Abstract

This article examines the link between wealth inequality and families’ financial investment, saving, and borrowing for the sake of children. Using the 1998–2016 Survey of Consumer Finances data, we show that American families have increasingly engaged in financially more intensive parenting but that there are substantial differences by wealth and race-ethnicity. Over time, White families above median wealth accumulate more financial assets and education savings as well as less education debt for children. In contrast, Black and Hispanic families across the wealth distribution have low financial assets and education savings for children. In addition, for Black families across the wealth distribution education debt has grown to substantial amounts. These findings suggest that the contemporary norm of intensive parenting has unequal financial manifestations, which have likely contributed to the widening of wealth and racial inequalities, especially between White and Black child households.

Wealth inequality increased dramatically over the past decades in the United States (Pfeffer and Schoeni 2016) and increased the most for families with children relative to any other type of household (Gibson-Davis and Percheski 2018). To contribute to the understanding of these trends, we focus in this article on families’ financial behavior, specifically their monetary investment, saving, and borrowing for the sake of children, which potentially lessen or augment intergenerational wealth differences. We ask, first, whether financial investment, saving, and borrowing by Americans for their children changed over the past couple of decades, and, second, whether those changes varied by wealth and race-ethnicity. Although researchers have studied expenditures for children (Bianchi et al. 2004; Kornrich and Furstenberg 2013; Schneider, Hastings, and LaBriola 2018), we call for a more comprehensive analysis of the economy of parenting. We argue that over the past decades, families with children have adopted financially intensive parenting practices: they have become increasingly engaged in financial investment, saving, and borrowing for children. However, the types of these financial behaviors (be it monetary investment, saving, or borrowing), and amounts linked to them, have varied substantially across the wealth distribution and by race-ethnicity. Indeed, financially intensive parenting happens in a context of high racial wealth gaps in the United States (see Gibson-Davis and Hill 2021, this issue). Based on nationally representative, cross-sectional data from the Survey of Consumer Finances (SCF), White child households’ median net worth (assets minus debts) was $95,610 in 2016, which was 2 percent lower than in 1998. Black child households’ median net worth was only $510 in 2016 and has decreased from 1998 by 90 percent.1 Median net worth for Hispanic child households was $5,600 in 2016 and has increased by 75 percent since 1998.

To answer the first question, analyzing SCF data, we find evidence of growing financial engagement of parents, as exemplified in the increasingly higher accumulation of financial assets2 under children’s names or co-owned with children, education savings for children, and education debt taken on for children, in the period between 1998 and 2016. As concerns the second question, we find that White families above median wealth have been investing significantly more financial assets and accumulating higher tax-advantaged education savings for their children over time. In contrast, Black and Hispanic families across the wealth distribution have low financial assets and education savings for children. In addition, among Black families across the wealth distribution, education debt has grown substantially.

WEALTH INEQUALITY TRENDS

As inequality in the United States increased on multiple dimensions over the past decades, inequality in wealth, an important outcome of social stratification (Killewald, Pfeffer, and Schachner 2017), rose most starkly (Gibson-Davis and Hill 2021, this issue). Since the 1960s, net worth of the top 1 percent of the wealth distribution increased sevenfold, and those at the top 90th percentile saw their wealth increase fivefold. In contrast, families at the bottom 10th percentile went from having no wealth to negative net worth, meaning that they had more debts than assets (Urban Institute 2017). The Gini coefficient for the wealth distribution increased from 0.79 to 0.85 since the late 1980s (Pfeffer and Schoeni 2016).

Wealth inequality did not grow equally across various sociodemographic groupings, however, and two patterns are particularly relevant for the purposes of our study. First, wealth inequality increased more for families with children than any other type of household (Gibson-Davis and Hill 2021, this issue; Gibson-Davis and Percheski 2018). Families with children witnessed large increases in net worth in the top 10 percent and the rise of the parental top 1 percent, accompanied by declining levels of median wealth, suggesting that those at the bottom were losing ground. Second, racial-ethnic gaps in wealth are vast and growing, particularly since the Great Recession (Killewald, Pfeffer, and Schachner 2017). The median wealth of White households is ten times greater than that of Black households and eight times that of Hispanic households. Notably, racial-ethnic disparities in wealth increase almost exponentially along the wealth distribution (Maroto 2016; Percheski and Gibson-Davis 2020). Moreover, the wealth of Black and Hispanic households dropped precipitously after the Great Recession in 2007 (McKernan et al. 2014), and Black households in particular have witnessed continued declines since then (Percheski and Gibson-Davis 2020). Indeed, Black-White household wealth gaps were smaller in 2004 than in 2016 (Wolff 2018). These existing and historical racial inequalities need to be considered when analyzing saving, investing, and borrowing for the sake of children.

FINANCIALIZATION AND INCREASING INDEBTEDNESS OF HOUSEHOLDS

Because the focus of this article is on financial behavior of families, it is important to place it in the context of broader trends of financialization of the U.S. economy (Krippner 2011; Davis and Kim 2015). Although the early literature on financialization has mostly focused on activities of firms (Krippner 2005; Epstein 2005), more recent work pays attention to the financialization of everyday life (Martin 2002; Pellandini-Simányi, Hammar, and Vargha 2015), as well as the consequence of financialization for inequality (Lin and Neely 2020). Scholars argue that availability of financial instruments has increased financial product consumption and leveraged investment (Davis 2009). Individuals have more aggressively pursued financial strategies, which make up today’s “finance culture” (Langley 2007; Fligstein and Goldstein 2015) and have become more tolerant of risk-taking and debt-reliance (Lea, Webley, and Levine 1993). Indeed, financialization has made various forms of credit more readily available to broad swaths of the population, resulting in rising levels of household indebtedness in the United States since the 1970s (Dwyer 2018).

Many researchers attribute the significant growth in how much debt American households owe to stagnant wages and declining purchasing power of the middle class, also known as “the middle class squeeze” (Wolff 2010; Leicht 2012; Porter 2012; Warren and Tyagi 2016). Scholars argue that the processes of deindustrialization and proliferation of liberal market economic policies heightened labor-market insecurity and economic instability while weakening the state welfare protections (Rajan 2010; Carruthers and Kim 2011; Leicht and Fitzgerald 2014). This led to the rising economic pressures and fluctuations in household income that necessitate borrowing on credit for the groups whose wages have either been stagnant or in decline (Leicht and Fitzgerald 2007, 2014; Wolff 2010, 2012; Collins 2009; Montgomerie 2006, 2009; Bucks 2012; Porter 2012; Sullivan and Kaufman 2012; Warren and Thorne 2012). Indebtedness rises when households experience a shock, such as job loss, illness, or death (Pressman and Scott 2009) because credit has assumed a function of a social safety net (Prasad 2012). Indeed, Joseph Cohen (2017) finds that the U.S. social welfare system provides little support for the working-age population and children. Hence middle-class families are taking on increasing debt to manage the rising costs of key basic necessities, such as education, childcare, or housing.

Other researchers examining indebtedness of households point to its cultural dimensions, namely, the changing understandings of the legitimacy of debt and financial engagement, as well as how maintaining or upgrading one’s lifestyle through consumption has resulted in households’ taking on more debt. Such status-driven accounts of indebtedness rely on classical sociological insights that social groups are differentiated through lifestyles marked by various consumption patterns (Weber 1946), and that people signal their wish to emulate groups with a higher social status through conspicuous consumption and the ostentatious display of wealth (Veblen 1994; but see Bagwell and Bernheim 1996; Ritzer 2001; Trigg 2001). Scholars document that people will often overleverage before reducing their consumption (Ritzer 1995; Frank 1999; Trigg 2001; Fligstein and Goldstein 2015), and that rising income inequality amplifies the increase in household debt via conspicuous consumption (Ritzer 1995; Schor 1999, 2007; Barba and Pivetti 2009; Wisman 2013). In line with this, Kerwin Charles, Erik Hurst, and Nikolai Roussanov (2009) find that Blacks and Hispanics use a greater share of their income on visible goods than Whites to signal their household’s economic position. Examining the cultural dimensions of debt, scholars note that Americans have become “overspent” (Schor 1999), or caught “the luxury fever” (Frank 1999), influenced by media images of the super-rich lifestyle and misconceptions that the wealthy are their appropriate reference category (Ritzer 1995; Wisman 2013). Status consumption is related to household indebtedness because, in many cases, the only way consumers can furnish the increases in (conspicuous) consumption is by use of credit (Manning 2000).

