Abstract

In this article we present new evidence that the capacity of households to cover earnings lost during spells of unemployment through a combination of drawing down of wealth and receipt of unemployment insurance and other transfer payments is very limited and has deteriorated since the 1980s. Since 2006, most households have not had nearly enough financial wealth to smooth their consumption over more than a very short spell of unemployment. Individuals experiencing involuntary job loss also tend to experience substantial earnings reductions upon reemployment, resulting in longer-term deterioration in household finances. Wealth inadequacy to cover lost earnings and the earnings reduction upon reemployment are both especially acute in long unemployment spells, such as those that were prevalent in the aftermath of the Great Recession.

The Great Recession not only was more severe in magnitude than other post–World War II economic contractions but also differed qualitatively in its impact on the labor market. Arguably the most important distinguishing characteristic of the Great Recession is the very large and persistent increase in long-term unemployment that it ushered in. The peak unemployment rate in the aftermath of the Great Recession was 10.0 percent, which is somewhat lower than the peak unemployment rate of 10.8 percent during the 1981-to-1982 recession. But, long-term unemployment rose much more during the Great Recession than it did in the early 1980s. The percentage of the labor force unemployed twenty-seven weeks or longer reached 4.4 percent, in early 2010, compared with an early 1980s high of 2.6 percent. The 2010 value was the highest since the Current Population Survey was started in 1948. The long spells of unemployment that became common during the Great Recession and its aftermath likely have a much more substantial impact on household finances and economic welfare than the shorter spells commonly experienced in prior recessions.

In this paper we examine the consequences of the Great Recession, and unemployment more generally, on household finances. In doing so we examine the extent to which households were in a position to maintain their consumption in the face of long spells of unemployment through a combination of drawing down their wealth and receipt of unemployment insurance and other social insurance benefits. We also examine the extent to which unemployed workers suffered a drop in earnings relative to their pre-recession level upon reemployment. Our conclusions are relatively pessimistic on both counts. Most workers are able to cover very few weeks of their reduced income during spells of unemployment by drawing down their financial wealth, and most also suffer substantial reductions in their earnings upon reemployment following a layoff or termination.

Our work most closely follows a study by Jonathan Gruber (2001) in which he examines how wealth buffers the effects of unemployment on consumption. Gruber concludes that workers with the median amount of wealth draw on it when unemployed so as to maintain two-thirds of their pre-unemployment consumption for the typical spell of unemployment. This requires them to draw down their wealth rapidly as their spells become longer. Gruber uses data from the U.S. Census Bureau’s Survey of Income and Program Participation (SIPP) panels for 1984 to 1992 for his analysis, and so his data contain relatively few spells of long-term unemployment.

Our study draws on SIPP data through the 2008 panel for which we have data up through mid-2013. This allows us to examine the consequences of the Great Recession, a contraction much more severe than the 1990-to-1991 recession that is captured in Gruber’s data. Using methodology similar to Gruber’s we find quite different results, with households in recent years being in a much worse position to self-insure against earnings disruptions than in the earlier period. We also use the SIPP to examine the distribution of earnings changes following job changes. Job changes that were precipitated by a layoff or termination typically result in substantial reductions in earnings upon reemployment, especially when a long spell of non-employment follows the initial job loss. Thus, households’ loss of earnings during a spell of unemployment is compounded by reduced earnings upon reemployment.

The Great Recession was especially hard for household finances because of the increased incidence of unemployment—especially long-term unemployment. Even before the Great Recession, many households were not in a position to cover more than a relatively minor earnings disruption by drawing down their wealth. Growth in wealth inequality since the 1980s has left those at the bottom of the distribution much less well prepared for unemployment. Further, the financial crisis and the Great Recession were accompanied by deterioration in household wealth. Finally, the Great Recession had a large effect on the household finances of those who became unemployed. The impact was greatly increased as the fraction of households that experienced layoffs and long spells of unemployment was much higher than in the past.

The rest of this paper is organized as follows: The first section is a survey of recent literature related to this topic. Next we present our empirical results on the ability of households to cover earnings disruptions by drawing down financial wealth. This is followed by presentation of our findings on the changes in labor earnings associated with job changes. The final section is a discussion of the implications of our findings.

RELATED LITERATURE

It is now well established that unemployment shocks have substantial and persistent effects on earnings. Bruce Fallick (1996) and Lori Kletzer (2008) survey early research documenting that workers undergoing involuntary separations tend to experience substantial reductions in earnings that extend for several years following displacement.

Following the insight of Robert Gibbons and Lawrence F. Katz (1991), research has focused on workers displaced during a mass layoff, since such displacements are unlikely to be confounded by selection on worker quality or productivity. Building on this literature, recent work by Till von Wachter, Jae Song, and Joyce Manchester (2009) examines the long-term effects of job displacements from mass layoffs during the 1982 recession. Using administrative records, they find that short-term annual earnings losses due to job displacement are approximately 30 percent, and that losses of over 20 percent persist fifteen to twenty years after displacement.

Aaron Flaaen, Matthew D. Shapiro, and Isaac Sorkin (2003) use data from the SIPP spanning 2001 to 2006 matched to administrative data from the Longitudinal Employer-Household Dynamics (LEHD) program to analyze the earnings losses associated with worker displacement. Interestingly, they find that the two data sources often disagree on whether a job separation is a quit, a termination unrelated to economic conditions, or a separation associated with distressed business conditions. In the case of large firms where the administrative data indicates that there is a mass layoff and the worker indicates that the separation is due to economic distress, the worker’s earnings tend to completely recover (relative to workers not separating from employment) within four years of the separation. This suggests that, at least during an economic expansion, a layoff that potential employers can readily identify as unrelated to worker quality results in little or no long-term depression of earnings.

It is debatable whether one should expect earnings losses associated with job displacement during a recession to be more or less persistent than those occurring during an expansion. On the one hand, widespread layoffs during recessions may lead to job separation being a weaker signal of low worker quality during a recession than if the job separation had instead occurred during an expansion, and Emi Nakamura (2008) provides some support for this view. However, the dearth of job opportunities during a recession may result in greater disruption of career trajectories when worker displacement occurs during a recession rather than during an expansion. Using unemployment insurance administrative records for Connecticut, Christopher D. Couch, Nicholas A. Jolly, and Dana W. Placzek (2011) find that the long-term earnings losses of workers displaced during a recession are substantially larger than the long-term earnings losses of those displaced during expansions. Steven J. Davis and Till von Wachter (2011) use a long panel of Social Security earnings records to show that the magnitude of lost earnings associated with displacement in a mass layoff when the unemployment rate is above 8 percent is about double the magnitude of lost earnings associated with displacement when the unemployment rate is below 6 percent. Till von Wachter and Elizabeth Weber Handwerker (2009) examine the consequences for workers of being displaced in a mass layoff in California during the strong economic expansion of the 1990s. They find that although earnings are depressed in the short term, the average displaced worker does not suffer a permanent earnings loss. Overall, research points toward displacement during recessions being associated with more persistent consequences for earnings than with job displacement during expansions.

