Abstract

Fifty years after the national Kerner Commission report on urban unrest and fifty-three years after California’s McCone Commission report on the 1965 Watts riots, substantial racial disparity in education, housing, employment, and wealth is still pervasive in Los Angeles. Neither report mentions wealth inequality as a cause for concern, however. This article examines one key dimension of racial wealth inequality through the lens of home ownership, particularly in South Los Angeles, where the 1965 Watts riots took place. It also analyzes the state’s role in housing development in codifying and expanding practices of racial and class segregation that has led to the production and reproduction of racial inequality in South Los Angeles compared with Los Angeles County.

In its now well-known report, the National Advisory Commission on Civil Disorders (the Kerner Commission, thus the Kerner report) cited the 1965 Watts riots in Los Angeles as an omen of violence before the summer of 1967 (Kerner Report 1968; Farley 2008). The commission noted, “The Los Angeles riot, the worst in the United States since the Detroit riot of 1943, shocked all who had been confident that race relations were improving in the North” (Kerner Report 1968, 38). Fifty years after the Kerner Commission’s report and fifty-three years after California’s McCone Commission’s report on Watts, we examine the extent to which a key component of racial inequality has or has not been addressed and the limitations of the solutions the two commissions put forth.1

The reports’ findings are not surprising, and they mirror the findings of similar postmortems into other large-scale urban racial riots, massacres, and uprisings before and after the 1960s, including the 1871 Chinese Massacre, 1943 Zoot Suit riots, and the 1992 civil unrest in Los Angeles.2 Both the Kerner and McCone reports recommend addressing racial disparities through emergency literacy and preschool programs, improved police-community ties, increased affordable housing, more job training projects, upgraded health-care services, more efficient public transportation, among many suggestions. However, none of the original proposals mention wealth inequality as a cause for concern.

This article examines one key dimension of racial wealth inequality through the lens of home ownership, particularly in South Los Angeles, where the 1965 Watts riots took place. Homeownership is the largest component of wealth for many Americans, particularly those in the middle class. Homeownership also has neighborhood benefits in terms of added stability. Yet, for many communities of color, homeownership is out of reach. Countless people of color are unable to move from “bad” neighborhoods or purchase a home in their community. This issue has reached crisis levels in Los Angeles, which ranks near the top in homelessness and near the bottom in homeownership (Lansner 2017).

THE MCCONE REPORT, KERNER REPORT, AND THE 1965 WATTS RIOTS

On Wednesday evening of August 11, 1965, an African American motorist was arrested for speeding. A minor roadside argument broke out, and then escalated into a fight. The community reacted in outrage to allegations of police brutality that soon spread, and six days of looting and arson followed. Los Angeles police needed the support of nearly four thousand members of the California Army National Guard to quell the riots, which resulted in thirty-four deaths and more than $40 million in property damage (Kerner Report 1968; Hinton 2016).3 The riots were blamed principally on police racism and brutality. It was the city’s worst civil unrest until the 1992 acquittal of the policemen who assaulted Rodney King.

The uprisings of 1967 in hundreds of cities across the nation involved blacks fighting against local symbols of white privilege in black neighborhoods, rather than against white individuals. It was only after the Watts riots and the many black uprisings that took place across America in the late 1960s that major municipal or federal commissions were appointed to investigate the depth of social and material inequality in urban centers, revealing a pervasive lack of awareness of the scale of the issues within government institutions and society. The reports document how social and economic conditions in the riot cities represented a systematic pattern of severe disadvantage for blacks relative to whites. Although racially biased police practices were the precipitating factors largely responsible for igniting the 1965 Watts civil unrest, both the Kerner and McCone Commissions point to inadequate housing conditions as one of the most severe root causes.4

The McCone Commission provided a more detailed account of the conditions in Los Angeles, uncovering how residents of the Watts area lived in conditions inferior to the citywide average and strikingly inferior to newer sections of the city. The commission also noted that conditions were not nearly as bleak as the highly visible deterioration of northern slums. Assessing the issues required peeling away at the structural differences in housing. Overcrowding stood out as one of the greatest sources of housing disparity. An average of 4.3 persons lived in each Watts household, versus an overall county average of 2.94 per household (Los Angeles County and City Human Relations Commissions 1985). Furthermore, 88.6 percent of the total black population lived in areas considered segregated and concentrated within South-Central Los Angeles (McCone and Christopher 1965).

The McCone Commission, despite its assessment that the area was neither “gem nor slum,” does express a major concern that a “serious deterioration of the area was in progress.” Homes in the area were old and required constant maintenance to remain inhabitable, and more than two-thirds were owned by absentee landlords (McCone and Christopher 1965). The barriers to homeownership residents faced exacerbated this situation creating a general deficit in housing investments. The McCone report states, “Compounding the problem is the fact that both private financial intuitions and the Federal Housing Authority consider the residential multiple unit in the curfew area an unattractive market because of difficult collection problems, high maintenance costs, and a generally depreciating area resulting from the age of surrounding structures” (1965, 79).

The recommendations of the McCone and Kerner reports focus on the preservation of and increased presence of affordable rental units, in large part by subsidizing private and non-profit investors and developers. Hypothetically, this strategy could address the challenge of improving the lack of decent and affordable housing, assuming that developers would significantly expand the supply, use government support to lower rents, and continue to maintain the housing stock.

There were three flaws with this approach. First, it was unlikely that funding would be adequate, thus overall impact would be minimal relative to the size of the housing problem. Second, the reports do not offer any detailed mechanisms to ensure the desired outcome from private developers; consequently the commissions implicitly relied on a simplistic assumption that market forces would be sufficient, that more competition would keep rents low and force absentee owners to pass along savings from the subsidies. However, it was just as likely that the housing market was operating to give the balance of economic power to landlords. Under these conditions, governmental support would end up in the developers’ pocket.

Third, the recommendations do little to address the lack of local ownership of land and housing, which meant that inequalities in asset and wealth holding would remain, or become worse. Indeed, it would have been better had the commissions recommended or given more priority to increasing access to financial resources to residents, ending discriminatory practices in mortgage lending, and encouraging and providing incentives for home ownership at manageable fees. Not only would this have increased local households’ wealth; it also could have generated the positive externalities and community stability that come with the presence of more homeowners.

Unfortunately, many of the recommendations were either not implemented or only partially implemented, and South Los Angeles remained a marginalized community. Nineteen years after the 1965 McCone report, the Los Angeles County and City Human Relations Commission found that housing remained one of the most critical problems in South Central Los Angeles.5 The persistent socioeconomic problems and frustration felt by local residents eventually led to another sociopolitical explosion, the 1992 civil uprising.

THE MULTIETHNIC RIOTS OF 1992

The 1985 Los Angeles County and City Human Relations Commissions report recommends that the mayor and city council request the City Planning Commission to develop a plan, including legislation if necessary, to address the critical housing problems of South-Central Los Angeles. The report concludes, “We cannot emphasize too strongly the critical nature of the problems described in this report and the implications of continued inaction. We should not have to wait for a second Los Angeles riot to erupt to bring these problems to serious public attention” (Los Angeles County and City Human Relations Commissions 1985, 16). Seven years later, Los Angeles would witness a massive second uprising—riots precipitated by the failure of a jury empaneled in Simi Valley to convict policemen who had engaged in a taped beating of Rodney King.6

The growing economic disparity in Los Angeles caused by corporate restructuring and government deregulation produced a widespread feeling of frustration and powerlessness among communities of color. The King beating verdicts, like the police force abuse of 1965, acted as the spark that set off the cumulative resentment in a violent expression of collective public protest (Davis 1992b). One main difference between the 1992 King riots and the 1965 Watts civil unrest was the multiethnic involvement of Koreans and Latinos, demonstrating that tensions were not limited to segregated black neighborhoods (Pastor 1995). This shift reflected a new racial paradigm that was taking shape not only in Los Angeles, but throughout America. This required a parallel shift in the analysis of issues such as segregation and access to decent housing from focusing solely on disparities between black and white people to one that is cross-cutting and multidimensional. The history of civil unrest in Los Angeles from the Chinese Massacre of 1871 to the 1965 Watts civil unrest, the 1968 Chicano Blowouts, and the 1992 Los Angeles uprising becomes part of a continuum of systematic oppression of communities of color that should spur renewed critical conversations about race, economics, and justice in America.7

THE ROLE OF PLACE AND RACE IN CREATING HOMEOWNERSHIP DISPARITIES

Unlike New York or San Francisco, Los Angeles is decentralized in its structure. Its major commercial, financial, and cultural institutions are geographically dispersed rather than concentrated in a single central urban core. This spatial structure led to urban sprawl, which arguably intensified the creation of racially segregated neighborhoods (Le Goix 2005). However, the structure of segregation in Los Angeles was created through racial discrimination, restrictions, and systematic displacement long before the metropolis sprawled to its contemporary limits.

In one of the more blatant uses of state power to displace people of color, the City of Los Angeles used eminent domain with funds from the Federal Housing Act of 1949 to acquire land largely owned by Mexican Americans in Los Angeles’ Chavez Ravine (Normark 1999). The city used California’s redevelopment law to justify massive “poor removal,” uprooting more than one thousand Mexican Americans (Davis 1992b; Becerra 2012). The land then was used to construct Dodger Stadium.

Federal subsidies for urban sprawl led to disinvestment in the central city and increased development of suburban areas, which, concomitant with the displacement of poorer residents and people of color, gave rise to contemporary patterns of segregation. This pattern was reinforced through two mechanisms. Although legalized housing discrimination and practices by the Fair Housing Authority (FHA) ended with the Fair Housing Act of 1968, the outcomes it gave rise to persist. For example, the systematic exclusion from the broader appreciating housing market and exploitive housing market-based strategies that have specifically targeted people of color (Kain and Quigley 1972; Sharp and Hall 2014, Massey 2005; Steil et al. 2017). The exodus of many of the wealthier and white households to the suburbs further contributed to marginalization as employment and commercial growth would follow, creating problems of spatial mismatch for poor residents of central cities (Davis 1992a; De Graaf and Taylor 2001; Pastor 2001b).

A growing post–World War II economy coupled with a severe labor shortage forced the federal government to finally abolish the national origins formula that had been in place since the 1924 Immigration Act and replace it with the 1965 Hart-Cellar Immigration Act (Chan 1991).8 This more open immigration policy coupled with the international episodes of war and large-scale violence in which the United States was involved opened the door both to more targeted programs, such as the Indochina Migration and Refugee Act of 1975, which provided refugees who fled from Cambodia and Vietnam with assistance in domestic resettlement (Takaki 1989; Chan 1991; Ong, Bonacich, and Cheng 1994), and to a greater influx from Latin America following the political upheaval of the 1970s and 1980s, in particular in the Central American nations of El Salvador, Guatemala, Honduras, and Nicaragua (Chinchilla and Hamilton 2004). Moreover, the ratification of the North American Free Trade Agreement in 1994 created favorable economic conditions and insourcing of immigrant labor from Mexico for U.S. firms until the late 2010s (Kelly and Massey 2007). Together, these events combined with Los Angeles’ size and strategic location have contributed to the region’s becoming home to some of the largest clusters of immigrant populations.9

Los Angeles offers a wide range of opportunities to immigrants that continues to make it an attractive destination despite the high cost of life in the region (Ley 2007). Despite the deindustrialization of the late 1970s, Los Angeles was able to thrive because of federal spending on defense in the Reagan-Bush era. It became a key center of the military industrial complex, primarily creating low-skilled assembly and manufacturing firms alongside higher-tech firms linked to electronics and media (Pastor 2001a). However, despite a relatively strong economic recovery following the withdrawal of the defense industry (thanks in part to financial investments from the Asia Pacific region and labor from Mexico), this path to development promoted a strong economic bifurcation that reinforced the creation of lower- to middle-wage jobs (Ong, Bonacich, and Cheng 1994; Storper et al. 2015).

The preponderance of low-wage employment available to new migrants locked many in conditions that make acceding to homeownership or renting more difficult and promoted suboptimal housing conditions (Painter and Yu 2008). In general, differences in socioeconomic status are the main source of disparity in homeownership between white households and Asian and Latino households (Kuebler and Rugh 2013). However, Latinos in Los Angeles in particular have a large degree of heterogeneity in nativity, citizenship, and legal status. Eileen McConnell finds that undocumented migrants were substantially less likely to be homeowners and that authorized noncitizens were also less likely than naturalized Latinos to be homeowners (2015).

Although immigration status creates further barriers to homeownership, many of the same obstacles apply to all residents of segregated central cities. Casey Dawkins explains that for individuals working low-wage jobs, access to transit is a necessity which creates a locational tradeoff (2005). Greater transit connectivity is required to access jobs, but such locations tend to have higher rents that prevent acquiring a car and moving to a location with lower rent and better access to higher-paying jobs. This trade-off also significantly delays ownership, further impeding the accumulation of wealth through home equity (see also Hilber and Liu 2008).

The housing downturn that began in 2006 had distinctive geographic patterns. The Pew Research Center reports that more than two in five of the nation’s Latino and Asian American households lived in Arizona, California, Florida, Michigan, and Nevada. These five states had the steepest declines in home prices in 2005. In contrast, about one in five of the nation’s white or black households lived in these five states and were not affected as severely (Kochhar, Fry, and Taylor 2011).

Nationally, Rakesh Kochhar and his colleagues estimate that the crisis cut the median net worth of Asian American households in half, from $168,103 in 2005 to $78,066 in 2009. Hispanic households’ net worth was only a third of what it was in 2009 ($18,359 to $6,325) while black households lost over half of their wealth ($12,124 to $5,677). Derek Hyra and Jacob Rugh find that black wealth was significantly reduced through systemic predatory lending practices by major lending institutions and mortgage brokers, who directed black borrowers into high-cost, high-risk loans that left them susceptible to default, foreclosure, and loss of home equity during the great recession (2016). In contrast, the white decline in median net worth was 16 percent, from $134,992 to $113,149 (Kochhar, Fry, and Taylor 2011).

In 1965, Martin Luther King Jr. had noticed the extreme levels of inequality unique to Los Angeles. Commenting on the proximity of Watts to affluent areas, he noted that the average black person in “Watts is closer to the affluence of our society and further away from it than any other American community.” Indeed, fifty years later, for every dollar of wealth held by the average white household, black and Mexican households have 1 cent, Koreans 7 cents, other Latinos 12 cents, and Vietnamese 17 cents (De La Cruz-Viesca et al. 2016).

The foreclosure crisis exacerbated the vulnerable position of people of color in Los Angeles, but it also affected them differently. African Americans and Latinos were more exposed to foreclosure, joblessness, and home value declines than other groups (Bocian, Li, and Ernst 2010; U.S. Census Bureau 2011). Asian Americans experienced lower unemployment rates and home value declines than non-Hispanic whites, but shouldered increased housing cost burdens to avoid foreclosure (U.S. Census Bureau 2011).