Financialization of the economy has been an unequal process (Lin and Neely 2020). That is, although access to financial products and services has generally widened, families of color relative to White families face differential access to financial markets, including banking and the credit market, often because of the state exclusionary policies and financial companies’ discriminatory practices rooted in the long history of racial inequality in the United States (Seamster and Charron-Chenier 2017; Baradaran 2019). Further, as financial markets have become more complex, racial-ethnic inequalities in terms, conditions, and types of financial products and services have widened (Dwyer 2018; Rona-Tas and Guseva 2018). For instance, evidence from audit studies and observational research shows that Blacks and Hispanics not only experience higher rejection rates, but also receive less favorable terms when securing mortgages than Whites with similar sociodemographic characteristics and similar credit history (for a review, see Pager and Shepherd 2008). Moreover, research shows that monetary sanctions imposed on people convicted of crimes in the United States and consequent legal debt create a disproportionate burden for racial minorities (Harris, Evans, and Beckett 2010), which would contribute to racial wealth gap. In addition, parents who are more likely to have contact with the criminal justice system and a history of incarceration, and who are disproportionately Black, are also more likely to accumulate child support debt (Turetsky and Waller 2020).

THE RISE OF INTENSIVE PARENTING

Our aim is to connect macroeconomic changes in financialization and indebtedness to the world of families and parenting. Scholars and practitioners alike have debated ways of contemporary parenting, proposing that a cultural shift has been under way toward intensive parenting, or a more child-centered and time-intensive approach to raising children. Initially, research suggested that it is mostly mothers of middle- and upper-middle-class background who practice intensive parenting (Hays 1996; Bianchi, Robinson, and Milkie 2006; Nelson 2010; Ramey and Ramey 2010; Elliott, Powell, and Brenton 2015). Subsequently, studies documented that mothers and fathers alike have been spending increasingly more time with children (Sayer, Bianchi, and Robinson 2004). They also point out, however, that the absolute amount of time and how it is spent vary between more- and less-educated parents (England and Srivastava 2013; Kalil, Ryan, and Corey 2012; Sayer, Bianchi, and Robinson 2004). This is related to Annette Lareau’s (2003) influential study, which distinguishes between styles of parenting across social class, with middle- and upper-class parents practicing concerted cultivation (or organization of children’s time and activities to help them become adept at institutional life) and lower-class parents practicing natural growth (or letting children structure their own time) (but see Calarco 2014; Weininger, Lareau, and Conley 2015).

Still, other research has countered the claim that intensive parenting is a sign of cultural capital among well-to-do parents, finding that parents of lower classes also exhibit such behavior (Chin and Phillips 2004; Waller 2010; Edin and Nelson 2013). To adjudicate between these perspectives, Patrick Ishizuka (2019) designed a survey experiment to gauge contemporary parenting standards using a nationally representative sample of parents that features variation across class groups. Ishizuka presented respondents with various vignette scenarios that reflected the more or less intensive parenting norm, such as a preference for structuring a child’s time and enrolling a child in extracurricular activities over a perception that parents should let their child entertain themselves when bored. He concluded that “parents of different social classes express remarkably similar support for intensive mothering and fathering across a range of situations, whether sons or daughters are involved” (2019, 31). Even if not examining actual parenting practices, Ishizuka’s study clearly points to the prevalence of the intensive parenting norm across socioeconomic groups.

Researchers have also asked how race and ethnicity may impact parenting. Although Lareau (2003) compares Black and White families, she does not identify significant differences between them in their parenting approach, with class differences prevailing. Recent studies of Black mothers also point to their intensive parenting (Dow 2019; Moore 2011; Turner 2020). Beyond the Black and White comparison, researchers find that immigrant parents of Hispanic and Latinx background tend to have higher educational expectations for their children than native-born parents (Kao and Tienda 1994; Goyette and Xie 1999; Glick and White 2004; Feliciano and Lanuza 2016), which would suggest their focus on investing in children’s education.

FINANCIALLY INTENSIVE PARENTING

This article advances research on intensive parenting by developing a perspective in the economy of parenting and turning the focus to financial behaviors and consequences of the intensive parenting norm, or what we call financially intensive parenting. Studies find that richer families spend increasingly more money on children (Kornrich and Furstenberg 2013; Schneider, Hastings, and LaBriola 2018). These studies suggest that well-to-do families are propelled by a motivation to maintain economic privilege and hoard economic and other status advantages in light of high economic inequality (Doepke and Zilibotti 2019; Schneider, Hastings, and LaBriola 2018).

We look beyond spending for children to consider a variety of financial behaviors that parents engage in for the sake of their children, including financial investment, savings, and borrowing on credit. Here we apply the social meaning of money and relational work in economy perspectives (Zelizer 1994; Bandelj, Wherry, and Zelizer 2017; Bandelj 2020), which assert that money is imbued with meaning and deployed differently in different social relationships. More specifically, people earmark money, or “assign different meanings and designate separate uses for particular kinds of monies” (Zelizer 1989, 343) and engage in “affirmation of social relations through economic activity” (Bandelj 2020, 11). Thus, we can expect the growing norm of intensive parenting to result in an increasing use of various monies earmarked for children to affirm the special relationship between parents and their children.

Indeed, over recent decades, the repertoire of financial instruments that parents can use for the sake of their children has widened. These instruments include various financial products, such as stocks, bonds, mutual funds, and money market accounts, that parents set up under their children’s names. In addition, parents can take advantage of special financial instruments related to children’s education, including 529 Savings Plans. These plans resulted from the creation of the Internal Revenue Code Section 529 in 1996 in response to some states’ efforts to help parents meet the demands of rising college tuition (Holden 2002; Ma 2005). The plans allow parents to allocate pretax money earmarked for children’s education into financial instruments, usually mutual funds, managed by financial firms hired by state governments. Reports show that the assets put aside in 529 plans grew to a record $329 billion as of year-end 2018, with the number of accounts rising to more than 13.8 million (College Savings 2020).

Moreover, credit-related instruments that parents can use to support children, primarily investment in children’s education, are available. These include Parent Loans for Undergraduate Students (PLUS loans), offered by the federal government through the Federal Student Aid Office, which have become increasingly popular since the 1990s (Grigoryeva 2015; National Center for Education Statistics 2016). Zach Friedman (2019) reports that in 2019 the balances in Parent PLUS loans reached almost $89 billion. Parents can also take on loans from private lenders to support enrollment of their children in college.

Given the wide range of financial instruments available to parents, our goal is to investigate whether over time parents have increasingly engaged in financial behaviors that reflect their prioritization of children and investment in their education, and how these trends may vary by wealth and race-ethnicity. We therefore test three hypotheses. The first is that financially intensive parenting has grown in the past two decades, as exemplified in the increasingly higher share of financial assets under children’s names or co-owned with children in light of all household assets, absolute amount of financial assets under children’s names or co-owned with children, education savings for children, and education debt taken on for children. The second hypothesis is that financially intensive parenting behaviors will vary by wealth position. Specifically, given structural constraints in wealth (Pfeffer and Schoeni 2016; Maroto 2016; Killewald, Pfeffer, and Schachner 2017), we expect parental financial behaviors that include investment and saving activity for children to be more pronounced among above-median-wealth households and parental financial behaviors that rely on borrowing on credit to be more pronounced among below-median-wealth households. The third hypothesis is that financially intensive parenting will differ across racial-ethnic groups, with Black and Hispanic families accumulating significantly fewer financial assets and savings for children than White families.

DATA AND METHODS

To document trends over time and across racial-ethnic groups in how families of different wealth status engage in financial investment, savings, and debt for the sake of children, we use data from the nationally representative, cross-sectional triannual Survey of Consumer Finances and focus on the survey waves from 1998 to 2016.3 The SCF is among the best sources of data on a wide range of household financial activities (Keister 2014, 350), including saving, investing, and borrowing financial activities associated with investment in children. Also, the SCF collects detailed sociodemographic data, thus making it possible to disaggregate trends in financial activities for the sake of children by wealth and race-ethnicity.

All analyses focus on families with at least one child (coresident or non-coresident), twenty-four years old or younger. This age threshold is chosen because, as part of our analyses, we examine parental borrowing for children’s education, which is mostly earmarked for college. For the other outcomes we examine, our results are robust to eighteen as the children’s age threshold. For education debt, because the SCF does not collect information about for whose education the debt is accrued, we analyze only families with children where the household head is older than forty (following other studies using SCF data, such as Akers and Chingos 2014) to exclude from the analysis families where parents are most likely paying off their own student loan debt rather than borrowing for children’s education. In all the analyses, we focus on three racial-ethnic groups: Whites, Blacks, and Hispanics. We do not analyze trends for other racial-ethnic groups (such as Asians or Native Americans) because these are not distinguished in the SCF data.

Our analysis focuses on a range of financial activities for children that cover investments, saving, and borrowing. First, we examine financial assets under children’s name or co-owned by children—including checking accounts, certificates of deposit, and savings and money market accounts—and both the absolute amount and as a share out of total household assets. Our second variable of interest is the amount of savings in state-sponsored education savings plans such as a 529 plan, which is available in the SCF since the 2001 wave.4 An important advantage of these two measures is that they capture long-term savings earmarked for children, which have consequences for children’s attainment and well-being. Also, both measures can be conceptualized as saving and investing simultaneously.

