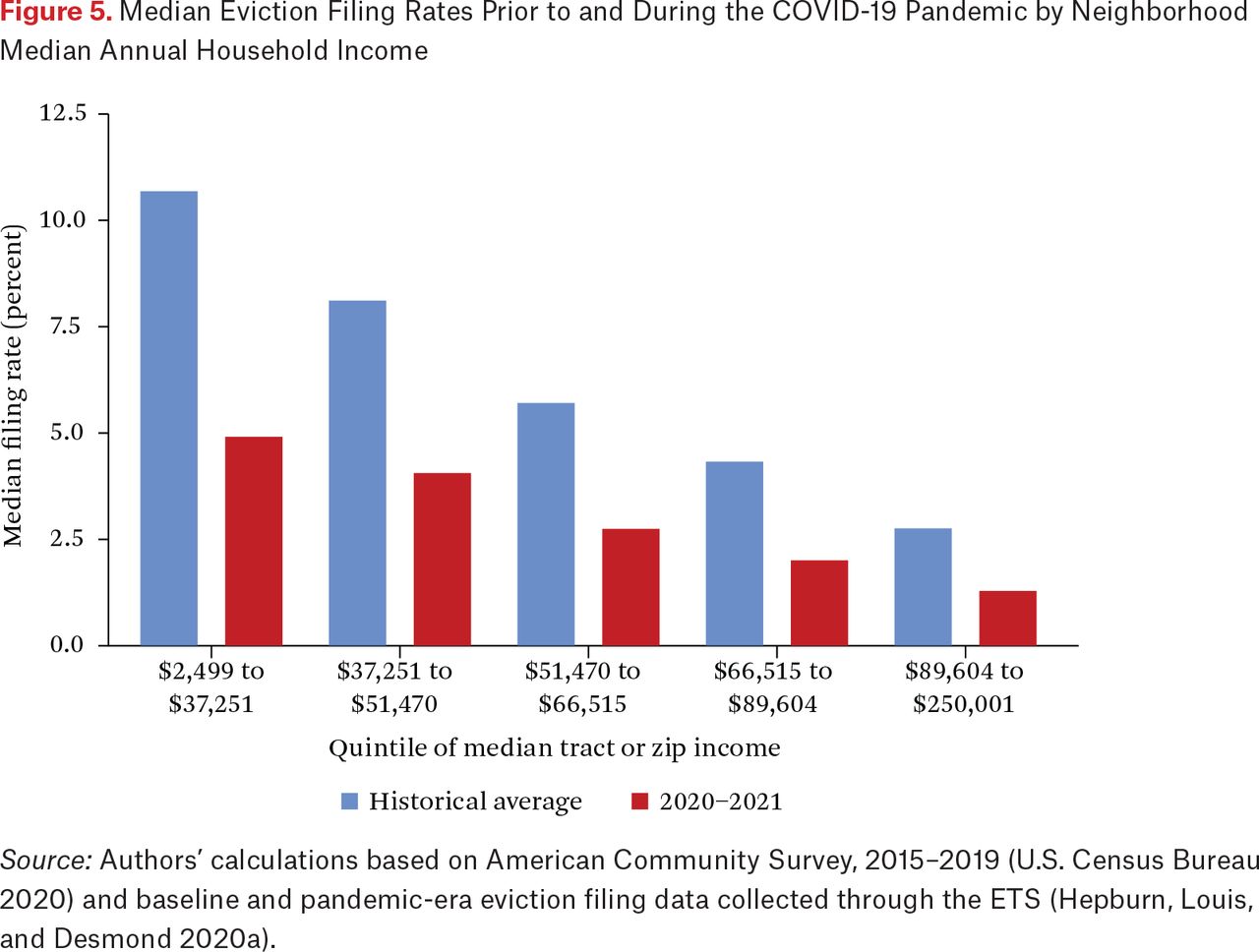

We also examined changes in filing rates by neighborhood income. We computed quintiles of neighborhood median household income across all cities in our sample and calculated baseline and pandemic-era EFRs for neighborhoods in each category. We plot median rates in figure 5.

Median Eviction Filing Rates Prior to and During the COVID-19 Pandemic by Neighborhood Median Annual Household Income

Source: Authors’ calculations based on American Community Survey, 2015–2019 (U.S. Census Bureau 2020) and baseline and pandemic-era eviction filing data collected through the ETS (Hepburn, Louis, and Desmond 2020a).

The income gradient on eviction risk is steep. Under normal circumstances, the median EFR in a neighborhood where annual household incomes fell below $37,251 (quintile one) was almost four times higher than in a neighborhood with household incomes above $89,604 (quintile five; 10.7 percent versus 2.8 percent). Even as filings were reduced during the pandemic, the shape and scale of the distribution remained the same. Put another way, relative disparities in eviction filing rates by neighborhood income were maintained throughout the pandemic. Still, the absolute reduction in case filings meant that a neighborhood in the first quintile of the household income distribution experienced a filing rate during the pandemic that was greater than normal, pre-pandemic EFR in a neighborhood in quintile four (4.9 percent versus 4.3 percent).

Variation in Individual Risk

We now turn to the individual level to assess the extent of changes in eviction patterns depending on the race-ethnicity and gender of defendants.13 During the study period, we found that Asian renters in these cities faced an average EFR of 1.3 percent, Black renters 4.2 percent, Latino renters 2.2 percent, and White renters 2.6 percent.

Across ETS cities, the Black EFR during the pandemic fell by between 9.5 percent in Las Vegas and 87.8 percent in Austin. Generally, reductions relative to average were similar within cities regardless of race-ethnicity. In Albuquerque, for example, pandemic EFRs were approximately 60 percent below historical average for members of all racial-ethnic groups. In several sites, however, the reductions for Black renters were notably larger than for White renters. This was true of Boston, Bridgeport, Gainesville, Hartford, Houston, Milwaukee, and New Orleans. Still, baseline filing rates were generally much higher for Black renters than White renters in these sites. Even with larger relative reductions, the EFRs recorded for Black renters during the pandemic were higher—often considerably higher—than among their White peers.

