Abstract

As wealth inequality increases, the importance of parental financial transfers for socioeconomic attainment may also rise. Using data from the 2013 Panel Study of Income Dynamics Rosters and Transfers Module, this study investigates two questions: how parental financial transfers for education have changed over time, and what the relationship is between these transfers and adult socioeconomic outcomes. Results suggest that transfers for education have increased, have become more commonplace, and have become more dependent on parental wealth over time. Holding constant several individual and parental measures, the relationship between parental transfers for school and adult socioeconomic attainment is positive. This relationship holds when using three-stage least squares models to account for potential endogeneity of financial transfers for school. Overall, results support arguments that parental financial transfers for education facilitate the intergenerational transmission of socioeconomic standing.

This research was supported by the Center on Assets, Education, and Inclusion in the School of Social Welfare of the University of Kansas. I am grateful to the participants of the Russell Sage Foundation workshop, the volume editors, and anonymous reviewers for helpful comments.

Receiving financial help from parents after reaching adulthood contradicts American individualistic explanations for status attainment (Davis and Moore 1945; Sewell and Shah 1977). Yet, according to one estimate, 34 percent of young adults receive financial transfers from parents at some point during their transition to adulthood, and these transfers are more common among high-income families (Schoeni and Ross 2005, 402).

As wealth inequality increases (Piketty 2014; Keister 2000; Wolff 1995, 2006, this volume), the importance of parental financial transfers for individual outcomes may also rise. Coupled with rising college tuition costs, the unequal ability of parents to pay for their children’s postsecondary education could increase inequality in graduation rates, student loan debt, or educational quality (Armstrong and Hamilton 2013; Houle 2013; Carnevale and Strohl 2010; Hoxby and Avery 2013). Unequal access to education has broad and enduring implications for adult outcomes, including income and wealth (Card 1999; Boshara, Emmons, and Noeth 2015). Thus, one potential consequence of wealth inequality could be unequal financial support for education and, in turn, increasingly unequal outcomes in the next generation of adults.

How have parental financial transfers for school changed over time? Have they increased or become more dependent on wealth as wealth inequality has increased? Furthermore, what is the relationship between these transfers for school and adult socioeconomic outcomes, including education, income, and wealth? If federal or institutional support makes up for lower parental support among low-wealth students, there may be no relationship between parental transfers and socioeconomic outcomes. Wealthy families may provide more financial support for their children’s education because they qualify for less need-based aid or their children attend more expensive institutions. At the same time, however, students from wealthy backgrounds may qualify for more academic scholarships because they had higher quality early education; they also may be savvier about applying to multiple schools and choosing the one that offers the best financial award package—reducing the amount of financial support from parents. In other words, the relationships between parental wealth, parental financial transfers to young adults for education, and socioeconomic attainment in adulthood are unclear.

Existing research on parental financial transfers tends to rely on older data. I address these questions using recently released data from the 2013 Panel Study of Income Dynamics (PSID) Rosters and Transfers Module. The PSID data allow analysis of changes in parental financial transfers over time as well as examination of the relationship between these transfers and adult socioeconomic outcomes.

THEORETICAL AND EMPIRICAL BACKGROUND

To provide background for this study, I review research on parent-to-adult child transfers, the relationship of these transfers to inequality and education, the transition to adulthood, and the relationship between wealth and child outcomes.

Parent-to-Adult Child Transfers

A financial transfer from a living parent is called an inter vivos transfer, to distinguish it from financial transfers or bequests to adult children after the death of a parent. A long line of research theorizes and investigates relationships—including transfers—between parents and their adult children (Parsons 1943; Stack 1974; Becker 1981; Hogan, Eggebeen, and Clogg 1993; Sarkisian and Gerstel 2004; for reviews, see Lye 1996; Swartz 2009; Seltzer and Bianchi 2013). Much of the research on transfers attempts to understand the motivation for inter vivos transfers (Becker 1981; Hogan, Eggebeen, and Clogg 1993; Eggebeen and Hogan 1990; Kohli and Kunemund 2003; Yamada 2006), document the consequences of divorce (Furstenberg, Hoffman, and Shrestha 1995; White 1992; Eggebeen 1992), or explain variation by race, gender, or other demographic characteristics (Sarkisian and Gerstel 2004; Berry 2006; Eggebeen and Hogan 1990). In a related area of research, evidence from Europe documents the relationship between inter vivos transfers and welfare regimes or state support for the elderly (Attias-Donfut, Ogg, and Wolff 2005; Albertini, Kohli, and Vogel 2007), echoing evidence from the United States that parental financial transfers differ by parental income. For example, Robert Schoeni and Karen Ross find that compared with young adults (ages eighteen to thirty-four) from families in the bottom half of the income distribution, those in the top quartile received nearly three times as much financial support from parents (2005, 411).

Only recently has research begun to investigate the potential consequences of parent-to-adult child transfers. For example, Claire Scodellaro, Myriam Khlat, and Florence Jusot (2012) find that transfer receipt is associated with health in a French sample. Others find evidence that parental transfers are associated with unequal living standards and adult socioeconomic outcomes (Semyonov and Lewin-Epstein 2001; Swartz 2008, 2009). These unequal outcomes make sense in light of the evidence showing substantial differences in financial transfers from parents to young adult children by parental income (McGarry and Schoeni 1995). This and other evidence, however, is based on relatively old data. For example, Schoeni and Ross rely on data from the 1988 PSID for their transfer analyses (2005). As Judith Seltzer and Suzanne Bianchi note, “A surprising number of articles on intergenerational relationships still rely on the first two waves of the NSFH [National Survey of Families and Households] begun in 1987–1988” (2013, 285). Thus, descriptive information on intergenerational financial transfers in the United States would benefit from more recent information, such as that available in the 2013 PSID Rosters and Transfers Module.

A small literature examines financial transfers for specific purposes, including education. Moshe Semyonov and Noah Lewin-Epstein (2001), for example, examine the association between adult living standards and parental transfers for education or the purchase of a house. Relying on an Israeli sample, however, their findings may not be generalizable to the United States. Other evidence suggests families with more children provide less college financial support for each one (Henretta et al. 2012; Steelman and Powell 1989, 1991; Yilmazer 2008) or that parental financial support for college may depend on the sex composition of children (Powell and Steelman 1989). Research, however, tends not to investigate variation in intergenerational transfers over time.

Thus, although class inequality in transfers is well documented (Eggebeen and Hogan 1990; McGarry and Schoeni 1995; Schoeni and Ross 2005), in many cases this evidence relies on data from two decades ago, and little research investigates changes in transfers over time or the relationship between transfers for education and socioeconomic attainment.