Next, in addition to saving and investing, we examine borrowing related to children. Our main focus is on debt accrued in education loans as a type of debt earmarked specifically for long-term investment into children. Additionally, we also consider, in supplementary analyses, mortgage debt and credit card debt. The SCF data do not let us distinguish to what extent mortgage and credit card debt are driven by investment into children as compared to other motives. However, research shows that schools are an important consideration in residential choices, and parents are willing to pay a premium for neighborhoods with better schools (Owens 2016). Evidence also shows that good school neighborhoods have been increasingly more expensive (Killewald, Pfeffer, and Schachner 2017; Johnson 2006; Shapiro 2004, 2017), which, for most families, would necessitate taking on more mortgage debt to afford to reside in such neighborhoods (Frank 2007; Warren and Tyagi 2016). Similarly, although credit card debt is not earmarked directly for children, parents may use this type of loan to fund expenditures on children, a practice shown to be on the rise (Kornrich and Furstenberg 2013; Schneider, Hastings, and LaBriola 2018). For all debt categories, we focus on absolute amounts. All dollar values are in 2016 U.S. dollars.

Our analysis also incorporates a range of demographic attributes. Our main variable of interest is household wealth, measured as all assets minus all debts (Killewald, Pfeffer, and Schachner 2017).5 To examine trends by wealth, we divide the wealth distribution into two categories: above and below the median wealth (or top and bottom halves of the wealth distribution), where the median wealth splits are computed for the full sample. This categorization scheme is admittedly crude but ensures that the (unweighted) number of racial-ethnic minorities within each wealth category is large enough for making meaningful statistical inference. Descriptive statistics show that in 2016 only 19 percent of non-Hispanic Blacks and 23 percent of Hispanic families with children fall above median wealth for these racial-ethnic groups, and that this number is 54 percent of non-Hispanic White child households. Therefore, in some of our analyses for Whites, we distinguished also the top 20 and top 5 percent of the wealth distribution. Other demographic variables include household income, education (measured by four dichotomous variables for high school degree, some college, college degree, or advanced degree, with less than high school being the reference category), number of children under twenty-five in the family, family structure (two-parent households being the reference category and two dichotomous indicators for single-parent family and all other families, where the latter includes, among others, multiple-generation households); age of the household head and its square term divided by 100, and gender of the respondent (a dichotomous variable with 1 = male).6 Table A1 presents all variable definitions and descriptive statistics. Tables A2 through A5 present full regression results.

Our analysis proceeds in two steps. First, we present descriptive trends in financial activities disaggregated by wealth separately for each of the racial-ethnic groups in our analysis on the pooled SCF data across all survey years. Second, we examine the trends by wealth and race within the multivariate framework. For each group, we again pool the SCF data across all survey years and predict the outcome variables with an interaction term between household position in the wealth distribution and survey year, the main effects of these variables, and sociodemographic controls. In all of these analyses, we exclude the value of wealth components we use as outcomes from the estimates of absolute net worth and the median wealth splits.7 Additionally, in all of our analyses, we follow previous research and apply weights to account for the oversampling of wealthy households in SCF.

FINDINGS ABOUT FINANCIAL ACTIVITIES FOR CHILDREN

We first document sizable differences in net worth for White, Black, and Hispanic child households as well as trends over time. Based on the nationally representative SCF data, as exhibited in tables 1 and 2, the White child households’ median net worth was at $95,610 in 2016, which was 2 percent lower than in 1998. In contrast, this figure was $510 for Black child households in 2016 and reflected a substantial decrease of 90 percent in Black child household median wealth since 1998. To compare, the median wealth for Hispanic child households was $5,600 in 2016, an increase of 75 percent since 1998. Moreover, the share of White families with children above median wealth (calculated on the basis of data for all families) increased from 52 percent in 1998 to 54 percent in 2016. In this period, the share of Black and Hispanic families above median wealth (calculated on the basis of data for all families) has hovered at around 19 percent and 23 percent respectively.

Net Worth ($) for Child Households, SCF

Percent of Households Above Median Wealth for Child Households, SCF

Descriptive Trends

Our examination of descriptive trends in monies earmarked for financial investment, saving, and borrowing for children shows that these have generally increased in the period we examine, from 1998 to 2016. The increasing trends are evident across wealth distribution and across racial groups, pointing to a prevalence of a common cultural norm of investment in children. However, in many ways, these financial trends also differ across wealth and across race-ethnicity, reflecting structural resource inequalities that dictate the absolute amounts of investment that can be made and amounts of debt that is accrued.

