Abstract

The federal government allocated an unprecedented level of funding to develop emergency rental assistance programs to help vulnerable low-income renter households remain housed during the COVID-19 pandemic. Using panel data from two waves of applicant surveys joined with administrative data, this article analyzes the impact of Phase 1 of the City of Philadelphia’s COVID-19 Emergency Rental Assistance Program and asks how emergency rental assistance affected households in their rent arrears, rent-related debt, and mental health. Analysis shows that receiving emergency rental assistance was associated with lower arrears, a lower probability of rent-related debt, and a lower probability of experiencing frequent debilitating anxiety. The findings suggest that the initial rent relief provided crucial support for households in terms of financial and mental well-being but also underscore that housing affordability challenges that predated the pandemic cannot be addressed by an emergency rental assistance program created in response to a pandemic.

COVID-19 precipitated a public health crisis and forced a drastic economic shutdown in the spring of 2020. As a result, millions of Americans lost their jobs and incomes and were at risk of losing their homes; particularly hard hit were those working in the hospitality, tourism, and entertainment industries, many of whom were low-wage workers and disproportionately people of color (Schwartz 2021). In response, Congress passed and enacted the $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act, known as the CARES Act, in March 2020. The CARES Act restricted eviction filings (Hepburn et al. 2023, this issue), provided economic impact payments (Bitler, Hoynes, and Schanzenbach 2023, this issue), and increased and expanded the unemployment insurance benefits (Ravenelle and Knoble 2023, this issue), among other things. Many state and local governments established emergency rental assistance programs, with funding streams available for providing rental and utility assistance and preventing eviction and homelessness (Aiken et al. 2022). This article examines the short-term impact of one such emergency rental assistance program—the City of Philadelphia’s COVID-19 Emergency Rental Assistance Program (CERA)—on households’ financial and mental well-being.

Over the course of the pandemic, an unprecedented level of federal support was approved for states and municipalities across the country to develop and implement emergency housing programs with record speed. In addition to the CARES Act, Congress enacted the Consolidated Appropriations Act of 2021 in December 2020 and the American Rescue Plan Act in March 2021, which, combined, allocated a further $46.55 billion for emergency rental assistance (ERA) for low-income households, known as the ERA program. These programs were intended to stabilize households facing housing insecurity during the pandemic and mitigate the short- and long-term effects of pandemic-related housing instability. However, given limited history of federal housing programs providing emergency assistance to renters during moments of national economic turmoil, the evidence base to inform the design of these programs was relatively scant.

This article is one of the first to present evidence of an emergency rental assistance program’s impact on households, addressing an important knowledge gap. It focuses on the first iteration of Philadelphia’s emergency rental assistance program. Phase 1, the first of four phases, received applications in May 2020 and disbursed just over $10 million to 4,257 households (City of Philadelphia 2022). We ask how Philadelphia’s emergency rental assistance program affected households in terms of their rent arrears, rent-related debt, and mental health. To answer this question, we use panel data constructed from two waves of surveys—the first, embedded in the emergency rental assistance application and administered in May 2020; and the second, a follow-up in March 2021—and program application data provided by the city, which included household demographic information and whether a household received the subsidy.

Our analysis of the panel data shows that receiving emergency rental assistance was associated with a lower level of rent arrears and with a lower likelihood of incurring rent-related debt. Furthermore, respondents who received the subsidy were less likely to experience debilitating anxiety. Our analysis suggests that the emergency rental assistance was indeed critical in reducing the impact of the pandemic on housing burdens and, in turn, had a significant positive impact on households’ financial and psychological well-being. Simultaneously, our results also highlight the unsurprising persistence of pre-pandemic difficulties that low-income renter households continued to face regardless of the emergency rental assistance, something the program was not designed, or could be expected, to ameliorate. We discuss the implications of these findings for emergency rental assistance as well as for housing policy more generally.

LITERATURE REVIEW AND BACKGROUND

The COVID-19 pandemic has both highlighted and amplified existing economic strains that low-income households face. Research consistently documents the severe economic fragility of households in the United States. For instance, many low- and moderate-income house-holds do not have enough savings to cover a $500 emergency (Brobeck 2008); one in four families have no retirement savings, and roughly four in ten have less than $750 (Mc-Kernan et al. 2016). Further, more than 25 percent of households in the 2009 TNS Global Economic Crisis survey could not cover an unexpected $2,000 cost in thirty days, and nearly half of Americans were financially fragile (Lusardi, Schneider, and Tufano 2011). In fact, in 2019, just before the pandemic, the Federal Reserve found that 37 percent of all adults could not cover an unexpected $400 expense and that nearly three in ten “were either unable to pay their monthly bills or were one modest financial setback away from failing to pay monthly bills in full” (Board of Governors of the Federal Reserve System 2020, 21, cited in Schwartz 2021, 381).

Households use a range of coping methods to survive financial shocks and precarity. For instance, households that face financial shocks often pursue a “pecking order” to cover expenses, with savings at the top. However, because many households do not have adequate savings, they then leverage other sources of financial support, such as family and friends and alternative forms of credit, including payday loans, to cope with risk (Lusardi, Schneider, and Tufano 2011). Although helpful and even important in moments of precarity, such financial support does not ensure economic security and mobility for low-income households (Henly, Danziger, and Offer 2005). Another coping method for unanticipated shocks to income is decreasing household consumption of goods and services, such as food (Aguiar and Hurst 2005); such reductions, however, may have material consequences for households’ well-being. In this context of widespread financial precarity and vulnerability to shocks, social programs and the safety net may play an important role in smoothing consumption and stabilizing households. For instance, unemployment insurance benefits have been associated with consumption smoothing benefits (East and Kuka 2015; Gruber 1997). Further, both anticipated and unanticipated changes to benefits—such as anticipated increases in social security and the unanticipated economic stimulus payments of 2008, respectively—have been shown to result in large changes in consumer spending (Stephens 2003; Parker et al. 2013).

