Abstract

Wealth ownership is a critical component of economic well-being, and wealth in early adulthood provides important clues about the trajectories along which individuals move throughout their lives. Using data from the National Longitudinal Study of Adolescent Health (Add Health), we find an association between growing up rural and adult wealth that varies across the components of wealth. We also find that growing up rural has unique implications for young adult wealth ownership that differ from growing up in other geographic regions, particularly in urban areas. Our results highlight an important outcome that is conditioned by growing up rural and underscores the importance of context for understanding how families save and accumulate wealth.

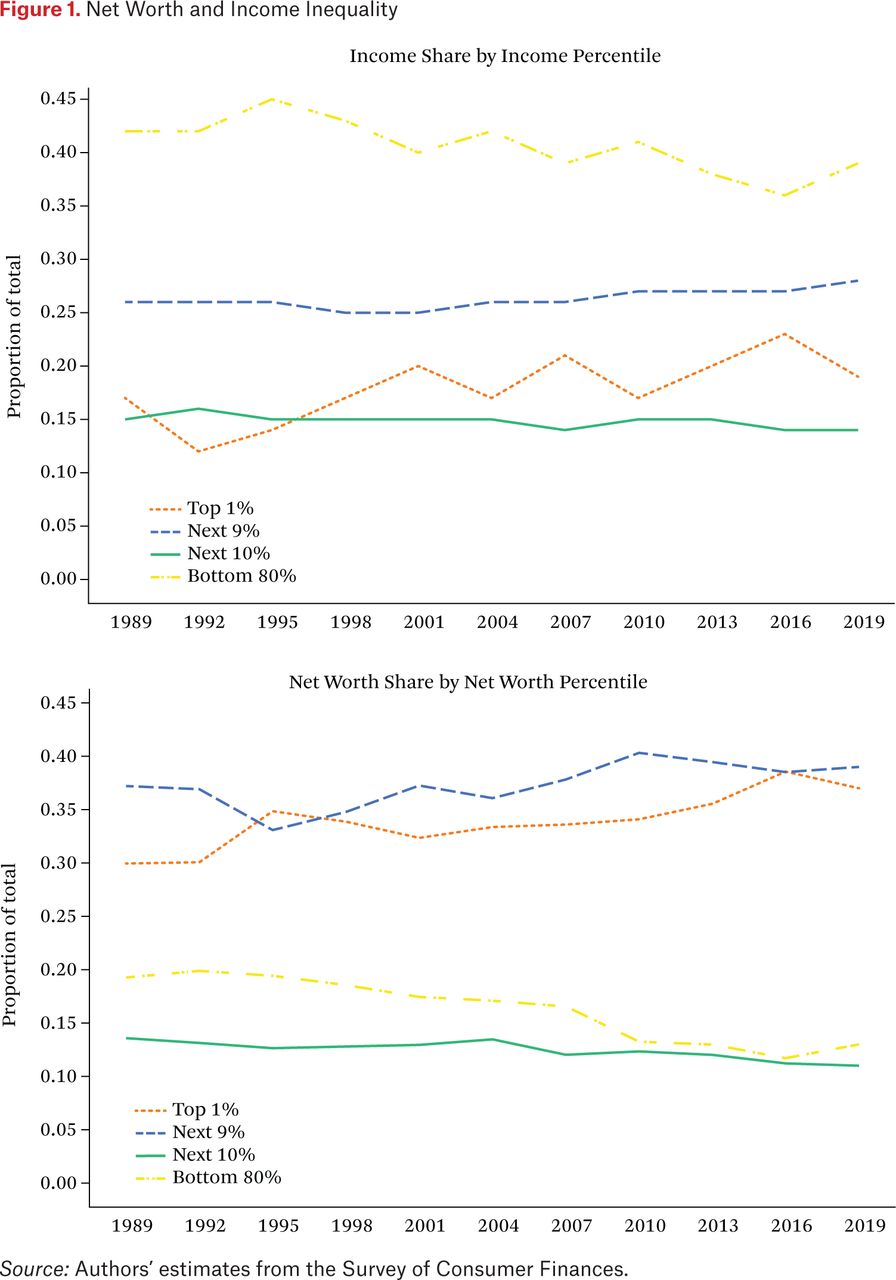

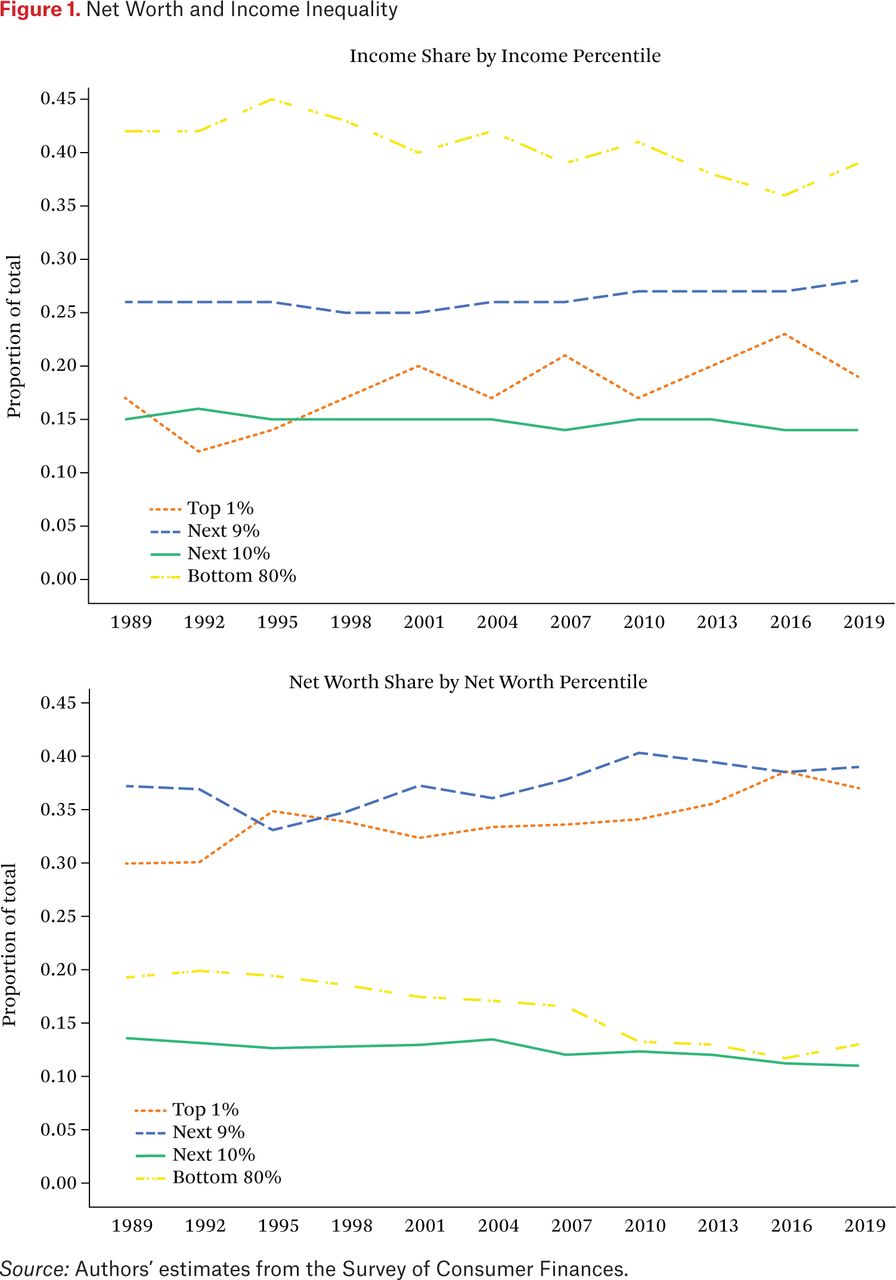

Wealth ownership is a crucial component of economic security (Keister and Lee 2014; Killewald, Pfeffer, and Schachner 2017; Skopek, Buchholz, and Blossfeld 2014), and wealth in early adulthood provides important evidence regarding the trajectories along which people move throughout their lives (Keister 2003, 2005). Wealth is the things people own and is usually measured as net worth (total household assets minus debts). Because wealth is cumulative, understanding the assets and debts of young adults can provide a glimpse into the lifelong wealth accumulation pathways that people follow. Wealth is sometimes relegated to conversations about high net worth households, but even a small amount of savings or home equity can provide significant advantages. Wealth can create a financial buffer in case of medical or other emergencies, the loss of an income, or unforeseen expenses. Assets can be invested to generate more wealth, and real assets (such as the home or other real estate) have both use value and investment value. Wealth is positively associated with children’s development (Gibson-Davis, Keister, and Gennetian 2019), improves health and emotional well-being across the life course (Boen 2016; Boen and Yang 2016), and can be used to fund a comfortable retirement. Perhaps more important, wealth can be passed to future generations to extend these benefits indefinitely. Income is often used to measure well-being, but wealth is more enduring and much more unequally distributed than income. Figure 1 shows that the top 1 percent of U.S. households received about 20 percent of total income in recent decades, but the top 1 percent owned at least 30 percent of net worth. By contrast, the bottom 80 percent of households received 35–45 percent of income but owned less than 20 percent of net worth. Given the importance of wealth to well-being, it is important to understand the factors that are associated with saving, asset ownership, and debt.

