Abstract

Successful Black reparations require a policy for delivering payments, one that provides for effective identification, disbursement, asset protection, and asset growth over time. In this article, we suggest a structural solution (structured wealth accumulation of reparations payments) to a structural challenge (deeply embedded racial wealth inequality). Analyzing evidence from a longitudinal experiment, we find that Child Development Accounts (CDAs)—a carefully designed and tested asset-building policy for children—provide a model that can inform effective delivery and sustainable growth of reparations. CDA policy models a system of potentially lifelong, centralized asset building, with automatic enrollment, sensible investment options, structured asset protections, low fees, asset growth, and investment targets to achieve individual and family goals. Policy and research implications for Black reparations and reduction in racial wealth inequality are discussed.

- Black reparations

- policy delivery

- racial wealth inequality

- Child Development Accounts

- lifelong asset building

Wealth inequality is extreme in the United States, having increased over the last four decades (Saez and Zucman 2020), and the gap between races is especially pronounced, with Whites holding six or more times the net worth of Blacks (Aladangady, Chang, and Krimmel 2023; Bhutta et al. 2020). Racial wealth inequality is built into the country’s history and into current social and economic structures. It is purposeful and persistent. Despite passage of economic reforms and various civil rights bills, racial wealth inequality remains shockingly high (Fergus and Shanks 2022; Shapiro, Meschede, and Osoro 2013).

What might be a solution? A majority of Black adults in the United States (77 percent) think that descendants of people enslaved in the country should be compensated in some way, and 30 percent of all U.S. adults now agree with this position (Pew Research Center 2022). The percentages reflect a notable recent change in public awareness and opinions regarding reparations. Never since the unfulfilled pledge of forty acres and a mule (Oubre 1978) and the uneven allotment of land under the Homestead Act (Williams 2003; Williams Shanks 2005)—during and after the Civil War—have reparations been as much on the table for policy consideration (for a fuller account, see Darity et al. 2024, this issue).

Americans who support reparations were recently asked about particular forms and purposes of repayment. Among surveyed Blacks, 76 percent supported financial assistance in buying or remodeling a home, 77 percent supported financial assistance for starting or improving a business, and 80 percent supported educational scholarships (Pew Research Center 2022). These findings highlight two key suggestions from the Black community. First, reparations should be provided in the form of substantial fund disbursements that are owned and controlled by recipients. Second, a significant number of Black individuals expressed a preference for utilizing these payments to create assets that can contribute to long-term growth and development.

The highest priority of reparations should be autonomy. As noted in the introduction to this issue (Darity et al. 2024) and described elsewhere (Darity and Mullen 2020), a direct monetary component is important because of its symbolism and autonomy given that many Black Americans have been deprived of such self-determination during most of U.S. history. Similarly, the introduction emphasizes that recipients should be allowed to use any disbursement for purposes they choose without paternalistic micromanagement.

In addition, it may be beneficial to support a portfolio of disbursements to enable Blacks to protect and grow their assets, which they could use to develop their families and communities. Ideally, the uses of such funds would be consistent with best practices for expanding postsecondary access and success, supporting homeownership and home repair, and promoting business start-up and improvement while intentionally sustaining Black-run institutions that enable success in these areas (Williams Shanks, Boddie, and Rice 2010; Williams Shanks, Boddie, and Wynn 2015). This study explores different forms for the delivery of reparations and proposes that Child Development Account (CDA) policy—a carefully designed and tested asset-building policy for children—provides a structural model that can inform effective delivery and sustainable growth of reparations.

DELIVERY VISION AND OPTIONS

For reparations, it matters how payments and resulting assets will be delivered and controlled by Black families, and what the funds accomplish over time in reducing wealth disparities and generating social and economic development in Black families and communities. The vision aims for sustained advances in equity and long-term well-being.

In this understanding, reparations aim to atone for slavery and to mitigate slavery’s economic, social, and political harms, which did not end with slavery’s abolition. They have been carried forward and expressed in Jim Crow policies (DuBois 1970), racist policing, mass incarceration of Blacks (Alexander 2010), redlining, voting suppression in many forms, and other discriminatory practices. These conditions continue into the present, severely undercutting the ability of Black families to participate in and benefit from American institutions. In other words, slavery did not merely steal wealth. It also reduced opportunities, lifespans, and freedom of self-determination (see Wrigley-Field 2024). We suggest that reparations should be guided by the large vision that Black families can reach their full potential in access to all of America’s institutions. In short, this vision goes beyond a focus on the amount of a direct cash payment. It also attends to effective delivery, protection, and growth of assets over time.

Ultimately, decisions about reparations delivery will determine the policy’s objectives, effectiveness, and impacts. Detailed considerations for reparations design have been discussed by others (Darity and Mullen 2022; Logan 2023). What are the policy design options? To set a frame for discussion, we identify three major alternatives: reparations in the form of direct cash transfer without an account structure, reparations in the form of resources held in a trust fund, and reparations in the form of assets held in a savings plan structure. Each has advantages and disadvantages, which we briefly summarize in the next section.

Direct Cash Payment

Many discussions of reparations assume a cash payment or payments (for example, Darity and Mullen 2022; Darity, Mullen, and Hubbard 2023). A large, one-time cash transfer seems to be assumed in many reparations discussions. A possible alternative is a series of smaller payments over time (Darity, Mullen, and Slaughter 2022). The large advantages of cash payments are delivering assets directly into the hands of recipients and making them available for immediate use with no need to design asset holding and investment arrangements. The major disadvantage is risk of asset depletion and losses. In general and on average, humans are not very good at asset management (Frydman and Camerer 2016). This is the reason Andrew Carnegie created TIAA (a savings plan), so that college professors would not be living in poverty in old age. The cash approach to reparations delivery would provide no policy support for asset protection and growth. Thus it is more of a point-in-time distribution than a policy structure. Nevertheless, it is a viable option. If families prefer to take reparations as cash, this choice should always be available.

Assets in a Trust Fund

Some proposals for wealth distribution and holding take the form of a trust fund, which can take many, varied forms and involve diverse arrangements. In general, a trust fund refers to an instrument whereby wealth is held by an overseer (in a federal policy, this would likely be the federal government), to be paid out to individual beneficiaries at some future time. A trust fund may or may not keep track of individual wealth as “notional” individual accounts.