Financial precarity translates into housing insecurity, as few households have enough savings to cover their housing costs for more than a few months in the event of an emergency. In addition to the financial fragility discussed, many renter households face high housing cost burdens; in 2018, nearly half of all renter households were paying more than 30 percent of their incomes on rent (Joint Center for Housing Studies 2020). Thus, with unexpected economic shocks like the pandemic, households—particularly those with the lowest incomes and fewest resources—are likely to find themselves not only severely financially strained but also susceptible to housing instability (McKernan et al. 2016; Morduch and Schneider 2017). Housing instability is associated with numerous negative consequences for both adults and children, including adverse health outcomes, reduced educational performance, and interference with employment (Harkness and Newman 2005; Pollack, Griffin, and Lynch 2010; Meltzer and Schwartz 2016; Newman and Holupka 2014; Been et al. 2010; Desmond and Kimbro 2015; Lubell, Crain, and Cohen 2007).

Households have coping methods to cover housing costs as well. Research shows that households often do all they can to pay rent and remain housed, including cutting back on basic needs such as food and clothing (Rosen et al. 2020). Indeed, a study by the Joint Center for Housing Studies, aptly titled “The Rent Eats First,” found that 62 percent of working-age renter households face high housing cost burdens according to the residual income approach, meaning that they are unable to afford a comfortable standard of living after paying rent and utilities (Airgood-Obrycki, Hermann, and Wedeen 2021). However, leveraging coping methods and trade-offs in household consumption decisions is often still not enough. A recent survey of more than twenty-five thousand renter households in Los Angeles found that, even after trading off a broad set of goods during the pandemic, including medical care, many households still could not pay their rent and were accumulating multiple forms of debt (Reina, Aiken, and Goldstein 2021).

These findings on housing insecurity can be grounded in the reality of federal housing policy in the United States. Put simply, the housing safety net in the United States is severely limited. Housing assistance for low-income households is not an entitlement, and demand far exceeds supply; estimates suggest that for every low-income renter household with a rental subsidy are as many as three to four who qualify but do not receive it (Schwartz 2021; Reina, Aiken, and Epstein 2021). However, deep subsidy programs are significantly beneficial for those households who are offered, and can use, the benefit. For example, rental assistance is associated with increased housing stability, increased food consumption, a reduction in household moves, and less likelihood of reporting low-quality housing and lack of housing-related autonomy (Mills et al. 2006; Schapiro et al. 2022).

COVID-19 Emergency Rental Assistance

In response to the pandemic and the subsequent economic shutdown in the spring of 2020, in which millions of Americans lost their jobs and incomes and were at risk of losing their homes, Congress enacted a series of bills. The $2.2 trillion CARES Act, enacted in March 2020, created a variety of programs, such as the economic impact payments, also known as the federal stimulus payments, enhanced and extended unemployment benefits, and an eviction moratorium. Emerging research on the effectiveness of these programs shows that the federal stimulus payments significantly reduced overall poverty rate as well as children’s poverty rate in 2020 (Bitler, Hoynes, and Schanzenbach 2023, this issue) and that the federal-, state-, and local-level eviction moratoria dramatically reduced eviction filings, especially in previously high-risk communities (Hepburn et al. 2023, this issue).

In regard to emergency housing programs, the CARES Act provided three main funding streams, including “$150 billion for the Coronavirus Relief Fund (CRF), administered by the U.S. Department of the Treasury (Treasury); $5 billion for the Community Development Block Grant CARES Act Program (CDBG-CV), administered by the U.S. Department of Housing and Urban Development (HUD); and $4 billion for the Emergency Solution Grant CARES Act program (ESG-CV), also administered by HUD” (Aiken et al. 2022, 4). By April 2021, the National Low Income Housing Coalition (NLIHC) had identified 391 emergency rental assistance programs funded primarily by the CARES Act, accounting for approximately $4 billion, some of which also covered mortgage assistance (Aiken et al. 2022). The Consolidated Appropriations Act of 2021, enacted in December 2020, and the American Rescue Plan Act, enacted in March 2021, allocated a further $46.55 billion ($25 billion and $21.55 billion, respectively) specifically for emergency rental assistance for low-income households. This subsequent ERA program could be used by state and local governments to provide financial assistance for rent and utility arrears, future rent and utility costs, and other housing-related expenses. Crucially, as the timeline from the CARES Act to the ERA program illustrates, most funding for emergency rental assistance was not available to municipalities until roughly the early months of 2021, nearly eleven months after the pandemic shut down the country in March 2020. As a result, initial programs launched in 2020 were often forced to balance a high level of need with an insufficient level of funding, as well as uncertainty about the availability of future funding and, in many cases, the challenges of developing a program from scratch.

The City of Philadelphia’s COVID-19 Emergency Rental Assistance Program (also known as PHLRentAssist) was one of the earliest to launch in the country (Reina, Aiken, Verbrugge, et al. 2021). The economic shutdown of the pandemic had struck a city with an already large share of low-income residents at risk of, or experiencing, financial precarity and housing instability. In 2018, approximately 40 percent of Philadelphia’s households were housing cost burdened, in line with many other major U.S. cities. However, notably, Philadelphia’s housing affordability issues owed more to low income levels than high housing prices; no other city “ha[d] a higher proportion of cost-burdened households with low incomes than Philadelphia” among the ten most populous cities in the country. Indeed, nearly 90 percent of renters with incomes below $30,000 per year were cost burdened, 68 percent spending more than 50 percent of their incomes on housing (Pew Charitable Trusts 2020, 1). Moreover, Philadelphia had a pre-pandemic baseline eviction filing rate of 7.6 percent—among cities with filing rates as low as 2.7 percent (Boston, Massachusetts) and as high as 24.8 percent (Richmond, Virginia) (Hepburn et al. 2023, this issue)—and, frequently dubbed the “poorest big city” in the United States, it had a poverty rate of 26 percent in 2017 (Pew Charitable Trusts 2019).

