Abstract

To address the housing affordability crisis for low-income Americans, we argue for a refundable renter’s tax credit. The proposed credit would be delivered through the tax code, reach a broad segment of renters, and target those with high housing cost burdens. We simulate the effects of the credit using Current Population Survey data. The credit would reach nearly 60 percent of poor renters and more than 70 percent of renters facing severe housing cost burdens, the credit amount averaging $2,059. Among recipients, the credit reduces the poverty rate by 12.4 percentage points and the deep poverty rate by 8.8 percentage points. For those who remain poor, it reduces the poverty gap by nearly a third. The annual cost is $24.1 billion.

The housing affordability crisis has reached historic levels in the United States amid rising rents, low wages, and an inadequate supply of housing. Fully half of renters face housing cost burdens, devoting more than one-third of their income to rent; one in four face severe cost burdens, handing over more than half of their income to rent (Joint Center for Housing Studies 2015). In 2015, a worker needed $19.35 per hour to afford the average two-bedroom rental in the United States, or two and a half times the federal minimum wage (National Low Income Housing Coalition 2016).

Problems of affordable housing are felt more acutely among the poor and near-poor, who do not earn enough to meet basic needs such as housing. Indeed, high housing costs are a primary driver of poverty because housing expenses represent such a large share of most families’ budgets. Under the Census Bureau’s Supplemental Poverty Measure (SPM)—which measures the typical spending of low-income families on the basic needs of food, clothing, shelter and utilities—housing expenses make up approximately half of the total poverty threshold (Bureau of Labor Statistics 2017).

In addition to stress on families’ current budgets, the lack of affordable housing has other negative ramifications, for communities as well as families. Families that pay too much for housing spend significantly less on food, health care, and retirement savings than those living in housing that is affordable (Joint Center for Housing Studies 2015). They are more likely to live in housing of substandard quality, to be evicted, and to go homeless (Desmond 2016). It comes as no surprise, then, that unaffordable housing negatively affects children’s health and school performance, and interferes with parents’ employment, parenting, and civic engagement (HUD 2014).

The United States has no entitlement program for housing, and public provision of affordable housing reaches only a fraction of all who are in need: only one in four families who are eligible for government subsidized housing receives it (Joint Center for Housing Studies 2015). This dearth of subsidized rental housing is inequitable, given the generous subsidies the United States provides to homeowners through mortgage interest and property tax deductions. Homeowners receive more than three-quarters of all federal housing subsidy allocations, and those making over $100,000 per year receive more than half of those dollars (Center on Budget and Policy Priorities 2017). Renters—who are excluded from this generous redistribution via the tax system—are much more likely to be poor than homeowners: from 2013 to 2015, the SPM poverty rate for homeowners stood at just 10 percent, versus 26 percent for renters.1 As a result, our nation’s existing portfolio of housing subsidies offered through affordable housing programs and the tax system fail to reach a majority of poor Americans.

In this article, we argue for a refundable renter’s tax credit for families facing high rental housing costs relative to their income. The credit is designed to reflect geographic variation in housing costs and delivers the largest subsidies, proportional to income, to those with the greatest housing cost burdens. The proposed credit builds on existing programs delivered through the tax code, but it reaches a much broader segment of the population than existing housing assistance programs: the proposed credit would reach one-fifth of all renters and more than 70 percent of severely housing cost–burdened renters. Using the SPM as a framework to simulate the effects of the proposed policy change, we find that among beneficiaries the credit reduces the poverty rate by 12.4 percentage points and the deep poverty rate by 8.8 percentage points. For beneficiaries who remain poor, it reduces the poverty gap by nearly one-third, at an annual cost of $24.1 billion. We argue that a renter’s tax credit harnesses the efficiencies of the tax system while targeting those who bear the brunt of the housing affordability crisis in the United States. The credit achieves a meaningful reduction in poverty for poor families while bringing overall federal housing expenditures into a more equitable equilibrium.

EXISTING HOUSING SUBSIDIES: INEQUITABLE AND INADEQUATE

Existing housing subsidy programs in the United States leave many poor families unassisted and have a number of administrative inefficiencies. The two largest sources of subsidized rental housing in the United States—the Low Income Housing Tax Credit (LIHTC) and the Housing Choice Voucher (HCV) program—have been successful in many ways. We argue, however, that scaling up these two programs would be inefficient and would not target poor families with the largest housing cost burdens.

The LIHTC is currently the largest project-based rental subsidy program in the United States, credited with the creation of more than two million rental units since its inception in 1986 (HUD 2017a). The program currently gives about $8 billion per year to states to issue tax credits to developers who build or rehabilitate rental housing and commit to reserving a certain share of units for lower-income households (those with incomes below 50 to 60 percent of the area median) for at least 15 years.2 The LIHTC has grown over time to become the most significant revenue source for the production of affordable housing. These tax credits are available only for new housing construction or rehabilitation, however, not to subsidize existing housing. Moreover, because the credits go only to developers, their success in reducing housing burden and poverty among intended beneficiaries is more diffusely realized than through policy mechanisms that target renters more directly.

Though LIHTC is successful in producing new housing, LIHTC developments are out of reach for the poorest households. Rents at LIHTC properties are typically set to be affordable for those with incomes around 50 to 60 percent of the area median, which means that the properties are typically too expensive for poor families with incomes below half the area median. The rental rates are also fixed in LIHTC developments, meaning they do not vary based on a household’s income. As a result, LIHTC housing can become unaffordable if a household’s income falls. In practice, very-low-income households are only able to live in LIHTC units by using a housing voucher; more than 60 percent of LIHTC properties include residents with housing vouchers (O’Regan and Quigley 2000; Climaco et al. 2006). Doubly subsidizing units in this way limits the already-inadequate supply of subsidized housing units nationally.

Compared with the LIHTC, the Housing Choice Voucher program—the largest demand-side program for low-income families—offers a much deeper rental subsidy. Low-income households receive a voucher that can be used to rent units on the private housing market. A voucher holder pays 30 percent of the family’s income toward rent, and the government makes up the rest. Low- and very-low-income families are given priority in the housing voucher program— public housing authorities must issue at least 75 percent of their vouchers to families with incomes less than 30 percent of the area median income.3

Despite the advantages of the deep subsidy, too few vouchers are issued each year to make the program widely accessible. In many large cities, the waitlists for housing vouchers are years—sometimes even decades—long.4 A number of administrative barriers also limit voucher use by both landlords and tenants. First, voucher holders can only lease units with rents that are lower than the local fair market rent as established by the U.S. Department of Housing and Urban Development (typically the 40th percentile of rents for that area), making units in more desirable areas or with higher-quality amenities inaccessible to voucher holders. Second, voucher holders typically have just sixty days to locate a unit and sign a lease. As a result, a substantial share of families who do receive housing vouchers cannot “lease up” and use the vouchers (Smith et al. 2015). Finally, tenants must find landlords who are willing to accept vouchers. Landlords report being reluctant to participate in the program because of the administrative hassles involved, including having the unit inspected before being able to rent it to a voucher holder, limits on rent that may be charged, and managing payments from both housing authorities and tenants (Rosen 2014). Once a landlord accepts a voucher, he or she may decide to stop accepting vouchers at any time.

The lack of affordable housing in the United States has adverse consequences for families and children. High housing costs are a direct driver of poverty. Families facing high housing costs must restrict expenditures on other basic necessities, such as food or health care, and the economic stress associated with financial insecurity undermines mental health and parenting resources (Harkness and Newman 2005; Leventhal and Newman 2010). Families in unaffordable housing are also more likely to live in substandard housing and to experience eviction or homelessness (Desmond 2016). Not surprisingly, unaffordable housing has negative effects on the health and school performance of children, and interferes with parents’ employment, parenting, and civic engagement (HUD 2014). Increasing access to affordable housing has been shown to improve children’s short- and longer-term outcomes (Newman and Harkness 2002).

EXISTING ANTI-POVERTY POLICIES: ONE SIZE FITS ALL

Existing anti-poverty policies play an undeniable role in improving the fortunes of low-income Americans. Nationally, programs like the Earned Income Tax Credit (EITC) and the Supplemental Nutrition Assistance Program (SNAP, or food stamps) reduce poverty rates significantly (Renwick and Fox 2016). Despite these laudable effects, existing means-tested programs exclude large segments of the poor population, such as those who do not work or do not have dependent children. Additionally, existing federal means-tested programs rarely account for the vastly different costs of living across the United States. In fact, fair market rents in the continental United States for a two-bedroom apartment varied from less than $600 per month to more than $3,000 per month in 2017. In effect, most federal anti-poverty programs treat families living in these different areas the same, ignoring the vastly different expenses they face, so that benefits received by families in high-cost areas have lower purchasing power and do less to mitigate economic hardship than the same amount of benefits received by families living in low-cost areas. Some states offset high costs of living by offering more generous benefits or tax credits, but these efforts are uneven and sensitive to state budgets.

Because housing is the single largest expense for most families, a housing subsidy that reflects local cost variations would offer significant relief for those in high cost-of-living areas. Homeowners already receive some federal tax relief that accounts for variation in housing costs, as those who face higher property taxes and home prices receive comparatively more from tax deductions. Moreover, renters have a substantially higher SPM poverty rate than homeowners (25.7 percent versus 9.8 percent) and make up more than half of the overall SPM poor population.5 They also typically face higher housing cost burdens than homeowners; nearly one-third have an expected housing cost burden of 50 percent or more, versus only 10 percent of homeowners. Thus poor renters are a particularly appropriate target population for both anti-poverty and housing affordability policy.

Renter households receiving federal housing subsidies via LIHTC or HCV programs already receive subsidies that account for local cost of housing because the value of these credits rises with housing costs. Thus, unsubsidized renters in high-cost areas stand out as receiving the least relief from both federal anti-poverty policy and existing housing programs.

ADVANTAGES OF A RENTER’S TAX CREDIT

Given these limitations of existing housing subsidy programs, we argue for a renter’s tax credit that targets families facing high rental housing cost burdens relative to their incomes. The tax system offers an advantageous way to deliver such a subsidy. The United States already has a generous quasi-entitlement program that subsidizes homeownership, in the form of mortgage interest and property tax deductions. These deductions are inequitable, however, because they are limited to homeowners, and affluent homeowners receive the lion’s share of the subsidies. Although no federal tax subsidy is in place for renters, several states have small renter’s tax credits, some of which are refundable (see table A6).

Additionally, tax credits are used to deliver the largest anti-poverty cash program in the United States, the EITC. In 2013, more than 27 million tax filers received about $61 billion from the federal EITC, lifting 6.2 million out of poverty, including about 3.2 million children (Center on Budget and Policy Priorities 2016b). For all its successes as an anti-poverty program, however, we argue that several features of the EITC limit its ability to tackle housing affordability directly. First, several key populations are excluded from receiving it, including those who do not work and those without custodial children (the latter receive a much smaller credit). Second, the federal EITC offers a uniform benefit amount that does not adjust for geographic variation in housing costs, which means that some EITC-eligible households face housing cost burdens while others do not.