DATA AND METHODS

This study relies primarily on summaries of key indicators pertaining to housing outcomes in South Los Angeles between 1960 and 2015. Detailed statistical analysis of the data is beyond the scope of this article, but we ran simple logit regressions for homeownership to isolate the effect of residing in South Los Angeles above and beyond its socioeconomic composition.

All demographic and socioeconomic data come from the Integrated Public Use Microdata Sample for 1960 (Ruggles et al. 2017), the decennial U.S. Census Bureau public-use micro samples (PUMS) for 1990, and the five-year American Community Survey PUMS for 2015. Home equity data were derived from the 2011 and 2013 Department of Housing and Urban Development’s American Housing Survey (AHS), and the National Asset Scorecard and Communities of Color Survey administered by the Samuel DuBois Cook Center on Social Equity at Duke University, that report information on race, and other key demographics such as income, education, and housing information.10

We use South Los Angeles as the focal area, which we contrast to Los Angeles County as a measure of broader patterns. There are many definitions of South Los Angeles and boundaries are fluid. We use the definition of the Los Angeles Times because it fully encompasses the historical curfew area which the McCone Commission relied on, allows for the gradual expansion of the relevant area over time, and closely matches the units within which data are available (for details, see the appendix).

Data availability and compatibility constrained the analysis to the years 1960, 1990, and 2015. Nonetheless, each year corresponds to meaningful historical junctures: 1960 captures Los Angeles on the eve of the Watts riots, but also the complete shift in socioeconomic structure. The year 1990, in addition to providing an overview of pre-1992 Los Angeles, shows the effect of major transformations due to the national recession of the early 1990s, global restructuring of the economy, and shifts in demographic patterns. Finally, 2015 represents contemporary Los Angeles.

Demographic Changes

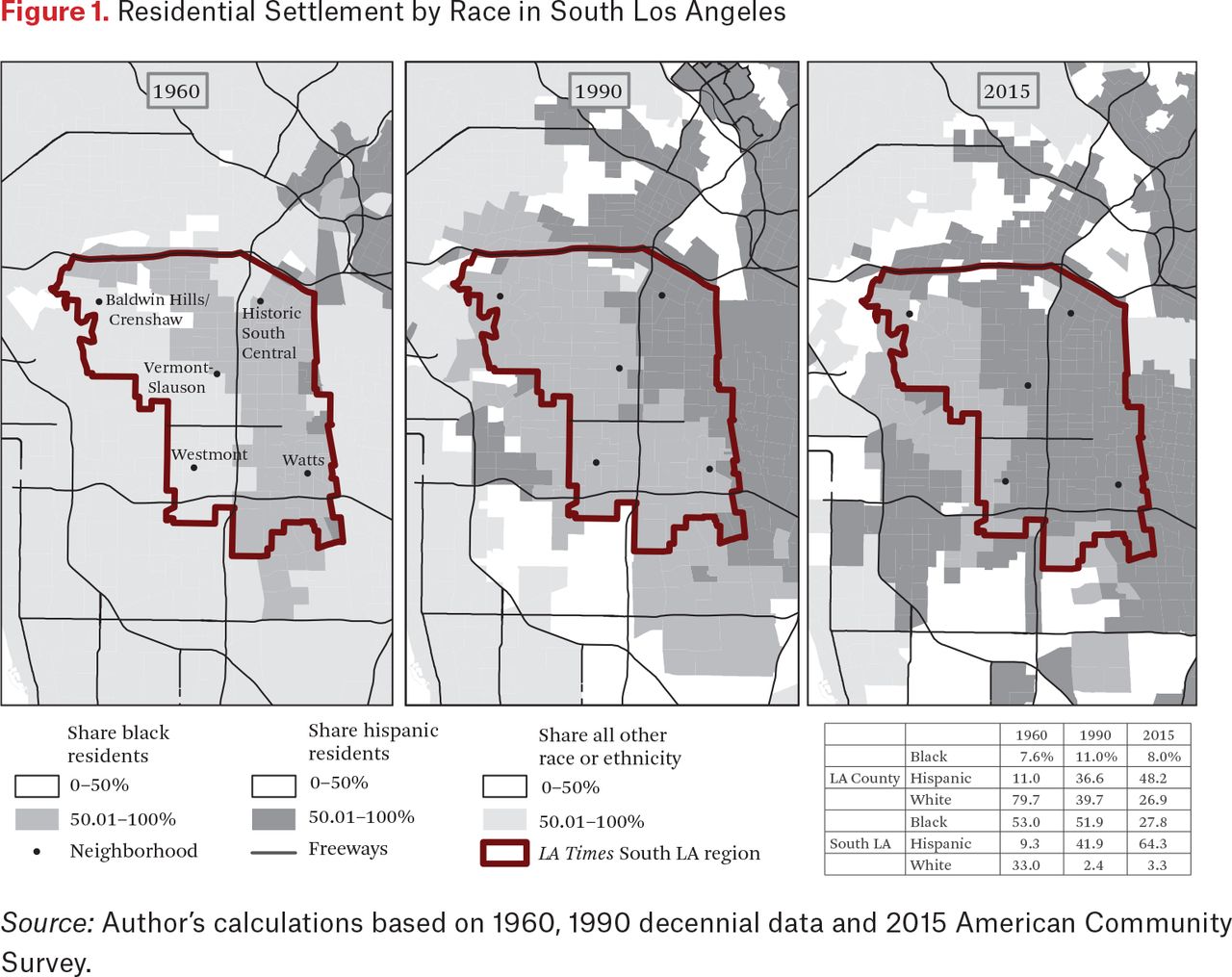

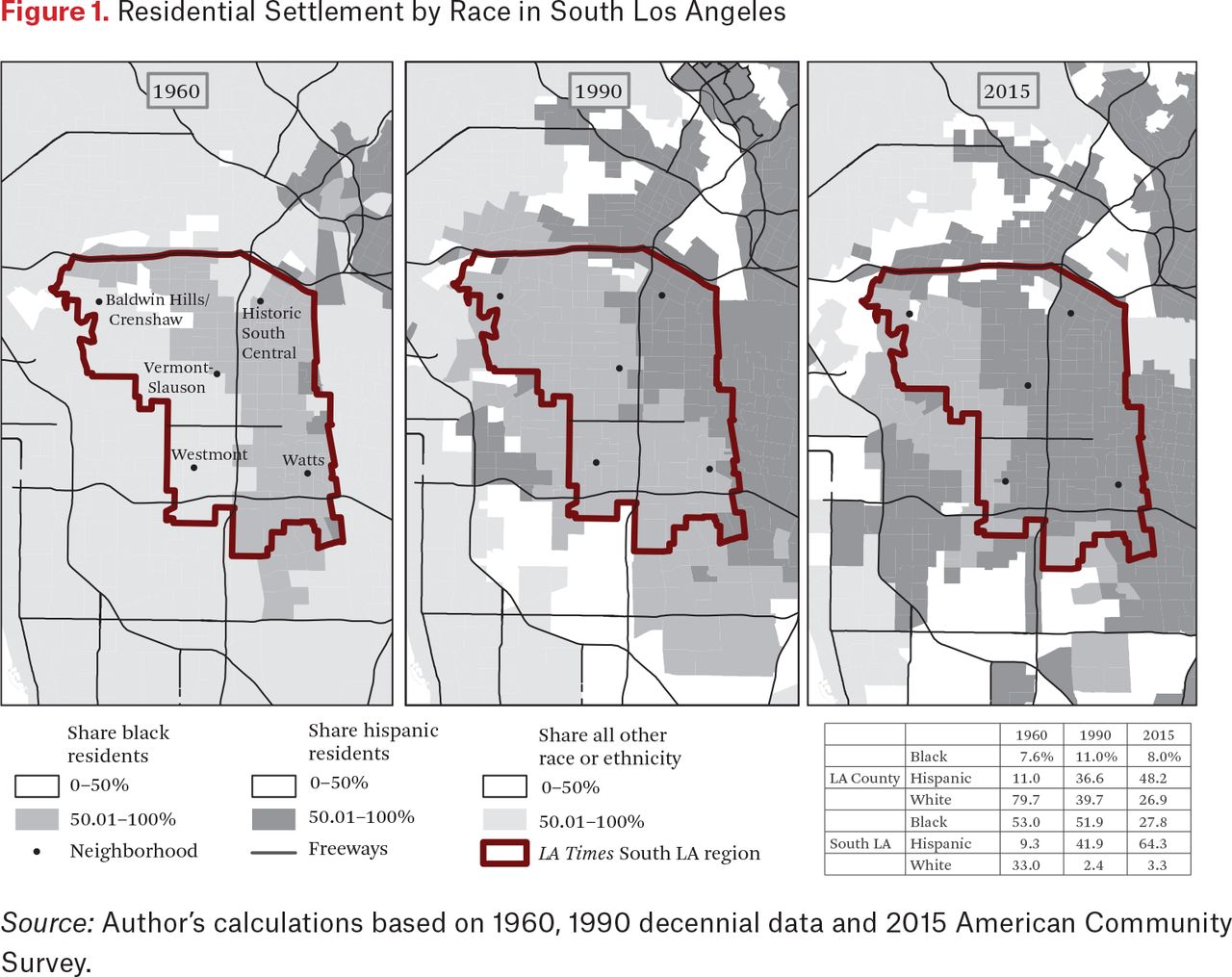

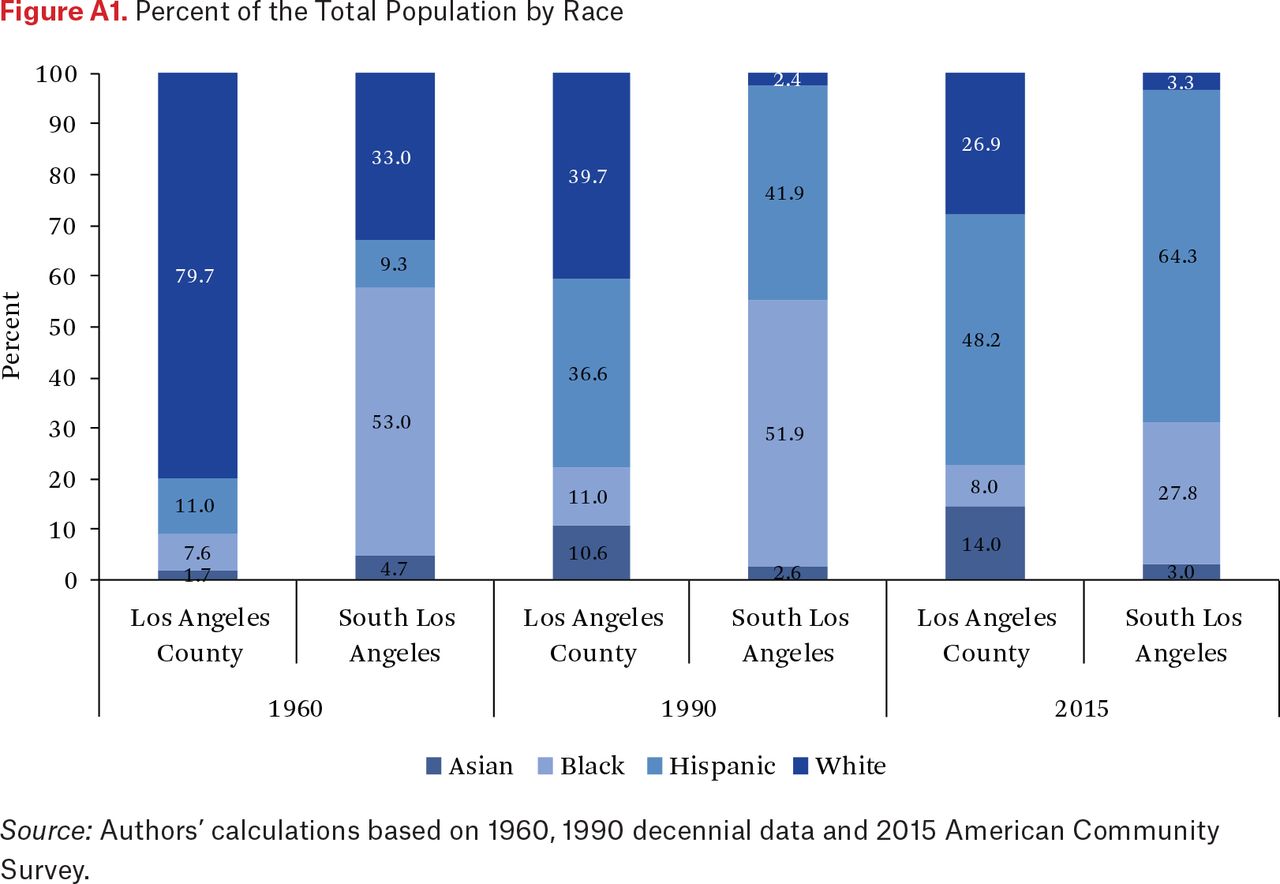

Between 1960 and 2015, Los Angeles County’s white population as a share of the county total fell from 4,719,780 to 2,637,477 (from 80 percent to 27 percent). The black population remained relatively stable (at about 8 percent). The Asian population grew exponentially, from 2 percent to 14 percent. Hispanics outpaced all groups, from 11 percent in 1960 to 49 percent in 2015, becoming the largest group by 1990 (see figure 1 and figure A1 and table A1 in the appendix). Meanwhile, the resident population of the county as a whole increased from six to ten million.

Population Number by Race, Los Angeles County and South Los Angeles

Residential Settlement by Race in South Los Angeles

Percent of the Total Population by Race

The population of South Los Angeles grew more slowly, increasing by a third since 1960. Still, at more than seven hundred, it would be the fifth largest city in California were it a municipality. In 1960, South Los Angeles was 53 percent black with a substantial but far smaller white population (around a third of the area total) and a smaller Hispanic population, a stark comparison to Los Angeles County. At the time, South Los Angeles was geographically divided between the western half, where most whites resided, and the predominantly black eastern half, with little overlap (see figure 1).

By 1990, the growth of the Hispanic population in South Los Angeles (LA) and the relative stability of the black population translated to a near complete disappearance of whites from the area. Geographically, this marked the largest extent of the black community in South LA. Most Hispanics were spatially clustered in the northeast corner of the area, and the neighborhood boundary extended much further east and was moving gradually west. The expansion westward of the Latino community made the area majority Hispanic (64 percent) by 2015. The black population, after a dramatic relative decline from 53 percent to 28 percent, was clustered at the western edge of South LA. This decline was not just relative: the number dropped by nearly one hundred thousand from 1960.

