Abstract

The subprime mortgage crisis was a devastating financial shock for many homeowners. This research uses a probabilistic matching strategy to link foreclosure records with birth certificate records from 2006 to 2010 in California to identify birth parents who experienced a foreclosure. Among mothers who did, those issued a loan during the peak of subprime lending from 2005 to 2007 were more Hispanic and socioeconomically disadvantaged than mothers with loans originating before 2005. We use a mother fixed-effects analyses of ever-foreclosed mothers issued a loan during 2006 and 2007 and find that infants in gestation during or after the foreclosure had a lower birth weight for gestational age than those born earlier, suggesting that the foreclosure crisis was a plausible contributor to disparities in initial health endowments.

The subprime mortgage crisis was characterized by an unprecedented rise in mortgage delinquencies and foreclosures (Duca 2013). At the national peak month of the crisis in January of 2011, foreclosures numbered 1.56 million (Core-Logic 2017). Between 2007 and 2010, homeownership rates fell most dramatically for minorities and households with incomes of $20,000 or less (CoreLogic 2017). In response to the crisis and to protect Americans from predatory lending practices in the future, policies such as Dodd-Frank Wall Street Reform were implemented, establishing regulatory entities, including the Consumer Financial Protection Bureau. Yet, in June 2017, the House passed the Financial CHOICE Act, which is designed to repeal certain provisions of Dodd-Frank and loosen regulatory policies.1 Given the contemporaneous nature of this policy and the ongoing debate about financial regulatory policies, the period in our recent history prior to the financial regulatory reform—the subprime mortgage crisis—can help us to predict how a less regulated financial environment might affect society in the future.

The economic causes and consequences of the subprime crisis have been well studied (Been et al. 2011; Financial Crisis Inquiry Commission 2011; Foote, Gerardi, and Willen 2012). The financial regulatory environment and cascade of events influenced a set of complex adaptive responses which included not only banks and government entities—but also communities, households, and individuals. Less is known about the unintended (spillover) effects of the subprime crisis.

Some evidence indicates that the foreclosure crisis contributed to increased racial segregation (Hall, Crowder, and Spring 2015a; Rugh and Massey 2010) and neighborhood crime (Ellen, Lacoe, and Sharygin 2013), and had negative effects on education (Bradbury, Burke, and Triest 2014). More recently, scholars have explored the effect of the foreclosure crisis on health (Downing 2016; Downing et al. 2017, 2016; Currie and Tekin 2015). Evidence from a small set of studies suggests that homeowners who experienced a foreclosure had more anxiety and depression, whereas population-level studies—which measure, for example, the relationship between health and the foreclosure rate in a given census tract—showed an increase in violent behavior and urgent unscheduled health-care visits (Downing 2016; Currie and Tekin 2015).

Research on the foreclosure crisis and health, though distinct from other work on the health effects of financial shocks, shares an underlying aim of quantifying unintentional effects of a phenomenon that plausibly served as an unexpected population-level stressor. A vast body of work has been undertaken on the effects of a coincident financial shock—the Great Recession—on health and health behaviors (Margerison-Zilko et al. 2016; Catalano et al. 2011; Margerison-Zilko, Li, and Luo 2017). Although the evidence does not converge across all areas of health, studies on the effect of economic shocks on a highly sensitive period of development—pregnancy—have shown particularly compelling evidence that fetal exposure to unexpected job loss reduced birth weight for gestational age and increased male fetal death (Margerison-Zilko et al. 2011; Catalano and Bruckner 2005). Although both the foreclosure crisis and the Great Recession serve as population-level stressors, we know of no research that examines whether the sensitive period of pregnancy responded to the foreclosure crisis.

MERIT OF LINKING ADMINISTRATIVE DATA

Use of administrative data to answer policy-relevant questions has become increasingly important (Harris-Kojetin and Groves 2017). Despite technical, legal, and perceptual challenges associated with its use, administrative data enable researchers to answer questions that were previously unanswerable (Penner and Dodge 2019). One type of administrative data, vital statistics, has been collected since the early 1900s, although use of birth certificates for population-level perinatal research was not feasible until the 1990s, when some states began to keep these in digital format (Buescher et al. 1993). The advantages of these data, such as their comprehensiveness (all births in a state), large sample sizes, and wealth of birth-related and socioeconomic variables, have made vital records increasingly attractive for research in the last decade (Schoendorf and Branum 2006). Although birth certificate data were collected for administrative rather than research purposes, their reuse for research has been beneficial because it allows a minimum set of questions to be answered without placing additional burdens of further data collection on vulnerable populations, pregnant women, and infants.

Linkage of birth certificate data with other sources of administrative data is the next frontier of perinatal epidemiology. The United States lags behind other countries in linking data for perinatal health (Delnord et al. 2016). For example, Denmark maintains a civil registration system that has allowed researchers to link all administrative data with birth certificate data by unique identifiers (Pedersen 2011). Although several studies in the United States have demonstrated feasibility of linking birth certificate records with hospital records (Barfield et al. 2008; Herrchen, Gould, and Nesbitt 1997; Hall et al. 2014), far fewer have linked birth certificate records with other sources of administrative data at the individual level (Autor et al. 2016; Coulton et al. 2016; Putnam-Hornstein et al. 2013).

This article fills an important gap by demonstrating feasibility of linking birth certificates with another source of public administrative data, foreclosure deed records. In the absence of unique identifiers, we use a probabilistic matching technique (Gliklich, Dreyer, and Leavy 2014). The linkage of the data allows us to answer two policy-relevant questions unanswerable without this approach. We describe each of these questions and how we leveraged this unique source of linked data to address key content and methodological gaps in the literature.

What are the demographics of families affected by the foreclosure crisis?

Family formation and homeownership are important goals of many Americans, and the transition to either tenet can be delayed or disrupted by changes in lending policies. The demographics of who was affected by the foreclosure crisis is still not yet well understood (Reid et al. 2017). The majority of studies have focused on specific cities or types of loans, or showed the impact on neighborhoods of varying demographics (Hall, Crowder, and Spring 2015a, 2015b; Bocian et al. 2011). Even one of the most comprehensive studies on demographics of lending during the subprime crisis was unable to include the complete universe of lenders because of data limitations (Reid et al. 2017). The Home Mortgage Disclosure Act data are considered one of the most comprehensive sources of mortgage and demographic data, yet do not cover all home loans nationwide.

Research on California finds that African American and Hispanic borrowers were more likely to have a subprime loan and more likely to default during the crisis, even after accounting for underwriting risk factors and neighborhood characteristics (Reid and Laderman 2009). These findings are troubling because the unequal distribution of foreclosures can contribute to social stratification by widening the racial wealth gap (Reid et al. 2017). It is then critical to understand its impact on young families, who are often in the process of transitioning to homeownership.

Young families often access family wealth to transition to homeownership, yet discriminatory institutional polices have reproduced racial differences in wealth and increased barriers for Hispanic and black young families to purchase a first home (Krivo and Kaufman 2004). Subprime loans provided an opportunity for households with less wealth to purchase their first home. Hispanic and black young families are then most at risk to be affected by the subprime mortgage crisis.

This is the first study we are aware of to examine population-level characteristics of families who went through foreclosure during the crisis. Differential responses to foreclosure, for instance, may affect the sociodemographic composition of who selects into, or postpones, fertility.

How might exposure to foreclosure affect birth outcomes?

Through this data linkage, we also investigate the repercussion on fetal development of experiencing a foreclosure during pregnancy. The maternal stress response, when activated by an external stressor such as job loss or another catastrophic event, reportedly perturbs timing of parturition, fetal growth, or both processes (Hobel, Goldstein, and Barrett 2008). This study investigates whether in utero exposure to foreclosure affected gestations by examining differences in birth weight for gestational age, which is sensitive to the maternal stress response and precedes adverse health and lower human capital development over the life course.

Acute and chronic psychosocial stressors have reportedly slowed fetal growth or accelerated the timing of delivery. Stress, smoking, and low socioeconomic status over the life course have been shown to increase risk of preterm birth (delivery before thirty-seven weeks) and reduced birth weight (Lu and Halfon 2003). Although some of the consequences of these risk factors are observable at birth, others are latent and appear much later in life. Adults who showed preterm delivery or slower fetal growth had increased morbidity, lower educational attainment, and even lower labor market outcomes (Almond and Currie 2011; Strauss 2000; Currie and Moretti 2007; Hack, Klein, and Taylor 1995; Black, Devereux, and Salvanes 2007; Goldenberg et al. 2008).