A renter’s credit administered through the tax code also overcomes some of the programmatic limitations of the existing housing assistance programs described. Delivery via the tax code allows for lower administrative costs and reduced barriers to securing assistance. A tax credit to renters complements the tax subsidies that already go to developers via the LIHTC. Unlike the LIHTC, which sets rents too high for the poorest families and uses tax credits only for new housing construction, the renter’s tax credit is targeted to those most in need, with the largest benefits, proportionate to income, going to those with the greatest housing cost burdens, and it applies to all forms of unassisted rental housing rather than just new housing construction. By offering a shallower subsidy than vouchers, with parameters that can be modified to respond to availability of federal funds, a tax credit can also be made available to all renters who meet specified eligibility criteria, avoiding the arbitrary rationing that results from housing voucher waitlists and the uneven spatial distribution of subsidized project-based rental units.

HOW THE PROPOSED RENTER’S TAX CREDIT WORKS

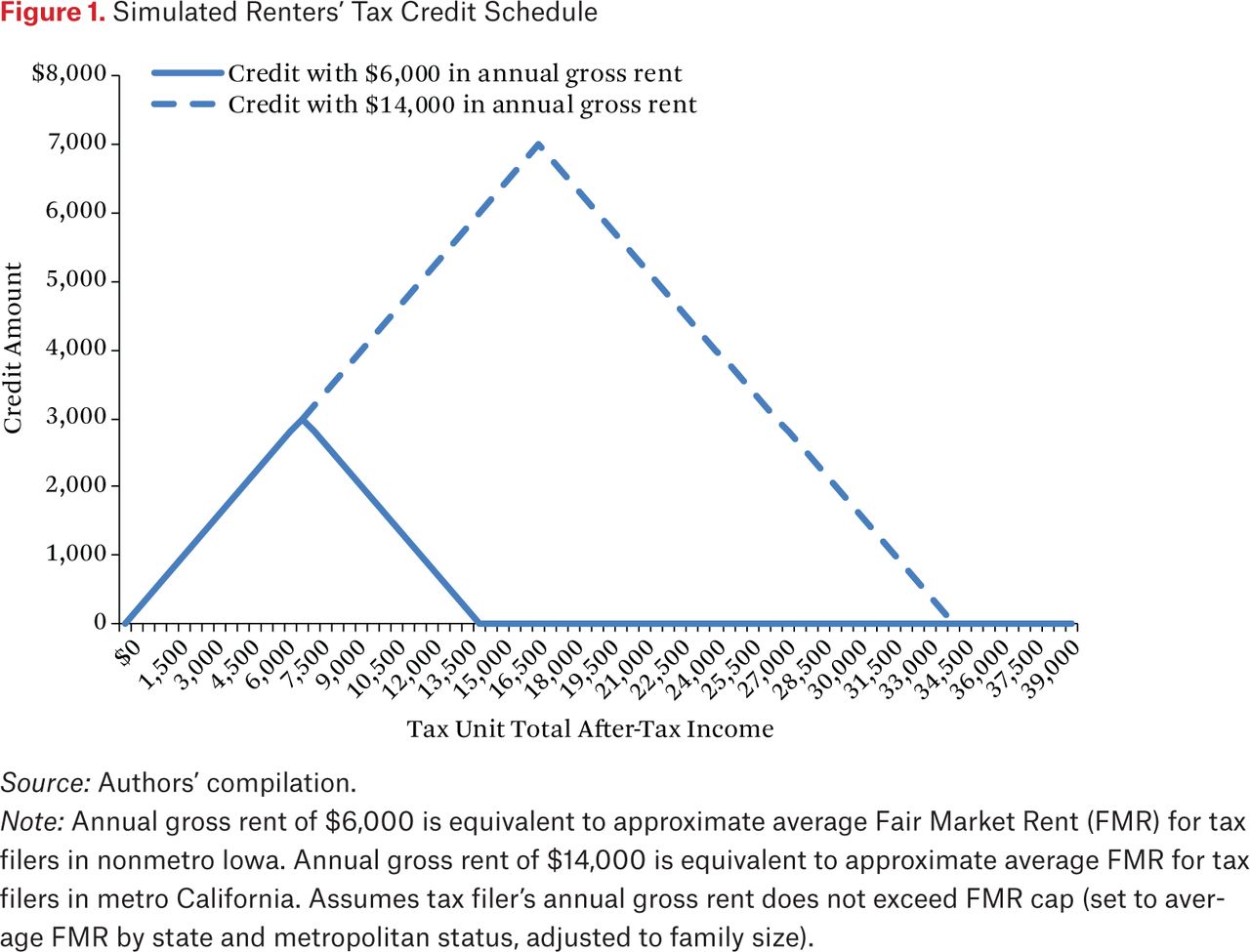

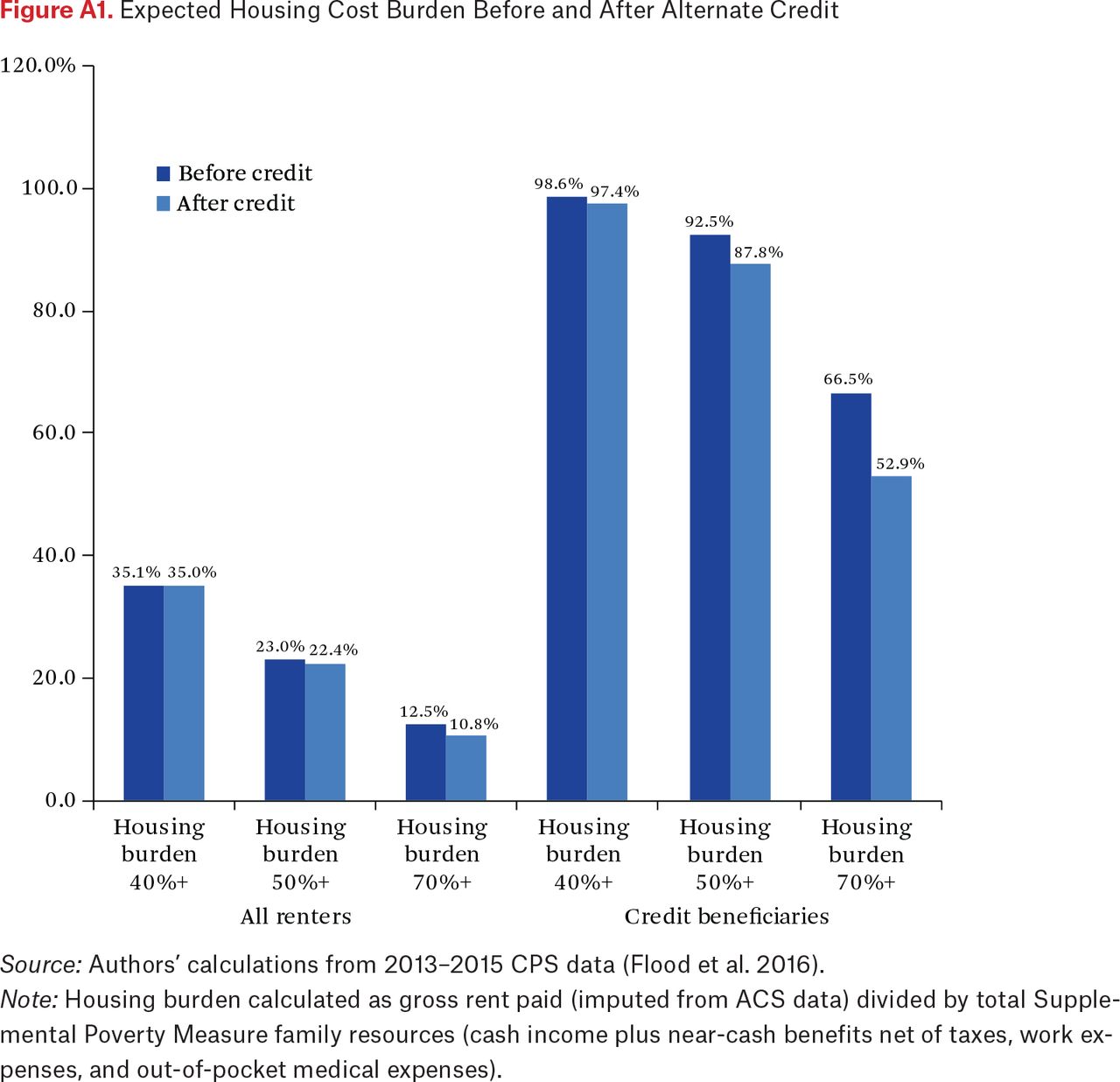

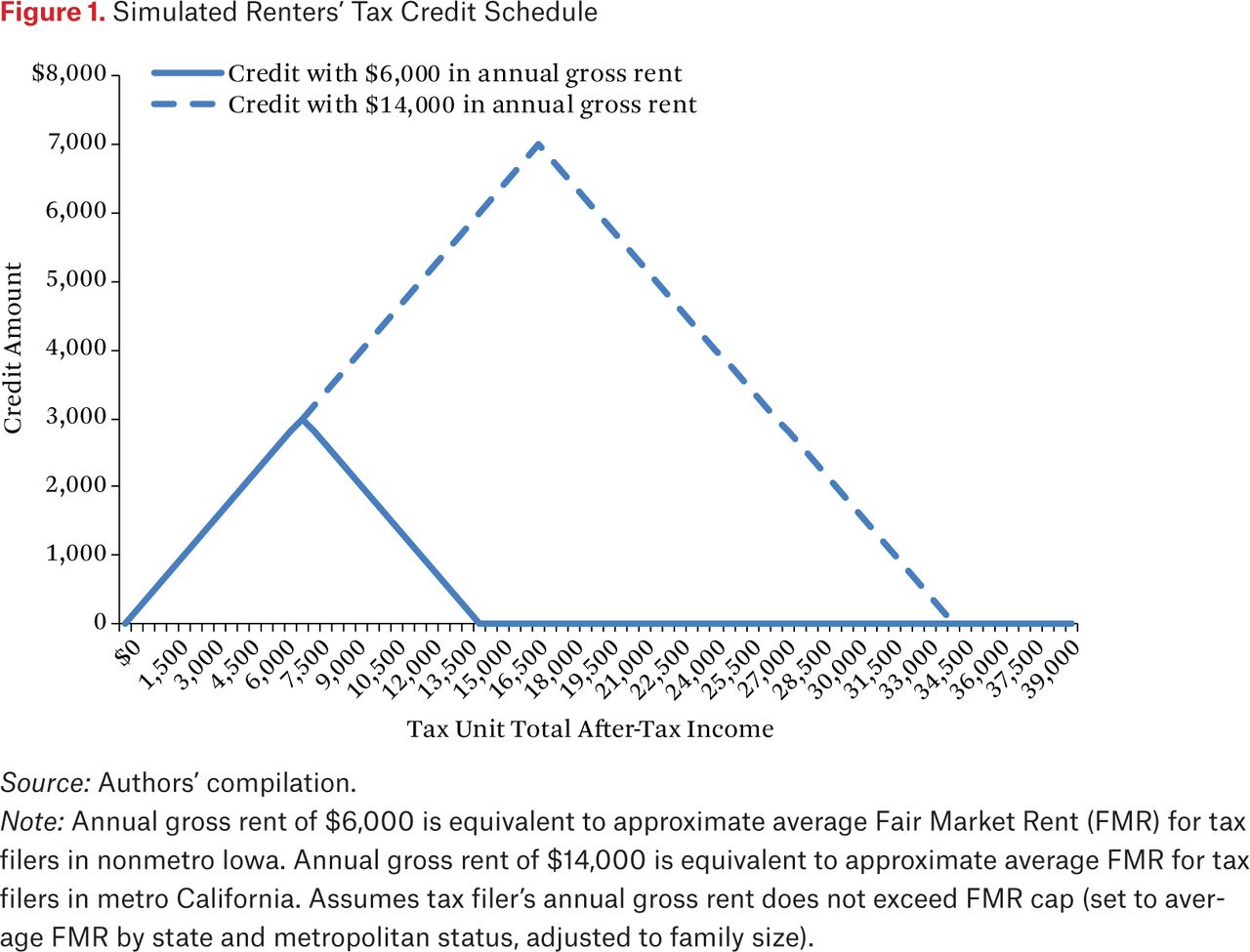

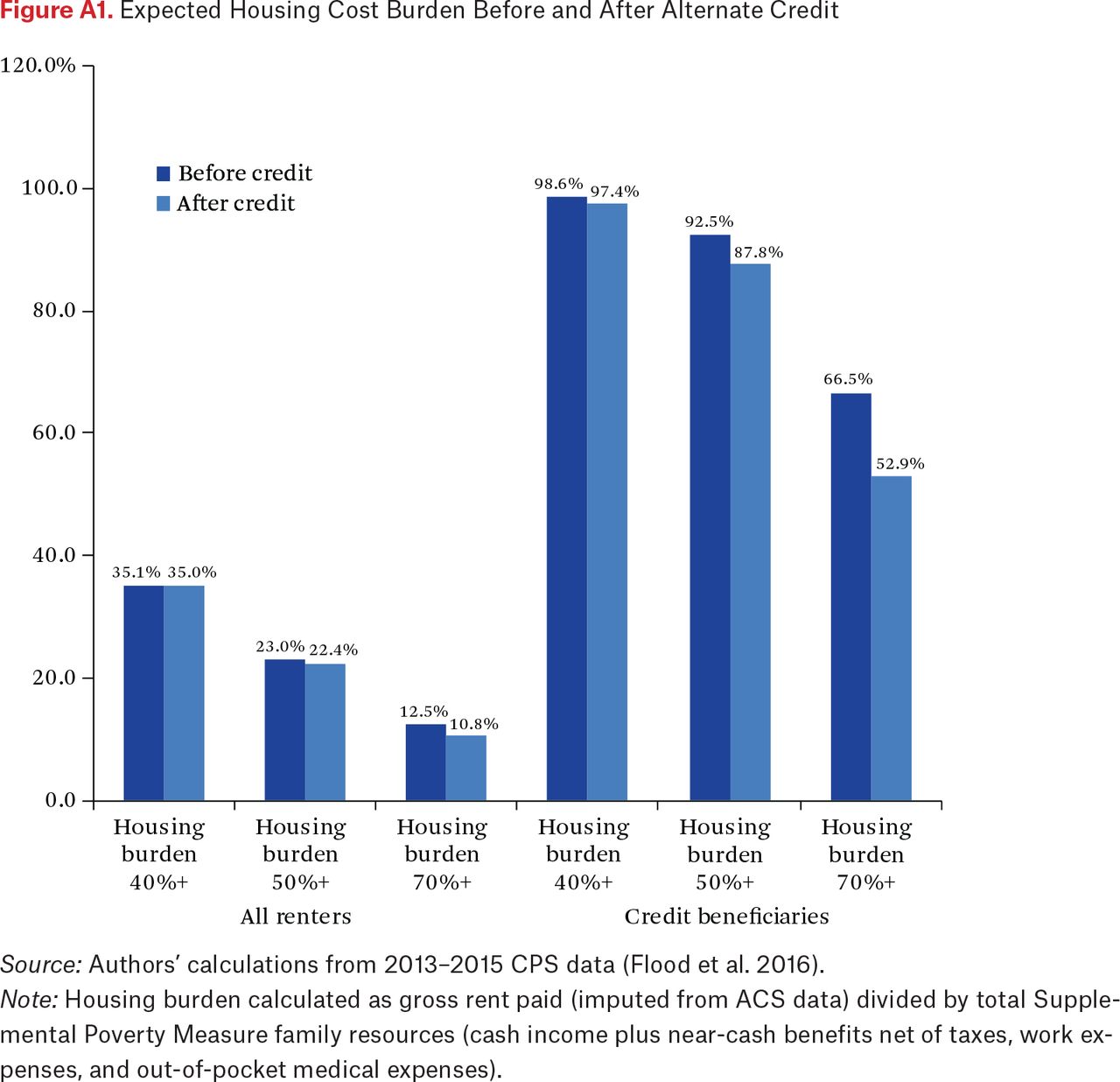

The credit is a refundable income tax credit designed to cover the gap between rent paid and 40 percent of a household’s after-income-tax cash income. HUD identifies an affordable housing cost burden as paying no more than 30 percent of income toward rent, and categorizes households paying more than 50 percent of income toward rent as severely housing cost burdened. The 40 percent target for the renter’s tax credit thus represents a middle ground between these two federal standards of housing affordability. (For simulations of credits based on a more stringent 50 percent housing cost burden eligibility threshold instead, see figure A1.)

The credit is calculated based on the amount of gross rent (cost of rent plus utilities) paid annually by a tax filer. Tax filers may claim rent paid at an amount that is the lowest of actual gross rent paid, assigned fair market rent (FMR), or 80 percent of after-tax tax unit income.

The amount of claimable rent is capped at the tax filer’s FMR to target the credit to renters in the bottom half of the rental market: tax filers may only claim rent paid up to the average FMR in their state and metropolitan or nonmetropolitan area, adjusted for household size. Table 1 lists the average monthly gross rent paid by credit recipients and the average monthly FMRs for tax filers from 2013 through 2015 by state and metropolitan status. Capping claimable rent at the FMR amount ensures that the credit subsidizes housing consumption only up to the level identified by HUD as adequate, and does not subsidize “overconsumption” of housing.

Average FMR and Credit Recipient Gross Rent Paid Amounts for Tax Units, by State and Metropolitan Status

Claimable rent paid is also capped at 80 percent of cash income for all family members, net of federal income taxes and credits, under the assumption that most households cannot sustainably pay more than 80 percent of total after-tax cash income toward rent. Note that this means that households with zero or negative after-tax income for the year are not eligible for a credit, even if they paid rent. We assume that tax filers with rent paid in excess of 80 percent of annual after-tax income would be likely to be either receiving additional unreported income, or are facing a temporary major income shortfall, which this policy is not intended to address. Limiting the claimable rent paid to 80 percent of income also incentivizes households to seek housing with a rent burden that does not exceed the very minimal sustainability threshold of 80 percent of income.6