Inequality, Education, and Parental Transfers

Unequal parental financial transfers for education have potentially long-lasting consequences. For example, research suggests intergenerational mobility varies by level of education. Comparing mobility among college graduates with that among others, evidence shows greater mobility among those with a degree (Torche 2011; Hout 1988). Not surprisingly, however, a college degree is not equally available to all (Carnevale and Strohl 2010; Haskins 2008). At the admission stage, student SAT scores are correlated with family income (Balf 2014), youth from families with lower socioeconomic status (SES) are less likely to apply to highly selective schools that provide more financial aid (Hoxby and Avery 2013), and higher SES families enjoy advantages in admission, grooming children from a young age to ensure acceptance to a selective postsecondary school (Stevens 2007).

After admission, the likelihood of graduating within six years remains unequal by socioeconomic background (Bowen, Chingos, and McPherson 2009). Enjoying financial support from parents, young adults from higher SES families can forgo work to focus on studies or social activities (Walpole 2003; Hamilton 2013). Alternatively, those from working-class backgrounds can borrow to pay for college but face daunting student loans, which can encourage dropout or limit choices after graduation (Armstrong and Hamilton 2013; Houle 2013).

By influencing the quantity and quality of education received, parental financial transfers for education may have meaningful implications for adult outcomes. Using survey data from Europe, Marco Albertini and Jonas Radl (2012) find evidence that financial transfers help reproduce inequality of occupational status across generations. Given higher costs of postsecondary education in the United States, parental transfers for education may play a similar role in reproducing inequality across generations in the United States.

Extended Adolescence

Parental transfers for education may be particularly important for adult socioeconomic outcomes in the contemporary context, which offers limited opportunity for early economic independence. Life-course theorists argue that the period between adolescence and adulthood has extended in recent decades and is now a distinct life stage, which some refer to as “emerging adulthood” or “extended adolescence” (Arnett 2000; Settersten, Furstenberg, and Rumbaut 2005). Evidence suggests this extension may be due to economic changes (Danziger and Rouse 2007). Regardless of the causes, however, young adults are undoubtedly struggling to establish themselves in the current social context (Silva 2013; Danziger and Rouse 2007; Newman 2013). Furthermore, this extended period of dependence on parental resources seems unlikely to shrink in the near future, given economic trends and the erosion of the social safety net (Kalleberg 2009; Hacker 2006).

As contemporary young adults struggle to complete their education, find a job that pays a living wage, pay off student loans, or afford health insurance (Danziger and Rouse 2007), those who received parental financial support for school may face fewer barriers to independence and greater opportunity to capitalize on their education. For example, parental transfers could prevent young adults from having to accrue student debt, which could allow them to take better advantage of their school experience, pursue further education, or accept a coveted but unpaid internship. At the same time, college tuition costs have risen and wealth inequality has increased in recent decades (College Board 2015; Piketty 2014; Keister 2000; Wolff 1995, 2006, this volume). Along with these economic changes, parental financial transfers for school may have increased over time, playing a greater role in the lives of contemporary emerging adults.

Wealth Inequality and Child Outcomes

Wealth has implications for a wide variety of outcomes, including health (Thompson and Conley, this volume; Pollack et al. 2007), intelligence (Mani et al. 2013), and educational attainment (Conley 2001; Pfeffer 2011, 2015). In fact, Fabian Pfeffer and Alexandra Killewald (2015) find that children’s educational attainment plays a major role in the intergenerational transmission of wealth. Wealth gaps in education may reflect differences in parenting behaviors, preschool attendance, school quality at the elementary and secondary level, parental financial support for postsecondary education, or “real and psychological safety nets” (Shapiro 2004, 11), among other things. Although evidence suggests the importance of parental wealth for postsecondary education (Conley 2001; Pfeffer 2015), it is unclear to what extent this reflects parental transfers for college as opposed to earlier investments in education or some other factor. Learning more about the mechanisms involved will help in understanding the potential consequences of growing wealth inequality and policies that could improve equality of opportunity. As the distribution of wealth and therefore of families’ ability to support their young adult children becomes increasingly unequal (Piketty 2014), parental transfers may become more unequal and their importance for individual outcomes may also rise.

Although some suggest that recent increases in wealth inequality are driven largely by gains among the top 0.1 percent of wealth holders (Saez and Zucman 2015), Fabian Pfeffer and Robert Schoeni point out (in this volume) that inequality has increased throughout the distribution and particularly for families with children. Thus, the growing wealth gap has implications for the ability of families throughout the wealth distribution to finance postsecondary education.

At the same time, parental transfers could contribute to wealth inequality. As of 1983, for example, evidence from Edward Wolff (1992) suggests that financial transfers from living parents accounted for half of the wealth of those born after 1933. More recently, Lingxin Hao (1996) finds evidence that financial transfers are positively associated with wealth among families with children. Thus, the relationship between parental financial transfers for education and wealth inequality may be reciprocal. I address potential endogeneity in this study but focus on assessing whether an association exists.

Several questions remain. How have parental financial transfers for school changed over time? Wealthier parents have more funds to transfer to their adult children, so their transfers will likely be higher. To what extent, however, is wealth related to transfers? Have transfers increased or become more dependent on parental wealth as wealth inequality increased? Furthermore, what is the relationship between these transfers for school and adult socioeconomic attainment, including education, income, and wealth?

HYPOTHESES

A growing body of evidence illustrates that early childhood investment is critical for successful development (Heckman and Masterov 2007; Heckman 2006). If early childhood is so critical, perhaps any meaningful benefits of parental support occur earlier in life and transfers in adulthood are redundant, with no bearing on adult outcomes. Hypothesis 1 is that parental transfers to young adult children for education are not associated with adult socioeconomic outcomes when holding parental SES measures constant.

Alternatively, parental transfers could promote a sense of entitlement, sap motivation, or promote laziness. For example, Laura Hamilton (2013) finds that parental support for college encourages students to adopt a strategy of “satisficing”—doing the minimum acceptable amount of school work and earning lower grades to meet graduation requirements. If parental financial transfers encourage satisficing behavior in school or other realms of life, young adults receiving transfers could find themselves outstudied and outearned on the job market by young adults who did not enjoy parental financial support. In other words, parental transfers could be negatively associated with adult SES outcomes. Hypothesis 2 is that parental transfers for education are negatively associated with adult socioeconomic outcomes.

The difficulties and experiences of contemporary young adults, however, suggest that parental support during young adulthood may have nontrivial consequences for adult outcomes (Silva 2013). Consistent with findings from Europe (Albertini and Radl 2012), parental transfers may help to reproduce inequality across generations. In the context of rising tuition costs and extended adolescence, parental transfers for education may be particularly important for young adult outcomes. Hypothesis 3 is that parental financial transfers for education are positively associated with adult socioeconomic outcomes.

DATA AND METHODS

The Rosters and Transfers Module of the Panel Study of Income Dynamics provides recent and long-term transfer information between parents and adult children from 9,107 families who participated in the 2013 survey. These data are linked to individual and household information from the regular PSID surveys using the child’s 1968 interview and person number. Individual and household information for mothers and fathers are also linked using the Family Identification Mapping System provided by the PSID.