For a historical example of a racial wealth trust fund, we turn to Individual Indian Money accounts, which were originally set up by the Department of the Interior, Bureau of Indian Affairs, to manage funds “paid” to American Indians following passage of the Dawes Act of 1877 and to hold other funding flows in subsequent years. However, the accounts were grossly mismanaged by the federal government, with most records severely damaged or lost. Legal challenges arose near the end of the twentieth century, led by Elouise Cobell, a Blackfeet from Montana. The Bureau of Indian Affairs dragged their feet. In her older years, Cobell finally agreed to a settlement of $3.4 billion as compensation for lost assets valued at many times that amount. This partial remedy is now being used constructively by Native Americans, but most of the losses will never be recovered (for a chronology of this policy disaster, see Friends Committee on National Legislation 2016).

A parallel to this tragic loss of racial wealth is the failure of the Freedman’s Bank during the collapse of Reconstruction and severe depression of 1874. The bank failure was due in part to the largely White board of directors making questionable loans to friends and business partners (Fergus and Shanks 2022; Oubre 1978). These lost deposits were not in a trust fund but instead overseen in a similar spirit by the federal government. Black savers lost all their wealth, and many did not trust banks for generations thereafter. Overall, the U.S. government has an unfortunate history in managing funds on behalf of communities of color. Perhaps this could be different in the twenty-first century, but little policy experience suggests that.

Advantages of the trust fund idea are that it has the appearance of asset protection (via government oversight) and can result in a predictable payout. Also, investments can be purposefully conservative, with the aim of avoiding declining asset values. Disadvantages are that appearances of protection and stability may be misleading; highly conservative investments, such as U.S. Treasury bonds, may not promote long-term asset growth; the government does not have expertise in management of accounts earmarked for specific individuals for investment growth; and practical applications in overseeing a trust fund can be daunting and limit autonomy. For example, identification of trust beneficiaries and effective distribution of funds over long time periods may be easy to take for granted, but are in fact huge practical challenges. For these reasons, clear individual ownership, accounting, and control, along with potential for asset growth over time, may be a better policy design than a government-managed trust fund.

Assets in a Savings Plan Structure

A third policy option would be for reparations to create or adapt a savings plan structure guided by a public policy but using private-sector asset management with full property rights (control) by individuals. In such a structure, direct cash payments would flow into individual accounts. Good examples are the federal Thrift Savings Plan and state-level college savings (529) plans. Employment-based savings plans, such as 401(k)s and their variations are also examples. Ideally, a savings plan structure for reparations would have automatic enrollment (with an option to opt out at any time), sensible investment options, an experienced and trusted asset manager, low fees, asset growth, and investment targets to achieve individual and family goals. Such accounts would be overseen and regulated by a federal agency charged with administering Black reparations and representing the Black community.

For example, in the SEED OK experiment, one family in more than 1,300 in the treatment group has opted out during the past seventeen years, which may indicate both the importance of this financial autonomy and the potential of a savings plan structure to serve a broad population effectively over time.

Reparations policy delivery is likely to involve larger amounts of money and may have more individuals seeking their funds in cash. These withdrawals should always occur without penalty or loss of funds. At the same time, participants should be informed about the potential for asset protection and growth within the savings plan, and the risks of predatory agents who may emerge to encourage cash withdrawals. The latter is a serious concern, though already familiar in the financial lives of most marginal people, who are typically careful about finance because they need to be.

A key advantage of the savings plan structure is that the assets are owned and controlled by individuals. Also, as with the Thrift Savings Plan and 529 plans, assets in a structured reparations plan would be managed by well-established and trusted asset-management firms chosen through competitive contracting. In the United States, the capacity for such asset management is highly developed. Large asset-management firms, such as TIAA and Vanguard, offer investment skill, effective delivery, and low fees. They are widely trusted. It is also important to point out that the considerable assets to be managed in any reparations policy would give the reparations agency leverage to negotiate on behalf of participants for both asset-building protections and very low investment fees. Such leverage would otherwise be unavailable to individuals in the marketplace. In sum, a savings plan structure would provide policy support for sustainable asset growth and development while allowing individual access to the funds at any time.

The major disadvantage of such a structure is the potential for poor investment performance. For example, average stock market returns over the past century are about 10 percent per year (about 7 percent after adjusting for inflation), but the average individual investor earns about half this amount, primarily because of individual stock trading. More trading leads to lower returns (Barber and Odean 2000). Most active professional fund managers also underperform the overall market (yet charge fees for this service). In contrast, savings plan administrators have learned to promote account stability by using index funds (minimizing trading of individual stocks) and tools in behavioral finance (especially opt-out instead of opt-in) to reinforce investing practices that build assets over time.

Although no policy design can be perfect, the combination of federal oversight with strong Black representation, contracting with a large and trusted asset manager, and individual ownership of accounts with full property rights creates capacities that can lead to policy effectiveness.

In this study, we explore a savings plan structure for reparations delivery, with a focus on Child Development Accounts as a model for universal asset-building policy. It is important to note that CDAs are not a Black reparations policy and were not designed for reparations delivery. However, the research, development, and implementation of CDAs may offer insights for effective delivery of Black reparations.

The CDA Policy Model: Implications for Effective Delivery of Reparations

CDAs are investment accounts that provide financial access and subsidies to promote wealth accumulation starting with all children, including economically disadvantaged and minoritized children (Sherraden 1991). They target financial exclusion and wealth disparities. The original proposal for CDAs addressed the stripping of Black American assets and other historical harms and recommended substantial public deposits, which would be more than $30,000 per child in today’s dollars (Sherraden 1991). The CDA policy was conceived to accumulate assets for education, entrepreneurship, homeownership, and other development purposes, though most CDA policies in the United States today designate assets for postsecondary education (Sherraden and Clancy 2005; Sherraden, Clancy, and Beverly 2018).

Policy interest in CDAs is growing (GAO 2020). CDAs have been adopted in various forms in Canada, Israel, Korea, Singapore, United Kingdom, and other countries (Huang, Zou, and Sherraden 2020). In the United States, the policies and programs have been created in states, cities, communities, and school systems. Seven states—California, Illinois, Maine, Nebraska, Nevada, Pennsylvania, and Rhode Island—have adopted statewide, universal CDA policies by legislation or administrative rule. All of these policies are built on transformed 529 college savings plans (Clancy, Sherraden, and Beverly 2019a, 2019b). More than five million children in the United States already have assets in CDAs, and this number grows automatically each year with new birth cohorts (Huang et al. 2021; Prosperity Now 2023).