Eviction filings disproportionately target women (Desmond 2016; Hepburn, Louis, and Desmond 2020b). This remained true during the pandemic, but the gender disparity was reduced. Normally, we estimate that 51.9 percent of people facing eviction across these cities were women and 43.5 percent were men (gender predictions cannot be made for the remaining 4.7 percent of defendants).14 During the pandemic, we estimate that 49.2 percent of filings were against women, that 45.2 percent were against men, and that no prediction was possible for the remaining 5.6 percent.

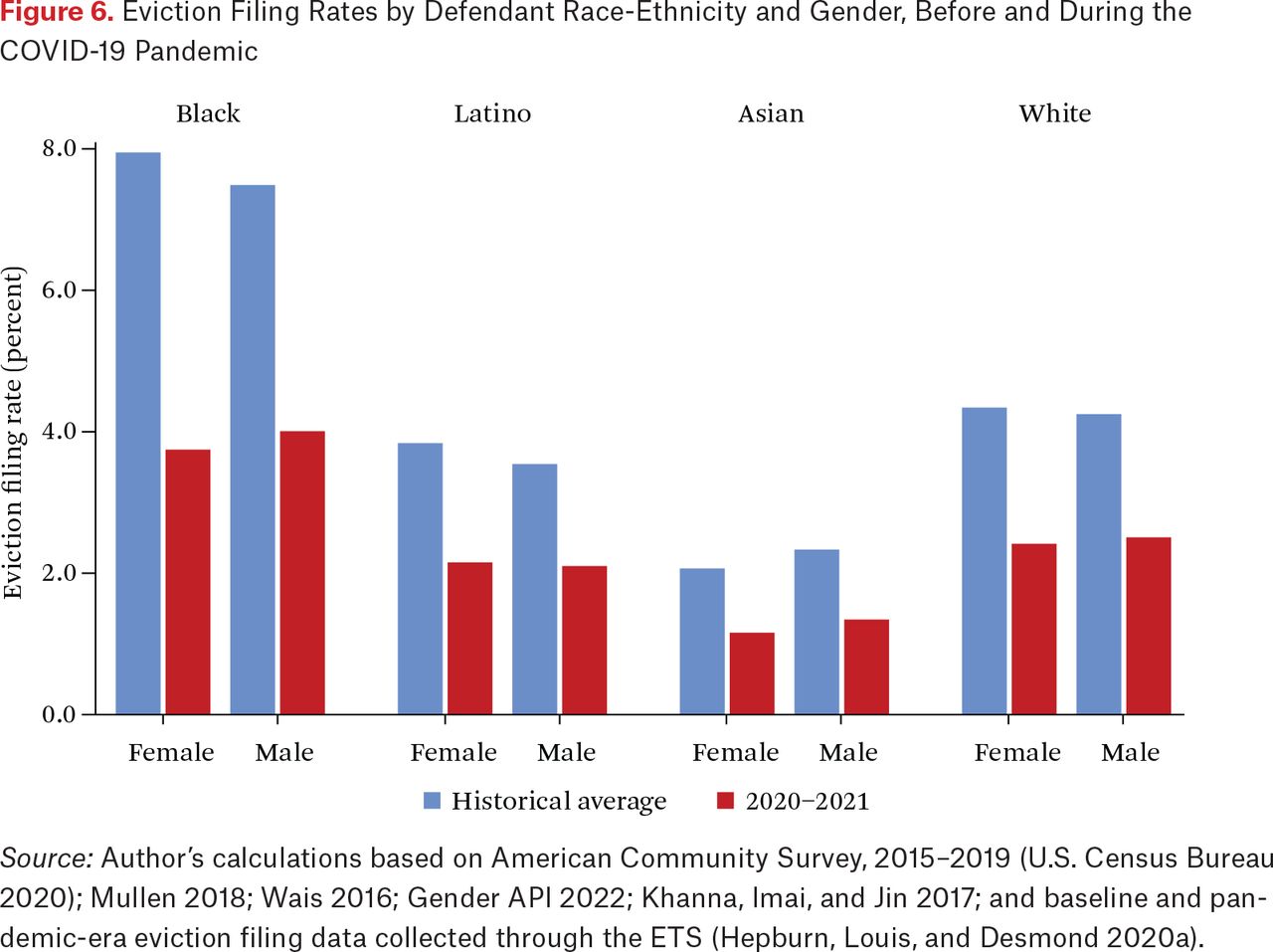

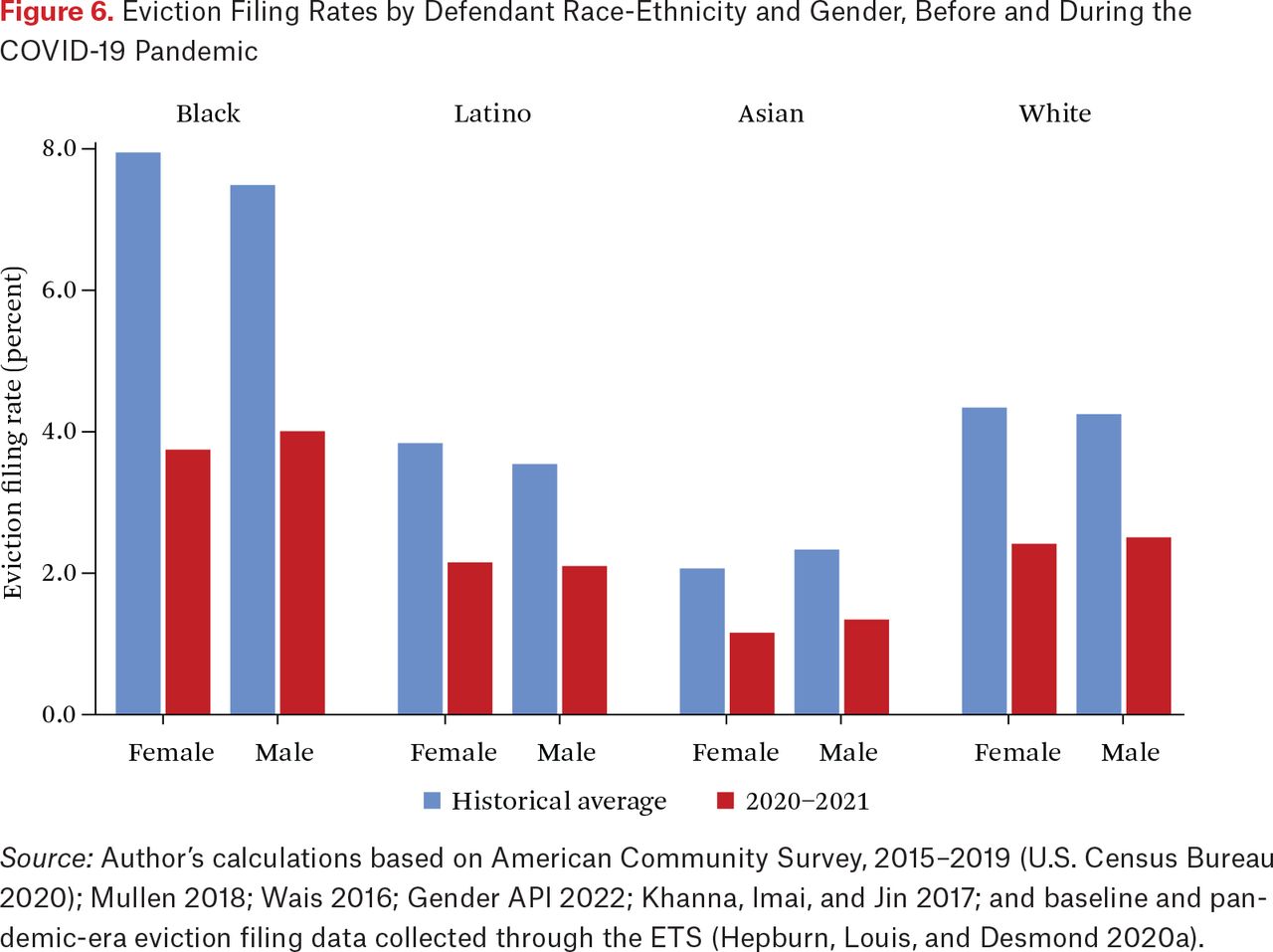

In figure 6, we combine these estimates to show how the distribution of eviction filings has shifted during the pandemic. We plot EFRs before and during the pandemic, cross-classified by defendant race-ethnicity and gender.

Eviction Filing Rates by Defendant Race-Ethnicity and Gender, Before and During the COVID-19 Pandemic

Source: Author’s calculations based on American Community Survey, 2015–2019 (U.S. Census Bureau 2020); Mullen 2018; Wais 2016; Gender API 2022; Khanna, Imai, and Jin 2017; and baseline and pandemic-era eviction filing data collected through the ETS (Hepburn, Louis, and Desmond 2020a).

Before the pandemic, Black women in these cities faced a median EFR of 7.9 percent, meaning that approximately one in twelve would face the risk of eviction annually. During the pandemic, that figure was reduced to 3.7 percent, or a risk of about one in twenty-seven. Before the pandemic, gender disparities in eviction filing rates were largest among Black renters (7.9 percent for Black women versus 7.5 percent for Black men). That gap was reversed during the pandemic, leaving Black men at highest risk of facing eviction (4.0 percent).