Homeownership has been portrayed as the American Dream and ideologically as a political right (Flood et al. 2015). Many who defaulted on their loans during the subprime crisis experienced feelings of anxiety, stress, and personal failure (Ross and Squires 2011). Mothers who defaulted on their loan and were undergoing foreclosure may also increase maladaptive coping behaviors such as smoking and alcohol use. Any of these exposures may adversely affect fetal growth and development.

A foreclosure can lead to a loss in time, wealth, and energy of a household. Mothers who manage paperwork and the cognitive burden of the foreclosure process may inadvertently place a lower priority or less time on receiving antenatal care and engaging in health-promoting behaviors (Mullainathan and Shafir 2013; Bruckner 2008). In addition, a foreclosure can reduce wealth and the amount of resources available to purchase healthy food and pay for health care. Finally, some households who lost a home to foreclosure experienced high levels of fear, shame, and guilt, which could reduce the degree to which mothers rely on others for social support (Ross and Squires 2011). Prior studies have found strong social support to be a contributor to normal fetal growth and term birth (Feldman et al. 2000).

METHODOLOGICAL CONCERNS AND INNOVATIONS

Pregnancy responses to adverse events are typically reported only among those that end in a live birth. Research, however, finds that stressful events may also increase the likelihood of fetal mortality. Specifically, stressful experiences reduce the chances that pregnant women will deliver males (Hansen, Møller, and Olsen 1999). A decline in the human secondary sex ratio (of male to female live births) has been reported following population stressors such as man-made disasters (Bruckner, Catalano, and Ahern 2010; Fukuda et al. 1998) and economic recessions (Catalano et al. 2011; Catalano and Bruckner 2005). Therefore, mothers who have the most stressful foreclosure may experience an early spontaneous loss, such that only “hardier” births are positively selected to live birth.

Furthermore, another concern is that there might be selection into treatment (being in utero during the foreclosure process). People with loans in default may be more likely to delay fertility. We suspect that only couples who were aware that a foreclosure was imminent would be able to delay fertility. However, individual decisions to take out a mortgage, refinance, or default implicitly reflect knowledge about current and future expectations of health, fertility, and economic status. For example, individuals who are sick might lose their job or take out a lien on their house to pay for medical bills, which could lead to foreclosure. In addition, relatively healthier persons who experienced an economic setback in advance of a foreclosure may have chosen to delay fertility until prospects improve.

The issue of selection into treatment is mitigated in part when studying the effect of foreclosure on health during the height of the foreclosure crisis. A majority of foreclosures during this period were caused by the loan characteristics (that is, the subprime structure) or declines in home equity rather than individual job loss or medical bills (Palmer 2015). The increase in the default rate of subprime mortgages during the crisis accounted for more than half of all the foreclosures at its peak (Palmer 2015). The year in which the mortgage originated plays a role in the likelihood of default. Subprime mortgages originating in 2006 and 2007 were more likely to default within three years than those originating in 2003 and 2004 (Palmer 2015). Therefore, borrowers with loans originating between 2006 and 2007 were less likely to be subject to selection into treatment than those borrowing at other times because of their lack of knowledge about riskiness of the loan.

To further address the issue of selection into treatment, we compare outcomes of siblings born to the same mother. Linkage of sibling births for the entire population base of live births in a state is relatively novel in perinatal epidemiology (Kramer, Dunlop, and Hogue 2014). Increasingly, scholars have recognized that mothers experience a dynamic socioeconomic trajectory during adulthood. This dynamism calls for innovative data linkage approaches to capture information about mothers and their pregnancies over a longer life course.

Our research aims to understand how fetal exposure to a loan that results in foreclosure relates to poor birth outcomes. To address this question while minimizing the risk of selection into pregnancy during stressful times, we compare birth outcomes within mothers (that is, across siblings) who ultimately experienced a foreclosure. In addition, consistent with the notion that loans in 2006 and 2007 are a plausibly exogenous stressor, we assess whether results appear stronger among those who took out a loan during 2006 and 2007 rather than before or after this period.

METHODS

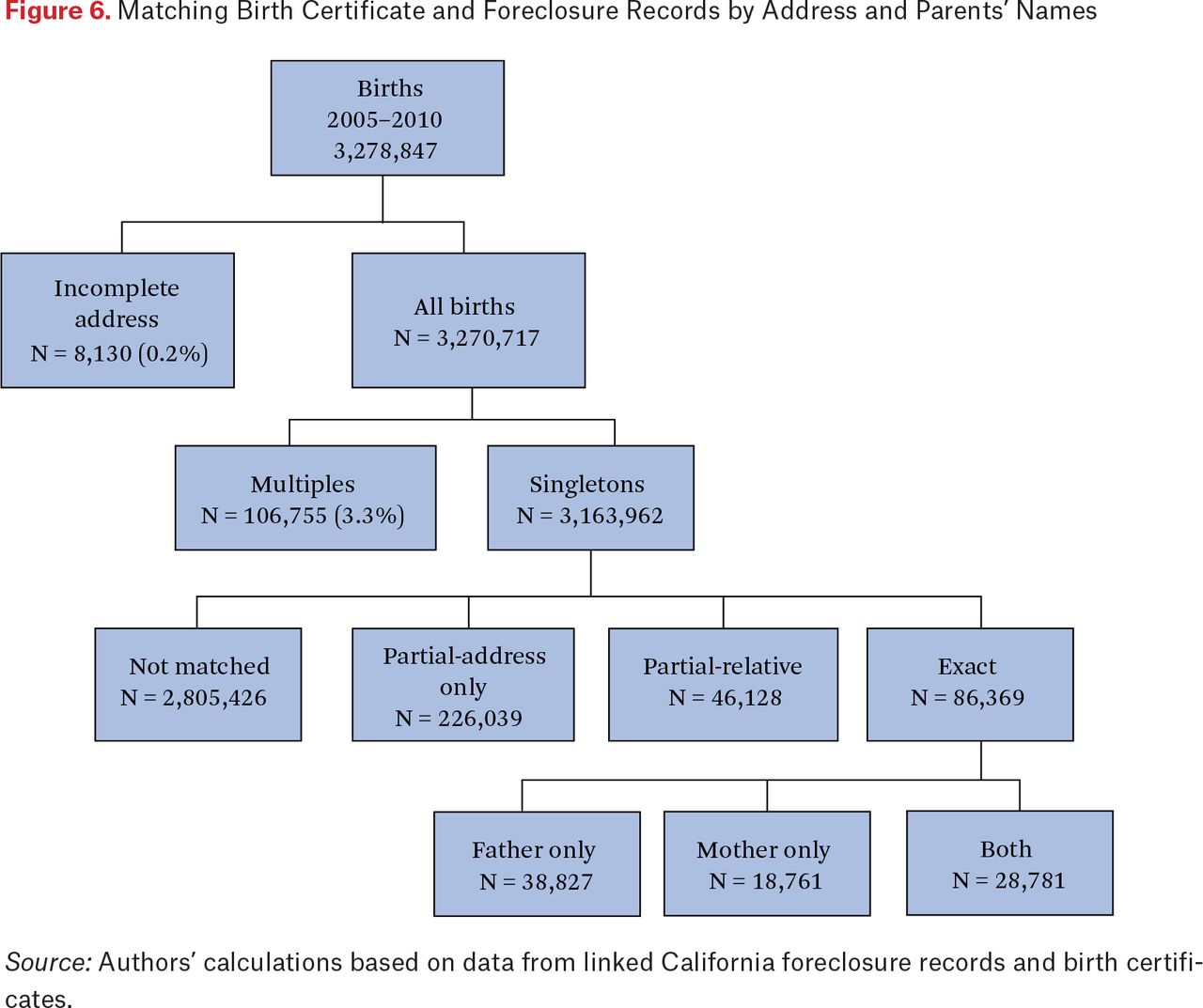

We obtained birth certificate records for all live births in California (2005 to 2010, n = 3,278,847) from the California Department of Health Services. We selected California as our study population because it was one of the hardest hit states by the foreclosure crisis (CoreLogic 2017). California also shows substantial within-state geographic variation in the foreclosure rate and yielded the highest number of live annual births of any state in the country (Martin et al. 2017). Mother’s address was geocoded using ArcGIS and a census tract was assigned to each record. Births to mothers with at least one multiple birth between 2005 and 2010 were excluded (n = 106,755) because birth outcomes for singleton and multiple births have different etiologies.

We retrieved foreclosure records on all residential properties in California that were subject to at least one completed foreclosure between 2006 and 2015 (n = 1,058,311). These records are publicly available from the clerk in each county. Because of the time cost of contacting each of the fifty-eight counties, we purchased the assembled and cleaned data of all records in California from CoreLogic. The foreclosure records were then geocoded using ArcGIS, and census tracts were assigned to each record.