Net Worth and Income Inequality.

Source: Authors’ estimates from the Survey of Consumer Finances.

Growing up in a rural area is likely to be associated with early adult—and thus lifelong—wealth ownership; however, no research documents the association between being raised rural and later wealth. Three gaps in the literature require attention. First, there are the likely differences in young adult wealth among rural youth relative to their peers raised in other geographic areas. Differences are across geographic regions in poverty, educational and occupational opportunities, and the pace at which areas recover from economic setbacks. Given that income, education, and occupational attainment are all highly predictive of wealth, differences between rural and urban youth in their saving, asset accumulation, and debt follow. Second, the relationship between growing up rural and young adult wealth is likely to be associated differently with total net worth and its components (such as financial assets, homeownership, debt). Parsing these patterns and processes has the potential to clarify the reasons a rural background matters more broadly. Third, differences are likely in wealth outcomes by detailed geographic residence in adolescence. Rural, urban, and other geographic regions offer unique benefits and challenges that may shape young adult wealth. Rural-urban differences are potentially most pronounced, but research to date has not explored this possibility.

We address these gaps by studying the differences in young adult wealth ownership in the United States across the rural-urban continuum. We have three primary objectives. The first is to document the association between growing up rural and young adult wealth. We study wealth in young adulthood because this is a critical life stage for understanding the trajectory along which a person will accumulate assets as both saving and debt can be cumulative, and early patterns are likely predictive of lifelong saving and debt pathways. Importantly, the large and growing literature on the correlates of wealth neglects this critical life stage and says nothing about the role of geography as a correlate of wealth at any life stage. Second, we study how the association between growing up rural and young adult wealth varies across key measures of wealth including having negative net worth, the value of financial assets, homeownership, and home debt. Third, we explore how the association between geographic region of residence in adolescence and young adult wealth varies across the rural-urban continuum using a detailed conception of rural, urban, and other geographic areas. We use the National Longitudinal Study of Adolescent to Adult Health (Add Health) to study these processes. Add Health is ideal for our work because it includes longitudinal information on both adolescent traits (including place of residence) and young adult outcomes (including place of residence and wealth). Our attention to young adult outcomes is particularly important given the foundational nature of this life stage and the reality that today’s young adults face a different set of social and economic contexts than previous generations. Moreover, we study detailed geographic conditions by using rural-urban commuting area (RUCA) codes, which allow us to explore differences across the rural-urban continuum in significant detail. Our findings contribute to understanding the long-term consequences of growing up rural, and they highlight the importance of geographic context in conditioning economic well-being across the life course.

YOUNG ADULT WEALTH

Four aspects of wealth are particularly important to understanding financial stability in young adulthood and the trajectory along which people are likely to accumulate assets and debts over their adult lives: total wealth (net worth), financial assets, homeownership, and mortgage debt. We focus on each of these measures, knowing, of course, that young adulthood is just the start of adult wealth ownership and acknowledging that wealth patterns will change as people age. However, total wealth and these components provide an important glimpse into the starting point for accumulation that will provide the foundation on which future wealth is built. First, it is important to consider net worth, a broad indicator of wealth status. In particular, having negative, zero, or positive net worth is a particularly salient indicator of wealth status in young adulthood when people have just begun to accumulate wealth and the distribution of assets across households has not yet become as skewed as it tends to be later in life. Positive net worth suggests that a household has begun to save and accumulate assets that can provide a foundation for lifelong financial security. By contrast, negative net worth results from having more debts than assets and might indicate a precarious start to adult financial status, particularly if a household has considerable consumer debt (rather than educational or home debt). Although net worth is an important measure of financial well-being, it follows that looking more closely at its components is necessary to better understand a household’s status. For this reason, we also study a second wealth measure: financial assets. Financial assets (such as savings accounts, checking accounts, stocks, and bonds) can be used to pay for necessary expenses in an emergency and can be invested to provide financial security over the life course. Liquid financial assets—those that are readily turned to cash—are particularly important. The ownership of financial assets is highly unequal in the United States (Keister 2014), and those who manage to save some financial assets at an early age are uniquely positioned to create financial stability over the course of their adult lives.

Third, homeownership is a form of wealth critical to the financial well-being of Americans. The home is one of the most significant assets that many Americans will own, particularly for those in the middle class; and home values have historically appreciated across most of U.S. history (Spilerman and Wolff 2012). Owning a home as a young adult can allow a household to accumulate significant positive net worth over time that can ultimately be used to fund other investments (for example, when home equity is used to buy a more valuable home or other real estate) or spending (such as through home equity lines of credit or by selling the house to pay for retirement expenses). Although home equity is less liquid than most financial assets, home equity lines of credit and other forms of borrowing against the home can make homeownership an important safety net as well. Importantly, there is a financial value to homeownership via consumption (that is, the owner can take loans against the equity if needed). However, owning some form of real estate has important advantages regardless of the value; that is, the very act of owning a home provides a foundation for saving, can reduce stress, can allow parents to obtain quality education for their children, and can be an indicator of success (Coley et al. 2013). Finally, debt is an important indicator of financial stability. It is important to remember that not all debt is problematic. Mortgage debt, for example, is a financial liability but it is associated with the benefits that come from investing in real estate. The 2007–2009 economic crisis and ensuing economic downturn highlighted that mortgage debt and homeownership are not always beneficial, that not all households are ideal homeowners, and that home values will not always increase (Fligstein and Goldstein 2011; Pfeffer, Danziger, and Schoeni 2013). However, most households cannot afford to purchase a home without a mortgage, and given that the benefits of homeownership can be substantial, mortgage debt is typically considered an advantageous form of debt for most households.

GEOGRAPHY AND WEALTH

The unique demographic, economic, and social conditions that characterize rural communities are likely to interact in nuanced ways to shape young adult wealth. In recent decades, jobs have moved from rural areas to metropolitan centers where financial, technical, and other employers are located (Probst et al. 2011). Rural areas were also considerably slower to recover from the Great Recession than metropolitan and other regions, leading to widening economic gaps (Fry 2013). These recent changes have exacerbated well-documented challenges of growing up rural and are likely to lead to distinctive patterns of saving, investing, and debt acquisition for young adults who were raised in rural areas.

Three correlates of wealth suggest that growing up in a rural community is likely to be associated with young adult wealth in important ways. The factors that relate growing up rural with young adult assets and debts are well-established correlates of wealth ownership, and the underlying processes that lead to young adult wealth are the same regardless of place of residence in adolescence. However, because the conditions under which rural youth are raised might involve impediments to attaining important adult outcomes such as education, it follows that rural youth might also accumulate different levels and types of wealth than their urban counterparts. In the following sections, we address the three most salient correlates of wealth accumulation (educational attainment, social connections, and income) and explore how these might result in differences in young adult wealth across the rural-urban continuum. Of course, many other factors contribute to wealth ownership both in young adulthood and beyond; identifying the salient adolescent factors that are associated with young adult wealth is not an implication that these are the only factors at play.

Education

The first factor that potentially leads to differences in young adult wealth across the urban-rural continuum is educational attainment. In particular, it is well documented that educational opportunities are limited in rural communities even relative to other small communities (Biddle and Mette 2017; Economic Research Service 2019b; Hamilton et al. 2008). High rates of poverty and low population density mean that funding for rural schools lags behind school funding in other regions (Biddle and Mette 2017; Carlson and Goss 2016). The result is dilapidated buildings, less experienced and qualified teachers, and limits to other resources such as after-school programs, athletics, music education, and other extracurricular activities (Biddle and Mette 2017; Carlson and Goss 2016; Lichter, Roscigno, and Condron 2003). Because of resource constraints in school and at home, rural students’ access to the internet tends to be low, and as a result, rural youth have lower rates of adoption of new technologies that might contribute to educational achievement (Biddle and Mette 2017; Carlson and Goss 2016). Moreover, as rural populations declined in recent decades, rural schools consolidated, requiring students to spend more time on buses, reducing time available for educational and extracurricular activities, socializing with friends and family, and doing homework (MacTavis and Salamon 2003).

