Article Figures & Data

Figures

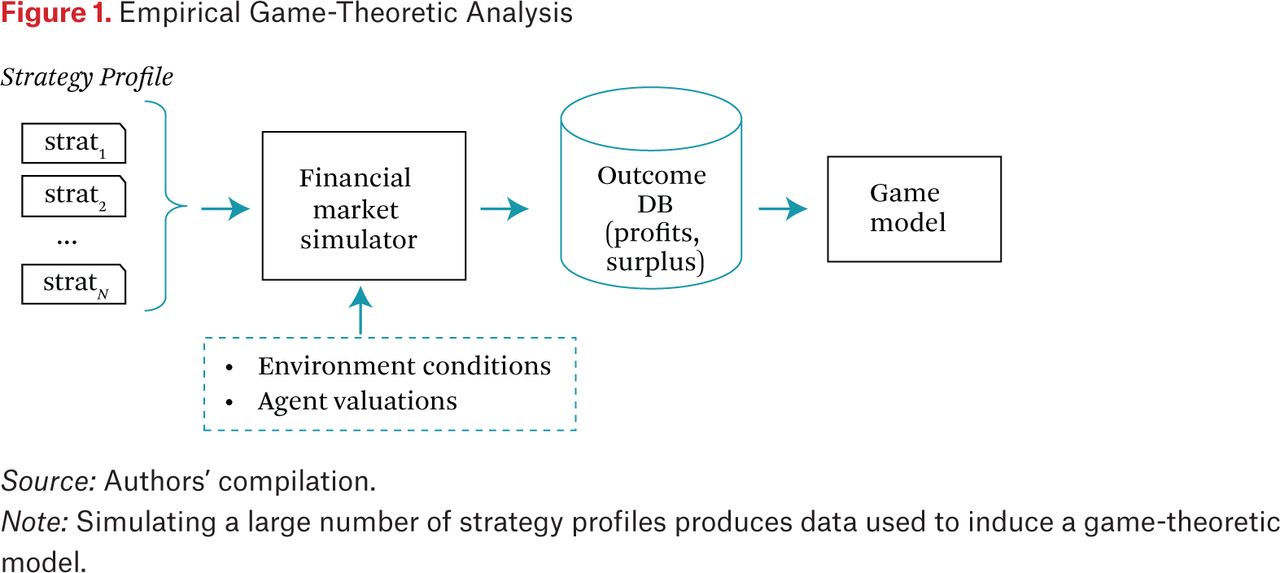

- Figure 1.

Empirical Game-Theoretic Analysis

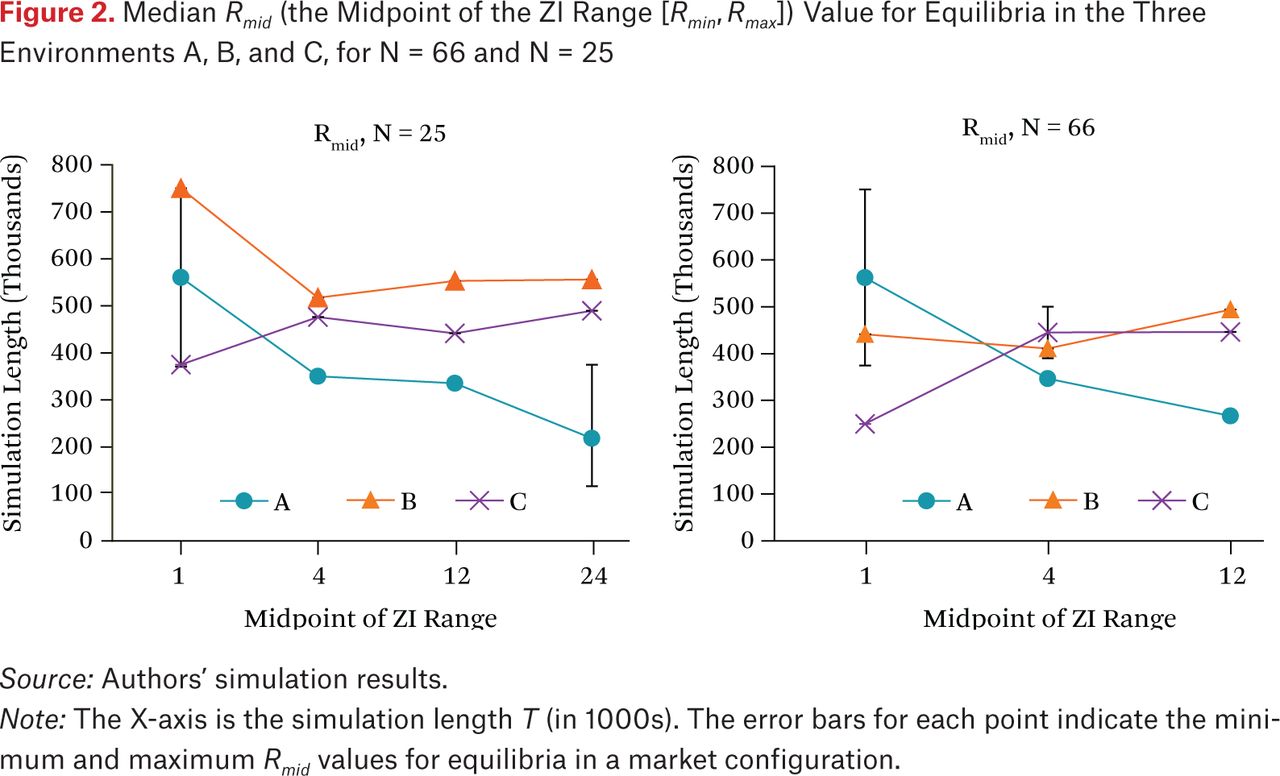

- Figure 2.