Recent research by Joseph G. Altonji, Anthony A. Smith, and Ivan Vidangos (2013) decomposes earnings losses from a spell of unemployment into a shorter-lived loss of earnings from a decrease in hours worked, and a more persistent loss in earnings attributed to a decreased hourly wage upon reemployment. The latter could be due to loss of tenure, movement to a lower-paying job, or decline in the worker’s human capital. Further research has broken down the impact of income shocks by income groups and suggests that positive shocks to high-income individuals are transitory, whereas negative shocks are persistent. For low-income individuals, positive shocks to income are found to be persistent, whereas negative shocks to income for low-income workers are transitory (Guvenen et al. 2015).

Looking at how workers fared after initial spells of unemployment during the Great Recession, it was found that a drop in earnings often follows an unemployment spell (Dickens and Triest 2012). That study was only able to look at data from the SIPP through 2010, so in this article we expand on the idea of job stability and outcomes using a larger dataset that includes longer spells of unemployment.

The persistent drop in earnings associated with worker displacement implies that many households will need to permanently lower their life-cycle consumption. However, the drop in income during an unemployment spell is often especially severe, and people would be expected to prepare to smooth consumption after job loss. One method to do so is through drawing down wealth, as highlighted in our discussion of the article by Jonathan Gruber (2001). Christopher D. Carroll, Karen E. Dynan, and Spencer D. Krane (2003) examine whether savings (and thus wealth) respond to the risk of unemployment. They find that increased unemployment risk does not lead to an increase in household savings for those who have low permanent income, whereas those with middle to high permanent incomes increase their precautionary savings when there is an increased risk for unemployment. These increases in precautionary savings can be seen in broad measures of wealth that include home equity, but not when a narrower measure of wealth excluding home equity is used.

Another possible method of consumption smoothing comes from borrowing and unsecured debt. James X. Sullivan (2008) finds that when unsecured debt is used as a form of insurance against income shocks, it is done by those who have some assets, and not done by those who have few or no assets. That article has a similar motivation to ours, but examines a different mechanism for maintaining consumption in the face of lower income.

Social insurance and transfer programs such as unemployment insurance, food stamps, and disability insurance serve to partially insure against unemployment risk. Hamish Low, Costas Meghir, and Luigi Pistaferri (2010) find that the welfare value of food stamps is greater than that of unemployment insurance in insuring against unemployment risk. Using data similar to the data we use, Richard W. Johnson and Alice G. Feng (2013) examine income losses among workers who were unemployed six or more months during the Great Recession and its aftermath. They find that although unemployment benefits helped to cushion the impact of job loss, half of job losers were not receiving unemployment benefits six months into their unemployment spells. In addition to receipt of social welfare and insurance benefits, a family’s income loss during unemployment may be buffered by other family members increasing their work hours while one family member is unemployed. The relative importance of the various methods to smooth consumption and income varies both across households and across points in time (Blundell 2014).

It is plausible that financial wealth allows individuals to be pickier when evaluating job offers, and may also allow unemployed people to engage in less intensive job searches than they otherwise would. This would generate a negative correlation between pre-unemployment wealth and the probability of reemployment, and a positive correlation between pre-unemployment wealth and the duration of completed unemployment spells. However, research has shown that employers tend to screen out job applicants with spells of non-employment lasting more than six months (Ghayad 2014), which would tend to discourage individuals from using their wealth to extend unemployment spells.

INCOME REPLACEMENT WITH HOUSEHOLD WEALTH AND UNEMPLOYMENT INSURANCE

Gruber (2001) used the SIPP to identify spells of unemployment, wages of those employed prior to a spell of unemployment, the wealth of those employed prior to a spell of unemployment, and the receipt of unemployment benefits, to analyze the extent to which wealth and unemployment insurance (UI) were adequate to replace lost earnings in the 1984-to-1992 period. Using later panels of the SIPP, we extend Gruber’s analysis to see how well people were prepared for the unemployment experienced during the Great Recession.

Due to differences between the questions in the SIPP and the Current Population Survey (CPS) it is not possible to exactly replicate the official definition of unemployment that comes from the CPS. Instead, we define someone as unemployed for a week if during that week the person was not employed and looked for work or if he or she reported being on temporary layoff. The SIPP tells us employment status on a weekly basis. We assume that if someone reports being unemployed during a week, that the person is unemployed for the entire week. We omit unemployment spells that began before the first wave of the panel (left-censored spells), but include spells that are still ongoing when the SIPP panel ends (right-censored spells) and spells that begin or end with missing data. Inclusion of the ongoing spells (and treating them as though they ended as of the end of the SIPP panel) and those that begin and end with missing data will tend to overstate the extent to which individuals could make up for lost earnings by drawing down financial wealth. An exception to treating missing data as ending a spell of unemployment is when there were less than 16 weeks of missing data between weeks of unemployment. In that case we treated the entire period of missing data as part of the spell of unemployment.

Following Gruber, we use three different definitions of wealth. Gross financial wealth is measured at the household level and includes savings and checking accounts, and the value of securities owned. It is a measure of readily accessible funds that can be used to smooth consumption. We chose not to include 401(k)s, 403(b)s, KEOGHs, or IRAs in this category because accessing them typically incurs substantial penalties. Net financial wealth subtracts all debts from gross financial wealth, including both secured (car loans, mortgages) and unsecured (credit cards) debt. Total net worth, as defined by the SIPP, adds the value of real property and the value of retirement accounts to arrive at net financial wealth.