Statewide CDA policies in the United States are characterized by ten core features designed to ensure that the accounts are universal, progressive, potentially lifelong, and built on an efficient, scalable, and stable policy platform capable of promoting asset accumulation for development purposes (Clancy and Beverly 2017; Clancy et al. 2019a, 2019b; Sherraden, Clancy, and Beverly 2018). The features are summarized in table 1, and synergy among them is a foundation for asset building.

Ten Core Features of the CDA Policy Model

CDAs are able to accumulate funds from multiple sources. The funds can receive tax or direct benefits from government and can be excluded from eligibility screening for other public benefits. Although not listed in table 1, financial guidance and education services may be provided to improve families’ financial capability and functioning within CDAs. Table 2 illustrates adoption of the CDA model features across states with CDA policies. We suggest that a policy with these core features might also be adopted or created to deliver reparations payments.

Features of State CDA Policies

College savings plans were not originally designed to be rolled out to a very large population and in fact have been elitist and regressive, serving mostly families who are well off, with tax benefits (public subsidies) that are greater for the rich than the poor. But, as we document in this article, the 529 policy structure can be transformed to serve the whole population. If this kind of policy transformation can be achieved at scale, reaching all eligible people with reparations payments and asset building, the results could democratize wealth building institutions and change lives. Impacts could stretch across generations, as envisioned by early proponents of asset-based social policy (Sherraden 1991; Oliver and Shapiro 1995).

THE SEED FOR OKLAHOMA KIDS EXPERIMENT: EVIDENCE TO SUPPORT EFFECTIVE DELIVERY OF BLACK REPARATIONS

Evidence is fundamental for the development of successful policy delivery. SEED for Oklahoma Kids (SEED OK), a longitudinal, randomized CDA experiment launched in 2007, provides rigorous evidence to inform this discussion.

Design of the Experiment: Sampling, Setting, Intervention

Currently in its seventeenth year (2007–2024) following a representative cohort of Oklahoma children, the SEED OK experiment is a large-scale test of statewide CDAs, with a probability sample randomly drawn from infants born in 2007 (Clancy et al. 2019b, 2021). The study randomly selected 7,328 children; the primary caregivers (mainly mothers) of 2,704 of those children agreed to participate (a participation rate of 38 percent). They were then randomly assigned into the treatment (n = 1,358) or control group (n = 1,346). SEED OK oversampled populations of color (African Americans, American Indians, and Hispanics): African Americans were 17 percent of the sample, American Indians 19 percent, and Hispanics 17 percent. SEED OK mothers completed three waves of surveys: the first in fall 2007 through spring 2008, the second in 2011, and the third in 2020.

The design of SEED OK is built on the core policy features discussed. CDAs in the experiment use the centralized account structure of a state’s 529 college savings plan. In standard 529 plans, all families are eligible. In Oklahoma, as in other states, only about 6 percent participate, and most are already well off (Clancy et al. 2021; GAO 2012). Investment earnings in 529 plan accounts are not subject to federal or state taxes if withdrawn for qualified educational expenses at postsecondary institutions. In addition, many states offer income tax benefits for contributions to 529 plans.

The Oklahoma treasurer’s office automatically opened a state-owned account for each CDA treatment child through the Oklahoma 529 plan (OK 529), that is, treatment children are beneficiaries, and deposited $1,000 into each account. We preferred a larger initial CDA deposit, but this is what was possible with funding available for the experiment. Such a program deposit system could also be adapted to disburse reparations payments. Funds in these SEED OK accounts are invested in the age-based option, a mix of stock, bond, and capital-preservation funds. Withdrawals are sent directly to postsecondary educational institutions. Reparations payments could similarly use this fund distribution strategy to support the asset-building purposes of Black families. Assets in these CDAs are not counted against asset limits of means-tested programs, such as the Supplemental Nutrition Assistance Program (Beverly and Clancy 2017).

Evidence from SEED OK

SEED OK is an experimental test of the CDA policy model. It was intentionally implemented to demonstrate that a simple low-touch model could reach a full population. Many important lessons emerge from this research.