Matching

To match foreclosure records to the birth file, we preprocessed all address and name data to ensure consistency in formatting across the two sources of data (Wasi and Flaaen 2015). Of these, 0.25 percent of birth records (n = 8,130) had missing addresses and thus were excluded. Given that some mothers had multiple births at the same address, we allowed for multiple matches as the father name might vary over time. Of the foreclosure data, 0.3 percent (n = 3,300) did not have an address and 2.1 percent (n = 22,143) did not list the mortgage-holder name and were therefore excluded. We reformatted the foreclosure data to include one unique address and lender for each row by collapsing multiple loans at the same property to the same borrower and retaining the earliest notice of default date and summing the loan amount and balance for each.

We used a deterministic matching technique in Stata to link foreclosure record data to the master birth certificate data by mother’s address. Because we wanted exact matches only and data were preprocessed, this method optimized speed without compromising accuracy. Next, we used a probabilistic matching technique in Stata (reclink) to link foreclosure record data to the master birth certificate data by first and last names of parents listed on the birth certificate. This technique used a bigram string comparator to assess imperfect string matches. We reviewed the output for quality of match and separated falsely matched files.

We created a variable, exact match, which was defined as matching on address and mother or father full name. Next, we reran the matching procedure with an exact match of an address and last name of mother or father using the same procedure. We created two partial match variables. First, relative match, which was defined as matching on address and mother and father last name (excluding exact matches). Second, address match, which was defined as matching on address only and not name (not exact match or relative match).

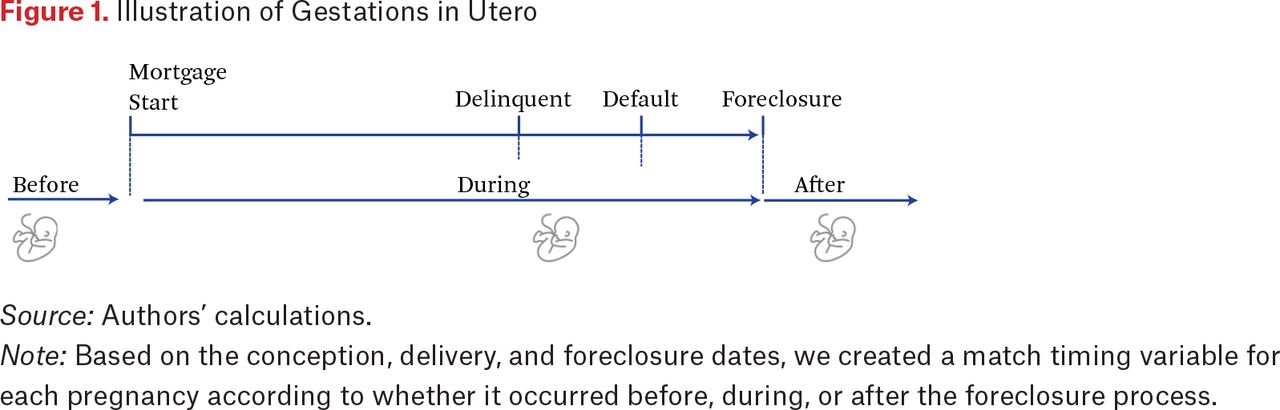

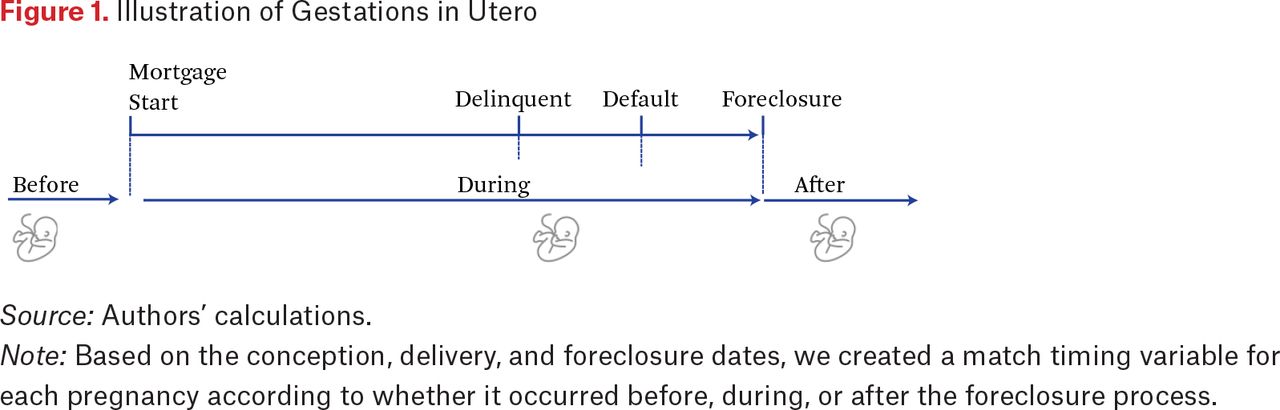

We link births for the same mother, creating a unique identifier based on her first name, last name, birthdate, and mother’s birthplace. A categorical variable, match type (0 = not matched, 1 = exact, 2 = relative, and 3 = address), and a binary variable, matched, (0 = not matched, 1 = exact, relative, or address) were developed from the above measures for each mother. Next, we created variables based on timing of the foreclosure process and gestational period. The variable, match timing, was a categorical variable (0 = not matched, 1 (before loan) = birth date < mortgage start date, 2 (during loan) = birth date > = mortgage start date & conception date < = foreclosure date, 3 (after foreclosure) = foreclosure date < conception date). For a visual explanation, see figure 1.

Illustration of Gestations in Utero

Note: Based on the conception, delivery, and foreclosure dates, we created a match timing variable for each pregnancy according to whether it occurred before, during, or after the foreclosure process.

Because we matched administrative records that likely contained legal last names (and maiden names for mothers on the birth certificates), we might have classified some mortgage-holders as address-only matches if they changed their last names or had variations in spellings of their name. Common reasons for changing one’s name include divorce or simplification. Therefore, we likely underestimated foreign-born mortgage holders and women, particularly those in unstable partnerships. In addition, our matching process relied on exact matching of addresses because a substantial number of foreclosures were condominiums or apartment buildings with multiple units. Although we preprocessed these addresses to standardize them, we likely did not match some people living in condominiums or apartment buildings if the number or letter of the unit was different or missing. Our matching process was conservative, and thus we avoided falsely matching at the cost of excluding some true matches.

Key Variables

Birth-related

Our dependent variable of interest is birth weight for gestational age percentile (BWGA). BWGA measures fetal growth and, unlike birth weight (in grams), separates being born light from being born early. Fetal growth and timing of delivery reportedly have distinct causes, and for this reason BWGA is preferred in perinatal epidemiology over the general measure of birth weight (Kramer et al. 2001; Oken et al. 2003). BWGA takes into account continuous birth weight conditional on gestational age. We calculated BWGA using the Oken method from the sex-specific birth tables after using the Alexander method to remove implausible birth weight for gestational age combinations (Oken et al. 2003; Alexander et al. 1996). We excluded all births that were missing BWGA (n = 141,099). In addition, we included sex of neonate (1 = female, 0 = male), and parity (1 = first birth, 2 = 1 or more prior births) as control variables.

Mother-related

The mother-related variables of interest include age at delivery, race-ethnicity (non-Hispanic white, non-Hispanic black, non-Hispanic Asian, Hispanic, non-Hispanic other), educational attainment, health insurance (Medicaid, private or self-pay, no insurance, other), and no father (had at least one birth with no father listed). We also used body mass index (BMI) (continuous kg/m2) and smoking status (never smoker, smoked prior to pregnancy only, smoked before and during pregnancy) for 2007 through 2010; data for 2005 and 2006 on BMI and smoking were not collected on the birth file.

Foreclosure-related

The foreclosure-related variables of interest include property address, mortgage-holder names, mortgage issue date, notice of default date, and deed transfer date (when the foreclosure was completed). We created a categorical variable for all matched births, borrower cohort, which was set to the calendar year in which the loan was originated (1 = before 2005, 2 = 2005, 3 = 2006, 4 = 2007, and 5 = after 2007).

Statistical Approach

We summarized the mean characteristics of all unique mothers (table 1) from 2005 to 2010 who had at least one birth. Mothers were separated into four groups based on the match type, which include exact, relative, address, and not matched.