Median Rmid (the Midpoint of the ZI Range [Rmin, Rmax]) Value for Equilibria in the Three Environments A, B, and C, for N = 66 and N = 25

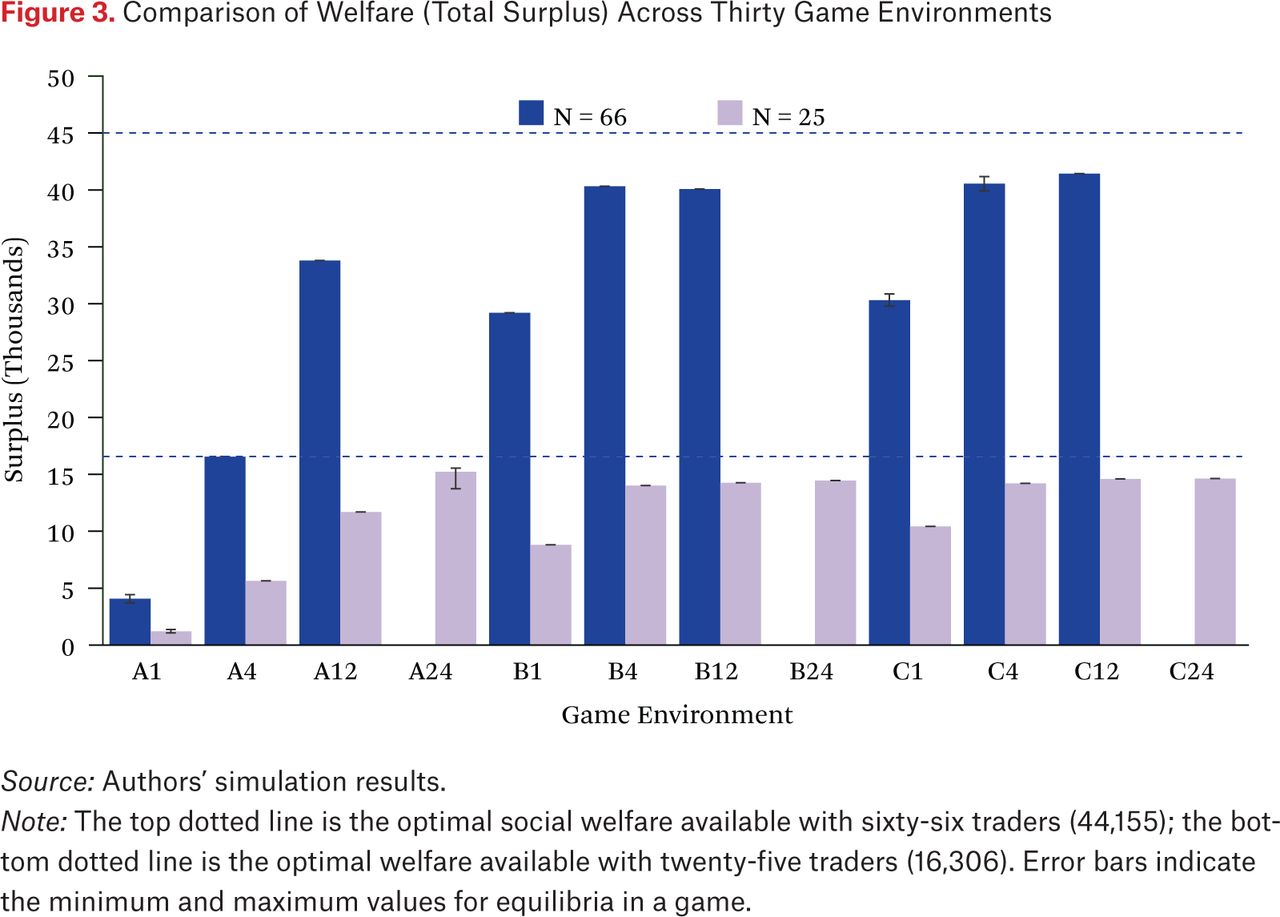

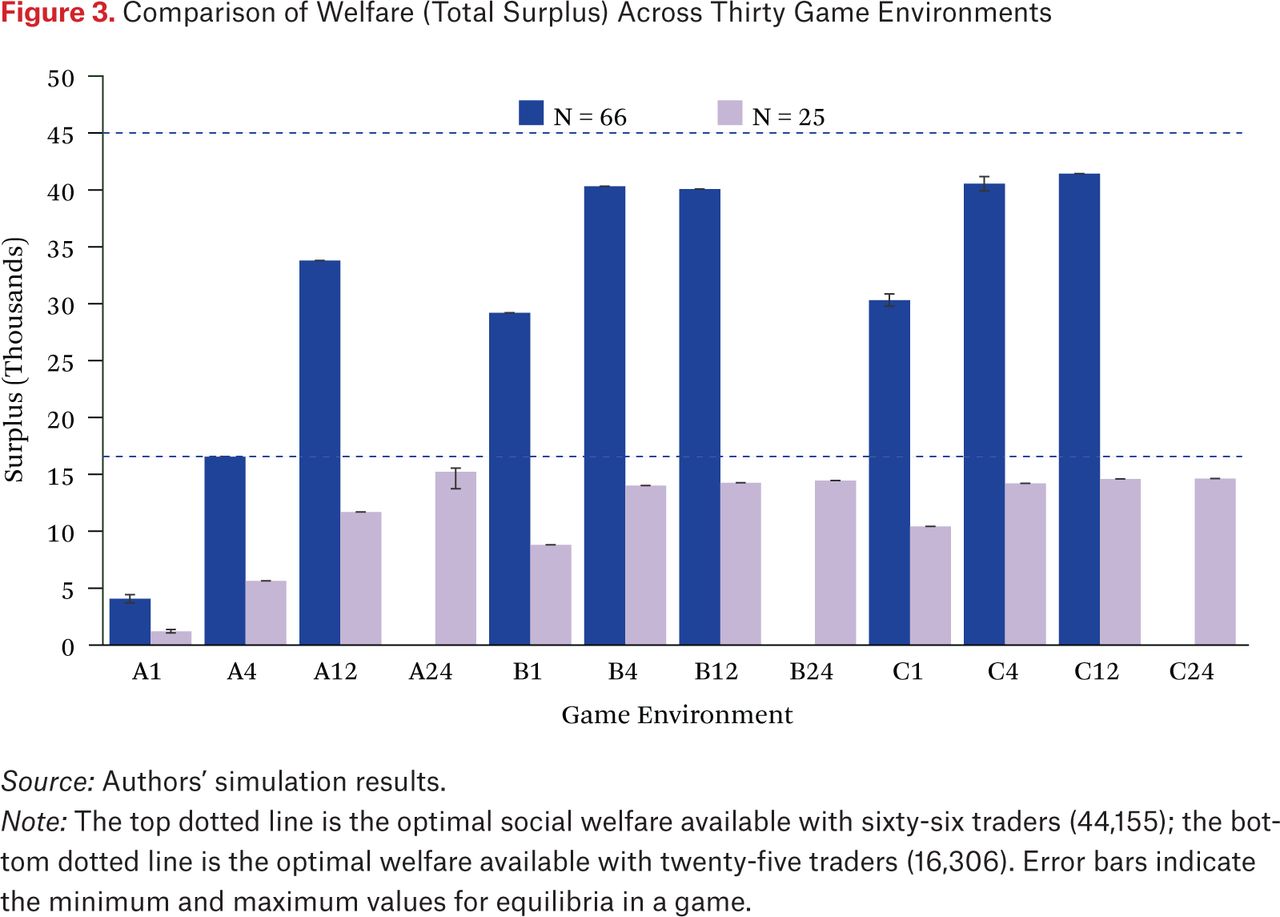

- Figure 3.