Universal Inclusion Built on a Centralized Account

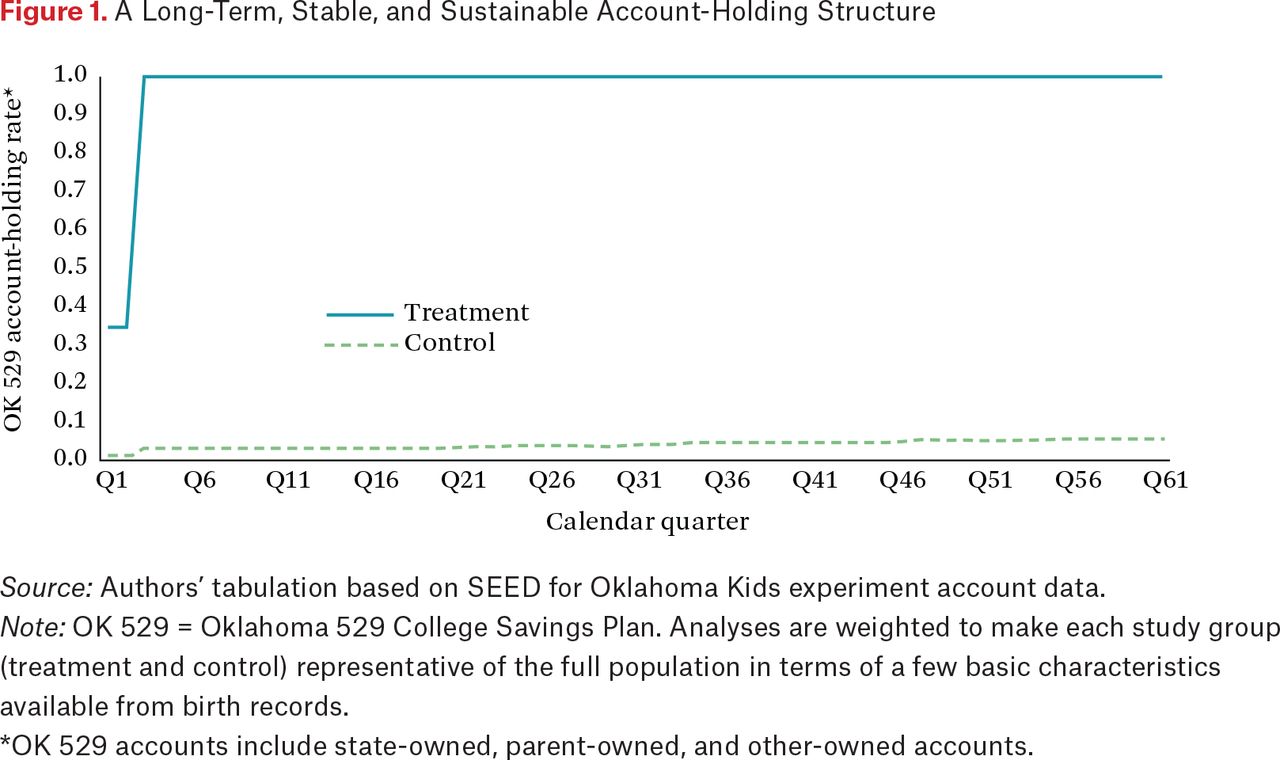

As the results in table 3 indicate, by the end of 2022, the CDA in SEED OK had a very large impact on OK 529 account holding, the outcome indicator for universal inclusion in a centralized account system. Altogether, 99.9 percent of treatment children and 4.7 percent of control children have an OK 529 account (p < .001). (The experiment did not prevent control children from having regular OK 529 accounts.) Thus, SEED OK successfully achieved near-universal 529 account holding among the targeted population sample by automatically opening accounts right after the birth of the children. If this can be done for a random sample, it can be done for all. A strategy similar to the CDA policy model could be used to create an account structure containing and managing reparations funds for all eligible Black individuals and families, with accounts fully owned and controlled by participants.

Financial Outcomes in OK 529 Accounts for SEED OK Children, December 31, 2022 (N = 2,704)

A Long-Term, Stable, Sustainable Policy Structure

The SEED OK intervention is a very low touch in that the technical aspects of fund delivery—account opening, deposits, and any future fund distributions—are fully automated. Annual financial data generated from the program over the previous fifteen years document that this account holding structure is both stable and sustainable (see figure 1). Limited administrative costs have been incurred in the program since the accounts were opened, making it also a promising option in terms of administrative and management costs for delivery of Black reparations and building wealth for Black families. Again, this may illustrate the advantage of transforming an existing policy structure to reach a universal population.

A Long-Term, Stable, and Sustainable Account-Holding Structure

Source: Authors’ tabulation based on SEED for Oklahoma Kids experiment account data.

Note: OK 529 = Oklahoma 529 College Savings Plan. Analyses are weighted to make each study group (treatment and control) representative of the full population in terms of a few basic characteristics available from birth records.

*OK 529 accounts include state-owned, parent-owned, and other-owned accounts.

Successful Fund Accumulation from Multiple Sources

The data in table 3 illustrate the effectiveness of the CDA policy model in delivering funds from multiple sources to the target population, with treatment children having a mean balance of $3,939 across all OK 529 accounts. The balance amounts to approximately 3.5 times that of control children ($1,132). This was made possible through the combination of funds from multiple sources, including automatic initial deposits of $1,000 for nearly all treatment participants, automatic progressive deposits of $600 for selected low-income participants, savings matches from the program, parent and family deposits, and investment earnings over time.

Among these fund sources, we pay special attention to the automatic initial deposits ($1,000 in SEED OK). Payments for Black reparations could be offered in a similar way via a federal policy or something like it. The delivery of automatic initial deposits in SEED OK shows that CDA policy can distribute funds universally (initial deposits to all treatment participants), as well as create subsidies for selectively targeted groups (matching the savings deposits of low-income participants). This successful fund delivery system could be replicated in a system for Black reparations, and also accommodate possible variations in eligibility by program feature.

Promotion of Wealth Building

Table 3 also presents data on the investment earnings for treatment and control participants over a fifteen-year span (2007–2022). The mean earnings in all OK 529 accounts was approximately 4.4 times higher for the treatment participants than for control participants, amounting to totals of $1,520 and $348 respectively. This documents that the CDA policy structure can promote wealth accumulation through investment options in the market. A closer look at the data reveals that $1,048 of the total investment earnings (69 percent) for treatment participants were generated from program deposits. The initial deposit amount more than doubled due to investment earnings. That matters a great deal for SEED OK youth with CDAs and would generate even more wealth with a larger initial deposit. This would likely matter even more in the case of reparations payments. Figure 2 provides a visual representation of the data, highlighting the potential for wealth growth if program deposits are utilized properly. Under a Black reparations policy structured to accord with the CDA model, payments could be distributed as initial deposits. The CDA experimental data document wealth accumulation over time. (It may be helpful to emphasize that this is not a simulation; the policy experiment has accomplished this.)

Wealth Growth of CDA Initial Deposit over Fifteen Years

Source: Authors’ tabulation based on SEED for Oklahoma Kids experiment account data.

Note: CDA = Child Development Account.

Black reparations proposals differ on the amount of cash payments and, therefore, on impacts on asset accumulation and capacity to reduce the racial wealth gap. If a reparation payment equivalent to $30,000 in today’s dollars—the amount specified in the original CDA proposal (Sherraden 1991)—had been deposited into the SEED OK account for an eligible Black family in 2007, the payment would have grown to more than $60,000 by the end of 2022. This amount would have reduced the 2021 median wealth gap between Black and White families by nearly 40 percent, and the mean wealth gap by about 7 percent.

Promotion of Social and Economic Development

Historical and structural racism have produced racial disparities in both wealth accumulation and human development (Oliver and Shapiro 1995). The pronounced racial wealth gap fuels educational and health inequities by constraining opportunities for development in Black families. In SEED OK, the designated asset building for children’s postsecondary education demonstrates the impacts of CDAs on social, behavioral, and mental health development. These positive experimental effects occur even before the CDA assets are used for postsecondary education. Analyses of data from the SEED OK wave 2 survey (conducted in 2011) indicate that the tested CDA policy sustained high expectations for children’s education (Kim et al. 2015), reduced the intensity of maternal depressive symptoms (Huang, Sherraden, and Purnell 2014), reduced punitive parenting practices (Huang, Nam, et al. 2019), and improved children’s early social-emotional development (Huang, Sherraden, Kim, et al. 2014). The sizes of CDA effects on these outcomes—approximately 0.10—were similar to effect sizes for Early Head Start, Head Start, and other early childhood interventions (Huang, Beverly, et al. 2019; Huang, Nam, et al. 2019; Huang, Sherraden, and Purnell 2014).