The sample is limited to those with parental transfer information who were older than twenty-two in 2013, the year income and financial transfers were measured. The sample therefore includes cohorts born between 1943 and 1990, who turned eighteen between 1961 and 2008. The main analyses include those with maternal measures, including education, household income and wealth, marital status, age, race, and ethnicity. These measures are calculated separately for each parent in case of divorce or separation. Sensitivity analyses using paternal measures allow a smaller sample size (because 23 percent of the main sample is missing paternal measures) but yield similar results (see the online supplement, tables 1 through 10).

Descriptive Statistics

I limit the sample to those over age twenty-two to ensure that all individuals are beyond the traditional college completion age, the period during which the majority of parent-to-child transfers for school likely occur. One potential concern is that children from wealthier or higher SES families may have received transfers for school after that age—to complete graduate degrees, for example. To address this concern, I conduct two sets of sensitivity analyses limited to those who were older than thirty and older than thirty-four in 2013. These results are consistent with the main analyses and are presented in table A1. In a second step to address concern that those from wealthier families received transfers after college, I compare the amount of financial transfers for any purpose between parents and children in 2012 (the year before the 2013 Rosters and Transfers Module) by cohort and parental wealth. The comparisons suggest low-wealth parents (below the median) gave their young adult children (ages twenty-three through twenty-nine) more money and received less money from them in 2012 than high-wealth parents (see table A2). Among cohorts in their thirties, those with wealthier parents received slightly more money from their parents on average than those with poorer parents ($10 more among those age thirty to thirty-four and $28 more among those age thirty-five to thirty-nine) but gave their parents quite a bit more than those with poorer parents ($1,712 among those age thirty to thirty-four and $1,569 among those age thirty-five to thirty-nine). Thus, young adults from wealthier families do not appear to receive more from their parents than others, whether before or after age thirty. In fact, at least in 2012, adult children from both high- and low-wealth backgrounds gave their parents more than they received.

The modest average transfer amounts suggest the PSID transfer data may not capture large transfers among the very wealthy. Individuals in the data may fail to report all transfers or very wealthy individuals may fail to appear in the data. These are limitations of the data and results should be interpreted with these limitations in mind.

Measures

Parental transfers for school measure the total amount of money parents report giving their child for school since age eighteen in the 2013 Rosters and Transfers Module. Transfers are adjusted for inflation based on the year in which the child turned eighteen, but results are similar using unadjusted values (see table A3). In some cases, children appear more than once in the data (if their parents are divorced and both parents completed the survey, for example). In those cases, the total amount of transfers from both parents is calculated. The long-term transfer question in the 2013 module requires parents to recall how much financial support they gave their child for education since that child turned eighteen. Depending on the child’s age, this could be a long period. Given the potential for recall bias, this retrospective reporting is less than ideal. The 2013 data provide more recent information over a longer range of cohorts than available in most existing research on parental transfers, which similarly relies on retrospective reports. Nevertheless, parental transfers may be measured with error.

In an effort to address concern about potential measurement error, I conduct sensitivity analyses limited to those who were younger than thirty in 2013. The recall period is shorter for these cohorts and transfers should therefore be measured with less error. However, because these cohorts are young, they are unlikely to have reached full earning potential and may not be employed. Financial transfers for school have had little time to generate any implications for income or wealth among young cohorts. The results, presented in table A4, are consistent with the main analyses, but the coefficients for parental transfers predictably do not reach significance in models predicting wealth (and in one model predicting household income).

Education is measured in years for both individuals and their parents and represents the highest grade or year of school completed. Individual education is measured in 2013. Father’s and mother’s education are the highest education reported for each parent from any previous wave of the PSID (1968 to 2011). Maximum parental education provides the best measure of parental educational attainment, even if it occurred after the traditional age.

Individual income is total household income in 2012 (reported in the 2013 survey and converted to 2013 dollars using the Bureau of Labor Statistics Consumer Price Index Inflation Calculator) and includes income of all members in the family unit. Parental income is the total household income of the mother’s or father’s household (measured separately in case parents are divorced or separated) the year the individual was seventeen years old (converted to 2013 dollars). Income is measured when the child was seventeen because it provides the parental income measure closest to but before the year the child turned eighteen. This parental income measure partially assesses parents’ ability to support their child’s postsecondary education and would be the year of income reported on initial financial aid applications for those attending college at the traditional age. Because parental income and ability to support a child could vary by parental age, I also measure (and control for) parental age when the child was seventeen.

Individual wealth is the sum of all family assets in 2013, including home equity and net of debt. Parental wealth is the same statistic in the year with available wealth data closest to the year the child was seventeen (converted to 2013 dollars). The PSID collected wealth in 1984, 1989, 1994, 1999, and every two years after that through 2013. For the earliest cohorts, the measure of parental wealth is just over twenty years after the child was seventeen. Fewer individuals are in the earlier cohorts of the sample; however, for approximately 27 percent of the sample, parental wealth is measured more than two years from when the individual was seventeen. Because of the potential measurement error, I do not control for parental wealth in the main analyses. Supplemental analyses controlling for parental wealth are presented in the online supplement (tables 11 through 13) and yield similar results. Models using parental wealth to predict the amount of financial transfers for school yield similar results when limited to those who turned eighteen after 1981 (for whom parental wealth is measured within two years of when the individual was seventeen).

Because financial transfers for school, household income, and wealth are skewed, I use transformed measures in regressions. I take the natural log of transfers and total individual and parental household income plus one, to include those with zero values. Some households have negative values for wealth. To reduce skewness without excluding those with zero or negative wealth values, I take the inverse hyperbolic sine (IHS) of wealth. Research suggests that the IHS transformation is methodologically sound and superior to other transformations in its retention of negative wealth values (Burbidge, Magee, and Robb 1988; Mac-Kinnon and Magee 1990; Pence 2006). All currency is either measured in or converted to 2013 dollars to adjust for inflation using the Bureau of Labor Statistics consumer price index inflation calculator.

I also measure and control for the child’s number of siblings. Parental financial support for education is related to the number of siblings a child has, likely because parental assets are typically divided among all their children (Henretta et al. 2012; Steelman and Powell 1989, 1991; Yilmazer 2008). Beyond number of siblings, I use family birth information to measure whether the first two children born to the individual’s mother are the same sex and whether her first child is male. Dalton Conley and Rebecca Glauber note that parents in the United States prefer to have children of both sexes: “Families with two same-sex children (either two boys or two girls) are about seven percentage points more likely to have a third child than are families with two opposite sex children” (2008, 723). Conley and Glauber use the sex mix of the first two children in a family as an instrument for sibship size to estimate its effect on educational outcomes. Others use sibling sex composition as an instrument to investigate adult labor market (Angrist and Evans 1998) and educational outcomes (Goux and Maurin 2005; Currie and Yelowitz 2000). Furthermore, some evidence suggests parental financial support for college and child educational outcomes may depend on the sex composition of children (Powell and Steelman 1989, 1990). I use indicators for whether the first two children born to the individual’s mother are the same sex and whether the first child is male, along with indicators for each birth year, as exogenous variables in three-stage least squares (3SLS) analyses to help address potential endogeneity of parental financial transfers.

