Abstract

The Affordable Care Act (ACA) introduced large changes to the individual market for health insurance. Using 2015–2019 HIX Compare and geographic-specific data, this study examines the volatility and vulnerability of local insurance markets using insurer participation and premium information. The study also examines how markets with higher volatility and vulnerability differ from others with respect to demographics, labor market conditions, health status, provider supply, and state policies. Entry and exit patterns suggest decreasing volatility, but forty-eight million Americans reside in markets that are vulnerable, given limited competition and high premiums.

In the United States, more than 250 million people are enrolled in private health plans (Berchick, Hood, and Barnett 2018; Jacobson et al. 2017: Kaiser Family Foundation 2018a). The market for private health insurance consists of several segments, each serving a distinct population. Segments include the large and small employer group markets for workers and their dependents; the individual market, which primarily serves non-elderly persons who may or may not participate in the labor force; and supplemental insurance for Medicare beneficiaries seeking additional financial protection against potential out-of-pocket medical expenses (Medigap). Private insurers also maintain large roles in the provision of insurance through publicly financed programs, including Medicaid managed care, Medicare Advantage, and Medicare Part D prescription drug coverage.

The Patient Protection and Affordable Care Act (ACA) of 2010 introduced significant changes to the federal regulation of private health insurance with particular focus on the individual market. The scale and complexity of these regulatory changes in conjunction with a high degree of political polarization around the ACA have created considerable uncertainty for insurers as they engage in strategic and operational decision making. Insurers’ participation and pricing decisions have important implications for consumer plan choice and affordability.

BACKGROUND

Historically, the individual market has been a residual market for those unable to obtain coverage from an employer or government source. Before 2014, in most states, people seeking individual coverage were subject to medical underwriting. Insurers could use information on a person’s age, sex, occupation, geographic residence, and medical history to determine eligibility, set premiums, or exclude coverage for specific, preexisting medical conditions. Based on a 2009 survey of America’s Health Insurance Plans (AHIP) members, the overall denial rate for individual market applicants was approximately 12 percent; rates approached 33 percent for those ages sixty to sixty-four (AHIP 2009). Although provisions within the Health Insurance Portability and Accountability Act included protections guaranteeing individuals access to a plan without preexisting condition exclusions, it did not regulate premiums, leading to affordability challenges for many seeking coverage (Pollitz 2017).

Provisions within the ACA sought to improve individual market functioning in several ways. First, the legislation created online marketplaces to facilitate easier access to information by consumers as they shopped for coverage. Second, it authorized and sponsored the creation of new health plans through the Consumer Operated and Oriented Plan (CO-OP) program as a way to stimulate insurance market competition (Harrington 2015). Third, it introduced greater standardization of plans based on actuarial values (defined as the percentage of an enrollee population’s covered medical expenditures that are paid for by the health plan) and required plans to include ten essential health benefits beginning in 2014 (CMS 2019b). Fourth, guaranteed issue provisions ensured that individuals could not be denied access to coverage on the basis of their health status, age, sex, occupation, or other factors. Modified community rating provisions also limited insurers with respect to the factors on which they could vary premiums to age (3:1), tobacco status (1.5:1), family composition, and geography. Finally, policymakers sought to increase coverage affordability for lower-income Americans by introducing advance premium tax credits (APTCs) and cost-sharing reduction (CSR) subsidies (CMS 2018b). Altogether, these changes were expected to transform the individual market so that it would better serve the needs of diverse population segments as well as improve equity in access to coverage and health outcomes (Grogan 2017).

By design, the individual market split into its on-Marketplace and off-Marketplace segments in 2014. The on-Marketplace is the segment through which persons with household incomes of between 100 and 400 percent of the federal poverty level (FPL) and no access to affordable alternatives may obtain subsidized coverage in the form of APTCs and CSRs. Individuals who are ineligible for subsidized coverage may purchase coverage from either the on- or the off-Marketplace. Despite certain differences between the on- and off-Marketplace segments in the characteristics of enrollees and plan offerings, regulations require that insurers treat both segments as a single risk pool in regard to setting premiums.1 As of the first quarter of 2019, an estimated 13.7 million Americans had individual market coverage, approximately 70 percent of policies purchased in the on-Marketplace and 30 percent of policies purchased in the off-Marketplace (Fehr, Cox, and Levitt 2019).

Recognizing the number and complexity of changes introduced in 2014, the federal government created two temporary and one permanent premium stabilization program to support the individual market. Operational from 2014 to 2016, the risk corridor program encouraged insurers to participate in the market by mitigating their risk from the uncertainty associated with setting premiums for an enrollee population likely quite different in terms of demand for medical care relative to enrollees before 2014. As a second temporary measure, the federal reinsurance program encouraged insurer participation by providing payments from the federal government to health plans that enrolled individuals who had high levels of medical spending during a plan year. By subsidizing a portion of high-cost enrollee expenditures, reinsurance mitigates an insurer’s risk of large financial losses and lowers overall premiums. Finally, the permanent risk adjustment program, also implemented in 2014, redistributes funds from plans that enroll disproportionately lower risk individuals to those that enroll disproportionately higher risk. By doing so, risk adjustment discourages insurers from pursuing tactics to select healthier enrollees for financial gain (Cox et al. 2016).