Comparison of Welfare (Total Surplus) Across Thirty Game Environments

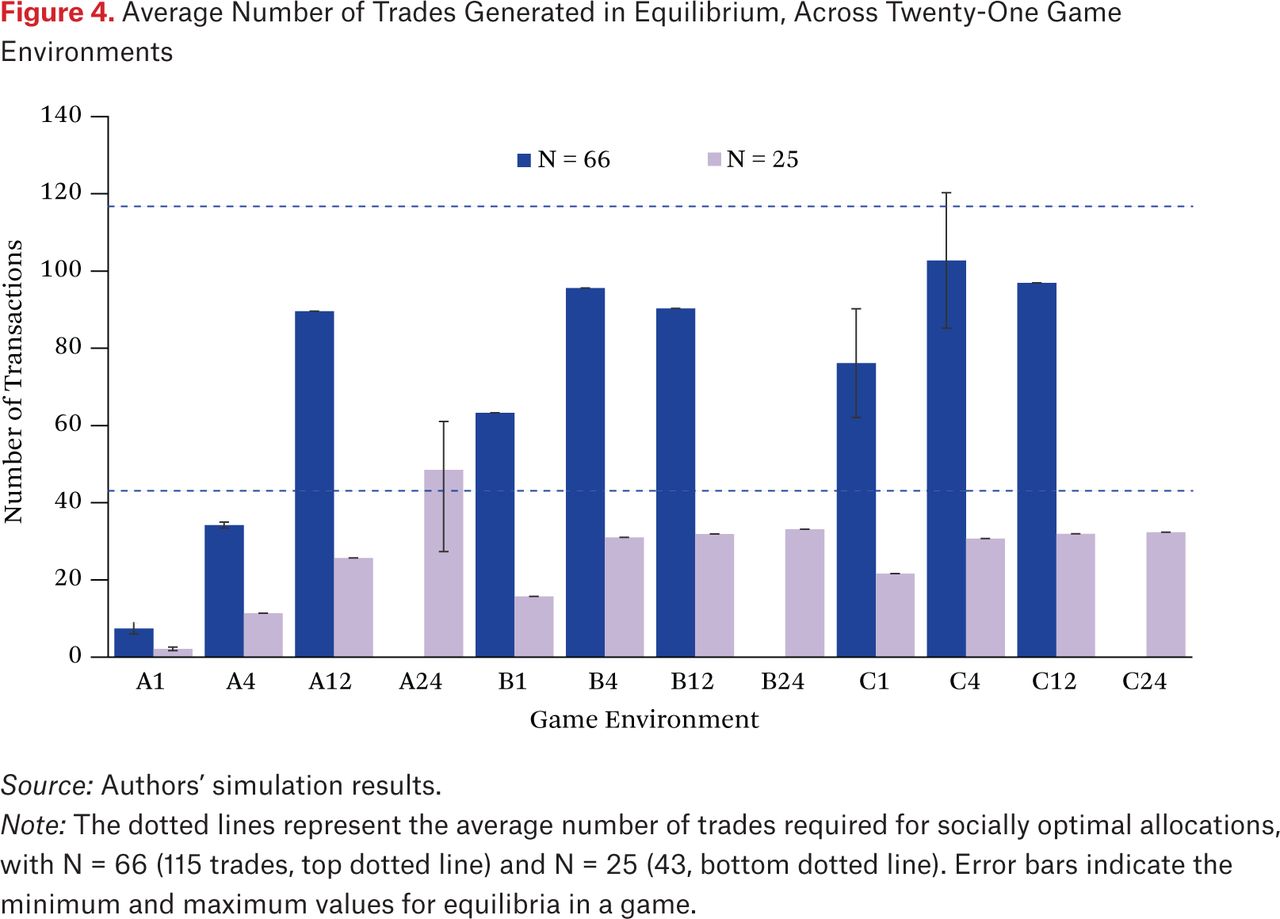

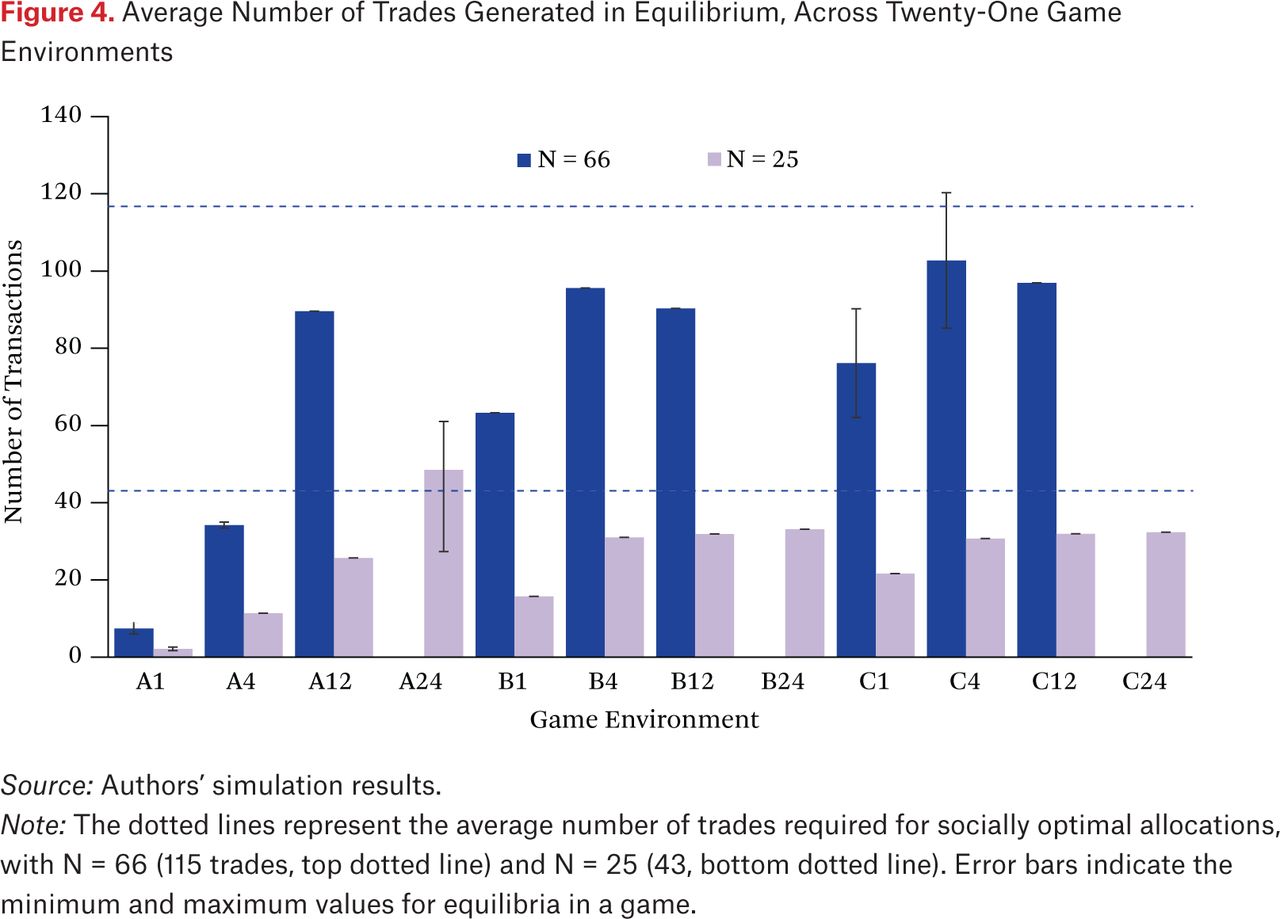

- Figure 4.