The capped rent paid amount is then compared with the tax unit’s income, the income including all taxable and nontaxable cash income for the tax filer, spouse, and dependents, net of federal income tax liabilities and credits. Tax filers would need to report their nontaxable income and the income of their dependents for this calculation. (Similar income reporting is currently required on the tax form used to calculate individual responsibility penalties for not having insurance coverage under the Affordable Care Act.) Linking the credit amount to after-tax income is highly feasible as the credit is claimed at the same time as the filing of annual income taxes. Moreover, using after-tax income better accounts for the resources available to pay for basic needs among low-income households by excluding income tax liabilities that reduce discretionary income and by including tax credits such as the EITC, which represent a large share of income for many low-income households.

A tax filer’s credit is equal to the difference between capped rent paid and 40 percent of the family’s total after-tax cash income. The credit as presented in this analysis is equal to the full rental cost gap—the difference between (capped) rent paid and 40 percent of a tax unit’s income—but the credit could easily be adjusted to cover only a portion of the rental cost gap (for example, half) if desired to reduce the policy cost. The final credit amount for tax unit i is thus calculated as

Credit Amti = Capped Rent Paidi – (0.4 × After – Tax Incomei)

The maximum credit is available to tax filers with extremely high housing cost burdens, of 80 percent or more, and those living in areas with high rental prices, as represented by assigned FMRs. From there, the credit gradually phases out to zero for tax filers for whom capped rent paid equals between 80 percent and 40 percent of after-tax income (for an illustration of the proposed structure of the renter’s credit schedule, see figure 1). The credit amount is then applied to any tax liability, and anything left over is refunded to the tax filer. Tax filers may apply to receive their refund as deferred payments on a quarterly basis, or in a lump sum when they file their annual tax return.

Simulated Renters’ Tax Credit Schedule

Tax filers are not eligible for the credit if they are already receiving a housing subsidy, or if they are not paying rent. Tax filers who receive a housing subsidy via the public housing program or housing voucher program already pay no more than 30 percent of their income toward rent, so their rental expenses are too low to qualify for the credit. Homeowners are categorically excluded from the renter’s tax credit. Although homeowners make up approximately 44 percent of the SPM poor, poor homeowners as a group are more advantaged than poor renters, having more assets and more housing security than poor renters, and existing tax structures address housing-related costs of homeowners. Thus they are not targeted for assistance through the renter’s tax credit. Poor nonhomeowners who pay no rent (including those living with friends or family, and those who are incarcerated or institutionalized) have no housing cost burden and so are appropriately excluded from the credit as well.

Compared with traditional housing vouchers, the proposed renter’s tax credit provides a shallower subsidy but is available to a much broader segment of the housing cost-burdened population—anyone with nonzero income who pays more than 40 percent of income to afford an adequate rental unit qualifies. No approval by the landlord or inspection of the housing unit is required to receive the credit. Compared with the LIHTC, the proposed credit is adjusted progressively, based on the tax unit’s housing cost burden, larger subsidies being proportional to income for those with higher housing cost burdens. The credit is not restricted to new construction or rehabilitation; that is, it can be used for any existing rental housing. The application process is highly accessible, because most households file tax returns anyway, and administrative costs are low, because it takes advantage of the existing (and relatively low-cost) tax processing infrastructure.

Compared with proposals to add cost-of-living adjustments to existing anti-poverty programs, such as the EITC, the renter’s credit provides more targeted assistance to those truly housing cost burdened, and it also reaches those left out of many contemporary anti-poverty programs such as SNAP or Supplemental Security Income (SSI), where benefit generosity is driven by the presence of children in the household or extreme levels of deprivation.