Despite these premium stabilization programs, insurers selling individual market coverage since the ACA was passed have experienced considerable uncertainty as they attempt to understand the preferences, health status, and expected costs of potential enrollees. Furthermore, several federal policy shocks have adversely affected insurers. Examples include the federal government’s decision to not make risk corridor program payments to insurers, leading to numerous legal challenges (Keith 2018a); Republican-led efforts to repeal and replace the ACA in 2017; elimination of the individual mandate penalty as part of the Tax Cuts and Jobs Act of 2017 (Pear 2017a); the Trump administration’s decision to cease CSR payments to insurers, but to require them to continue offering such plans in the Marketplace for plan year 2018 and beyond (Pear 2017b); reductions in federal-government-sponsored advertising to promote on-Marketplace enrollment (Shafer et al. 2020), and the administration’s executive order to expand the availability of short-term and association health plans in 2018 (White House 2017).

Many state and federal policymakers remain concerned about consumers’ access to and affordability of coverage. Although access has improved for those who would have been denied coverage because of preexisting medical conditions and for lower-income Americans who could not otherwise afford coverage, another challenge has emerged—limited insurer participation in local geographic markets (Griffith et al. 2018). Research has established important linkages between insurer participation and individual market outcomes. Specifically, the number of insurers participating in a market is associated with fewer plan choices, including diversity of plan types (for example, HMOs, PPOs) and the availability of platinum level plans (Abraham, Royalty, and Drake 2019). The body of evidence is also growing that local markets with only one or two insurers have significantly higher premiums than those with more competitors (Dafny et al. 2015; Jacobs et al. 2015; Abraham et al. 2017; Zhu et al. 2017; Polyakova et al. 2018; Drake and Abraham 2019). The relationship between competition and affordability is more complex in the individual market, given the APTC subsidy design. Households that are APTC-eligible as a result of having incomes of between 100 and 400 percent of FPL are protected from rising premiums because their out-of-pocket requirements are based on a percentage of their household income rather than on premiums themselves. In contrast, individuals with household incomes greater than 400 percent of FPL bear the full effects of rapid premium growth, creating significant affordability challenges in some markets (Drake and Abraham 2019). Affordability concerns have escalated further for the unsubsidized population segment because states and insurers have responded to federal CSR payment cuts by building those expected costs into premiums through “silver loading” practices (Anderson, Abraham, and Drake 2019).

In the section that follows, I introduce a conceptual framework of insurer decision making and define the market-level concepts of volatility and vulnerability.

CONCEPTUAL FRAMEWORK

Firms make strategic and operational decisions regarding the types of products or services to sell and the geographic markets in which to sell them. Within the market for private health insurance, an insurer must first decide on the particular segments (employer group, individual, Medicare Advantage, and so on) in which to operate. For the individual market, this decision also includes whether to participate in the on- or off-Marketplace, or both. Conditional on individual market participation, an insurer must then decide which geographic markets to serve. Because insurance markets are regulated at the state level, insurers may first choose which states to enter and then select the particular local markets in which to operate.Since ACA passage, local markets for individual coverage most often are defined using the geographic rating area (GRA) or the county. Geographic rating areas are typically individual counties or clusters of counties that exhibit similar unit costs.2 Given data availability, I define local markets as a GRA within a state.

Insurers’ entry and exit decisions are driven largely by their expectations about financial performance, which may include a particular profit margin or break-even threshold, depending on a firm’s ownership status and objectives. An insurer’s expected revenues depend on the premiums it sets for its offered plans, enrollment, and any risk adjustment payments. Enrollment and risk adjustment payments depend not only on an insurer’s own decisions but also on the decisions of other insurers in the market. Although these competitive dynamics may be potentially important to an insurer’s financial outcomes, they are challenging to model empirically and are beyond the scope of this analysis.

An insurer’s costs include both claims incurred for medical goods and services that are covered by policies as well as administrative expenses. Medical claims costs are a function of an insurer’s contractual agreements with providers (for example, hospitals, physicians, and laboratories) around payments for services as well as use by its enrollee population. The market power of physician groups, hospitals, and health systems stemming from increased consolidation over time in local markets may result in higher negotiated payment rates for medical services, higher claims costs, and ultimately higher premiums for enrollees (Scheffler et al. 2016; Van Parys 2018). Use is expected to depend on several factors, including enrollees’ demographic attributes, income, health status, and the benefit design (such as annual deductibles and coinsurance3). Administrative costs include claims adjudication, broker and agent commissions, marketing, use management, and quality improvement activities. Insurer participation decisions also may be affected by complementarities in production, including cost efficiencies generated by selling coverage in other market segments (such as the employer group market or Medicare Advantage).

Finally, federal or state-level insurance regulations may facilitate or mitigate an insurer’s likelihood of individual market participation. Federal medical loss ratio regulations, for example, specify that insurers must spend at least 80 percent of premiums on medical care or quality improvement activities in the individual market or they must issue consumer rebates (CMS 2018c). States may also pass legislation or implement regulatory changes that influence insurer participation. Examples include state-based premium stabilization efforts through 1332 state innovation waiver programs; state mandates to require residents to have insurance coverage; limiting consumer access to non-ACA-compliant plans, such as short-term and limited duration plan offerings; and regulations that link an insurer’s participation in the individual market to public insurance program participation (Center on Health Insurance Reforms 2019). Weighing these considerations, insurers make entry and exit decisions that in turn determine the supply side of a local market.

Consumer choice and affordability are two important outcomes that align with the ACA’s goal of a better functioning individual market. Consistent with this, I use information on insurer participation and premiums to define the concepts of individual market volatility and vulnerability. Volatility reflects the magnitude of changes over time in insurer participation and premiums within local geographic markets. Let us consider a simple example of two hypothetical markets—market A and market B. Suppose market A had eight active insurers in 2015 but then experienced significant exit and was left with only two active insurers in 2019. Moreover, suppose that over this period, market A experienced large premium growth resulting in a 120 percent cumulative increase in the lowest cost silver plan premium available to consumers. In contrast, market B started with four insurers in 2015 and had three in 2019. Although market B experienced premium growth, it was a 70 percent cumulative increase in the lowest cost silver plan premium over the same period. In this example, market A would be classified as having higher volatility relative to market B, given its larger changes over time in insurer participation and premium growth.