In May 2020, Philadelphia’s Department of Planning and Development opened its application portal for phase 1 of CERA. Based on initial funding levels, the city estimated it could support approximately four thousand households and proposed a lottery for the receipt of assistance should there be more applicants. Within a week of opening, the program received more than ten thousand applications, and the city conducted a randomized lottery to determine which households would receive the benefit. Households were notified of their status in early June, at which point the city began to process payments. Some households were waitlisted, and a subset eventually was recontacted and offered assistance by the end of 2020. All selected tenants received rental assistance for up to three consecutive months, up to $2,500 total. For this phase 1 of the CERA, the city disbursed $10,071,689.00 in assistance by December 2020, which funds came from the CARES Act CDBG-CV funding stream.

To be eligible for phase 1, the applicant needed to meet the following criteria: rent an apartment or a house in Philadelphia, have a valid and current written lease signed by the landlord, and have lost income because of COVID-19. Assistance was limited to renters whose household earned 50 percent or less of the area median income; for a four-person household, the limit was $48,300. Further, for a tenant to participate, their landlord was required to enter into an agreement with the city, committing to four actions, among other things: first, to apply all of the CERA to their tenant’s monthly rent due in the months of May, June, and July of 2020, reducing the monthly rent by the amount of the CERA; second, to allow the tenant a six-month repayment period for any unpaid rent, commencing from the latest date the CERA funds were received by the landlord; third, to not pursue eviction of the tenant for nonpayment of rent for six months following the latest date the CERA funds were received by the landlord; and, fourth, to not charge any late fees or penalties on unpaid monthly rent from April or May of 2020, or at any time while receiving the CERA funds.

Phase 2 accepted applications between July and November of 2020 and drew funds from the CARES Act CRF, passed through the Commonwealth of Pennsylvania as part of Pennsylvania’s Rent Relief Program. It reached 6,596 households, providing up to $1,500 per month per applicant, and disbursed $31,739,593.00 total. Phase 3, also drawing from the CARES Act CRF, did not accept new applications but reached 5,149 households that had applied to prior phases but that were not eligible due to landlord nonparticipation or lack of response; nearly $24 million were disbursed, and applicants were eligible for up to $1,500 per month for up to six months. Finally, phase 4, using funds from the ERA Program and funds through the Pennsylvania’s Emergency Rental Assistance Program, began accepting applicants in April 2021 and, as of October 2022, has supported 30,210 households, disbursing $230,493,163.09 in assistance so far. Average amount and duration of rental assistance for phase 4 have been $7,171.62 and eight months, respectively. In total, through the four phases, the City of Philadelphia has served 46,212 low-income renter households and disbursed $296,121,929.09 in emergency rental assistance (and utility assistance for phase 4) as of October 2022 (City of Philadelphia 2022).

This study focuses on the initial round, phase 1, of the CERA, which provided households up to $2,500 total for up to three months of rent.

DATA AND METHODS

This article uses panel data constructed with data from two rounds of applicant surveys administered approximately ten months apart: the baseline survey in May 2020 and the follow-up survey in March 2021. The baseline survey was embedded into the city’s application process for the emergency rental assistance such that those applying to the CERA could, after completing their application on the city’s website, follow a link and fill out the survey. The survey was designed to take ten to fifteen minutes and featured questions that dealt with a wide range of topics, including current and past housing situation, employment history and finances, childcare, and general mental health. The survey recorded 3,887 responses, of which 2,620 (67.4 percent of the survey data) could be joined to the application data provided by the City of Philadelphia.1 The follow-up survey covered similar topics and some identical questions as the baseline survey and recorded 932 responses. In all, 594 respondents with application data had responded to both the baseline and the follow-up surveys. Thus, in summary, we have an analysis sample of 594 observations, 42.3 percent of whom (251 respondents) received the CERA and 57.7 percent of whom (343) did not.

Explanatory Variables

Table 1 summarizes the descriptive statistics of several contextual variables, including the survey respondents’ race and ethnicity, family situation, employment status, and receipt of other forms of COVID-19-related government assistance. The shares are further broken down by the CERA status, each cell containing the column-wise proportions.

Descriptive Statistics of Independent Variables

As table 1 shows, non-Latinx Black households were the largest ethnoracial group in the sample (56.4 percent). They were followed by Latinx households (17 percent) and non-Latinx Whites (15 percent). The group categorized as Other—Pacific Islander, American Indian, and multiracial—came next (7.9 percent). Asian households were the smallest group (only 3.7 percent). The column-wise proportions for the CERA “Received” column demonstrate that, for the most part, the ethnoracial composition of those who received the CERA reflects the overall ethnoracial composition of the sample. However, some groups did have slightly higher instances of receiving the subsidy than others. For instance, non-Latinx Whites, who made up 15 percent of the sample, represented 16.7 percent of those who received the emergency rental assistance, whereas non-Latinx Black and Latinx respondents were underrepresented relative to the study sample composition, 55 percent to 56.4 percent and 16.3 percent to 17.0 percent, respectively.

The majority of the survey respondents in our sample (61.8 percent) had children under eighteen. No significant discrepancy is apparent between the with-children and without-children groups in terms of whether they received the CERA. Individuals who responded that they were currently unemployed constituted 64.3 percent of the sample and were slightly underrepresented among those who received the CERA relative to the sample composition. As for whether the respondent or anyone in their household received other kinds of government assistance, 27.8 percent said they received unemployment insurance benefits in February 2021, and 45.8 percent said they had received a federal stimulus payment in 2021. Those who received other forms of subsidy were slightly overrepresented among those who received the CERA; those who received unemployment insurance benefits and the federal stimulus payments made up 31.1 percent and 47.0 percent, respectively, of those who received the CERA, both figures slightly larger than the aforementioned shares in the overall sample.