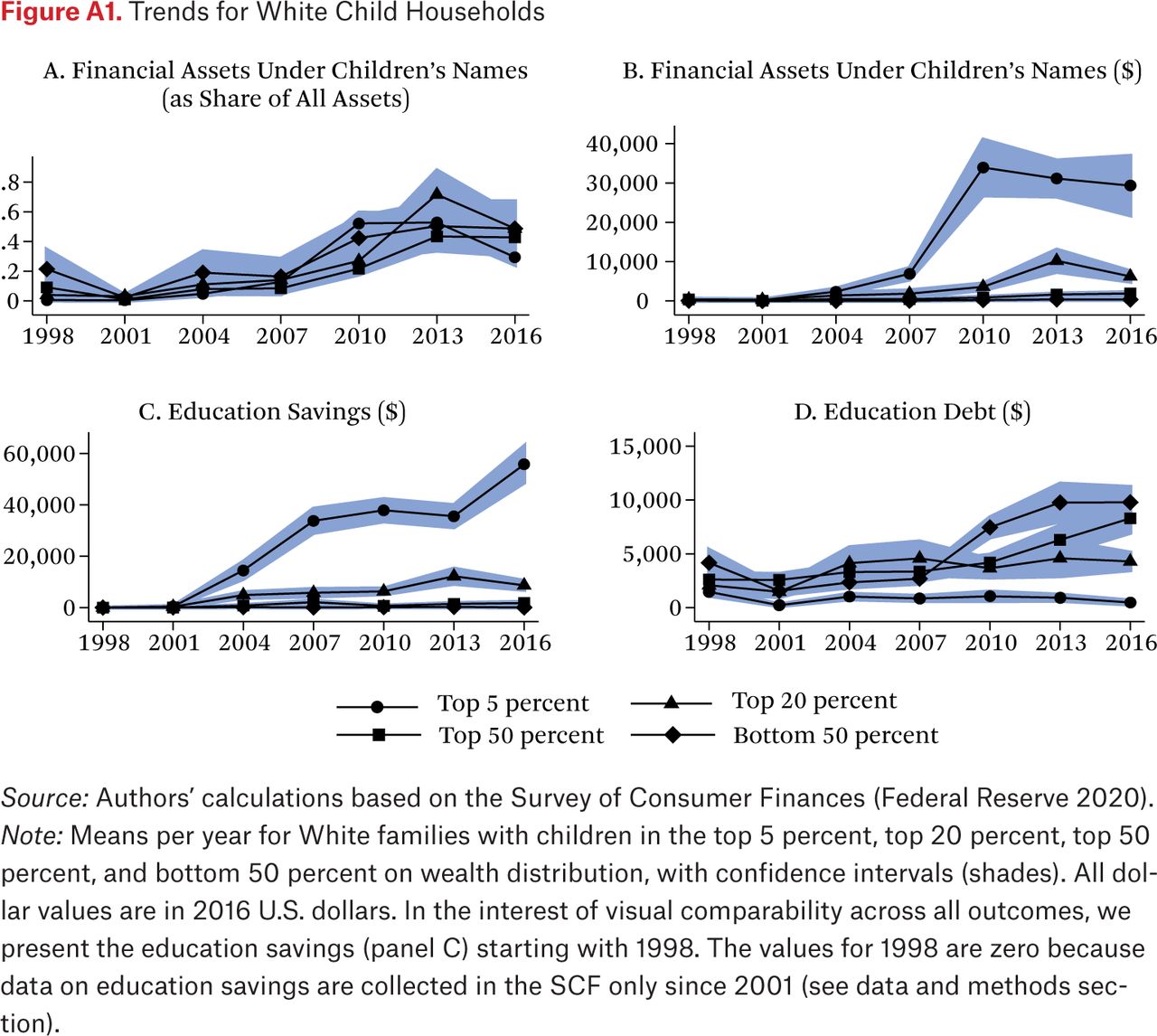

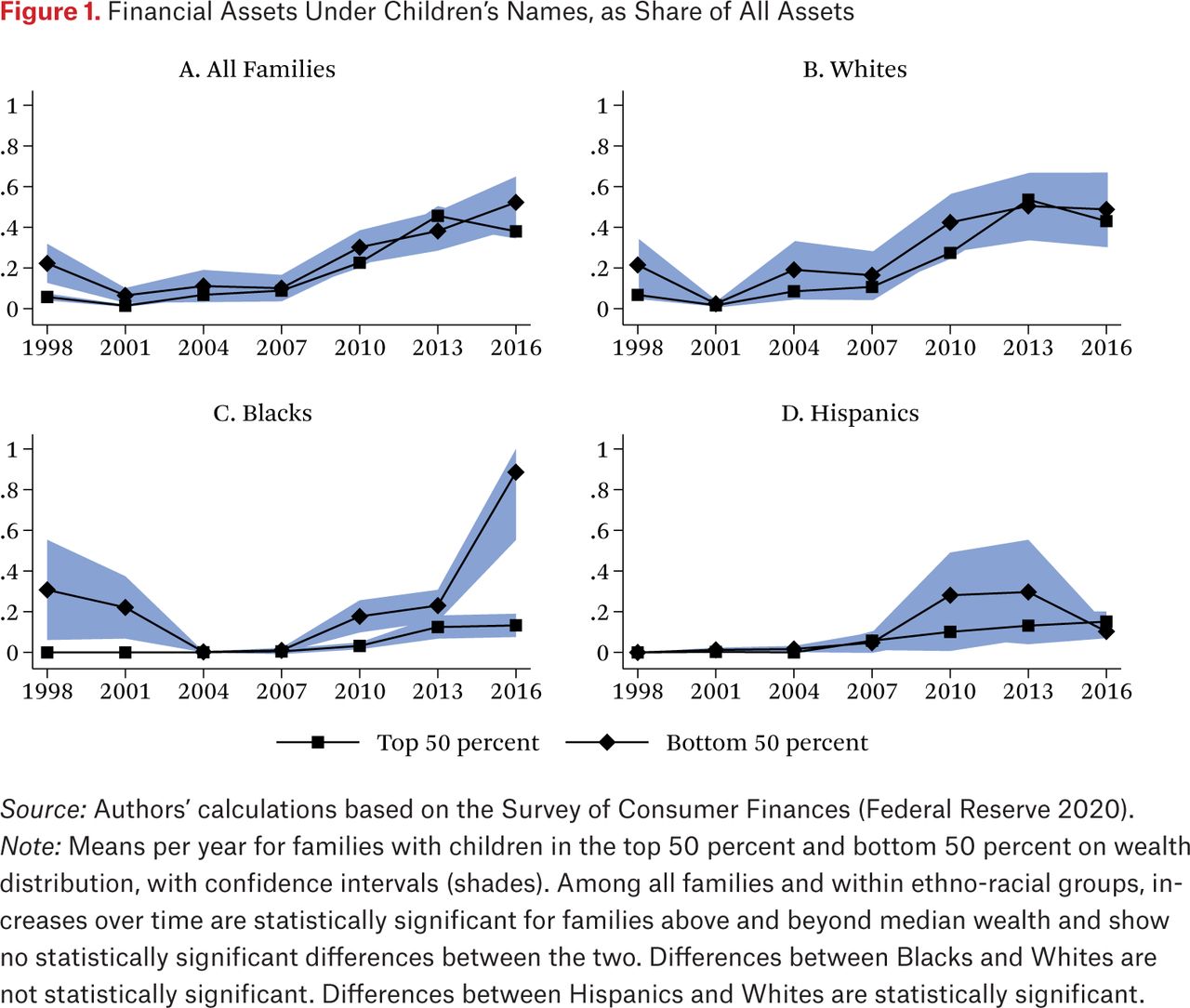

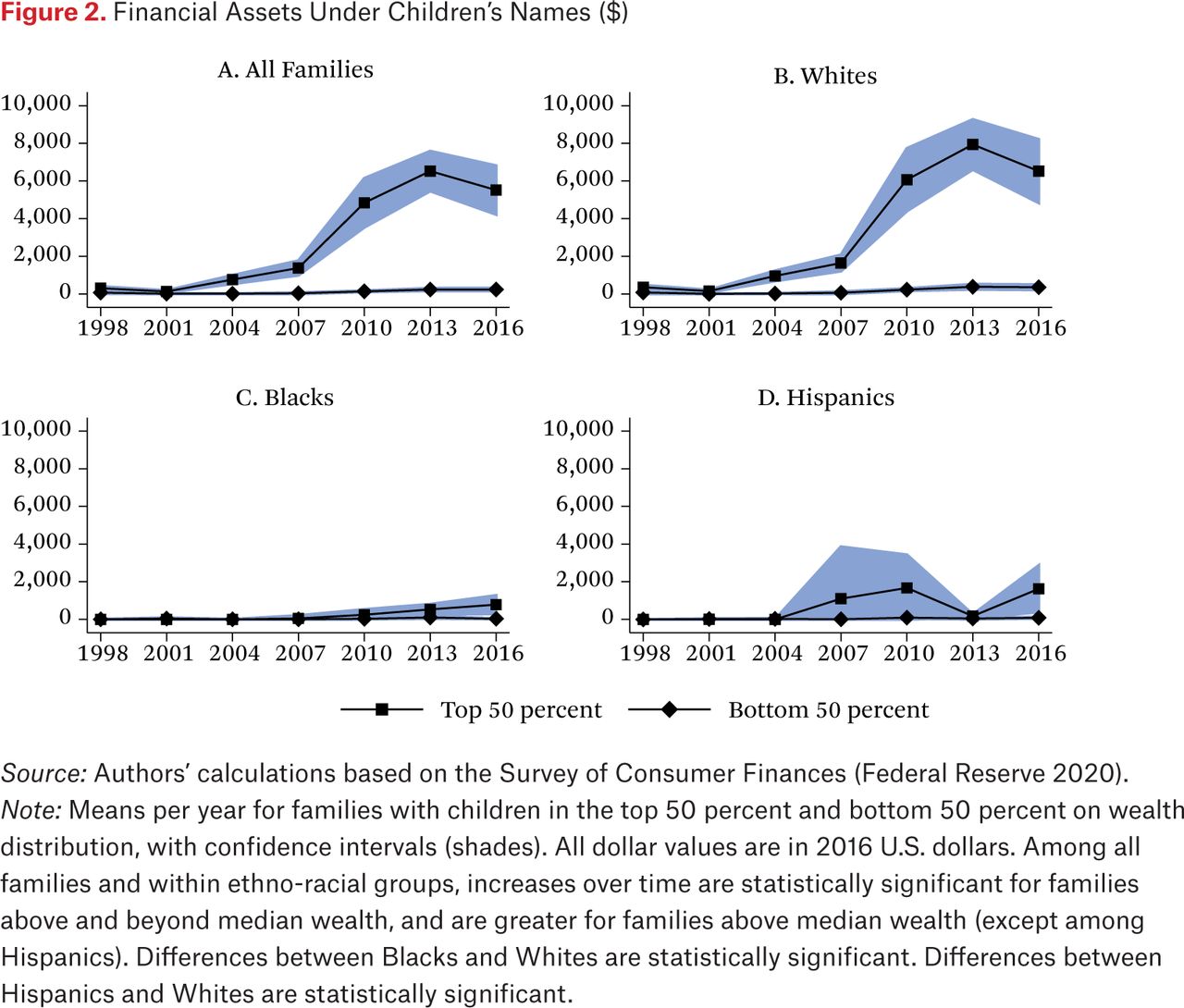

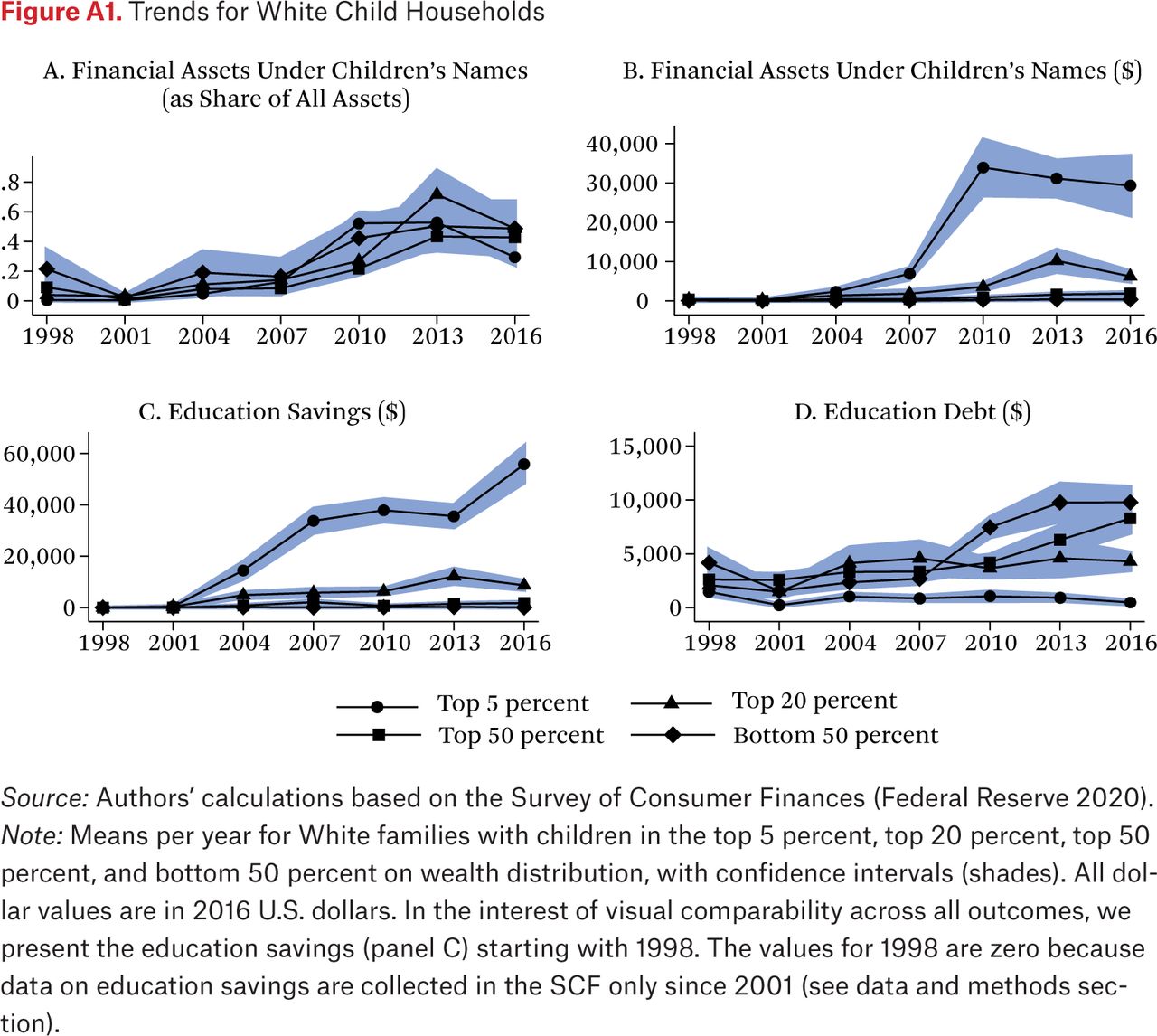

In regard to financial assets under children’s names (checking accounts, certificates of deposit, and savings and money market accounts), all child families in our sample, across wealth position, have allocated a progressively larger share of their assets toward children over time (figure 1). They have also allocated increasingly more monies in absolute terms (figure 2). However, the disparities in the actual amount of these assets are dramatic across wealth of families. Although below-median-wealth child households have increased from about $78 (in 1998) to about $242 (in 2016), the increases for above-median-wealth families have been orders of magnitude larger, starting at $238 (in 1998) and increasing to $5,520 (in 2016). Moreover, racial-ethnic differences in the amount of financial assets under children’s names are stark, especially for above-median-wealth families. Here, White families above median wealth have increased financial assets for children from $361 (in 1998) to $6,528 (in 2016). (As figure A1 shows, the size of these assets is even further pronounced for the top 5 percent in terms of wealth for White child households, which hold on average around $30,000 under children’s names in 2016.) In contrast, the amount of financial assets under children’s names for Black and Hispanic child households above median wealth stand at $784 and $1,622 respectively in 2016 (figure 2, panels C and D), rising from almost no such assets in 1998.

Financial Assets Under Children’s Names, as Share of All Assets

Source: Authors’ calculations based on the Survey of Consumer Finances (Federal Reserve 2020).