Volatility was expected during the initial implementation period, but markets have varied widely in terms of the magnitude of changes in both insurer participation and premiums. Even if a local market is relatively stable in terms of both, it may still be vulnerable if consumers’ plan choices are limited and coverage is deemed unaffordable. Local market vulnerability is assessed based on a local market’s current performance with respect to insurer participation and premium levels relative to the distribution of performance on these dimensions across geographic markets. Drawing on our example, if market A’s number of participating insurers is small and below the median value and its lowest cost silver plan premium is above the median value of the distribution, then market A would be classified as having higher vulnerability compared to market B. In the next section, I summarize my empirical approach for investigating individual market volatility and vulnerability as well as the market-level factors associated with these outcomes.

EMPIRICAL APPROACH

Data

The primary data source to examine local market volatility and vulnerability across the United States is the 2015 to 2019 HIX Compare from the Robert Wood Johnson Foundation, October 2018 release.4 The HIX Compare data include comprehensive information on insurers’ offered plans across GRAs in the on- and off-Marketplaces.5 Using the HIX Compare plan-level file, I created an analytic extract to measure the number of unique insurers and lowest cost silver plan premium offered in each GRA-market segment (on- versus off-Marketplace) year.

Next, I augmented the HIX Compare data with several sources of geographic-specific information to provide a comprehensive picture of how markets that exhibit higher volatility or vulnerability differ from those that do not (HHS 2018; University of Wisconsin 2018; U.S. Census Bureau 2018; BLS 2018; Kaiser Family Foundation 2018b; AANP 2018; NCSL 2018).6

Measures

Markets are classified as having higher volatility if the percentage change in the number of their insurers over the period (the number of insurers in 2019 less the number of insurers in 2015 divided by the number of insurers in 2015) is smaller than the median (reflecting larger declines in insurer participation) and the percentage change in the lowest cost silver plan monthly premium for a fifty-year-old, nonsmoker exceeds the median value of the distribution. I selected the lowest cost silver plan as the focal plan because it is the most affordable choice within the most popular level of plan generosity metal tier selected by consumers in the individual market (CMS 2019a). Analogously, I define a market as exhibiting higher vulnerability if its level of insurer participation is below the median value and its lowest cost silver plan premium is in excess of the median value in 2019.

Insurance markets in rural geographic areas are distinct from urban markets on a number of dimensions (HHS 2018). To account for this in the construction of the market volatility and vulnerability measures, I first stratified the sample of markets based on whether a GRA includes rural counties only (rural) or whether it is a market with urban counties only or a mixture of urban and rural counties (urban-mixed). I then applied the criteria for volatility and vulnerability based on the specific distributions corresponding to each subsample.

To better understand the attributes of the populations affected by individual market volatility and vulnerability, I considered several geographic-specific characteristics. These include the market size and demographic composition, labor-market conditions, health status of the adult population, provider supply, and the policy and political environment. I measure market size using information on the GRA’s total population and the percentage of adults younger than sixty-five who are uninsured. To capture the population’s racial diversity, I include the percentage of a GRA’s population that reports being nonwhite. Local labor-market conditions are associated with access to employer group coverage as well as income, which may affect potential demand for individual market coverage.7 Using three measures from federal data sources, I include the unemployment rate, average annual payroll per worker, and the percentage of establishments that are very small (defined as having one to four workers) in the GRA.

To capture the health status of the local market population, I include several measures: the percentage of the adult population in the GRA self-reporting fair or poor health status, the average number of days per year of poor mental health reported by adults, the percentage of individuals reporting a diagnosis of diabetes, the percentage of adults who smoke, and the percentage of adults who are classified as clinically obese based on having a body mass index of 30 or greater.8

The supply of providers within the local market is hypothesized to affect both enrollees’ access to medical care as well as insurers’ abilities to contract with providers to include in a plan’s provider network. The first measure of provider supply is the number of hospital beds per ten thousand persons in the market; the second measure is a binary indicator for whether the market is located in a state that permits full scope of practice for nurse practitioners. Full scope of practice expands primary care capacity, which may be important to insurers seeking to comply with state-based provider network adequacy requirements.

Finally, I consider several state-level measures to capture the policy and political environment. Two factors, including whether the GRA is located in a state that expanded Medicaid over the period and whether the GRA is located in a state did not approve the continuation of transitional plans (grandmothered plans in effect between March 23, 2010, and end of 2013), are expected to influence the composition of the individual market risk pool. Both decisions are likely to be favorable to on-Marketplace insurers. Additionally, I consider whether the GRA is located in a state with its own rather than the federal Marketplace. This policy measure likely reflects a state’s preference to have greater control over decisions and resources to promote insurer participation, coverage affordability, and outreach efforts. Finally, I include a measure of whether the GRA is in a state that had a Democratic governor as of 2015. Affiliation with the Democratic Party is expected to be positively related to support for the ACA and inversely related to the likelihood of markets in that state being more volatile and vulnerable.

Sample

The final sample includes 480 GRAs across the United States. I excluded from consideration markets located in states that use three-digit zip codes in lieu of county-based geopolitical boundaries for their service area designation (such as Massachusetts, Alaska, and Nebraska). I also excluded GRAs located in the states of Washington and New Jersey given changes in GRA definitions over the period.