Parental ability to offer their children financial assistance also depends on marital status (Amato, Rezac, and Booth 1995) and race (Conley 1999; Shapiro 2004). I therefore control for parental marital status when the child was age seventeen and parental identification as African American, other nonwhite race, or Latino. Because many of the financial benefits of marriage accrue to cohabiters as well, marital status is an indicator for whether the mother or father was married or permanently cohabiting when the child was seventeen. Parental race and ethnicity are based on self-report. However, self-reported race depends on a variety of factors, including social context and question wording and—as in previous research (Kramer, Burke, and Charles 2015; Saperstein 2006)—is not consistent over time. Therefore, I average each self-reported race category (white, African American, other, and Latino) over all waves with nonmissing information and assign the parent to the category if the parent so identified at least half the time. For example, if a parent identified as Latino in at least half of the waves for which data are available, that individual is assigned a 1 for the Latino indicator. The process is the same for each racial category. Additional controls include individual birth year and gender.

Analysis

To address the first question about how parental financial transfers for school have changed over time, I aggregate transfer information by cohort and graph the pattern over time. I also examine differences in parental financial transfers for school by wealth and whether parental wealth has become more important for predicting transfers over time.

To address the second question about the relationship between transfers for school and adult SES outcomes, I use ordinary least squares (OLS) and 3SLS regression models. In OLS models, I regress individual outcomes (including education, income, and wealth) on the amount of parental financial transfers for education, an indicator for whether parents gave the individual no money for school, and control variables (including birth year, gender, number of siblings, parental education, parental income when child was seventeen, parental age when child was seventeen, parental marital status when child was seventeen, and parental race and ethnicity). The OLS model is as follows:

The coefficients of interest, β1 and β2, measure the relationship between the outcome and parental transfer amount and receipt, adjusted for individual and parental differences. All analyses are weighted using the 2013 PSID longitudinal weight, and standard errors are robust to potential heteroskedasticity.

In some cases, control measures limit the sample size or may raise concerns about multicollinearity, particularly between amount of parental transfers for education and the indicator for receipt of any transfers for education. I therefore show results from models limited to those who received at least some financial assistance from parents. As a sensitivity analysis, I also fit the models with controls limited to birth year, gender, and parental education, age, and income or further limited to only birth year and gender. Results are consistent in both cases, and the latter results are shown in table A5.

This study investigates whether an association exists between parental transfers for education and adult socioeconomic outcomes. It cannot establish a causal relationship because multiple unobserved factors, including parental characteristics or individual ability, could influence both parental transfers and child attainment as an adult. An association is of interest because it would suggest that parental transfers are one mechanism through which parents may pass advantage on to their children. However, in an attempt to address concern about a potential spurious relationship, I also conduct 3SLS analyses, using two measures of sibling sex composition and birth year indicators as exogenous variables to adjust for endogeneity of parental financial transfers for school and number of siblings. As in previous analyses using sibling sex composition as an instrument (Conley and Glauber 2008), to increase precision, I limit the 3SLS sample based on number of siblings. Because sibling sex composition affects whether families with two children have more children, I limit the sample to those with one to three siblings.

Briefly, 3SLS uses the exogenous variables in the model to predict instrumented values of the endogenous variables (Zellner and Theil 1962). Similar to an instrumental variable analysis, the instrumented values are the predicted values of the endogenous variables after regressing them on all of the exogenous variables in the model. 3SLS uses these instrumented values to estimate a consistent covariance matrix and uses them both to fit the final model. The 3SLS results provide a more precise estimate of the relationship, after adjusting for potential endogeneity of parental transfers and number of siblings.

RESULTS

Table 1 presents descriptive information for the sample used in the main analyses. Descriptive information for paternal measures is provided in the online supplement table 1. These tables provide raw information about income, wealth, and parental transfers, because it is more meaningful than the transformed versions used in all regressions. On average, table 1 shows that individuals received over $13,000 from parents for school since they turned eighteen (in 2013 dollars). However, 75 percent received no educational transfers from parents.

Based on table 1, the sample completed an average of just over fourteen years of education. This reflects that nearly 34 percent of the sample did not complete more than a high school diploma and may therefore have accrued no postsecondary educational expenses. Approximately 26.6 percent completed more than twelve but fewer than sixteen years of education, 22.6 percent completed sixteen years, and 17 percent completed more than sixteen. On average, the sample completed slightly more education but have lower household incomes than their parents (after adjusting for inflation).