Note: Means per year for families with children in the top 50 percent and bottom 50 percent on wealth distribution, with confidence intervals (shades). Among all families and within ethno-racial groups, increases over time are statistically significant for families above and beyond median wealth and show no statistically significant differences between the two. Differences between Blacks and Whites are not statistically significant. Differences between Hispanics and Whites are statistically significant.

Financial Assets Under Children’s Names ($)

Source: Authors’ calculations based on the Survey of Consumer Finances (Federal Reserve 2020).

Note: Means per year for families with children in the top 50 percent and bottom 50 percent on wealth distribution, with confidence intervals (shades). All dollar values are in 2016 U.S. dollars. Among all families and within ethno-racial groups, increases over time are statistically significant for families above and beyond median wealth, and are greater for families above median wealth (except among Hispanics). Differences between Blacks and Whites are statistically significant. Differences between Hispanics and Whites are statistically significant.

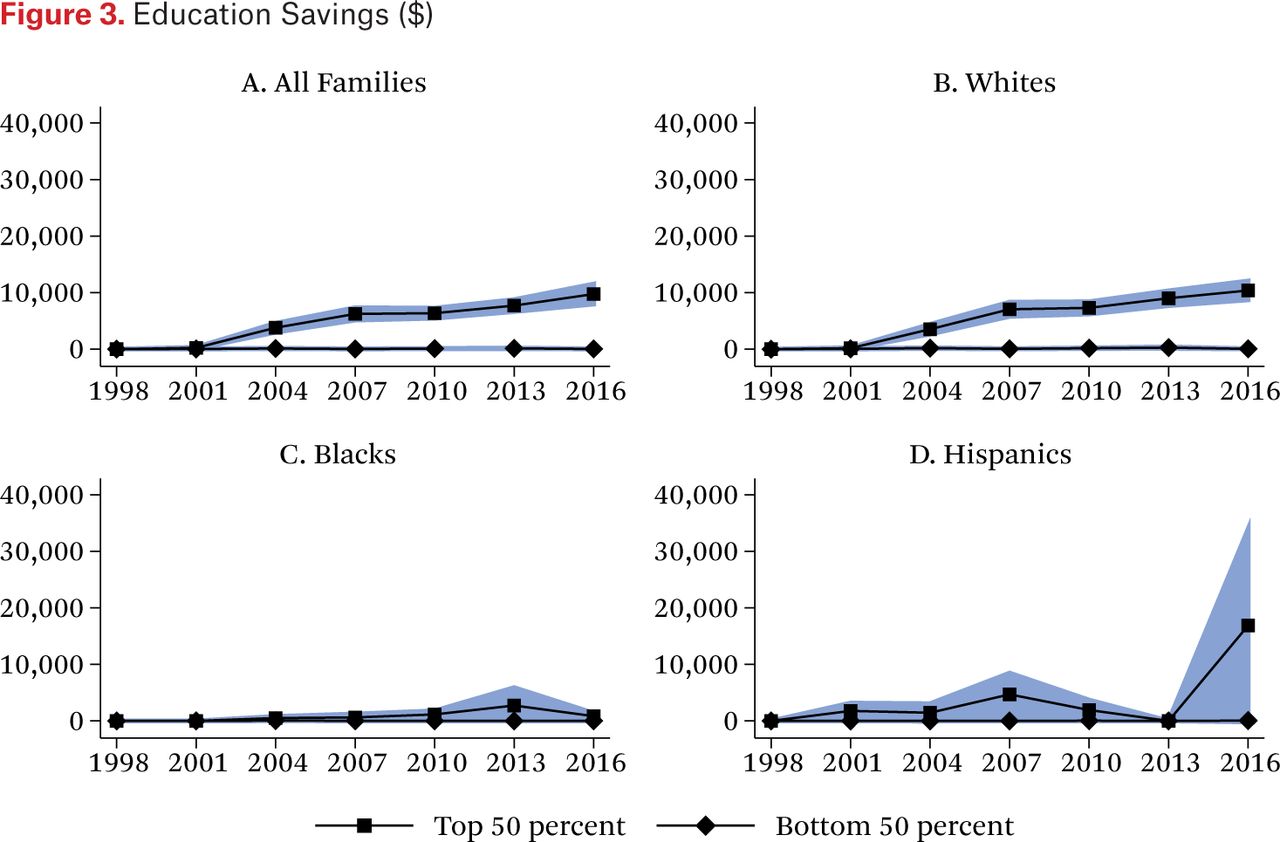

Education savings accounts (mostly 529 college savings plans) became available in the data set after 2000. As documented in figure 3, these savings plans quickly took off as a feature of investment in children but only for above-median-wealth child households, and specifically for above-median White child households. For instance, White families above median wealth have an average of around $10,000 in education savings accounts for children in 2016, relative to those below median wealth, where these savings have stagnated since 2001 around $40 (figure 3, panel B). (As figure A1 shows, these savings are quite large among the top 5 percent of White families, which typically have around $55,000 in those accounts). Among Hispanics, increases over time are statistically significant, showing no differences between families above and below median wealth. Among Blacks, amounts in 529 Savings Plans are quite negligible, and differences across the wealth distribution and over time for Black families are not statistically significant.