Having noted these discrepancies, we check for any statistical imbalance between the treatment and control groups and find that they are balanced across these observable characteristics.2

Outcome Variables

To ascertain the impact of the CERA on alleviating financial and psychological burdens faced by tenants during the COVID-19 pandemic, we focus on the following questions from the follow-up survey, from which we derive our dependent variables:

Are you behind on rent? If so, what is the total amount of rent that you owe?

Have you borrowed money to pay rent?

Over the last two weeks, how often have you been bothered by not being able to stop or control worrying?

Have you consumed less food since November 2020 to make life more affordable?

Have you gone without medicine or seeing a doctor since November 2020 to make life more affordable?

Table 2 presents the descriptive statistics for the key outcome variables and their breakdown by the CERA status.

Descriptive Statistics of Outcome Variables

The majority of the sample (60.8 percent) responded that they were behind on rent as of the follow-up survey, months after the disbursement of the CERA, and, descriptively, the receipt of the grant does not appear to have made a significant difference on whether a household is behind on rent. However, comparing the median dollar value of the amount owed in rent for the subset of the sample respondents who were behind on rent shows that the CERA may have been instrumental in reducing the amount of back rent. Among the 361 respondents who were behind on rent, the median dollar amount owed was $2,400; the median for those who received the CERA was $2,100 (mean = $2,394.55), relative to $2,550 for those who did not (mean = $3,169.11). The majority of the sample (57.6 percent) had also borrowed money to pay rent, and a comparison of shares by CERA status suggests that the subsidy may have affected the outcome. Of those who received the CERA, only 51.8 percent borrowed money to cover rent compared to those who did not receive the CERA (61.8 percent).

As for being unable to stop or control worrying in the last two weeks, 26 percent of the respondents answered that they were bothered by worrying uncontrollably “nearly every day”; 19.9 percent responded with “more than half the days”; 37.5 percent worried “several days”; and 16.5 percent indicated “not at all.” These responses to the follow-up survey reflect an overall worsening in the respondents’ mental health as the COVID-19 pandemic carried on. For instance, between the baseline survey and the follow-up survey, the share of respondents who selected “not at all” decreased from 27.3 percent to 16.5 percent, and the share of respondents who chose “nearly every day” increased from 23.2 percent to 26 percent. With respect to CERA status in the follow-up survey, the distribution of responses among those who received the CERA is more concentrated on the “less worried” end of the spectrum (that is, “not at all” and “several days”) relative to the distribution of responses among those who did not receive the CERA, which is more skewed toward the “more worried” end of the spectrum (“more than half the days” and “nearly every day”), suggesting that the CERA may have helped in renters’ mental health.

The next set of outcome variables concerned whether respondents were forced to adjust essential consumption decisions to keep life affordable. Regarding food consumption, nearly 40 percent reported that they had resorted to eating less, and receipt of the CERA does not appear to have made a difference. Regarding going without medicine or seeing a doctor, almost 25 percent indicated that they had chosen not to seek medical care to save money, and, again, the CERA does not seem to have affected this outcome.

As mentioned, the baseline and follow-up surveys contained several identical outcome-based questions. Where possible, we test for differences in the treatment and control groups at pre-treatment baseline, so that, provided no difference, we have greater confidence that the effects observed in our models are a function of the treatment. Of our dependent variables, the outcome variables for which we have matching questions in the baseline and follow-up surveys are the following three variables: “over the last two weeks, bothered by not being able to stop or control worrying,” “reduced food consumption since November,”3 and “went without medicine or seeing a doctor since November.”4 For the outcome variables “behind on rent” and “borrowed money to pay rent,” we test the closest proxy in the baseline survey: “needed money for housing expenses like rent, mortgage, or security deposit.” For all of the outcome variables, the treatment and control groups do not exhibit any statistically significant difference at baseline (p > .05).

Regression Analyses

We use three regression techniques to test the relationship between the receipt of the CERA and our five outcomes of interest. First, for the continuous dependent variable, “amount owed in rent,” because the amount owed in rent is observable only for those respondents behind on rent, we assign those who are not in rental arrears zeros and use quantile regression to account for this sample selection bias and the variable’s skewed distribution from the added zeros.5 For the three binary dependent variables (“borrowed money to pay rent,” “reduced food consumption,” and “went without medicine or seeing a doctor”), we use logistic regression to see if receiving the CERA is associated with these outcomes. Finally, we use ordinal logistic regression to test whether receiving CERA is associated with a lower likelihood of experiencing more frequent worrying and anxiety (in ascending order, “not at all,” “several days,” “more than half the days,” and “nearly every day”).

For all of the models, we first start with a basic model with just the CERA status as the independent variable; then control for baseline conditions where identical questions from the baseline survey enable us to incorporate pre-treatment responses; then control for basic demographic and socioeconomic characteristics, such as race and ethnicity, the presence of children under eighteen, and employment status; and finally include other forms of government assistance that the respondents received during the COVID-19 pandemic (that is, the unemployment insurance benefits and the federal stimulus payment).

FINDINGS

In this section, we discuss the results from our regression models for the five outcome variables. For the logistic regression models, we provide the model results, in which the coefficients signify the log odds, followed by a separate table showing the average marginal effects (in probability) for statistically significant variables for ease of interpretation.

1. “Are you behind on rent? If so, what is the total amount of rent that you owe?”

