Abstract

We assess the progress of the Affordable Care Act a decade after it became law. Although most of it remains intact, some parts have been repealed and others have not been implemented as expected. We review how and why the law has aged. Legal challenges have done less damage than is commonly appreciated, with the exception of the Supreme Court case that thwarted full expansion of Medicaid. Most of the important changes have other sources. Some parts were born to fail. Others were dismantled in response to interest-group pressure. Still others have failed to thrive for any number of reasons. Finally, the sabotage campaign by the Trump administration has had modest effects so far, but could pose a serious threat in the coming years.

After a decade, what is left of the Affordable Care Act (ACA)? The question is more difficult to answer than it might seem. The ACA is a remarkably complex statute, which partly reflects the complexity of the health-care system it aimed to reform. But it also reflects the broad scope of the law, hundreds of provisions touching on every aspect of that system—and some having no connection to health care at all. Reports on implementation tend to focus, understandably, on high-profile provisions such as coverage expansions or delivery-system reform (Blumenthal and Collins 2014; Obama 2016). These high-level reviews, however, overlook scores of other provisions that are important in their own right. The ACA has also been under siege from the moment it was enacted, and its Republican opponents have notched some victories in their campaign against it (Oberlander 2017).

Those victories, combined with genuine setbacks, have fostered the view in some quarters that most of the law has been dismantled. The well-regarded Kaiser Health Tracking Poll reported in May 2017 that one-quarter of the American public either believed the ACA had been repealed or were unsure whether it was still in effect (Kirzinger et al. 2017a). In September 2017, the Kaiser poll reported that half of the public thought the ACA marketplaces were “collapsing” (Kirzinger et al. 2017b). President Donald J. Trump has suggested on more than one occasion that the ACA is dead: “some people would say, essentially, we have gotten rid” of the law (Rappaport 2018; see also Savransky 2017).

But is that right? If not, just how wrong is it? In this article, we assess the status of the most significant provisions of the ACA. In particular, we identify those parts that have been repealed, invalidated, or abandoned, and offer a thematic framework for understanding the pressures that have buffeted the ACA in its first decade. Legal challenges are part of the story, but they have inflicted less harm than is commonly appreciated, with the exception of the Supreme Court case that thwarted full expansion of Medicaid. Most of the other major changes to the ACA have had different sources: some parts of the law were born to fail; others were repealed under intense pressure from interest groups; still others failed to thrive for a grab bag of reasons. And today, of course, the Trump administration is working to undermine or eliminate some parts of the ACA.

Three broad conclusions emerge from this overview. First, despite the partisan campaign to undo the ACA, the large majority of the law has been successfully implemented, often without much publicity. Second, many parts that have not been implemented, or that have been implemented slowly, were not the victims of Republican attacks. Repeated delays of some of the law’s revenue-raising and budget-cutting provisions, for example, have received bipartisan support. It was the Barack Obama administration that declared unfeasible an entire title of the original ACA—the CLASS Act—as early as 2011. Third, President Trump’s attempt to use executive power to sabotage the ACA has been only modestly successful so far, and some of his administration’s most significant initiatives have been held up in lawsuits. The outcome of those cases, and the coming presidential election, will matter enormously for the future of the ACA.

METHODS

We begin with a quantitative analysis of key provisions of the ACA. At the outset, however, we caution readers against placing too much weight on the numerical estimates. First, counting which provisions have and have not been implemented does not account for their relative importance. Second, we do not evaluate each of the hundreds of sections and thousands of provisions of the ACA.1 Instead, the subset of provisions consists of those that John McDonough (2011) designated as “key” shortly after the law was adopted. These 199 provisions span all of the ACA and range from relatively minor to major in both size and significance.2

In our analysis, we sought to determine the degree to which each provision has been implemented. Our analysis is inherently subjective and our goal therefore is to be as transparent as possible so that readers can make their own judgments. All sources of information used to determine implementation and outcome progress are publicly available and include federal regulations (as published on Federalregister.gov), Congressional Research Service reports, government webpages, and peer-reviewed journal articles. After making a qualitative judgment, we assigned a quantitative rating to each provision based on the degree to which it was implemented (0 = not implemented; 1 = partially implemented; 2 = all or virtually all of provision implemented).3 We also experimented with a more complicated five-category rating system, but because the summary results were virtually identical to those reported here, we use the simpler three-category rating system. We omit from our analysis several provisions that required no implementation; for example, Section 6801, which “conveys the sense of the Senate that health reform presents an opportunity to address issues related to medical malpractice and medical-liability insurance” and that “states should be encouraged to develop and test alternative models to the existing civil litigation.” Finally, we omitted several provisions because we could find no evidence on their implementation status, such as Section 6402(a), which directs “the Secretary [of the Department of Health and Human Services] to enter into data-sharing agreements with the Commissioner of Social Security, the VA and DOD Secretaries, and the IHS Director to help identity fraud, waste, and abuse.”

No obvious natural scaling applies to the importance of the provisions that we surveyed. To get an overall implementation score for each title, we simply average the zero-to-two measure across that title’s key provisions and express the result divided by two as a fraction. For example, a title with two provisions, one of which was fully implemented and the other of which was partially implemented, would have an overall score of 0.75 (= [0.5*2 + 0.5*1]/2). When possible, we present additional quantitative metrics of the extent to which a title’s provisions have been implemented. For example, in Title IX: Revenue Provisions, we use the original estimates from the Joint Committee on Taxation (JCT) of the amount of revenue each provision in Title IX was projected to raise to calculate what proportion of the projected revenue is attributable to provisions that have been implemented. Finally, we calculate an overall score for the ACA that takes into account the relative importance of each title by using the original projection of the spending and revenue associated with each title from the Congressional Budget Office (CBO) as a weight in averaging implementation scores across titles (CBO 2010).

We discuss the implementation of key provisions title by title, offering brief descriptions of what was implemented successfully and what was not in order to provide context for the quantitative scores.

After completing the quantitative analysis, we developed five categories that broadly capture the various reasons why some provisions were not implemented. These categories are legal challenges, born to fail, interest-group pressure, failure to thrive, and executive-branch sabotage.

ACA IMPLEMENTATION TITLE BY TITLE

Measured using our rough quantitative score, we find that 83 percent of the ACA has been implemented as written (see table 1). Here, we review the content of the ACA and the progress of implementation title by title.

Overview of ACA Implementation by Title

Title 1: Quality, Affordable Health Care for All Americans. The largest title of the ACA, measured in number of key provisions or in total spending and revenue, Title I focuses on the private health insurance sector. It includes forty-nine provisions, $509 billion in spending, $81 billion in revenue, and is 88 percent implemented. These provisions represented a revolution in the nongroup market and a much smaller but still substantial change for employer-sponsored coverage. Title I includes high-profile provisions such as the creation of health insurance marketplaces, premium tax credits, employer and individual mandates, community rating requirements, and the ban on lifetime caps on coverage, among others. With some exceptions, such as the individual mandate, most of these provisions have been implemented as written. As of 2019, 11.4 million Americans are covered by marketplace health insurance plans, down slightly from the peak of 12.7 million in 2016 (Kaiser Family Foundation 2019).