Education Savings ($)

Source: Authors’ calculations based on the Survey of Consumer Finances (Federal Reserve 2020).

Note: Means per year for families with children in the top 50 percent and bottom 50 percent on wealth distribution, with confidence intervals (shades). All dollar values are in 2016 U.S. dollars. When all families are analyzed, increases over time are statistically significant only for families above median wealth. These trends are driven entirely by Whites. Among Blacks, differences across the wealth distribution and over time are not statistically significant. Among Hispanics, increases over time are statistically significant, with no differences between families above and beyond median wealth. Differences between Blacks and Whites are statistically significant. Differences between Hispanics and Whites are statistically significant. In the interest of visual comparability across outcomes, we present education savings trends starting with 1998. The values for 1998 are 0 because data on education savings are collected in the SCF only since 2001 (see data and methods section).

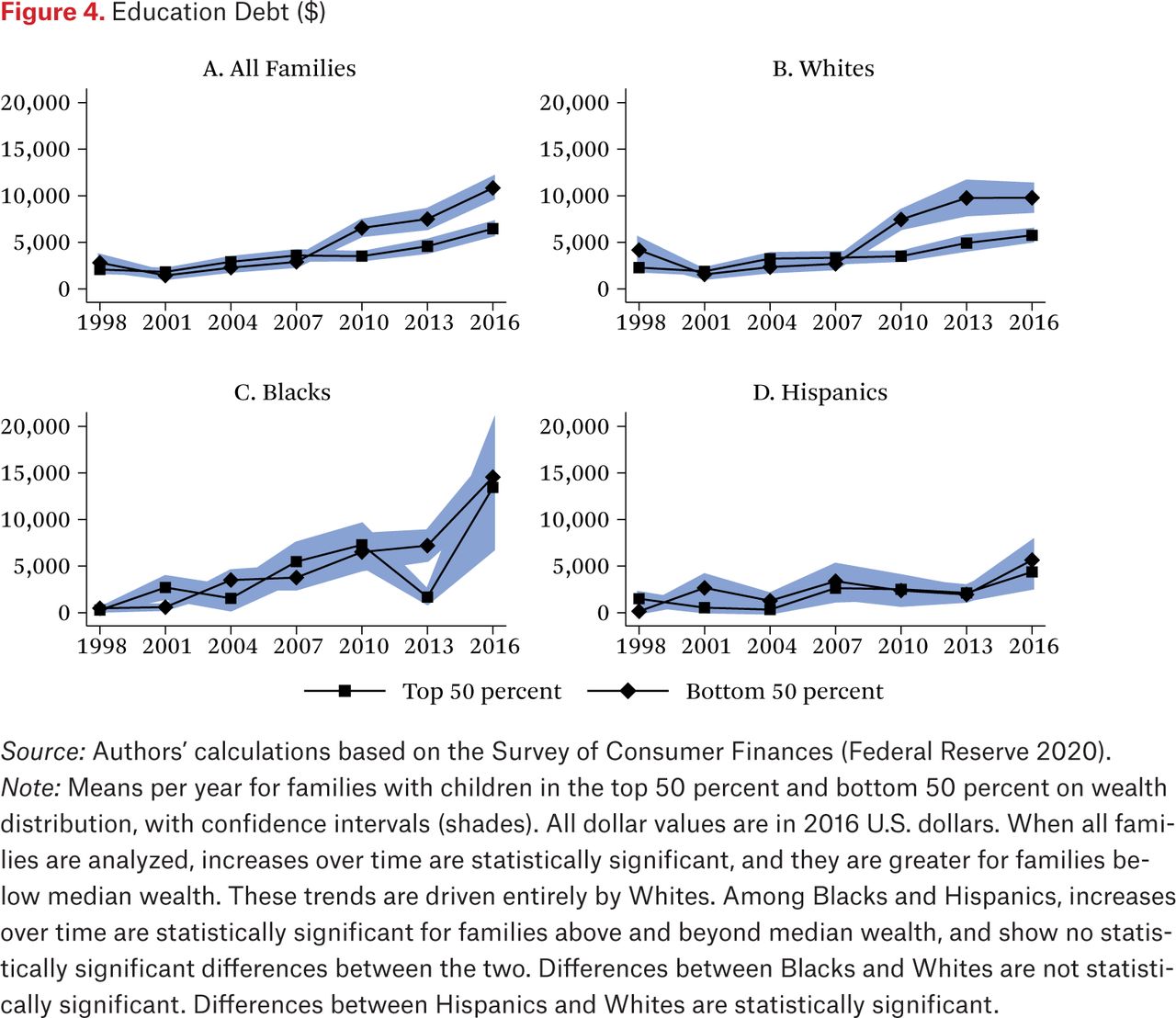

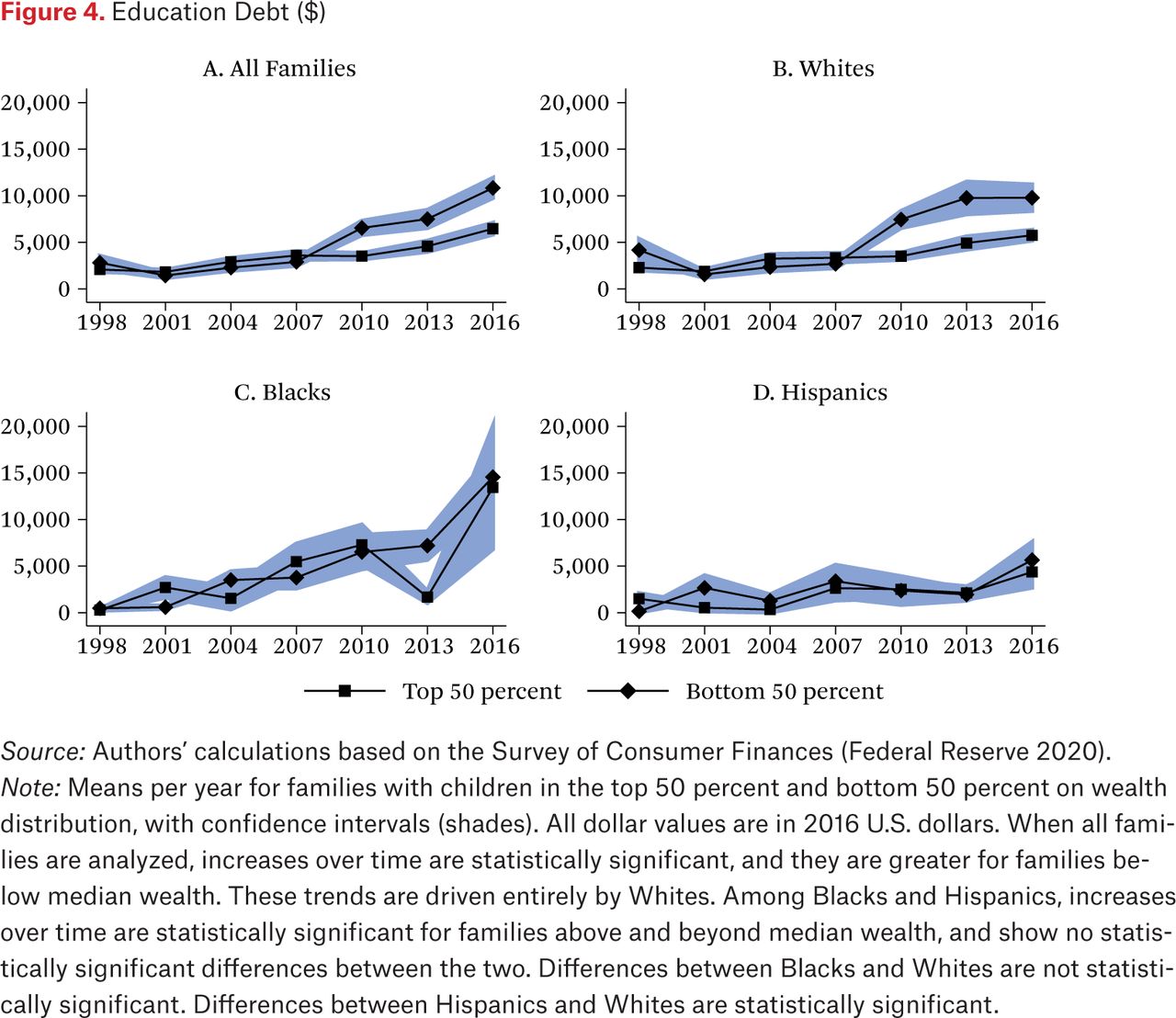

Regarding education debt (figure 4), we find that it has significantly increased for above-median- as well as below-median-wealth child households but has increased more substantially for below-median-wealth families. Moreover, education debt has increased substantially for Black child households, with values running at around $14,000 per household in 2016, for both above-median- and below-median-wealth families. For comparison, average education debt for White above-median child households is considerably lower, around $5,800 in 2016, which is consistent with the fact that education savings (figure 3) for this group have been increasing over time. Among Blacks and Hispanics, increases over time are statistically significant, and show no significant differences between those above and below median wealth. Differences between Blacks and Whites in education debt are not statistically significant but Hispanics have significantly less education debt than Whites.