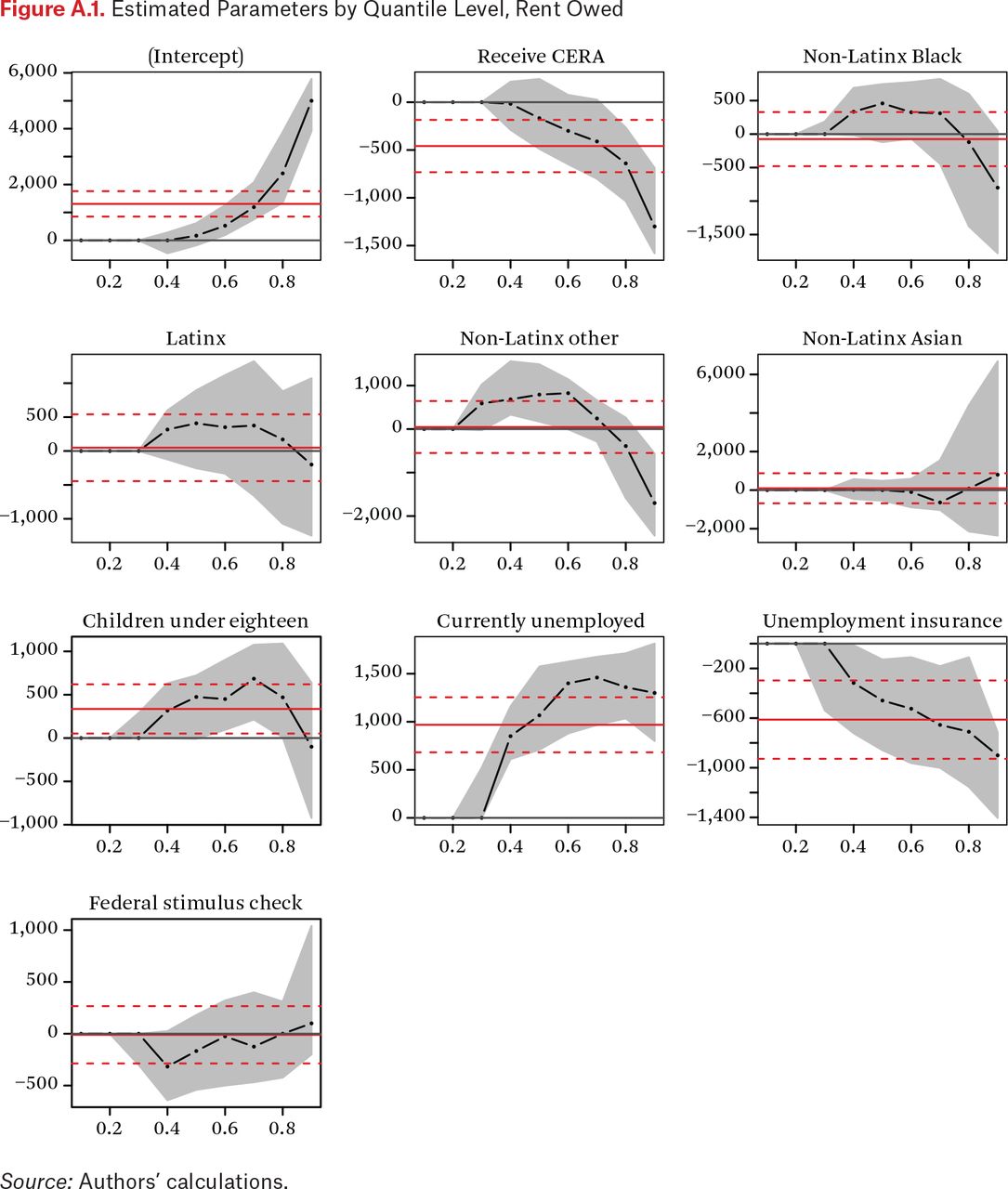

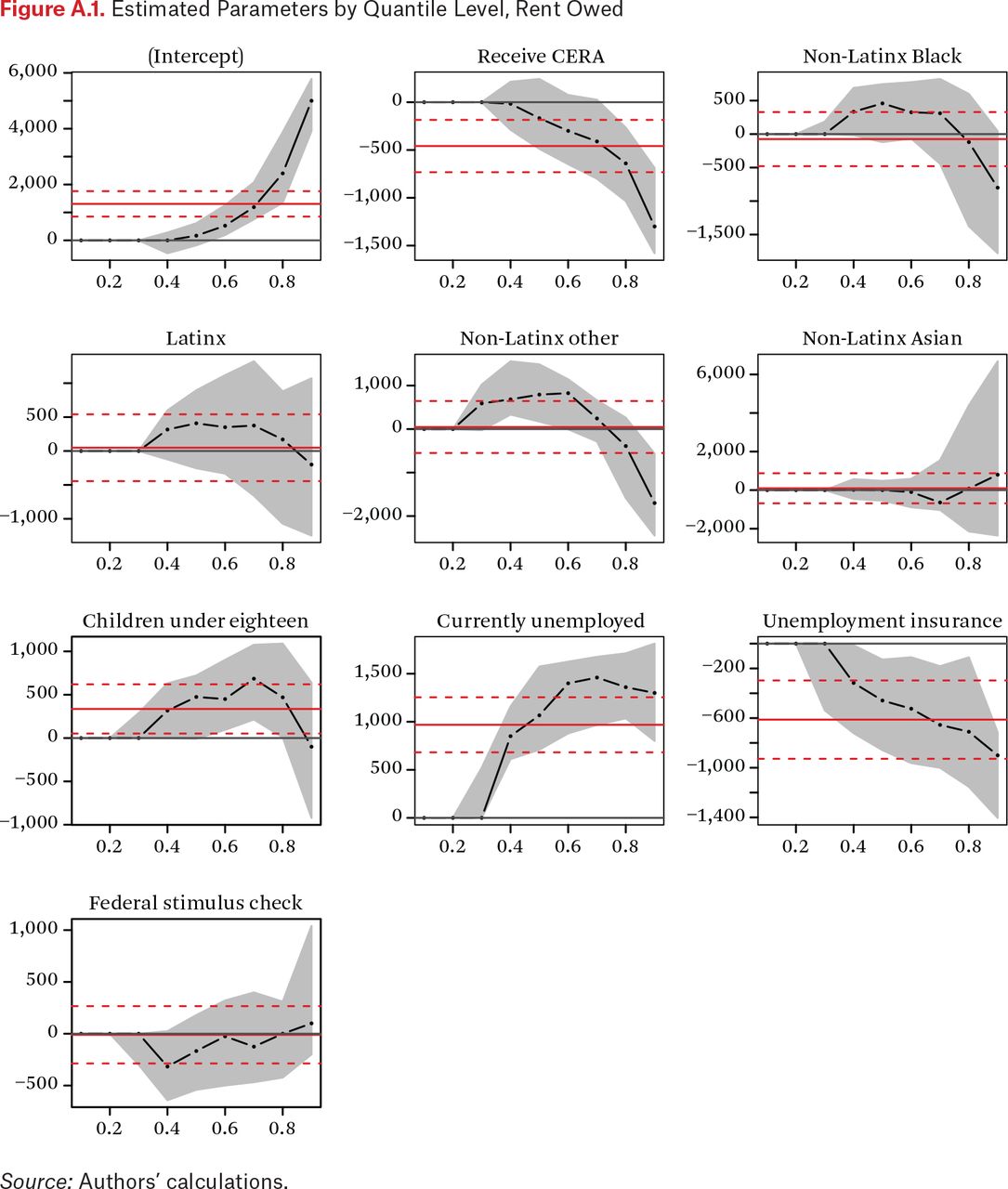

Table 3 illustrates the results from the quantile regression model estimating the effect at the 75th percentile of the dependent variable, “amount of rent owed.” As mentioned, those who responded that they were not currently behind on rent were assigned zeros. Models 1, 2, and 3 consistently show that receiving the CERA predicts owing less in back rent. After controlling for demographic and socioeconomic variables, as shown in model 3, the CERA is associated with a $525 decrease in the amount of rent owed. Being currently unemployed is associated with a $1,275 increase in the amount of rent owed. Notably, receipt of unemployment benefits is also associated with a $575 reduction in the amount of rent owed, an effect size that is greater than the CERA. The models show that, as observed at the 75th percentile, receiving the CERA is associated with a significantly lower amount of back rent owed (for a plot of the coefficient values along the quantile levels, see figure A.1).

Quantile Regression Model (tau = 0.75)

2. “Have you borrowed money to pay rent?”

Table 4 summarizes the logistic regression model outputs for “borrowed money to pay rent.” Model 1 shows that receiving the CERA is statistically significantly associated with a lower likelihood of borrowing money to pay rent (coefficient = –0.410, p < .05); this equates to an average marginal effect of reducing the probability of incurring rent-related debt by 0.10 (see table 5). Model 2 again illustrates that the CERA is a statistically significant predictor (coefficient = –0.394, p < .05) for not borrowing money to cover rent; neither family status nor unemployment status is significant. Model 3 affirms the effect of the CERA (race is no longer significant controlling for other forms of government assistance). The results in tables 4 and 5 consistently demonstrate that households that received the CERA were less likely to borrow money to cover rent.

Logistic Regression Results, Borrowed Money

Average Marginal Effects for Significant Variables, Borrowed Money

3. “Over the last two weeks, how often have you been bothered by not being able to stop or control worrying?”