Resource and other constraints in rural areas have clear implications for both short- and long-term educational outcomes for youth. In particular, growing up in a rural area is associated with lower educational and occupational aspirations (Biddle and Mette 2017; Cobb, McIntire, and Pratt 1989; McLaughlin, Shoff, and Demi 2014), increased dropout rates, reduced preparation for postsecondary education, and ultimately lower lifelong educational achievement (Lichter, Roscigno, and Condron 2003). Youth who stay in rural areas are less likely to complete college degrees or professional training (Economic Research Service 2019b; Hamilton et al. 2008). Those who migrate to other areas in search of educational and occupational opportunities (often the most talented youth) contribute to the acute outmigration problem that faces many rural communities and that further lowers education levels in rural areas (Carr and Kefalas 2009; Gibbs and Cromartie 1994; Johnson 2012; Sherman and Sage 2011). Rates of return to rural communities are notably low despite the draw of ties to family and friends (Hamilton et al. 2008) because employment opportunities are limited (von Reichert, Cromartie and Arthun 2011).

Because education is one of the strongest correlates of adult wealth, differences in educational opportunities between rural and other areas may lead to differences in young adult wealth. Education provides the skills needed to invest, buy real estate, and sensibly assume and pay off debt (Keister 2000, 2005; Killewald, Pfeffer, and Schachner 2017). Educational attainment also affects wealth accumulation indirectly because it reduces family size, increases female labor force participation, and increases both personal and total household income (Keister 2000, 2005), and these outcomes also affect wealth. In young adulthood, educational attainment is likely to reduce the likelihood that a household has negative net worth, and it is likely to increase overall savings and the accumulation of financial assets. Educational attainment is also likely to increase the propensity to own a home and, correspondingly, the amount of mortgage debt that a household has acquired. In the case of those with higher levels of education, mortgage debt is likely to be a long-term benefit to overall wealth accumulation because education improves job and income stability, which increase the potential for the household to pay off the debt and increase home equity.

Social Connections

Second, social connections across geographic areas may lead to differences in young adult wealth. Research has highlighted the presence of strong social support in rural communities, and rural youths may share stronger ties and denser networks than do youths in other areas (Crockett, Shanahan, and Jackson-Newsom 2000; Howarth 1995; Stegner 1992). Social connections during adolescence are particularly important: in modern industrial societies adolescents are largely sequestered from adults, allowing students to form their own unique social systems (Coleman 1961; Milner 2004). As James Coleman (1961, 174) notes, “There are few periods in life in which associations are so strong, intimate, and all-encompassing as those that develop during adolescence.” Whereas adult society is functionally differentiated into worlds such as work, family, or neighborhoods, adolescent social life is comparatively one dimensional. Most adolescents spend the majority of their time involved in school or school-related activities that bring students together with the same sets of people. Informal relations with other adolescents—primarily friendship and romance—make up the core of the adolescent society.

The intense peer relations, influential cliques, and broader social hierarchies that characterize adolescence affect behaviors and outcomes during youth and continue to shape well-being into adulthood (Bearman and Moody 2004; Haynie 2002; Milner 2004; Umberson, Crosnoe, and Reczek 2010). Evidence indicates, for example, that adolescent social relations affect important development outcomes including grades, high school graduation, and other measures of academic achievement (Singh and Dika 2003); delinquency, violence, contact with the criminal justice system; self-esteem, depression and suicidality (Bearman and Moody 2004; Haynie 2002; Kreager 2007; Mueller and Abrutyn 2015); and self-reported health, smoking, substance abuse, body mass index, and other measures of health (Crosnoe 2002; Ennett and Bauman 1994; Mercken et al. 2010; Osgood et al. 2013). Evidence also indicates that adolescent social ties are associated with success in adulthood as measured by employment status and income (Shi and Moody 2016).

We anticipate that differences in adolescent social networks between rural and nonrural areas are likely to contribute to young adult wealth outcomes for three reasons. First, the experience of being connected to others—that is, the experience of having constituencies that confer status and information—might contribute to creating a still-unmeasured skill that translates into later success. This might include the ability to ease tensions between conflicted peers, switch language or behavior quickly between microsocial crowds or easily pick up on social cues that allow one to navigate later employment settings, to earn income, and ultimately to generate wealth with greater ease (Davis 1966; Festinger 1954; Shi and Moody 2016). Second, having social connections that can provide opportunities for educational advancement, occupational training and success, capital to buy a house or start a business, and related tangible outcomes might translate into adult wealth (Davis 1966; Festinger 1954; Shi and Moody 2016). For these reasons, we anticipate that more socially connected adolescents will have higher net worth and more financial assets in early adulthood. We also anticipate that adolescent social relations will increase the likelihood of homeownership in young adulthood. Third, social relations can confer and reinforce savings habits that manifest in different propensities to buy certain types of assets in a somewhat predictable order. For example, people with traditional values tend to buy homes earlier in life and to invest more of their savings in the family home than those with less traditional values (Keister 2008). Similarly, traditional values are associated with postponing investments in financial assets until later in life, even controlling for other predictors of these forms of saving (such as education and income). Because people imitate the savings behaviors of family and other social relations (Chiteji and Stafford 1999; Chiteji and Stafford 2000), it is likely that those raised in rural communities—particularly if they are highly connected to others—will imitate more traditional savings trajectories, including early home purchases and later investments in financial assets.

Job Opportunities and Income

Third, job opportunities and income are an important link between geographic residence in adolescence and young adult wealth. Agriculture, low-skilled manufacturing, and natural resource industries have been replaced with lower-paying jobs in the service industry in many rural areas (Hamilton et al. 2008). As a result, many rural communities that already lagged behind other geographic regions struggled to recover from the Great Recession, leading to even larger gaps among geographic regions (Fry 2013). Declines in federal investment in infrastructure for rural communities exacerbated these problems and, although not all rural communities are the same (Hamilton et al. 2008), the broad trend has been toward high and rising levels of unemployment (Duncan 2015; Economic Research Service 2019a) and few opportunities for self-employment (Tsvetkova, Partridge, and Betz 2017). Consistent with increasing unemployment, incomes are comparatively low, and poverty—including child poverty—is high in rural areas (Duncan 2015; Economic Research Service 2019a). Recent evidence also suggests that poverty risk is high and increasing even for those who are employed in rural areas, that the rate of working poverty is higher in rural areas than in other geographic areas (Thiede, Lichter, and Slack 2018), and that poverty is persistent across generations (Lichter and Graefe 2011; Lichter and Schafft 2016; Thiede, Kim, and Slack 2017). Evidence that low-income children who grow up in rural commuting zones tend to be more upwardly mobile than their rural counterparts may, in reality, reflect lower starting points for rural children rather than a particularly propitious pattern (Chetty et al. 2014).

We expect that limited job opportunities and low income levels will be important factors driving differences in young adult wealth across the rural-urban continuum. Importantly, income (the flow of funds into a household from wages, salaries, government transfer payments, and other sources) and wealth (net worth or net saved assets at a single point in time) measure different aspects of financial well-being. Income is a measure of short-term security that reflects current employment status as well as educational attainment and other aspects of human capital. Wealth is broader: it can come from intergenerational transfers, from active saving, or from the appreciation of investments. Of course, income and wealth are positively correlated, but the correlation is not particularly high. The correlation between total household income and total net worth among U.S. households is only about 0.50 and is relatively stable over the life course (Keister 2018). Part of the explanation for the relatively low correlation is intergenerational transfers: people who inherit may have high wealth and low income. Another part of the explanation is behavioral. Some households have high income from current work but low saving rates and, as a result, low wealth. At the other extreme, some households have a high net worth but low income. A person who inherited wealth or a retiree who saved consistently during the working years may have high levels of assets but low income. The association between income and wealth is likely to be fairly low for young adults who grew up in rural communities because they are unlikely to have inherited and have had little time to save on their own. Nonetheless, income remains a critical determinant of saving, investing, and wealth accumulation. Income also affects whether a household will qualify for loans such as mortgages. For these reasons, we expect that income is likely to increase net worth, financial assets, and homeownership.