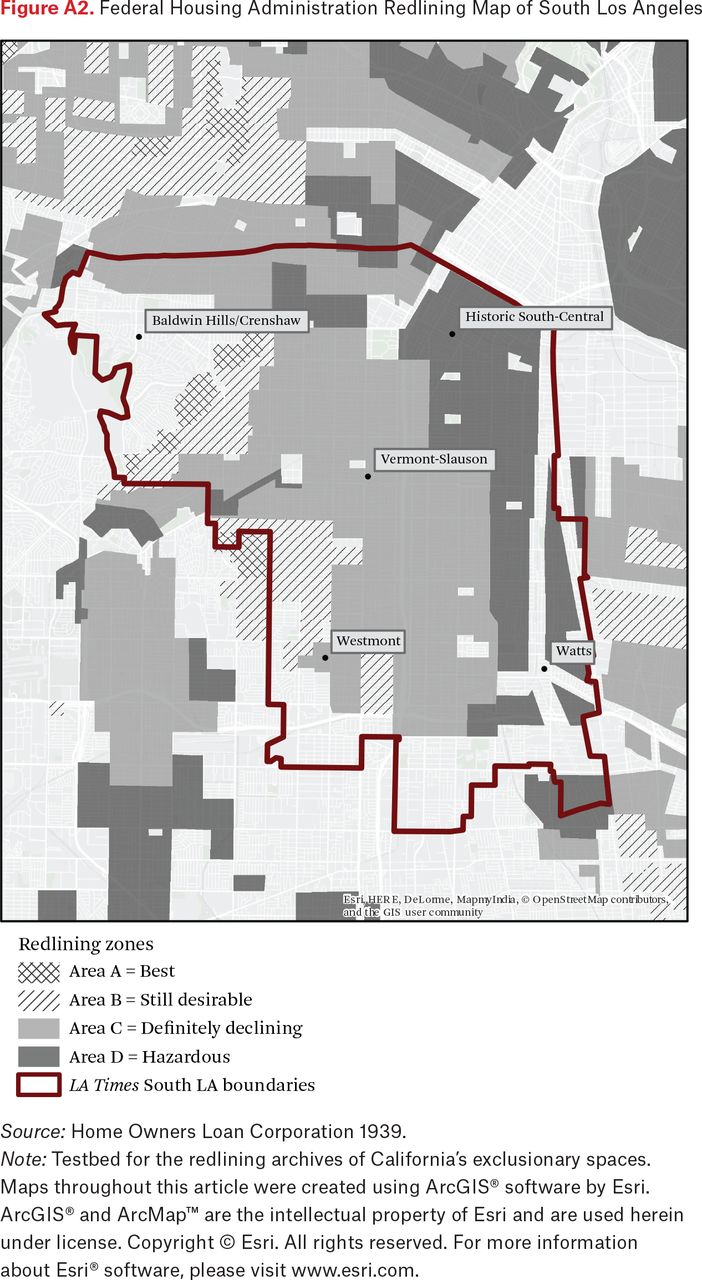

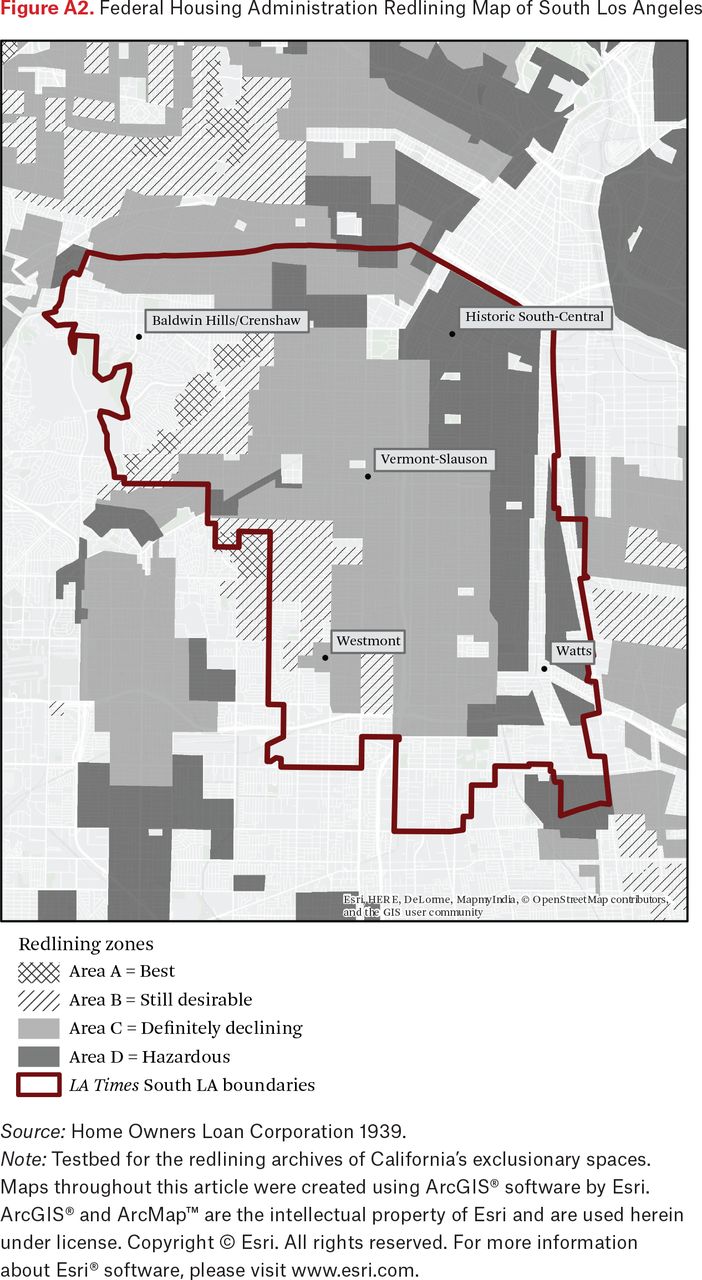

These patterns are not solely the results of demographic pressures. Both the Kerner and McCone reports explicitly state that the regulations of the Federal Housing Administration, such as redlining, were major factors in creating substandard housing conditions in South Los Angeles. Redlining practices emerged with the first wave of the Great Migration from the South to northern and western cities in the 1920s. They became institutionalized and systematically implemented in large cities through the initiative of a set of institutions of which the Home Owners’ Loan Corporation (HOLC) was the central player. At its height, the HOLC recruited and trained mortgage lenders, developers, and real estate appraisers in nearly 250 cities to create maps that color-coded credit worthiness and risk on neighborhood and metropolitan levels (for map and details, see figure A2 in the appendix). Among other things, these practices had long-term effects through the erection of high barriers to either investing in one’s neighborhood or moving out of neighborhoods deemed too risky (Dymski, Veitch, and White 1994). Redlining is no longer legal, but research shows that other nefarious practices have emerged, this time with the consequence of displacing many families (Pfeiffer et al. 2014; Berg 2017).11

Federal Housing Administration Redlining Map of South Los Angeles

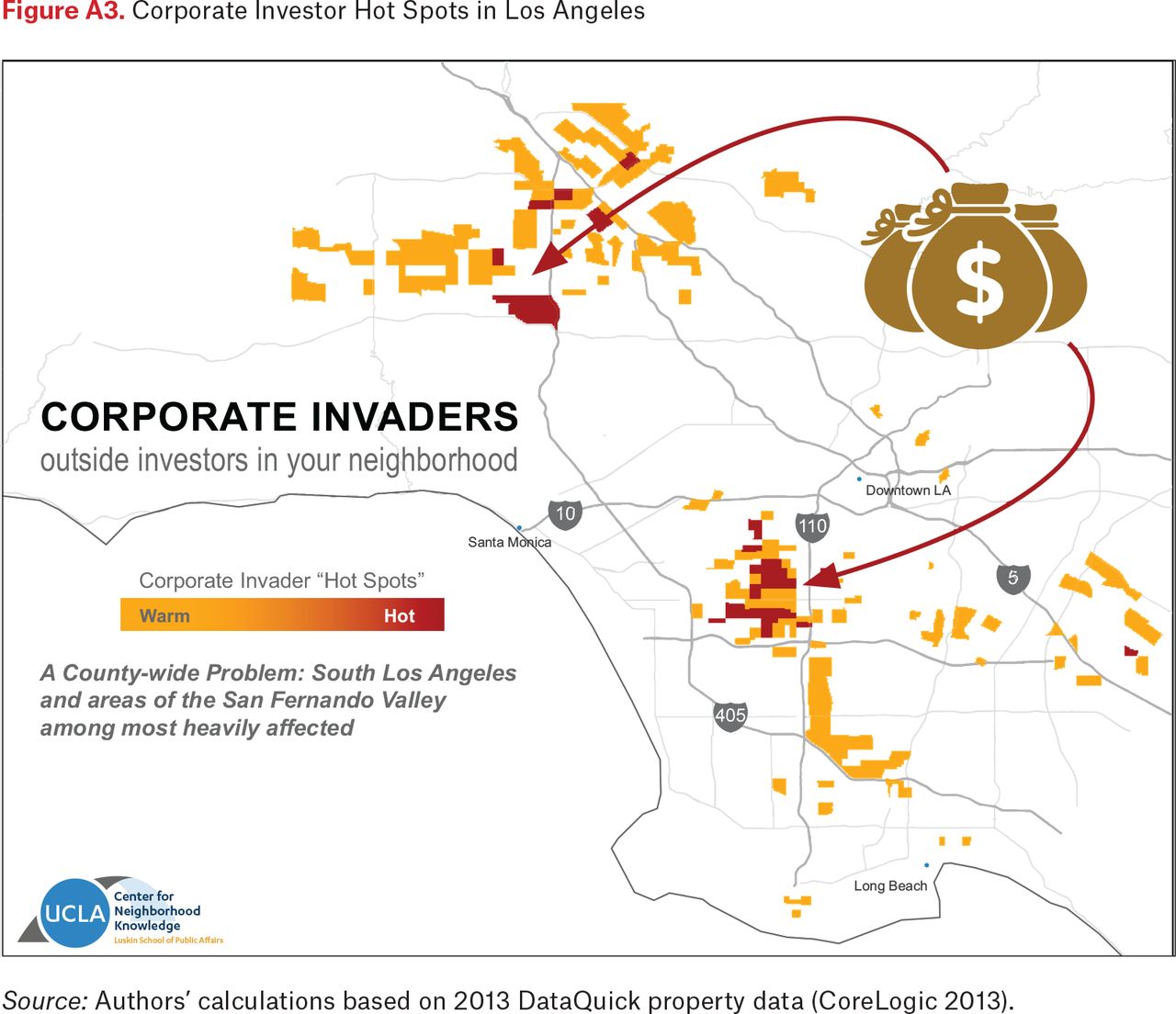

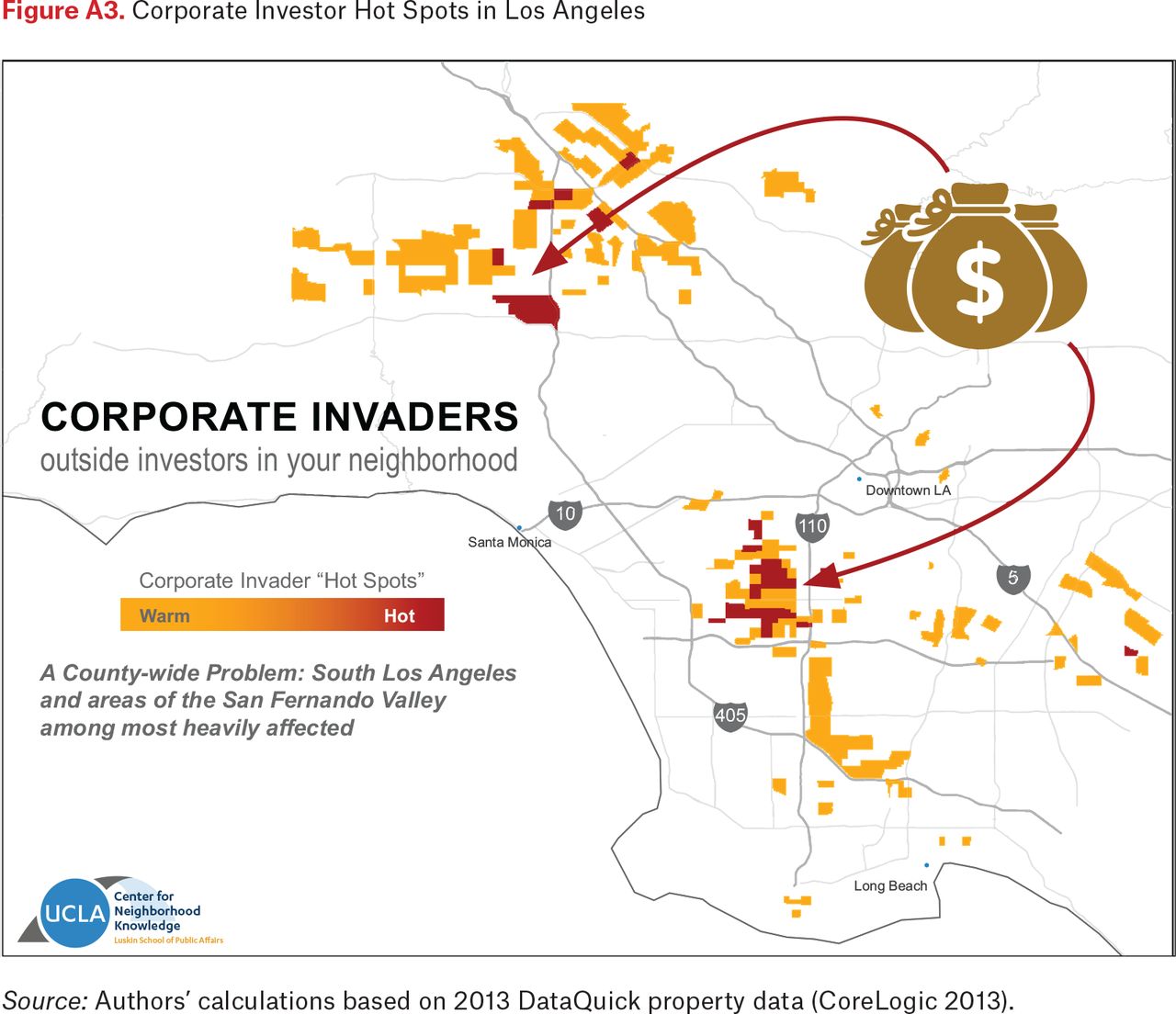

Corporate Investor Hot Spots in Los Angeles

Homeownership 1960, 1990, and 2015

Homeownership is a primary asset for most Americans with positive net worth. The federal tax code also provides incentives for homeownership by providing tax savings associated with mortgage interest deductions. Moreover, owning a home offers other benefits, such as access to a good public school district, convenient shops, and parks. Finally, fairly or unfairly, the purchase of a home and regular on-time mortgage payments leads to higher Fair, Isaac and Company (FICO) credit scores than families that regularly make on-time payments for rent.