Mean Characteristics of Mothers by Foreclosure Match Status

Next, we restricted our sample to exact match only (mothers who have ever experienced a foreclosure, for example). We created a descriptive table of mothers ever foreclosed with within- and between-mother standard deviations for each of our key variables (see table 2). Mother-invariant characteristics included race-ethnicity, educational attainment, borrower cohort, and borrower type. Characteristics that varied within-mother (for mothers with more than one birth during the test period) included BWGA, infant sex, parity, health insurance, and mother’s age. In addition, we summarized the mean characteristics of all unique mothers ever foreclosed by loan cohort (table 3).

Descriptive Statistics of Mothers Ever Foreclosed, 2005–2010

Mean Characteristics of Mothers with a Foreclosure by Loan Cohort

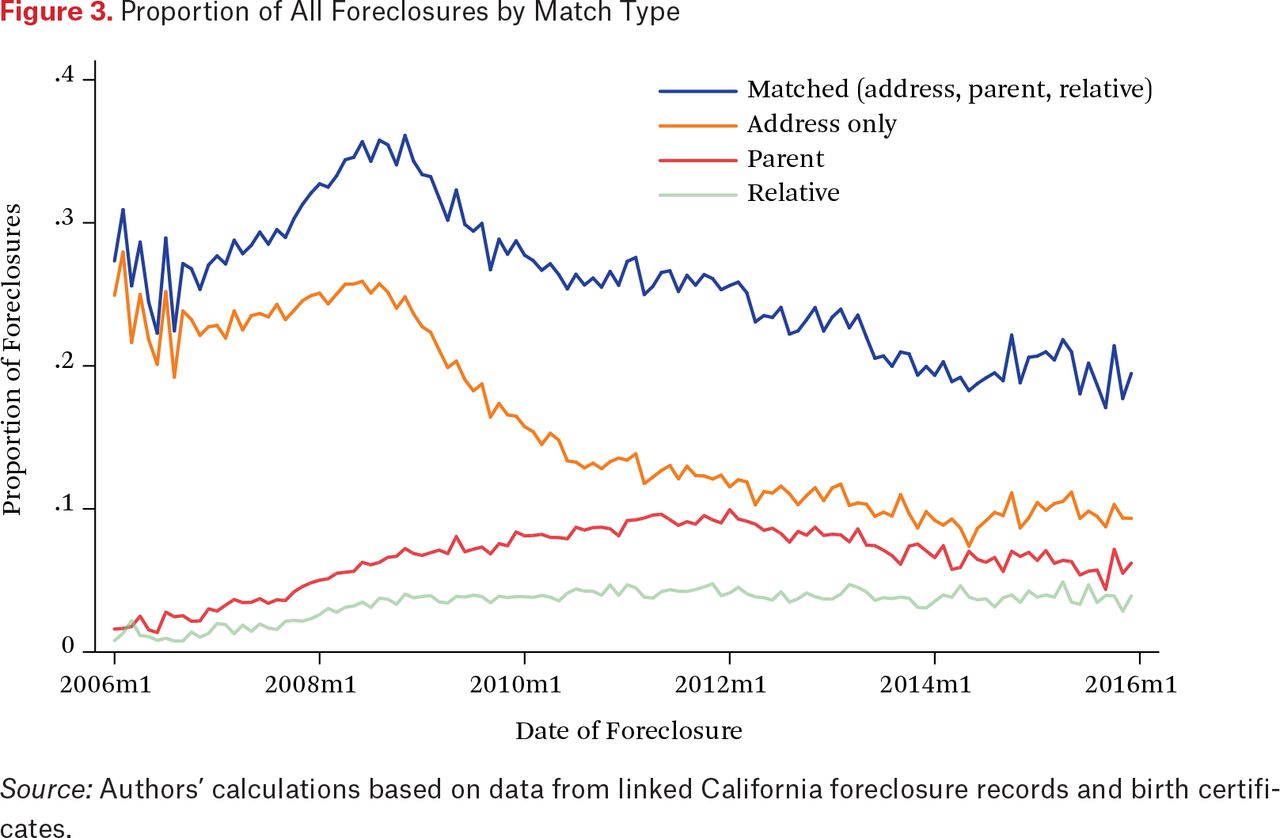

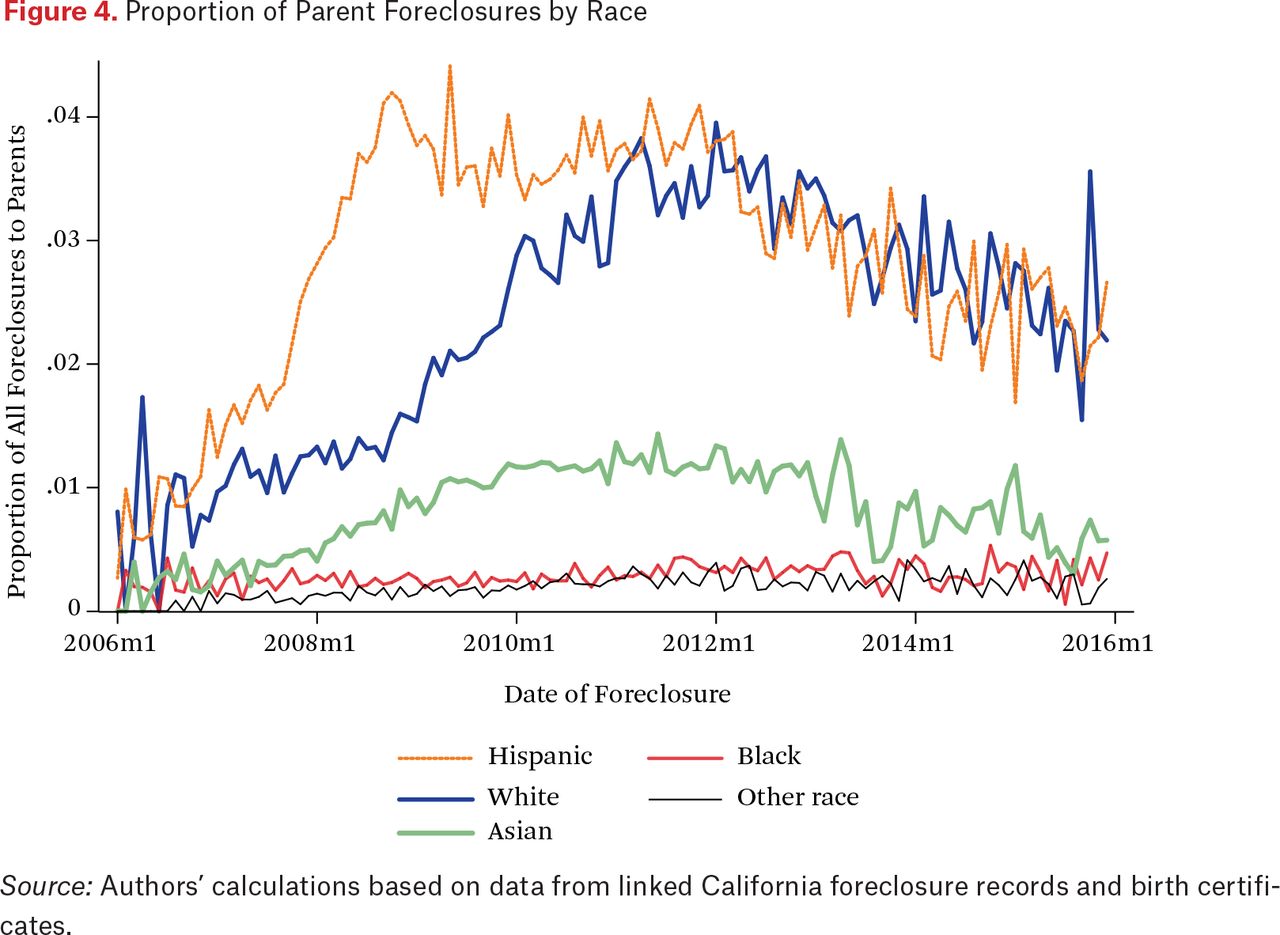

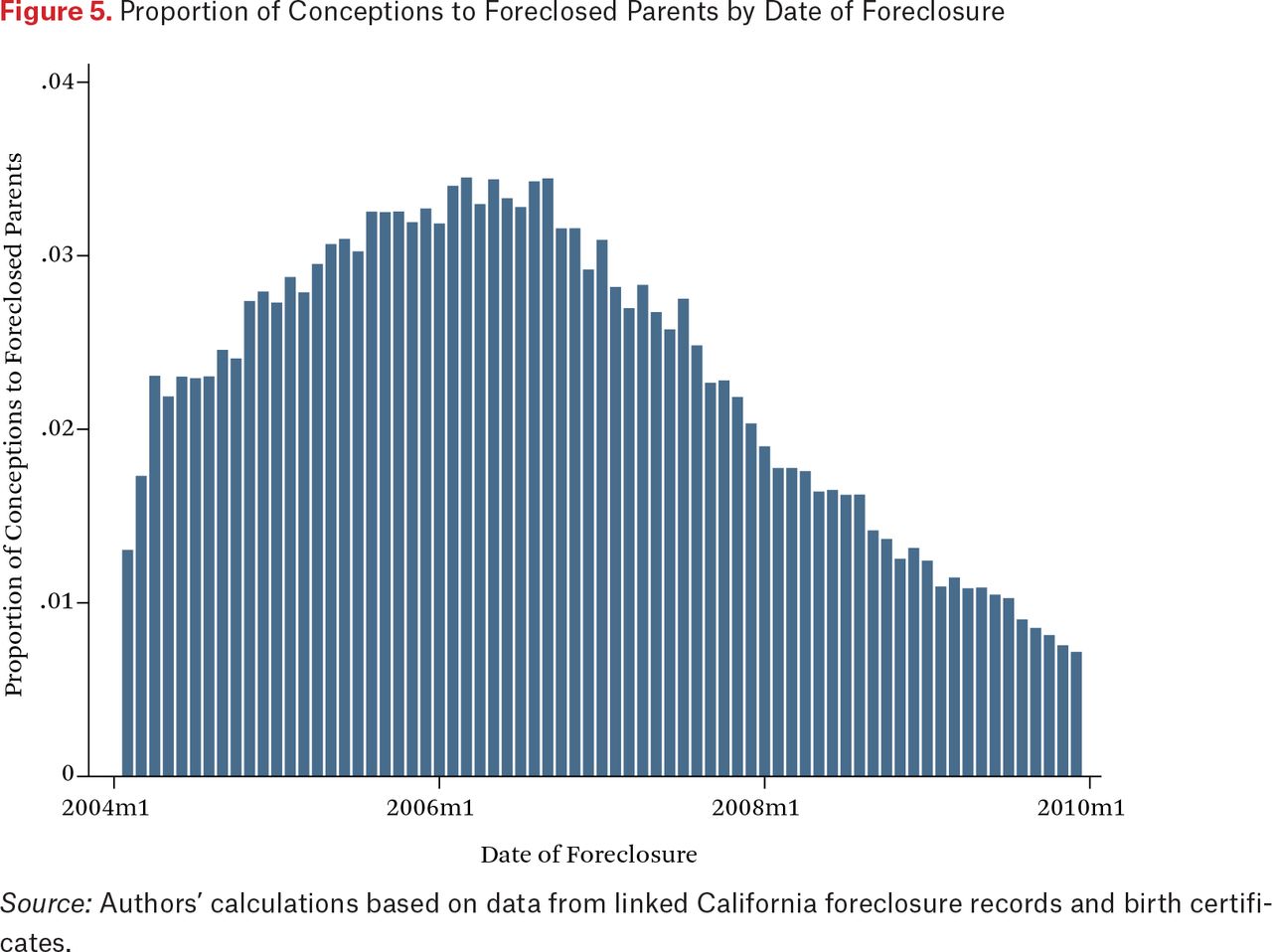

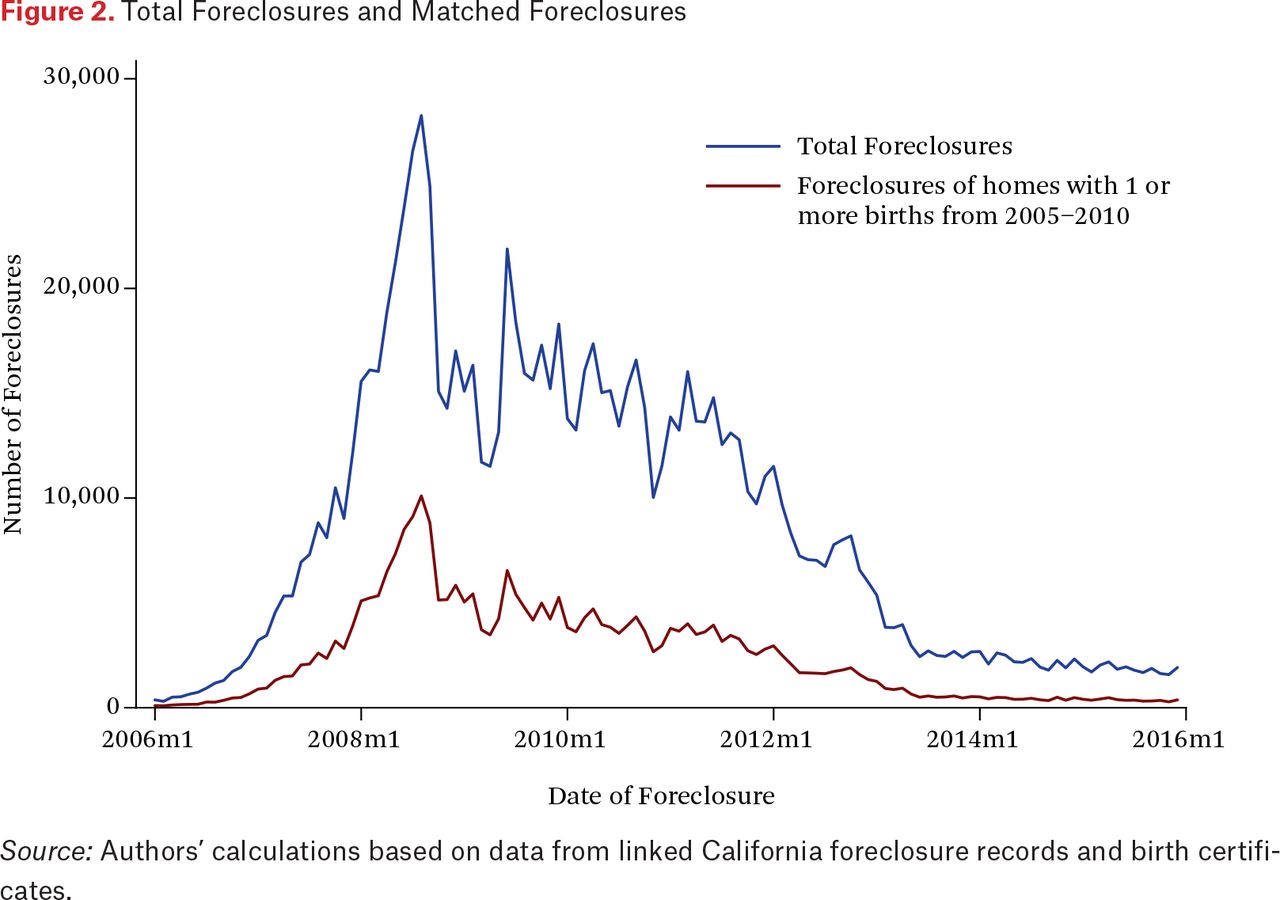

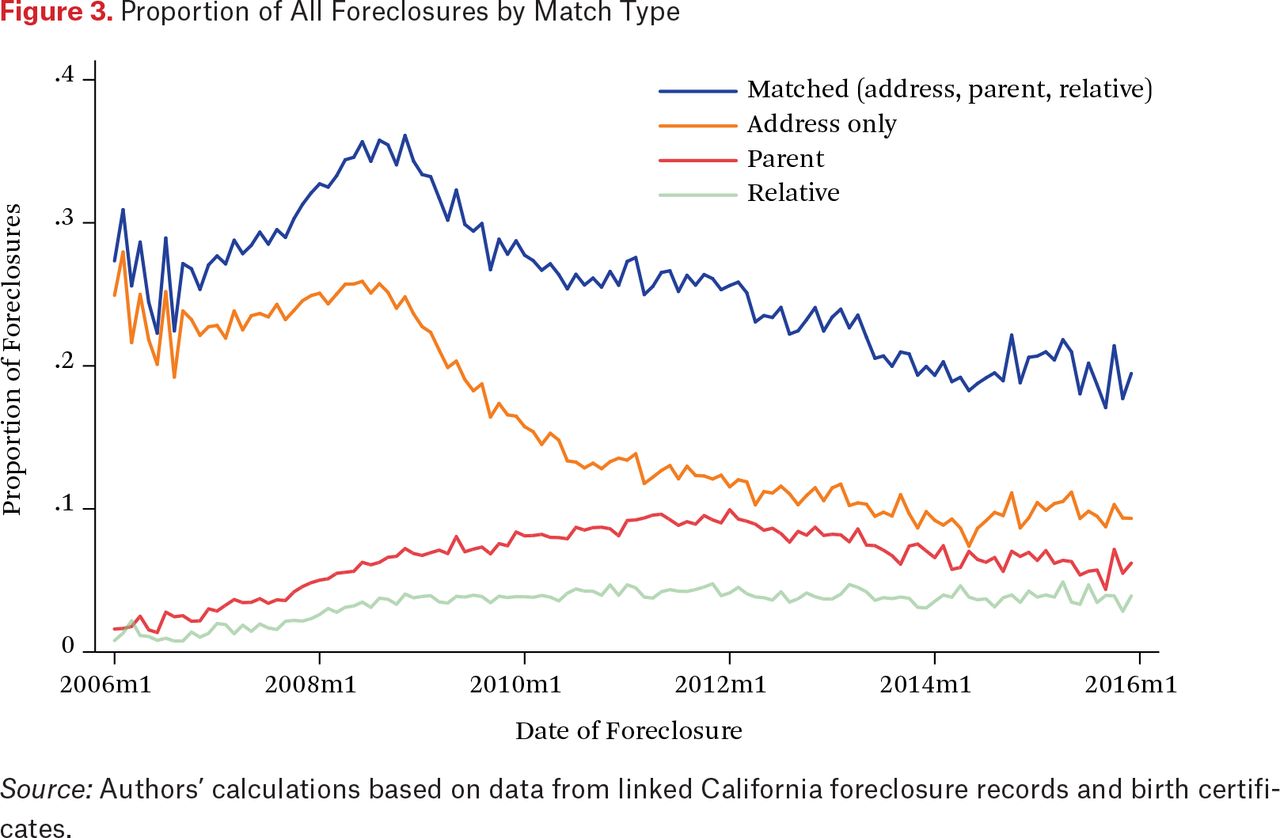

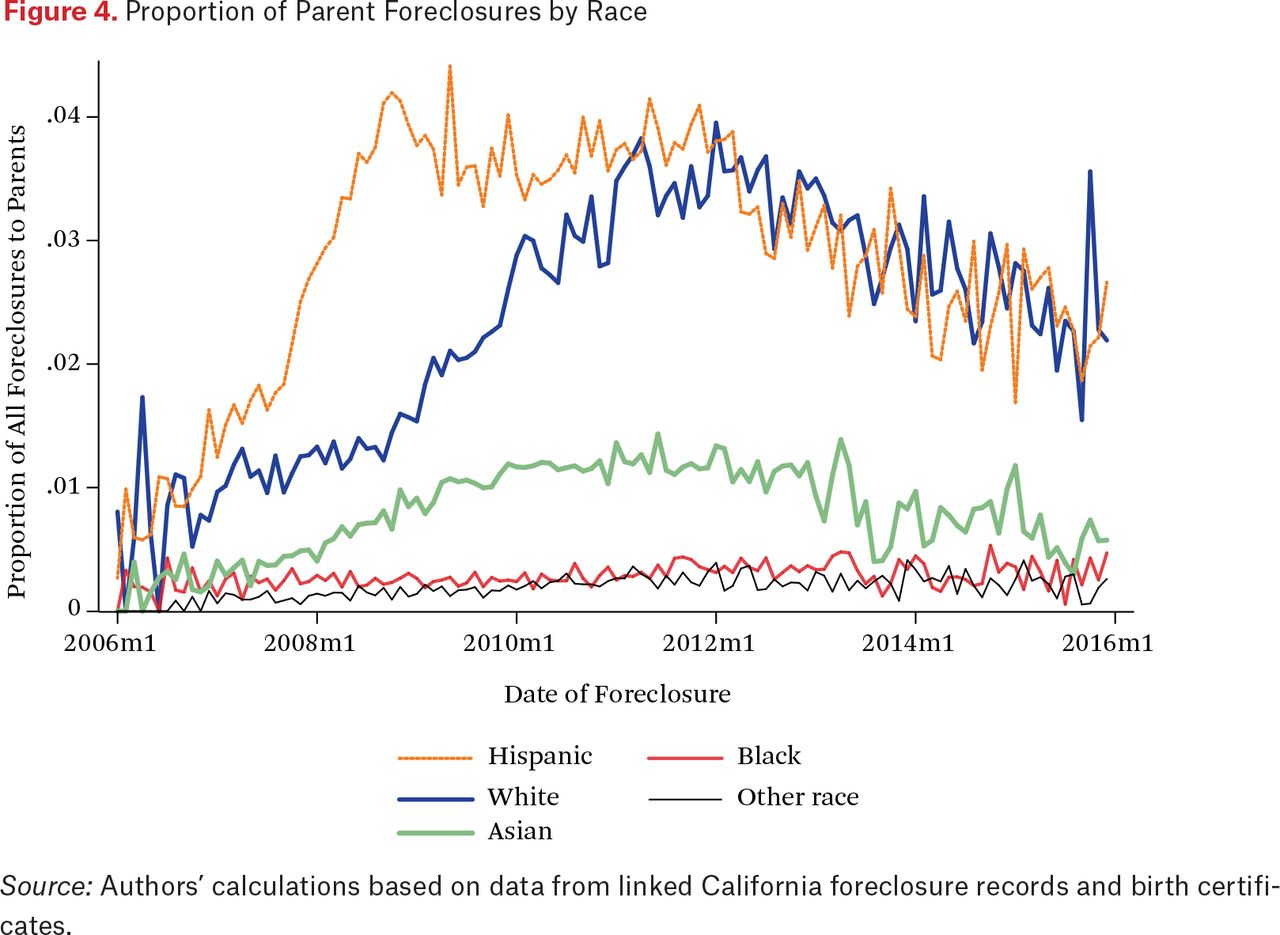

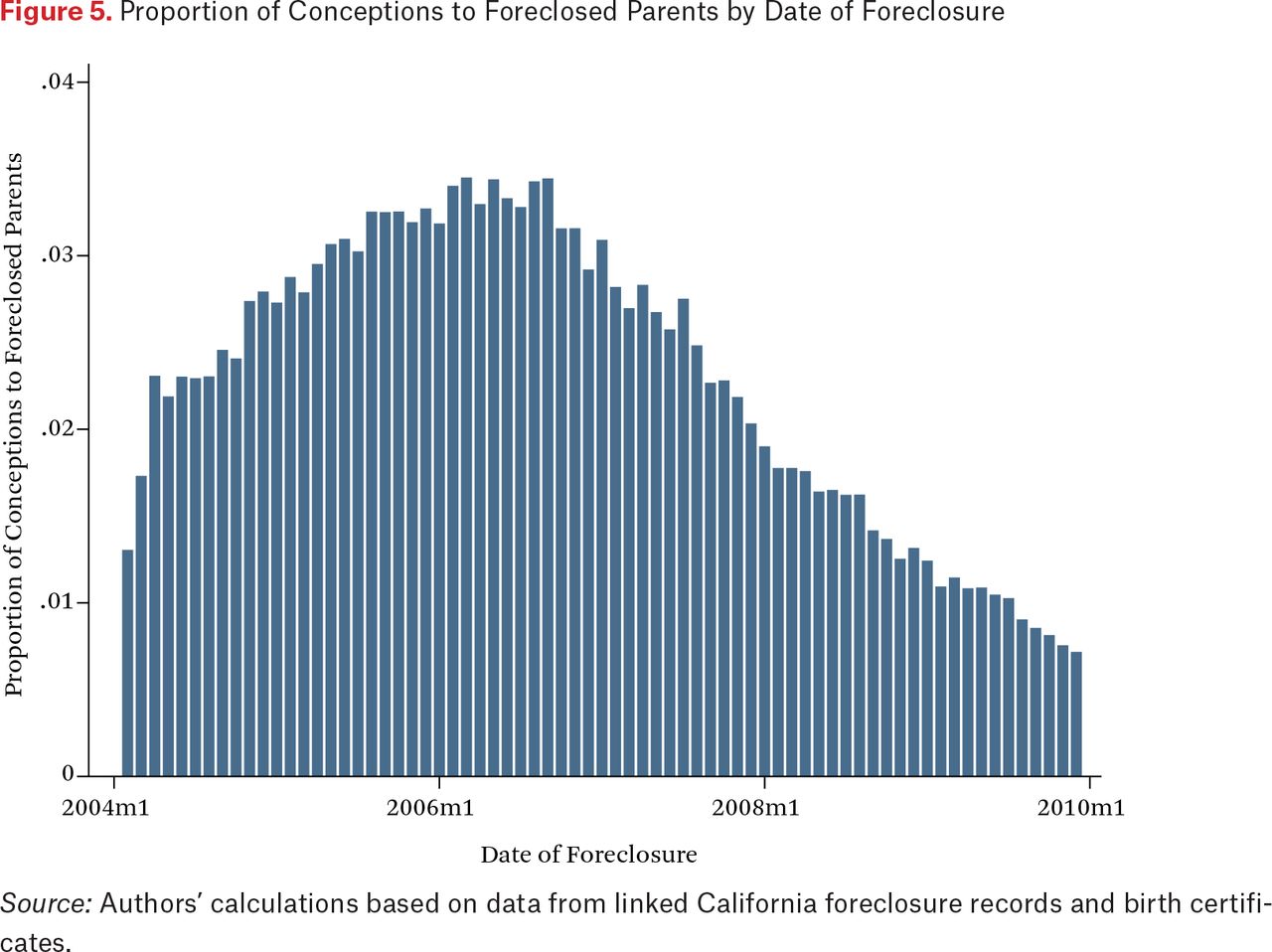

To understand how foreclosure rates for various matched groups vary over time, we created a series of descriptive monthly time series plots. We used the total universe of foreclosures in California as our denominator. Figure 2 presents the total monthly count of all foreclosures in California and the total monthly count of all