METHODOLOGY

To estimate the likely anti-poverty effects of the proposed renter’s tax credit, we use the Census and Bureau of Labor Statistics’ SPM as a framework in which to simulate the proposed policy scenarios. Importantly for our purposes, the SPM uses a broad definition of resources, which include not only cash income but tax subsidies and in-kind assistance like housing subsidies (Renwick and Fox 2016). In so doing, the measure provides a suitable context for assessing the effectiveness of government policies and programs in reducing the poverty rate, as well as comparing the potential effectiveness of policy alternatives.

For our main analysis, we use data from the Current Population Survey’s March Supplement from 2014 to 2016 (corresponding to calendar years 2013 to 2015). These data are the primary source of both official and supplemental poverty statistics in the United States (n=583,693).7 We use the individual and household microdata to construct tax units and simulate those eligible for the renter’s tax credit, assuming full take-up among those eligible, using the criteria spelled out above to define eligibility parameters and benefit amount parameters. We identify gross rent paid by each tax unit.8 We assign an FMR cap for claimable rent paid based on each tax filer’s place of residence and number of dependents.9

With these data, we examine the reach and cost of the program and the demographics of beneficiaries. We estimate changes in poverty status for credit recipients, and then assess the overall impact a renter’s credit would have on poverty rates for the total population, all renters, and credit beneficiaries, nationally and by state. We also explore other dimensions of economic hardship, including the poverty gap, as well as housing cost burden (calculated as gross rent paid divided by total family SPM resources). In the appendix, we also explore options for targeting the credit more narrowly to specific subgroups (for example, to families with children, or families with seniors, or renters in high housing-cost states).

The design of the credit allows for modification of the credit parameters (such as share of rental gap covered, maximum rent amount allowed to be paid, phase-out level and rate) to target particular households or adjust the cost or depth of subsidy. In the appendix, we present results for a version of the credit with parameters modified to target households with more severe housing cost burden (those expected to spend at least 50 percent of income on housing).

To put the projected impact of the credit in context, we compare the reach and poverty reduction of the credit with three other safety net programs: SNAP, EITC, and existing housing subsidies. We calculate reach using reported program participation in Current Population Survey (CPS) data. To present a consistent measure of poverty reduction across these programs, we calculate the SPM poverty rate with and without each of these programs included in families’ resources, after adding the renter’s tax credit for eligible families. Note that safety net program participation is known to be underreported in survey data such as the CPS (Meyer, Mok, and Sullivan 2015), thus these estimates likely underestimate program impact for SNAP and housing subsidies, less so for EITC.10

Throughout our analysis, we focus primarily on the impact of the renter’s credit on the population of renters, given that homeowners are categorically ineligible for the credit.

RESULTS

We begin by presenting descriptive information on the impact of our proposed credit. Table 2 presents estimates of the number of beneficiaries and cost of the credit, its reach, and the demographics of simulated beneficiaries. More than 11.5 million tax filers would receive the simulated credit, which translates into more than 20 million total beneficiaries whose family incomes would see a boost from the program. The total cost of the program would be roughly $24 billion. The average amount of these credits would be about $2,100, and would be of more value for poor families (roughly $2,300) than to nonpoor families (roughly $1,500).11

Beneficiaries and Cost of the Proposed Renters’ Tax Credit

The credit would also reach a wide swath of American renters. Approximately 20 percent of all renters and nearly 60 percent of poor renters would benefit from the proposed credit. By design, renters with high housing cost burden—who are the majority of all poor renters—would stand to gain the most. More than 70 percent of severely cost-burdened renters and more than three-quarters of renters spending 70 percent or more of their income on housing would benefit from the credit.

Table 3 shows the demographics of those simulated to receive the renter’s credit. More than half of beneficiaries are in families with children, and more than a quarter in families with very young children. Because a growing literature suggests that low income and poverty are detrimental to children’s short- and long-term outcomes, that so many beneficiaries would include children suggests that this credit would have a positive impact on child well-being (see, for example, Duncan, Morris, and Rodrigues 2011). The credit would also enhance the resources of a diverse group of Americans by race-ethnicity. Approximately half of beneficiaries would be in families with the highest educational attainment of a high school degree or less, and they would be most concentrated in the South, where incomes tend to be low, and West, where housing costs tend to be high.