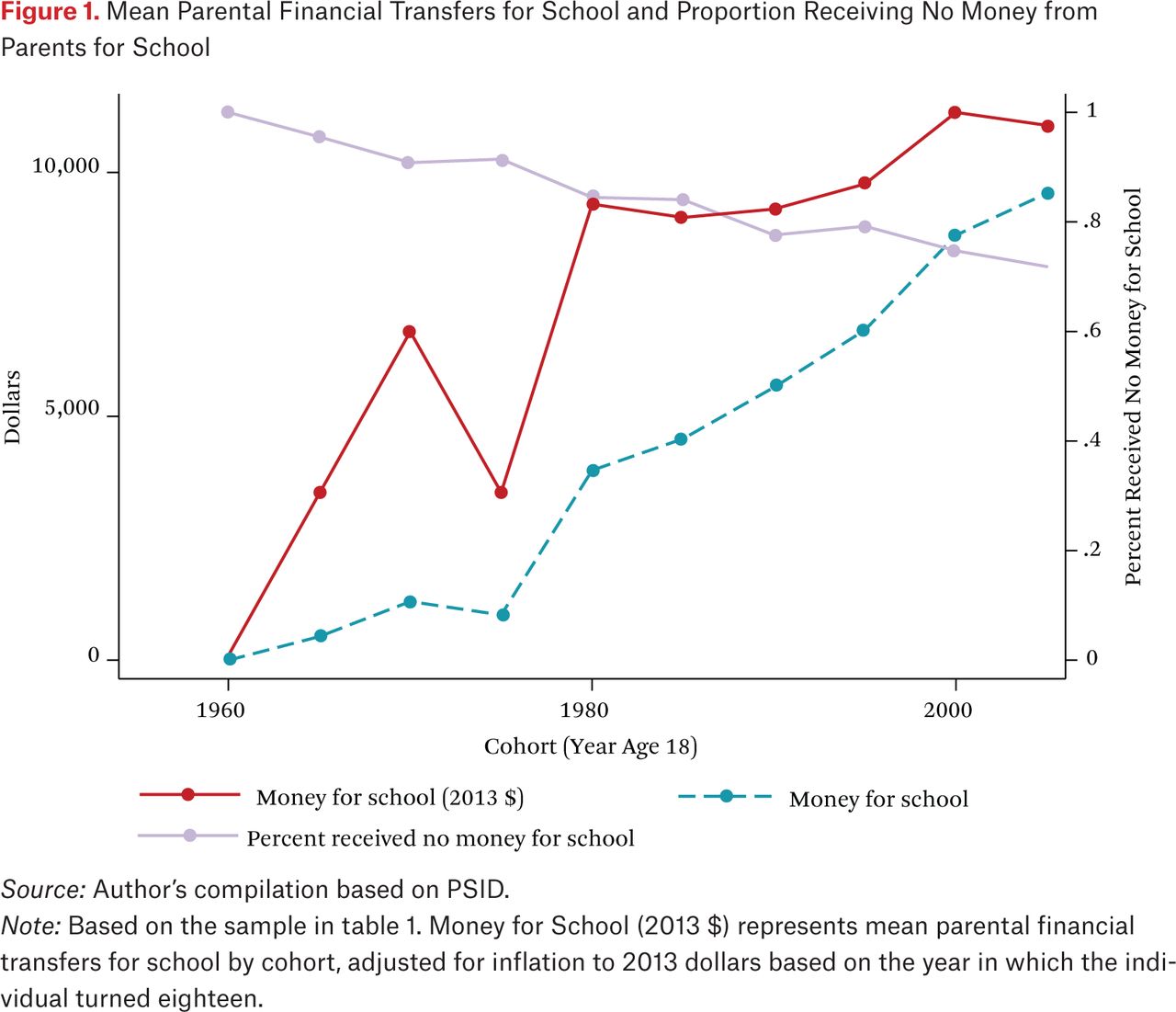

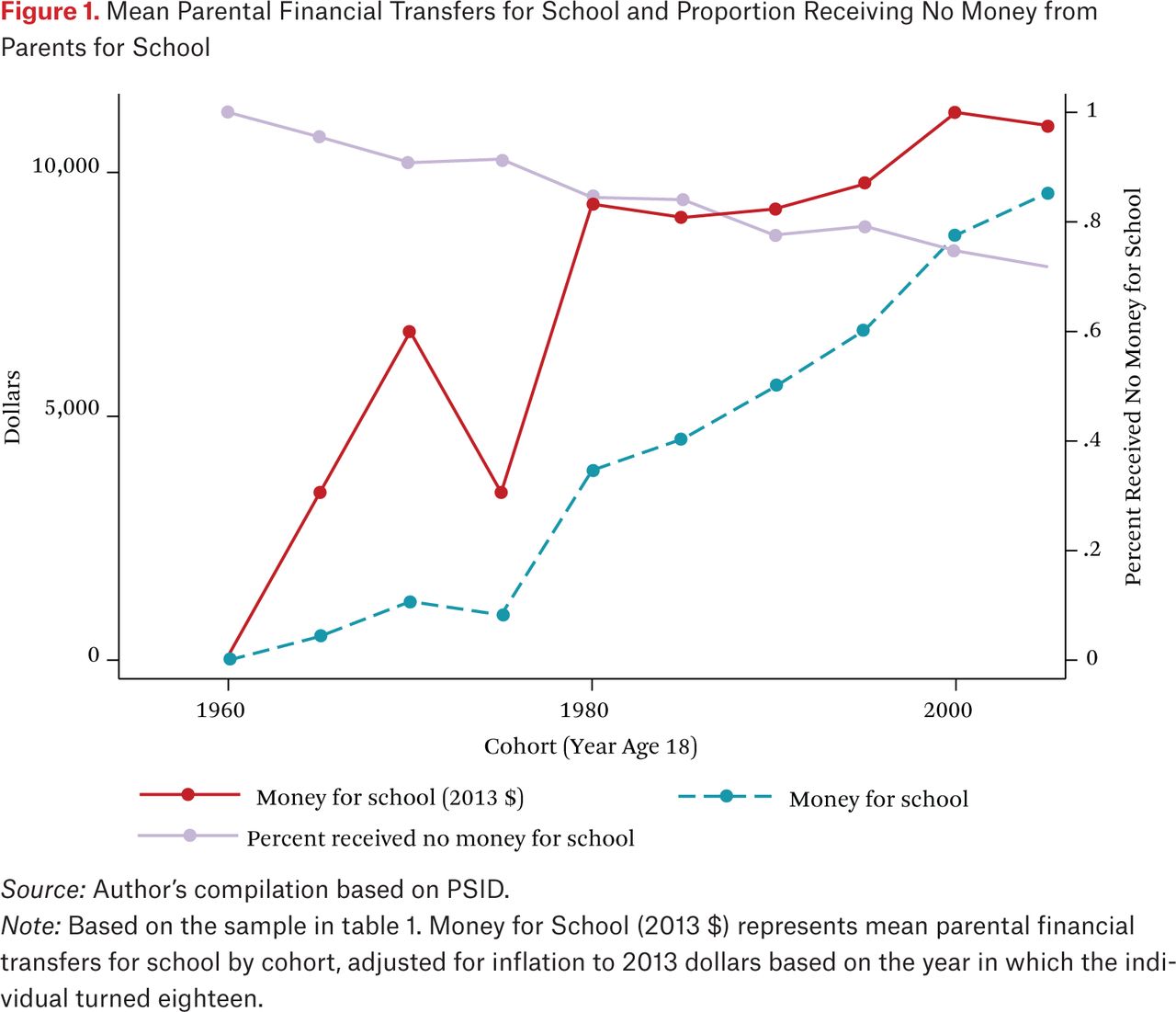

Figure 1 graphs mean financial transfers for school (in both raw and 2013 dollars) by the year cohorts turned eighteen (in five-year cohort categories). The figure also shows changes in the proportion receiving no transfers for education by cohort. The figure illustrates that average parental financial transfers for school have increased over time—whether adjusting for inflation or not. At the same time, the proportion receiving no transfers for education has declined, suggesting parental assistance for education is becoming more common.

Mean Parental Financial Transfers for School and Proportion Receiving No Money from Parents for School

Table 1 compares mean values of those who received financial assistance from parents for education with those who did not. Educational attainment, wealth, and household income are significantly higher among those who received financial transfers (p < 0.01). Nearly all other measures differ significantly as well. For example, children who received transfers have fewer siblings and are from later cohorts (p < 0.01). Parents who gave their children money for school were older, completed more education, had higher income, and were more likely to be married when the child was seventeen years old (p < 0.01). These parents were also more likely to be white and less likely to be black or Latino (p < 0.01).