Methods

This descriptive analysis uses univariate, bivariate, and multivariate statistical methods. To examine differences in the proportions and means of market attributes across volatility and vulnerability categories, I used chi-square and one-way analysis of variance methods. Additionally, I estimated binary logistic regression models for the probability that a local market exhibits higher vulnerability to estimate the independent effects of particular demographic, economic, health-related, and policy or political factors on the outcome.

RESULTS

Market Volatility

In the years immediately following implementation of the ACA’s regulatory changes, insurers quickly learned about the actuarial and political risks associated with operating in the individual market (Hall 2020). Although the introduction of large government subsidies to enhance coverage affordability led many insurers to perceive the individual market as increasingly attractive, the new regulatory environment also eliminated insurers’ ability to use medical underwriting and mandated more transparent price competition. Given the scale and scope of reforms, some market volatility was to be expected initially, although the expectation was that if the premium stabilization programs were implemented fully, the degree of volatility could be lower.

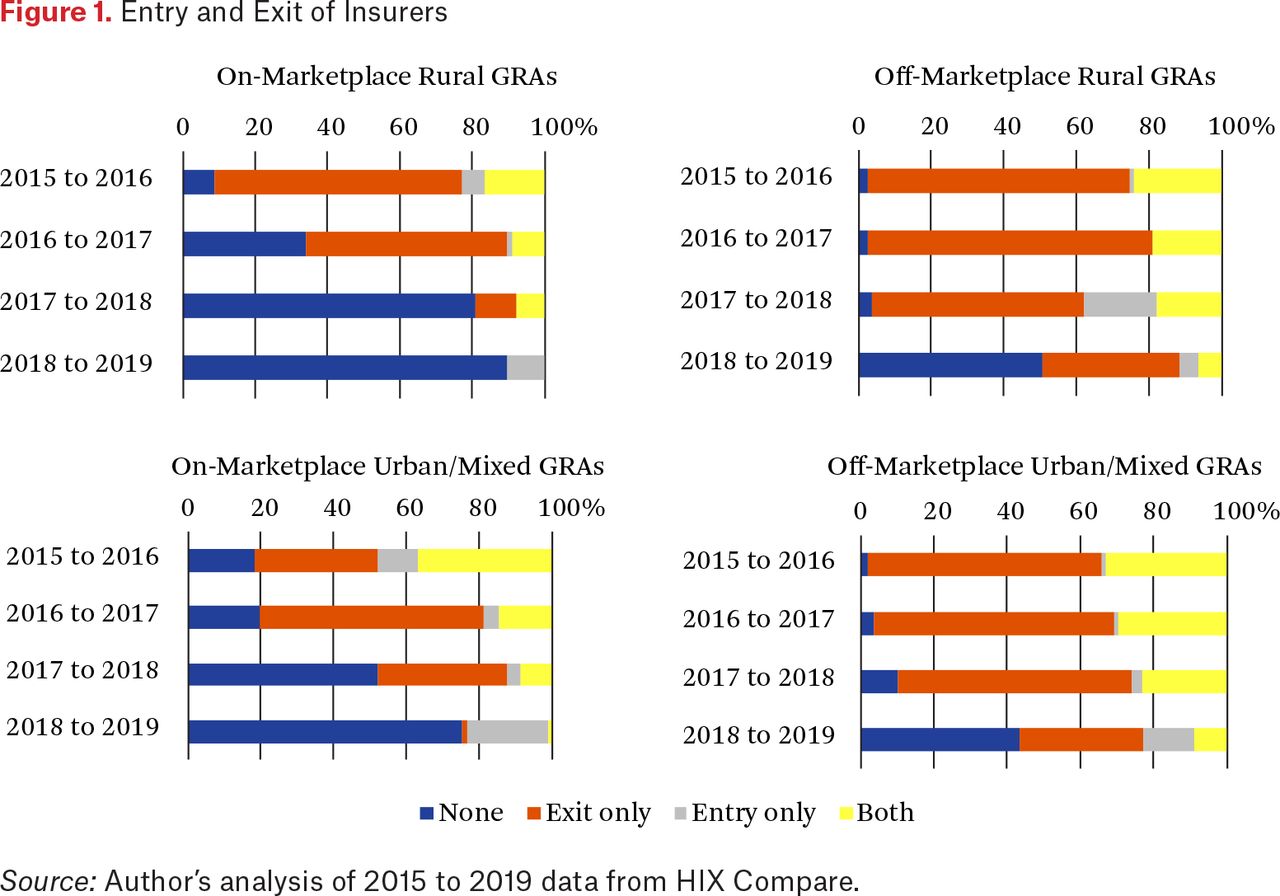

Figure 1 summarizes overall insurer entry and exit behavior across the 480 GRAs, including 79 rural markets and 401 urban-mixed markets. The exhibit depicts the share of markets each year that experienced no entry or exit by insurers, exit only, entry only, or both entry and exit, separately for each combination of Marketplace segment and market type (rural versus urban-mixed). Between 2015 and 2016, more than 30 percent of urban-mixed markets in the on- and off-Marketplace segments experienced both entry and exit. Rural markets, in contrast, were much more likely to have incumbent insurers exiting without new entry. Between 2016 and 2017, insurer exits accelerated in both the on- and off-Marketplace segments, given significant financial losses by insurers as well as continued uncertainty generated by Republican-led efforts to repeal and replace the ACA. By 2018 or 2019, the observed patterns of entry and exit behavior reveal increasing stabilization. More than 70 percent of GRAs experienced neither entry nor exit of insurers in the on-Marketplace in 2019, and 25 percent of markets experienced entry only. Notably, the off-Marketplace appears to be slower to reach a stable position with respect to insurer participation than the on-Marketplace.