Assessing the Efficacy of Eviction Moratoria

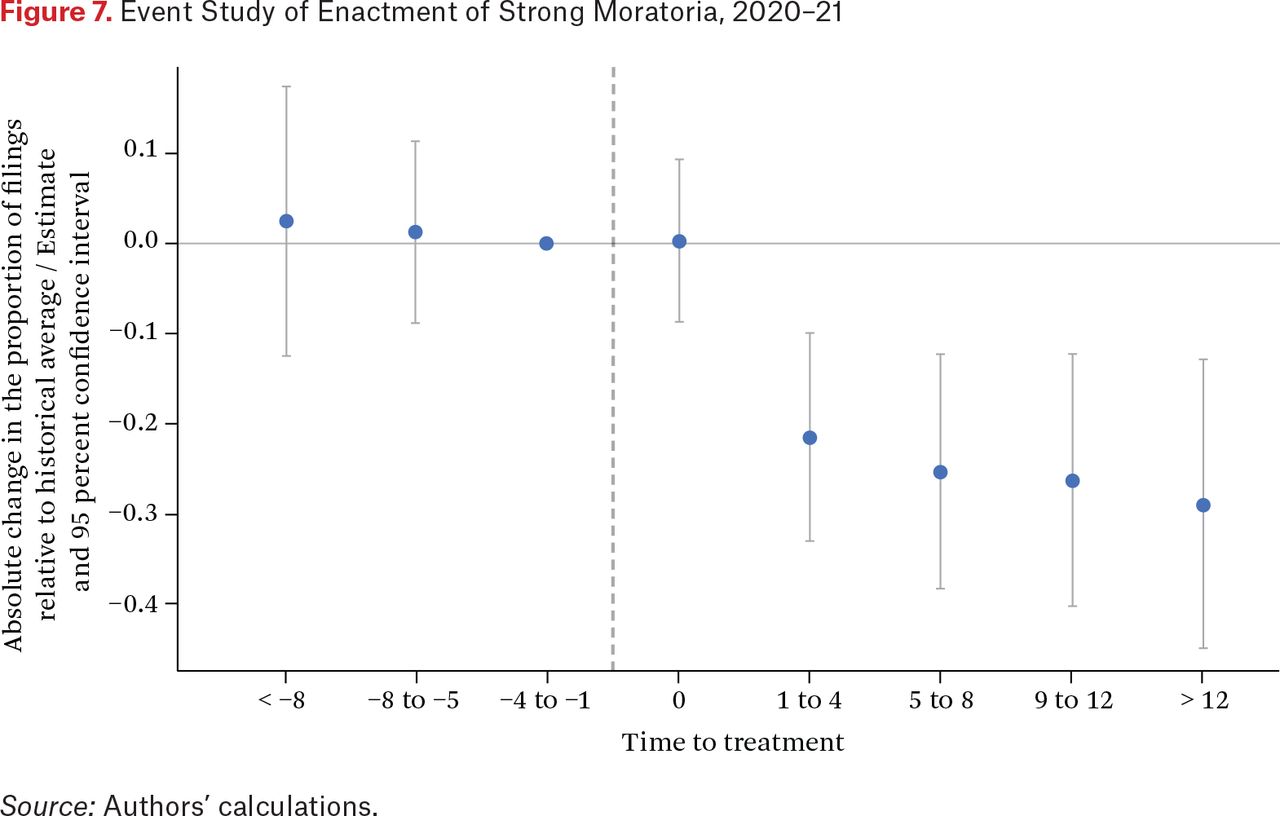

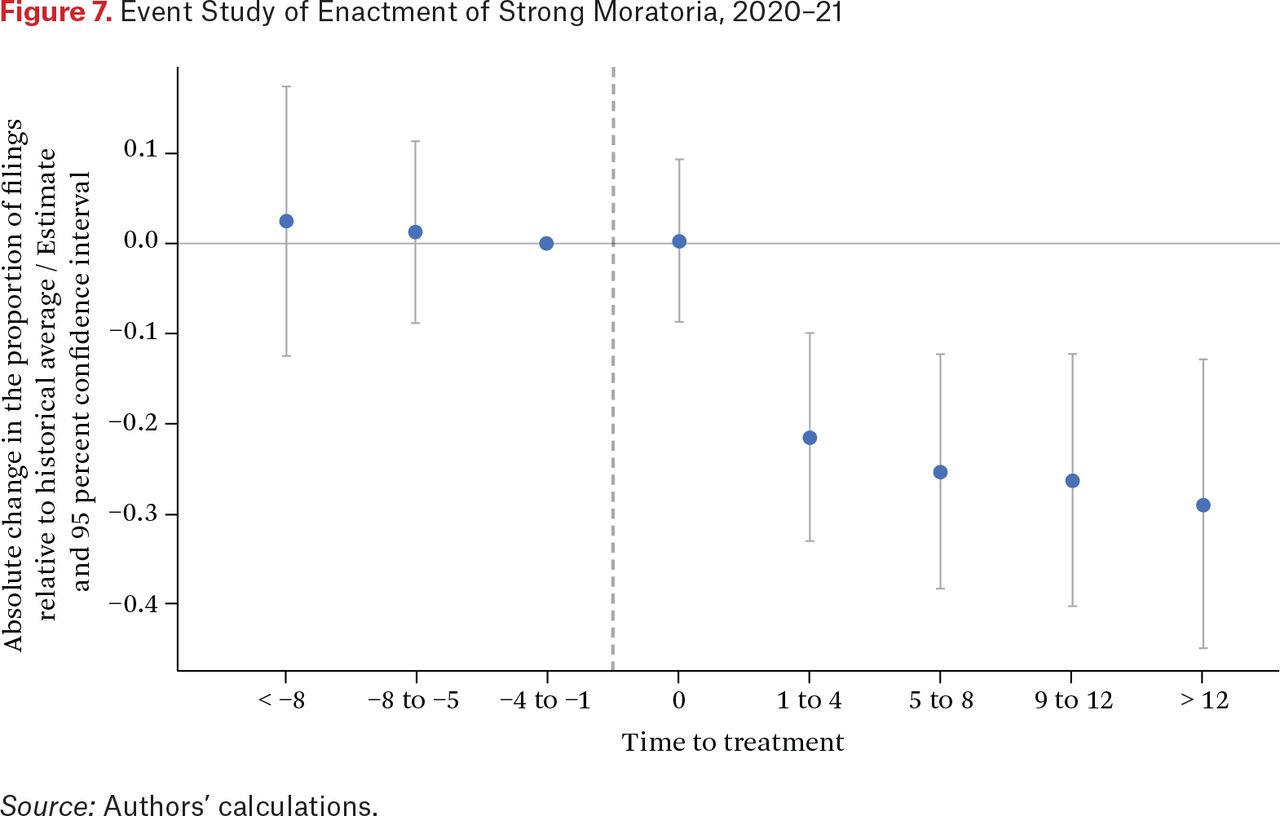

Finally, we examine the effects that moratoria had in reducing the filings of eviction cases. As specified in equation (1), we identified the effects of strong moratoria on eviction filings relative to historical averages, comparing eviction filings before and after treatment of a strong state or local moratorium.15 We define a strong moratorium as one that halted the notice, filing, or hearing stage of the eviction process unless it required a declaration of hardship due to COVID-19. Results are presented in figure 7.

Event Study of Enactment of Strong Moratoria, 2020–21

Source: Authors’ calculations.