Table 6 shows the results from the set of ordinal logistic regression models that were leveraged to address the ordinal nature of the categorical dependent variable, whose levels in ascending order are “not at all,” “several days,” “more than half the days,” and “nearly every day” in response to the survey question, “Over the last two weeks, how often have you been bothered by not being able to stop or control worrying?” We regress the outcome variable on the respondents’ answers to the same question in the baseline survey, in addition to the key independent variable of CERA status and the usual control variables of race and ethnicity, family status, and other forms of government assistance. Thus, we are able to control for the respondents’ pre-treatment conditions in these models.

Ordinal Logistic Regression, Worrying

Overall, across models 2 through 4, receiving the CERA is statistically significantly associated with reporting less frequent uncontrollable worrying in recent weeks. For instance, model 2 shows that, for respondents who received the CERA, the odds of responding that they have been more worried than not (“several days,” “more than half the days,” or “nearly every day” versus “not at all) is 0.70 times (coefficient = –0.357, p < .05, e^(–0.357) = 0.70) that of respondents who did not receive the CERA. Table 7, which lays out the average marginal effects for each outcome level from “not at all” to “nearly every day,” helps with the interpretation. Receiving the CERA, on average across the sample, is associated with an increase in the probability of reporting “not at all” by 0.04 and reporting “several days” by 0.05 relative to not receiving it; it is associated with a decrease in the probability of reporting “more than half the days” by 0.02 and reporting “nearly every day” by 0.06.

Average Marginal Effects for Significant Variables, Worrying

Model 2 also illustrates that those who responded with a greater frequency of worrying in the baseline survey are more likely to report a greater frequency of worrying again in the follow-up survey. For instance, for those who responded that they had been bothered by not being able to stop or control worrying “nearly every day” in the baseline survey, the odds of responding that they have been more worried than not are 10.3 times (coefficient = 2.334, p < .01, e^(2.334) = 10.3) than of those who had responded “not at all” in the baseline survey. Put in terms of probability, as shown in table 7, those who experienced debilitating anxiety “nearly every day” in the baseline survey have a 44-point higher probability of responding “nearly every day” in the follow-up survey than those who did “not at all.” Models 3 and 4 affirm the preceding findings and add that unemployment is a significant predictor of more anxiety. Other forms of government assistance are not statistically significant.