Entry and Exit of Insurers

Source: Author’s analysis of 2015 to 2019 data from HIX Compare.

Table 1 summarizes the distribution of changes in both insurer participation and premiums within local markets over the 2015 to 2019 period. In the on-Marketplace segment, half of all markets experienced at least a 50 percent decline in the number of insurers. For the off-Marketplace segment, the median change was –71.43 percent in urban-mixed markets and –80 percent in rural markets. Within-market growth for the lowest cost silver plan premium offered was also large in absolute terms and relative to other insurance market segments (employer group coverage, for example) during this period. For approximately one-quarter of local markets across the on- and off-Marketplace segments, lowest cost silver plan premiums have grown in excess of 100 percent between 2015 and 2019.

Percentage Change in Number of Insurers and Lowest Cost Silver Plan Premiums, 2015–2019

Applying these criteria based on within-market changes in insurer participation and premiums over time, 148 GRAs in the on-Marketplace and 132 in the off-Marketplace may be classified as exhibiting higher volatility. Of these, 119 markets exhibit higher volatility in both segments, affecting an estimated 38.9 million persons (12.5 percent of the total population in markets analyzed).

Market Vulnerability

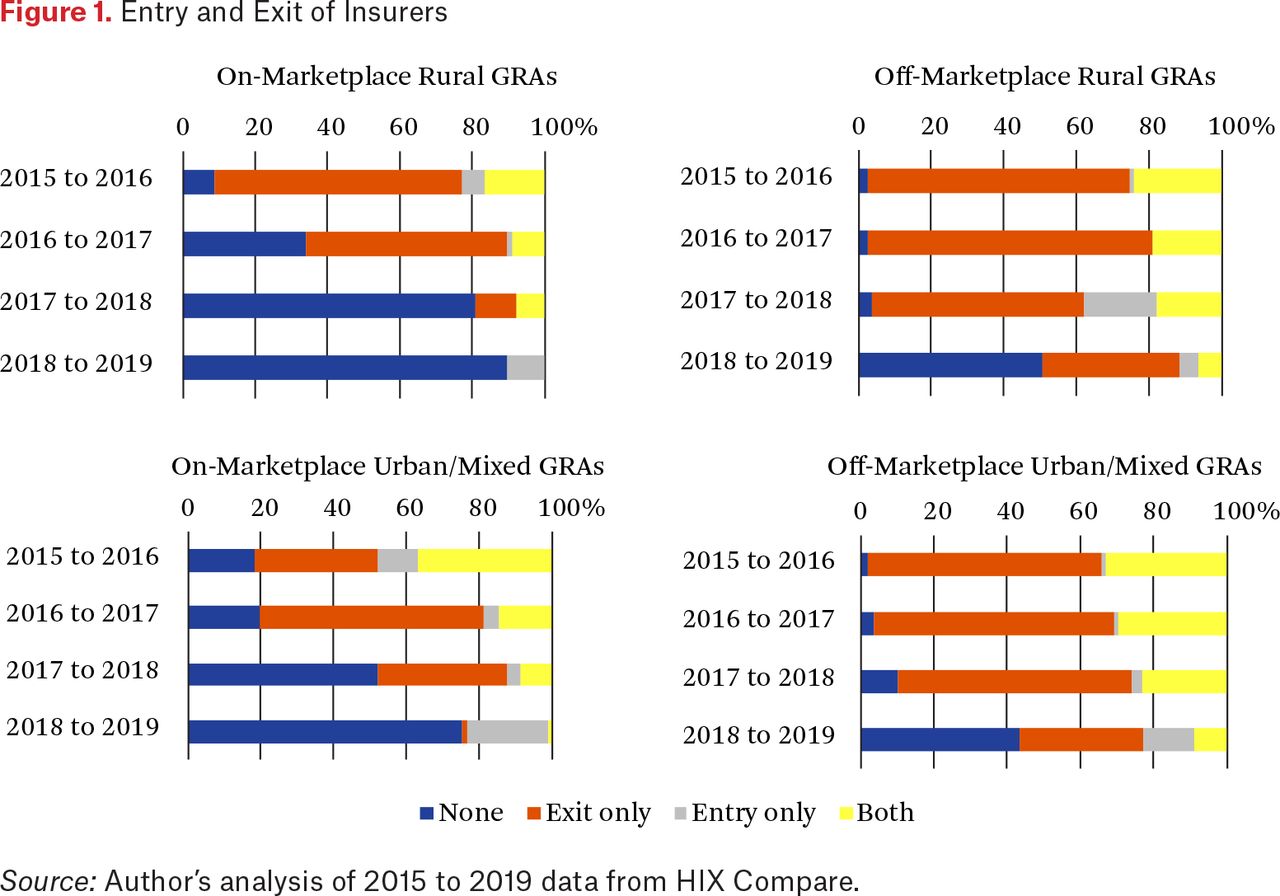

Markets are classified as exhibiting higher vulnerability if their insurer participation in 2019 is below the median value of the distribution and their premium amount for the lowest cost silver plan is above the median in 2019. Figure 2 summarizes insurer participation in 2019 by Marketplace segment and market type (urban-mixed and rural).

Insurer Participation in 2019

Source: Author’s analysis of 2015 to 2019 data from HIX Compare.