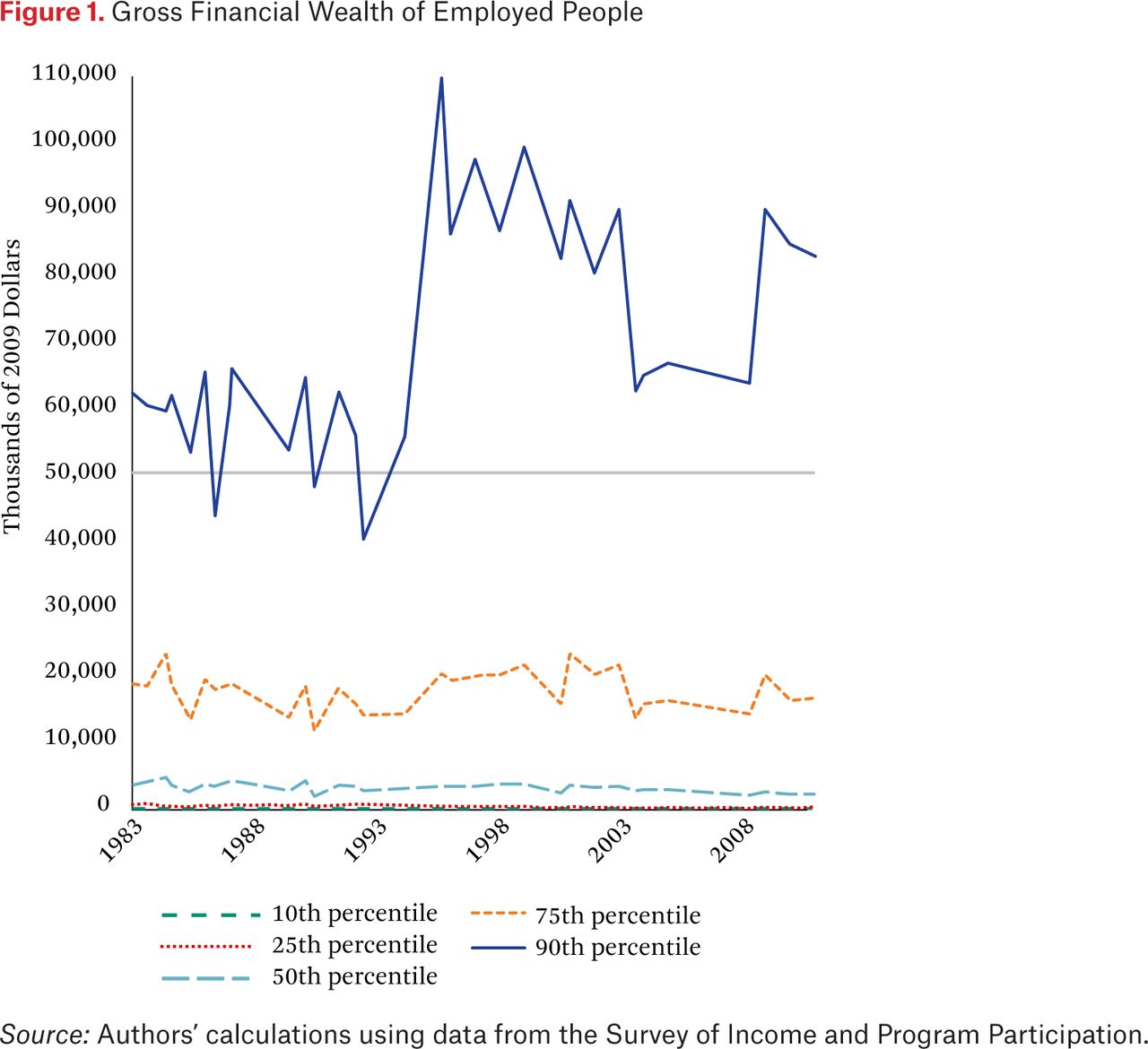

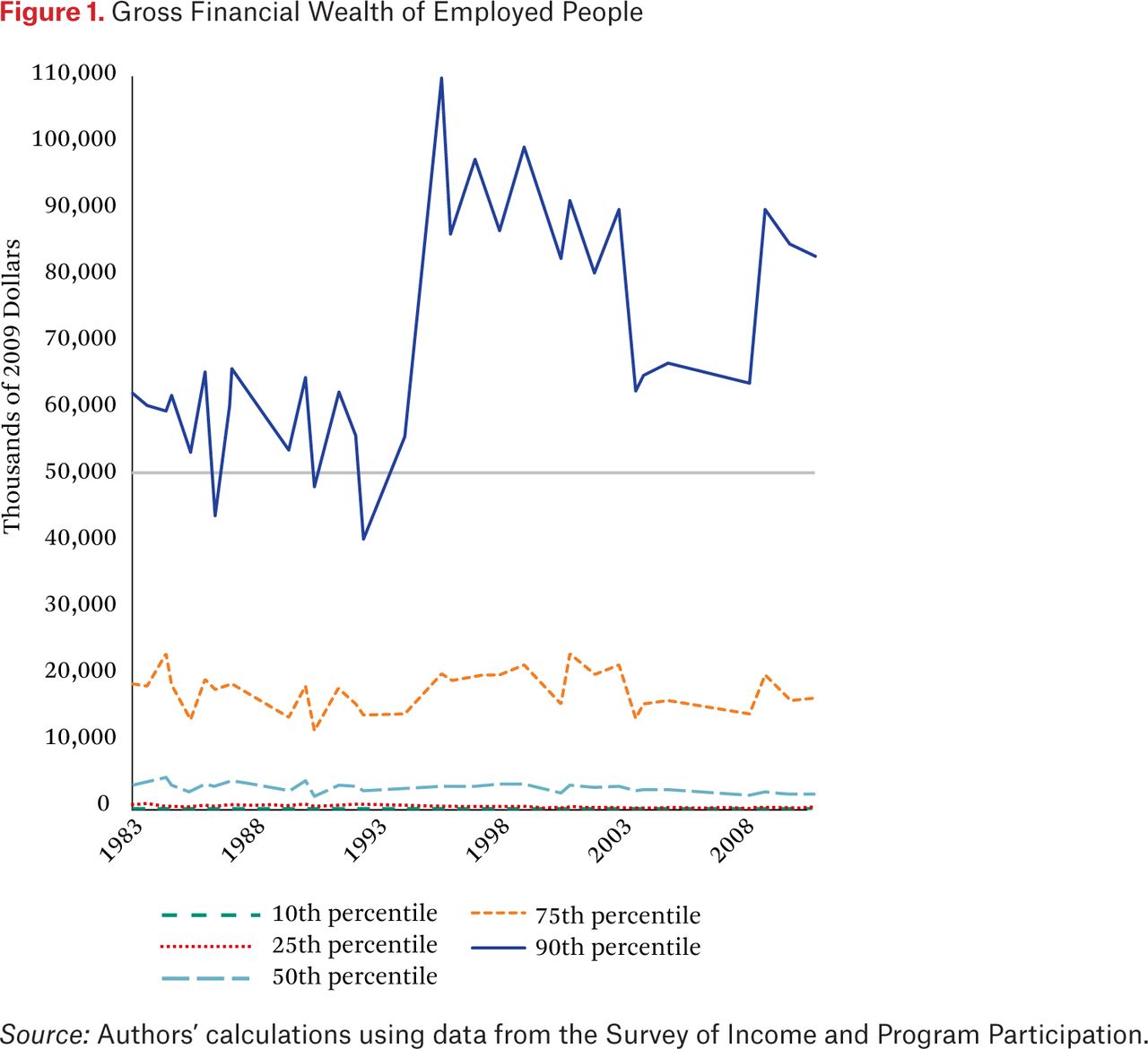

The distribution of real (inflation adjusted, measured in 2009 dollars) gross financial wealth held by employed people is shown in figure 1, for dates when wealth information was collected in special topical modules of the SIPP. This figure shows that wealth has been very unevenly distributed during the past three decades and that most employed people have very little financial wealth that could be drawn down to use for consumption spending during a spell of unemployment. Gross financial wealth is zero for the bottom 10th percentile for all years, and the 25th percentile of the distribution is either zero or just slightly greater than zero. Median gross financial wealth is small. The 75th percentile of the gross financial wealth distribution has a somewhat erratic pattern. The 90th percentile is also erratic but shows a clear increase between the 1980s and the later period.

Gross Financial Wealth of Employed People

The distribution of wealth for those who become unemployed would be expected to differ somewhat from that of all employed people. Table 1 displays the distribution of our three wealth measures for individuals starting a spell of unemployment subsequent to dates when the SIPP collected information on wealth holdings (again, all dollar amounts are in terms of constant 2009 dollars). We start with the observation that net financial assets and total net worth both declined between the earlier period, analyzed by Gruber, and the start of the Great Recession. In contrast, wealth in the upper part of the total net worth distribution increased over time, as did gross and net financial wealth at the 90th percentile, reflecting a marked increase in wealth inequality over the period covered by our data. Overall, it is striking that individuals in the lower part of the wealth distribution clearly were not in a position to draw down financial wealth to compensate for earnings lost during a spell of unemployment.