Moreover, some effect sizes were larger for the low-income subsample than for the full sample, indicating that those treatment effects were greater for families with disadvantaged backgrounds (Huang, Beverly, et al. 2019; Huang, Nam, et al. 2019; Huang, Sherraden, and Purnell 2014). This suggests that the policy model may lessen some child-development disparities caused by social, structural, and historical inequality.

A Foundation for Building Financial Capability

The SEED OK intervention does not offer direct financial guidance services to promote participants’ financial capability, although some CDA programs have done so. Nevertheless, SEED OK research demonstrates that a universal and centralized account system efficiently creates premises for individuals to develop financial knowledge and skills, accumulate assets, and manage financial resources. For example, financial knowledge and skills are positively related to asset-building outcomes only in the treatment group, such as additional private account opening and deposits (Huang et al. 2015; Huang, Nam, and Sherraden 2013). Moreover, the CDA intervention positively increased both asset- and debt-product use among treatment mothers age eighteen to twenty-four, suggesting improvements in overall financial functioning (Huang et al. 2022). In sum, CDA policy generates opportunities to practice financial knowledge and skills and has positive impacts on financial capability. This suggests that, by promoting financial capability, a similar policy model could support Black reparations families in household finances.

THE POTENTIAL OF A CDA DELIVERY MODEL TO PROMOTE RACIAL WEALTH EQUALITY

We have used the core CDA features and empirical evidence from SEED OK to demonstrate a potential policy structure for the effective delivery of Black reparations. If adapted for that purpose, the model has the potential to reduce the racial wealth gap and improve family outcomes.

Evidence of this is presented in table 4, which reports findings from SEED OK wave-3 data on the relationships among race (Black versus White) homeownership, retirement account ownership, 529 account ownership, and 529 asset balance, by CDA treatment status. Among the four wealth indictors, 529 account ownership and 529 asset balance are the targeted outcomes of SEED OK, and the results demonstrate no difference by race among treatment households (panel A). Other assets do not show the same effect. These data illustrate how the CDA intervention in SEED OK creates a supportive institutional setting and policy structures to improve the targeted financial outcomes among Black children and to eliminate the racial wealth gap on these indicators. We do not want to overstate the meaning; CDA policy cannot do everything; but on the targeted intervention, the result is no racial wealth gap.

Racial Wealth Gaps by Treatment Status, 2020–2022

For the control group (panel B), which might be thought of as business as usual, race was negatively and statistically significantly associated with three outcomes—homeownership, retirement account ownership, and 529 account ownership. The Black-White comparisons on the control-group wealth outcomes reflect historical and ongoing racial wealth disparities.

These results suggest that CDAs achieve the modest wealth effects intended, leading to the observation that the right policies and structures can reduce the racial gap on targeted wealth outcomes. To generalize the evidence, when Blacks are in the same institutional structures as Whites, wealth outcomes can also be the same. And his reasoning can be extended: wealth outcomes for Black children would likely be more positive if a universal CDA policy, or something like it, were paired with targeted reparations.

In sum, the CDA policy model addresses wealth inequality by race with modest yet identifiably positive impacts in 529 account holding and balances. Leveraging public and private funds to open accounts automatically for all children, the policy model has the potential to grow assets through large opening deposits, contributions at life milestones, savings matches, tax benefits, and exemptions for public-benefit eligibility. CDAs are not reparations, but they offer a policy model with inclusive, positive effects for people of color, a model on which a reparations policy might be effectively delivered with positive long-term impacts.

POLICY DELIVERY AS PURPOSEFUL STRUCTURAL CHANGE

Overall, evidence from SEED OK and CDA research suggests that the model lends itself to a policy for delivering Black reparations. We summarize some key observations.

Centralized accounts can accomplish automatic enrollment of all eligible reparations recipients into an integrated policy system.

With the development of reparations at different levels (such as schools, municipalities, states, and the federal government), the possibility of multiple, overlapping sets of eligibility rules further complicates the difficult process of identifying eligible populations. A single, centralized account system could make the process streamlined, accurate, and synergistic. A centralized policy would ensure efficient and effective delivery of reparations to all who qualify and also create a framework to facilitate policy coherence and growth. For example, a centralized policy might enable multiple municipalities to learn from success of a particular city.

Public oversight of a centralized account structure can ensure full inclusion, protections, low fees, effective delivery, and prudent asset management.

As states demonstrate by state-level negotiation and contracting with 529 asset managers, a centralized account structure affords leverage. States can use it to refine outreach, specify client protections, set low fees, and identify prudent investment options. Nothing like this would occur if individuals were left to negotiate for financial services in the market. States could use such leverage to specify a safe low-cost account option prenegotiated to offer the best financial terms. Note that this would not detract from an individual’s right to opt out of a reparations account and participate directly in the financial marketplace, and some people might choose to do so.

Centralized accounts can receive and manage multiple funding flows.

It is important, in our view, that such a publicly sponsored centralized account system have the capacity to receive funds from multiple reparations programs and multiple sources. Funds for reparations may come not just from public sponsorship, but also from the private-sector contributors, including corporations. Nonprofit organizations, from schools and churches to professional associations and national interest groups, may also contribute. And a reparations policy should become a target of American philanthropy, from community foundations to large national foundations. A centralized account system would make it relatively easy to track funds from all reparations programs and, through regular audits, to ensure that the money was used to support those who were eligible. A centralized account system with public sponsorship would also streamline implementation and increase accountability and efficiency.

Additional funding flows are desirable as long as they are consistent with the reparations goal of closing the racial wealth gap. In this regard, guidelines for direct giving and taxation would be needed. Those parameters would be designed to ensure progressivity and reduce economic inequality. For example, they should require that direct flows be progressive, with more going to the lowest income families, and perhaps impose an income-level cap. Any tax benefits for holding reparations assets would be available only up to a modest income level or with an overall cap.