Strong state and local eviction moratoria significantly reduced eviction filings relative to historical averages. Point estimates imply that a strong moratorium reduced eviction filings as a percent of historical averages by 21.3 percentage points (CI [confidence interval]: 9.5, 33.2) in a given site in the four weeks immediately after implementation and gradually increased to 28.7 percentage points (CI: 12.2, 45.2) for more than twelve weeks after implementation. In other words, given an area at 70 percent of historical baseline levels, establishing a strong state or local moratorium would have reduced filings, on average, to around 41 to 49 percent of baseline. Parallel trends assumptions are plausible given pre-treatment trends.

The majority of strong moratoria were enacted over the course of a few weeks at the start of the pandemic. Just four cities were not fully covered by a strong moratorium over the length of this initial period, and each of them was covered at least by a weak eviction moratorium (that is, no sites in our sample failed to implement a moratorium). Thus our control group does not represent a situation lacking eviction prevention measures or supports available to renters. Even in the control setting, weak moratoria and site-invariant federal policies reduced filings. Our results, therefore, are a measure of the additional protection against eviction filings that strong state and local policies afforded during the study period above and beyond concurrent pandemic policies.

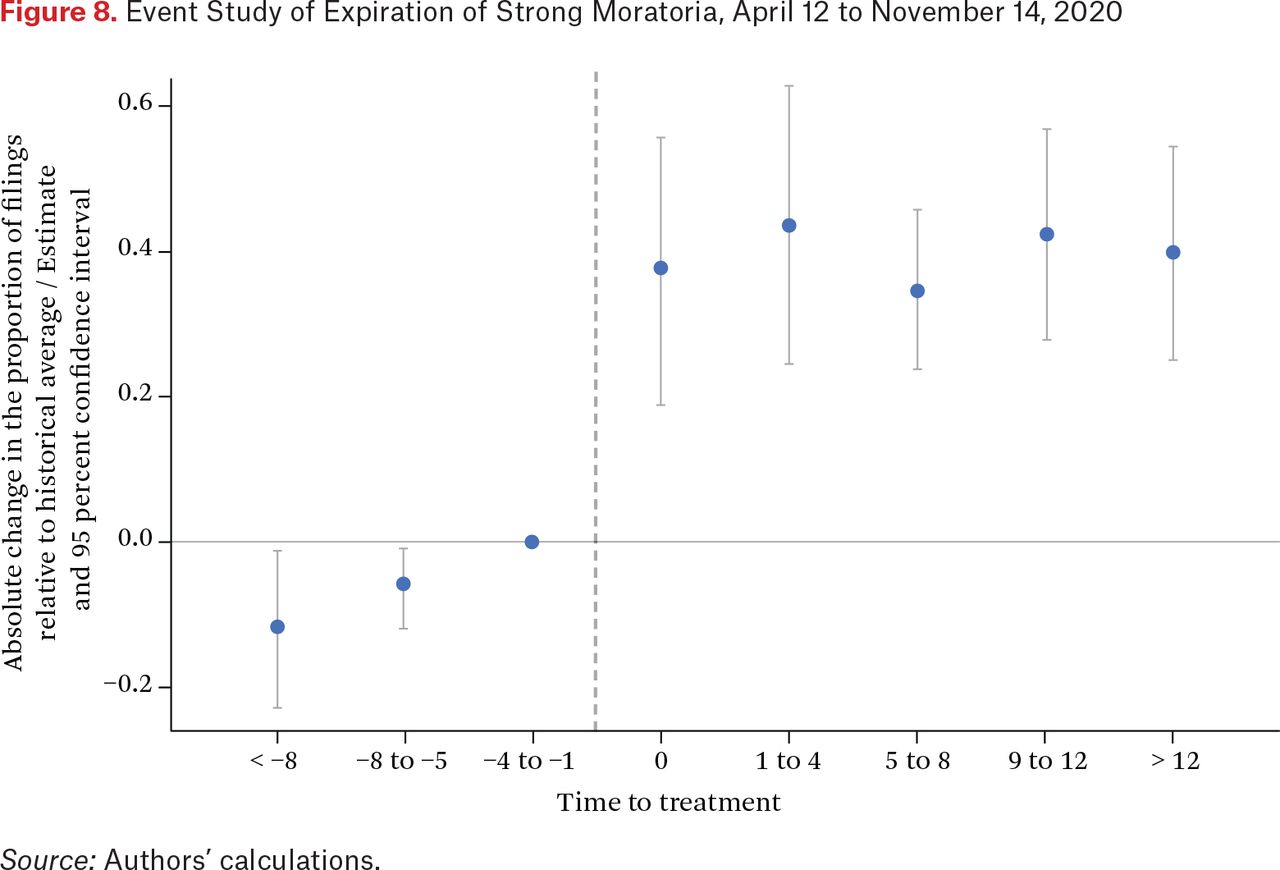

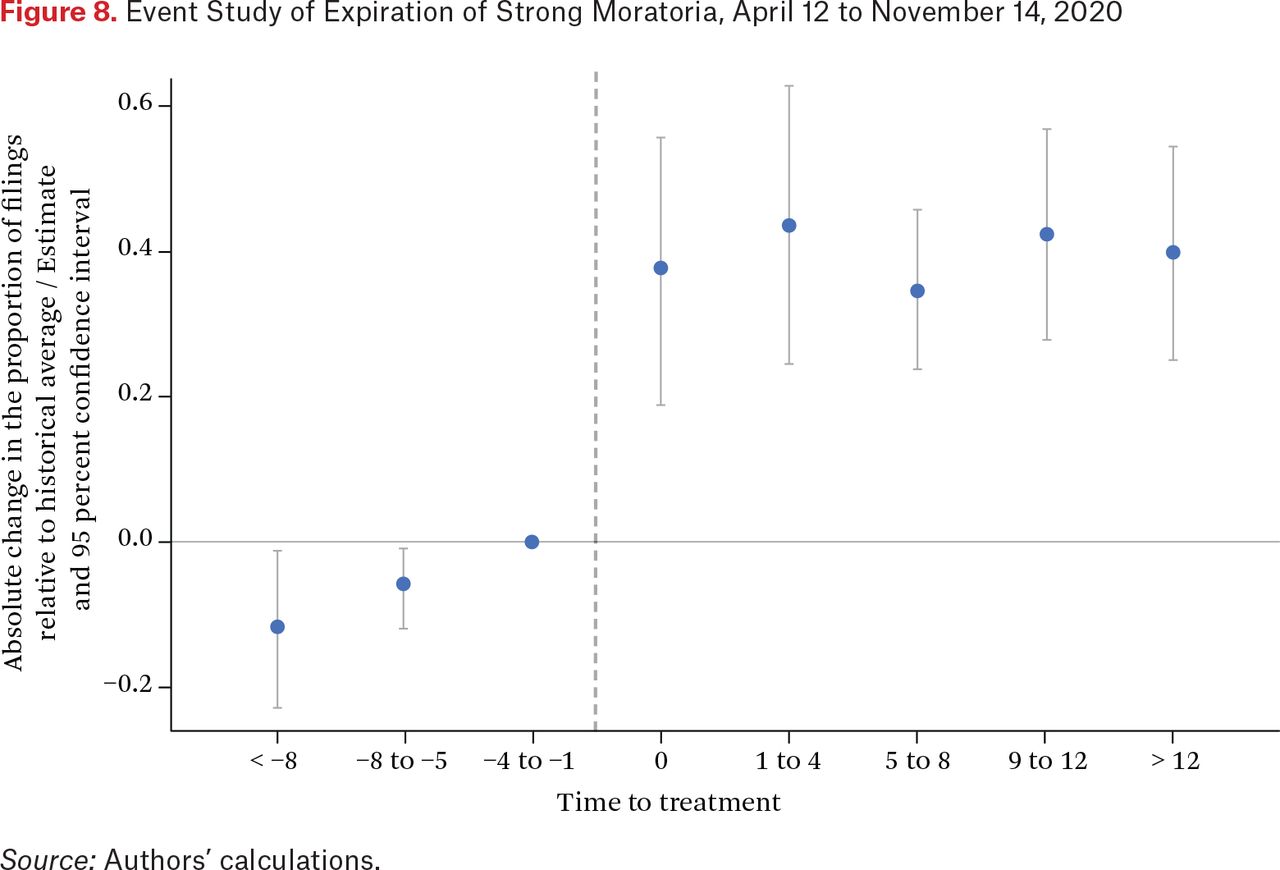

The lack of a robust control group limits our ability to identify precise estimates in the above results. We therefore also present results from the six months between April and November 2020, when initial state and local moratoria expired in a more staggered time frame. Of the twenty-seven sites in our sample with strong moratoria on April 12, 2020, only four still had that order in place by November 14, 2020. We exploit variation in the timing of sites lifting their moratoria to estimate the effects of these policies. Treatment in this specification is flipped from our earlier models: for these results, we define treatment as going from a strong moratorium to no strong moratorium. Thus, a positive coefficient on a post-treatment period would indicate that the expiration of a moratorium led to an increase in filings relative to historical averages. Results are presented in figure 8.16

Event Study of Expiration of Strong Moratoria, April 12 to November 14, 2020

Source: Authors’ calculations.