In 2019, more than 60 percent of rural markets in both the on- and off-Marketplace segments are served by a single insurer and more than 80 percent have two or fewer insurers. The majority of urban-mixed market types also face challenges with respect to insurer participation; only 40 percent of markets have at least three insurers competing with one another in both the on- and off-Marketplaces.

Table 2 summarizes the focal plan premium distribution in 2019 by Marketplace segment and market type. Within the on-Marketplace segment, average monthly premiums for the lowest cost silver plan offered to a fifty-year-old, nonsmoker are higher in rural markets ($771) relative to urban-mixed ones ($656). In the off-Marketplace segment, average premiums are slightly lower in absolute levels, but urban-rural differences persist ($630 in urban-mixed versus $755 in rural markets).

Distribution of 2019 Monthly Premiums for Lowest Cost Silver Plan for a Fifty-Year-Old, Nonsmoker

Using information on both current market structure and premium levels, 186 GRAs in the on-Marketplace and 194 GRAs in the off-Marketplace may be classified as exhibiting higher vulnerability. Among these markets, 166 GRAs exhibit higher vulnerability in both segments, affecting approximately forty-eight million persons residing in these areas (15.6 percent of the total population).

Characterizing Markets by Volatility and Vulnerability Status

Table 3 summarizes the attributes of local markets based on their classification into one of four mutually exclusive categories: market exhibits lower volatility and lower vulnerability, market exhibits higher volatility and lower vulnerability, market exhibits lower volatility and higher vulnerability, and market exhibits both higher volatility and higher vulnerability. Findings are reported separately for the on- and off-Marketplace segments.

Differences in Market Attributes Across Volatility and Vulnerability Categories

Within the on-Marketplace segment, 186 of 480 (38.75 percent) markets can be classified as exhibiting higher vulnerability (sixty-four are higher vulnerability only and 122 are both higher volatility and vulnerability). Differences in market size are significant between those that are more vulnerable and those that are not. The average population in markets that have lower volatility and vulnerability is 854,067. In contrast, the average population in markets that have higher volatility and vulnerability in the on-Marketplace segment is 272,712. A similar pattern is observed for the off-Marketplace segment.

In addition to having significantly smaller populations, the racial composition of more vulnerable markets is different than those of less vulnerable markets. Specifically, in the on-Marketplace segment, the average percentage of the nonwhite population is 24.25 percent among markets with higher volatility and vulnerability and 17.77 percent among those with lower volatility and vulnerability. More vulnerable markets also appear to have higher rates of uninsurance among the non-elderly population as of 2015.

Local labor-market conditions, including the unemployment rate, the share of businesses that are small (one to four workers), and average payroll per worker, are all associated with demand for health insurance. Of the three measures considered, only the average payroll per worker measure is found to vary systematically with individual market volatility and vulnerability. For the on-Marketplace segment, markets with lower volatility and vulnerability report an average payroll per worker of $41,404 relative to $37,214 in markets with higher volatility and vulnerability. The pattern is similar for the off-Marketplace segment.

Next, I examine how the health status of populations differs by market classification. Analyses show that the average health status of populations in markets with higher volatility and vulnerability is worse on every measure relative to markets with lower volatility and vulnerability. For example, within the on-Marketplace segment, the average percentage of adults with diabetes is 12.25 percent in markets with higher volatility and vulnerability and 10.54 percent in those that are lower on both dimensions. With respect to smoking prevalence and obesity, significant differences also persist, rates being generally higher among markets with higher volatility and vulnerability than among those with lower volatility and vulnerability.

The ability of consumers to access medical care is another factor insurers might consider when deciding whether to sell coverage in a particular geographic market. However, I find no significant differences across market categories in regard to the average number of hospital beds per ten thousand persons. Primary care capacity is another factor given that insurers in many states are required to demonstrate that they have an adequate provider network. One way primary care capacity can be expanded is allowing nurse practitioners full scope of practice—that is, diagnose and treat patients, including prescribing medications and controlled substances under the exclusive licensure authority of the state board of nursing (AANP 2019). I find that the percentage of markets in states with full scope of practice laws are much less likely to exhibit higher volatility and vulnerability than those that do not (8.2 percent versus 22.76 percent in the on-Marketplace, for example).

The next set of attributes pertain to the ACA-specific policy decisions made by state governments where the market is located. Policies include whether the state expanded Medicaid, whether the state had a state-based marketplace, and whether the state opted to prohibit transitional plans (such as grandmothered plans). Finally, I consider one measure that reflects the party affiliation of a state’s governor in 2015. All of these measures are hypothesized to be associated with the degree of state-level support for the ACA’s goals and the efforts taken by state governments to promote a well-functioning individual market. Findings suggest that markets that have lower volatility and vulnerability are much more likely to be located in states that chose to expand Medicaid, those that established their own marketplaces, those that prohibited transitional plans, and those with a Democratic governor in office as of 2015.

Predicting Higher Market Vulnerability

As a final exercise, to better understand the independent effects of various market attributes on this outcome, I estimate binary logistic regression models corresponding to the probability that a market exhibits higher vulnerability. Given high levels of multicollinearity among subsets of market attributes, I opt for a more parsimonious specification. Table 4 reports marginal effects and standard errors with separate models estimated for the on- and off-Marketplace segments.

Binary Logit Model of Probability of Higher Vulnerability, Marginal Effects

Table 4 shows that the probability that a market is more vulnerable is inversely related to market population. The multivariate results also affirm the inverse associations between state policy decisions to expand Medicaid eligibility and adopt a state-based marketplace and higher vulnerability propensity. In contrast, smoking prevalence within a local market is positively related to higher vulnerability, all else constant. The multivariate results indicate some differences between the on- and off-Marketplace segments. Notably, in the off-Marketplace segment, markets with higher percentages of non-elderly uninsured are less likely to be characterized as having higher vulnerability and markets with higher percentages of nonwhite persons are more likely to be classified as having higher vulnerability. Other factors are statistically insignificant (average payroll per worker, for example) or opposite in sign (such as full scope of nursing practice) to patterns observed in the simpler, bivariate analyses.