Title II: The Role of Public Programs. Medicaid expansion in the Affordable Care Act—which includes seventeen provisions, $459 billion in spending, $53 billion in revenue, and is 78 percent implemented—was meant to cover all adults ages nineteen through sixty-four living in families with income below 138 percent of the federal poverty level on January 1, 2014. Instead, a Supreme Court ruling rendered this expansion effectively optional for states.4 Table 2 shows the dates on which different states have implemented expansion and the proportion of the population of poor adults ages nineteen through sixty-four living in those states. Twenty-four states plus the District of Columbia chose to expand Medicaid on or before January 2014; these states contained about half of the target population of low-income non-elderly adults. Additional states implemented Medicaid expansion in the years just after 2014 or are now in the process of doing so. As of 2019, 64 percent of the adults in the expansion population live in states in which Medicaid expansion has been implemented or in which implementation is pending. It is thus reasonable to say that about two-thirds of this important component of the law has been achieved.

Growth of Medicaid Expansion

Title III: Improving the Quality and Efficiency of Health Care. Title III includes thirty-five key provisions, $54 billion in spending, $450 billion in revenue, and is 96 percent implemented. Its key provisions are intended to improve the quality of care (or at least not degrade it) while reducing federal payments, an effort broadly described as delivery-system reform. The provisions included large cuts in Medicare payments to Medicare Advantage plans and to hospitals; together, CBO scored these cuts as achieving $290 billion in savings over the 2010 to 2019 scoring window. The cuts, like most of the key provisions of Title III, have been implemented as planned. In addition to (relatively) simple spending cuts, Title III expanded quality measurement and value-based purchasing initiatives, and also created the Center for Medicare and Medicaid Innovation to facilitate the development and diffusion of innovations in Medicare policy (Rocco and Kelly 2020). Title III introduced innovative payment models for Medicare such as the Shared Savings Program, which spurred the growth of accountable care organizations, and expanded pilot projects of bundled payments. It remains unclear whether these initiatives will succeed in “bending the curve” of health-care spending, but they are still in place. The most significant Title III provision that has not been implemented is the Independent Payment Advisory Board, which we discuss in more detail later.

Title IV: Prevention of Chronic Disease and Improving Public Health. This title includes $18 billion in spending and $1 billion in revenue, and is 85 percent implemented. It includes a variety of provisions, nineteen in all, related to public health. The most significant of these, at least in terms of planned federal expenditures, was the creation of the Prevention and Public Health Fund. Other key provisions include nutrition labeling for restaurant menus, which happened slowly; a requirement that large firms provide break time and lactation space for employees who are nursing mothers; and a smorgasbord of relatively small grant programs to promote public health.

Title V: Health Care Workforce. This relatively brief title of the ACA, which includes $18 billion in spending and zero revenue, included some grant programs and changes to residency program rules. Eight of its nine key provisions—94 percent—were implemented. The ninth established a National Health Care Workforce Commission, and members were appointed in September 2010. Congress, however, never appropriated the money for the commission, which has therefore never met (Buerhaus and Retchin 2013).

Title VI: Transparency and Program Integrity. This title includes $3 billion spending and $7 billion in revenue, and is 90 percent implemented. Among its forty-three key provisions, it includes a variety designed to prevent fraud, including the creation of provider data banks for Medicare and Medicaid. It also includes a number of key provisions that could have been enacted independently but were instead enacted as part of the ACA, perhaps because they yield net revenue. (This is true of Titles VII and VIII as well.) Its standalone policies include the Elder Justice Act, intended to prevent abuse, neglect, and exploitation of older Americans; the Physician Payments Sunshine Act, which requires pharmaceutical companies and drug manufacturers to report payments to physicians; and the creation of the Patient-Centered Outcomes Research Institute.

Title VII: Improving Access to Innovative Medical Therapies. Including seven key provisions, this title entails zero spending and $7 billion in revenue. Fully implemented, it has accomplished two things. First, it adopted the Biologics Price Competition and Innovation Act of 2009 (BPCI Act), intended to create a simplified path for the approval of “biosimilar” therapies—essentially, generic versions of biological products approved by the Food and Drug Administration (FDA). This provision was faithfully implemented by the FDA but has not lived up to expectations. Title VII also expanded the 340B Drug Pricing Program in Medicaid, effectively increasing the number of hospitals that receive drug rebates from manufacturers.

Title VIII: Community Living Assistance Services and Supports. This title has only one key provision, includes zero spending and a stated $70 billion in forecast revenue, and was not implemented. The CLASS Act, as it was known, was intended to create an insurance-like program that would cover expenses for services required to help disabled individuals remain living in the community rather than having to move to a nursing home.