Education Debt ($)

Source: Authors’ calculations based on the Survey of Consumer Finances (Federal Reserve 2020).

Note: Means per year for families with children in the top 50 percent and bottom 50 percent on wealth distribution, with confidence intervals (shades). All dollar values are in 2016 U.S. dollars. When all families are analyzed, increases over time are statistically significant, and they are greater for families below median wealth. These trends are driven entirely by Whites. Among Blacks and Hispanics, increases over time are statistically significant for families above and beyond median wealth, and show no statistically significant differences between the two. Differences between Blacks and Whites are not statistically significant. Differences between Hispanics and Whites are statistically significant.

Regression Results

Next we examine trends in financial investment, saving, and borrowing for children in a multivariate framework. Regression results are consistent with our descriptive findings, showing that financially intensive parenting has become more pronounced over the past two decades. 8 Specifically, for financial assets under children’s names as share of all family’s assets the year coefficient is positive and statistically significant for all families (table 3, panel A). This is consistent with our proposition that the norm of financially intensive parenting has been growing for all child households. Indeed, no evidence suggests that families above median wealth have been more engaged in prioritizing children in the share of financial assets allocated to them than their counterparts below median wealth. Moreover, we note increasing trends over time across racial-ethnic groups even if in absolute terms the share of assets allocated for children in Black and Hispanic families is less than in White families. In regard to the actual amounts of these assets (table 3, panel B), growth in financial assets for children for top 50 percent wealth families for all racial-ethnic groups over time is significant. Still, all else equal, White families above median wealth allocate about $411 more per year in financial assets under children’s names; this figure is much lower for Black families at around $43, and for Hispanic families at around $88. These differences across racial-ethnic groups are statistically significant.

Multivariate Regression Results

Next, the take-up of the education savings, mostly in 529 college savings plans, has increased significantly over time for White above-median-wealth child households (table 3, panel C). In contrast, Black child households have significantly less savings in 529 plans than Whites, but no notable difference between Whites and Hispanics is apparent. Some evidence does suggest that for Black families in the upper half of the wealth distribution, the education savings have been increasing over time, by about $105 per year. This figure for White families in the upper half of the wealth distribution is more than six times larger, at around $623 per year, net of all covariates.

In regard to education debt (table 3, panel D), notably, in the models for all families and for each of the groups separately, the year coefficient is positive and statistically significant, indicating that education debt has increased substantially between 1998 and 2016 for all child households. The growth per year is the highest among Black households at about $690 each additional year, versus about $600 for Whites and $153 for Hispanics. In addition, consistent with descriptive analyses, the White and Black families have comparable amounts of education debt, and Hispanics have significantly less than Whites.

To examine the role of wealth position further, we conducted a sensitivity analysis in which we dropped families in the top 10 percent of the wealth distribution from our analytic sample to test the extent to which the trends we find for those above median wealth may be in fact driven by the most wealthy families. The results remain substantively the same for the families in the top 11th to 50th percentile in wealth, relative to the top 50 percent in wealth. That is, similar to the findings reported in tables 3 through 6, the trends for top 11th through 50th percentile in wealth are statistically significantly different from those for families below median wealth on three indicators: in terms of the growing amount of financial assets under children’s names over time, growing amounts of education savings over time, and lower education debt over time. This indicates that the rise of financially intensive parenting is not driven by only very wealthy families. In addition, the differences between households below the 50th percentile and the top 11th through 50th percentile in wealth are not significantly different in the share of financial assets for children, which has increased for families across the wealth distribution. We suggest this points to a broad common trend of increasing financial prioritization of children over time.

Other Findings

In addition to education loans, we also consider mortgage and credit card debt, with a caveat that they cannot be attributed directly to children (see methodology section). In terms of mortgage debt, our descriptive analysis shows that families above median wealth have significantly higher mortgage debt than those below median wealth, with $37,000 and $174,000, respectively, in 2016. These differences hold across all racial-ethnic groups, even if absolute levels of mortgage debt are lower for Blacks and Hispanics than for Whites. The multivariate analysis of mortgage debt shows that increases during the 1998 to 2016 period are only notable for White families, especially above-median-wealth White families. In fact, additional analysis reveals that these results are driven by families in the top 10 percent of the wealth distribution. In contrast, credit card debt shows significant declines over time across racial-ethnic groups between 1998 and 2016, though it shows some increases over time for above-median-wealth White households.9 Lack of overtime increases in credit card debt would be consistent with the idea that expenditures on children are mostly focused on long-term investment, such as for education, rather than short-term investment on consumer purchases. These analyses also show the limit of arguments about conspicuous consumption on credit as a major driver of household debt in recent decades.

Education of the respondent is also an important determinant of financial investment, saving, and borrowing for children. Especially taking on education savings such as 529 plans is strongly related to holding an advanced degree for Whites and Blacks, but not pronounced for Hispanics. This suggests that understanding financial instruments is not only a matter of material resources but also a part of cultural capital. In addition, holding mortgage, education, and credit card debt among child households across racial-ethnic groups is consistently related to education, with higher education being associated with more debt.

Our analyses also show that single-parent families among Blacks have a significantly higher share of financial assets devoted to children than other Black family forms, which is consistent with qualitative evidence uncovering the painstaking efforts of Black single mothers to parent their children, despite racism and structural disadvantages (Turner 2020). Another noteworthy finding is that when the man, relative to a woman, is responding to the survey on behalf of the household, reported financial assets for children as a share of all assets as well as the absolute amount of these assets in White families are significantly lower. Similarly, reported education debt is significantly lower and mortgage debt is significantly higher when the male is completing the survey for the White child household respondents. These gender differences are not notable for Black or Hispanic families.

DISCUSSION

Our study examines the link between wealth inequality and families’ financial behavior related to their children using the Survey of Consumer Finances data, 1998 to 2016. We find evidence for our argument that, over the past few decades, American families increasingly practice financially intensive parenting, or engagement in financial investment, savings, and borrowing for the sake of their children, in large part to finance children’s education. In addition, we find that the types of financial instruments and amounts of money invested or borrowed vary significantly across wealth position of child households, in particular when we compare families below and above median wealth. Moreover, these activities differ significantly across race and ethnicity. Over time, White families above median wealth accumulate more financial assets and education savings as well as less education debt for children. This suggests that with greater education savings, such as in 529 plans, White wealthy families have been financing college for their children without having to take on significant parental college debt. In contrast, Black and Hispanic families across the wealth distribution have accumulated fewer financial assets under children’s names or co-owned with children. Moreover, Black families across wealth distribution have accumulated significant amounts of education debt relative to White families.

Scholars have documented the pervasiveness of the norm of intensive parenting (Ishizuka 2019). We place people’s understandings of how to parent in the context of significant macroeconomic changes, brought on by forces of financialization, globalization, deindustrialization, the rise of the service sector, and the increasing prominence of precarious work (Kalleberg 2009). Americans today worry more about economic security than they did in the past (Cooper 2014) and college education is considered paramount to securing prosperity (Immerwahr and Foleno 2000). However, the costs of higher education have been increasing (Ramey and Ramey 2010; Carr 2013), and students and their families have come to rely on loans to pay for college education (Avery and Turner 2012; Houle 2014; Zaloom 2019), to a point where outstanding student loan balances are approaching $1 trillion (Brown et al. 2014). All these structural changes have affected how families focus on investment in children, especially into children’s education. Our analysis shows that in the past two decades parents, not only college students, have taken on significantly more debt to cover their children’s college expenses. Moreover, parents have also intensified the use of other financial instruments that support the norm of intensive parenting, such as allocating financial assets under children’s names, and establishing education savings, such as 529 plans.

Additionally, we examine how this financially intensive parenting is affected by wealth inequality (Gibson-Davis and Hill 2021, this issue). Indeed, our analysis shows how unequal the consequences of financially intensive parenting are across the wealth distribution as well as racial-ethnic groups. It is the child households above median wealth, and especially White families, that have been able to accumulate increasingly more financial assets earmarked for their children as well as education savings that they can put toward their children’s college education. The education savings accumulated in 529 plans provide tax advantages. Also, because monies in these 529 plans are highest among White families in the top 5 percent of the wealth distribution, who are able to invest thousands of dollars, they provide the most tax advantages to already rich families.