Demographic Characteristics of Renter’s Credit Beneficiaries

Poverty Reduction Effects of the Renters’ Tax Credit

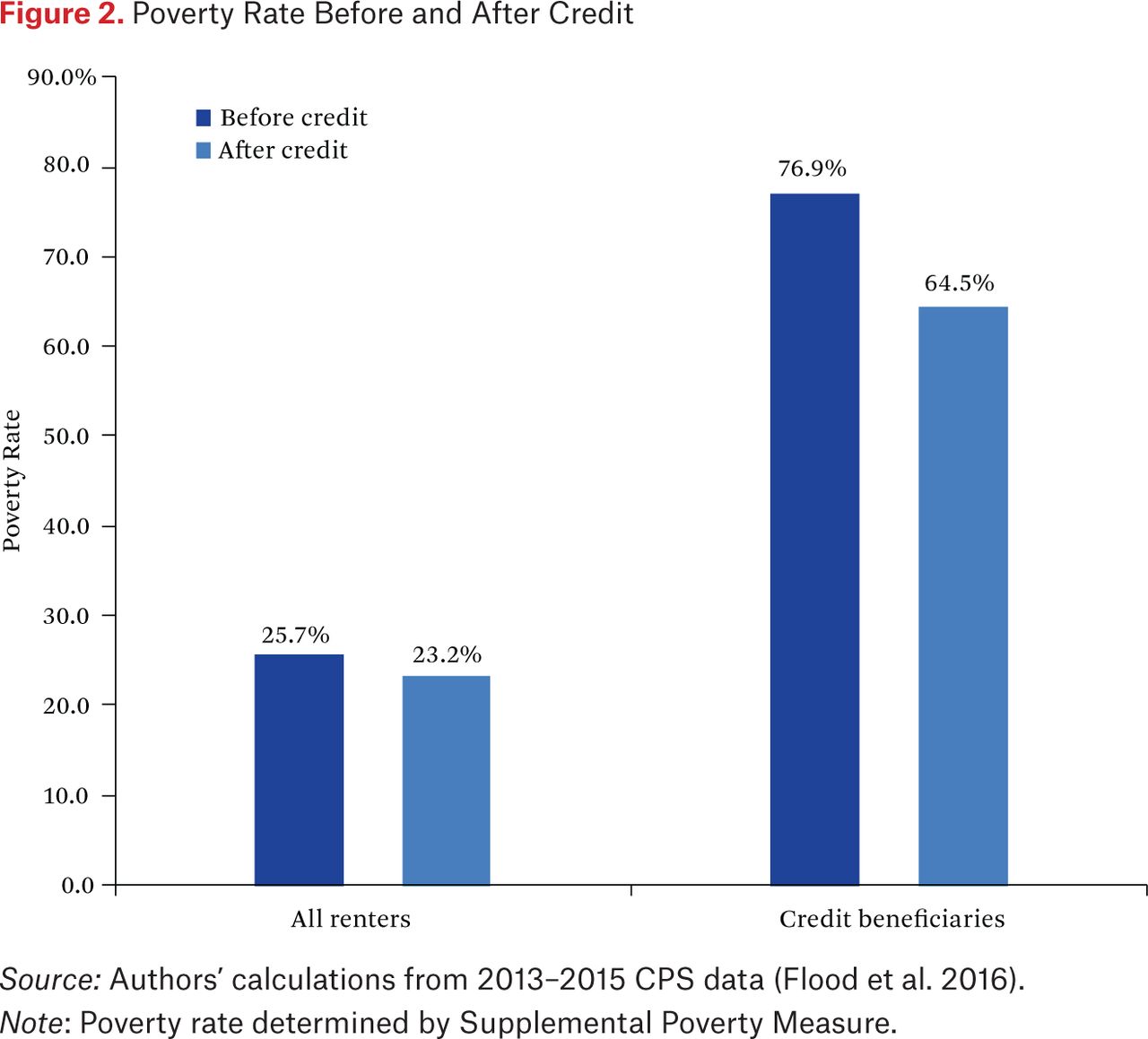

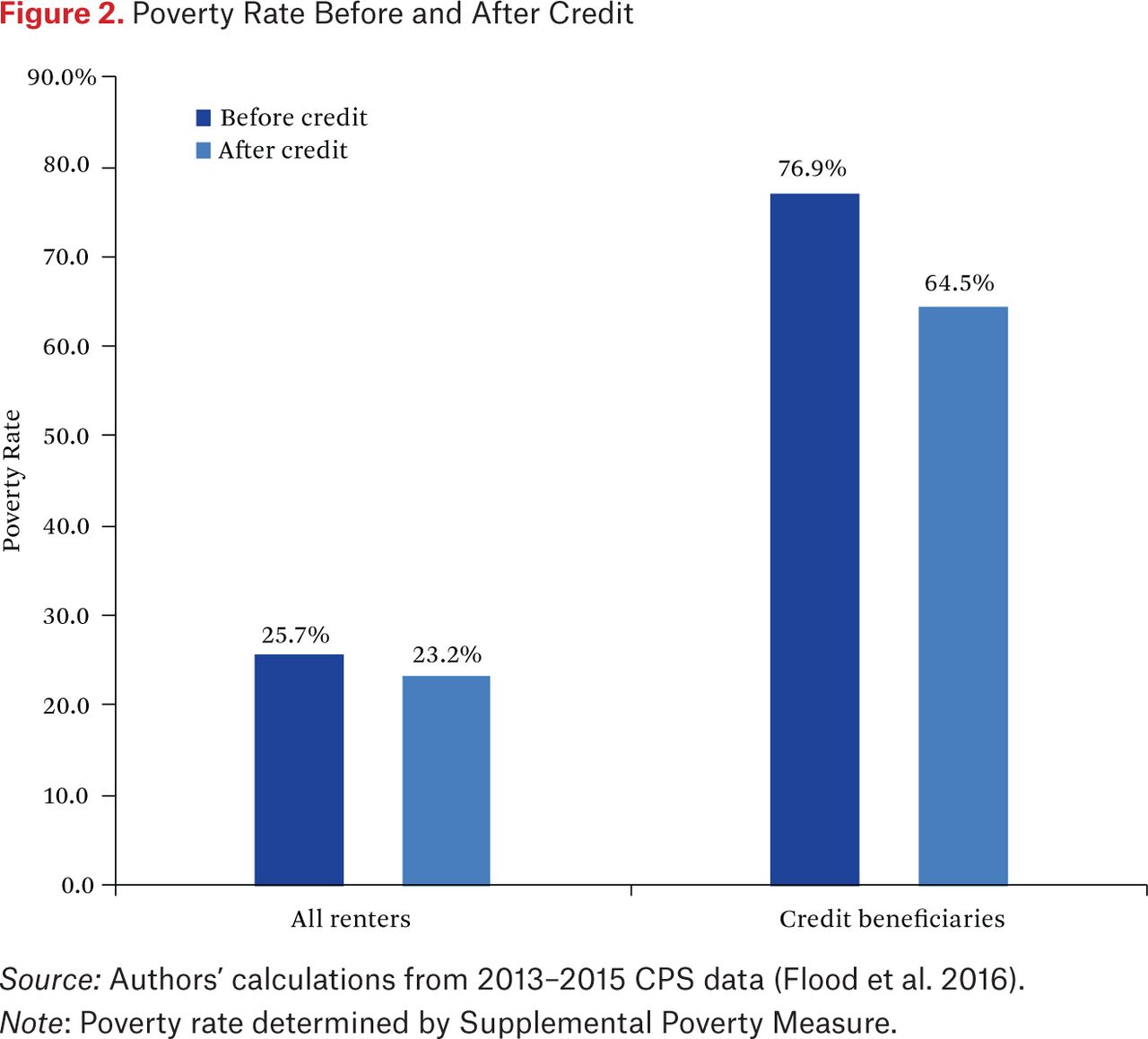

Table 4 presents our key results for the impact of the proposed renters’ tax credit on poverty. We find that, overall, the credit would reduce poverty among renters by 2.5 percentage points, a 10 percent relative reduction (see also figure 2), and would reduce deep poverty by 1.7 percentage points, a 22 percent relative reduction. For the full U.S. population (including homeowners categorically ineligible for the credit), the credit would reduce the poverty rate by 0.8 percentage points, a 5 percent relative reduction, and would reduce the deep poverty rate by 0.6 percent, a 12 percent relative reduction. The anti-poverty effects of the proposal are of course larger among beneficiaries. These families, who are more likely to be poor and facing a housing cost burden before the credit, would see a drop in poverty rate of 12.4 percentage points, a 16 percent relative reduction, and a decline in the deep poverty rate of 8.8 percentage points, a 35 percent relative reduction. In total, 2.6 million people would be lifted out of poverty by the credit (for results by state and for versions of the credit targeting only families with children, families with seniors, or residents of high housing cost states, as well as a credit that targets more severely housing-burdened households, see the appendix).

Anti-poverty Effects of Renter’s Credit

Poverty Rate Before and After Credit

Of course, the credit’s effects would extend beyond simply lifting some people over the poverty line. In the second half of table 4, we show that another 13.4 million Americans would see a decline in their poverty gap, or the gap between their level of resources and the poverty threshold. This reduction would be substantial. The median poverty gap among poor beneficiaries was more than $7,700 before the simulated credit, which is reduced to roughly $5,100 after the credit. The median decline in the poverty gap for poor credit beneficiaries is 32 percent. In addition, more than 4 million individuals who start out somewhat above the poverty line, but still face high housing cost burdens, would also benefit from the credit.12

Effects of Renter’s Credit on Housing Cost Burden

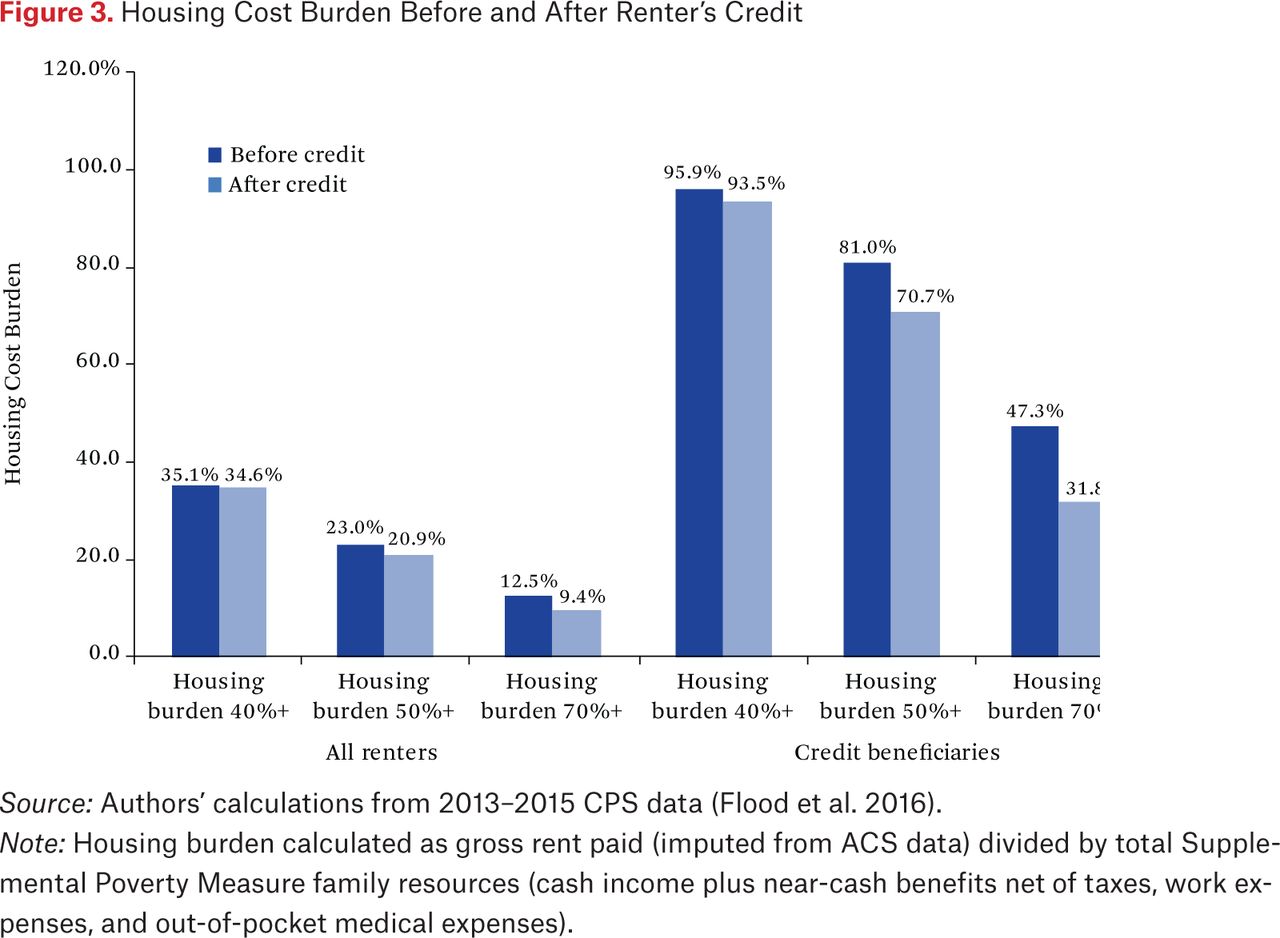

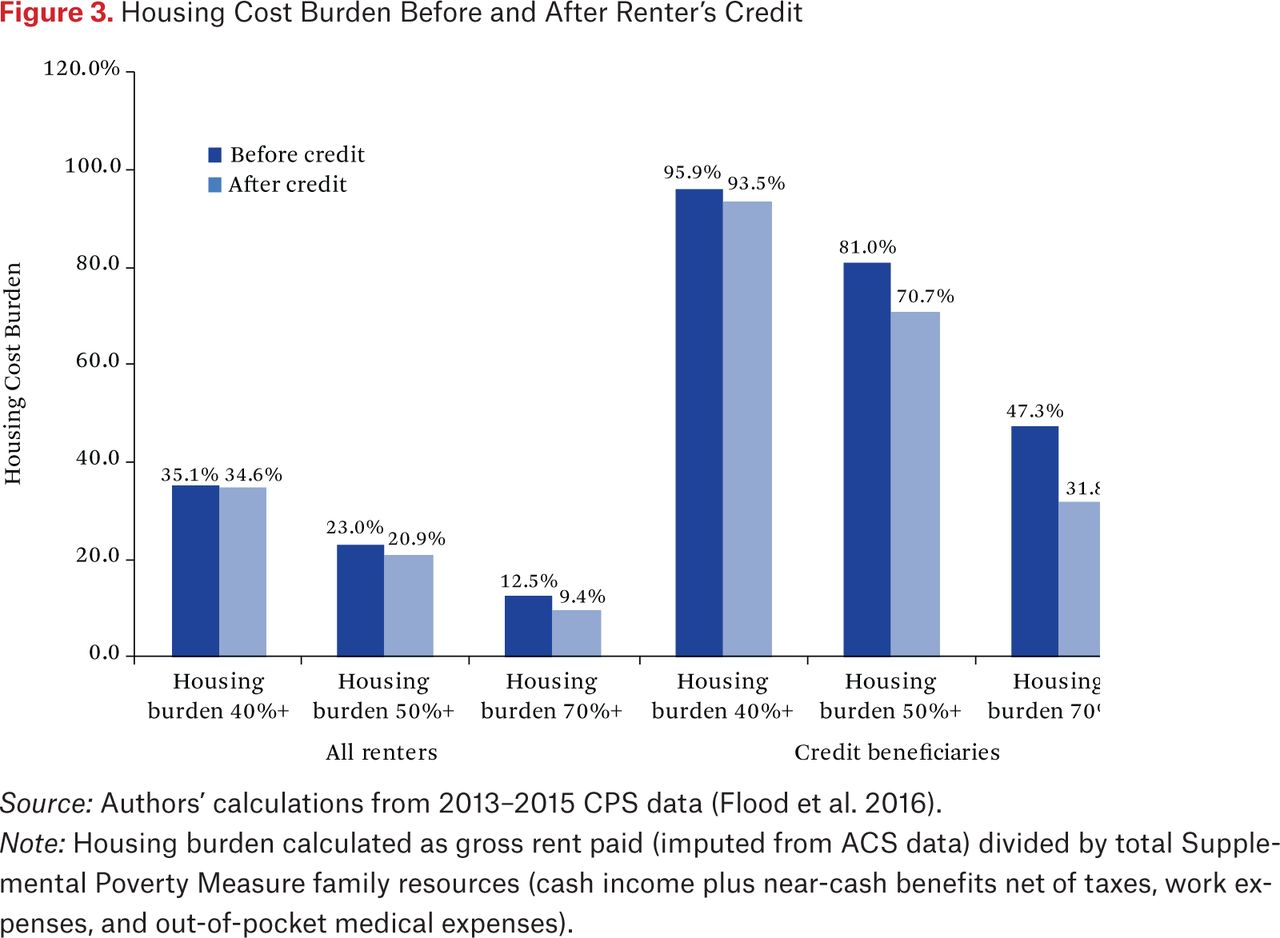

We also examine the projected effects of the credit on housing cost burden (gross rent divided by total family SPM resources). Figure 3 shows that that the share of renters who are severely housing cost burdened (paying 50 percent or more of income toward housing) declines by 2.1 percentage points, a 9 percent relative reduction, and the share of renters with an expected housing cost burden of 70 percent or more declines by one quarter (3.1 percentage points). Among credit beneficiaries, the impacts are larger: severe housing cost burden declines by 10.3 percentage points, a relative reduction of 13 percent, and housing cost burden of 70 percent or more declines by 15.5 percentage points, a 33 percent relative reduction.