Reparations funds should be distinct from individual-level funding.

Reparations assets would represent a societal commitment to greater equity, and this value is fundamental. Therefore, a reparations policy should account separately for individual-level contributions (whether from self, family, or friends). Reparations policy should maintain distinct accounting. Even if the reparations account is part of a larger asset-building structure, it should be partitioned as the reparations account to prevent those with greater resources or personal wealth to disproportionately benefit from a reparations infrastructure. In other words, everyone, rich or poor, has the right to save and invest as they choose, but the reparations policy framework serves a distinct social and economic purpose in seeking to reduce wealth inequality. And those eligible should be able to clearly identify funds that come to them as redress for racial injustice.

Delivery of a reparations policy could take the form of lifelong asset building, with investments for personal and family development.

A reparations delivery strategy does not have to be limited to a single large payment. It can instead be a process for building and using assets over time. A secure financial platform with desirable features could facilitate that process. Additionally, reparations policy could offer different programs and provisions at different stages of life. Multiple, sequenced reparations deposits would require a long-term, stable, and sustainable account system. A lifelong account would provide a sustainable system to support the purposes of Black reparations, and to maximize the wealth and social impacts for account holders. We emphasize that the current 529 policy structure does not have an age limit, and anyone can be a beneficiary across the life cycle from birth to postretirement life. In this way, the 529 structure might be a policy resource for reshaping lifelong asset accumulation and use, though major federal policy revisions would be required. For example, multiple uses of CDA assets are very desirable, and these policy changes will be important (current federal legislation already envisions major expansion of 529 purposes). Because effective asset management and recordkeeping are already in place within the 529 structure, this could be a more efficient and feasible pathway than creating a new policy from scratch.

Reparations can promote narrowing of the racial wealth gap.

The account system for delivery of Black reparations should include key design features, including investments that allow for market appreciation. Such features can, in turn, promote asset building over time and reduce the racial wealth gap.

As discussed, Black reparations proposals identify a wide range of asset-building goals and development purposes intended to enable each individual to reach their full potential. Homeownership, higher education, job training and employment, health care, retirement security, and entrepreneurship are among the specified purposes (Darity and Mullen 2022; Darity et al. 2023). The system might include mechanisms to connect reparations accounts with other publicly sponsored financial products for asset building and development (such as retirement savings accounts, college savings accounts, and health savings accounts). Additional programming and incentive policies could be implemented to encourage targeted withdrawals (such as withdrawals for college education, homeownership, and retirement). Significant resource investments in the Black community might in turn lead to institutions and systems that better support Black families and communities.

Asset accounts for reparations should create fair tax benefits.

Reparations payments would ideally not be subject to taxation. Holding the funds in a centralized account system would make tax treatment more straightforward. In addition, the inherently regressive nature of tax benefits should be offset by direct public benefits (a refundable or negative tax) for low-income account holders who have little or no tax liability.

Reparations in asset accounts should offer public-benefit exclusions.

Some discussions have proposed reducing sums paid for reparations by the value of benefits received from social welfare and assistance (Darity and Mullen 2022). The implications of this adjustment are not completely clear and require further investigation. Nonetheless, we suggest that reparations should not interfere with recipients’ rights to social-welfare entitlement programs.

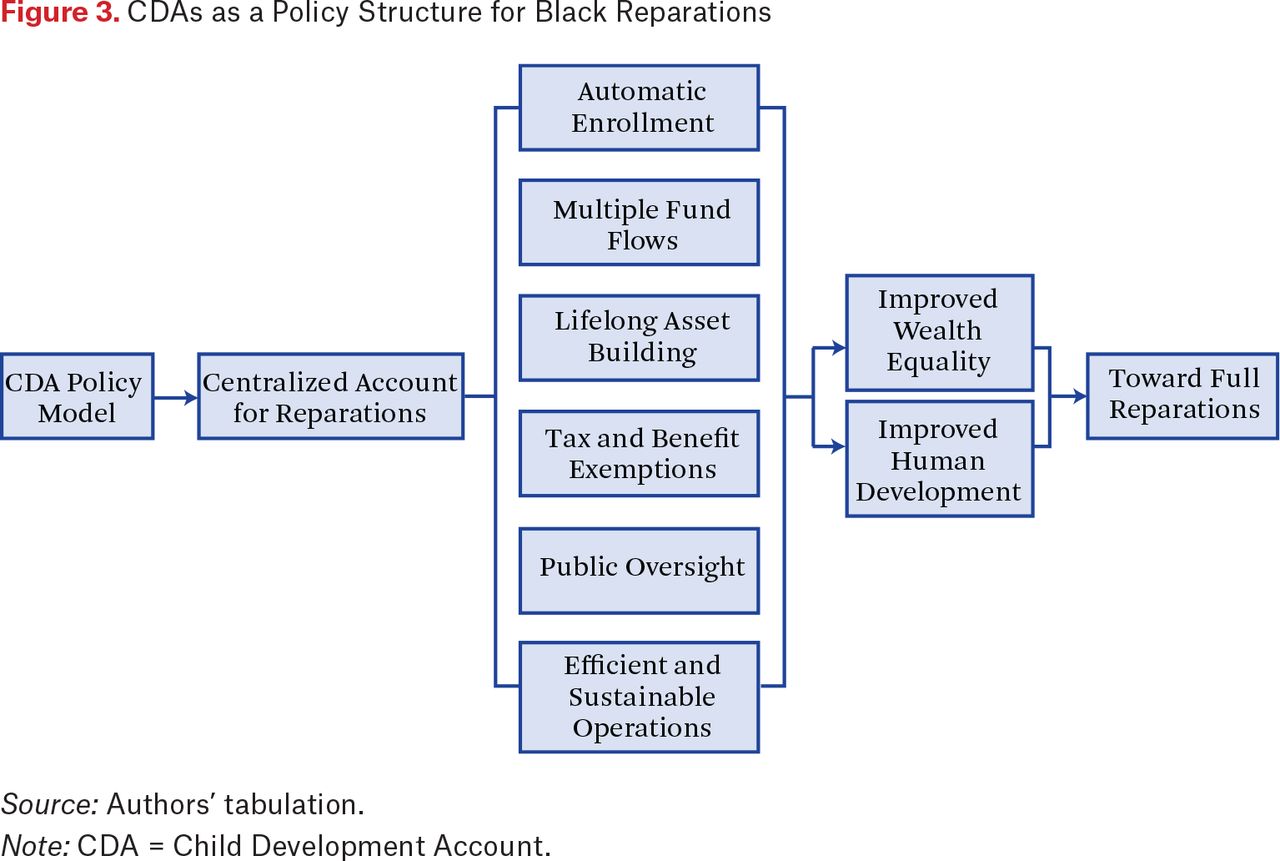

These observations are consistent with the core features of the CDA policy model summarized in table 1. As figure 3 illustrates, the model suggests that CDAs with these ten features can support purposeful structural changes toward racial wealth equality through Black reparations.