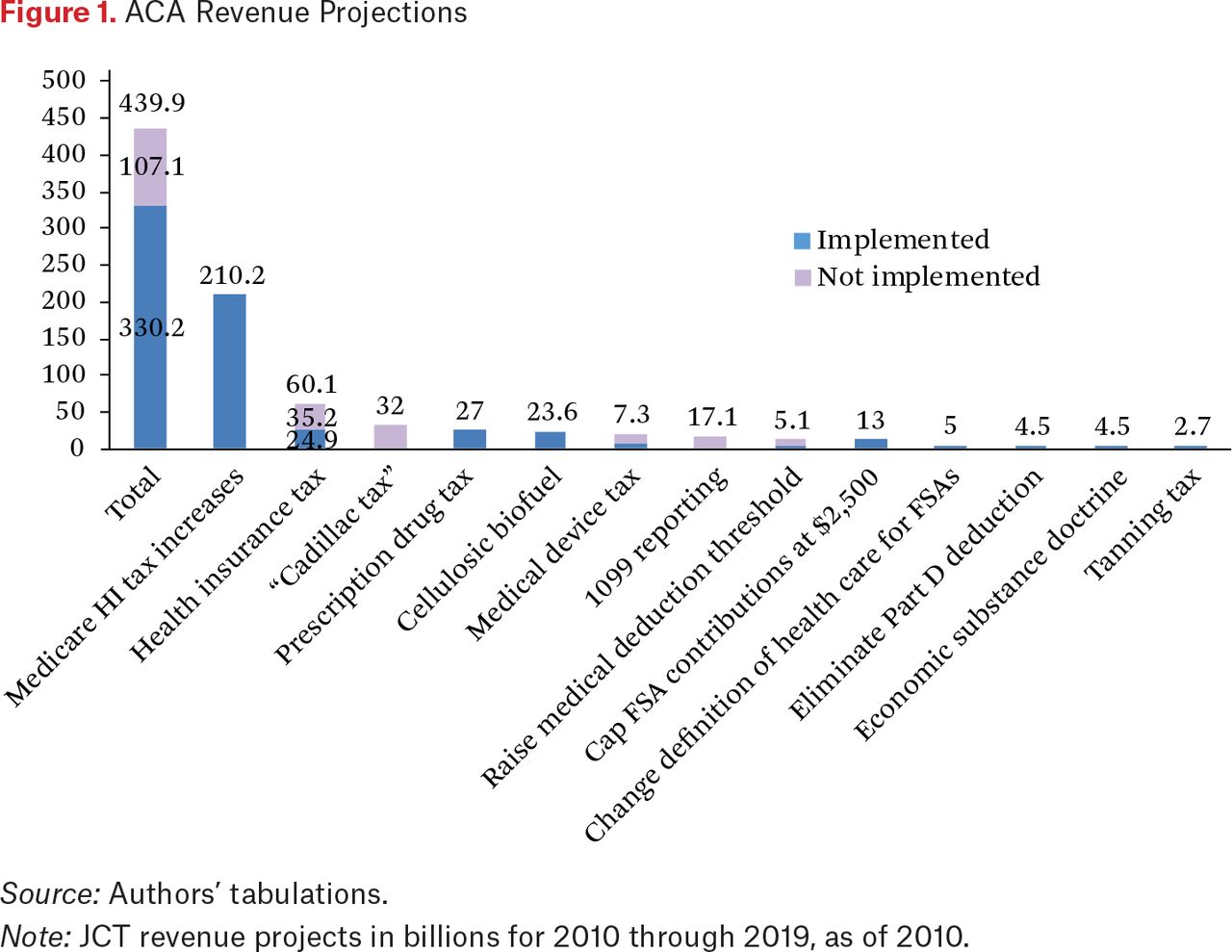

Title IX: Revenue Provisions. Revenue provisions in the ACA, nineteen in all, were projected to raise $438 billion between 2010 and 2019 (CBO 2010). Table 3 summarizes the provisions, the revenue projection associated with each, and the extent to which—79 percent—they have been implemented; figure 1 summarizes this information graphically. The largest of these revenue provisions, by far, were two new Medicare-related taxes on high-income individuals, one of which increased the tax rate on earnings and the other of which imposed a new 3.8 percent tax on unearned income. (Interestingly, only the former of those actually goes to the Medicare Trust Fund.) These two provisions were responsible for just over half of the projected new tax revenue in the ACA—and both have been implemented as written. Many smaller revenue provisions, such as capping contributions to flexible spending accounts at $2,500 and a tax on tanning salons, have also been fully implemented. Other revenue provisions, however, have not. Indeed, one related to tax reporting requirements was the first element of the ACA to be repealed, thirteen months after the law was passed. Others—including a tax on health insurers and medical device manufacturers, as well as the Cadillac tax—have been repeatedly suspended or delayed. Indeed, as of this writing, news reports indicate that all three of those taxes may be repealed as part of an end-of-2019 budget deal (Sullivan 2019).

Implementation of ACA Revenue Provisions

ACA Revenue Projections

Source: Authors’ tabulations.

Note: JCT revenue projects in billions for 2010 through 2019, as of 2010.

In all, the suspensions, delays, and repeals wiped out provisions that were projected to raise about a quarter of the $440 billion in revenue. Nonetheless, the other (revenue-projection-weighted) three-quarters of provisions have been implemented.

THEMATIC FRAMEWORK

Running though the ACA’s titles offers a sense of the law’s scope and complexity, as well as of the relatively small number of its provisions that have been invalidated, repealed, or abandoned. The raw description, however, obscures the reasons that the ACA has evolved as it has. Here we offer a loose thematic framework for understanding that evolution, examining legal challenges, parts of the ACA that were born to fail, interest-group pressure, a catch-all category for provisions that have not lived up to expectations for various reasons, and executive-branch sabotage. Table 4 presents examples of provisions in each category. We view these categories as a work in progress; the law is still evolving and will evolve still further in the coming years (witness the ongoing legal challenges). A generalizable analysis of why some provisions fail (Patashnik and Zelizer 2013), or of whether the ACA’s implementation reflects policy retrenchment (Hacker 2004), awaits the resolution of that ongoing uncertainty.

ACA Provisions Not Implemented: Themes and Examples

Legal Challenges

Thwarted in their efforts to prevent the ACA’s adoption, its opponents sought to undo the law in the courts. Over ten years, they filed dozens of lawsuits challenging various aspects of the ACA and its implementing regulations (see table 5). Although most of these cases were unsuccessful, a handful have fundamentally reshaped the law. More recently, ACA supporters have enlisted the courts to forestall Trump administration efforts to undermine the law.

Significant Litigation over the ACA

By far the most significant change to the ACA came in 2012, with the Supreme Court’s decision in National Federation of Independent Business v. Sebelius (NFIB).5 The case was lauded at the time as a victory for the Obama administration, and in some respects it was. Four conservative justices wanted to invalidate the entire statute because they believed Congress lacked the power to adopt the individual mandate. But the chief justice balked, and the Court held, by a 5–4 vote, that Congress had the power to impose the individual mandate under the taxing clause. The ACA’s reforms to the individual and employer-sponsored markets were thus constitutionally secure.

In another respect, however, NFIB was a calamity for the ACA. In a ruling as novel as it was unexpected, the Supreme Court held, by a 7-2 vote, that Congress lacked the power to condition the continuing receipt of traditional Medicaid on the adoption of the Medicaid expansion. Doing so was unconstitutionally coercive—“a gun to the head” of the states. As a remedy, the Court concluded that the federal government could not “withdraw existing Medicaid funds for failure to comply with the requirements set out in the expansion.”

Measured against the remedy that the Court’s most conservative justices would have preferred—the complete invalidation of the ACA—this again looked like a victory. But the Supreme Court’s decision transformed the stakes of the expansion decision for the states and, in so doing, distorted how the ACA was supposed to work (Sunkara and Rosenbaum 2016). Instead of forcing states to pick between an expanded Medicaid program and no Medicaid at all, the Supreme Court allowed states to pick between the status quo and the Medicaid expansion. Expansion was still tempting: the federal government picked up 100 percent of the expansion’s costs from 2014 to 2016, which dropped gradually to 90 percent in 2020. But states were free to decline the money if they wished.

Many did. About half of the states declined to expand their Medicaid programs as of January 1, 2014; nearly six years later, fourteen states have refused to expand. Most are in the South and Midwest, and include the major population centers of Texas, Florida, Georgia, and North Carolina. As a result, millions are uninsured who would have been covered had the ACA been left intact. A litany of studies has documented the adverse effects of not expanding Medicaid on coverage rates, access to care, financial stability, self-reported health outcomes, hospital budgets, and state budgets (Antonisse et al. 2018). One recent study estimates that “approximately 15,600 deaths would have been averted had the ACA expansions been adopted nationwide as originally intended by the ACA” (Miller et al. 2019).

Apart from the constitutional challenge to Medicaid expansion, however, constitutional attacks on the ACA have not fared well. The circuit courts have brushed aside arguments that the ACA violated the Origination Clause, that the employer and individual mandates infringe on religious freedom, that Congress impermissibly delegated its lawmaking powers, and that a provision preventing states from changing their Medicaid programs is unconstitutionally coercive (see table 5).

Three sets of statutory challenges to the ACA have gained more traction. The first, which culminated in King v. Burwell,6 involved a challenge to an Obama administration rule that made premium subsidies available nationwide. The challengers in King seized on a snippet of the ACA’s text that, read literally, would have offered premium subsidies to people in the one-third of states that set up their own exchanges, and not in the two-thirds that defaulted to the federally operated exchange. Over a three-justice dissent, the Supreme Court turned back the challenge, holding that adopting the plaintiffs’ interpretation of the statute would conflict with the legislative plan. But the vote was closer than commonly appreciated—both Chief Justice Roberts and Justice Kennedy were apparently on the fence after argument (Biskupic 2019, 291)—and the ACA only narrowly avoided a blinkered construction that would have led to massive state-to-state variations in exchange coverage.