EXPECTATIONS

Our expectation is an association between geographic residence in adolescence and young adult wealth. We also anticipate that this association varies in meaningful ways across the components of wealth including net worth, financial assets, homeownership, and mortgage debt. In particular, we expect that those who grow up rural will be less likely than their peers to have negative net worth but will also have fewer financial assets. We expect that homeownership will be high for those raised in rural areas but that they will have comparably less mortgage debt. Homeownership is a particularly important wealth measure in young adulthood. The history of high rates of homeownership in rural areas is a long one (Goodman et al. 2016); research has also shown that people learn how to save from family and friends (Chang 2005). It follows that those raised in rural areas may gravitate toward homeownership more readily as young adults regardless of where they live. Debt is also important: those who stay in rural areas and buy homes are likely to assume comparatively low levels of mortgage debt because home values are relatively low in rural areas. Those raised in rural areas also assume less education debt, consistent with having less education, and this will contribute to their overall wealth as well. Together, these patterns suggest that young adults raised in rural communities are less likely than their peers to have negative net worth. Because rural areas have a unique set of characteristics and challenges, we expect that the association between growing up in a rural area is unique in its association with young adult wealth relative to growing up in all other geographic regions but that the differences are most pronounced when rural and urban youth are compared. Notably, we are not proposing that place of residence in adolescence is more (or less) strongly associated with place of residence in young adulthood; instead, we propose that place of residence in adolescence is associated with young adult wealth even when place of residence—and other factors that contribute to wealth—are held constant. We are also not making formal causal arguments. That is, we expect

Young adults raised in a rural area are less likely to have negative net worth, but they also have fewer financial assets compared to those raised in other regions.

Young adults raised in rural areas are more likely to be homeowners, but they have less mortgage debt than those raised in other regions.

Young adults who grew up in rural areas have assets and debts that differ from their peers who grew up in all other geographic regions, but the difference is most pronounced between those raised in rural versus urban areas.

DATA

To study these issues, we use data from the National Longitudinal Study of Adolescent to Adult Health (Add Health). Add Health is a longitudinal study of U.S. adolescents who were in grades seven through twelve (ages twelve through eighteen) during the study’s first wave (1994–95). We use Add Health because it is a high-quality source of information about young adults that also includes important data about their upbringing. Importantly for our purposes, young adults—including Add Health respondents—do tend to have some savings by the time they are in their mid-twenties and even more commonly by their early thirties. It is also common for people this age to be homeowners. Many of the data sets that include wealth information (such as the National Longitudinal Survey of Youth, the Panel Study of Income Dynamics, and now Add Health) start to include questions about wealth when respondents are in their mid-twenties for this very reason. Many young people (again, including Add Health respondents) still have zero or negative net worth at this life stage, but many people have begun to accumulate something by their twenties. Consistent with this, in Add Health, we see that 83 percent of respondents have some assets and 44 percent are homeowners. These estimates are in line with data from the Survey of Consumer Finances (SCF), the gold standard for wealth information in the United States and with research published from the SCF (see, for example, Bricker et al. 2014; Keister 2014, 2018).

Add Health collected four additional waves of data on these adolescents, including a third between 2001 and 2002 (ages nineteen through twenty-five) and a fourth between 2008 and 2009 (ages twenty-six through thirty-two). We use waves 1, 3, and 4. Wave 1 includes detailed information about respondents’ adolescent region of residence, family structure, friendship ties, and demographic information. Waves 3 and 4 include follow-up information about young adult wealth (including net worth, homeownership, financial assets, and debts), educational attainment, income and job status, family structure, region of residence in young adulthood, and demographics. Together, these data provide a rich source of information on both adolescent social and demographic conditions and young adult achievements uniquely suited to our purposes. We include only respondents who were represented in waves 3 and 4 and who provided valid data for variables of interest in our sample and those who were still living with their parents (16 percent of Add Health respondents). A small number of respondents (fewer than 2 percent) reported being homeowners but also reported living with their parents. We coded these respondents as not owning a home. Our ultimate sample includes 7,758 respondents for models of negative net worth, financial assets, and homeownership. For models of mortgage debt, our sample is 3,232 because we omit nonhomeowners.

MEASURES AND METHODS

We use four outcome variables to measure young adult wealth; all outcomes are taken from wave 4 of Add Health. First, we measure overall net worth as self-reported negative net worth, relative to zero or positive net worth. We focus on negative net worth because having more debts than assets can indicate that a household is in a financially precarious position. However, the substance of our findings does not change if we model overall net worth as positive net worth relative to zero or negative net worth. This simple categorical measure is ideal for our study because our respondents are young and variation in net worth across households is still relatively minimal. Second, we measure financial assets as the dollar amount of assets other than real estate owned by the household. Add Health reports financial assets in nine dollar-range categories. We assign the midpoint of the category selected by the respondent to indicate the value of their financial assets. Ideally, we would have the actual amount of financial assets owned, but Add Health does not make these values public to ensure respondent confidentiality. Our measures are consistent with well-documented financial asset values owned at this life stage (see Bricker et al. 2014; see also discussion of table 1). We do not know the details of the types of financial assets owned by Add Health respondents because the survey does not include this level of data.

Descriptive Statistics

Third, we use a dichotomous measure of homeownership to indicate that the respondent’s household currently owns a home. Becoming a homeowner is a significant step in a financial trajectory, separate from the value of the home owned. Therefore, we model ownership of this asset as a dichotomous state to capture the importance of this step in a financial life course. Ideally we would have home value as well, but Add Health does not include home value. Fourth, we measure mortgage debt as a continuous dollar amount. We focus on mortgage debt because it is a liability that has investment value as well as being an obligation to repay a sum of money. Simultaneously, the value of mortgage debt indicates the value of the home owned, providing a uniquely rich source of information about the household’s finances. Although it does not do so with financial assets, Add Health reports the value of mortgage debt as a continuous measure, allowing us to evaluate this outcome with greater precision. Descriptive statistics for mortgage debt values in our sample are consistent with other well-documented values for mortgage debt owned.

Our primary independent variable is the RUCA coding for respondents’ place of residence during adolescence. Geographic differences between rural and urban areas cannot be captured by a simple binary and are experienced differently across the United States (Lichter and Brown 2011; Lichter and Ziliak 2017). RUCA codes, taken from census files, provide a better classification of these differences and assign locations to one of seven categories: metro core, metro area, micro core, micro area, small town core, small town area, and rural. Our use of the RUCA measure resembles previous research using Add Health data (Lawrence, Hummer, and Harris 2017).

We also include several control variables. We measure highest level of education attained using data from wave 4; we code education as a series of dichotomous measures including less than high school, high school, some college, college degree, and advanced degree. Some respondents may not have completed their educations, although only 6 percent of respondents were still taking college courses by wave 4. Future research might explore whether those who continued their educations are unique in ways that affect the results included in this article.

We include two measures of social connections. First, we include a continuous measure of indegree or popularity using data from wave 1. In wave 1, respondents in eligible schools identified up to five male and five female peers as friends from a roster of students in their school. For single-gender schools, respondents were allowed to select five students from a corresponding sister school. Thus, each individual could nominate up to ten friends. Second, we include a binary measure indicating whether a respondent was an isolate in adolescence, meaning that they neither selected peers as friends nor were selected as a friend by their peers in wave 1. Add Health does not include adult social connections, so we are unable to control for these ties. We measure total household income with a continuous measure from wave 4 indicating all sources of wages, salaries, transfer payments, and other income. We use household income because our unit of analysis is the household. However, preliminary analyses using personal income produced substantively similar results.

We also include controls for marriage and fertility to capture family structure. We measure marital status using a dichotomous indicator of whether a respondent lives with either a spouse or a romantic partner as opposed to living with neither; those who are not married are our reference category. We use married as the omitted category. We capture fertility with a continuous indicator of the number of children ever born in the household. We control for race-ethnicity using a series of dichotomous indicators showing that the respondent reports identifying as white, black, Asian, Native American, Latino, or other. Gender is a dichotomous indicator that the respondent is female.