In regard to Black and Hispanic families’ financial behavior for the sake of children, we find few differences across the wealth distribution of these families in the financial assets they are able to put aside for children. We do find evidence, however, that these families increasingly prioritize children, just as White families do, in the share of financial assets that they allocate toward children relative to their overall assets. Still, these financial assets for children as well as education savings for children by Black and Hispanic families are very low relative to what their White counterparts accumulate. In contrast, education debt for children has been increasing for families of all racial-ethnic backgrounds over the past two decades. Moreover, for Black families across the wealth distribution, education debt has grown to substantial amounts. This is consistent with studies on PLUS loans, which show disproportionate take-up of these government loans by Black families relative to other families. Cautioning, these studies conclude that “PLUS loans are becoming predatory for Black PLUS borrowers who are more likely to be low income and low wealth, and who will likely struggle to repay” (Fishman 2018, 7). Hence, debt for children’s college education represents significant pressure on limited resources of Black families who, at the same time, lack accumulation of financial assets and education savings for their children and have already seen their wealth holding decrease substantially in recent decades (Percheski and Gibson-Davis 2020) and are in a severely disadvantaged position relative to White families (Wolff 2018). Indeed, if Blacks take on education debt on predatory terms, as Louise Seamster and Raphael Charron-Chenier (2017) argue, then what seems like a valuable investment in children with potentially favorable outcomes is instead a liability with limited (or eliminated) longer-term benefits. Therefore, it is plausible that some of the devastating decline in Black child household wealth, 90 percent from 1998 to 2016 (table 2), is related to the fact that taking on education loans for their children has substantially depleted Black child household resources across generations. We hope that future research will more directly test this relationship.

Although our research provides empirical evidence on the rise of financially intensive parenting, our study has limitations. First, our analysis focuses on financial behaviors that we infer as related to long-term investing in children (such as education savings in 529 accounts or financial assets under children’s names). However, it is possible that parents consider many other financial activities as related to investing in their children. Mortgages for houses may be related to parental investment in good school neighborhoods (Frank 2007; Owens 2016) but cannot be directly attributed to investment in children. Also, we do not have information on child arrears. Further, we cannot distinguish conclusively whether certain education loans that households have are specifically for children’s education. Hence our workaround by restricting the age of parents to forty in the analysis of determinants of education debt is not ideal. Also, because the SCF collects data only on the actual financial activities and not on the meanings attributed to them, our analysis cannot directly address the process of the social meaning of money (Zelizer 1994) motivating parental behavior.

CONCLUSION

That inequality in the United States has substantially increased over recent decades is clear. It is much less known that both income inequality (Western, Bloome, and Percheski 2008) and wealth inequality (Gibson-Davis and Percheski 2018) rose faster among households with children than among those without children. To explain this phenomenon, we contend, requires special attention to the inner workings of child households related to the economy of parenting. Specifically, we focus in this article on the trends in parental financial investment, saving, and borrowing for children over the past few decades, and we compare these trends by wealth of families and by their race-ethnicity.

Based on analyses of nationally representative samples of U.S. households collected by the Survey of Consumer Finances, we find evidence of rising financially intensive parenting behavior across American families between 1998 and 2016. But we also find evidence of substantial inequality across families, depending on their wealth position and their racial-ethnic background, in the type of financial parenting activities they engage in and the amounts they invest, save, or borrow for the sake of their children. White families above median wealth have been putting aside significant amounts of assets under children’s names and accumulating education savings, which give them sizable tax advantages. On the other hand, Black and Hispanic families have significantly lower amounts of such assets in child-investment financial instruments, even if they have progressively increased assets that are dedicated to children as a share of all assets. Furthermore, Black and White families across the wealth distribution have accumulated significant amounts of education debt for their children. But Black families have less resources with which to repay the debt, and Black college graduates have lower earnings than Whites, limiting their ability to pay back loans. This suggests that the growing norm of intensive parenting across class and race—a valiant effort of families to try to do everything they can for their children—may, paradoxically, disadvantage children from minority households because it likely contributes to the growing intergenerational disparities in wealth inequality in America, most significantly between wealthy White child households and less well endowed Black child households (Gibson-Davis and Hill 2021, this issue; Percheski and Gibson-Davis 2020).

Ultimately, it appears that the price of parenting for American parents these days seems to be increasingly high, but not only in terms of the actual dollars invested, saved, or taken on credit for the sake of children. Instead, the high price of parenting is also borne by the society as a whole because of the significant inequality that results from the fact that some families benefit from investment into their children, and that others, trying equally hard to give their children opportunities these children deserve, further deplete their very limited resources. Consequently, when individual families attempt wholeheartedly to do everything they can for their children, including engaging in financially intensive parenting, the unintended societal consequences of such behavior mean that many children are left behind. Regrettably, the state and federal policies that financialize education, such as 529 plans and federal PLUS loans as well as linking school funding to property taxes, have likely widened disparities across families. Such policies encourage privatization of educational costs by individual families, but deep structural inequities across wealth and race have rigged the equality of opportunity in this education race. Structural reforms that call for better public funding of education from kindergarten through college are necessary if we are to see any systemic change that enshrines a collective responsibility for education and investment in all children.

Appendices

Trends for White Child Households

Source: Authors’ calculations based on the Survey of Consumer Finances (Federal Reserve 2020).

Note: Means per year for White families with children in the top 5 percent, top 20 percent, top 50 percent, and bottom 50 percent on wealth distribution, with confidence intervals (shades). All dollar values are in 2016 U.S. dollars. In the interest of visual comparability across all outcomes, we present the education savings (panel C) starting with 1998. The values for 1998 are zero because data on education savings are collected in the SCF only since 2001 (see data and methods section).

Descriptive Statistics

Regression for Financial Assets Under Children’s Names (Share of All Assets)

Regression for Financial Assets Under Children’s Names ($)

Regression for Education Savings Accounts, 2001–2016 ($)

Regression for Education Debt ($)

FOOTNOTES

↵1. Throughout the article, by Black we refer to those identifying in the Survey of Consumer Finances as non-Hispanic Black. Our data do not allow us to distinguish other racial-ethnic groups than White, non-Hispanic Black, and Hispanic. We define child households as those with children age twenty-four or younger.

↵2. Although the term assets is often used as synonymous with wealth, we use it in a narrower definition that refers to financial assets for children as the data from SCF allow us to distinguish. Financial assets for children include checking accounts, certificates of deposit, and savings and money market accounts under children’s names or co-owned with children.

↵3. Although the data for debt goes back to 1989, we present analysis for the period of 1998 to 2016 for all outcomes in the interest of consistency. Our conclusions remain the same when we extend analysis for debt to 1989.

↵4. If education savings accounts are reported as co-owned with children, then they are also included in the measure of financial assets co-owned with children. Notably, among families with children with some (nonzero) education savings, the vast majority (68 percent) do not co-own education savings accounts with children.

↵5. Following research by Christina Gibson-Davis and Christine Percheski (2018), we exclude the value of vehicles because their resale value is far less than the consumption value. Our results remain the same when the value of vehicles is included toward a household’s net worth.

↵6. For the individual-level sociodemographic attributes, we use the characteristics of the respondent reporting for the household. Because characteristics of all family members are reported by the respondent, we use these characteristics to minimize reporting errors. Our results remain substantively the same when we use average values between the respondent and the spouse (such as average educational attainment) or highest values of one of the spouses (such as, highest level of education). Data on children’s attributes in the SCF are collected only for coresident children. Because non-coresident children (in college, for example) and information on their characteristics is missing in the SCF, we do not include any characteristics of the children in the models presented. Our results remain the same when we control for coresident children’s attributes (such as age of the youngest coresident child).

↵7. Our results remain the same when the wealth measures do not exclude the values of wealth components used as our outcomes.

↵8. Two differences between our descriptive and regression findings relate to Hispanics, which may be due to the loss of statistical power. For the amount of financial assets under children’s names, the descriptive results indicate increases among all Hispanic families, and multivariate results indicate increases only for above-median-wealth Hispanic families. For education savings, the descriptive results indicate increases across all Hispanic families, but the coefficient is not significant in the multivariate framework, indicating no increases.

↵9. Analyses for mortgage and credit card debts are available on request.

- © 2021 Russell Sage Foundation. Bandelj, Nina, and Angelina Grigoryeva. 2021. “Investment, Saving, and Borrowing for Children: Trends by Wealth, Race, and Ethnicity, 1998–2016.” RSF: The Russell Sage Foundation Journal of the Social Sciences 7(3): 50–77. DOI: 10.7758/RSF.2021.7.3.03. Direct correspondence to: Nina Bandelj at nina.bandelj{at}uci.edu, 3151 Social Sciences Plaza, University of California-Irvine, Irvine, CA 92617, United States; and Angelina Grigoryeva at angelina.grigoryeva{at}utoronto.ca.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.