Average Number of Trades Generated in Equilibrium, Across Twenty-One Game Environments

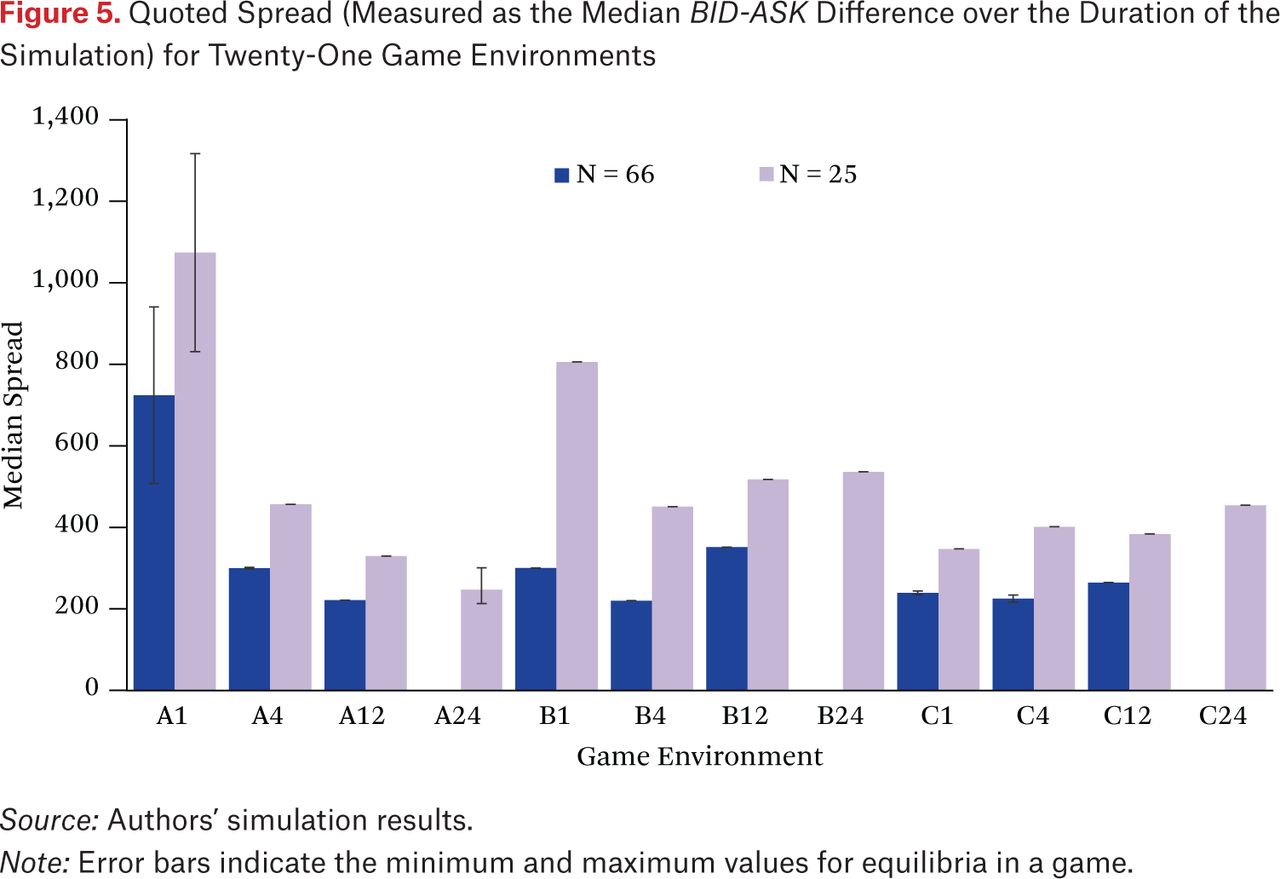

- Figure 5.

Quoted Spread (Measured as the Median BID-ASK Difference over the Duration of the Simulation) for Twenty-One Game Environments