As strong eviction moratoria were repealed, eviction filings increased markedly. Estimates imply that the rolling back of a strong moratorium increased eviction filings as a percentage of historical averages by 43.6 percentage points (CI: 23.4, 63.8) in a given site in the four weeks immediately after implementation. Effects fluctuated modestly in following periods but ranged from 34.7 to 42.4 percentage points. Alternative specifications—using a Poisson model; with a relaxed definition of moratoria; where no covariates were included; where weeks were not binned; where the dependent variable was log-transformed; where we removed trailing nontreated weeks from treated sites; and results that follow the methods of Liyang Sun and Sarah Abraham (2021) and Clément de Chaisemartin and Xavier D’Haultfœuille (2020)—are largely consistent with those presented here (see the online supplementary materials). Overall, our results indicate that state and local moratoria significantly reduced eviction filings relative to historical averages.17

DISCUSSION

The COVID-19 pandemic and resulting economic fallout exposed the U.S. rental housing market to an extraordinary level of stress. Before the pandemic, nearly half of all renters were cost burdened (JCHS 2020), and few had the personal savings to weather an unexpected financial shortfall (Pew Charitable Trusts 2018). As millions lost their jobs in March and April of 2020, the concern that a surge in eviction cases might follow was well founded. Under strong economic conditions, millions annually risk losing their homes to eviction (Gromis et al. 2022), a threat felt most acutely by Black renters in poor, urban communities (Hepburn, Louis, and Desmond 2020b; Desmond and Gershenson 2017). How much worse would it get?

In this article, we demonstrate the extent to which, cumulatively, policies enacted at the local, state, and federal levels averted this potential calamity. In the thirty-one cities we analyzed, 57.6 percent fewer eviction cases than usual were filed during the pandemic. This reduction was concentrated in neighborhoods that normally see the most evictions. In raw numbers, 476,000 fewer cases were filed than usual just in the fifth of neighborhoods that typically see the highest eviction filing rates. Rates were cut by more than half in majority-Black neighborhoods and in neighborhoods with the lowest median incomes. Black women saw the largest absolute reduction in rates.

Despite massive reductions, though, inequalities in eviction risk remained. We documented significant heterogeneity between cities in the extent to which filings were reduced. During the pandemic, a tenant in Minneapolis struggling to pay rent would have been much better protected from the threat of eviction than an equivalent tenant in Columbus. State and local eviction moratoria can explain some of the variation, but hardly all of it. Indeed, even among cities in which local protections were short lived, variation in the scale of reductions was considerable.