Housing Cost Burden Before and After Renter’s Credit

Renter’s Credit Relative to Other Anti-poverty Programs

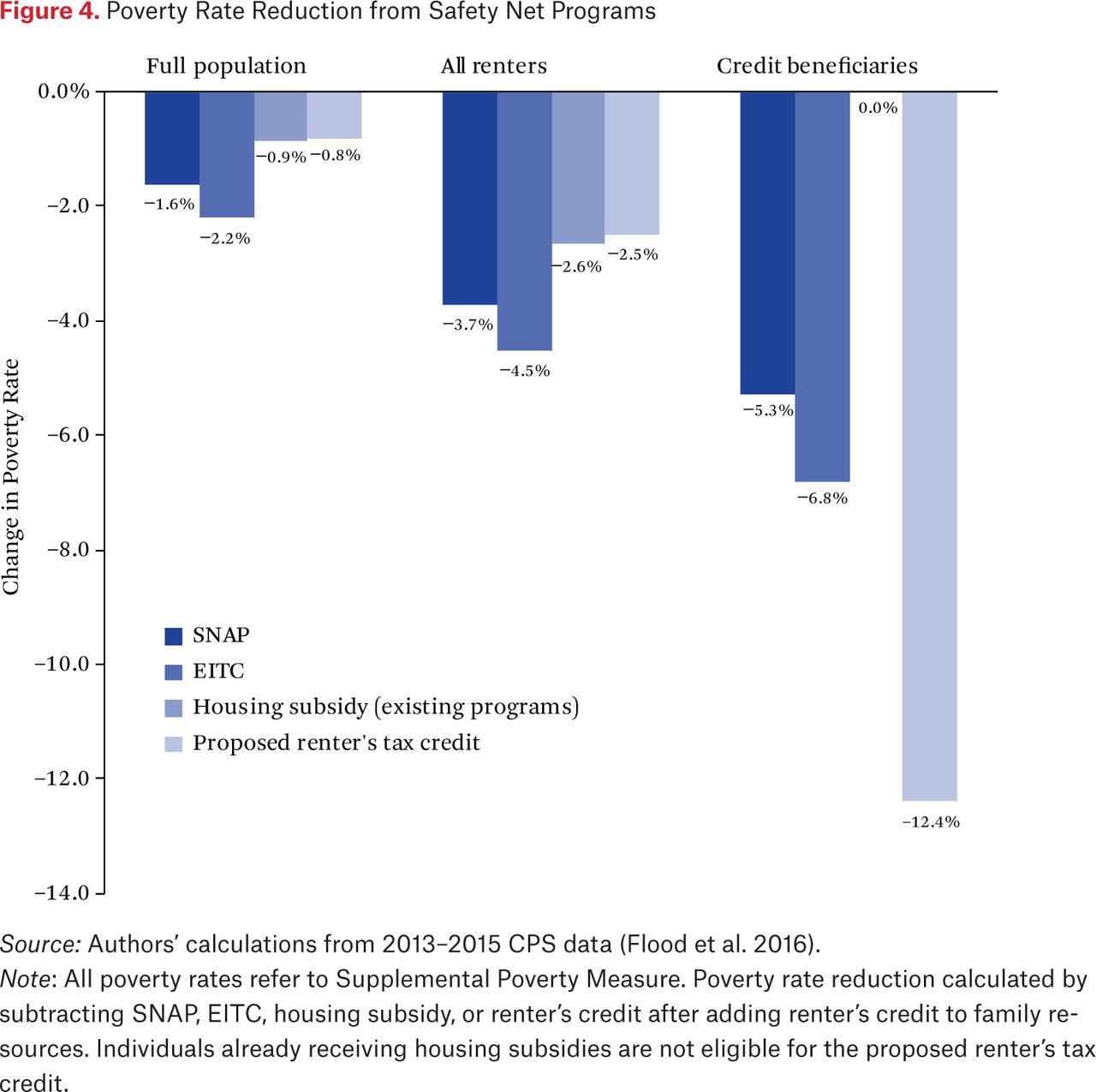

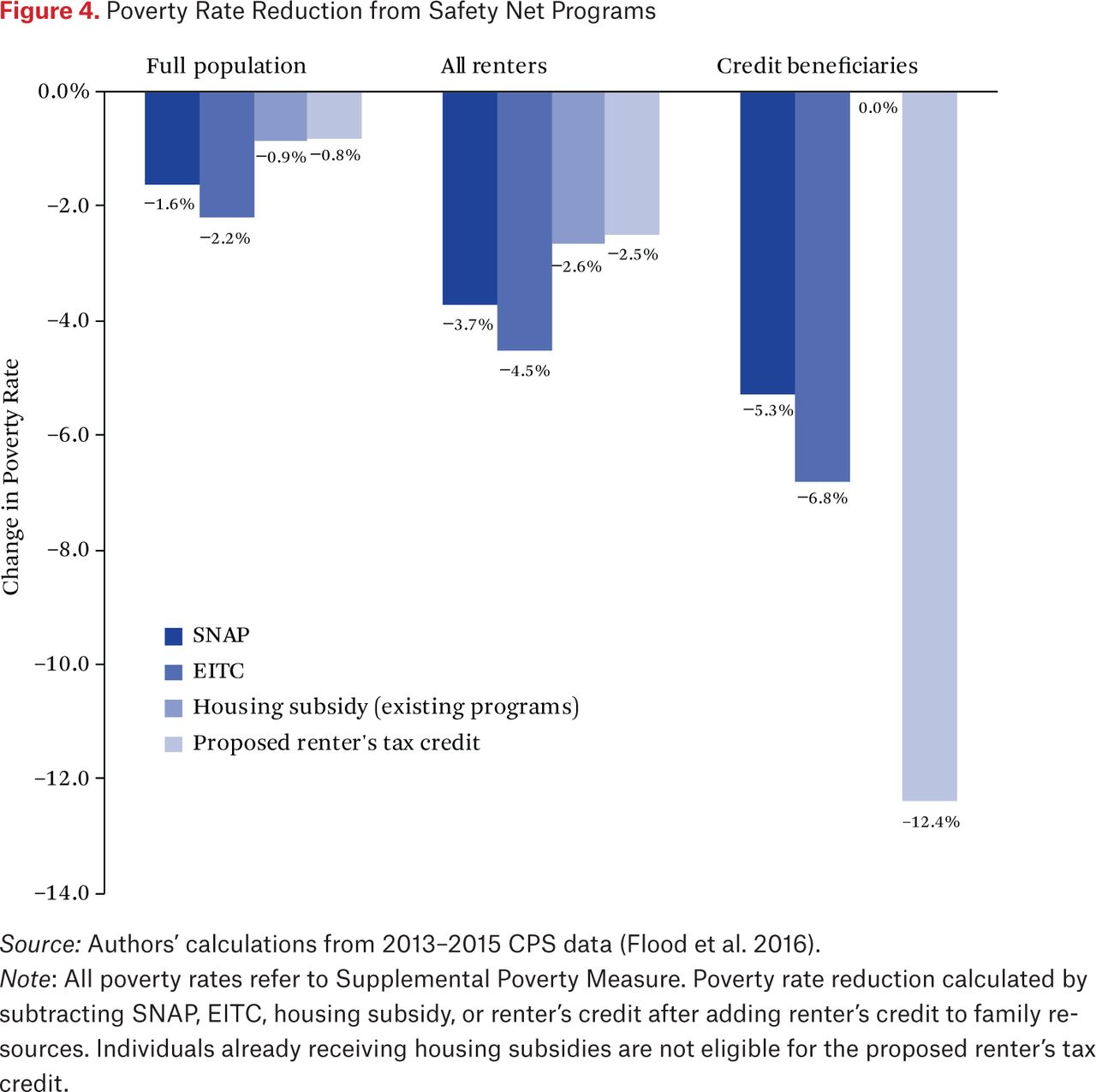

To put the poverty reduction impact and reach of the credit into perspective, we compare the credit with SNAP, the EITC, and existing housing subsidies. At an estimated cost of $24.1 billion, the credit would be substantially less expensive than the EITC (approximately $67 billion in 2016), SNAP (approximately $71 billion in 2016), and existing housing subsidy programs (approximately $55 billion in 2016, including approximately $37B for HUD rental assistance and public housing programs) (Center on Budget and Policy Priorities 2016a). Comparison of poverty reduction for these programs is presented in figure 4. (As noted, these results rely on safety net program participation as reported in CPS data; because participation is known to be underreported, these estimates are conservative.) For the full population, the credit reduces poverty a similar amount as existing housing subsidies, less than the EITC, and somewhat less than SNAP. Among renters, the credit again reduces poverty a similar amount to existing housing subsidies, less than the EITC and somewhat less than SNAP. Among credit beneficiaries, the credit reduces poverty substantially more than either the EITC or SNAP (and more than housing subsidies, by definition, because individuals already receiving housing subsidies are ineligible for the credit).