We use a combination of descriptive statistics, logistic regression, and generalized least squares regression to explore our ideas. We first provide descriptive statistics comparing the wealth and other traits of respondents by adolescent RUCA. We model negative net worth and homeownership with logistic regression models; we model financial assets and debt with generalized least squares regression models. We present model results with and without control variables for comparison and to suggest directions for future research. We include basic control variables in model 1. In model 2, we add additional controls for marital status and fertility. In models 3 and 4, we add measures that we discuss in the background section and young adult place of residence. Notably, these models suggest that formal mediation analysis might usefully identify whether the control variables we include mediate the relationship between geographic place of residence in adolescence and young adult wealth. However, we make no formal claims about causal relationships and hope that future research will explore the potential for causation between rural upbringing and young adult wealth.

Table 1 provides descriptive statistics for our variables. Consistent with previous research on wealth ownership, approximately 20 percent of respondents have negative net worth, and median financial assets owned at this stage is a little more than $20,000 (Bricker et al. 2014; Bricker et al. 2016; Keister 2014). Also consistent with previous research, the distribution of financial assets is highly skewed, a pattern that is evident in the difference between mean (more than $82,000) and median ($20,679) in financial assets (Bricker et al. 2016; Killewald, Pfeffer, and Schachner 2017). Approximately 46 percent of respondents are currently homeowners, and the median mortgage owned is $99,499. Sample demographics are consistent with other research published using Add Health data (Bearman and Moody 2004; Shi and Moody 2016) including gender, age, and family structure. Our descriptives also match other published sources using RUCA codes for these samples (Lawrence, Hummer, and Harris 2017). Because we restrict our sample to respondents with valid data in waves 1 and 4, slight differences between our descriptive statistics and other published research reflect differences in the sample used for analyses (Lawrence, Hummer, and Harris 2017; Shi and Moody 2016). Missing data on wealth variables are minimal, and robustness checks indicated that results are not sensitive to missing data.

Additional descriptive data in table 2 provide preliminary evidence that young adult wealth varies by adolescent geographic residence in ways that are consistent with our expectations. The first four rows of the table include mean values for our dependent variables (measured in wave 4, when respondents were young adults) broken down by adolescent RUCA. Young adults who grew up in rural communities were less likely to have negative net worth than their peers, especially those who grew up in metro core, metro commuting, small town core, and small town commuting areas. Those who grew up rural owned fewer financial assets than other young adults, especially those who grew up in metropolitan areas. Respondents who grew up rural were also more likely to be homeowners but had considerably less mortgage debt than their peers from metro areas.

Wealth by Adolescent RUCA

Table 2 documents systematic individual differences in our control variables by adolescent RUCA as well. We include family structure in this table—measured with marital status and number of children—because family structure has historically varied across the rural-urban continuum (Heaton, Lichter, and Amoateng 1989; McLaughlin, Lichter, and Johnston 1993). In recent decades, however, family structure has changed quite noticeably in rural areas. Delayed marriage, nonmarital fertility, cohabitation, and divorce are all increasingly common in rural communities (Carson and Mattingly 2014; Glasgow 2003; MacTavis and Salamon 2003). Likewise, fertility rates have declined in both rural and urban areas, and as a result, total fertility in rural areas are increasingly comparable to fertility in other geographic areas (Hamilton, Rossen, and Branum 2016; Jones and Tertilt 2006; Ng and Kaye 2015). As a result of these changes, gender roles and the division of labor both in and out of the household have changed dramatically, rural men spending more time on childcare and rural women spending more time working out of the home (Smith 2017). Consistent with these social and economic changes, the descriptive statistics in table 2 show that marriage rates and family size vary only modestly across the rural-urban continuum. The descriptive statistics in table 2 also compare educational attainment, social ties, and income by RUCA code and show some small but systematic differences. Rates of college completion and attaining advanced degrees are noticeably lower for those who grew up in rural communities, particularly when compared with those who grew up in all other regions with the exception of those from small town commuting areas. The most notable difference in social ties is for those who grew up in metro core areas who were more likely to have no ties and to have somewhat lower indegree than their peers. Finally, young adult incomes are somewhat lower for respondents from rural, small town, and micro commuting RUCAs.

ADOLESCENT RUCA AND YOUNG ADULT WEALTH

Our multivariate results suggest that growing up in a rural community is indeed associated with young adult wealth. Table 3 presents results from logistic regression models predicting negative net worth. In all models, we omitted those raised in rural areas so that all other coefficients are compared to respondents from a rural RUCA. Model 1 is a base model and shows that those who were raised in metropolitan core and metropolitan commuting RUCAs were more likely than those raised in rural RUCAs to have negative net worth. There is no difference between those raised in other RUCAs and those raised in rural RUCAs; this is notable because it suggests that rural, small town, and micropolitan RUCAs have similar long-term associations with wealth. Other control variables are in the direction we would expect. The likelihood of having negative net worth decreases with age; and black respondents are more likely than white respondents to have negative net worth, and Asian respondents are less likely than white respondents to have negative net worth (Boen 2016; Taylor et al. 2011).

Logistic Regression of Whether Respondent Has Negative Net Worth

Notably, the coefficient for Latino respondents in table 3 is negative and statistically significant, indicating that Latino respondents are less likely than white respondents to have negative net worth. This finding is consistent with a growing body of research on status attainment—including wealth accumulation—among Latino Americans. This literature builds on a large literature about immigrant attainment that is characterized by intense debate regarding the degree to which immigrants incorporate into the host country over time. Some scholars propose that immigrants tend to follow a straight line trajectory leading to integration into the host country and progressively higher attainment on key measures such as education, income, and wealth (Alba and Nee 2003; Alba, Kasinitz, and Waters 2011). Others argue that racial distance from the American mainstream and other challenges associated with membership in the immigrant second generation created what is referred to as segmented or downward assimilation (Haller, Portes, and Lynch 2011a, 2011b; Portes and Zhou 1993; Zhou et al. 2008). A growing body of work explicitly looks at the wealth ownership, including financial asset ownership, of Latino respondents; this literature finds high levels of early-life disadvantage among Mexican Americans and other Latino Americans, but these disadvantages are less pronounced in the second and third generations than in the first. This work also confirms other research that finds high levels of young adult impediments to mobility for Mexican Americans and other Latino Americans; but evidence suggests that these early roadblocks do not translate into lower adult wealth. Indeed, researchers find that Latino Americans have less total wealth than whites but more than African Americans and that many Latino Americans are beginning to accumulate significant financial assets from sources such as business startup (Aguilera 2009; Keister, Agius Vallejo, and Borelli 2014; Vallejo and Keister 2019). We conducted significant sensitivity tests to ensure that our results are not influenced by outliers, whether particular high-SES subsamples (such as some Cuban respondents) are being weighted appropriately, and to otherwise ensure the robustness of our findings. A full examination of the wealth accumulation patterns of Latino respondents in the Add Health is beyond the scope of this article, but future research might usefully engage more fully with this issue.

Model 2 adds controls for family structure and shows that adding this control does not change the relationship between RUCA and negative net worth; that is, growing up in a metropolitan core or metropolitan commuting area is still positively associated with negative net worth. Model 3 also controls for educational attainment and social ties, and model 4 controls for income. Once these control variables are included, our adolescent RUCA measures are no longer significant.

Table 4 contains results from generalized least squares regression models of financial assets. Again, we include only basic controls in model 1 and subsequently include controls for family structure, educational attainment, social ties, and household income. Model 1 shows that respondents raised in rural communities have fewer financial assets than those raised in metropolitan core RUCAs; other RUCA codes are not significant. When we add education and social ties in subsequent models, the association between adolescent RUCA and young adult financial assets is no longer significant. Models 3 and 4 also show that our control variables are associated with net worth as we would expect. Educational attainment and income, for example, are both associated with higher levels of financial assets (Keister 2000, 2014). The association between social ties and financial asset ownership is not significant. There is no literature on social relations and wealth ownership to which we can compare this result, but previous work on adolescent social connections and income suggests that the association might be positive (Shi and Moody 2016). Consistent with our finding that Latino respondents were less likely to have negative net worth than white respondents, the coefficient for Latino respondents in table 4 is large and positive; however, this association is not statistically significant.