Although the absolute reduction in case filings was largest in majority-Black and lower-income neighborhoods, these changes did not eliminate inequalities that existed before the pandemic. Poor and majority-Black neighborhoods saw large reductions in eviction case filings, but so did wealthier, whiter spaces (see figures 4 and 5). Lower-income neighborhoods still saw much higher rates than more affluent neighborhoods. The reduction in filing rates in majority-Black neighborhoods (documented in figure 4) still left them with a higher median filing rate than among majority-White neighborhoods before the pandemic.

Still, that inequalities endured should not distract from the fact that hundreds of thousands fewer households than usual in these cities faced the threat of eviction during the worst months of the pandemic. Take the Hill District in Pittsburgh as an example (zip code 15219). The neighborhood has a median household income of around $25,000 and, during a typical period extending from mid-March to the end of December of the following year, would be the site of nearly one thousand eviction case filings. Between March 15, 2020, and December 31, 2021, only 186 cases were filed (81.2 percent less than usual). Future research should aim to explore the full significance of that sort of reduction, both for households who avoided displacement and for communities seeing far less churn. Against a backdrop of tremendous economic and public health uncertainty, what did that increased residential stability entail for individuals’ health and well-being? For children’s educational attainment? For the neighborhood’s collective efficacy?

As detailed, a wide variety of policies implemented at the federal, state, and local levels either restricted the eviction process (such as moratoria) or improved tenants’ odds of being able to pay rent (such as ERA, stimulus payments, expanded unemployment), thereby reducing eviction risk. Which of these policies were most significant in reducing eviction filing rates? Answering this question is critical to the design of effective housing stabilization policies, both in response to future crises and under normal conditions. The co-occurrence of these policies, however, makes accurately assessing the marginal contribution of each difficult if not impossible (Matthay, Hagan, et al. 2022; Matthay, Gottlieb, et al. 2022). We were able to exploit temporal variation in enactment and repeal of strong state and local eviction moratoria to demonstrate that such policies reduced eviction filings by around 20 to 45 percentage points relative to a baseline with no strong protections in place.18 These findings are context dependent and should be interpreted as conservative: effect sizes may be larger in future contexts in which no other federal or local policies are concurrent.

Future research should bring similar methods to bear in analyzing the effects of ERA in reducing eviction filings. The ERA allocation formula—based on state population but requiring a sizable minimum payment—resulted in large disparities between states, far more funding being available in small, rural states than in large, urban states. State, county, and local grantee programs also established differing qualification standards and application processes, and varied in how efficiently they were able to distribute funds (Yae et al. 2020; Reina et al. 2021). Data are not currently available that demonstrate the pace of ERA distribution at the tract-month or county-month level. As such data become available, however, it should be possible to leverage variations in the generosity of benefits to estimate a dose-response relationship. These analyses are particularly significant in making a case for the long-term viability of rental assistance.

It remains unclear what lasting changes to housing policy will emerge from the pandemic. The Supreme Court’s decision striking down the CDC moratorium—coupled with landlords’ vocal opposition to such policies—makes it likely that eviction moratoria will be reserved for emergency situations. The long-term potential of ERA depends on proof of efficacy and the availability of federal funding. Landlord-tenant law varies primarily at the state level and has significant implications for eviction rates (Hatch 2017; Gromis et al. 2022). A number of states established policies during the pandemic to afford tenants greater protections, including the expansion of record sealing laws, eviction mediation, and programs to provide legal counsel to those facing eviction. These programs, however, were clustered in states that already had more tenant protections in place. The divide between renters living in states with more or less landlord-friendly eviction laws likely grew during the pandemic, leaving millions of renters returning to the pre-pandemic status quo as emergency policies expire and ERA funding runs out.

Our reliance on administrative data entails a potential liability: we miss extrajudicial informal evictions that may have occurred over this period. Collecting data on informal evictions is notoriously difficult. Previous studies in Milwaukee and New York City indicate that the rate of formal-to-informal evictions varies across jurisdictions (Desmond and Shollenberger 2015; Collyer and Bushman-Copp 2019), but we know little about how it varies over time. Landlords might have more readily turned to informal evictions with access to the courts limited, but little or no evidence exists to support the hypothesis. If the “missing” eviction filings documented here were simply replaced by lock-outs and informal forced moves, the net benefits of pandemic renter protections would clearly deserve to be reevaluated. Likewise, our analysis of changes to eviction filing patterns during the pandemic is limited to the thirty-one cities analyzed and is not intended to be representative of all urban spaces in the United States. The findings of our study indicate the importance of attending to local variation (figure 2), and we hope that future research can expand the map to include other jurisdictions.

At a moment of generational instability and uncertainty, new policies and regulatory changes were rolled out that kept an extraordinary number of households out of court and safely in their homes. We find that 807,000 fewer eviction cases than usual were filed in just thirty-one cities between mid-March 2020 and December 31, 2021. The largest reductions were in majority-Black and low-income neighborhoods, signaling the relatively progressive benefits of economic and housing policies enacted in response to the pandemic. Strong eviction moratoria were instrumental in reducing eviction filing rates (figures 7 and 8). Despite landlord outcry, available evidence suggests that such policies had limited effect on rent collection rates, even in places where strong moratoria were in place for extended periods (Choi, Pang, and Goodman 2022; NMHC 2022). Even with moratoria in place, tenants routinely prioritized rent payment above almost all other expenses, going so far as to take on debt to keep current on rent (Keene et al. 2022; Manville et al. 2022). Landlords offset any losses to revenue by reducing expenses, resulting in increases, year over year, in their overall balances (Greig, Zhao, and Lefevre 2021). They also benefited from mortgage forbearance programs—some aimed at multifamily properties made permanent during the pandemic (Jensen 2021)—that resulted in record-low foreclosure rates (ATTOM 2021). Future analyses should attend to the costs and benefits of rental assistance, which may prove to be a more politically viable long-term policy option. Taken as a whole, the pandemic response makes clear that significant reductions to eviction filing rates are feasible. The challenges of establishing lasting reforms of this sort given the jurisdictional patchwork of civil law are significant, but so are the potential benefits to millions of renters nationwide who face the risk of eviction each year.