Wealth Percentiles for Unemployed Sample

Wealth relative to income is more relevant than the dollar amount of wealth in gauging how well equipped people are to smooth over earnings losses during spells of unemployment by drawing down their wealth. This is addressed in table 2, which shows the distribution of wealth relative to weekly earnings. The number of weeks of earnings that could be covered by drawing down gross financial wealth remained quite small for most of the distribution. At the median of the distribution of the ratio of gross financial wealth to weekly earnings, gross financial wealth could cover six weeks of earnings when measured by the SIPP in the early 1990s, but by the start of the Great Recession this had fallen to approximately three weeks. Someone at the 75th percentile of the distribution would have been able to cover approximately thirty-one weeks of earnings by drawing down financial wealth at the start of the Great Recession, with some evidence of a moderate downward trend over time. Looking at net financial wealth, even at the 75th percentile of the distribution individuals would be able to cover only eleven weeks of lost earnings at the start of the Great Recession, down considerably from the 1990s. Analysis of total net worth provides a somewhat more favorable picture, although even by this measure there is little scope for much of the population to draw down wealth to cover lost earnings.

Ratio of Wealth to Earnings on Previous Job for Unemployed at Different Percentiles of the Wealth Earnings Rate

It is debatable whether gross financial wealth, net financial wealth, or total net worth is most relevant to the question of how well equipped people are to compensate for earnings lost while unemployed by drawing down wealth. A case can be made that gross financial wealth is the most relevant measure, because it best reflects the relatively liquid assets that can be readily drawn down and which may have been accumulated partly for precautionary purposes. Total net worth, in contrast, includes the value of illiquid assets that would be difficult to tap for purposes of smoothing consumption expenditures while unemployed. If credit lines collateralized by illiquid assets, such as a home equity line of credit, had been established before the start of an unemployment spell, then the illiquid assets might be drawn down through increasing debt. However, once an unemployment spell starts the potential borrower becomes much less credit-worthy and new or increased lines of credit would become difficult or impossible to obtain. If existing loans or lines of credit must be repaid over a fairly short time frame, then a case can be made that net financial wealth is the measure most relevant to our analysis.

Table 3 provides more direct information on the adequacy of wealth to cover earnings losses while unemployed. The “median” column shows the median fraction of lost earnings (calculated as pre-unemployment normal weekly earnings times the length of the completed unemployment spell in weeks) that could be covered by drawing down wealth. The other columns show the percentage of spells where wealth could potentially cover 10, 25, 50, or 100 percent of the earnings lost to unemployment.

Ratio of Wealth to Earnings Lost Due to Unemployment

There has been a clear deterioration over time in the potential for gross financial wealth to cover the earnings lost during unemployment spells. By the start of the Great Recession, the median amount of lost earnings that could be covered by gross financial wealth was only 57 percent, down from 128 percent in 2001 and 138 percent in 1990. During the Great Recession, gross financial wealth were insufficient to cover even 10 percent of lost earnings for about 40 percent of unemployment spells. Although gross financial wealth covers only a relatively modest proportion of earnings lost in most unemployment spells, during the Great Recession it was sufficient to cover 100 percent of lost earnings for about 45 percent of spells (down from over half in the 1990s). This reflects a combination of there being many short unemployment spells, which can be covered with very modest wealth, and a high degree of inequality in the wealth distribution, with some people capable of covering earnings lost during long spells with their wealth.

As expected, relative to gross financial wealth, a smaller fraction of lost earnings can be covered by net financial wealth and a larger fraction can be covered by total net worth. Strikingly, the fraction of lost earnings that can be covered by wealth decreases over time for all three of the wealth measures that we examine. Clearly, by the time of the Great Recession people were less equipped to cover earnings losses by drawing down wealth than they had been in previous recessions.

In addition to drawing down wealth, individuals may also be able to use social welfare and insurance benefits to cover lost earnings. Tables 4 and 5 shed some light on the quantitative importance of transfer payments to the unemployed. The distribution of benefits from several transfer programs during spells of unemployment is shown in the top panel. Each row in the table shows the benefits received by unemployed individuals at the indicated percentile of the distribution of benefits received for the specified program; rows for the 50th percentile and below are not shown because benefits were zero at these percentiles for all programs in all of the time periods shown. Benefits from any given transfer program are received in only a very small minority of spells. Most unemployed individuals are either not eligible for many of the benefit programs, or do not elect to participate. Consequently, benefit receipt is positive only at the very top of the distribution for most benefit programs.

Value of Benefits Received by All Unemployed in the 75th and 90th Percentile

Value of Benefits Received by Those Receiving Benefits (Dollars)

The relatively small fraction of the unemployed receiving UI benefits in our data is consistent with that found in the Current Population Survey (CPS). Examining data from the March 2005 special CPS supplement, Wayne Vroman (2009) finds that 24 percent of unemployed people indicate that they received unemployment insurance benefits; the equivalent calculation for March 2005 in our data yields 26 percent. He notes that the rate of UI benefit application found in the CPS supplement is close to that found in UI program administrative data, suggesting that the CPS estimates are reasonably accurate. The primary reason for the low UI benefit recipiency rate is that most people who meet the official definition of unemployment do not file for benefits (Wandner and Stettner 2000). In the 2005 CPS supplement, over half of the unemployed who do not apply for benefits indicate that they believe that they are not eligible for benefits (Vroman 2009).

The distributions of benefits from transfer programs for unemployed individuals who are recipients of benefits from the program are shown in table 5. Although only a minority of unemployment spells involve receipt of benefits from any given transfer program, transfers play a large role in replacing income—relative to wealth—for those who do receive benefits.

Social welfare and insurance benefits are also quantitatively important as a source of funds for covering earnings lost during spells of unemployment. Table 6 displays for several demographic groups, and by duration of unemployment, the median percentage of earnings lost due to an unemployment spell that could be covered by gross financial wealth or by gross financial wealth plus cumulative benefits from all of the transfer programs shown in table 5. Transfer payments substantially increase the percentage of lost earnings that can be covered, although there is still a clear deterioration over time in the percentage of lost earnings covered, even when transfer payments are included.

Percentage of Loss Covered by Gross Financial Wealth and Wealth Plus Benefit for Median Worker

There are stark differences over demographic groups in the median percentage of lost earnings covered. Young (less than twenty-five years old) and relatively old (over fifty-five years old) workers have a high median percentage of lost earnings covered (the young because many are living with their parents), although the median percentage decreases going into the great recession. Wealth and transfer payments make substantial contributions to earnings replacement for both of these groups.

The median percentage of lost earnings covered by wealth is very low for single adult households with children and for prime-working-age (twenty-five to fifty-five years old) nonwhite workers. Transfer payments provide some protection against earnings losses for both of these groups, but the median percentage of lost earnings replaced by transfer payments decreases over time for both groups. The median percentage of lost earnings replaced by transfer payments during spells of unemployment that started early in the Great Recession is just 1 percent for single adults with children and 14 percent for prime-working-age nonwhite individuals. Members of these groups are very vulnerable to economic deprivation during long unemployment spells.