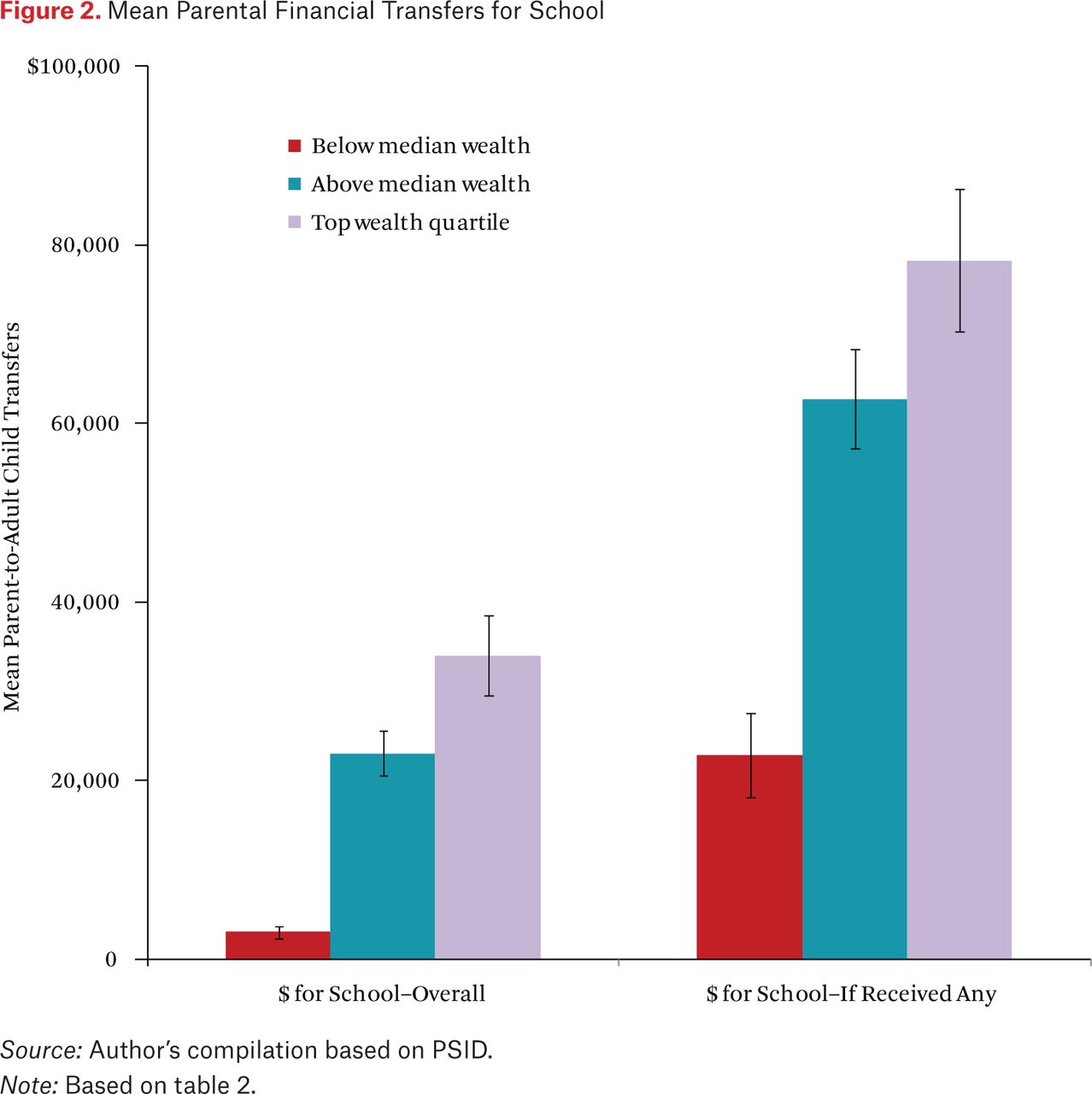

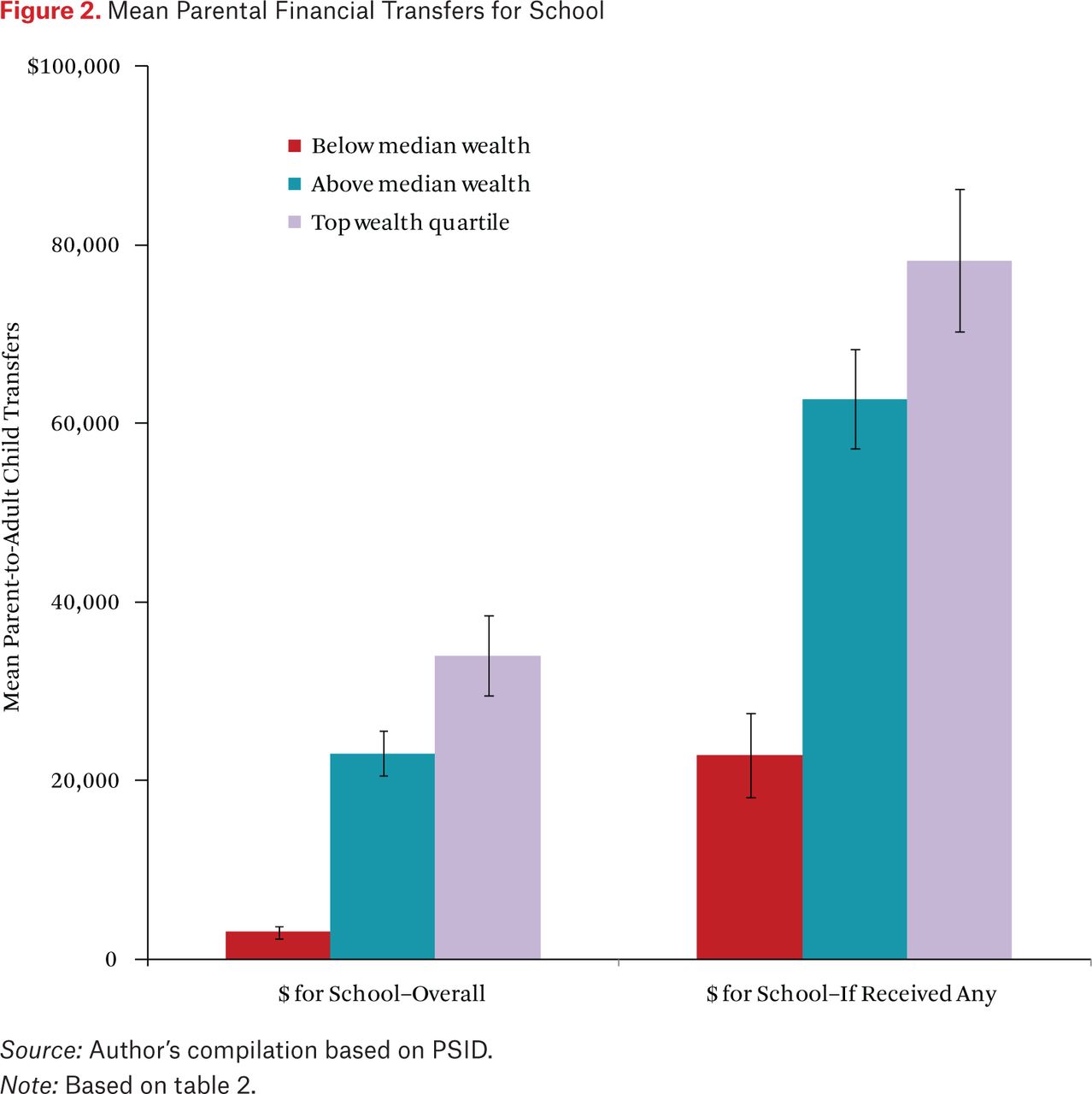

Table 2 shows differences in the amount and prevalence of transfers for school among those above and below median parental wealth as well as those in the top wealth quartile (see also figure 2). Young adults whose parental household wealth was above the median received more than seven times more money for school than those below. Excluding those who received no help for school, those above the median still received more than double those below. The gap is even wider when comparing transfers below the median with the top quartile. Those in the top quartile of parental wealth received more than eleven times more transfers for education than those below the median and more than three times more when limited to those who received some financial help for school. The proportion receiving transfers also differs by parental wealth. Only 13 percent of young adults below the median received parental transfers for school, compared with 37 percent above the median and 43 percent in the top quartile.