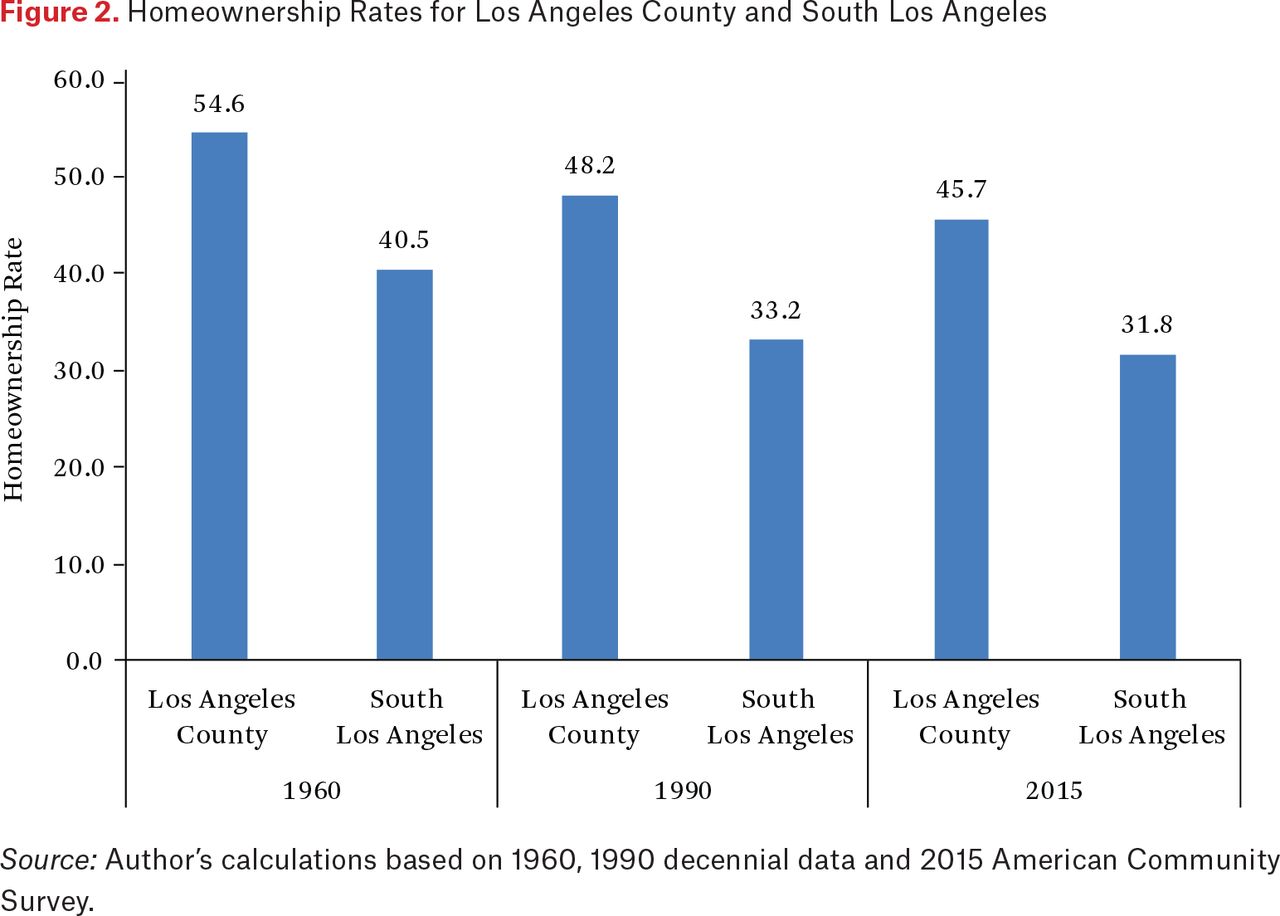

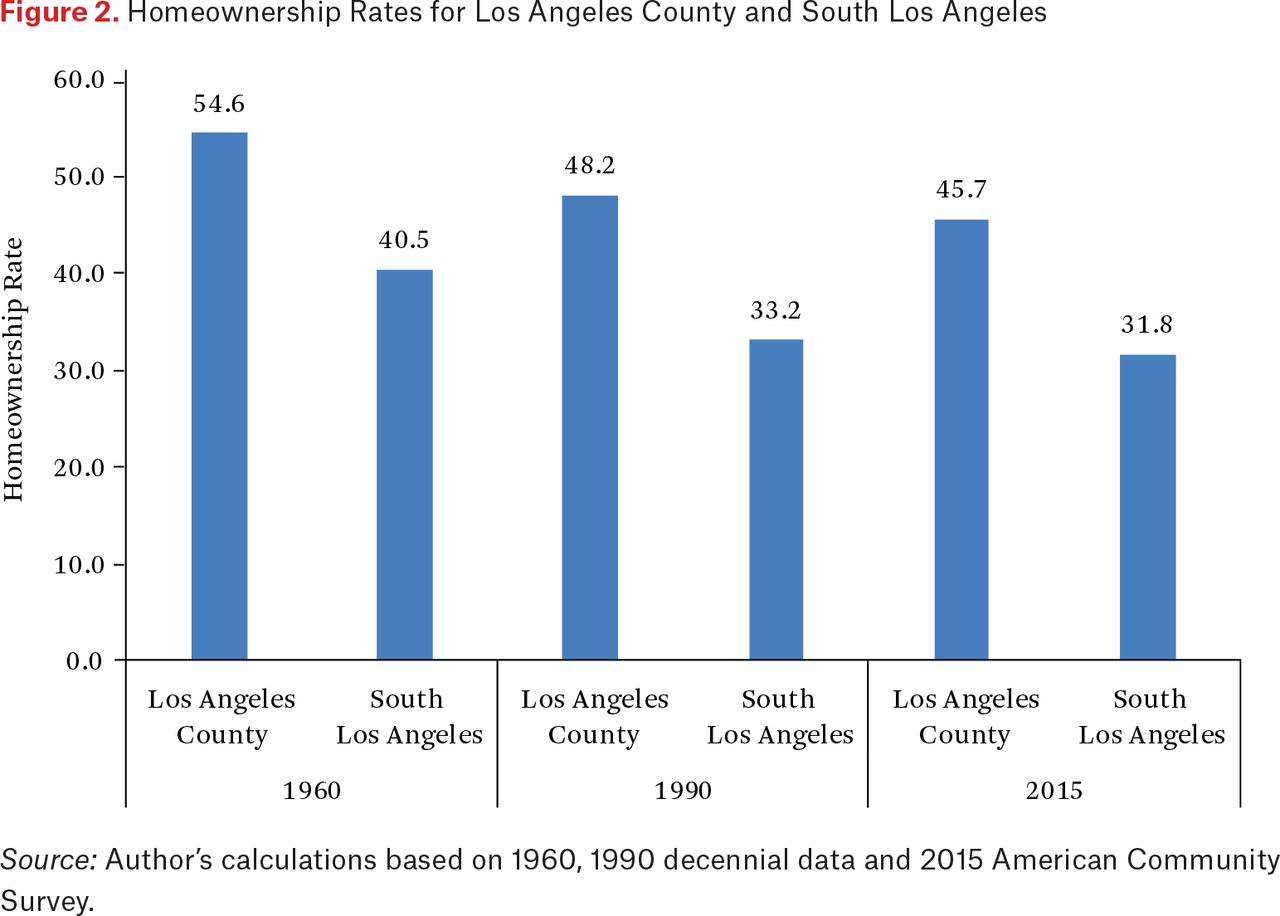

As figure 2 shows, homeownership rates in Los Angeles County have fallen from 55 percent in 1960 to 48 percent in 1990 and again to 46 percent in 2015. The rate in South Los Angeles ran parallel to the declining trend in Los Angeles County from 1960 to 2015. However, rates in South Los Angeles continually lagged behind county rates on average by 15 percentage points and did not reach parity over fifty years.

Homeownership Rates for Los Angeles County and South Los Angeles

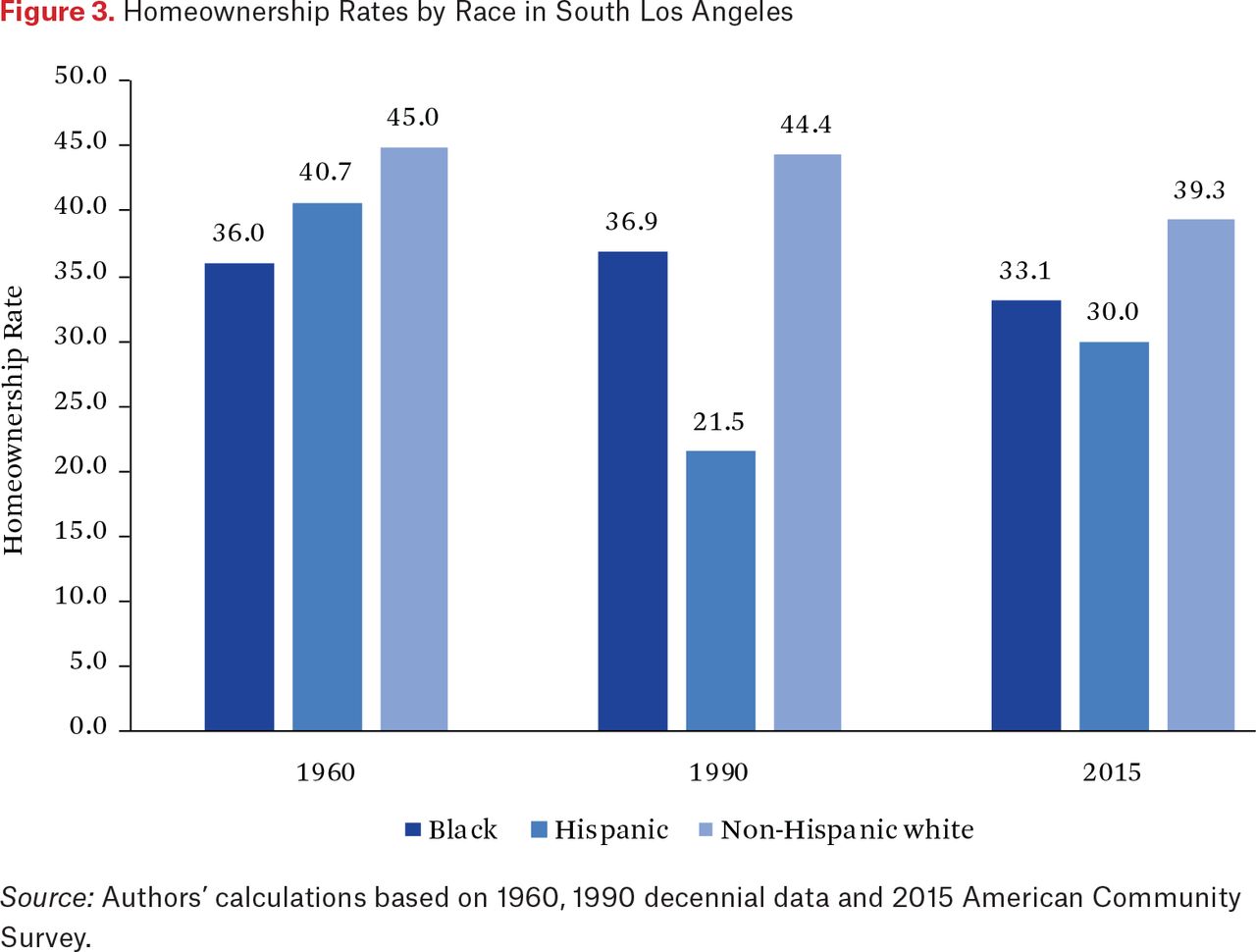

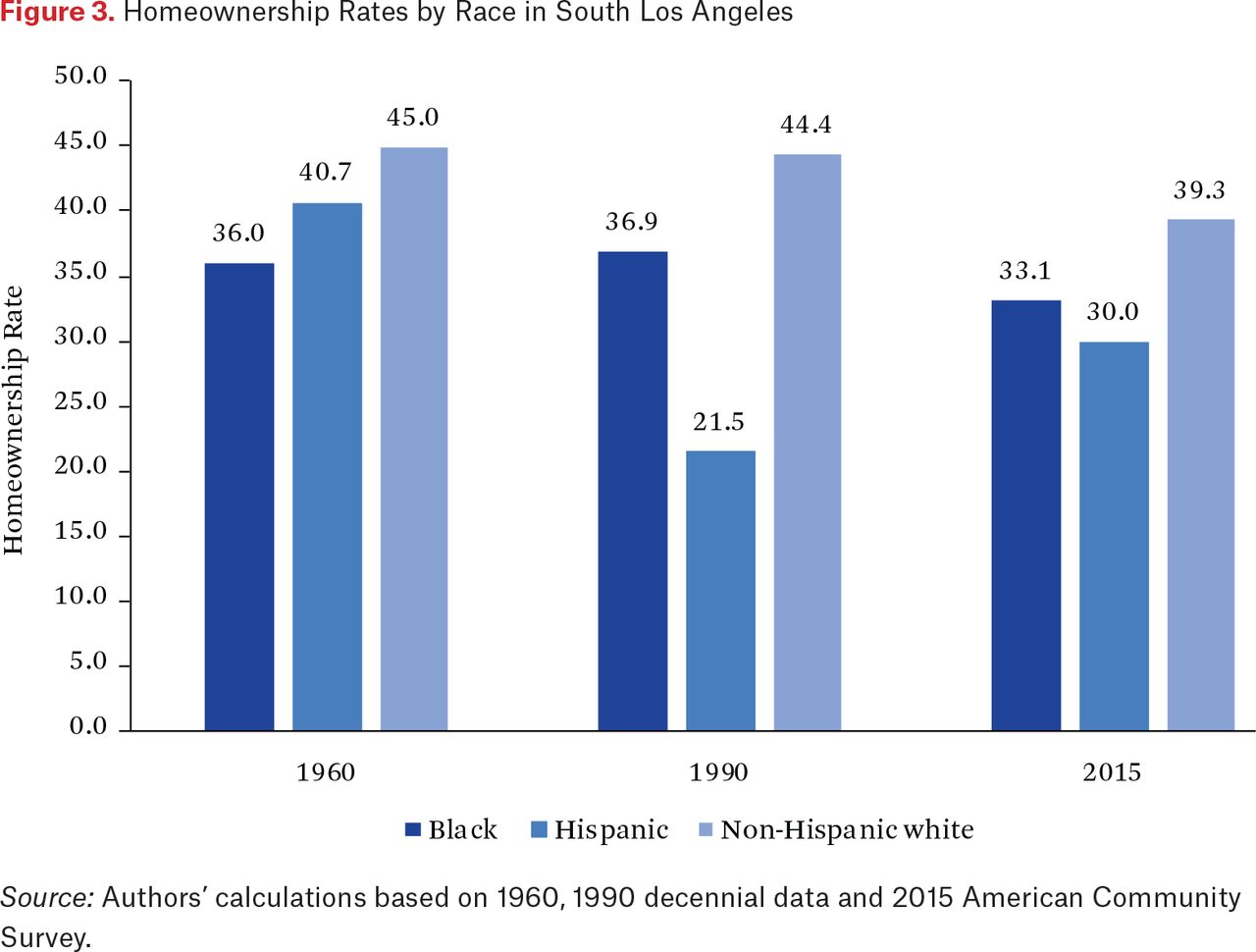

In 1960, the black homeownership rate (36 percent) was the lowest of all racial groups in South Los Angeles (figure 3). By 1990, the percentage of blacks who owned homes improved slightly, to 37 percent, the corresponding percentage of Hispanic population fell 19 points to 22 percent. In 2015, blacks (33 percent), by a slight margin, continued to have a higher homeownership rate than Hispanics (30 percent) in South LA. Across all periods, whites have the highest homeownership rates, though low by the national standard, dipping below 40 percent by 2015.