The second set of legal challenges involved the “contraception mandate.” Technically, the ACA itself imposes no such mandate. It instead requires health plans to cover “preventive care and screenings” for women “as provided for in comprehensive guidelines” issued by a Department of Health and Human Services (HHS) subagency. But it surprised no one when the Obama administration announced that such preventive care included contraception. Since that announcement, religious organizations have filed a number of lawsuits challenging the contraception mandate. In Burwell v. Hobby Lobby,7 the Supreme Court held that, under the Religious Freedom Restoration Act, a privately held corporation need not provide contraception to its employees. Subsequent cases have also cast doubt on the legality of an Obama administration effort to accommodate the concerns of religious nonprofits.

Although Hobby Lobby and related cases loom large in the culture wars, they have had modest real-world effects. In 2015, only sixty-three employers availed themselves of the Obama administration’s accommodation for religious employers—and, per that accommodation, their employees still received contraception coverage, albeit without their employer’s involvement (HHS 2018c, 57575). The Trump administration has now issued rules to fully exempt any employer voicing religious or “moral” objections to the mandate. Even under those rules—which, for now, have been enjoined by the courts—only an estimated 109 employers, covering perhaps 727,000 people, would drop contraception coverage altogether (HHS 2018c, 57578). The vast majority of U.S. employers adhere to the contraception mandate, and the vast majority will continue to do so, Hobby Lobby notwithstanding.

The third case is House v. Burwell, a challenge brought by the Republican-controlled House of Representatives to the Obama administration’s issuance of billions of dollars in cost-sharing payments. A crucial ACA funding stream, these payments are meant to reimburse insurers for adhering to ACA rules that require them to limit the out-of-pocket costs of their low-income enrollees. The judge hearing the case held that the House had standing to sue and that, on the merits, the House was right: Congress never appropriated the money to make the cost-sharing payments. Although the Court allowed the payments to continue while the administration pursued an appeal, the 2016 election threw the status of the cost-sharing payments into doubt. After unsuccessfully trying to use the threat of cutting off cost-sharing payments to force Democrats to negotiate over a plan to repeal and replace the ACA, President Trump scrapped the payments in October 2017.

The funding cutoff was partly a response to an adverse court decision, but it also capitalized on a glaring oversight by the ACA’s drafters. Regardless, insurers found a way to cope. Working with state insurance regulators, they have channeled low-income enrollees into silver plans and then increased the premiums for those plans—and those plans only—to make up for the lost cost-sharing money. Because the amount that low-income enrollees can pay for coverage is capped at roughly 10 percent of their income, they are insulated from the resulting silver-plan premium spikes. In the meantime, higher-income enrollees are encouraged to buy platinum, gold, or bronze plans, whose prices have remained stable. Silver loading has thus protected enrollees and insurers from the full consequences of the loss of cost-sharing payments (Dorn 2019).

Although the ACA now finances cost-sharing protections through a much different mechanism than originally anticipated, the ACA’s basic protections are intact. The big loser is the public fisc. Not only does the federal government pay inflated premium subsidies to cover silver-loaded plans, but insurers have also sued to recover the billions of dollars in cost-sharing payments that they believe they are owed. If they win—they have had success so far, and the issue is now pending before the U.S. Court of Appeals for the Federal Circuit—they could recover more than $10 billion per year.

By 2017, the courtroom assault against the ACA appeared to have run its course. Such was not to be. As part of the tax reform bill—more on this in a moment—Congress effectively repealed the individual mandate by zeroing out the tax penalty for going without insurance. That spurred a group of red-state attorneys general to file a lawsuit, Texas v. United States, arguing that Congress created a constitutional defect in the ACA when it eliminated the mandate penalty. In their view, the individual mandate—the naked instruction to buy insurance—remained on the books, but could no longer be defended as a tax. What is more, because the Congress that adopted the ACA believed the individual mandate was essential to the law, the constitutional defect required the entire ACA to fall.

Lawyers from across the political spectrum derided the lawsuit, in particular the claim that fidelity to Congress’s intent required complete invalidation of a statute that Congress spent 2017 trying, and failing, to repeal. But the case was assigned to a conservative judge with a partisan reputation, and in late 2018, he declared the entire law invalid. An appeal has been filed; depending on how the U.S. Court of Appeals for the Fifth Circuit rules, the case may work its way to the Supreme Court sometime in 2020, perhaps in time for the election.

Born to Fail

Several features of the ACA were designed so poorly that they were doomed from the start. The most conspicuous early change came when Congress, in April 2011, repealed a requirement that businesses submit a 1099 Form for every business to which they paid more than $600 in the tax year.8 The anticipated compliance costs were thought to be “disproportionate as compared with any resulting improvement in tax compliance.”9 The Obama administration hailed the repeal as “a big win for small business” (Mills 2011).

That was a minor change, however. Not so the Obama administration’s determination in October 2011 that it would not implement the CLASS Act. As Secretary Kathleen Sebelius explained in a letter to Congress, she could not devise a long-term benefit plan that would be “both actuarially sound for the next 75 years and consistent with the statutory requirements” (HHS 2011a). This was the sobering conclusion of a disaster that had unfolded in slow motion. The goal of the CLASS Act was to offer a public, voluntary insurance plan that would help pay for supportive services to enable individuals with mild functional limitations to remain in the community rather than entering nursing homes (for more, see Gleckman 2011, 2012). It was a worthy goal, and one that might even have saved Medicaid some money in the long run. Whether a simple plan—perhaps one financed in part by beneficiary premiums and in part by government funds, along the lines of Medicare—might have been devised to meet this goal remains open to debate. The CLASS Act, however, contained two provisions that presented insurmountable obstacles. The first, included largely for political reasons, required the program to be self-sustaining. The second capped the premiums for low-income and student enrollees at an extremely low level, effectively requiring any better-off, nonstudent enrollees to pay even more for their coverage. Squaring this circle was simply not possible.

What was the CLASS Act doing in the ACA? As McDonough (2011) explains in detail, a version of the CLASS Act was originally introduced by Senator Ted Kennedy in 2005. The policy had powerful supporters as well as powerful opponents, and was controversial even among Democrats, who disagreed about whether it should be part of the ACA. Its inclusion may have had something to do with the fact that the CLASS Act gave the ACA’s CBO score a $70 billion bump, accounting for the lion’s share of projected $123 billion in deficit reduction. Premiums for long-term insurance would start being paid during the initial years of the program—most significantly, during the ten-year budget window that the CBO used to score the ACA—but most outlays would be made much later. Then Senate Minority Leader Mitch McConnell was not far off the mark when he charged that “the Class Act was a budget gimmick that might enhance the numbers on a Washington bureaucrat’s spreadsheet but was destined to fail in the real world” (Radnofsky 2011). Congress repealed the act in January 2013 as part of a bipartisan budget deal.10

Another quizzical feature of the ACA, at least in retrospect, was the $6 billion in loans that it appropriated to support the establishment of “cooperative health plans.” A consolation prize for the failure of the public option, cooperative health plans were to be nonprofit entities governed by their members, modeled on the success of flourishing plans such as Group Health in the Pacific Northwest and HealthPartners in Minnesota and Wisconsin (James 2013). Because they would plow profits back into the plans instead of distributing them to shareholders, and because of their consumer-focused governance structure, the hope was that they would offer an attractive insurance option for at least a portion of the exchange population.