Transfers for School by Parental Wealth

Mean Parental Financial Transfers for School

Table 3 shows results of OLS regressions predicting the amount of parental transfers for school. Comparing the coefficient for household wealth over successive cohorts suggests that transfers became more dependent on parental wealth over time. All currency measures used in the regressions are adjusted to 2013 dollars, so changes over time are not due to inflation. Further supporting the increasing importance of wealth, the interaction term between household wealth and birth year in the final model is positive and significant (p < 0.01). Results using paternal measures are consistent (see online supplement table 3).

Predicted Parental Transfers for School

Parental differences between those who received or did not receive educational transfers seem to reflect financial differences in ability to assist children with their education. Racial differences in wealth are well established (Conley 1999; Shapiro 2004) and parents with higher wealth, income, and education are better able to support their children’s education (Lareau and Cox 2011; Conley 2001). Holding these factors constant, is there still a relationship between parental transfers and socioeconomic outcomes?

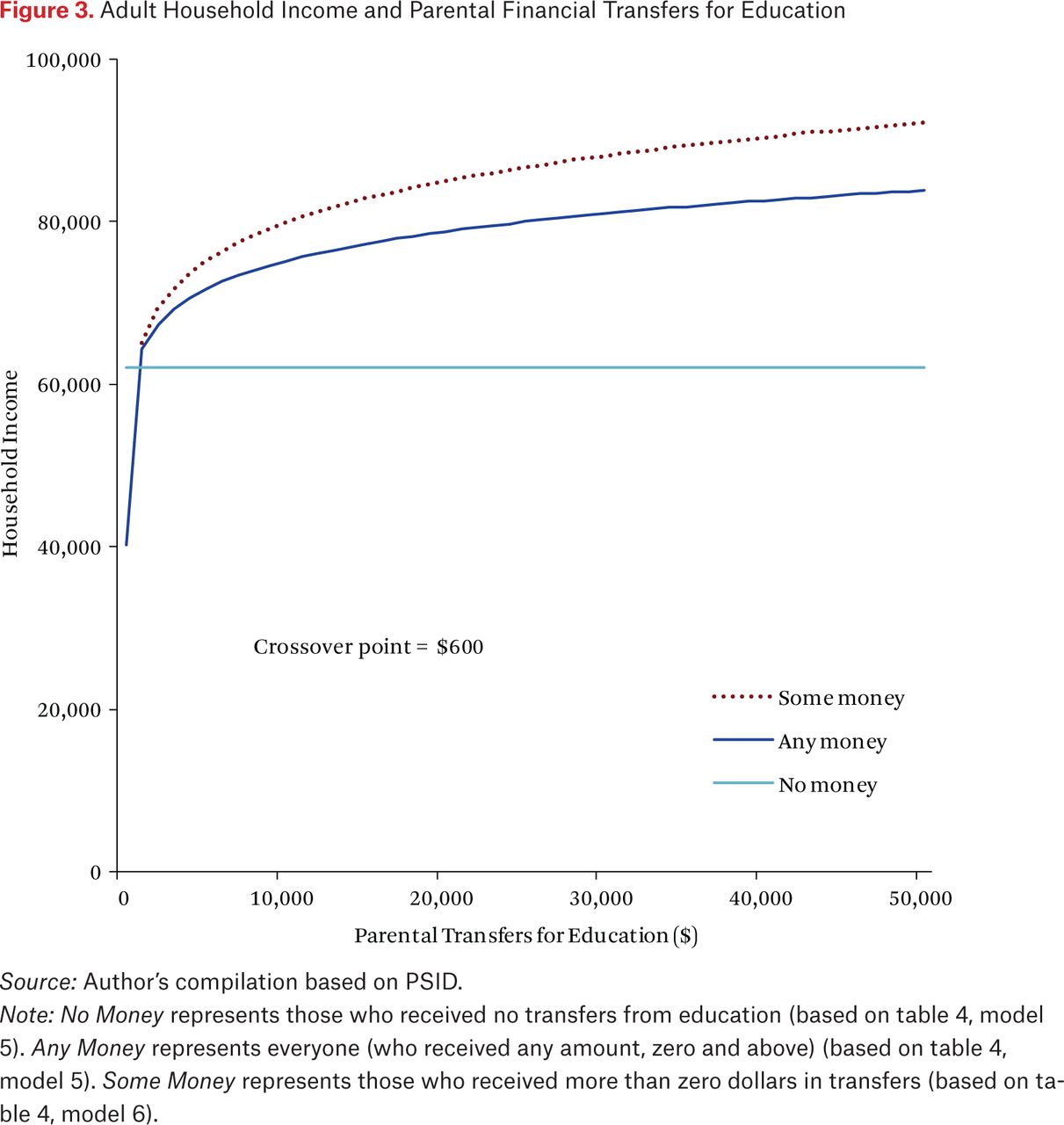

Regression results—shown in table 4—suggest that financial support from parents for school is positively associated with educational attainment, wealth, and household income, even when holding constant several parental measures, including income, age, and marital status when the child was seventeen, as well as parental educational attainment, race, and ethnicity. The indicator for whether parents gave an individual no money for school is positively associated with socioeconomic attainment measures. This suggests that individuals who received no financial transfers had higher socioeconomic attainment than those who received only a small amount of parental transfers. Receiving no financial assistance for education could reflect greater financial independence, other sources of financial support for education such as scholarships, or some other factor. However, the crossover point at which receipt of financial transfers is associated with higher socioeconomic outcomes is generally quite low. For example, figure 3 illustrates predicted household income based on models 5 (solid lines) and 6 (dotted lines) from table 4. The graph shows that predicted household income is higher than for those receiving no parental transfers when parental transfers exceed a relatively modest $600. The crossover point is also low ($250) when predicting education but is higher when predicting wealth ($2,200).

Parental School Transfers and Adult Outcomes

Adult Household Income and Parental Financial Transfers for Education

I include the indicator for receiving no parental transfers because three quarters of the sample fall into this category, and the model may not accurately reflect the relationship without it. However, this indicator is negatively correlated with the amount of transfers received and makes multicollinearity a concern in regressions. Therefore, I also run the regression models when limiting the sample to those who received some money from parents for education. These results are shown in the even-numbered models in table 4. Consistent with the results from the full sample, results show that the amount of parental financial transfers is significantly associated with educational attainment and household income as an adult. The association does not hold when predicting wealth. Thus, among those who received any parental financial support for education, the amount received is significantly associated with adult SES even when controlling for several parental and individual characteristics. However, this financial support is not associated with adult wealth, suggesting that the amount received may play little role in wealth accumulation.