Homeownership Rates by Race in South Los Angeles

During this period, growth of the foreign-born population in all major racial and ethnic groups was significant, but increases were much higher among Asians and Hispanics. By the 1960s, 35 percent of the Asian population and 19 percent of the Hispanic population in Los Angeles County were foreign born (Ong et al. 2016). By the 1980s, these figures nearly doubled, to 62 percent of Asians and 45 percent of Hispanics (Ong et al. 2016). The share of black and white immigrants also increased, but from much lower levels and peaking in 2014 at 18 percent for whites and 7 percent for blacks (Ong et al. 2016).

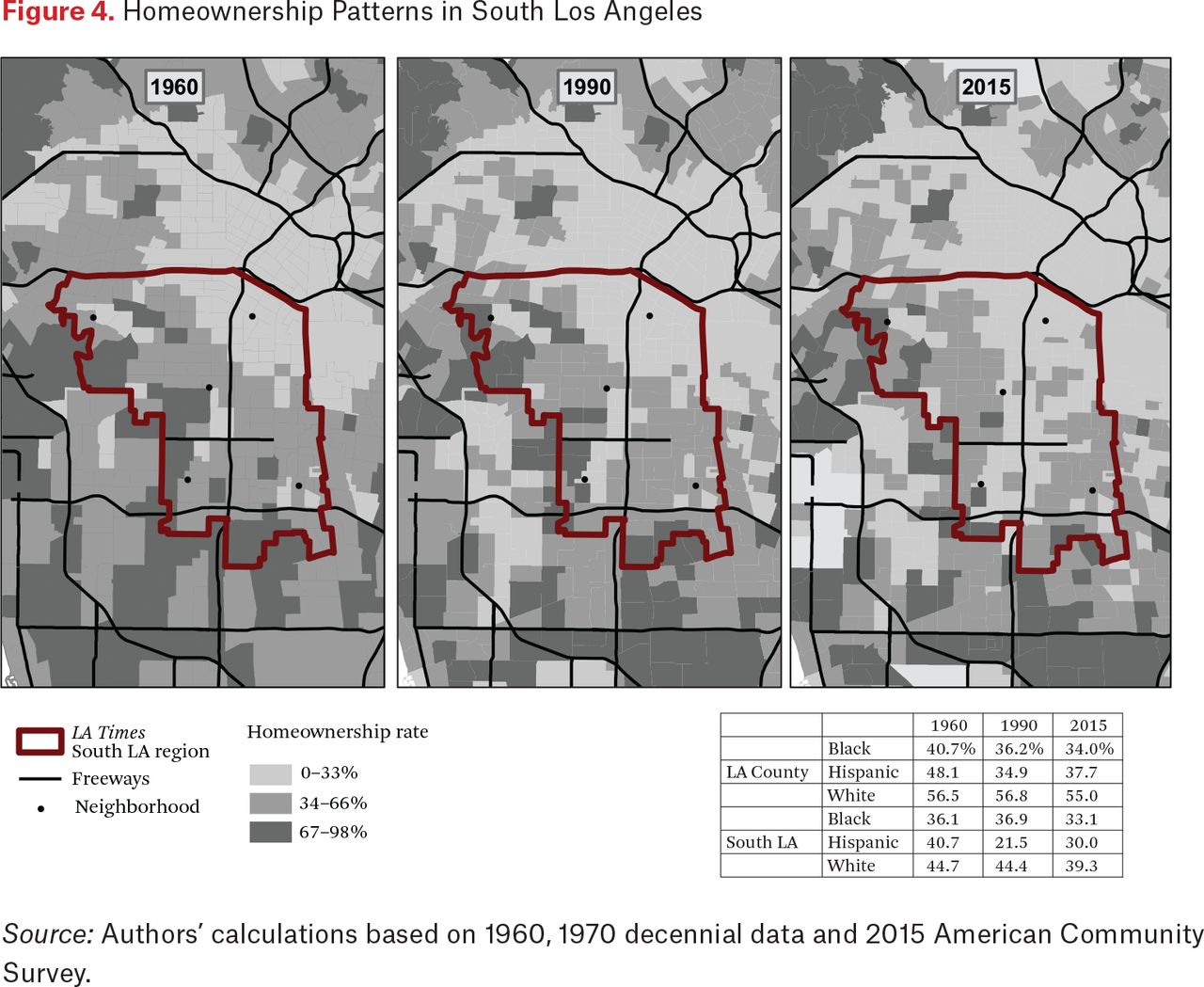

As seen in figure 4, the overall homeownership rates in South Los Angeles decreased over time, in particular the historic South-Central, Watts, and Westmont neighborhoods. In historic South-Central, a high percentage of tracts had homeownership rates between 26 percent and 50 percent in 1960. By 1990 and 2015, homeownership ranged between 0 percent and 25 percent in much of the area. In Watts, the majority of tracts had rates between 51 percent and 75 percent in 1960. By 1990, homeownership decreased to between 26 percent and 50 percent and remains the same in 2015. In Westmont, the largest share of tracts had rates between 51 percent and 75 percent in 1960. The proportion declined to between 26 percent and 50 percent in 1990 and to between 0 percent and 25 percent in 2015.

Homeownership Patterns in South Los Angeles

The foreclosure crisis contributed significantly to the patterns of homeownership in South Los Angeles by creating pockets of concentrated vacancies or rental conversions in distressed communities. Subprime lending increased for all racial groups, but blacks and Hispanics were much more likely than whites to receive higher-cost mortgages. In 2005, more than half of all loans to blacks and Hispanics were subprime, versus only 16 percent for whites. Moreover, black and Hispanic homebuyers were approximately 40 percent to 75 percent more likely than their white counterparts to receive high-risk loans during the 2005–2007 boom period. Throughout the 2007 to 2012 recession period, Hispanics had the highest rate of foreclosure (13 percent), followed by blacks (12 percent)—three times higher than that of whites (Ong, Pech, and Pfeiffer 2014). These trends for the greater Los Angeles region provide insights as to why homeownership rates in South Los Angeles dipped in 2015.

To measure the impact of some of these hard-to-measure factors specific to South Los Angeles, we ran a model of homeownership to control for life cycle, ethnoracial, education, and income variables on the likelihood of owning a home. We report the odds ratio to summarize the output (see table A2). In this case, the odds ratio is the odds that a household will own their home given that they live in South Los Angeles rather than the county, after controlling for all other variables. In other words, an odds ratio of one indicates no difference in the odds of owning in South Los Angeles and the county. A number higher or lower than one signifies that the odds of owning is higher or lower.

Odds Ratio Based on Output of Logit Regression

The gap in homeownership between South Los Angeles and the county remained fairly constant, fluctuating between 14 and 15 percentage points from 1960 to 2015. Over this half century, household attributes—particularly race, nativity, and income—are the key drivers of disparities in homeownership. However, the odds of owning a home correlated with residing in South Los Angeles have had a large and significant effect. In 1960, the ratio was 0.68, qualitatively lower than the rest of the county, ceteris paribus. This same number decreased to 0.65 in 1990 but increased to 0.89 in 2016. The role of South Los Angeles as a place has therefore decreased over time in that more of the gap is explained by the composition of the resident population.

Home Values, 1960, 1990, and 2015

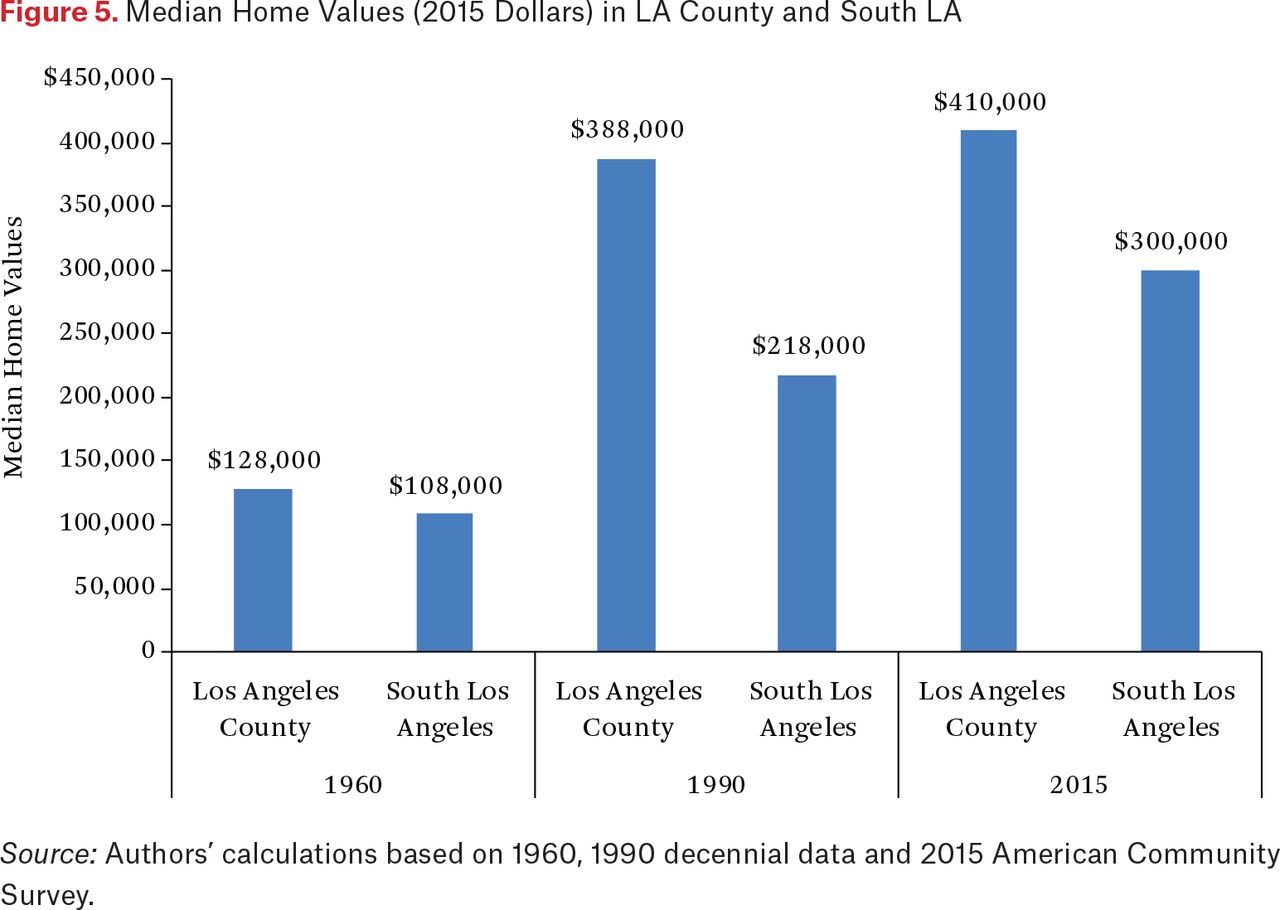

The county’s median home values adjusted to 2015 dollars have risen over time from $131,000 in 1960 to $383,000 in 1990 to $420,000 in 2015 (see figure 5).12 In contrast to the consistently low homeownership rate in South Los Angeles, the property value gap relative to the county closed from 1990 to 2015. This is in part due to an increase in values between 1990 and 2015 that far outpaced the county’s (South LA’s values increased by 60 percent against 10 percent for the county). However, despite this relative convergence, over the entire period South Los Angeles trails the county. In 1960, the gap in median home value between South Los Angeles and the county was about $20,000. By 1990, the gap had widened considerably to more than $190,000, making home values in South Los Angeles approximately half that of the county. In 2015, thanks to the convergence in values, the gap shrank to approximately $150,000.

Median Home Values (2015 Dollars) in LA County and South LA

The Los Angeles housing market experienced a robust recovery following the 2006 foreclosure crisis, and the concurrent lag in new construction has created a growing housing shortage. In this context, it is to be expected that South Los Angeles home values would increase faster since it has a concentration of relatively affordable homes in proximity to major job centers (downtown and El Segundo). However, this also means that home owners are not benefiting equally from home equity.

Home equity value is the main measure of the financial gains homeownership confers. Equity is the value of the home minus what is owed on the property. Therefore, for homeowners who own their home outright, the entire value of the property is their equity, and equity will continue to grow as property values rise. On the other hand, equity can be negative if owners owe more than the property is worth, a situation that became widespread during the 2006 crisis, leading to many people losing their entire wealth. In the early 2010s, black homeowners’ equity was only 54 percent of that of non-Hispanic white owners. Hispanic homeowners’ equity was only 45 percent of non-Hispanic white owners’; the statistics for Asians is only 66 percent of non-Hispanic white owners.