Generalized Least Squares Regression Models of Financial Assets (In Thousands of Dollars)

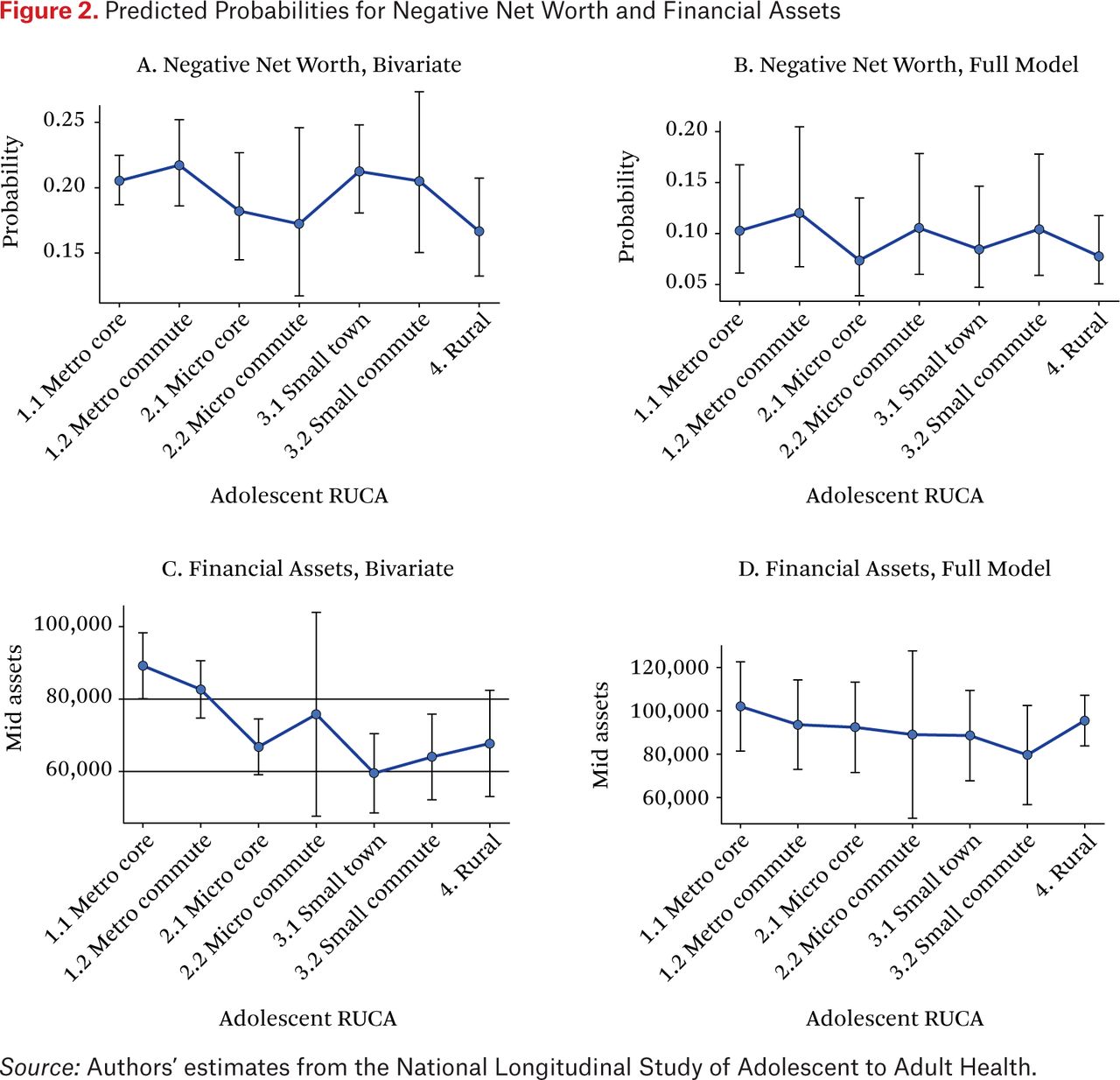

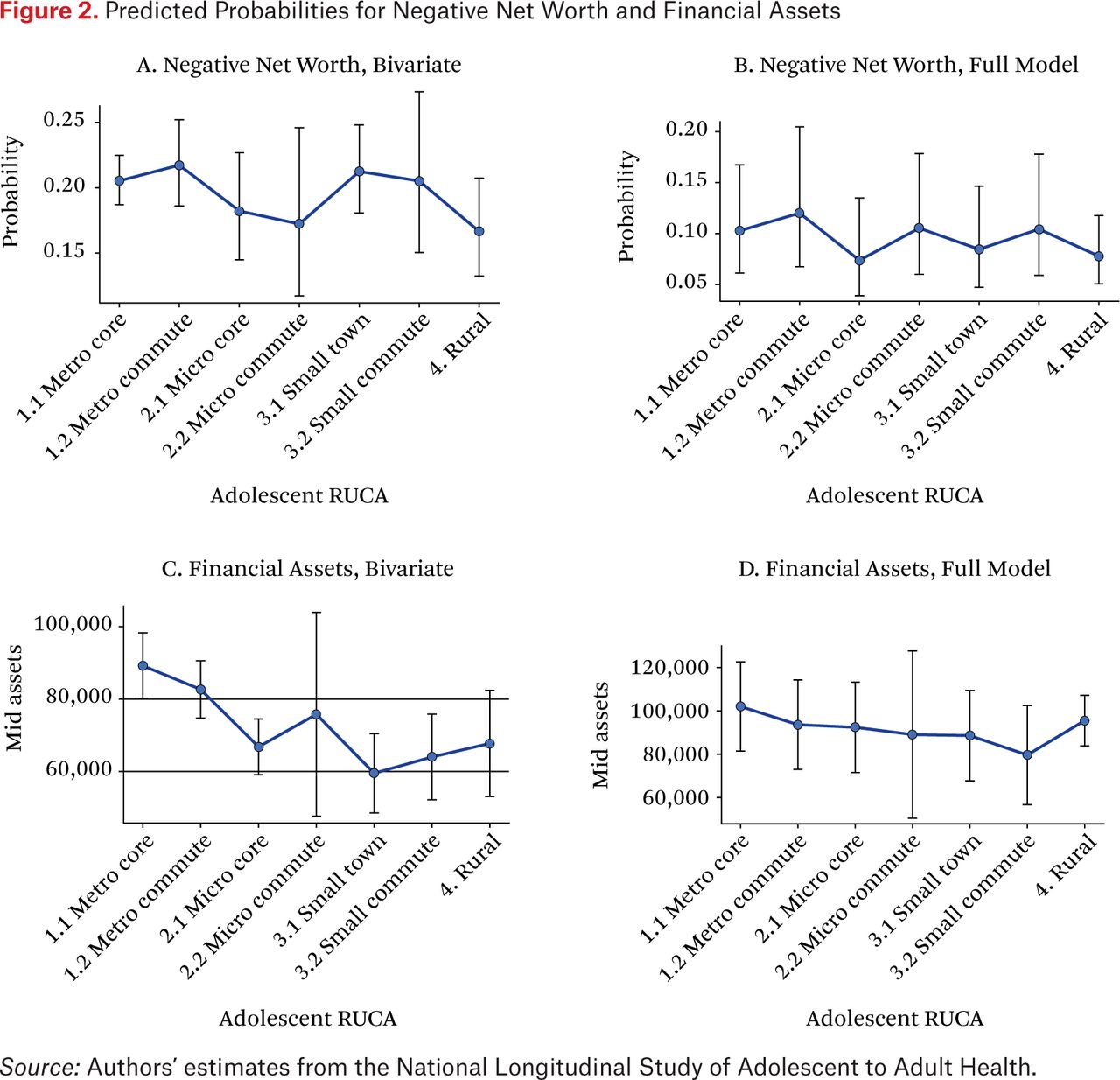

Figure 2 illustrates the findings shown in tables 3 and 4 using predicated probabilities. The figure includes four visualizations of predicted negative net worth and financial assets. Panel A is the predicted bivariate association between adolescent RUCA and having negative net worth in young adulthood; the figure compares respondents by adolescent RUCA code with no other variables included in the model. These results are based on models similar to those shown in table 3, model 1 but with no control variables. Panel B also displays predicted probabilities for models of negative net worth, but results in this figure include all covariates included and held at their means (computed using model shown in table 3, model 4). Similarly, panel C shows bivariate predicted financial asset values, and panel D shows predicted financial asset values with all covariates included in the models and held at their means (computed using model shown in table 4, model 4). All figures include 95 percent confidence limits.

Predicted Probabilities for Negative Net Worth and Financial Assets.

Panels A and B highlight the similarities in wealth outcomes for those raised in rural, micropolitan core, micropolitan commuting, and small town core RUCAs: the predicted probability of having negative net worth given that a respondent was raised in one of these RUCAs is lower than for those raised in other (metropolitan and small town commuting) RUCAs. The difference between panel C and panel D is more striking. The bivariate model (panel C) shows a clear decline in the probability of having negative net worth over the RUCA codes, ordered from metropolitan core to rural. When the full array of covariates is included (panel D), the association is much more tenuous. This provides additional evidence and a visual demonstration of the association between geographic region in adolescence and young adult wealth.