Poverty Rate Reduction from Safety Net Programs

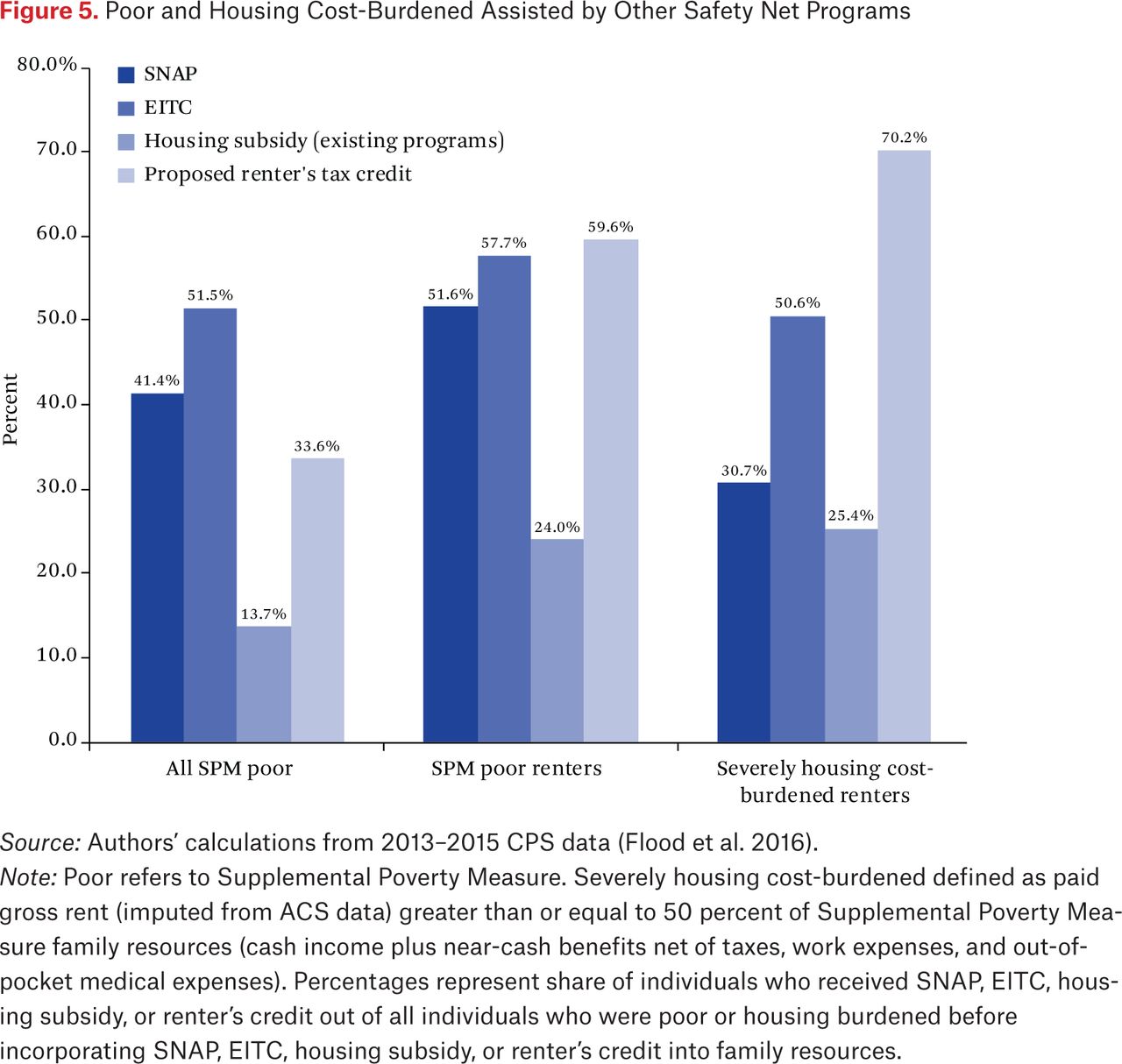

Reduction in the poverty rate is not the only relevant measure of impact on poor families, however, because it captures only the number of individuals moved across the poverty line by the benefits, and not the total number of poor individuals assisted (many of whom benefit from increased resources yet remain below the poverty threshold). We present a comparison of the reach of these programs to vulnerable households in figure 5. In comparing the reach of the credit with other safety net programs, we find that the credit assists nearly 1.4 times as many severely cost-burdened renters as EITC and more than twice as many severely cost-burdened renters as report receiving SNAP, suggesting that a significant share of renters who struggle with housing affordability and would be eligible for the credit may not already be participating in these other safety net programs. The credit also assists nearly two and a half times as many poor renters and more than 2.75 times as many severely housing cost-burdened renters as existing housing subsidy programs, suggesting that the credit would mitigate the extremely limited reach of the current system of housing-specific assistance.

Poor and Housing Cost-Burdened Assisted by Other Safety Net Programs

Administrative data from HUD provide another point of comparison for the cost and reach of the proposed renter’s credit. In fiscal year 2015, HUD’s rental assistance and public housing programs had a budget of $35.9 billion and assisted 9.9 million individuals (HUD 2017b).13 The proposed renter’s credit would have an annual cost of $24.1 billion, equal to two-thirds of the HUD rental assistance and public housing budget, and assist 20.8 million individuals, more than twice as many as these HUD rental programs. The renter’s credit would thus reach a substantially larger number of low-income renters than HUD’s existing subsidies for renters, at a lower cost (and shallower subsidy) per assisted individual.

DISCUSSION

A refundable renter’s credit stands to significantly curtail the current dearth of affordable housing in the United States. Our estimates suggest that more than 20 million individuals would benefit from the proposed credit, with an average benefit amount of $2,300 for poor families. We estimate that the credit would reach more than 70 percent of all severely cost-burdened renters, who spend more than half of their incomes on rent. The credit has a significant impact on the poverty rates of beneficiaries, reducing their poverty rate by 12.4 percentage points and lifting 2.6 million people above the poverty line. Another 13.4 million poor Americans would be made less poor by the credit, reducing the gap between their incomes and the poverty line by nearly one third. A substantial number of near-poor individuals would also benefit from the credit.

Some might argue that we should incorporate cost-of-living adjustments to existing anti-poverty and housing subsidy programs, rather than create a new renter’s credit. An example of such an approach is adjusting the size of credits for the EITC for local differences in the cost of living. The renter’s credit reaches a different subset of the population than existing anti-poverty programs or existing housing subsidy programs, however, and seeks to accomplish a different goal. Our estimates show that the renter’s credit assists more severely cost-burdened renters than the EITC or SNAP. Significant numbers of poor and nonpoor renters who struggle with housing affordability are not eligible for or may not participate in these other programs. As a result, a renter’s credit would reach more poor renters than would a cost-of-living supplement to existing anti-poverty programs.14 The credit also reaches more than twice as many poor and severely cost-burdened renters as existing housing subsidy programs, which are highly rationed. Administering the credit via the tax code also has the added benefits of greater administrative efficiency compared to existing housing programs like vouchers and developer tax credits, and reducing inequities between renters and homeowners in the existing tax code.

As a result of the distinct targeting to high-cost areas, the proposed renter’s credit reaches a different segment of poor Americans than related proposals to address housing costs through the tax code, such as a proposal to add a housing supplement to the EITC (Dreier 2016). As noted, the proposed credit would reach substantially more severely cost-burdened renters than a housing supplement to the EITC, given that many poor and cost-burdened renters do not receive the EITC. Only half of the renter’s credit beneficiaries in our simulation are in tax units eligible for the EITC. Even among tax filers who receive the EITC, the renter’s tax credit differs from a EITC housing supplement in that it specifically targets renters, and 54 percent of tax filers receiving EITC are homeowners.15 Because renters generally have higher poverty rates, fewer assets, less housing security, and fewer existing tax benefits than homeowners, targeting low-income housing assistance specifically to renters prioritizes the neediest households who are often excluded from existing safety net programs. To address housing need specifically, therefore, a renter’s tax credit offers more efficient targeting to individuals with greater housing need than an EITC housing supplement.

The proposed renter’s credit also serves a different anti-poverty purpose than a child allowance, such as the ones proposed elsewhere in this double issue (Shaefer et al. 2018; Bitler, Hines, and Page 2018). Whereas the child allowance addresses poverty among all children in all locations, the renter’s credit targets poor renters in areas with high housing costs, regardless of whether they have children. As a result, the proposed credit offers an important complement to anti-poverty efforts that specifically target families with children (as much of the existing safety net does), reaching segments of the poor population that receive fewer benefits from existing anti-poverty programs, particularly individuals hardest hit by the growing crisis of housing affordability in the United States. The renter’s credit is responsive to differences in cost of living across the United States, as it is based on rent paid, while the proposed child allowance is the same regardless of place of residence. The child allowance thus, in effect, provides smaller real benefits to families living in high-cost areas and larger real benefits to those in low-cost areas. The universal design of the proposed child allowance—with benefit levels that are the same nationwide and serving both poor and nonpoor children—has specific benefits, particularly politically, though consequently it has a substantially higher cost, with a larger share of benefits directed to individuals with less economic need. The renter’s credit is more targeted to the lowest-income households, which have a smaller share of nonpoor beneficiaries and thus lower costs, corresponding to a smaller number of individuals assisted, but this narrower targeting could also make it more vulnerable politically.

Why not simply expand existing affordable housing programs, such as the housing voucher program or the LIHTC? We believe that a renter’s credit delivered via the tax system is the most efficient and equitable way to get the most money into the hands of the families who need the most help. The voucher program is stymied by the fact that landlords must consent to be in the program and limits are placed on eligible units based on cost and housing quality inspections. Although the voucher program offers the very deep subsidies needed for the lowest-income households, these restrictions also make the program extremely expensive per household served. Thus the program is far too limited in its reach. A renter’s credit, by contrast, offers no restrictions on the housing units eligible for subsidies so it expands the supply of eligible units significantly. Because landlords and neighbors would not need to know who receives the credit, it may also be less stigmatizing than the voucher program.

Administration through the income tax system offers many advantages over the voucher administration system. Because most households file income taxes anyway, the administrative barriers to applying for and receiving the renter’s credit are much lower than the barriers to applying for and successfully using housing vouchers. The renter’s tax credit is also designed to function as a shallower subsidy that reaches a broader share of renters than existing housing vouchers. Indeed, largely replacing the existing highly rationed voucher program, which provides deep subsidies to some households while leaving the majority unassisted, with a wide-reaching refundable renter’s tax credit that is more accessible, more administratively efficient, and distributes assistance more evenly across housing-burdened households could offer benefits. A final advantage to administering the renter’s credit through the tax system is that subsidies offered through the renter’s credit would not be subject to annual appropriations votes in the same way as other subsidized housing programs, making the credit less subject to budget cuts and political gridlock.

We also believe that a renter’s credit delivered directly to cost-burdened renters is more advantageous than delivering a credit to landlords or to housing developers. The LIHTC is an important mechanism for increasing the supply of affordable housing via new construction and rehabilitation. But the housing it produces remains unaffordable to most low-income households and, even more significantly, a nontrivial share of the profits go to private investors, diverting funding that could be used to supply more affordable housing. We therefore argue that the proposed renter’s credit channels more money directly to cash-strapped households and as a result serves as a more effective anti-poverty program. Targeting subsidies to renters directly also means that renters have more choice over the locations and characteristics of their housing, and are not limited to the units that developers or landlords have chosen for participation in subsidy programs. This might have the added benefit of promoting greater racial and socioeconomic integration, given that landlords in the housing voucher program have been known to concentrate units disproportionately in poor and high-minority neighborhoods (Rosen 2014). On the downside, any effort to subsidize low-income renters on a large scale runs the risk of contributing to rent inflation, with some of the credit captured by property owners in the form of higher rents. Capping renter’s credits at FMR or a percentage of renters’ incomes, however, should help mitigate this concern.

What would it take to implement a renter’s credit like the one we have proposed here? Many of the administrative structures for delivering the credit are already in place, which is one key advantage of providing the credit via the tax system. The Internal Revenue Service (IRS) already requests most of the information needed to determine credit amounts; the only additional pieces of information that would need to be collected on tax returns are the tax unit’s nontaxable cash income (such as SSI or Temporary Assistance to Needy Families payments) and income of dependents (similar to the income data currently collected on Affordable Care Act health insurance tax forms), and rent paid. The FMRs used to cap the base credit amounts are already collected by the Department of Housing and Urban Development routinely every year for use in other housing programs. There is precedent at the state level as well: many state tax systems already offer tax rebates or credits for renters, often framed as a way to recoup some of the cost of local property taxes that renters pay indirectly through their rent. However, these systems are uneven across states in terms of their presence and generosity (see table A6). Following the lead of other refundable tax credits, the proposed renter’s credit would not need to be counted as income when determining eligibility for other means-tested programs. An additional benefit of administering the proposed credit via the tax system is that it would reduce the inequities in how homeowners and renters are treated under existing tax law.