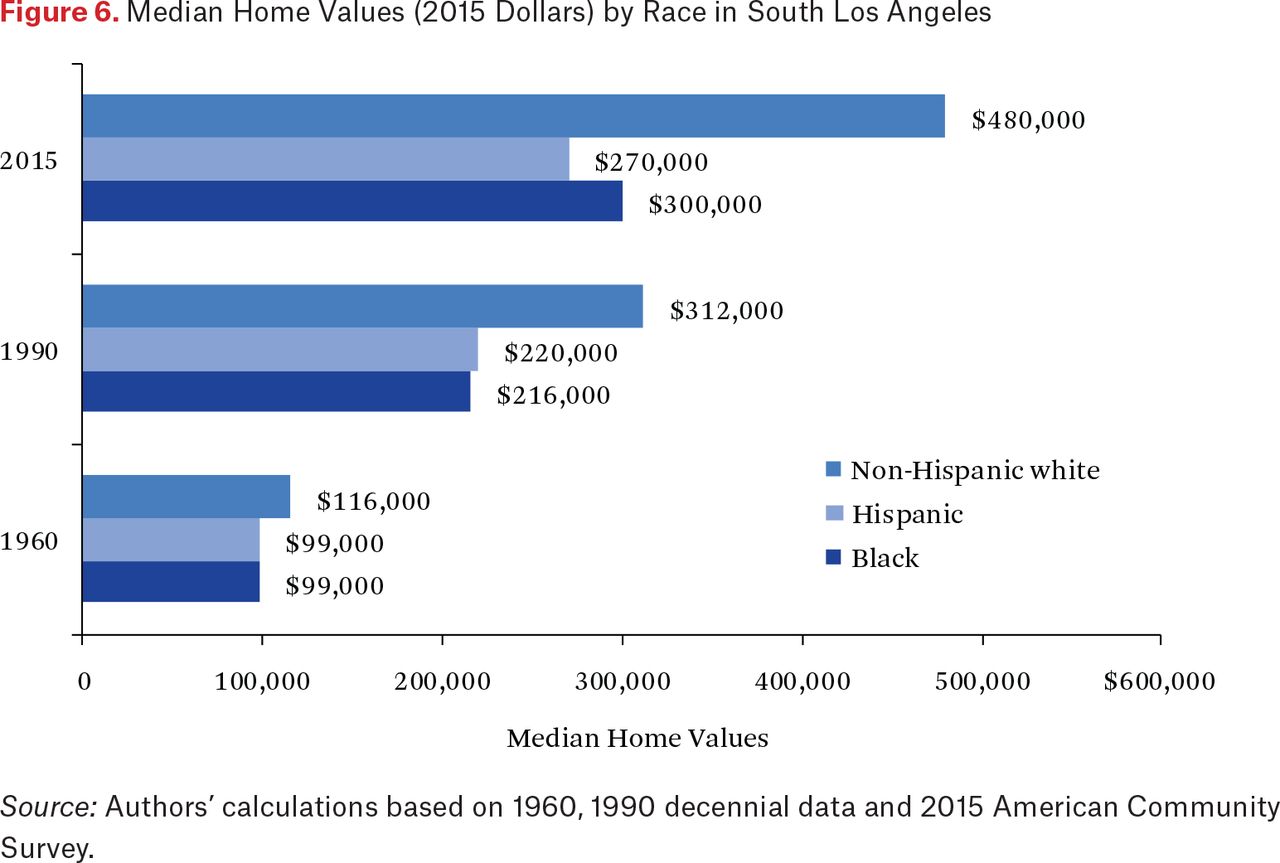

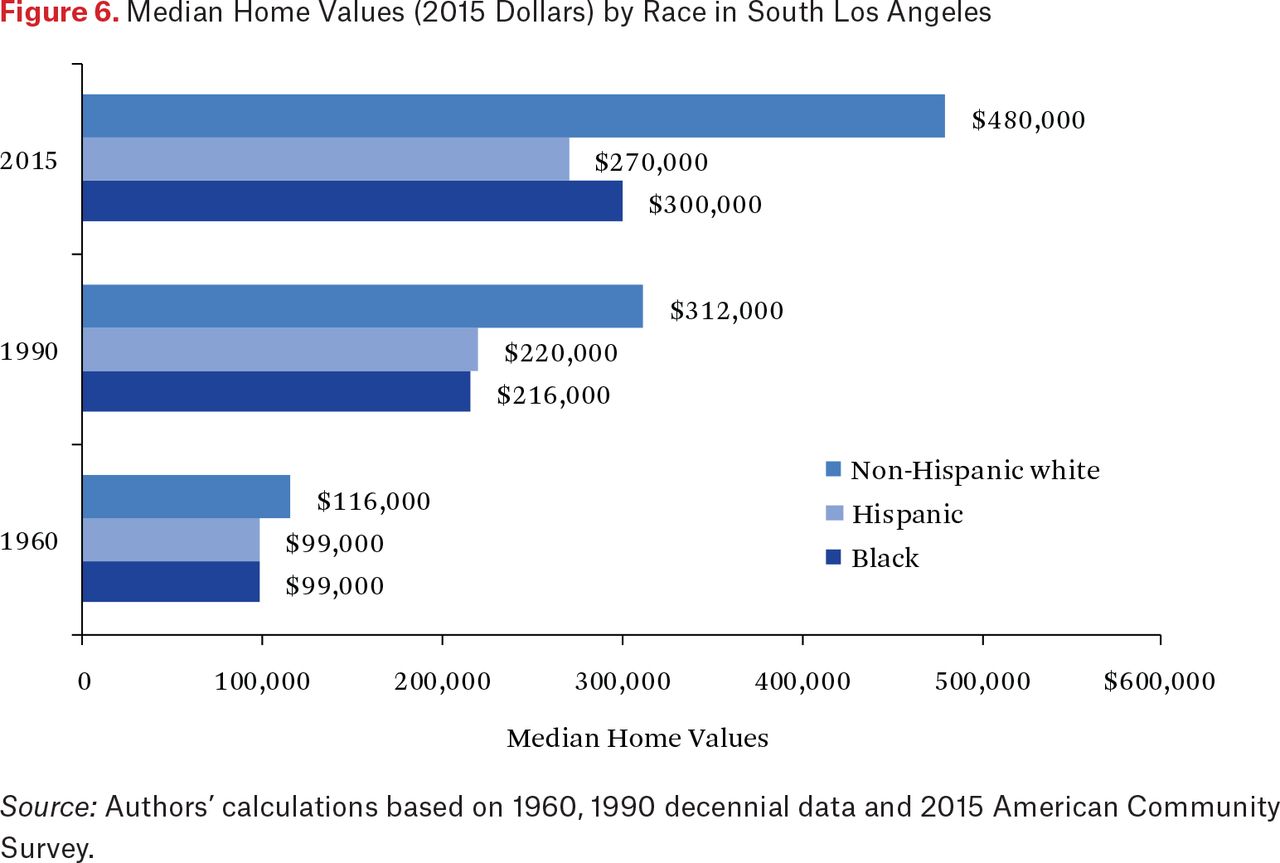

The combination of high barriers to achieving homeownership with lower home values creates stark disparities between nonwhite racial and ethnic groups and whites. Figure 6 demonstrates how the median home values of black households do not appreciate as greatly as those of white households in South Los Angeles. Median home value for blacks and whites was similar in 1960: $91,000 and $111,000 respectively. However, that $20,000 gap increased to $96,000 in 1990 and $150,000 in 2015. In light of the lower equity levels found, these housing disparities between communities of color and whites in Los Angeles are even starker than they appear.

Median Home Values (2015 Dollars) by Race in South Los Angeles

In terms of parity, the home value of blacks and Hispanics in South Los Angeles failed to catch up to whites in the county. For both groups, home values were about 80 percent of non-Hispanic whites’ home values in 1960, but by 2015 that figure had worsened to 67 percent for blacks and 58 percent for Hispanics. In contrast, non-Hispanic whites in South Los Angeles did not experience a relative decline compared with non-Hispanic whites in the county.

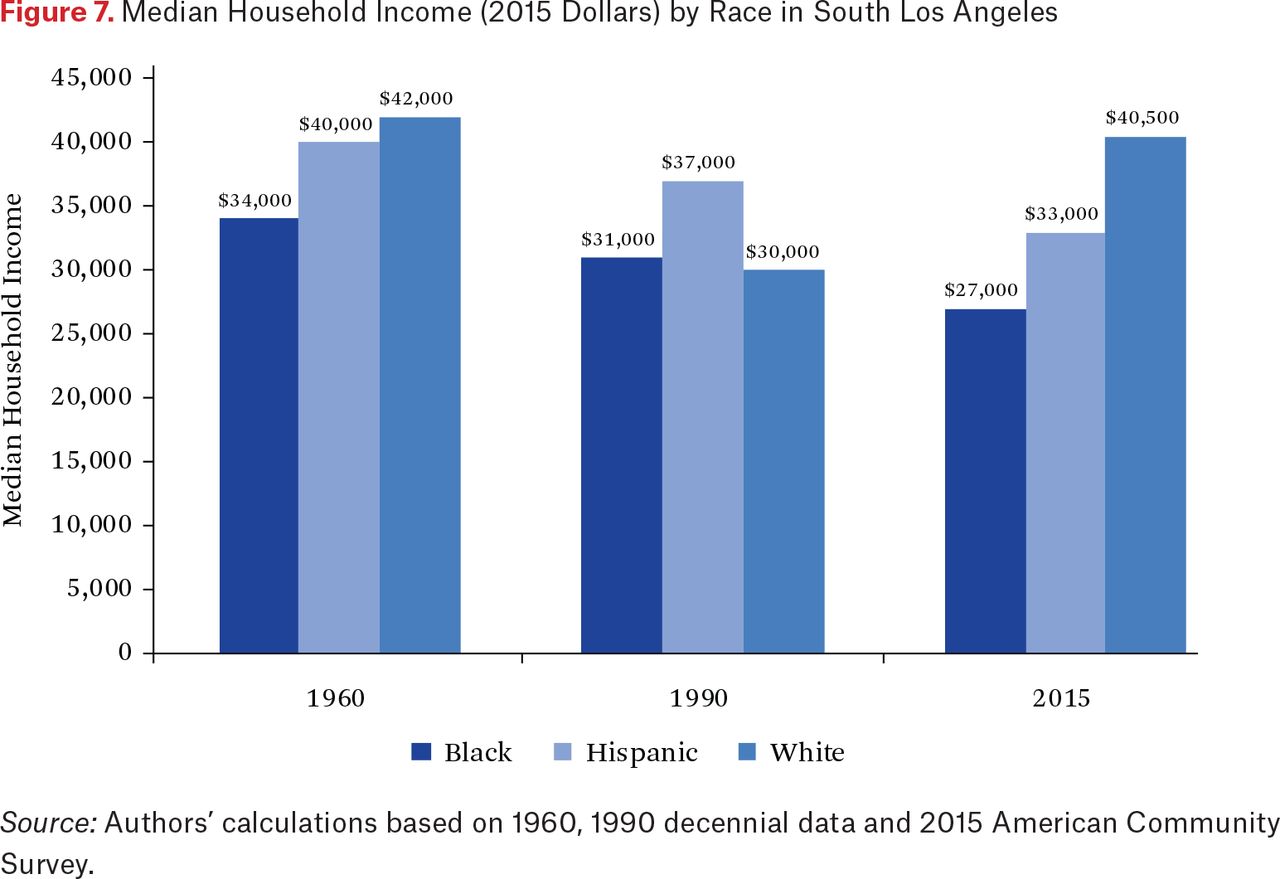

Median income trends help explain why the homeownership rate is low in South LA. Households with limited income are unable to afford a mortgage, among many other high housing costs, and are more likely to be renters. Given the regional trends in housing, rents have also increased, putting an ever-growing number of households under severe housing burdens and locking them into not only renting but also renting in locations that may not be optimal for accessing jobs and educational opportunities. Figure 7 shows the median income adjusted to 2015 constant dollars for blacks in South Los Angeles and how it decreases over time. Given that housing costs have clearly outstripped inflation in Los Angeles, the median household income decrease of $7,000 understates the magnitude of the increasing demands housing puts on households. We see an even more pronounced trend among Hispanics whose median income decreases by $11,000 over the half century. This is not a common trend. Although the drop in median income for whites between 1960 and 1990 is consistent with the trend for the area, by 2015 whites’ incomes recovered to levels $5,000 or higher than in 1960.

Median Household Income (2015 Dollars) by Race in South Los Angeles

In addition, South Los Angeles became a hot spot of speculative real estate investments in the wake to the 2006 crisis. A disproportionate number of units have been bought up by corporate investors, such as Blackstone developers (see figure A3), adding to the pressure on home prices. Many of these units are being renovated and turned into luxury housing. Moreover, neighborhood upscaling spillover effects from the new University of Southern California village housing and commercial development, the new Los Angeles Stadium at Hollywood Park in Inglewood, and the renovation of Crenshaw Plaza with a new transit station are driving gentrification in South Los Angeles, making the prospects of a more accessible housing market all the fainter.

WHAT WORKED AND WHAT DID NOT WORK

As we reflect on the findings from the Kerner Commission report, we focus on racial wealth inequality through the lens of homeownership and the role of place by studying South Los Angeles, where the 1965 Watts riots took place. Through our research, we fill the gap within the existing literature by examining how housing influences wealth building, a clear component missing in the recommendations from both the Kerner and McCone reports. The two commission reports failed to adequately address the paramount pathway toward economic security via wealth accumulation including homeownership. Mainly, the recommendations focused on increasing the supply of affordable rentals. This is a policy failure that perpetuates wealth inequality. Both reports document poor housing conditions and high housing burden as underlying causal factors, but both focused on the rental sector. The solutions were to increase good and affordable rental units, but by and large ignore homeownership. In a sense, this silence means implicitly perpetuating the lack of asset building through remedial policy, thus the reproduction of wealth inequality. The housing recommendations dealt with some symptoms but not the deeper roots of racial economic inequality.

Another issue largely missed by both the Kerner and McCone reports was the increasing racial complexity in Los Angeles that was so nascent at the time of the release of the Kerner and McCone reports. The 1968 Chicano Blowouts and the 1992 Rodney King riots are examples of shifting demographics that challenged the black and white relations binary. These changes are embedded in the demographic shift in South LA, again something that the two commissions did not foresee. Thus, the two reports lacked the ability to predict the evolving nature of racial inequality in Los Angeles.

However, the current state of South Los Angeles is a mixed picture. The median home value data suggest an uptick in the area. This is a positive development because it may increase a homeowner’s equity and allow them to gain wealth over time, but only for a minority of the households, and, as this article demonstrates, home value appreciation rates are not equally shared across racial and ethnic groups both across and within neighborhoods. Nonetheless, overwhelmingly, renters are missing out on gains across the board. If this is the case, policymakers, advocates, and community leaders must develop new ideas on what can be done to increase homeownership opportunities and build wealth.