The duration of the unemployment spell has a strong association with the extent to which wealth, or wealth plus benefits, cover lost earnings. Those who are unemployed for very short periods of time are reasonably well prepared to cover their earnings loss, but those who experience a long spell of unemployment tend to be very poorly prepared. This is not surprising—the adequacy of a given amount of wealth decreases as the length of the time without current earnings increases. That said, the contrast between the rows for all unemployed and the rows pertaining to those with unemployment spells exceeding twenty-five weeks is stark.

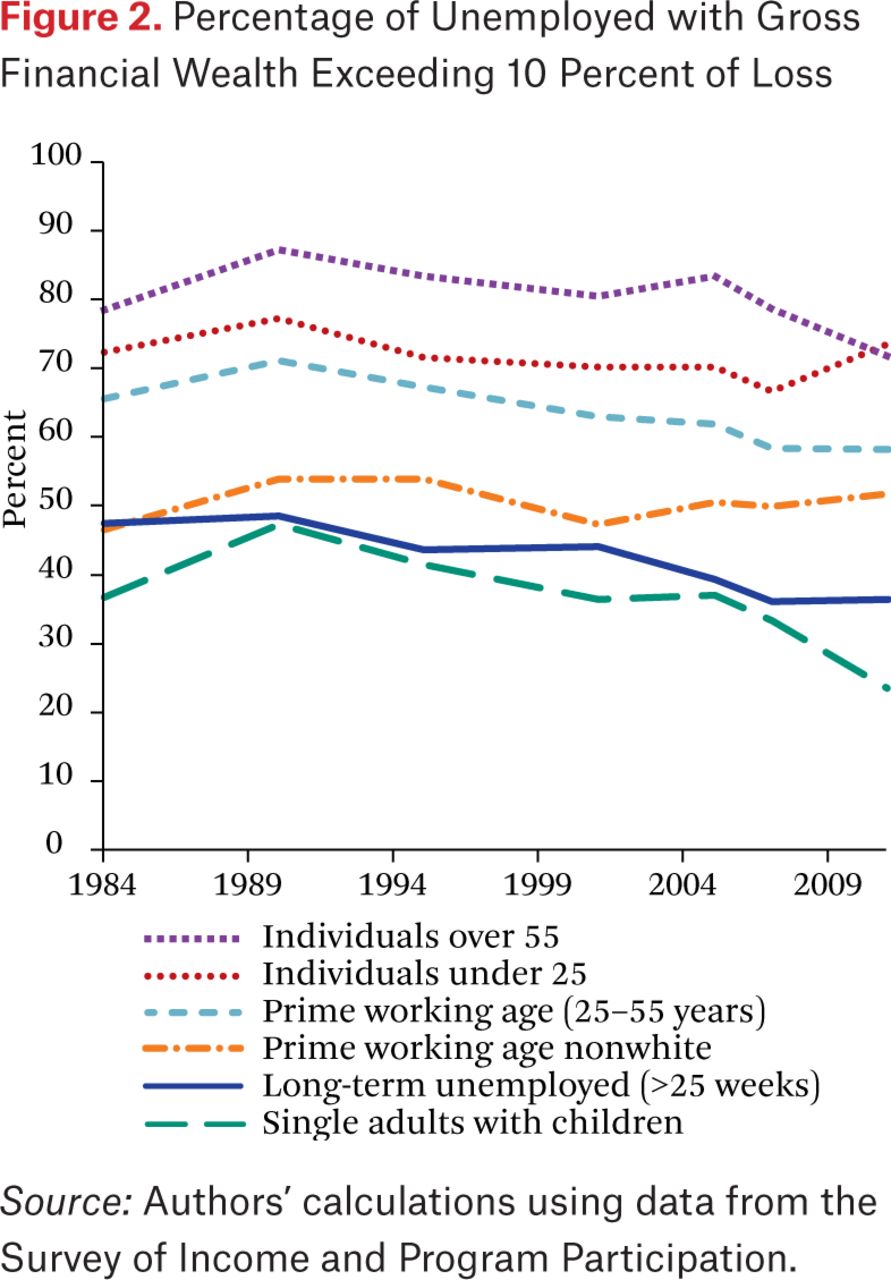

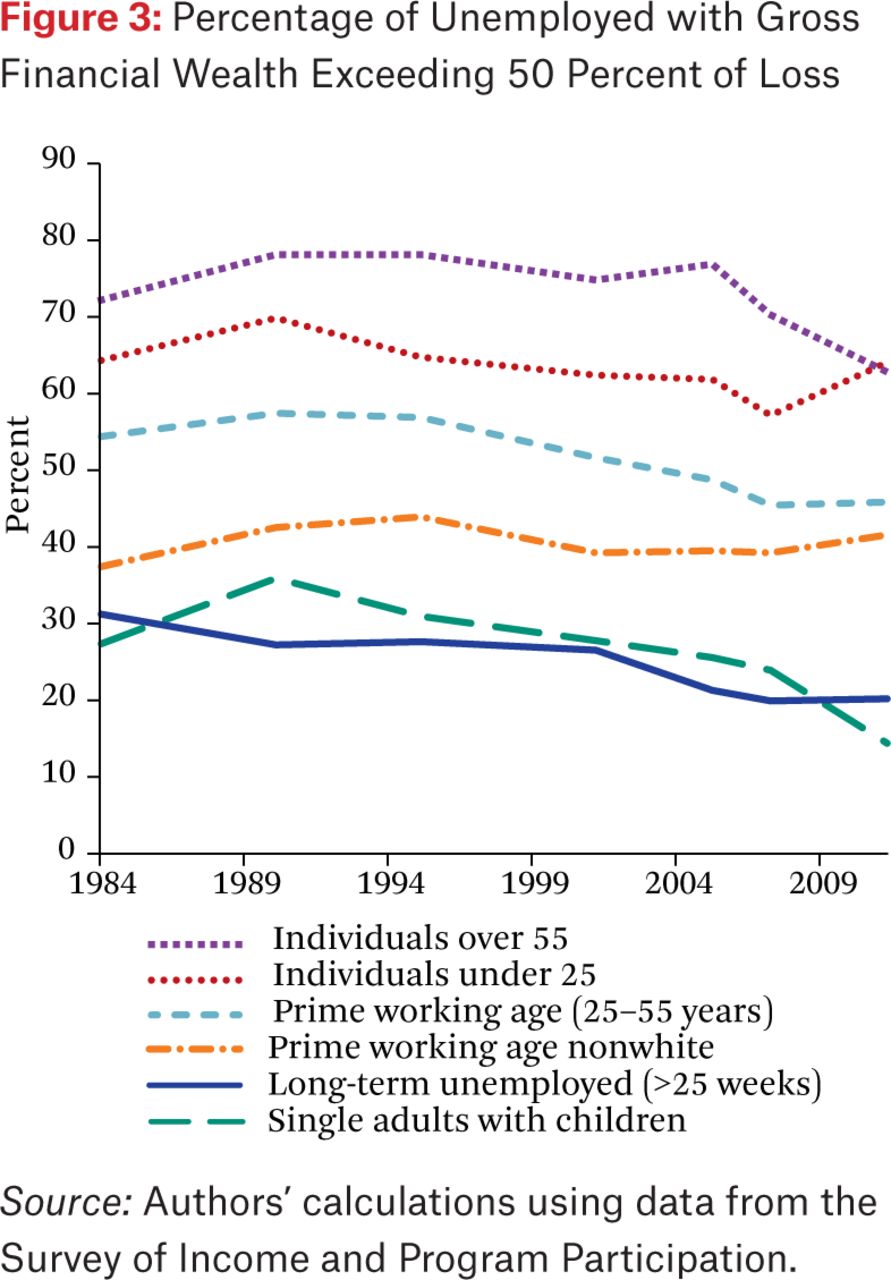