foreclosures that matched at least one birth from 2005 to 2010 (foreclosures to exact or partial matches). Figure 3 presents the proportion of all foreclosures in that month that were to exact, relative, and address, and figure 4 presents the proportion of all exact match foreclosures by race-ethnicity with all foreclosures as the denominator. Given that the foreclosures could have happened after the birth, the time axis extends through 2015. Next, to show how conception cohorts changed over time, we used the total universe of births in California as our denominator. Figure 5 presents trends in the proportion of conceptions resulting in a live birth to parents who experienced a foreclosure.

Total Foreclosures and Matched Foreclosures

Proportion of All Foreclosures by Match Type

Proportion of Parent Foreclosures by Race

Proportion of Conceptions to Foreclosed Parents by Date of Foreclosure

Modeling Approach

All Births

We treat all births as statistically independent of one another and fit an ordinary least squares model to estimate the association between BWGA and match type (exact, relative, address) where the reference group is unmatched, adjusting for infant sex, parity, and health insurance, mother’s age, mother’s race, mother’s educational attainment (model 1).

Births to Matched

Next, we keep only births to exact or partial (exact, relative, address) matches. We compare the match timing across all groups (model 2). Given that higher order births are typically heavier than first births, we use the earliest period (before loan) as our reference group with the expectation that our results would be biased toward the null if foreclosure stress corresponded with lower BWGA. We then include a mother fixed effect (that is, sibling comparison) to compare differences in BWGA within each mother’s pair of singleton siblings (model 3).

The use of mother-fixed-effects strategy, though useful in minimizing unobserved confounding between mothers, may introduce selection bias (Kaufman 2013). The strategy relies on observing only a select population of mothers with a specific sequence of events—namely, she had an infant, later took out a loan that resulted in foreclosure, and then had yet another infant. This approach likely biased our results toward the null, given that mothers who were able to detect that foreclosure was imminent were likely to delay pregnancy. In addition, all second births in this sibling pair occurred to an older mother of higher parity, both of which tend to increase BWGA. The fixed-effects approach cannot statistically control for these influences on BWGA when estimating the foreclosure–BWGA relation. Thus, we interpret the mother-fixed-effects coefficients as a lower bound estimate of the true effect.

Births to Mothers Ever-Foreclosed (Exact Match)