CDAs as a Policy Structure for Black Reparations

Source: Authors’ tabulation.

Note: CDA = Child Development Account.

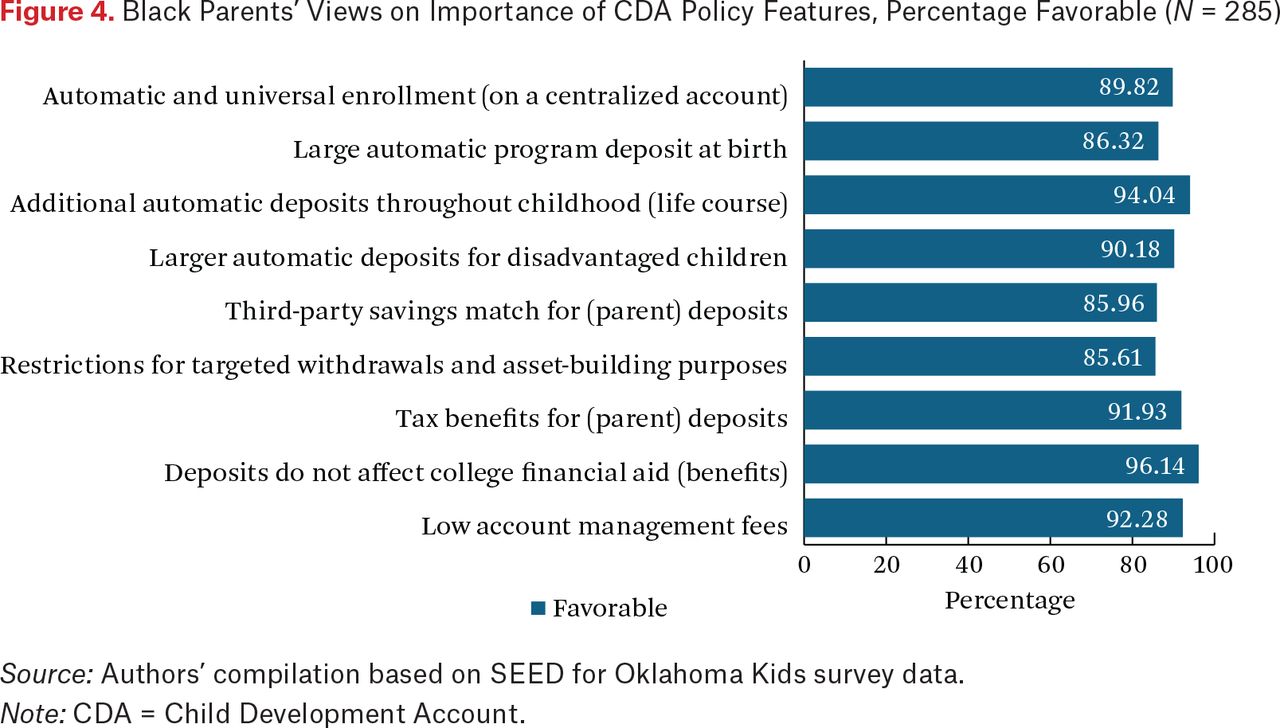

BLACK PARENTS’ VIEWS ON CDAS AS A POLICY MODEL

A system for reparations delivery should have the general approval of Black families and communities. In the SEED OK wave-3 survey, Black parents reported strong support for the features of the CDA policy. As a thought experiment on creating asset-building policies for children, the survey asked 285 Black parents in both the treatment and control groups to assess the importance of nine policy features. Although those surveyed in the control group (n = 149) did not receive CDAs, results from the two groups were similar. More than three-quarters of the Black parents surveyed in each group endorsed each of the features (figure 4).

Black Parents’ Views on Importance of CDA Policy Features, Percentage Favorable (N = 285)

Source: Authors’ compilation based on SEED for Oklahoma Kids survey data.

Note: CDA = Child Development Account.

One way to interpret these results is that the policy design work paid off; the policy features are popular regardless of the respondents’ experience with the SEED OK treatment. The results may also lend strength to the suggestion that this particular CDA policy model might find other productive applications, including perhaps as a platform for delivery of reparations.

LIMITATIONS

Some limitations should be noted. First, our evidence on the SEED OK CDAs does not lend itself to recommendations for reparations eligibility, the amount of reparations funds, or the identification of eligible families. A delivery structure similar to the CDA policy model, however, may be able to effectively distribute reparations payments to all eligible families.

Second, the ideal reparations delivery system should be based on a federal policy structure that covers all eligible families. The SEED OK CDAs and statewide CDA policies that followed are based on state policy platforms. However, federal legislation oversees state 529 policies, and it is therefore possible to think about a nationwide CDA policy in this format. Whether a reparations policy might build on this policy option, we do not take a position.

Third, when compared with ideal reparations payments, the $1,000 initial program deposit in the SEED OK experiment is very small. In this regard, the experimental data presented here does not speak to larger public funding. As noted, the original CDA model proposed a much larger program transfer (approximately $30,000), but it was not possible to implement this in the SEED OK policy experiment due to resource limitations. However, the data and outcomes do inform an automatic enrollment and deposit mechanisms, which could also be used for reparations payments.

Fourth, some design features in the SEED OK CDAs may not be suitable for a savings plan structure for Black reparations. For instance, CDAs are built on 529 plans, and assets in the plans can only be used for postsecondary education, and this is only one of the asset-building goals of Black families. Other long-term objectives are also desirable, including homeownership, entrepreneurship, and long-term social protection. In this regard, a new federal provision allows rollovers of 529 assets into Roth IRAs for retirement security. Additional policy adjustments would be needed to create a CDA-like policy structure for reparations delivery.