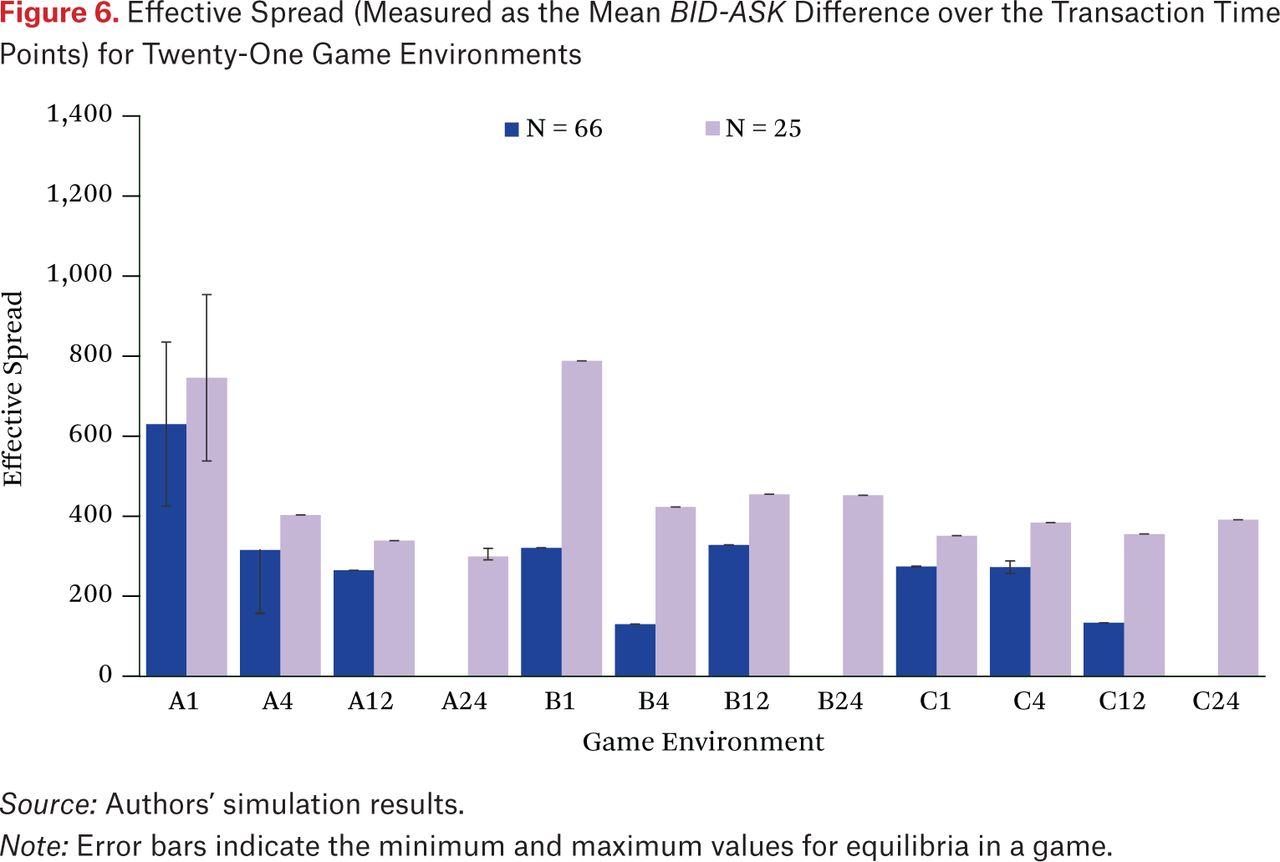

- Figure 6.

Effective Spread (Measured as the Mean BID-ASK Difference over the Transaction Time Points) for Twenty-One Game Environments