Overall, Los Angeles has failed to remedy the housing problem in South Los Angeles despite the recommendations and political promises. If the high cost of housing (for example, higher rents and home prices) and neighborhood upscaling continue to drive gentrification and displacement, Los Angeles may be headed into a new round of problems given growing economic inequality and declining housing affordability. The demographics may have changed dramatically, but South Los Angeles remains at the margins of the economy, as well as society.

WHAT ARE THE IMPLICATIONS FOR THE TWENTY-FIRST CENTURY

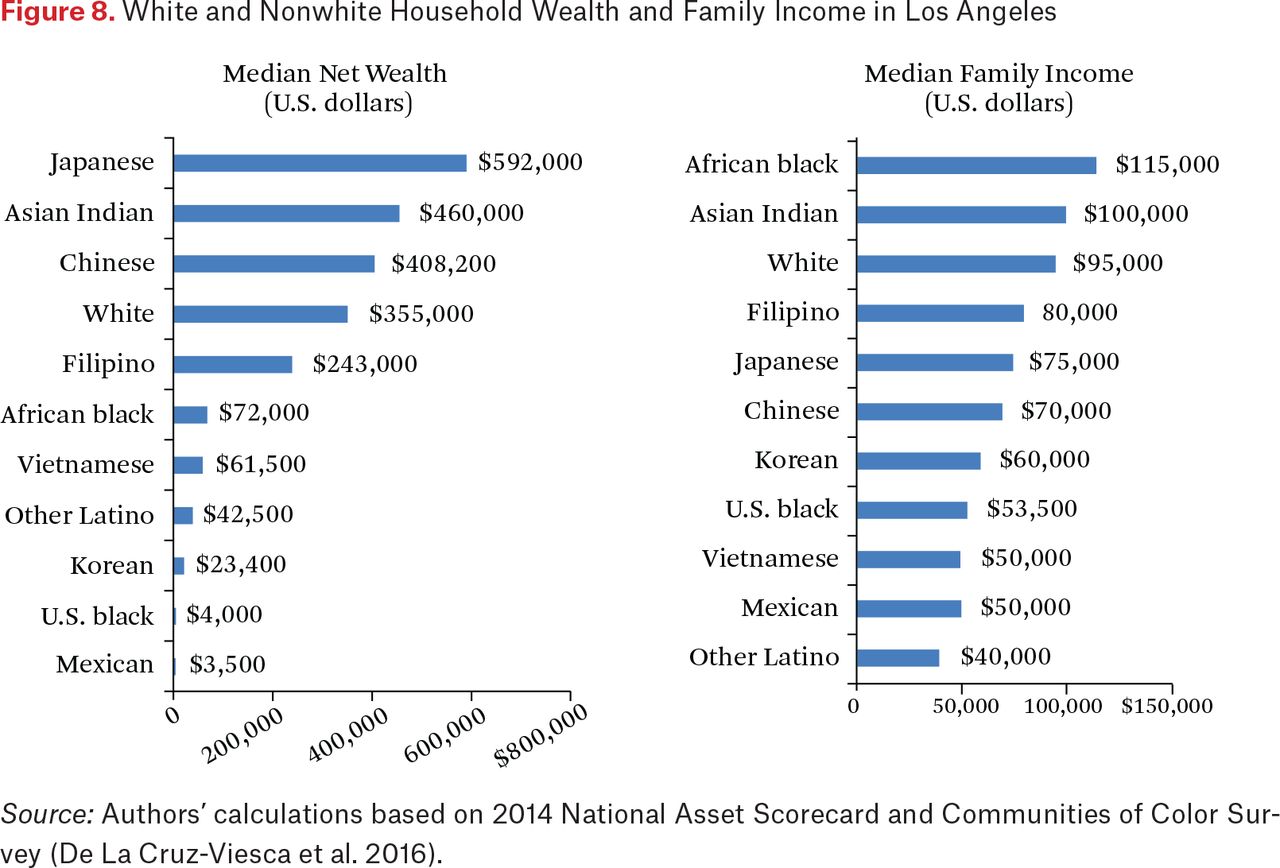

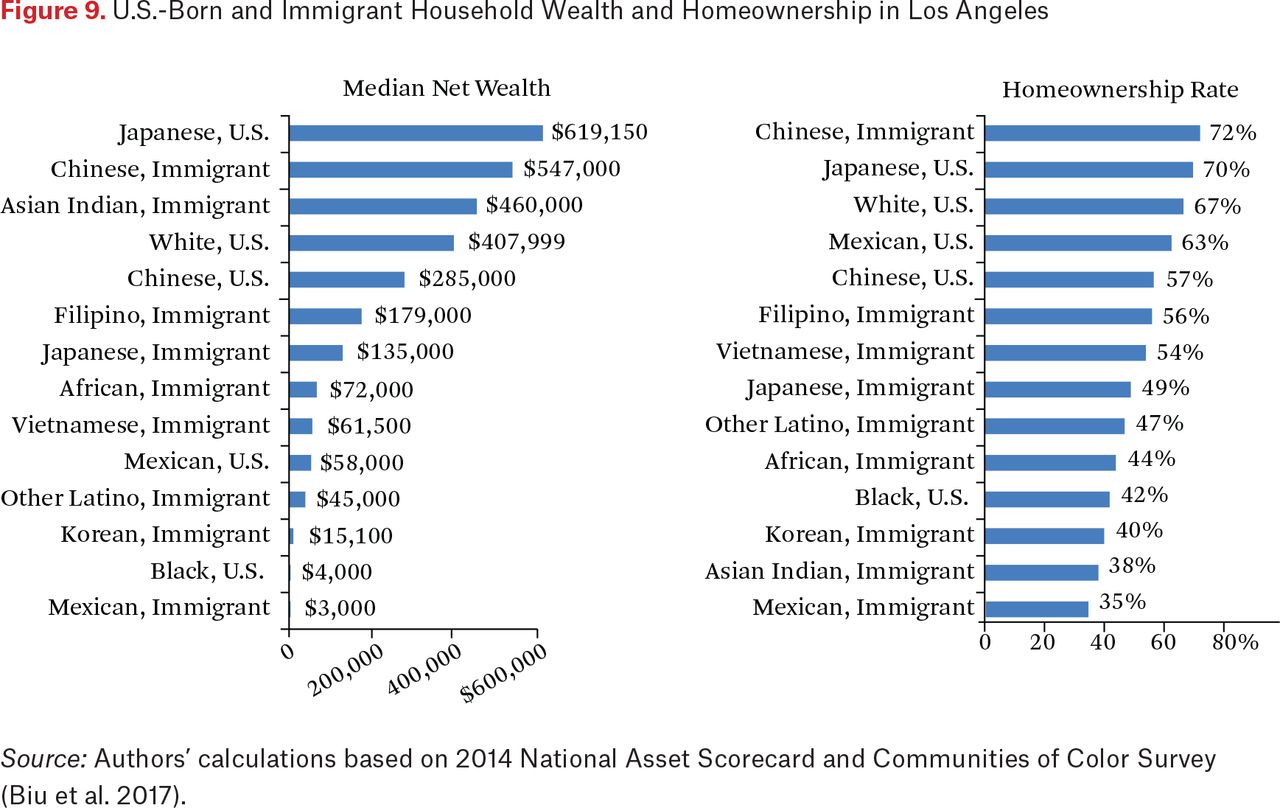

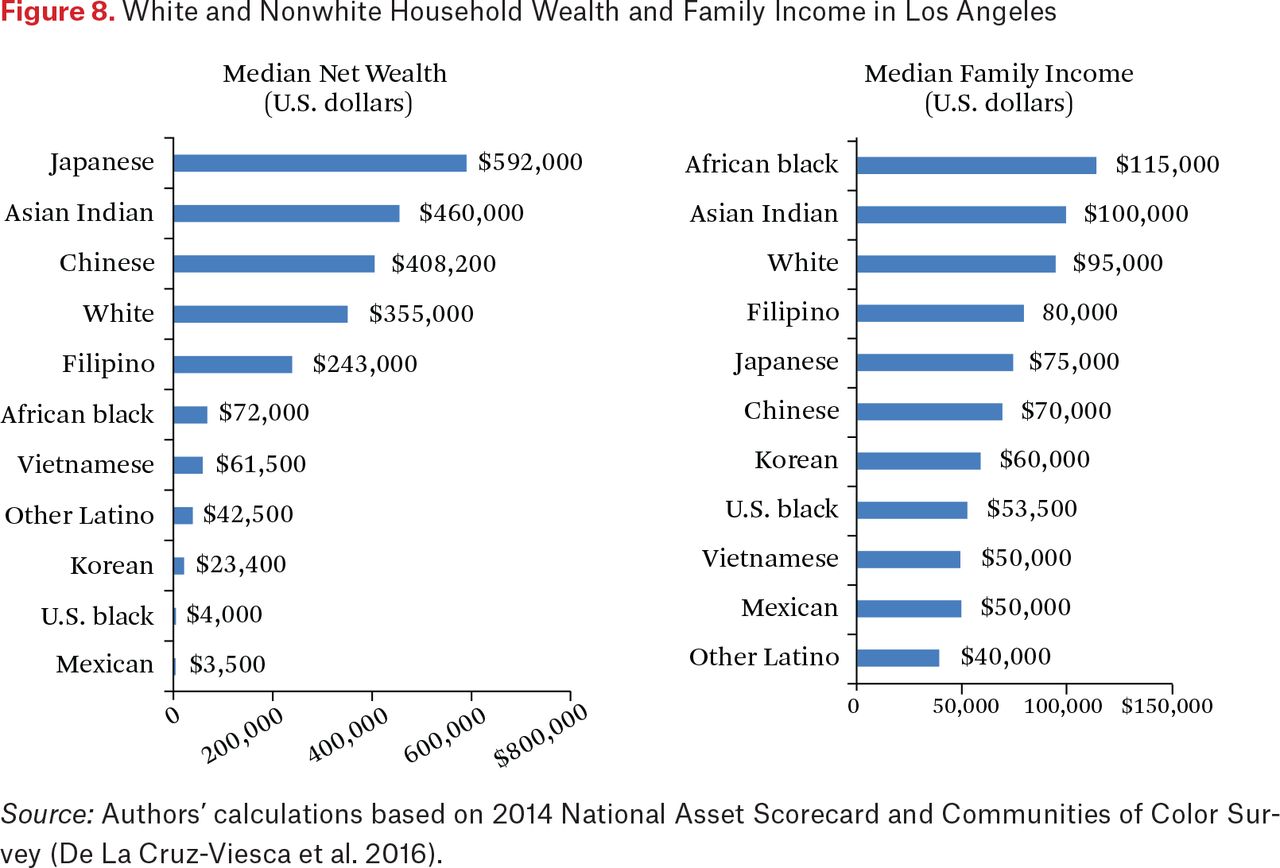

Wealth is derived from taking the total market value of all physical and intangible assets owned, then subtracting all debts. Although homeownership is a primary asset for the majority of Americans with positive net worth, it is not a driver of wealth. Data from the National Asset Scorecard and Communities of Color (NASCC) collected in 2014 found that one of the wealthiest ethnic groups in Los Angeles, Asian Indians, have a lower rate of homeownership than blacks—whose low level of wealth indicates a population overwhelmingly reliant upon income (De La Cruz-Viesca et al. 2016). As figure 8 shows, the median net worth for Asian Indians is $460,000 in contrast with $4,000 for non-immigrant blacks in Los Angeles and homeownership rates are 40 percent and 42 percent, respectively (De La Cruz-Viesca et al. 2016). The median net wealth of Asian Indians is most likely attributed to higher incomes, stock ownership, and savings. Thus, not all high wealth racial groups are homeowners. Wealth is also derived from assets such as intergenerational wealth transfers, savings, stocks, and retirement.

White and Nonwhite Household Wealth and Family Income in Los Angeles

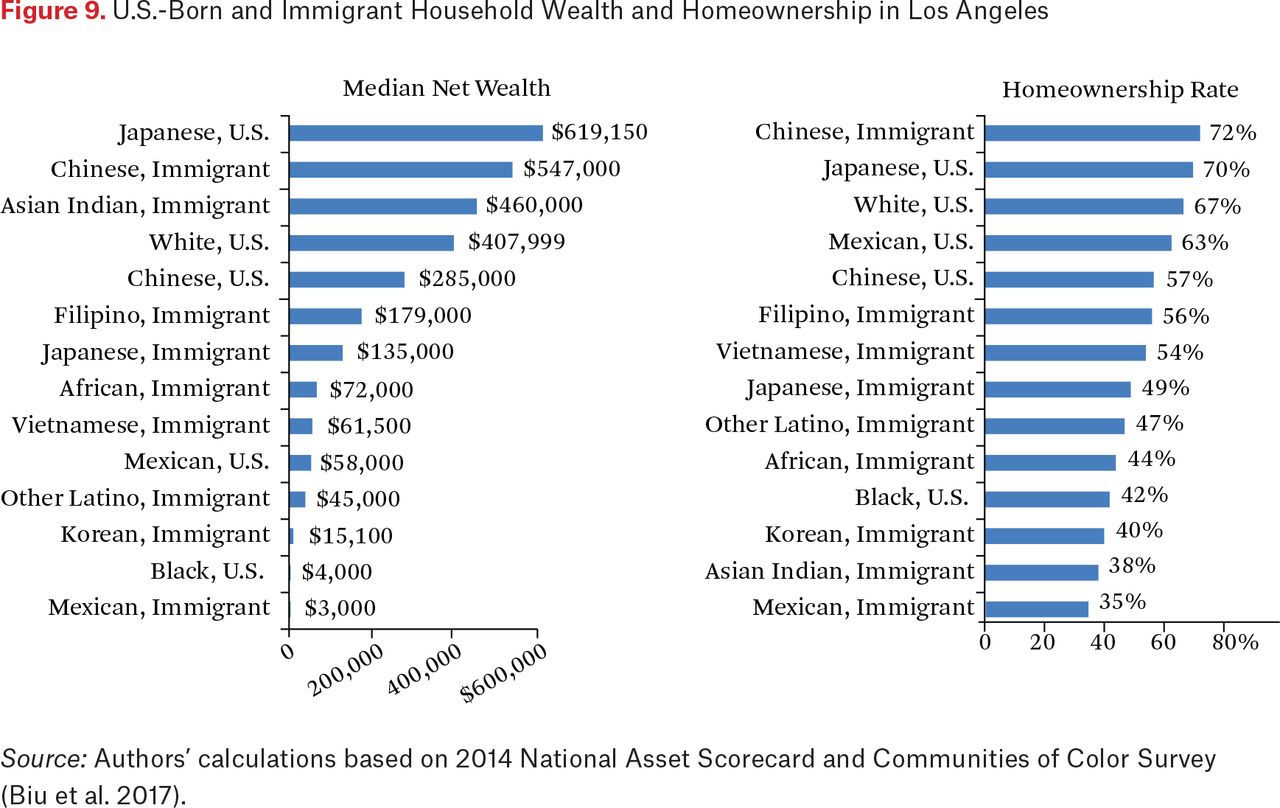

Moreover, when we examine differences by nativity, a more nuanced picture emerges. NASCC data revealed that for the Los Angeles metro area, the median wealth for African immigrants is $72,000. Figure 9 shows the median wealth for Mexican immigrants is $3000 compared with $58,000 for U.S.-born Mexicans (Biu et al. 2017). Even more noteworthy is the difference in homeownership rates between Mexican immigrants (35 percent) and U.S.-born Mexicans (63 percent) (Biu et al. 2017). The NASCC data sheds light on within-group differences by nativity and ethnicity and demonstrates the great diversity that exists within each racial group.