In model 4, we restrict our sample to births to mothers who have ever been foreclosed (exact match) and apply the same approach as in model 2. Finally, we investigate how BWGA varies within-mother (model 5). Given the increased probability that foreclosures among those who took out a subprime loan in 2006 or 2007 was plausibly exogenous, we then restrict the sample to parents who took out their loan in 2006 or 2007. This loan cohort group may have been less likely to delay foreclosure due to the nature of their loan, and therefore may have exhibited more acutely the stress of foreclosure. All analyses were conducted using Stata 14.

RESULTS

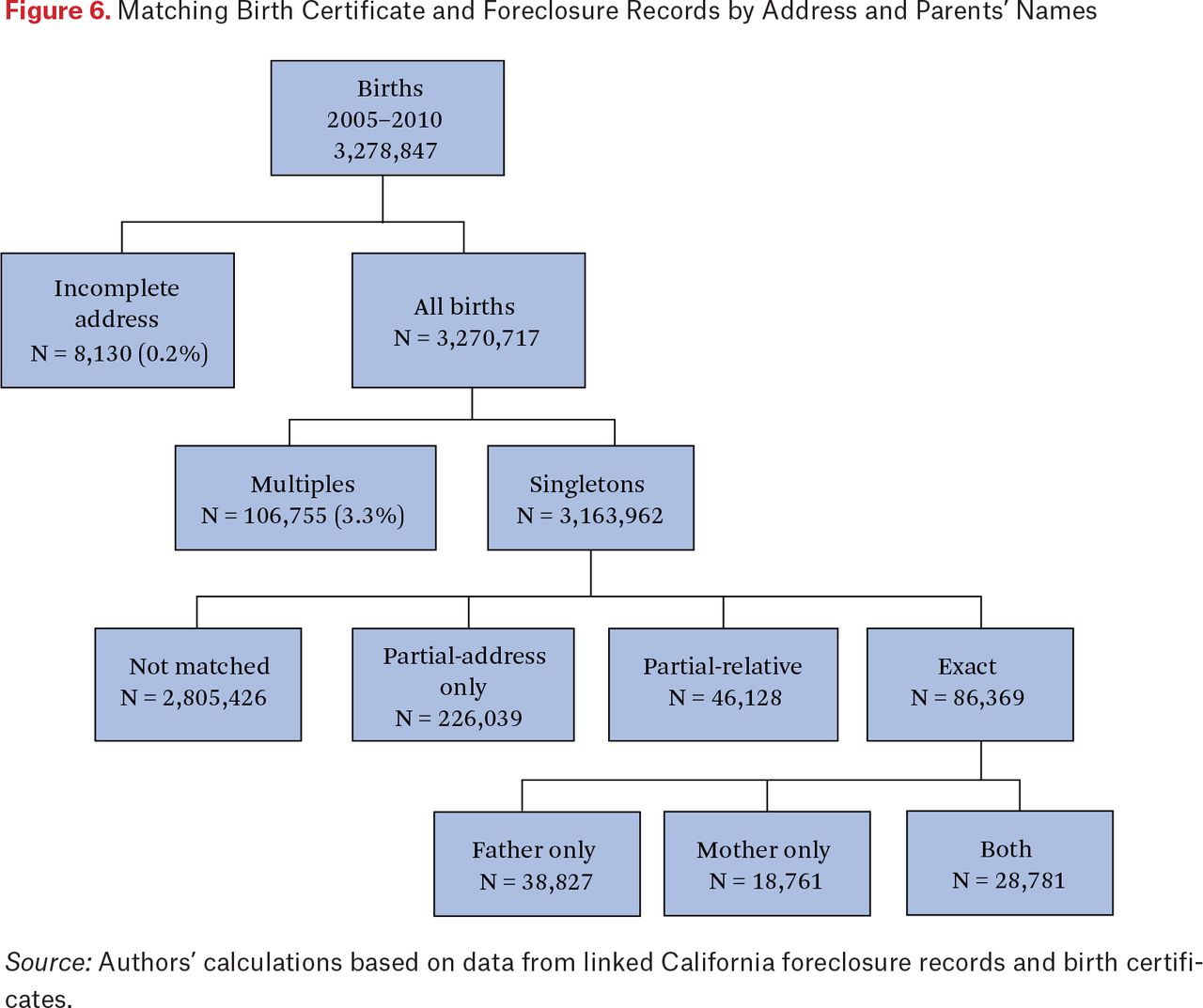

Figure 6 shows the inclusion criteria and number of births (not unique mothers) classified by the foreclosure matching algorithm. Table 1 shows the mean characteristics of unique mothers by match status: 60,611 mothers were classified as an exact match, 31,374 as a relative match, 155,611 as address-only match, and 2,179,690 as not matched.

Matching Birth Certificate and Foreclosure Records by Address and Parents’ Names

Compared with non–mortgage holders, mothers who were mortgage holders or had a child with a mortgage holder (exact match) were older, more likely to be non-Hispanic white, highly educated, had a prior birth, and listed the father on the birth certificate (table 1). In addition, they were less likely to have ever used Medicaid for a birth. Mothers who were residing with a relative who experienced a foreclosure (relative match) were younger and more likely to be Hispanic, less educated, use Medicaid, and be obese (BMI higher than 30) than the other groups.