Almost all families receive their tax rebates as a lump sum payment at the time they file their taxes. Rent payments are due on a monthly basis, however, which means that the timing of payment for the renter’s credit at tax time may not align with the timing of need for households facing high housing costs. If the misalignment in the timing of the credit and rent payments is a concern, the disbursement of the credit payments could be handled several ways. One option would be to offer a deferred disbursement plan, where the credit is paid out quarterly, at the same time that estimated tax payments are due (for a related proposal for deferred disbursement of the EITC, see Shaefer et al. 2018). A second option would be to allow tax filers who have some tax liability to take a deduction for the credit on their W-4s, which would increase the amount of money they keep in their paycheck each week. A monthly disbursement plan via another federal agency, such as HUD or the Social Security Administration (SSA), might offer more regular rental support, but some of that benefit would be eroded because such monthly payments would be counted as income when determining eligibility for other means-tested programs, and administrative costs would likely be higher.

Finally, how might a renters’ tax credit be funded? One possibility would be to fund the tax credit by reducing the subsidies that currently go to high-income homeowners. Currently, more than 75 percent of the tax expenditures devoted to homeownership via mortgage interest and property tax deductions go to homeowners who make more than $100,000 per year, at a cost of more than $70 billion per year (Center on Budget and Policy Priorities 2016b). Cutting these tax expenditures to fund a renter’s credit would improve both the horizontal and vertical equity of our tax and transfer system by shifting resources from affluent homeowners to poor renters. Another option would be to tax profits from residential rental property income, or to tax capital gains from residential real estate sales; either would allow for sharing some of the profits of landlords and property owners with renters burdened by high rental costs, though landlords’ passing on the taxes in the form of higher rents is a risk.

Overall, the proposed refundable renter’s tax credit is a promising policy tool to address the affordable housing crisis and reduce poverty. It offers efficient targeting, broad reach, low administrative burden for beneficiaries, and low administrative costs for the government, and it would achieve a noteworthy reduction in poverty. The renter’s tax credit can also be flexibly modified to achieve specific policy goals in terms of target households, depth of subsidy, and total cost. Innovative approaches such as this renter’s credit are urgently needed to reduce the high housing cost burdens faced by low-income households and the resulting problems of poverty and housing instability and all of their negative consequences.

APPENDIX

Renter’s Tax Credit Impact by State

Credit Reach, Cost, and Poor Beneficiaries by State

Credit Impact on Poverty Rate and Severe Housing Burden by State

Credit Results Targeting Children, Seniors, Residents of High Housing Cost States

Reach, Cost, Poverty Impact, and Housing Burden Impact for Credits Targeting Subpopulations

Modified Renter’s Tax Credit Targeting Households with Severe Housing Burden

The design of the renter’s tax credit allows for modification of the credit parameters to adjust the population targeted, the depth of the subsidy, and the total cost of the credit. Here we present an alternative version of the credit with modified parameters to target households with more severe housing burden.

The credit follows the same formula as that presented as our main results, except that a tax unit is eligible for the credit if they are expected to spend more than 50 percent of their total after-tax cash income on the average rental unit rather than 40 percent. The final credit amount for tax unit i is calculated as

Credit Amti = Capped Rent Paidi – (0.5 × After – Tax Incomei)

This modified version of the credit, then, targets a narrower population of households with more severe housing cost burden. Results for this modified credit are presented in the tables.

Alternate Credit Reach, Cost, and Beneficiary Demographics

Anti-Poverty Effects of Alternate Renter’s Credit

State-Level Renter’s Tax Credits

Expected Housing Cost Burden Before and After Alternate Credit

FOOTNOTES

↵1. Per authors’ calculations of Current Population Survey data 2012–2014 (Flood et al. 2016).

↵2. Developers must commit to reserving at least 20 percent of their units for households with incomes less than 50 percent of AMI (known as the 20-50 rule), or at least 40 percent of their units for households with incomes less than 60 percent of AMI (known as the 40-60 rule).

↵3. “Housing Choice Vouchers Fact Sheet,” http://portal.hud.gov/hudportal/HUD?src=/program_offices/public_indian_housing/programs/hcv/about/fact_sheet (accessed October 6, 2017).

↵4. “Open Public Housing Waiting Lists by State,” Affordable Housing Online, http://affordablehousingonline.com/public-housing-waiting-lists/ (accessed November 17, 2017).

↵5. Homeowners make up 43.6 percent of the SPM poor population in our data; renters make up 56.4 percent.

↵6. The primary purpose of this policy is to assist households facing ongoing high rent burdens, not to serve as an emergency safety net for households whose incomes have dropped dramatically due to a short-term crisis, hence the cap on claimable rent at 80 percent of after-tax income (which includes taxable and nontaxable unemployment benefits, disability benefits, and retirement income as well as refundable tax credits, over the course of a full year). Capping the claimable rent paid minimizes incentives to misreport rent paid or take on an unsustainable ongoing rent burden, and allows the renter’s credit resources to be focused on the primary target problem. Other policies such as homelessness assistance, homelessness prevention programs, public housing, and income support programs are better suited to address short-term housing crises or the chronic inability to secure enough ongoing income to achieve a rent burden of 80 percent or less. For this simulation of the renter’s tax credit in CPS data, capping the allowable rent paid at 80 percent of after-tax income also helps to minimize potential distortions of the estimated policy costs and poverty impact that could be introduced by our imputation of rent paid, as necessitated by the lack of reported rent paid in the CPS data.

↵7. Sample size for renters, our focal population, is n=187,181. We use a three-year sample (2013 to 2015) to maximize sample size for individual states and for demographic subgroups. In contrast, estimates of costs and poverty impact for this renter’s credit proposal presented elsewhere in this double issue use a one-year CPS sample, for 2015 only (Wimer, Collyer, and Kimberlin 2018).

↵8. Because the CPS does not collect information on rental costs, we impute rental cost values from the American Community Survey based on the following characteristics: number of adults, any young adults, any elderly adults, number of children, race of household head, any foreign-born household members, highest educational attainment in household, any household member receiving TANF, SNAP, SSI, or SS household income, FMR, state, metro or nonmetropolitan status, and survey year. Rent paid is imputed to the household or housing unit. We prorate the amount of rent paid by each tax unit as follows. First, we prorate rent paid to SPM family units within each household based on the number of individuals in each SPM family unit relative to the total number of individuals in the household (most households include only one SPM family unit, which includes all individuals related by blood or marriage as well as cohabiters and their relatives). Next, we prorate rent paid to tax units within SPM family units based on the share of after-tax income represented by each tax unit relative to the SPM family unit total income. This approach assumes that within SPM family units, family members will share rent expenses proportionate to their income.

↵9. FMR amounts are calculated as the population-weighted average FMRs for a two-bedroom apartment across all metropolitan areas and all non-metropolitan areas by state. FMR amounts are then adjusted for units with one, three, and four or more bedrooms based on the ratio of FMR costs for other size units relative to two-bedroom FMRs. For example, to calculate the FMR for a three-bedroom unit, the two-bedroom apartment FMR amount is multiplied by 1.3, which represents the mean ratio of FMRs for three-bedroom apartments to FMRs for two-bedroom apartments. The number of tax dependents is used to assign the number of bedrooms for the tax filer’s FMR, with the one-bedroom FMR assigned to filers with no dependents, two-bedroom to filers with one dependent, three-bedroom to filers with two dependents, and four-bedroom to filers with three or more dependents. This method of assigning FMRs thus utilizes only two FMR amounts for each state—the population-weighted average two-bedroom FMR for metro areas and nonmetro areas—simplifying administration of the credit. In addition, specific geographic location is not identified for more than half of the CPS sample, necessitating FMR assignment based on broader location data for the analysis.

↵10. EITC receipt is fully imputed in CPS data and thus not subject to the same level of underreporting.

↵11. As noted, the renter’s credit is designed to reduce rent burden from a maximum of 80 percent of after-tax income, and claimable rent paid is capped at 80 percent of income (out of consideration of both policy goals and simulation practicalities). That said, it would be possible to modify the renter’s credit to provide larger credits to households paying rent in excess of 80 percent of income, and to provide credits to households paying rent that have no after-tax annual income. A total of 4.74 million tax filers with nonzero income who were found to be eligible for renter’s credits had imputed rent paid (after capping rent at the appropriate FMR) equal to more than 80 percent of income. Allowing these filers to claim rent paid up to 100 percent of after-tax income, rather than capping the allowable rent at 80 percent of income, would increase the estimated annual cost by $2,844 million. Providing these filers with a refundable credit equal to their total imputed rent paid (after capping at the appropriate FMR), even if that amount exceeded total after-tax income, would increase the estimated annual cost by $12,232 million, a substantial increase. In addition, 3 percent of renter tax filers, or 1.86 million filers, had no reported after-tax income for their entire household (and did not report a housing subsidy). Providing these filers with a refundable credit equal to their imputed rent paid (after capping at the appropriate FMR) would increase the estimated annual cost by an additional $12,356 million.

↵12. Beneficiaries who start out above the poverty line have median family resources equal to only 127 percent of the poverty threshold.

↵13. These programs include tenant-based rental assistance, project-based rental assistance, Section 202 elderly housing, Section 811 housing for people with disabilities, and public housing.

↵14. Among renters who are SPM poor in the CPS data before assigning any renter’s tax credit, 43 percent are in families with reported SNAP, 49 percent are in families with reported EITC, 14 percent are in families with reported housing subsidies, and 60 percent are in families eligible for the renter’s tax credit.

↵15. Figures are per authors’ analysis of EITC receipt as imputed in CPS data.

- © 2018 Russell Sage Foundation. Kimberlin, Sara, Laura Tach, and Christopher Wimer. 2018. “A Renter’s Tax Credit to Curtail the Affordable Housing Crisis.” RSF: The Russell Sage Foundation Journal of the Social Sciences 4(2): 131–60. DOI: 10.7758/RSF.2018.4.2.07. We thank Meaghan Mingo for superb research assistance and the conference participants, reviewers, and editors for helpful feedback on earlier drafts of this manuscript. Direct correspondence to: Sara Kimberlin at skimber{at}stanford.edu, 450 Serra Mall, Bldg. 370, Stanford, CA 94305; Laura Tach at lauratach{at}cornell.edu, 253 Martha van Rensselaer Hall, Cornell University, Ithaca, NY 14853; and Christopher Wimer at cw2727{at}columbia.edu, 1255 Amsterdam Ave., New York, NY 10027.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.