The co-op program was troubled from the start. Insurance is a tough business, and brand-new co-ops generally lacked the wherewithal and the financial reserves to compete with established insurers in a novel market. Neither the co-ops’ nonprofit status nor their member-driven governance structure made them better than commercial insurers at pricing risk or designing health plans. At the behest of the insurance lobby, the ACA also saddled co-ops with onerous restrictions. Co-ops could not move into the employer-sponsored insurance market, for example, and could not use federal funds to market their plans.

When the exchanges went live in 2014, twenty-three co-ops participated. By January 2019, only four remained. The co-ops’ demise was hastened by a hostile Republican Congress and an Obama administration that hesitated to support such a fragile group of insurers. In budget negotiations in 2011, the Obama administration agreed to $2.2 billion in cuts to the loan program; in 2013, it accepted a Republican demand to end the program altogether (Markon 2013). The funding drawdown squeezed off the establishment of new co-ops. Then, in late 2014, Congress adopted an appropriations rider limiting the funds available under the “risk corridor” program.11 The loss of risk corridor funding drove many thinly capitalized co-ops into insolvency (CCIIO 2015; Jost 2016). Thus the co-ops did not fail on their own; they were pushed. But there was never any good reason to think they would succeed.

Interest-Group Pressure

Even as lawsuits and repeal efforts played out on the front page, powerful interest groups have quietly lobbied Congress, with some success, to dismantle portions of the ACA that threaten their bottom lines. Most of the resulting changes affect financing: either the repeal or delay of taxes, or the reversal of anticipated funding cuts. The changes have not threatened the basic operation of the ACA’s coverage expansions, and they have generally commanded bipartisan support.

The most noteworthy change has been the delay of the so-called Cadillac tax. An excise tax of 40 percent of the employer contributions to health plans over a certain threshold (initially $10,200 for an individual or $27,500 for a family, growing over time with inflation), the Cadillac tax was initially supposed to take effect in 2018. It was not designed primarily to raise revenue but instead to correct a distortion created by the tax code’s exclusion of health insurance from employee wages. That distortion encourages employers to expand insurance offerings at the expense of wages, which in turn dulls employers’ incentives to constrain health-care spending (for more, see Glied and Striar 2016).

Perhaps more than any single feature of the ACA, the Cadillac tax held the most promise for slowing spending growth over time. But large employers and unions hated it (Goodnough 2019). Although the nickname evokes a tax only on the richest of the rich, in fact the tax would have affected one-fifth of employers in 2022 and more than one-third by 2030. That’s because the thresholds at which the tax was imposed would grow with general inflation—much slower, typically, than the growth of health insurance premiums (Rae, Claxton, and Levitt 2019). In December 2015, Congress delayed the law for two years and did so again in February 2018.12 In July 2019, a Democratic-controlled House of Representatives voted to repeal the Cadillac tax, leading many observers to doubt that it will ever take effect (Goodnough 2019).

A similar dynamic has played out with two other taxes. Starting in 2013, the ACA imposed an excise tax on the sale of any medical device (Kramer and Kesselheim 2013). Congress, however, adopted a moratorium on its collection for 2015 and 2016 and adopted another two-year moratorium in 2018.13 The collection of an ACA-imposed annual tax on health insurers was also suspended for two separate one-year periods.14 And, as of this writing, Congress appears poised to repeal both taxes—along with the Cadillac tax—as part of a 2019 budget deal (Sullivan 2019). The legislature has been similarly irresolute when it comes to the ACA’s cuts to Medicaid’s disproportionate share payments, ultimately delaying most of them through 2025.15

The Independent Payment Advisory Board (IPAB) was another casualty of interest-group pressure. The IPAB was originally supposed to be a board of fifteen Senate-confirmed appointees. When Medicare cost growth exceeded certain targets, the board would recommend cuts to bring Medicare spending into line. Unless the secretary of HHS offered an alternative slate of cuts, or Congress intervened, those cuts would automatically take effect. Though the Obama administration never nominated anyone to serve on IPAB, the HHS secretary was authorized to wield the board’s powers in their absence.

In the ACA’s early years, IPAB authorities were not triggered because of an unexpected slowdown in per capita Medicare spending growth—a slowdown that may or may not have been due to the ACA (Chandra, Holmes, and Skinner 2013). But because the Medicare targets looked as if they might be exceeded in 2017 or 2018, IPAB came under intense fire from the hospital, physician, and pharmaceutical lobbies (McDonough 2017; Oberlander and Spivack 2018). At their behest, and without much fanfare, Congress repealed the IPAB in a 2018 budget bill.16

“Free choice vouchers,” championed by Senator Ron Wyden, were also a casualty of interest-group lobbying. These vouchers would have allowed employees whose employer-sponsored health coverage cost more than 8 percent of their income to secure a voucher from their employers to buy coverage on the exchange. Among other things, free choice vouchers would have solved the so-called family glitch, which arises when family coverage for an employee is unaffordable, but family members are still ineligible for premium subsidies. Subject to lobbying from business organizations who claimed that the vouchers would destabilize employer risk pools, Congress repealed the program in 2011).17

All of these changes notwithstanding, most of the tax increases and spending cuts included in the ACA are still in place. Cuts to Medicare Advantage plans and the adjustment to the annual increase in Medicare hospital reimbursement remain intact. So too are the ACA’s new taxes on the payrolls and investment income of high earners, as well as a sizable tax on drug manufacturers. Powerful groups often get their way in Washington, but not always.

Failure to Thrive

Some parts of the ACA have never been implemented, were implemented years later than anticipated, or simply failed to live up to expectations—not necessarily because they were politically controversial, though some were, but because they were starved for funds, were hard to implement, or were not given high priority.

Consider, for example, the Prevention and Public Health Fund. The ACA appropriated almost $19 billion for this fund between 2010 and 2022 and an additional $2 billion per year after that. Beginning in 2012, however, Congress began chipping away at these funds, redirecting them to other uses or cutting them outright (Haberkorn 2012). In each of fiscal years 2015 through 2019, the fund’s actual appropriations have been less than half the $2 billion originally envisaged by the law (Lister 2017). Numerous other new grant programs authorized by the ACA have not received any appropriations (Redhead et al. 2017).

Also defunct is a provision to foster the sale of health insurance across state lines. Section 1333 of Title I instructs HHS, by “not later than July 1, 2013,” to issue rules allowing for two or more states to enter into “health care choice compacts.” These compacts would allow a single health plan to be sold in all of the agreeing states. But HHS has not issued or even proposed the required rules, partly because no state has passed a law authorizing interstate compacts and partly because insurers have expressed little interest in offering such plans. In March 2019, keen to explore the possibility, the Trump administration released a “request for information” about how it could use 1333 to facilitate such sales (CMS 2019, 8657). For now, however, Section 1333 is a dead letter.