Table 2 presents the mean characteristics of the mothers with nonmissing data who experienced a foreclosure and the within- and between-standard deviations of the key variables. Mean BWGA was 48.3 with a within-mother standard deviation of 10.4. The mean BWGA is lower than 50 percent because California has a greater proportion of Asian (lighter) births than the United States as a whole does.

Table 3 presents the mean characteristics by loan cohort of mothers who experienced a foreclosure. More than a third of mothers were part of the 2006 cohort. Among mothers who were in the 2006 cohort, there was the lowest proportion of non-Hispanic white mothers, highest proportion of black and Hispanic mothers, highest proportion of Medicaid ever mothers, highest proportion of no father, and lowest proportion with a bachelor’s degree.

At the peak in late 2008, ten thousand homes where newborns lived were foreclosed (figure 2), which represents roughly 35 percent of all foreclosures (figure 3). Yet the proportion of all foreclosures of parents (mortgage holders) peaked in 2012 at about 10 percent. The trend in proportion of foreclosures of parents varied widely by race-ethnicity (figure 4), the rate of foreclosed Hispanic parents rising earlier and faster than that of white parents.

Figure 5 plots the monthly proportion of conceptions resulting in live births of foreclosed parents (exact matched). This proportion rose from 1 percent in 2004 to more than 3 percent in 2007, and then returned to its pre-crisis rate.

Main Results

Table 4 presents the results for change in BWGA based on match type and foreclosure timing. Model 1 shows that births to parents with a mortgage that ultimately foreclosed have a 0.93 percentage point higher BWGA than those not matched to a foreclosed home. There was no difference in the relative and address-only matches relative to the unmatched group.

Differences in Birthweight for Gestational Age Percentile

Model 2 includes only those matched to a foreclosed property (n = 339,620). Despite the fact that advancing parity and maternal age is typically associated with heavier infants, births before the loan period are heavier for gestational age than those during and after the foreclosure period. When we include mother fixed effects (model 3), our results cannot reject the null. We find no evidence of within-mother difference in BWGA across various timing of exposure to the foreclosure process.

Model 4 includes only parents of exact matches (n = 82,058), and as in model 2, births before the loan period are heavier for gestational age compared to those before the loan. Inclusion of mother fixed effects attenuates these results and makes the coefficients statistically insignificant (model 5). Restricting our sample further, only to mothers who took out their loan in 2006 and 2007 and including mother fixed effects, we find that relative to before the loan, BWGA was 1.3 percentage points less during the foreclosure and 6.9 points less after it (model 6). Given the within-mother standard deviation of BWGA percentile is 10.4 percentage points, these results represent 13 percent and 66 percent of the average change in BWGA for each mother.

DISCUSSION

Our study indicates strong feasibility of linking birth vital statistics records to foreclosure deed records to examine perinatal outcomes before, during, and after foreclosures. Using the universe of administrative data from both birth certificates and foreclosure records in California, we find that the proportion of foreclosures in California among parents increased from 2 percent in 2006 to 10 percent in 2012. This suggests that families with newborns—particularly Hispanic and white mothers—faced challenges to transitioning to homeownership during this period.

We find that a higher proportion of non-Hispanic white and college-educated mothers had ever gone through foreclosure than those who had not. This finding is not surprising given that the population not exposed to foreclosure contained—in addition to secure homeowners—a large population of renters. However, among mothers who had ever gone through foreclosure, those who received their loan from 2005 to 2007 were more likely to be Hispanic, less educated, and to use Medicaid to pay for their birth than those who received their loans before 2005. Given that our study consists of all foreclosures and births in California, these descriptive statistics provide compelling evidence that the foreclosure crisis disproportionately impacted more marginalized families. Our results are consistent with other work using a subpopulation of adult mortgage holders, demonstrating racial-ethnic disparities in lending and foreclosure in California (Reid and Laderman 2009).

Next, we find that—among all infants with a mother who had a birth while residing in foreclosed home as the owner, relative, or renter—those who were in gestation during the loan period or resided in the home after the foreclosure were worse off than those who were born prior to the mortgage. It remains possible that unobserved factors correlate with both BWGA and a mother’s decision to conceive before (rather than after) the initiation of a home loan that ultimately leads to foreclosure. We, however, controlled for maternal race-ethnicity, maternal age, and socioeconomic status in the full sample (model 2); rival explanations of confounding would have to invoke an unmeasured variable not strongly correlated with these covariates but which strongly predicts later timing of fertility and causes a reduction BWGA. We know of no such variable in the perinatal epidemiology literature. When we compare sibling’s outcomes of each mother in the fixed-effects approach which controls for unobserved, time-invariant maternal characteristics (model 3), we cannot reject the null, although the direction of this foreclosure effect on BWGA remains negative.

Infants with a mother who had a birth while residing in a foreclosed home as the mortgage holder show lower BWGA than infants who were born prior to the mortgage (model 4). As in the full test, these coefficients are attenuated in the mother-fixed-effects approach (model 5). We suspect that this pattern of results arises from a circumstance in which healthier mothers who were aware of the upcoming foreclosure delayed fertility, but those who were worse off (either unaware or faced other circumstances) gave birth during the loan period.

Finally, our results are particularly compelling when we restrict our sample of all infants with a mother who took out a loan during the peak of the subprime boom (2006–2007) and later had a birth while living in a foreclosed home. In the maternal fixed-effects model, those who were born during the mortgage had a 1.3 percentage point lower BWGA than their siblings in gestation before the mortgage. Those conceived after the foreclosure showed a 7 percentage point lower BWGA than their siblings conceived before the mortgage. These coefficients are substantially large and statistically detectable, accounting for 10 to 70 percent of a within-mother standard deviation.

Our results go against the tide to show that—although advancing maternal age and increasing parity correlate with higher BWGA—infants born during the foreclosure process and after the foreclosure had a lower BWGA relative to their siblings born earlier (before the mortgage). The results, taken in combination with the finding that Hispanic, socioeconomically disadvantaged families were disproportionately represented in the loan cohorts of 2005–2007, suggest that the foreclosure crisis may have contributed to disparities in initial health endowments.

This study has several limitations. Our findings rest on the assumption that different periods of the loan elicited stress and anxiety, yet the magnitude and qualitative experience of this stress was not directly measured. Additionally, we assume that those born prior to the loan are less likely to be exposed to the financial stress. This circumstance may not hold if parents decide to take out a second lien on their home after the birth of their child because they are stressed. We suspect that additional administrative data on finances and loan characteristics may elucidate a nuanced picture of finance-related stress in this population.

Finally, absent routinized data collection on pregnancy loss, we cannot know the extent to which pregnancy loss induced by foreclosure may affect our findings. It remains possible that, consistent with the literature, the most at-risk gestations may be less likely to survive until birth (Bruckner, Mortensen, and Catalano 2016). Such selection in utero may have attenuated the foreclosure coefficient toward the null.

The feasibility of linking public foreclosure records to individual-level vital statistics holds promise for future research applications. The literature examining social and economic stressors before and during the perinatal period tends to rely on mother’s self-report of stressors (Hogue et al. 2013), which can introduce strong measurement error (Kesmodel 2018). By contrast, linkage to administrative datasets which records key social and economic setbacks to a family have the potential to minimize measurement error of these important exposures. In addition, the use of linked siblings for perinatal health studies remains an underused strategy to minimize confounding that arises from unmeasured differences in maternal health (Kramer, Dunlop, and Hogue 2014).

Population-level work such as this could complement existing small (and relatively expensive) cohort studies that rely on sampling. For instance, identification of economic (such as credit constraints) and neighborhood stressors experienced at multiple time points among adults of childbearing age could inform basic research on fertility timing, family formation, and migration patterns. In addition, to the extent that the timing, dose, and duration of family stressors can be measured from administrative data, such work has the potential to identify economic and social antecedents of endowments at birth.

FOOTNOTES

↵1. H.R. 10—Financial CHOICE Act of 2017, 115th Congress, 1st session.

- © 2019 Russell Sage Foundation. Downing, Janelle, and Tim Bruckner. 2019. “Subprime Babies: The Foreclosure Crisis and Initial Health Endowments.” RSF: The Russell Sage Foundation Journal of the Social Sciences 5(2): 123–40. DOI: 10.7758/RSF.2019.5.2.07. This study was approved by the Committee for the Protection of Human Subjects of the California Health and Human Services Agency and the Institutional Review Board of the University of California, Irvine (IRB #2013–9716). Direct correspondence to: Janelle Downing at downingj{at}ohsu.edu, 3181 SW Sam Jackson Park Rd., Portland, OR 97239; and Tim Bruckner at tim.bruckner{at}uci.edu, 653 East Peltason Dr., Irvine, CA 92697.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.