Although the strongest predictor of debilitating worrying in recent weeks appears to be the respondent’s mental state as recorded in the baseline survey, we find that receipt of the CERA is a consistently significant predictor of a lesser degree of worrying.

4. “Have you consumed less food since November 2020 to make life more affordable?”

Table 8 summarizes the logistic regression results for “reduced food consumption since November 2020.” Here again, we can control for the respondents’ pre-treatment condition of whether they had reduced their food consumption in the past two years to make life more affordable. Model 1 shows that receiving the CERA is not a statistically significant predictor of (not) reducing food consumption. Model 2 also illustrates that the CERA did not have any effect. However, reporting a history of reducing food consumption to get by is a statistically significant predictor of reducing food consumption at the time of the follow-up survey (coefficient = 0.921, p < .01): a respondent who has previously reduced food consumption to make life more affordable has a greater probability of reporting that they have done so recently, by 0.21 (see table 9).

Logistic Regression Results, Food Consumption

Average Marginal Effects for Significant Variables, Food Consumption

Model 3 affirms these findings and, in addition, shows that those respondents with children under eighteen are less likely than those without to reduce food consumption to cope financially (coefficient = –0.607, p < .01); their probability of doing so, on average, is 0.13 lower than those who do not have children under eighteen, which suggests that reducing food consumption may not be a viable option for households with young children. Finally, according to model 4, having received a federal stimulus payment in 2021 is statistically significantly associated with a lower likelihood of consuming less food for financial reasons (coefficient = –0.427, p < .05), translating to an average marginal effect on probability of –0.09. Thus, although the CERA did not affect food consumption decisions, the federal stimulus payment did, which corroborates the finding that the federal economic impact payments led to a reduction in poverty (Bitler, Hoynes, and Schanzenbach 2023, this issue). Most important, whether someone had resorted to eating less food in the past was the strongest predictor of whether they were resorting to the same, illustrating that deep, persistent financial hardships are not ameliorated by a one-time rental assistance.

5. “Have you gone without medicine or seeing a doctor since November 2020 to make life more affordable?”

Table 10 presents the logistic regression results from regressing “went without medicine or seeing a doctor” on the same set of variables as table 8, the only difference being the replacement of the corresponding control variable from the baseline survey (“have you gone without medicine or seeing a doctor in the past two years to make life more affordable?”). Models 1 through 4 show that none of the variables are statistically significant, other than whether someone had indeed made such a decision due to financial reasons in the past; if they had, their probability of resorting to going without medical care again is on average greater by 0.31 to 0.33 than those who had not (see table 11). These results emphasize, again, that deep-cutting, entrenched, and systemic issues remain after the one-time or short-term assistance. Contending with them was, of course, not the goal of the COVID-19 emergency rental assistance programs; nevertheless, policymakers must grapple with what the COVID-19 pandemic and the CERA experience revealed about the state of the housing and broader social safety net.

Logistic Regression Results, Medicine

Average Marginal Effects for Significant Variables, Medicine

Limitations

This study has several limitations. First, our analysis sample is a subset of the more than ten thousand households that applied to receive the CERA and the 4,257 households that received it. The baseline survey captures 2,620 of those who applied and could be joined to administrative data, and between the baseline survey and the follow-up survey, the retention rate was 22.7 percent, resulting in our analysis sample of 594 respondents. Furthermore, even though no differences between the study sample and the baseline survey sample are statistically significant, some differences between the study sample and the all-applicant data, though minor, are.6 For a comparison of the study sample with the baseline survey data and the all-applicant data, see tables A.1 and A.2.7

In addition, comparing the figures with those derived from the 2015–2019 American Community Survey (ACS) Public Use Microdata Sample (PUMS) for low-income8 renters in Philadelphia, it is evident that all of our data—the study sample and the pool of applicants—diverge from the city’s demographics. We note the divergence, but it is not surprising. Research shows that not all eligible households apply to housing assistance programs in general, and variation by race and ethnicity is also considerable, in Philadelphia in particular (Reina and Aiken 2021). Thus, although our data are not representative of all low-income renters in Philadelphia, they likely are of those residents who are in need and are likely to engage in, and be reached by, government assistance programs.

Finally, although we exploited the random assignment of households into treatment and control groups via the lottery the city conducted, the assignment was not without its limitations because the treatment assignment and the actual treatment were not delivered simultaneously to all households. Households that won the lottery were notified at the same time, but some had to wait longer to receive the rental assistance because of obstacles such as document verification and landlord compliance. Further, households placed on the waiting list were also notified that they were wait-listed at that time, but some eventually received the rental assistance. These limitations could make our results a conservative estimate of the CERA’s effect. Regardless, the imperfect assignment means that the causality of our findings should be considered with caution.

DISCUSSION AND CONCLUSION

Our analysis suggests that Philadelphia’s rent relief program had significant positive effects on households. Specifically, receiving the emergency rental assistance was associated with lower levels of rent owed (a $525 reduction in rent arrears at the 75th percentile), a lower likelihood of borrowing money for rent (a 9-point decrease in the probability of incurring rent-related debt), as well as a lower likelihood of reporting debilitating anxiety (a 4-point increase in the probability of reporting no uncontrollable worrying and a 7-point decrease in the probability of experiencing uncontrollable worrying nearly every day). The city’s emergency rental assistance was a much-needed subsidy that led to benefits, not only in housing-related outcomes but also in overall well-being. Given that our sample is balanced across the treatment and control groups in both observed household characteristics and stated responses to the baseline survey, these effects can be reasonably attributed to the CERA. Nevertheless, given the noted variations between the study sample and all households that applied and the divergence between the study sample and the low-income renter population in Philadelphia at large (tables A.1 and A.2), caution is needed in applying these findings to contexts beyond this study, such as to all renters.