DISCUSSION, POLICY ALTERNATIVES, AND CONCLUSION

Insurer participation and premiums are two key dimensions of individual market performance and have direct implications for consumer choice and affordability. Not only do insurers’ decisions affect what types of plans are available for purchase, including specific benefit designs and the providers accessible to enrollees within the plans’ networks, but their pricing behavior also determines coverage affordability, particularly for consumers who are ineligible for advance premium tax credits.

Looking across markets, insurer entry and exit patterns over time suggest that an increasing proportion of markets have begun to stabilize. However, almost 39 percent of markets in which forty-eight million people reside have two or fewer insurers with offered plan premiums that are high in absolute terms (for example, averaging $7,250 annually for the lowest cost silver plan premium for a fifty-year-old). Markets characterized by higher vulnerability are distinct from those that are not on three key dimensions. First, across the on- and off-Marketplace segments, markets that exhibit higher vulnerability have significantly smaller populations, on average. Insurers may perceive those markets as having too little potential demand to support their ability to meet financial expectations. Second, the empirical results suggest that markets in which populations are in poorer health status are more likely to be vulnerable as of 2019. Some evidence also suggests that these markets are more likely to have a higher percentage of nonwhites as well as higher rates of non-elderly uninsured. The third dimension relates to state policy decisions about ACA implementation, including the decision to expand Medicaid eligibility and the decision to establish a state-based marketplace. Although both decisions convey overall support for the policy goal of expanding coverage in order to reduce the number of uninsured, the choice of establishing a state-based marketplace further signals state policymaker intention to directly invest resources in infrastructure and processes that support individual market functioning.

Limitations

This study is subject to several limitations. First, although the HIX Compare data are a valuable resource for studying the individual market given their breadth and timeliness, the data vendor acknowledges potential issues of completeness, particularly for off-Marketplace insurers (HIX Compare 2019). Thus, analyses related to the off-Marketplace should be interpreted with some caution. Second, as part of their decision making, insurers may choose to selectively enter specific counties within a multicounty GRA. Unfortunately, the HIX Compare data in their current form cannot support a county-level analysis of insurer participation for the off-Marketplace. However, the use of a GRA-based market definition is a reasonable trade-off to be able to analyze conditions in the off-Marketplace, which is of increasing importance for the subsidy-ineligible population that faces full exposure to rising premiums. Some counties within GRAs may be even more vulnerable should insurers engage in selective entry and not offer plans in certain counties within a GRA. Third, as noted, a few states use designations based on zip codes rather than counties in defining some or all of their geographic rating areas. These markets are located primarily in Massachusetts, Alaska, and Nebraska. As a result, the findings presented here do not generalize to the entire country. Finally, individual market vulnerability is a subjective concept. Other market attributes may factor into insurer decision making but are not easily observed by researchers or policy analysts. Such examples include insurer negotiating power with particular providers in local markets, state-level enforcement activities of provider network adequacy requirements, and approaches adopted by state insurance commissioners to engage with insurers regarding participation and premium setting.

State and Federal Actions to Address Market Vulnerability

To address individual market vulnerability, state and federal policymakers are taking several distinct approaches to address concerns about choice and affordability resulting from lack of robust competition and high premiums. One common strategy is to establish state-based reinsurance programs, which can protect health insurers against the risk of high-cost claimants, lead to lower offered premiums, and encourage entry or retention of insurers in the individual market. To date, twelve states (Alaska, Colorado, Delaware, Maine, Maryland, Minnesota, Montana, New Jersey, North Dakota, Oregon, Rhode Island, and Wisconsin) have acquired 1332 state innovation waivers to establish reinsurance programs; the application of one other state (Georgia) is pending (Kaiser Family Foundation 2019).

Other state efforts seek to more actively regulate the individual market risk pool to address insurers’ concerns about adverse selection and subsequent impacts on premium growth. At present, thirteen states and the District of Columbia limit transitional plans from being sold in the market and three states (Massachusetts, Vermont, and New Jersey) maintain state coverage mandate requirements (Center on Health Insurance Reforms 2019). Both types of policies encourage broad representation of health risks in the ACA-compliant risk pool to promote stable premiums. A few states are also addressing consumer affordability challenges directly. For example, California has allocated temporary funding to provide subsidies to households with incomes of up to 600 percent of the federal poverty level. The state of Washington also recently passed legislation to expand subsidy eligibility for those with incomes of up to 500 percent of FPL (Tolbert et al. 2019).

Another approach being explored involves modifying market definitions. As noted, more vulnerable markets are considerably smaller in population. States may consider enlarging or modifying the composition of geographic rating areas to create large enough scale to support multiple insurers in a market. This could include, for example, mandating that all GRAs have at least one urban county (Frank 2019). Although larger markets may be more attractive to insurers, given larger volumes, concerns remain about establishing adequate networks of primary care, specialty care, and hospital-based providers across the entire geographic area. Expanding market sizes also create the potential for larger cross-subsidization across counties within the GRA if those counties are heterogeneous in enrollees’ claims experience. Other states have considered merging their individual and small group market. This type of action may lead to a larger risk pool, but it also introduces concerns related to cross-subsidization if the risk pool for the small group market is healthier than that of the individual market.