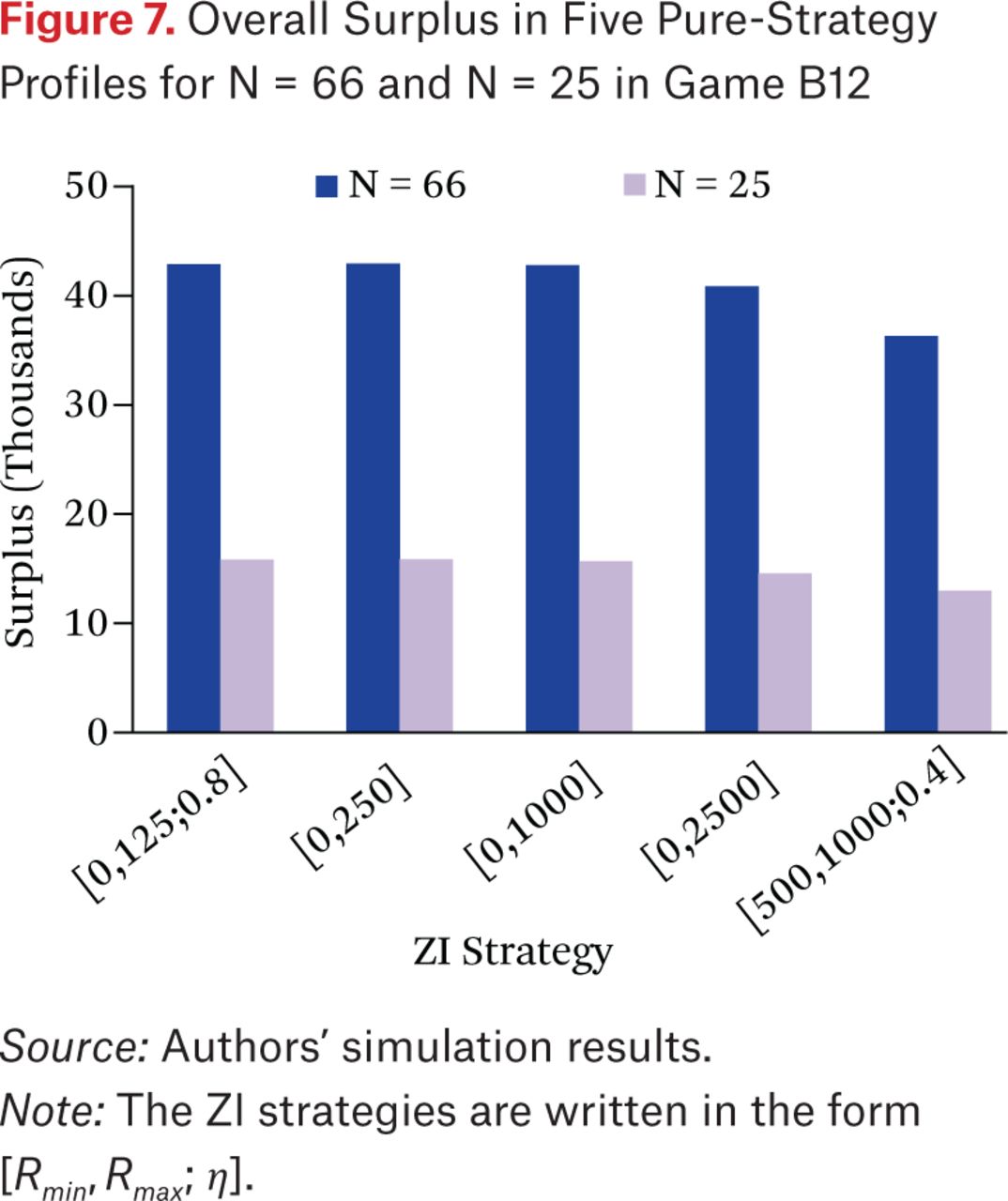

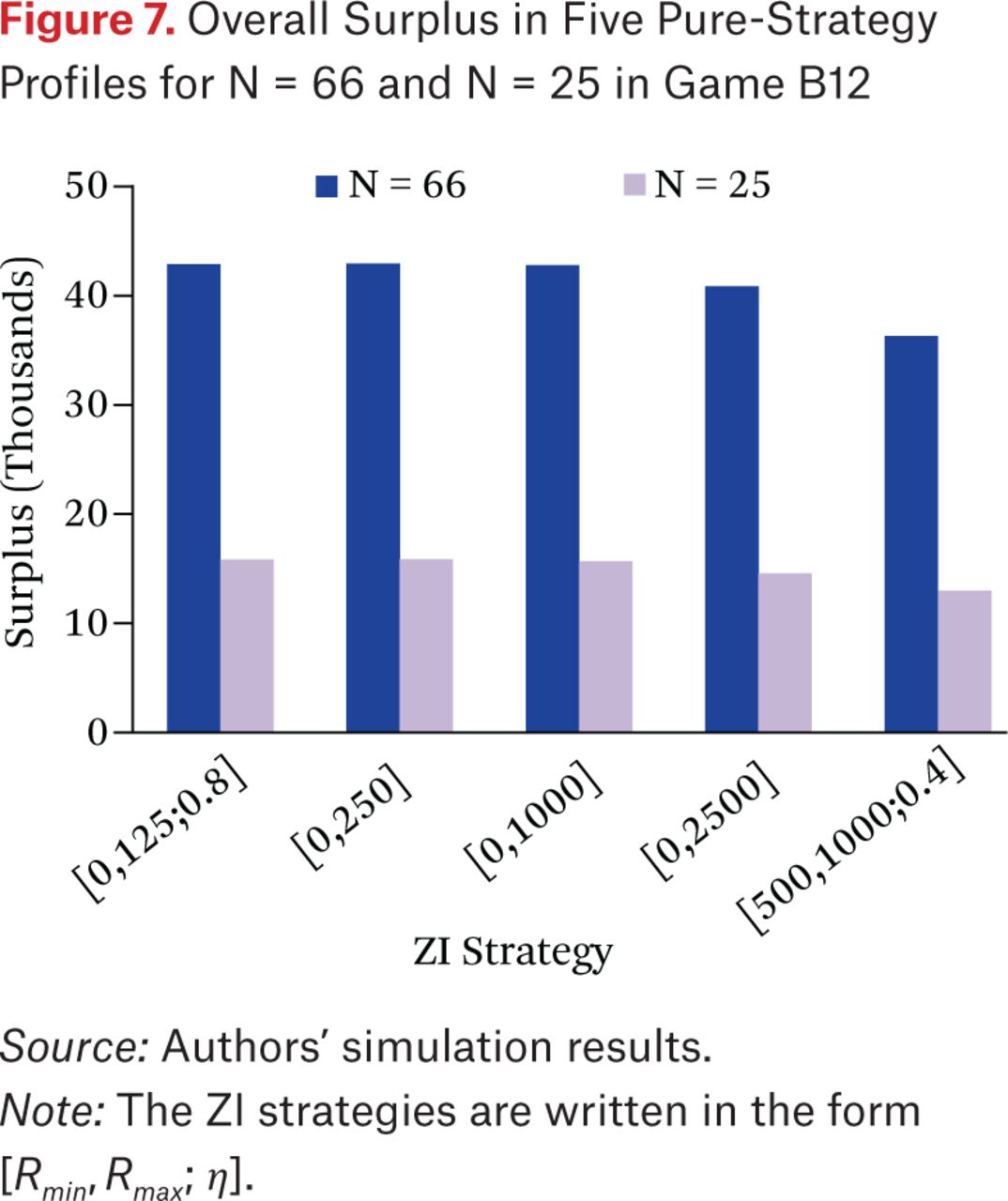

- Figure 7.