A similar provision, Section 1334, orders the Office of Personnel Management (OPM) to contract with health insurers to offer at least two “multi-State qualified health plans through each Exchange in each State” by 2017. The idea was that federal employees receive high-quality coverage through OPM, and that consumers on the exchanges should have similar options. OPM did issue rules to implement the provision (HHS 2011b, 53904), and for a few years worked with Blue Cross to offer multistate plans in about two-thirds of the states. Consumers did not flock to the plans, however, nor did the plans much appeal to insurers, which had to design multistate provider networks and secure approval from each state in which they operated, plus OPM. By 2017, only one OPM contract remained in effect—with Arkansas Blue Cross—and the Trump administration announced in April 2019 that it would stop administering the multistate program altogether (Baker 2019).

Title VII of the ACA was largely the Biologic Price Competition and Innovation Act (BPCI), an effort to create more competition for biologic drugs by creating a streamlined mechanism for approving follow-on products. But BPCI has not lived up to expectations. In general, the generic drug industry works as well as it does because small-molecule compounds are easy to copy and cheap to manufacture. Biologics, in contrast, are large-molecule, protein-based drugs, and they are exquisitely difficult to replicate. By one estimate, developing a “biosimilar” costs somewhere between $100 million and $250 million (Blackstone and Joseph 2013). Further, a biosimilar will not be biologically identical to the brand-name drug; for approval, it only needs to be “highly similar.” The lack of perfect substitutability may limit clinical use of biosimilars, reducing the incentives to invest in their development.

To date, the FDA has approved only eighteen biosimilar applications, ten of which have not been marketed. Even where biosimilars are on the market, “competition has been thin and price reductions modest” (Atteberry et al. 2019). The slow pace of approvals may be an intrinsic feature of a market plagued by high fixed costs and imperfect substitutability. Some research, however, indicates that European countries offer a more hospitable environment for biosimilars, perhaps because centralized buyers can credibly play competing drug manufacturers against one another (Morton, Stern, and Stern 2018). Whatever the case may be, the ACA’s drafters did not attend to the full range of challenges associated with biosimilars in the United States.

Other parts of the ACA have taken many years to implement. Take the rule requiring chain restaurants to include calorie counts in their menus and menu boards. Subject to furious lobbying by the food industry, the FDA took four years to finalize its calorie-count rule, its original effective date set for December 1, 2015 (HHS 2014, 71156). But it soon extended that effective date by a year (HHS 2015, 39675). Shortly after, Congress prohibited the FDA from implementing or enforcing the rule until one year after issuing new guidance about it.18 When the FDA issued that guidance in May 2016, the new effective date became May 2017 (HHS 2016b, 96364). Four days before the new effective date, however, the Trump administration’s FDA announced another delay (HHS 2017, 20825). Only under litigation pressure did the rule finally go into effect in May 2018, more than eight years after the ACA’s adoption (Gottlieb 2017).

The Obama administration also moved slowly in implementing Section 1557 of the ACA, which prohibits discrimination in “any health program or activity” that receives federal funds on the grounds of race, color, national origin, sex, age, or disability (for an overview of health equity provisions, see Grogan 2017; for background on the legal framework extended by Section 1557, see Rosenbaum and Schmucker 2017). It took six years for HHS to release a rule that, among other things, clarified that discrimination on the basis of sex included discrimination on the basis of gender identity and pregnancy status (HHS 2016a, 31376). Soon after, however, a Texas judge—the same judge who declared the entire ACA invalid—entered a nationwide injunction against those aspects of the rule. On taking office, the Trump administration said it would revise the rule. Not until May 2019, however, did it release a proposal (HHS 2019, 27846), and no rule has been finalized as of this writing.

One last example. As a condition of taking advantage of the tax exclusion for employer-sponsored health coverage, the ACA prohibits firms from discriminating in favor of highly compensated employees.19 Previously, that prohibition applied only to firms that self-insured, not those that purchased commercial insurance. In 2011, however, the Internal Revenue Service (IRS) decided that the ACA’s new prohibition would not take effect until the agency issues rules to implement it (IRS Notice 2011–1). The IRS has yet to do so.

Executive-Branch Sabotage

The 2016 election ushered in a new era for the ACA, one in which the Trump administration has sought to undermine the law. President Trump is not subtle about this. On his first day in office, he issued an executive order instructing his agencies “to waive, defer, grant exemptions from, or delay the implementation of any provision or requirement of the Act that would impose a fiscal burden” (White House 2017). Even after congressional Republicans failed to repeal the law, Trump claimed that “we are getting rid of Obamacare” (Rappaport 2018).

But presidents cannot rewrite statutes and, with one big exception, the ACA remains firmly in place. That exception, of course, is the individual mandate. In the Tax Cuts and Jobs Act, Congress, with the Trump administration’s full-throated support, eliminated the mandate by zeroing out the penalty for going without insurance.20 As a result, CBO estimates that about four million fewer people will be uninsured in 2019 than had the individual mandate remained in place, and thirteen million fewer in 2027. Prices for individual insurance are expected to rise 10 percent faster each year relative to the baseline (CBO 2017).

At the same time, eliminating the mandate spurred the Texas v. United States lawsuit. Although it was the nominal defendant, the Trump administration announced that it would not mount a defense of the mandate’s constitutionality—a decision that broke with the Justice Department’s long-standing, bipartisan tradition of defending federal laws if any reasonable argument can be made in their defense. Initially, the Trump administration took the view that the proper remedy for the mandate’s unconstitutionality was the invalidation of the ACA’s rules about guaranteed issue and community rating—in effect, the protections for people with preexisting conditions. In March 2019, however, the administration changed its view and announced that it now agreed with the Texas judge that the entire ACA had to fall. Reporting confirms that the legal maneuvers were politically motivated: White House officials apparently believed that “taking a bold stance would force Congress into repealing and replacing the law” (Johnson and Everett 2019).

The refusal to defend the ACA is perhaps the clearest example of Trump administration sabotage. It is not the only one, however. Of greatest significance, HHS has approved waivers allowing nine states to impose work requirements on their Medicaid expansion populations, with nine additional waivers still pending. The agency claims that the waivers advance Medicaid’s purposes because they enable states to test whether work incentives conduce to enrollees’ health. HHS, however, granted waivers to states that did not supply evaluation protocols, suggesting that work requirements are not meant to test anything (Levey 2019). More important, little evidence indicates that work requirements in other programs effectively spur beneficiaries to work (Falk, McCarty, and Aussenberg 2014), and there is no good reason to think that they will function better in Medicaid. Most beneficiaries already work (60 percent) and, of those who do not, about 80 percent are disabled, ill, caring for family members, or in school (Musumeci, Garfield, and Rudowitz 2018).