Both state and federal policymakers are also examining options related to expanding consumer choice of plans, whether within or outside the ACA’s Marketplace reforms. One incremental strategy is to tie insurer participation in the individual market to that of another program, such as Medicaid. Offering a public option is another initiative gaining traction in a few states, including Washington and Colorado. Policymakers are interested in whether a public option can offer more plan options at lower costs, particularly in geographic markets that are too small to support multiple insurers. Examples include a standalone, government-sponsored plan or a buy-in option for an existing government-sponsored program, such as Medicaid (Brooks-LaSure et al. 2019). Proponents of public option strategies argue that these programs can provide coverage more affordably than current private insurance given administrative efficiencies and provider payment rates that are generally lower than those of commercial insurers. One point of debate over a public option is its scope. In other words, should a public option be created to compete with private insurers in a local market, or should a public option be available only for markets in which no insurers are willing to sell coverage (Frank 2019). Financing a public option is a second area of concern. Although the idea remains popular, states continue to struggle with how they might finance such a program, particularly when new state monies would need to be identified or states would require federal approval and pass-through funding to support implementation efforts.

Finally, at the federal level and within several states, policymakers are advocating for expanded plan options that are not ACA compliant. Short-term, limited duration plans are one such example. Through a regulatory change introduced by the Trump administration in August 2018, insurers are now able to sell short-term limited duration health plans for periods of up to 364 days per year with the potential to renew them up to three years. This rule change significantly expands the length of time and renewability of these plans relative to what was permitted under the Obama administration (Keith 2018b). Short-term plans differ from ACA-compliant plans sold on the on- and off-Marketplaces in terms of eligibility limits and coverage limits. Individuals can be subjected to medical underwriting and preexisting conditions may be imposed. Benefit designs may also exclude certain services (maternity care, for example) and not have limits on cost sharing (such as deductibles) Although these plans may provide more affordable options to healthy individuals, they also have the potential to further segment the individual market risk pool and create upward pressure on premiums within the ACA-compliant individual market. Currently, twenty-three states and the District of Columbia regulate short-term plans more stringently than the federal rule. A second alternative type of coverage gaining popularity includes Farm Bureau plans, which are currently approved for sale in the states of Kansas, Iowa, and Tennessee. Like short-term plans, Farm Bureau health plans do not have to comply with ACA regulations and may rely on medical underwriting for determining eligibility and setting premiums (Tolbert et al. 2019).

CONCLUSION

Today, almost fourteen million Americans rely on the individual market for health insurance (Fehr et al. 2019). The individual market enrollee population is heterogeneous in terms of age, sex, racial composition, rurality, income level, labor-force attachment, and health status. Although the individual market overall has become less volatile over the past five years, many local markets remain vulnerable because of low insurer participation and high premiums. Analyses reveal that markets characterized as more vulnerable are smaller in population, have poorer health status, and are less likely to be in states that expanded Medicaid eligibility or have state-based marketplaces. State policymakers and regulators play a critical role in ensuring market conditions capable of supporting consumer choice and affordable options for all individuals seeking coverage, regardless of income or health status. As first-mover states implement strategies to address concerns about plan choice and affordability, it will be important to evaluate the effectiveness of such interventions so that other states may learn what works and what does not in creating a well-functioning individual market.

FOOTNOTES

↵1. Non-ACA compliant plans are also sold in the off-Marketplace segment, but are not part of the same risk pool. These include plans that have grandfathered or grandmothered status as well as other types of plans that do not conform to ACA minimum requirements or regulations (for example, short-term duration plans). Grandfathered plans are plans that were in force before 2010, whereas grandmothered plans are those that were in force between 2010 and 2014. In this study, I consider only ACA compliant offerings because no data exist at a local level to capture noncompliant plans.

↵2. Although the vast majority of states use county-level geopolitical units to create rating areas, a few use zip code–based service area designations. I do not consider local markets in states that use zip code–based service area designations.

↵3. A deductible represents an amount that an insured person must pay out-of-pocket prior to the insurer paying for medical services incurred. Coinsurance is the percentage of the total allowed amount for a covered medical service to be paid by the enrollee.

↵4. HIX Compare datasets 2014 to 2019 available at https://www.hixcompare.org/ (accessed February 24, 2020).

↵5. County-level data are available for the on-Marketplace, but an accurate count of number of insurers in the off-Marketplace at the county level is not possible. Given this, I use the GRA as my market definition.

↵6. For most geographic-specific measures, I use information from the baseline year, 2015. Exceptions to this include the state policy measures that reflect activity between 2015 and 2018.

↵7. The percentage of small business establishments in a local market may be particularly important. Some policymakers anticipated that a reformed individual market could provide a viable substitute for workers in small firms if those employers decided to stop offering group coverage.

↵8. For all multicounty GRAs, I construct GRA-level market attributes based on either aggregation of county-level values to the GRA-level (such as population) or as a weighted average of the county-level market attributes, depending on the particular measure. Weights are constructed as the share of the GRA’s total population located within a given county.

- © 2020 Russell Sage Foundation. Abraham, Jean Marie. 2020. “Individual Market Volatility and Vulnerability, 2015 to 2019.” RSF: The Russell Sage Foundation Journal of the Social Sciences 6(2): 206–22. DOI: 10.7758/RSF.2020.6.2.09. The author would like to thank the Robert Wood Johnson Foundation for financial support (Award #75027). The views expressed here do not necessarily reflect the views of the foundation. Direct correspondence to: Jean Marie Abraham at abrah042{at}umn.edu, 420 Delaware St. SE, MMC 729, Minneapolis, MN 55455.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.