FOOTNOTES

↵1. The moratorium ended on July 24, 2020, but protections remained in place for thirty days.

↵2. An untold number of courts shut down in the early weeks of the pandemic, establishing de facto moratoria on eviction cases even in jurisdictions in which no de jure moratorium was established. Courts quickly reopened, however, many using video-conference technology to hold hearings remotely.

↵3. The exception is ERA, which was targeted to low-income renters. Treasury Department guidelines specified that recipient households needed to fall at or below 80 percent of area median income. Over the course of 2021, nearly two-thirds of all ERA applicants (64 percent) were from households with income below 30 percent of area median income (U.S. Department of the Treasury 2022).

↵4. In four court systems—Allegheny County, Pennsylvania, Travis County, Texas, Richmond, Virginia, and New York, New York—we rely on zip codes rather than exact defendant addresses. In New York, we do not observe defendant names.

↵5. This sample was not designed to provide robust generalizability nationwide. Notably, coverage of Western jurisdictions is limited, extending only as far West as Las Vegas, Nevada, and we do not include any sites that never implemented an eviction moratorium. In table 1 of the online supplementary materials we assess characteristics of ETS cities included in analyses here relative to metro areas nationwide and to the United States as a whole (see https://www.rsfjournal.org/content/9/3/186/tab-supplemental).

↵6. For details on the calculation of denominators for these rate estimates, see Hepburn et al. 2020b.

↵7. Researchers have used similar methods and variation in the timing of these policies to estimate the effects of eviction moratoria on health outcomes, such as COVID-19 incidence and mortality or mental health indicators (Leifheit, Linton, et al. 2021; Leifheit, Pollack, et al. 2021).

↵8. Information on state and local moratoria were collected using legal mapping and policy surveillance techniques (Benfer and Koehler 2022). We assign a site’s moratorium level based on the maximum strength of an order in the geography, enacted for the majority of a given week. For example, if St. Louis County has a strong moratorium for four of seven days of a given week and St. Louis City only has a weak moratorium during that time, we define St. Louis as having a strong moratorium. Unemployment rate data comes from Federal Reserve Economic Data and the Bureau of Labor Statistics. Data on ERA distribution comes from the National Low Income Housing Coalition’s ERA Dashboard, and represents the maximum percentage of ERA distributed among all programs available in a given site.

↵9. Results analyzing the effects of any moratorium are presented in the online supplementary materials.

↵10. For more, see the online supplementary materials.

↵11. None of the EFR estimates presented here correct for serial eviction filings—cases filed repeatedly against the same household at the same address over a series of months (Leung, Hepburn, and Desmond 2021).

↵12. Neighborhood racial-ethnic majority and median incomes were determined on the basis of ACS five-year estimates from 2015 to 2019 for the full population (not just those living in rental housing).

↵13. Estimates for the denominators for filing rates are based on ACS five-year data from 2014 to 2018 in Public Use Microdata Areas (for more information, see Hepburn, Louis, and Desmond 2020b).

↵14. The sample comprises thirty rather than thirty-one cities because New York City is excluded from these analyses. We do not collect defendant names in New York.

↵15. In these analyses, we include filings from January 5, 2020, through January 1, 2022, in order to start and end our analysis period at the bookends of calendar weeks. Unlike in our descriptive analyses, we do not begin our period of analysis on March 15, 2020.

↵16. Sites that never enacted a strong moratorium and sites that switched on and off during this period are excluded from the analysis. Within this period, the federal CARES Act moratorium expired and the CDC moratorium began. Though time fixed effects are included in these models to control for such site-invariant conditions, results are robust to further limiting the period to before the expiration of the CARES Act. Only the unemployment rate covariate is included in these regressions.

↵17. An assumption made in this reverse-DID specification is that effects of a moratorium do not carry over to future untreated periods.

↵18. In the supplementary materials, we exploit the staggered expiration of expanded UI benefits between May and December 2021 to conduct a similar analysis, controlling for county-level unemployment rate, strength of state/local moratorium, and ERA distribution. We find little or no effect of the cessation of these benefits.

- © 2023 Russell Sage Foundation. Hepburn, Peter, Jacob Haas, Nick Graetz, Renee Louis, Devin Q. Rutan, Anne Kat Alexander, Jasmine Rangel, Olivia Jin, Emily Benfer, and Matthew Desmond. 2023. “Protecting the Most Vulnerable: Policy Response and Eviction Filing Patterns During the COVID-19 Pandemic.” RSF: The Russell Sage Foundation Journal of the Social Sciences 9(3): 186–207. DOI: 10.7758/RSF.2023.9.3.08. Support for the Eviction Tracking System is provided by the Russell Sage Foundation, the C3.ai Digital Transformation Institute, and the Pew Charitable Trusts. The Eviction Lab is supported by the JPB and Bill & Melinda Gates Foundations, the Chan Zuckerberg Initiative, and the Eunice Kennedy Shriver National Institute of Child Health & Human Development of the National Institutes of Health (NIH) under Award No. P2CHD047879. Direct correspondence to Peter Hepburn, at peter.hepburn{at}rutgers.edu. 618 Hill Hall, 360 Dr. Martin Luther King Jr. Blvd., Newark, NJ 07103, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.