Work requirements, however, are very good at pruning the Medicaid rolls. Many beneficiaries—even those who work the requisite hours—struggle to cope with the burden of documenting their work history. In Arkansas, for example, only 12 percent of people subject to the work requirements reported at least eighty hours of qualifying activities; as a result, more than eighteen thousand lost coverage in the program’s first nine months (Rudowitz, Musumeci, and Hall 2019). Work requirements are thus best understood as an attempt to undo the ACA’s transformation of Medicaid—to make it a program that, as before, is open only to the “deserving poor.” For that reason, the courts have pushed back. In declaring three of those waivers invalid, a judge in Washington, D.C., held that HHS could not exercise its waivers authority “to refashion the program Congress designed in any way they choose.” As of this writing, the case is on appeal to the U.S. Court of Appeals for the D.C. Circuit.

The Trump administration has also issued two rules that attempt to exploit loopholes in the ACA. The first involves its redefinition of the phrase “short-term, limited duration insurance.” Originally meant to cover temporary breaks in coverage, short-term insurance is exempt from most ACA rules, including those that prohibit discrimination against the sick and mandate the coverage of essential health benefits. The Trump administration, however, has issued a final rule defining it to include plans that offer coverage for up to 364 days in a year and are renewable for up to three years (HHS 2018b, 38212). The professed goal is to “promote consumer choice” and “enhance affordability of coverage for individual consumers.” In a sense, the rule will achieve that goal: short-term insurance will be cheaper than ACA-compliant coverage for the young and healthy.

It achieves that goal only, however, by undermining the ACA’s effort to spread health risk across a broad population. Siphoning young and healthy people from the exchanges will divide the common risk pool, potentially destabilizing the insurance markets for the sick and elderly who have no choice but to buy insurance on the exchanges. The new rule may also be illegal. Though HHS has some interpretive discretion, it is difficult to see how plans that last 99.7 percent as long as conventional insurance are short term in any sense of the phrase. So far, however, a lawsuit pressing that argument has not met with success: in July 2019, a district court in Washington, D.C., held that the rule was valid. That case has also been appealed.

The second rule is of a piece with the first. Under federal law, small businesses can band together to form association health plans for their employees. Because those plans are treated as employer-sponsored coverage, they are exempt from the ACA’s underwriting restrictions, though they must still cover the essential health benefits. Originally, only those businesses in the same line of work, or those that had some other common interest independent of the provision of insurance, could band together. The Trump administration, however, adopted a rule that greatly expanded the ability of employers—and even individuals running their own businesses—to form association health plans (DOL 2018, 28912). As with the rule governing short-term insurance, the goal is to enable healthier-than-average employees and individuals to exit the shared risk pool, potentially destabilizing it. Again, as with the short-term rule, it is probably unlawful. In March 2019, a judge in Washington, D.C., held that the rule “was intended and designed to end run the requirements of the ACA, but it does so only by ignoring the language and purpose of both ERISA and the ACA.” An appeal is in the works.

Beyond these two rules, the Trump administration has taken other steps to undermine the exchanges. The decision to cut off the cost-sharing subsidies was driven not by a cool evaluation of the legal merits of the claim that the requisite money had not been appropriated. It was a political decision, made on the eve of open enrollment, in a manner calculated to sow confusion (Bagley 2017). The Trump administration has cut funding in half for the ACA’s “navigators,” who are meant to help people enroll for coverage (Pollitz, Tolbert, and Diaz 2019), and nearly all (90 percent) used to advertise for open enrollment (Kliff 2017). It also threatened to halt $5.2 billion in risk adjustment transfers between exchange insurers, before backing down in the face of insurer outrage (Bagley 2018; HHS 2018a, 36456).

Do all of these actions, taken together, constitute a deliberate campaign to sabotage an act of Congress—one that oversteps the administration’s authority? To be sure, the administration resists that description: in any particular case, it claims to be exercising discretion within the four corners of the ACA, not working to impair it (Council of Economic Advisors 2019). The record, however, suggests otherwise. Some of the Trump administration’s implementation decisions have been declared unlawful; others may be defensible in a narrow legal sense, but nonetheless deliberately aim to enfeeble the law in an effort to pave the way for its repeal (Bagley and Gluck 2018). For now, the administration’s actions have done limited damage to the ACA. This is partly because some of the administration’s moves have been snarled in the courts, and partly because some of them—such as the measures described that may destabilize the exchange risk pool—are likely to cause more damage over time. Some states have also acted to offset the potentially de-stabilizing effects of the Trump administration’s actions on insurance markets by using waivers to continue reinsurance programs beyond their original three-year time frame (Blumenthal et al. 2018). The ACA’s future is uncertain, however, and depends a great deal on the coming election.

LIMITATIONS

Our assessment of the ACA’s progress is far from definitive. One limitation is the relatively subjective nature of our coding scheme. Although we tried to provide as objective an assessment as possible of the implementation progress of each provision, it is certainly possible to take issue with some of our decisions. Recognizing this limitation, we have been as transparent as possible by making all of our coding, and the sources on which it is based, available as supplementary materials.21

Our thematic discussion is limited not only by a similar inevitable subjectivity but also by the inherent difficulty of assigning a single “cause of death” to provisions that may in fact have died from multiple complex causes. For example, the CLASS Act as structured was born to fail, but only because of partisan and interest-group pressure to structure the act in a certain way (Gleckman 2012). Similarly, analysis of the politics of the Prevention and Public Health Fund suggest that partisan and interest-group pressure partly explains why it has not thrived (Fraser 2019). But politics is not always the root cause of a provision’s failure, even if it played a role: both the demise of the co-ops and the lackluster effort to promote biosimilars seem victims of underlying market forces rather than political pressures.

We also believe it is still too early to render a final determination as to which parts of the law have thrived and which will fail. Many other shoes are still to drop and, in the grand scheme of things, ten years may not be long enough for a major reform such as the ACA to take its final shape, let alone for scholars to discern its broader significance in reshaping the policy and political landscape.22 Our assessment is unavoidably an interim one.

CONCLUSION

What, then, is left of the Affordable Care Act after ten years? Most of it. Of greatest moment, the ACA has successfully expanded the Medicaid program in more than two-thirds of the states, extending coverage to millions of individuals at or near the poverty level. Not one of those states has walked away from the expansion; indeed, a recent string of successful ballot initiatives in deep-red states—Idaho, Nebraska, Maine, and Utah—suggests that Medicaid is more popular with the American public than commonly appreciated.

On the individual market, the ACA still protects people with preexisting conditions; it still requires every insurer to cover the full range of essential health benefits; and it still subsidizes, through premium subsidies, the purchase of individual coverage. The exchanges have remained stable, even as premiums have surged in response to Trump administration sabotage. Reforms that apply to people who get health insurance through their jobs have similarly endured. Employers cannot discriminate on the basis of health status, they cannot impose lifetime or annual caps, and they must allow children to stay on their parents’ plans until they turn twenty-six.

Nor have the law’s revenue-raising and budget-cutting provisions been wiped away. Most of the ACA’s taxes are still in place. The ACA’s multibillion dollar Medicare cuts have also been allowed to take effect, though the repeal of the IPAB and the repeated delays of cuts to disproportionate share hospital payments suggest that Congress remains imperfectly committed to budget cuts. Significantly, the relatively modest changes that Congress has made to the ACA’s financing mechanisms have resulted from low-profile and often bipartisan legislative action, not as a consequence of the partisan war over health reform.