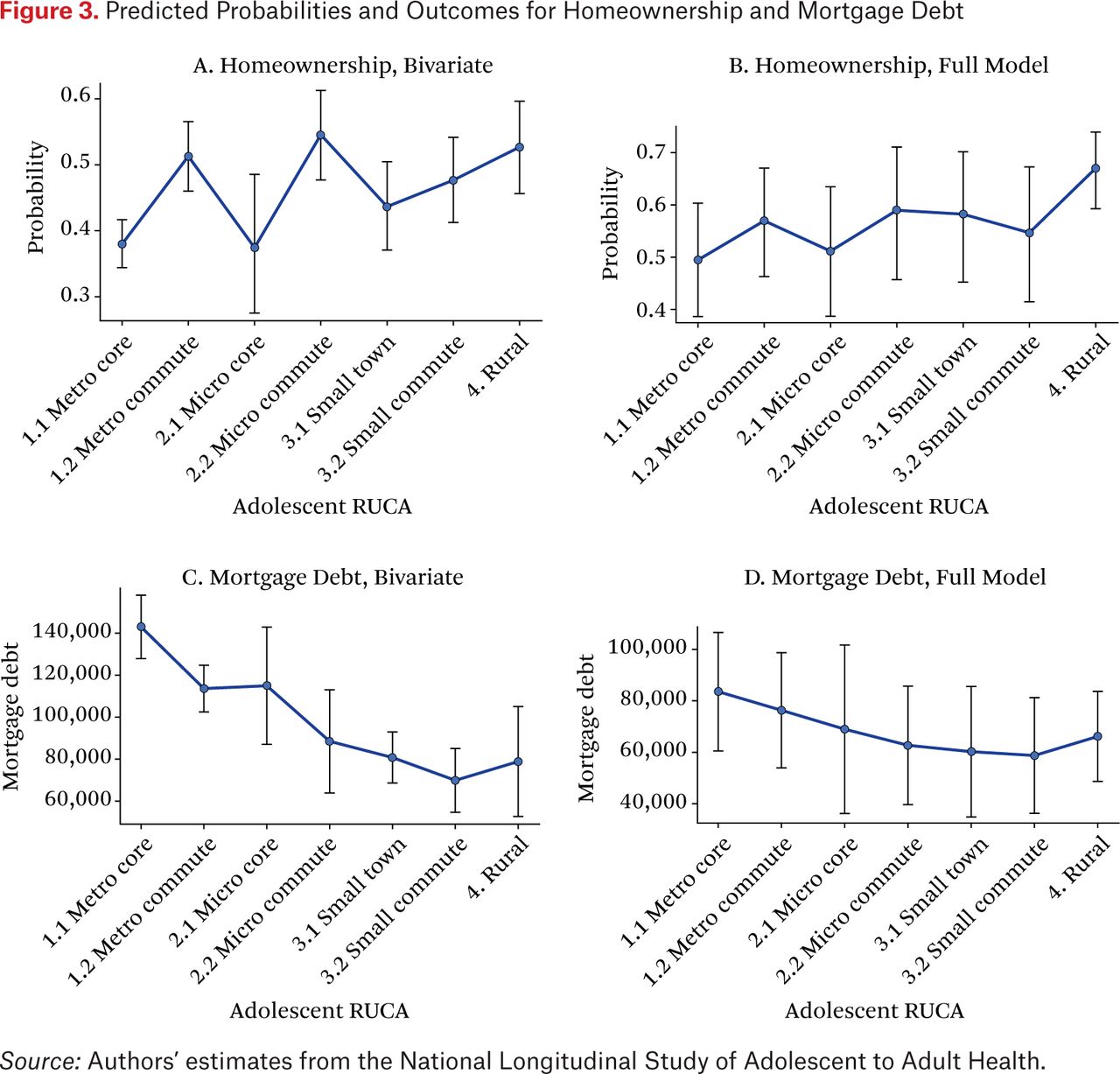

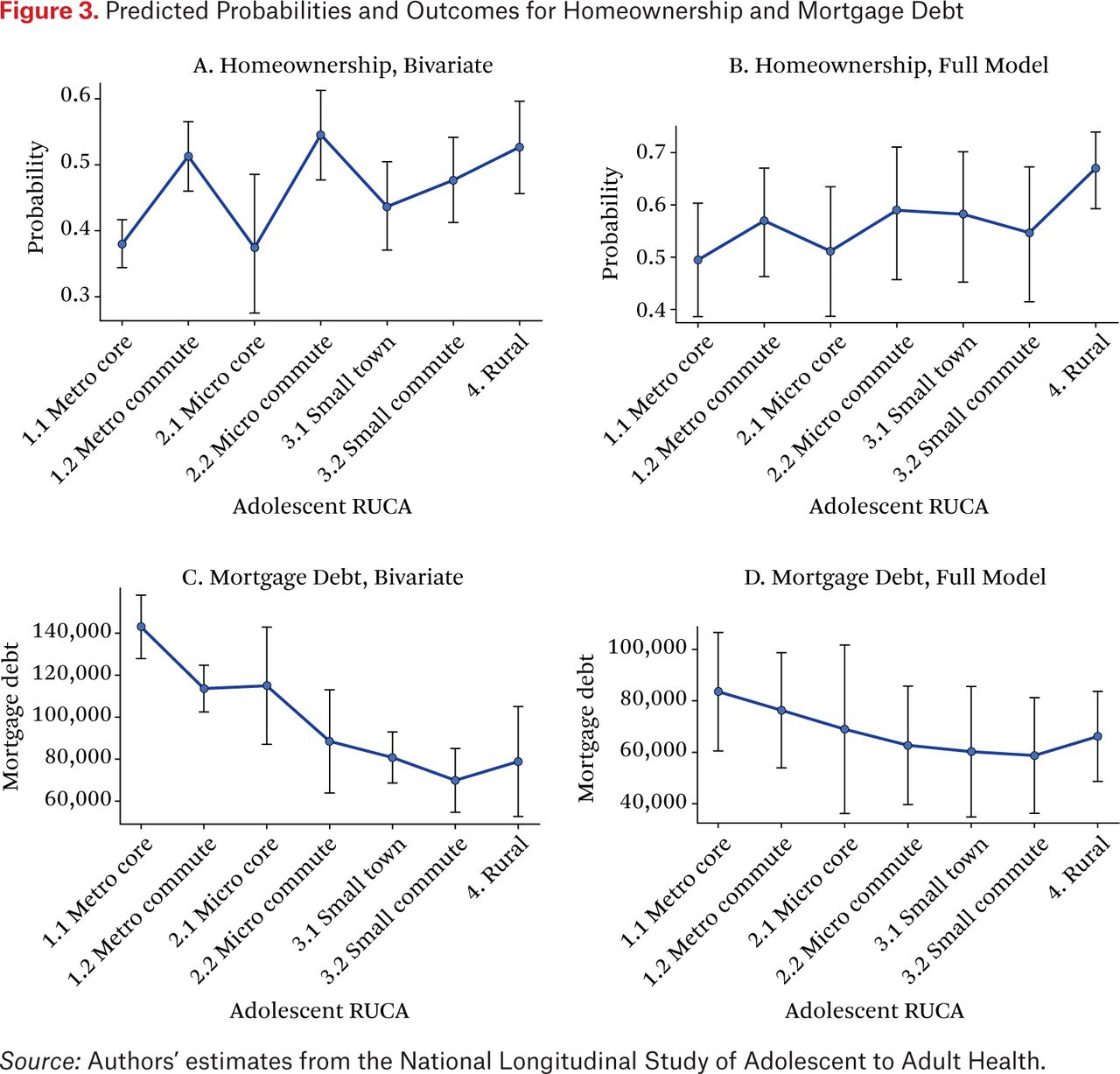

The association between adolescent RUCA and young adult homeownership is particularly strong. Table 5 includes results from logistic regression models of homeownership in young adulthood as a function of adolescent RUCA and other covariates. Again, model 1 includes only basic controls, and we add covariates in stages in subsequent models. Consistent with our expectations, model 1 results show that respondents who grew up in metropolitan core and micropolitan core communities are significantly less likely than those who grew up in rural communities to own homes. In model 1, the difference in homeownership between those who grew up in rural communities and those who grew up in metropolitan commuting, micropolitan commuting, small town core, and small town commuting RUCAs is not significant. These patterns persist in model 2, which includes family structure controls. In models 3 and 4, the difference between those who grew up in rural RUCAs and those who grew up in metropolitan commuting areas, small town core, and small town commuting areas is also significant. Given that some of the rural association operates through home prices in rural areas, it is notable that the adolescent RUCA codes remain significant even when young adult RUCA is controlled. Notably, our key control variables—educational attainment, indegree, and income—are positively associated with homeownership (having no ties is not significant). However, the significance of the adolescent RUCA does not decline across our models. This suggests that other unmeasured variables might mediate the associations between geographic area in adolescence and adult wealth. For example, if we were able to measure traditional approaches to saving more directly, we might find it to be the key mediator. Although a formal mediation analysis is beyond the scope of this article, future research could explore this possibility.