U.S.-Born and Immigrant Household Wealth and Homeownership in Los Angeles

Also, the socioeconomic status of immigrants prior to entering the United States plays an important role in influencing the wealth position of particular groups. The majority of immigrants who arrived after the passage of the 1965 Immigration Act are highly educated, possess higher levels of wealth than the average American, and are highly skilled professionals who are more likely to hold jobs with higher earnings levels (Lee and Zhou 2015). Thus, the selectivity status of immigrants to Los Angeles has vital implications for how they are able to accumulate assets over time, especially relative to primarily native-born populations. It is critical to understand how the nature of inequality has been transformed by immigration and the overall growth of income and wealth inequality.

Furthermore, one study has shown that income differences are only a small fraction in producing ethnoracial residential segregation and that segregation is largely driven by ethnic and racial differences (Ong et al. 2016). Though most social scientists point to individual prejudices and structural racism, others counter that segregation is a mere byproduct of systematic economic differences. For example, some minority groups are poorer and thus disproportionately concentrated in low-income neighborhoods. The Ong report indicates that although black-white segregation has been decreasing steadily in Los Angeles, segregation levels remain high while increasing between Hispanics and non-Hispanic whites (2016).13 Nonetheless, we observe evidence that even in the same neighborhoods, black and Hispanic homeownership rates, home values, and appreciation rates are lower than among their white neighbors.

The findings provide us with a better understanding of what might influence racial wealth disparities. A review of the economic literature demonstrates that inheritances, bequests, and intrafamily transfers also account for more of the racial wealth divide than any other demographic and socioeconomic indicators, including education, income, and household structure (Hamilton and Chiteji 2013; see also, for example, Blau and Graham 1990; Menchik and Jianakoplos 1997; Conley 1999; Charles and Hurst 2003; Gittleman and Wolff 2007). Thus, it is important to understand the racial differences in resource transfers across generations.

It is beyond the scope of this article to identify the causal mechanisms influencing racial wealth disparity in Los Angeles, but the findings outlined in this paper do help us identify potential factors influencing wealth accumulation. As discussed earlier, people of color were excluded from post-Depression and World War II (1939–45) policies that were largely responsible for the asset development of an American middle class (for example, racially discriminatory local implementation of FHA loans and G.I. Bill benefits; see Katznelson 2005; Lui et al. 2005; Oliver and Shapiro 2006). Thus, explanations that attribute the lack of assets among minority groups to a relative deficiency in current savings behaviors are at the very least an oversimplification the problem.14

The staggering disparities identified in this analysis should urge us to find policies that can help narrow racial wealth inequality by providing opportunities for asset development; ensuring fair access to housing, credit, and financial services; ensuring equal opportunity to well-paying jobs regardless of race or ethnicity; strengthening retirement incomes; promoting access to education without overburdening individuals with debt; and providing access to health care while helping minimize medical debt.15 All policies aimed at bridging the wealth gap also should consider the wide diversity among nonwhite populations and be targeted or adapted accordingly. Policy solutions are complex and need to use a multifaceted approach that includes input from practitioners who are familiar with the unique needs and challenges that different communities of color face.

We also need to broaden the analysis of how transnational capital has affected household assets. For example, the importance of remittances for many immigrants inhibits their ability to save or accumulate assets in the United States or abroad. The Alliance for Stabilizing Our Communities found that about 22 percent of low- and moderate-income Asian American and Pacific Islander survey respondents used remittances or wire transfers—a rate slightly higher than the 17 percent of Latinos (2014). Moreover, some studies have shown that the Philippines, Tonga, Samoa, and Fiji islands depend on remittances, where family members are identified to work abroad so as to increase economic returns for the family (Brown, Connell, and Jimenez-Soto 2014). However, there are few studies that focus on how remitters in America are impacted in their ability to build assets either in the United States or abroad.

Finally, this analysis highlights the importance of collecting wealth data at the local level, including disaggregated information for specific national origin groups. Having access to this type of data is an important step to help shape policymakers’, practitioners’, and foundations’ responses to the enormous challenges communities of color experience across the country. Wealth is perhaps more important than income in better understanding economic inequality, and wealth is critical in ensuring financial security and opportunity for future American families.

More needs to be done to ensure that the diverse voices of nonwhite groups are included in public debates and to understand the reasons behind the enormous differences uncovered in this analysis. More than ever, it is important to include data and analysis of indigenous and communities of color that are often overlooked in traditional studies in the development of a more inclusive, fair, and comprehensive narrative about racial inequality and financial justice in America.

APPENDIX

In this section, we define key terms and technical documentation about the data used in this article. The variables are analyzed at the individual level for the entire sample.

Race and ethnicity. The questions asked about race and ethnicity changed across the decades we examine (1960, 1990, and 2015) leading to some discrepancies in definition. In 1960, the question that comes closest to the later definition of Hispanic relates to whether the respondents have a Spanish surname. In later decades, the question about self-identified Hispanic origin is used. Asian respondents in 1960 are identified by the categories Japanese, Chinese, and Filipino. Later decades are both more comprehensive and consistent in their definition. In 1960, the share of respondents that were not black, white, or Asian was extremely small and is included with the white population.

Household variable. For household variables, data for all respondents belonging to the same unit are aggregated. This is of particular relevance in 1960 when no household income variable existed. In that case, the incomes of individuals belonging to the same household were added up to obtain the household value. In summarizing household data by race and ethnicity, no information regarding who owns the home is available. Therefore, following Collins and Margo (2003), we assume that the home belongs to the head of household and his or her race and ethnicity to subset the data.

Property values. The data reported in this section suffer a number of limitations due to differences in how property values were reported in 1960, 1990, and 2015. The main difference is that the 1960 and 1990 data are reported as ordinal data where each household belongs to a bin with a range of values. In contrast, the 2015 data are reported as a continuous variable. As such, the values in 1960 and 1990 correspond to the midpoint of the bin within which the median household falls.

Home values are reported differently in 1960, 1990, and 2015. In all three surveys, the values were self-reported. This is a common issue about which evidence is contradictory as to the potential bias, but not much can be done to mitigate it. The main difference comes from the format of the data. In 1960, home values were coded into ten bins with ranges of $2,500 (about $20,000 in 2015 dollars) between $5,000 and $20,000. Then, $20,000 to $24,900, $25,000 to $34,900, and more than $35,000. In 1990, there were twenty-five bins starting with less than $10,000 as its lowest value. The values increase in $5,000 (a little less than $9,000 in 2015) increments up to $80,000. Then, $10,000 increments up to $100,000; $25,000 increments up to $200,000; $50,000 increments up to $300,000. The last two are $300,000 to $399,999 and $400,000 and more. In 2015, the data are continuous but granular in that values tend to be rounded and recur at relatively high frequency.

In handling the 1960 and 1990 data, we assign the midpoint of the bin within which the household falls to calculate the median values. For example, a household falling in the bin $100,000 to $124,999 in 1990 would be assigned the value $112,500. This method has limitations given that the ranges can be quite wide. However, no alternative data sources that would allow us to replicate this analysis with greater accuracy are available. As an alternative, we fitted the data to parametric functions and found that the results were close to those obtained with the simpler estimation based on midpoints.

However, in interpreting the values we provide, rather than the single value we provide for clarity and simplicity, median home values fall within the range of the bin containing that value. To use the same example, if the median home value in 1990 were $112,500, this value should be interpreted as the median falling between $100,000 and $125,000.

Home equity. The American Housing Survey (AHS) is funded by the U.S. Department of Housing and Urban Development and conducted by the U.S. Census Bureau. Collected every two years, the AHS is a national longitudinal survey that collects very detailed information on housing units and their occupants. The AHS is a reliable data source to examine housing assets because it includes questions on home ownership, total mortgage, home value, and basic demographic information such as age, race, and place of birth.

FOOTNOTES

↵1 A commission under California Governor Pat Brown, headed by former CIA director John A. McCone and thus known as the McCone Commission, investigated the Watts–Los Angeles riots. On December 2, 1965, it released a 101-page report titled Violence in the City—An End or a Beginning? (McCone and Christopher 1965).

↵2 The attack on Chinese was the single largest racially motivated mass lynching in the United States (Johnson 2011). The Zoot Suit riots, a series of racial attacks on primarily Mexican youth by American military servicemen, occurred during World War II, when many migrants arrived for the defense effort and newly assigned servicemen engulfed the city.

↵3 The race of the thirty-four individuals killed is not identified in either the McCone or the Kerner report.

↵4 Although specific grievances varied from city to city, at least twelve deeply held grievances were identified and ranked into three levels of relative intensity. The first level of intensity consisted of police practices, unemployment and underemployment, and inadequate housing. The second level of intensity comprised inadequate education, poor recreation facilities and programs, ineffectiveness of the political structure and grievance mechanisms. The third level included disrespectful white attitudes, discriminatory administration of justice, inadequacy of federal programs, inadequacy of municipal services, discriminatory consumer and credit practices, and inadequate welfare programs.

↵5 The McCone Commission urged the immediate creation of a city human relations commission to develop comprehensive educational programs designed to enlist the cooperation of all groups, both public and private, in eliminating prejudice and discrimination in employment housing, education, and public accommodations.

↵6 On April 29, a trial jury acquitted four white officers of the Los Angeles Police Department of the use of excessive force in the videotaped arrest and beating of an African American, Rodney King. In response, South-Central Los Angeles was once again a site of protest, where protestors blocked freeway traffic and beat motorists, wrecked and looted numerous downtown stores and buildings, and set more than one hundred fires. The three days of rioting killed more than sixty people, injured almost two thousand, led to seven thousand arrests, and caused nearly $1 billion in property damage, including the burnings of more than three thousand buildings (Crogin 2002; Thomas 2016).

↵7 The East Los Angeles Walkouts, or Chicano Blowouts, were a series of 1968 protests by Chicano students against unequal conditions in the Los Angeles Unified School District high schools. The first protest took place on March 1, 1968. The students who organized and carried out the protests were primarily concerned with the quality of their education. This movement involved thousands of students in the Los Angeles area and was one of the first mass mobilizations by Mexican Americans in Southern California (Los Angeles Times 1968; Torgerson 1992).

↵8 The national origins formula was an American system of immigration quotas between 1921 and 1965 that restricted immigration on the basis of existing proportions of the population. It aimed to reduce the overall number of unskilled immigrants, to allow families to reunite, and to prevent immigration from changing the ethnic distribution of the population. The 1924 Immigration Act included the Asian Exclusion Act that barred specific origins from the Asia Pacific Triangle, which included Japan, China, the Philippines, Thailand, Laos, Vietnam, Cambodia, Singapore, Korea, Indonesia, Burma, India, Sri Lanka, and Malaysia (Office of the Historian 2016).

↵9 According to the 2015 American Community Survey five-year estimates, the Los Angeles metro area was home to the most Salvadorians, 447,788, followed by Houston, 169,935.

↵10 The NASCC survey was developed to supplement existing national data sets that collect data on household wealth in the United States but rarely collect data disaggregated in detail by race and ethnicity. The survey targets five metropolitan areas in order to collect data about the asset and debt positions of racial and ethnic groups at a detailed ancestral-origin level.

↵11 Neighborhood upscaling is the combination of a decrease in low-income households and an increase in high-income households due to luxury housing and transit orientated development.

↵12 The data reported in this section suffers from a number of limitations due to differences in how property values were reported in 1960, 1990, and 2015. The main difference is that the 1960 and 1990 data are reported as ordinal data where each household belongs to a bin with a range of values. In contrast, the 2015 data is reported as a continuous variable. Thus, the values in 1960 and 1990 correspond to the midpoint of the bin within which the median household falls. See the appendix for a detailed discussion of the variable and the range of each bin (for a detailed discussion, see Collins and Margo 2003).

↵13 This is in part due to the white population share falling and in part to the Hispanic population rising.

↵14 Economists ranging from Milton Friedman (1957) to Marjorie Galenson (1972), to Marcus Alexis (1971), have found that, after accounting for household income, blacks have a slightly higher savings rate than whites. More recently, Maury Gittleman and Edward Wolff (2007) using the Panel Study on Income Dynamics (PSID) have found that, after controlling for household income, if anything blacks had a mild savings advantage compared to whites (Hamilton and Chiteji 2013).

↵15 Two of the authors of this report have previously proposed universal gradationally endowed based familial wealth position at birth child trust accounts, “baby bonds.” The accounts would be used as seed money to purchase an asset like a home or a new business that might appreciate over a lifetime (Hamilton and Darity 2010; Aja et al. 2014).

- © 2018 Russell Sage Foundation. De La Cruz-Viesca, Melany, Paul M. Ong, Andre Comandon, William A. Darity Jr., and Darrick Hamilton. 2018. “Fifty Years After the Kerner Commission Report: Place, Housing, and Racial Wealth Inequality in Los Angeles.” RSF: The Russell Sage Foundation Journal of the Social Sciences 4(6): 160–84. DOI: 10.7758/RSF.2018.4.6.08. This research is made possible by the generous support of the Ford Foundation’s Building Economic Security Over a Lifetime initiative. We especially acknowledge our Ford Foundation Program Officers—Kilolo Kijakazi, Amy Brown, Leah Mayor, and John Irons. Funding was also provided by the UCLA Institute for American Cultures, UCLA Asian American Studies Center, UCLA Luskin Center for History and Policy, and the Haynes Foundation. This research is also part of the UCLA Center for Neighborhood Knowledge’s (CNK) Kerner Revisited project. We are grateful to CNK staff, Chhandara Pech and Alycia Cheng, for their research and technical assistance. Direct correspondence to: Melany De La Cruz-Viesca at melanyd{at}ucla.edu, UCLA Asian American Studies Center, 3230 Campbell Hall, Los Angeles, CA 90095.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

References

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.