For all its resilience, however, the ACA is not the same law it was on the day it was enacted. Three major changes stand out. First, the Supreme Court’s decision in NFIB has allowed fourteen states to decline to expand their Medicaid programs, depriving millions of people of coverage the ACA originally offered. Second, Congress has reduced the penalty associated with the individual mandate to zero, hampering to some extent the law’s ability to spread risk across a broad population. Third, the Trump administration terminated the cost-sharing payments, forcing insurers to adjust their plan offerings and altering how the ACA subsidizes private coverage for low-income people.

None of these is a minor tweak; all are significant and substantial deviations from how the ACA was supposed to work. Nor is the ACA out of the woods. Texas v. United States represents an existential threat to the law, even if the lawsuit is ultimately unlikely to succeed. And though Medicaid work requirements and the rule governing short-term, limited duration plans have faced legal challenges, the courts may yet approve them. If they do, they could undermine the ACA in states that remain opposed to the law. The ultimate success or failure of Trump-era sabotage may thus depend on the outcome of those cases—and on the 2020 presidential election.

For now, however, the ACA has proven resilient. It has been bruised; it has been battered; but it is still here. Its durability is all the more remarkable because the Obama administration could not turn to a Republican-controlled Congress to address unexpected implementation challenges. That’s not generally the case with complex legislation. In 1965, for example, a Democratic-controlled Congress passed the law creating Medicare and Medicaid over staunch Republican opposition,23 but the subsequent implementation of Medicare was quite swift and relatively smooth (Gluck and Reno 2001). By 1972, Democrats and Republicans were cooperating to expand Medicare to the disabled, to constrain higher-than-expected spending, and to address administrative difficulties.24

The ACA has not been so fortunate. Even ten years in, it remains the object of intense partisan conflict. The law’s rough edges have therefore never been smoothed out. The family glitch, for example, is unpopular across the political spectrum, but has not been addressed. Congress could have appropriated the necessary money to make the promised cost-sharing payments but has chosen not to do so. All of these changes and more might have come to pass in a less dysfunctional political system.

Instead, the basic features of the ACA have been locked into place since 2010. That situation is likely to persist. The collapse of the 2017 repeal effort suggests that Republicans will never muster the political will to undo the law, much less to pass some yet-to-be-determined alternative. But it seems equally likely that Democrats (who are themselves divided) will not have the political muscle to replace the law with an ambitious version of Medicare for All. From where we stand today, it looks like the ACA—older now, but not much worse for wear—will shape the health-care system for many years to come.

Appendix

Timeline of Key ACA Events

FOOTNOTES

↵1. Table A1 presents a timeline of key events both before and after the law’s passage.

↵2. Our analysis categorizes provisions in Title X of PPACA (the Manager’s Amendment) and ACA-relevant provisions of the Health Care and Education Reconciliation Act of 2010 (HCERA) with the relevant provisions in Title I through IX of PPACA. For example, we group the tax on tanning salons (which was in Title X) and the change in the tax treatment of cellulosic biofuels (which was in HCERA) with the other revenue provisions in Title IX.

↵3. Our ratings and the sources on which we relied to evaluate each provision are available online as supplementary material (see https://www.rsfjournal.org/content/6/2/42/tab-supplemental).

↵4. Evaluating the Medicaid expansion raises the question of whether we are asking “was the provision implemented according to the law,” taking into account that the law was changed as a result of the subsequent Supreme Court ruling; or “was the provision implemented as it was written?” Our goal is to answer the latter question, so in the case of Medicaid expansion, we conclude that it was only partially implemented.

↵5. National Federation of Independent Business v. Sebelius, 567 U.S. 519 (2012).

↵6. King v. Burwell, 576 U.S. 988 (2014).

↵7. Burwell v. Hobby Lobby, 573 U.S. 682 (2014).

↵8. Comprehensive 1099 Taxpayer Protection and Repayment of Exchange Subsidy Overpayments Act of 2011, Pub. L. 112–9, 125 Stat. 361 (2011).

↵9. Comprehensive 1099 Taxpayer Protection and Repayment of Exchange Subsidy Overpayments Act, H.R. 112–16 (February 22, 2011), 6.

↵10. American Taxpayer Relief Act of 2012, Pub. L. 112–240, 126 Stat. 2313 (2013).

↵11. Consolidated and Further Continuing Appropriations Act, 2015, Pub. L. 113–235, 128 Stat. 2130 (2014).

↵12. Consolidated Appropriations Act of 2016, Pub. L. 114–113, 129 Stat. 2242 (2014), div. Q, §174; Suspension of Certain Health-Related Taxes, Pub. L. 115–120, 132 Stat. 28 (2018), div. D, §4002.

↵13. Suspension of Certain Health-Related Taxes, §4001.

↵14. Consolidated Appropriations Act of 2016, title II, §201; Suspension of Certain Health-Related Taxes, §4003.

↵15. American Taxpayer Relief Act of 2012, Pub. L. 112–240; Bipartisan Budget Act of 2013, Pub. L. 113–67; Protecting Access to Medicare Act of 2014, Pub. L. 113–93, 128 Stat. 1040 (2014); Medicare Access and CHIP Reauthorization Act of 2015, Pub. L. 114–10, 129 Stat. 87 (2015), 42 USC 1305; Bipartisan Budget Act of 2018, Pub. L. 115–123, 132 Stat. 64 (2018).

↵16. Bipartisan Budget Act of 2018, div. E, §52001.

↵17. Department of Defense and Full-Year Continuing Appropriations Act, 2011, Pub. L. 112–10, 125 Stat. 38 (2011), §1858.

↵18. Consolidated Appropriations Act of 2016, §747.

↵19. 42 U.S. Code §300-16: Prohibition on discrimination in favor of highly compensated individuals, Pub. L. 111–148, 124 Stat. 135 (2011).

↵20. Tax Cuts and Jobs Act of 2017, Pub. L. 115–97, 31 Stat. 2054 (2018), §11081.

↵21. Available at https://www.rsfjournal.org/content/6/2/42/tab-supplemental.

↵22. Medicaid was not implemented in all fifty states until 1982, seventeen years after it was enacted. Jonathan Oberlander’s definitive study of the politics of Medicare was published nearly forty years afterward (2003). These things take time.

↵23. Social Security Amendments of 1965, Pub. L. 89–97, 79 Stat. 286 (1965)

↵24. Adjustment of the Contribution and Benefit Base, Pub. L. 92–336, 86 Stat. 406 (1972).

- © 2020 Russell Sage Foundation. Levy, Helen, Andrew Ying, and Nicholas Bagley. 2020. “What’s Left of the Affordable Care Act? A Progress Report.” RSF: The Russell Sage Foundation Journal of the Social Sciences 6(2): 42–66. DOI: 10.7758/RSF.2020.6.2.02. Direct correspondence to: Helen Levy at hlevy{at}umich.edu, Institute for Social Research, University of Michigan, 426 Thompson St., Ann Arbor, MI 48106; Andrew Ying at aying1{at}jhmi.edu, School of Medicine, Johns Hopkins University, 733 N. Broadway, Baltimore, MD 21205; and Nicholas Bagley at nbagley{at}umich.edu, University of Michigan Law School, 625 South State St., Ann Arbor, MI 48109.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.