Overall Surplus in Five Pure-Strategy Profiles for N = 66 and N = 25 in Game B12

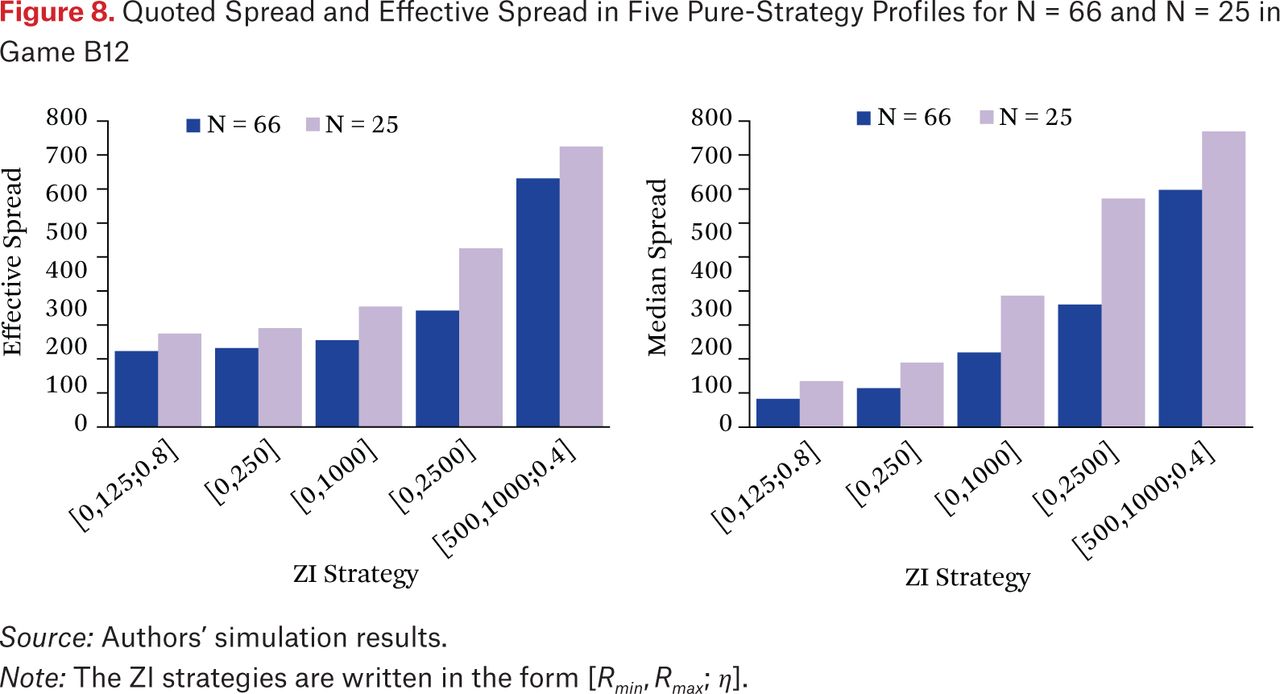

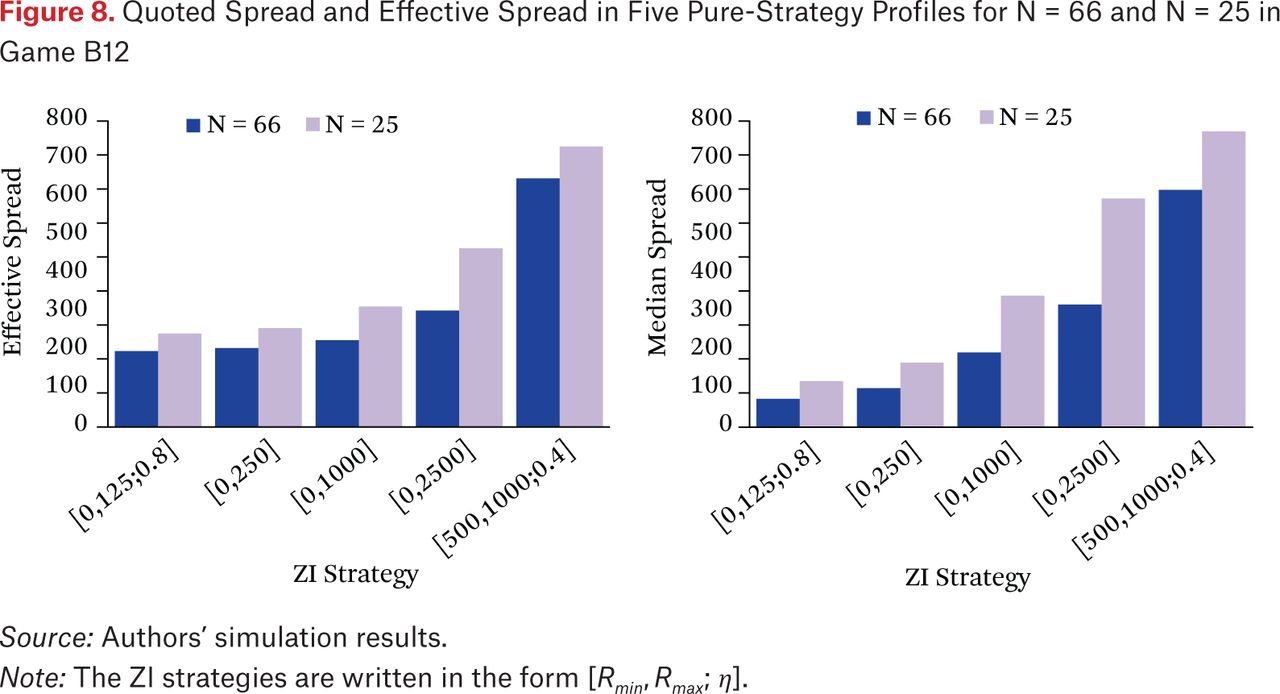

- Figure 8.

Quoted Spread and Effective Spread in Five Pure-Strategy Profiles for N = 66 and N = 25 in Game B12

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.