CONCLUSIONS

The idea of Black reparations is not new, but it has gained renewed momentum due to tragic racial events and ensuing discussions about racial equity. Constructive policy proposals, most notably reparations, are drawing more serious consideration. Several U.S. cities have undertaken Black reparations initiatives. In 2019, the City of Evanston, Illinois, became the first in the country to approve a plan to provide reparations to its Black residents, and the chair of its reparations committee called for a federal policy to address Black reparations (see Newton and Nelsen 2024, this issue; Davies, Jackson, and Knight 2024, this issue). Recently, a city-appointed reparations committee in San Francisco recommended a large cash payment to each eligible Black resident. The committee also suggested guaranteed annual income of $97,000 and homes for qualified recipients (Har 2023). Other cities—such as Asheville, North Carolina, Detroit, Michigan, St. Louis, Missouri, and Providence, Rhode Island—have passed resolutions to study the issue of reparations and explore potential solutions (Associated Press 2021; Afana 2023; Detroit City Council, n.d.; Salter 2022; Abdul-Hakim et al. 2023). At the federal level, provisions for a commission to study reparations have been reintroduced in Congress over a long period,1 and the proposal has gained support from a growing number of lawmakers. Research and publications on Black reparations have been expanding, with scholars and activists exploring implementation strategies. An effective solution might be a nationwide reparations policy that is framed, led, and mostly funded by the federal government but that also welcomes local engagement and participation.

Regardless of the reparations policy design, we have offered evidence from rigorous applied research, and also considerable policy experience, in how to deliver a reparations policy so that it might have positive and sustainable impacts. We suggest a platform that could be adapted for any version of reparations eligibility, funding level, or funding source. Policy flexibility matters because it takes advantage of institutional arrangements that are already in place. Any policy for nationwide reparations would almost certainly require legislative changes, but transformation of existing options may be less daunting than creating an entirely new policy structure. As policymakers are keenly aware, it is usually easier, less time consuming, and less costly to adapt an effective policy platform than to create a new one.

The CDA policy discussed here is built on a transformed 529 account platform. We emphasize the word transformed because 529 policies have been highly regressive, serving only a small proportion of the population, disproportionately well-off White people. Through the CDA policy, 529s can be adapted to serve the entire population, starting with all children at birth. Our evidence documents that all children (and over a long period, all people) can be included, and that people of color can benefit as least as much as Whites. In addition, the CDA policy model is efficient, trusted, and sustainable. It enjoys bipartisan support, which will be required to enact federal legislation. Thus, in both practical and political terms, a CDA policy model, or something like it, may be a promising candidate for effective delivery of reparations.

Views about this policy design direction will differ. Ongoing discussion and debate will be inevitable and necessary. Regardless of policy viewpoint, however, we hope that this article makes it clear that an effective and sustainable design for delivery of reparations will be necessary for implementation, stability, and effectiveness of a future reparations policy.

FOOTNOTES

↵1. Commission to Study and Develop Reparation Proposals for African Americans Act, H.R. 40, 118th Cong. (2023).

- © 2024 Russell Sage Foundation. Shanks, Trina R., Jin Huang, William Elliott III, Haotian Zheng, Margaret M. Clancy, and Michael Sherraden. 2024. “A Policy Platform to Deliver Black Reparations: Building on Evidence from Child Development Accounts.” RSF: The Russell Sage Foundation Journal of the Social Sciences 10(3): 92–111. https://doi.org/10.7758/RSF.2024.10.3.05. Current support for the SEED for Oklahoma Kids Experiment (SEED OK) and using evidence to inform policy comes from the Ford Foundation, the Charles Stewart Mott Foundation, and an anonymous donor. The authors are grateful for our partnerships with the State of Oklahoma through Todd Russ, state treasurer; Randy McDaniel, Ken Miller, and Scott Meacham, former state treasurers. This work would not have been possible without the steadfast partnership over more than fifteen years with Tim Allen, deputy treasurer for communications and program administration in Oklahoma. During the implementation of SEED OK, we were grateful to James Wilbanks, former director of revenue and fiscal policy. The Oklahoma College Savings Plan Program Manager, TIAA Tuition Financing, also has been a valuable partner. We appreciate the contributions of staff at RTI International. At CSD, we are grateful to SEED OK research team members Yunju Nam, Youngmi Kim, Nora Wikoff, and SEED OK research staff from years past, including Bob Zager, Krista Taake Czajkowski, Lisa Reyes Mason, and others. The authors thank Chris Leiker and John Gabbert for editorial assistance and graphic design. Direct correspondence to: Trina R. Shanks, at trwilli{at}umich.edu, Harold R. Johnson Collegiate Professor of Social Work, School of Social Work, University of Michigan, 1080 S. University, Ann Arbor, MI 48109, United States; Jin Huang, at jin.huang{at}slu.edu, School of Social Work, Saint Louis University, 3550 Lindell Blvd., St. Louis, MO 63103, United States; William Elliott III, at willelli{at}umich.edu, 1080 S. University, Ann Arbor, MI 48109, United States; Haotian Zheng, at haotian.z{at}wustl.edu, Washington University, MSC 1196–251–46, One Brookings Dr., St. Louis, MO 63130, United States; Margaret M. Clancy, at mclancy{at}wustl.edu, Washington University, MSC 1196–251–46, One Brookings Dr., St. Louis, MO 63130, United States; Michael Sherraden, at sherrad{at}wustl.edu, Washington University, MSC 1196–251–46, One Brookings Dr., St. Louis, MO 63130, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

- Article

- Abstract

- DELIVERY VISION AND OPTIONS

- THE SEED FOR OKLAHOMA KIDS EXPERIMENT: EVIDENCE TO SUPPORT EFFECTIVE DELIVERY OF BLACK REPARATIONS

- THE POTENTIAL OF A CDA DELIVERY MODEL TO PROMOTE RACIAL WEALTH EQUALITY

- POLICY DELIVERY AS PURPOSEFUL STRUCTURAL CHANGE

- BLACK PARENTS’ VIEWS ON CDAS AS A POLICY MODEL

- LIMITATIONS

- CONCLUSIONS

- FOOTNOTES

- REFERENCES

- Figures & Data

- Info & Metrics

- References

Related Articles

Cited By...

- No citing articles found.