Logistic Regression of Whether Respondent Owns Home

The association between adolescent RUCA and young adult wealth is also clear in table 6, which includes results of generalized linear models of mortgage debt for those who are homeowners. Model 1 shows that respondents who grew up in rural communities and who currently own a home have less mortgage debt than those who grew up in metropolitan communities. The RUCA association is unchanged in model 2, but RUCA is not significant when education and social ties are controlled. These results provide additional suggestive evidence that education might be a mediating variable. That is, the association between educational attainment and mortgage debt is strong and significant. Research has documented a strong, positive relationship between education and mortgage debt, a pattern that reflects both supply (lenders are willing to lend to those with more education) and demand (educated consumers are more likely to apply for home loans) (Killewald, Pfeffer, and Schachner 2017). Our findings confirm this pattern and suggest that future research might usefully explore the role of education as a mediator between place of residence in adolescence and young adult wealth status. Figure 3 includes predicted probabilities to illustrate these models.

Generalized Least Squares Regression of Mortgage Debt (in Thousands of Dollars)

Predicted Probabilities and Outcomes for Homeownership and Mortgage Debt.

Our findings are largely consistent with our expectation of unique association between growing up in a rural area—relative to all other geographic areas—and young adult wealth. This unique relationship holds for net worth as well as for financial assets, homeownership, and debt. Despite some variation in the importance of growing up rural relative to other geographic regions across the models we present, the importance and unique relationship between a rural upbringing and early adult wealth is clear. It may not surprise readers to learn of a difference between the long-term trajectories of rural youth and of their metropolitan peers, given that urban-rural differences seem quite stark. However, an important takeaway from this work is that the effects of growing up rural are neither unilaterally good nor bad.

DISCUSSION AND CONCLUSION

In this article, we have studied the extent to which wealth ownership in early adulthood differs across the rural-urban continuum and the factors that are associated with those differences. We asked whether young adult wealth differs for those who grow up in rural communities and their peers who grew up in other geographic areas, and studied how these differences vary across four key wealth measures: net worth, financial assets, homeownership, and mortgage debt. Young adults raised in rural communities are less likely than other young adults to have negative net worth, but those raised in rural areas had lower financial assets than their peers in young adulthood. Differences in homeownership were an important component of our findings. Evidence indicates that young adults raised in rural communities are more likely to be homeowners than their peers, but that those who own homes have less mortgage debt than those raised in other regions. Although some of these patterns can be explained by rural youth who remain in their hometowns, our findings suggest that the patterns hold even for those who move to other regions. Evidence also indicates that growing up rural has a particularly important association with young adult wealth relative to other geographic areas. We speculate that this unique relationship reflects distinct characteristics of rural areas that are highlighted in other papers in this double volume; future research might usefully expand on these findings and explore in greater detail the reasons for these patterns.

Research on residential differences in well-being has often used a simple rural-urban distinction, but this strategy obscures nuanced and complex regional differences that are increasingly salient (Thiede, Lichter, and Slack 2018). We used detailed RUCA codes to measure region of residence in both adolescence and young adulthood, consistent with research that encourages researchers to move beyond the simple rural-urban dichotomy (Lichter and Brown 2011). Using the more detailed RUCA codes allowed us to document, indeed, more detailed differences by region than we might have found otherwise. In particular, those raised in rural areas were less likely to have negative net worth than those raised in metropolitan core and metropolitan commuting areas, but no differences between those raised in rural areas and those raised in other areas were apparent. Differences in financial asset ownership were significant only for those raised in rural and metropolitan core RUCAs. For homeownership, the differences were slightly different still: those raised rural were more likely to be homeowners and to have less mortgage debt than those raised in metropolitan core, metropolitan commuting, and micropolitan core areas. These patterns underscore clear differences in adult wealth between those raised rural and those raised in somewhat larger, more metropolitan areas. The difference between being raised in a rural area and in a micropolitan area or small town, however, are minimal at best.

Our research contributes to understanding an important long-term outcome associated with growing up rural, and also highlights the relevance of region to patterns of saving, investing, and debt that lead to adult wealth ownership. Despite this contribution, our work has limitations. For example, it would be ideal to have more detailed measures of assets and debts, including dollar values for all wealth components (such as value of the home, other real estate, all financial assets, pensions, other forms of debt), which would enable us to parse in even greater detail how a rural upbringing is related to young adult wealth. Important reasons related to confidentiality are the reason surveys do not collect more detailed wealth information; the severe skew of the wealth distribution means that when detail is available about a respondent’s assets, the risk is real that a respondent’s identity could be revealed. However, exploring the association between region and wealth would benefit from having more detailed data on key outcome variables.

In addition, results for our models suggest the importance of some of our key control variables in explaining the relationship between rural upbringing and young adult wealth ownership. These results indicate the potential benefit of using formal mediation analysis to identify which variables mediate the relationship between geographic place of residence in adolescence and young adult wealth. Future research may usefully explore this possibility. Exploring the interaction between place of residence in adolescence and place of residence in young adulthood would also be an important contribution to the literatures on wealth, rural residence, and residential mobility. That is, understanding whether those who stay in rural areas and those who move differ (thinking in terms of flows) could provide additional information about how place of residence is associated with assets and debts. Unfortunately, such analysis was beyond the scope of this article, but future research might extend the current work in this more dynamic direction.

Moreover, it would be ideal to have additional information on the reasons that respondents save and assume debt. For instance, understanding respondents’ risk preferences, knowledge about personal finance, approaches to borrowing and obtaining credit, long-term goals for saving and spending, plans for future education, and other savings goals would all clarify the mechanisms that lead to wealth ownership. Finally, it would be ideal to have additional longitudinal information about respondents’ life and family situations, education, work, and wealth in order to explore the longer-term effects of a rural upbringing on saving and wealth accumulation. Fortunately, Add Health continues to collect new information on respondents, suggesting that it will ultimately be possible to address this in the future. We acknowledge that Add Health respondents are at the early stages of adulthood and that their wealth ownership will certainly change over time. To be clear, our objective was to document their wealth ownership patterns in early adulthood, to explore the association between growing up rural and these wealth patterns, and thus to contribute to both the literatures on rural youth and wealth. Our contribution to the wealth literature includes looking at this critical life stage, one that is typically neglected in the wealth and wealth inequalities literature. Nonetheless, future work will usefully follow Add Health respondents to study how their ownership and assets and accumulation of debt changes as they pass through other life stages.

- © 2022 Russell Sage Foundation. Keister, Lisa A., James W. Moody, and Tom Wolff. 2022. “Rural Kids and Wealth” RSF: The Russell Sage Foundation Journal of the Social Sciences 8(4): 155–82. DOI: 10.7758 /RSF.2022.8.4.07. The authors would like to thank NICHD, 2 R25 HD079352-06 “Focused Training in Social Networks & Health.” Add Health is directed by Robert A. Hummer and funded by the National Institute on Aging cooperative agreements U01 AG071448 (Hummer) and U01AG071450 (Aiello and Hummer) at the University of North Carolina at Chapel Hill. Waves I-V data are from the Add Health Program Project, grant P01 HD31921 (Harris) from Eunice Kennedy Shriver National Institute of Child Health and Human Development, with cooperative funding from twenty-three other federal agencies and foundations. Add Health was designed by J. Richard Udry, Peter S. Bearman, and Kathleen Mullan Harris at the University of North Carolina at Chapel Hill. Direct correspondence to: Lisa A. Keister, at lkeister{at}duke.edu, Sociology-Psychology Building, Box 90088, Durham, NC 27708, United States; James W. Moody, at jmoody77{at}duke.edu; Tom Wolff, at tom.wolff{at}duke.edu.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.