In an effort to assess sensitivity to the controls included in the model, I rerun the models controlling only for birth year and gender. These results (shown in table A5) yield higher coefficients for amount and receipt of parental transfers. The larger coefficients suggest the controls included in table 4 partially account for factors related to both parental transfers and individual SES attainment. To further address potential endogeneity of parental transfers, table 5 presents 3SLS results. The results suggest that parental transfers increase educational attainment and household wealth (p < 0.05). The coefficient for parental transfers only reaches marginal significance (p < 0.10) when predicting household income.

Parental School Transfers and Adult Outcomes, Three-Stage Least Squares

Finally, table 6 compares the intergenerational association of education, wealth, and income with and without controlling for parental transfers. That is, it provides coefficients for parental education, wealth, and household income in models predicting the same outcome in the next generation. Controlling for parental transfers accounts for between 5 and 29 percent of the parent-child association. Parental transfers reduce the intergenerational wealth association the least (5 percent), educational association the most (29 percent), and income association moderately (20 percent). Overall, parental transfers for school explain a nontrivial amount of intergenerational socioeconomic association.

Intergenerational Socioeconomic Association Accounted for by Parental Transfers for School

CONCLUSION

Wealth inequality has increased in recent decades (Piketty 2014; Keister 2000; Wolff 2006), along with college tuition costs (College Board 2015). One potential consequence of wealth inequality could be unequal parental financial support for education and, given the enduring implications of education for adult outcomes (Card 1999; Boshara, Emmons, and Noeth 2015), increasingly unequal socioeconomic attainment in adulthood. Using recently released data from the 2013 PSID Rosters and Transfers Module, this study investigated two questions: how parental financial transfers for education have changed over time; and what the relationship is between these transfers and adult socioeconomic outcomes, including education, wealth, and income.

Results suggest that parental transfers for education have increased (even after adjusting for inflation), become more commonplace, and grown more dependent on parental wealth over time. Robert Schoeni and Karen Ross note that young adults from those in the top income quartile received nearly three times as much financial support from their parents as those in the bottom half of the income distribution (2005, 411). The difference by wealth is even more striking: young adults from families in the top wealth quartile received more than eleven times more money for school than those below the median. Excluding those who received no help, those in the top quartile still received more than triple the amount received by those below the median. These statistics echo Jonathan Fisher and his colleagues in this volume, who show that wealth inequality surpasses inequality of other financial measures.

Holding constant several individual and parental measures—including education, income, and wealth (see online supplement)—the relationship is positive between parental transfers for school and individual socioeconomic attainment, including education, household income, and wealth. The positive relationship holds when predicting education and wealth in 3SLS models, which account for endogeneity of transfers.

Overall, results are consistent with hypothesis 3 and suggest that parental financial transfers for education may be one mechanism through which inequality is transmitted across generations. These findings support evidence that parental wealth is an important predictor of children’s education (Conley 2001; Pfeffer 2015; Pfeffer and Killewald 2015) but add empirical evidence that parental transfers are one mechanism of that relationship. In addition, results raise further concern that rising inequality in parental wealth—and therefore in ability to finance postsecondary education—may exacerbate inequality of income and wealth as well as educational opportunity. Furthermore, if parents of lower means extend themselves to help their children pay for college, they may sacrifice saving for retirement and contribute to even greater inequality in retirement savings (Devlin-Foltz, Henriques, and Sabelhaus, this volume).

This study has important limitations. First, I can only identify an associational relationship. An association between transfers and attainment is of interest in its own right because it suggests one mechanism through which inequality may be transmitted between generations. However, controls for parental characteristics and 3SLS analyses offer steps toward reducing concern about a spurious relationship. Second, the long period of recall required by the PSID parental transfer question provides a less than ideal measurement of parental transfers. Although examination of younger cohorts (see table A4) yields consistent results for education and helps mitigate this concern, error in the parental transfer measure is likely to result in attenuation bias. Third, this study does not identify mechanisms. Because children from wealthy families are more likely to receive scholarships for college, parental expenditures on tuition may be lower. However, these same children tend to enroll in more expensive, higher quality schools. Therefore, one potential mechanism for the relationship between parental transfers for school and socioeconomic attainment may be school quality. Other potential mechanisms include student loans, student employment, and social connections developed in college. However, definitively identifying mechanisms is beyond the scope of this paper. Finally, this study examines only parental financial transfers to adult children for school, which excludes other transfers, including those of time, for other purposes, or from children to parents.

Despite these limitations, results suggest parental financial transfers for education are increasing (even after accounting for inflation) and may play a nontrivial role in the intergenerational transmission of inequality. In fact, controlling for parental transfers accounts for between 5 and 29 percent of the parent-child association of socioeconomic status, depending on the measure. Although early childhood inputs are critical, evidence suggests that financial transfers in young adulthood are not redundant but instead provide important benefits.

If we aim to improve equality of opportunity—and allow individual effort and ability to play a larger role in socioeconomic attainment—results raise at least two policy-related questions. First, to what extent would additional financial assistance for education improve the socioeconomic attainment of young adults from disadvantaged backgrounds? Some sources of financial assistance exist, including federal Pell Grants for students with financial need, the McNair Scholars Program intended to help first generation college students succeed, and the federal Work-Study Program. Other options include state or federal financial matching in college savings accounts, subsidized living expenses or paid student internships for those with unmet financial need, free community college tuition, or student debt relief.

Second, Caroline Hoxby and Christopher Avery note that most high-achieving, low-income youth do not apply for selective colleges, which provide better financial aid and therefore often cost less than less selective colleges (2013). To what extent could information campaigns and increased counseling efforts—that target disadvantaged youth and encourage applications to selective colleges—improve financial outcomes in adulthood? Informed policy decisions require empirical evidence comparing the costs and benefits of each of these programs, including their effects on equality of opportunity.

Appendices

Parental Transfers for School and Adult Outcomes, Older Cohorts

Intergenerational Financial Transfers in 2012

Parental Transfers for School and Adult Outcomes, Not Adjusted for Inflation

Parental Transfers for School and Adult Outcomes, Cohorts Younger than Thirty in 2013

Parental Transfers for School and Adult Outcomes, Minimum Controls

- Copyright © 2016 by Russell Sage Foundation. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Reproduction by the United States Government in whole or in part is permitted for any purpose. This research was supported by the Center on Assets, Education, and Inclusion in the School of Social Welfare of the University of Kansas. I am grateful to the participants of the Russell Sage Foundation workshop, the volume editors, and anonymous reviewers for helpful comments. Direct correspondence to: Emily Rauscher at emily.rauscher{at}ku.edu, 716 Fraser Hall, 1415 Jayhawk Blvd. Lawrence, KS 66045.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.