Even though these findings are positive, this initial round of the city’s emergency rental assistance was by no means a panacea. Rent relief did not reduce the dire trade-offs households were making during the pandemic, such as surviving on less food or without medical care. In fact, baseline instances of households making trade-offs in the past were the most significant predictor of their odds of making the same trade-offs, which illustrates that many of these challenges predated the pandemic and require much bigger, deeper solutions. These findings are not surprising. The pandemic response programs were not designed to address long-standing challenges of housing affordability and financial fragility. Further, phase 1 of the city’s emergency rental assistance program consisted of a $2,500 subsidy, which represents just over two months of the median rent in Philadelphia ($1,042 according to the 2015–2019 ACS). Thus, despite being a significant sum in in-kind assistance, it likely was not enough to make substantial changes to household budgets during a time of economic and public health crisis. However, receipt of federal stimulus payments was associated with a lower probability of reducing food consumption (tables 8 and 9). This finding is significant and resonates with the conclusion that the near-universal economic impact payments reduced overall poverty rate (Bitler, Hoynes, and Schanzenbach 2023, this issue). Therefore, in assessing household well-being during this time, it is crucial to consider the unprecedented array of programs that provided support and might have been fungible across household spending and borrowing categories.

The findings in this study on phase 1 of Philadelphia’s Emergency Rental Assistance Program are important and contribute to the emerging body of research on emergency rental assistance. In Philadelphia, phases 2 through 4 reached more households and provided larger amounts in assistance through increased federal support and changes to program rules, such as direct-to-tenant assistance for those who were not eligible in phase 1 because of landlord nonparticipation or nonresponse (City of Philadelphia 2022). As a result, these later phases may be associated with even greater and more diverse sets of positive outcomes. Furthermore, more than three hundred state and local emergency rental assistance programs were developed with considerable flexibility within the outlines of the federal guidelines, adapting to local needs and capacity (Reina, Aiken, Verbrugge, et al. 2021; Reina, Aiken, Harner, et al. 2021). Thus, additional research on other localities’ emergency rental assistance programs and their impacts, as well as the later phases of the Philadelphia case, is sure to be instructive for future housing policy discussions.

The COVID-19 pandemic laid bare the broader systemic issues of housing and economic insecurity in the United States that predated 2020, including a lack of housing affordability and high levels of housing cost burden. This article shows that phase 1 of the City of Philadelphia’s rental assistance program had important, measurable benefits for recipient households, but it also highlights the long-standing challenges around housing affordability that cannot be addressed through an emergency response program.

Appendices

Estimated Parameters by Quantile Level, Rent Owed

Authors’ calculations.

Comparison of Study Sample

Chi-Square Test Results (p-values)

FOOTNOTES

↵1. The research team included an optional checkbox in the CERA application that enabled households to enroll in the study. If a household enrolled in the study, the research team could access the household’s application information. The City of Philadelphia provided administrative data for approximately 8,800 rent relief applicants, more than half of the total applicants.

↵2. We regress treatment (receipt of the CERA) on all of the variables in table 1 (race and ethnicity, children under eighteen, unemployed, unemployment insurance, and federal stimulus payments). The likelihood ratio chi-square test comparing the test model with a null model returned a p-value of .7954. Thus we find no signs of imbalance between treatment and control groups.

↵3. Equivalent question in the baseline survey was “Have you made any of the following adjustments in the past two years to make life more affordable? (Check all that apply).” The response option was “reduced total food consumption.”

↵4. The response option here was “went without medicine or seeing a doctor.”

↵5. Rather than using a technique that more explicitly deals with the sample selection bias, such as a Heckman two-stage model, we assign the value of 0 to those who do not owe back rent and use quantile regression to model the effect at the 75th percentile, which roughly corresponds to the mean of the nonzero values of rent arrears, for both simplicity and ease of interpretation.

↵6. The City of Philadelphia shared summary statistics for the all-applicant pool with the research team.

↵7. Chi-square tests run for the two pairs of datasets (that is, study sample and baseline survey data, study sample and all-applicant data) show that the study sample and the baseline are not statistically significantly different with regard to basic household characteristics—racial and ethnic composition and the percent of households with children under eighteen. The study sample does deviate from the all-applicant data for racial composition, resulting in a significant chi-square test result (p = .01458), although the percentages are descriptively proximate (for example, 58.1 percent Black in the study sample versus 52 percent Black in the all-applicant data; 19.9 percent White in the study sample versus 22 percent White in the all-applicant data). However, no differences based on percentage Latinx or percentage of households with children under eighteen between all three groups are significant.

↵8. Low-income was defined as households whose incomes do not exceed 80 percent of the median household income for the Philadelphia metropolitan statistical area.

- © 2023 Russell Sage Foundation. Reina, Vincent J., and Yeonhwa Lee. 2023. “COVID-19 and Emergency Rental Assistance: Impact on Rent Arrears, Debt, and the Well-Being of Renters in Philadelphia.” RSF: The Russell Sage Foundation Journal of the Social Sciences 9(3): 208–29. DOI: 10.7758/RSF.2023.9.3.09. The Stoneleigh Foundation and the Wells Fargo Foundation have generously supported this research. We thank them for their support but acknowledge that the findings and conclusions presented in this paper are those of the authors alone and do not necessarily reflect the opinions of these funders. Vincent J. Reina’s contributions to this article occurred prior to his taking a leave of absence from the University of Pennsylvania to join the Biden-Harris administration and therefore reflect his personal views only. Direct correspondence to: Yeonhwa Lee, at yeonhwa{at}upenn.edu, 127 Meyerson Hall, 210 S. 34th Street, Philadelphia PA 19147, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.