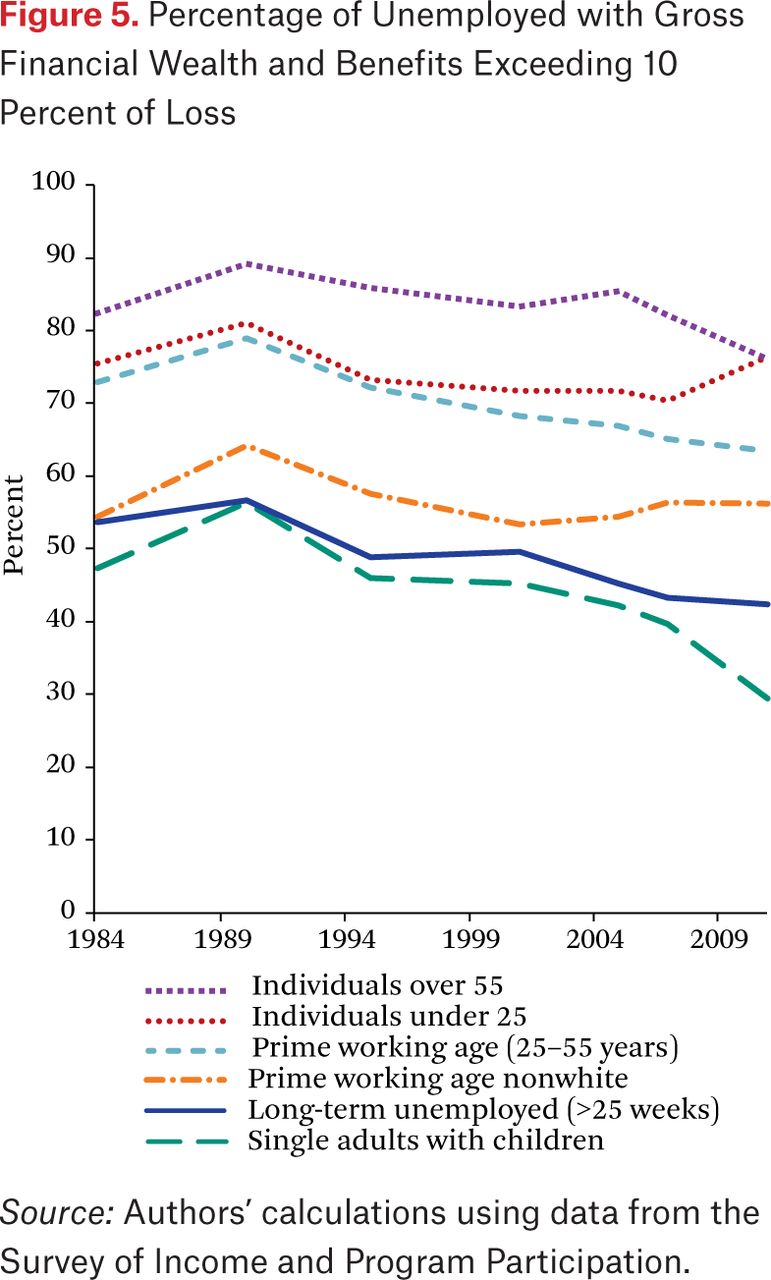

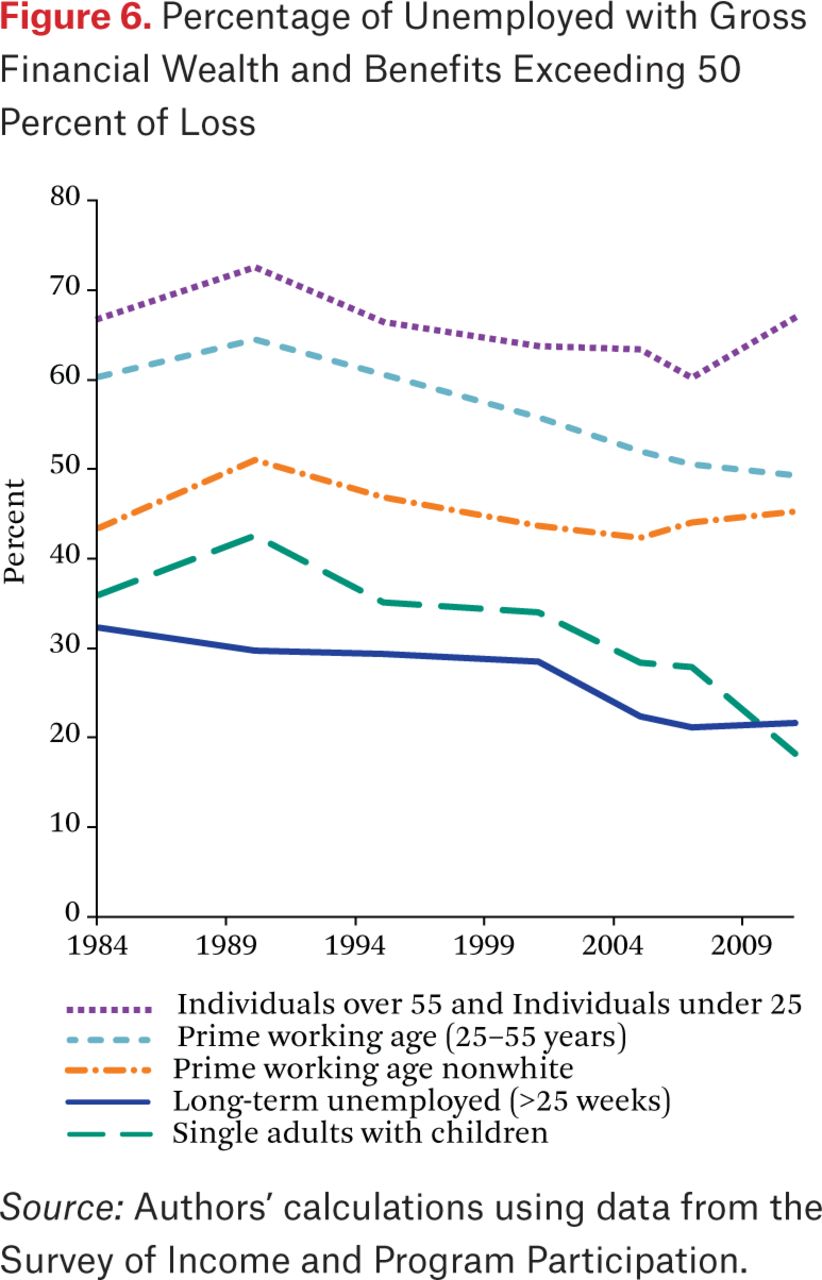

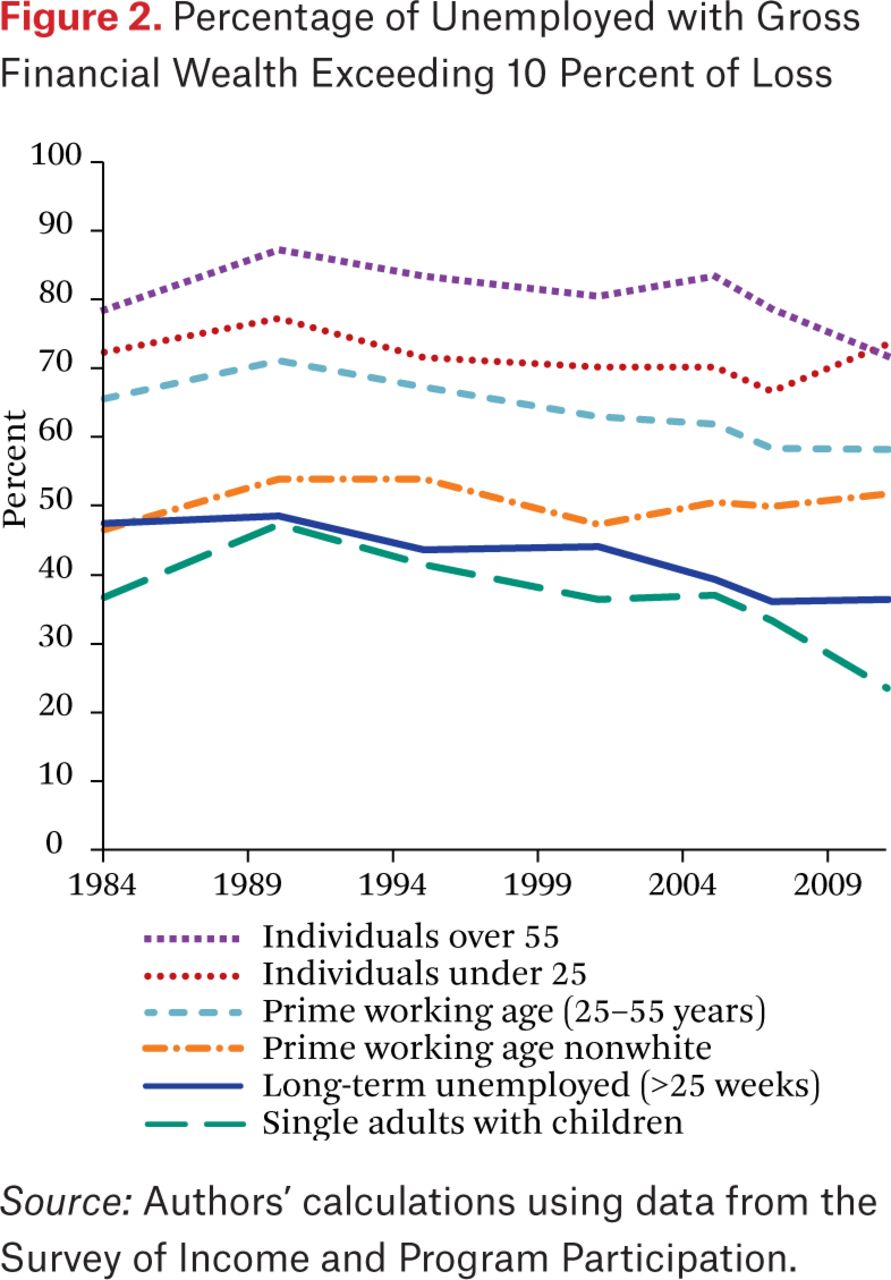

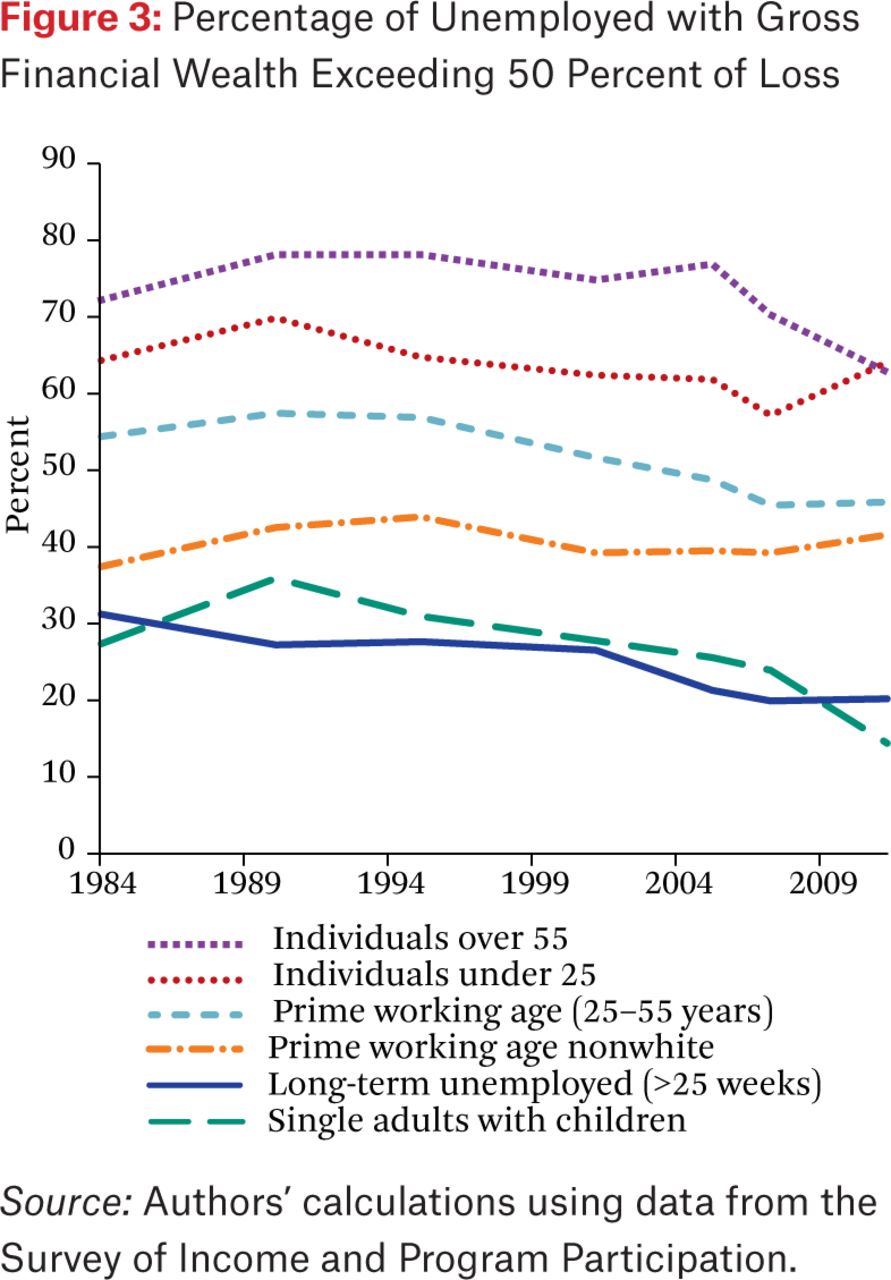

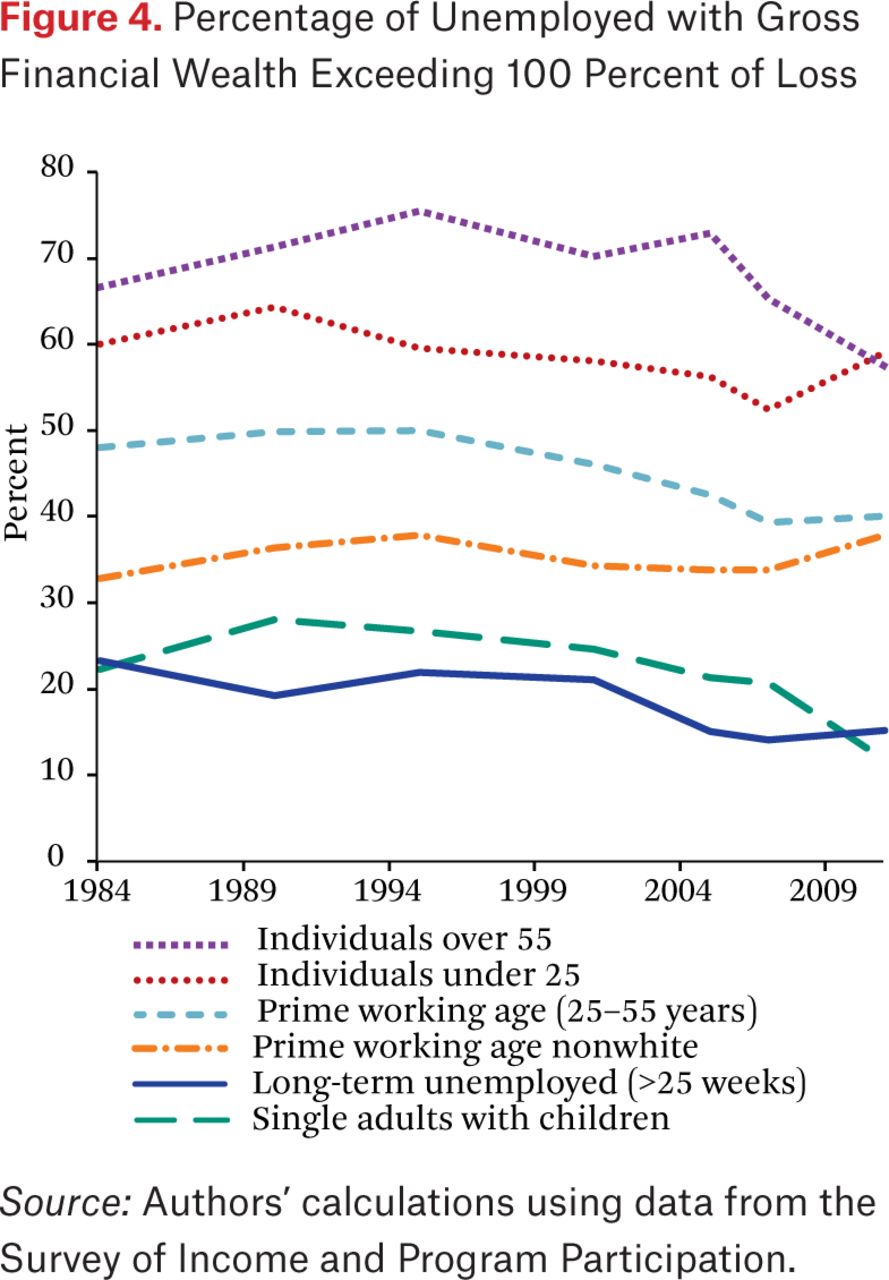

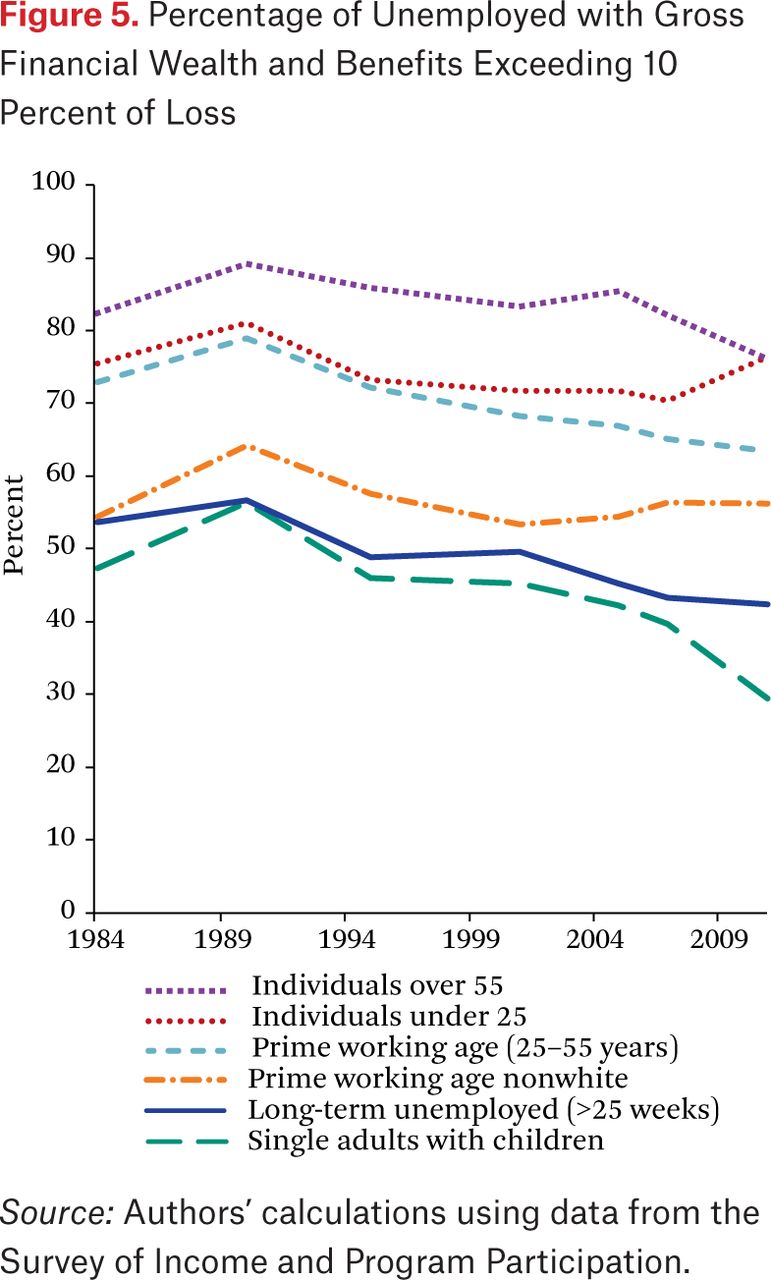

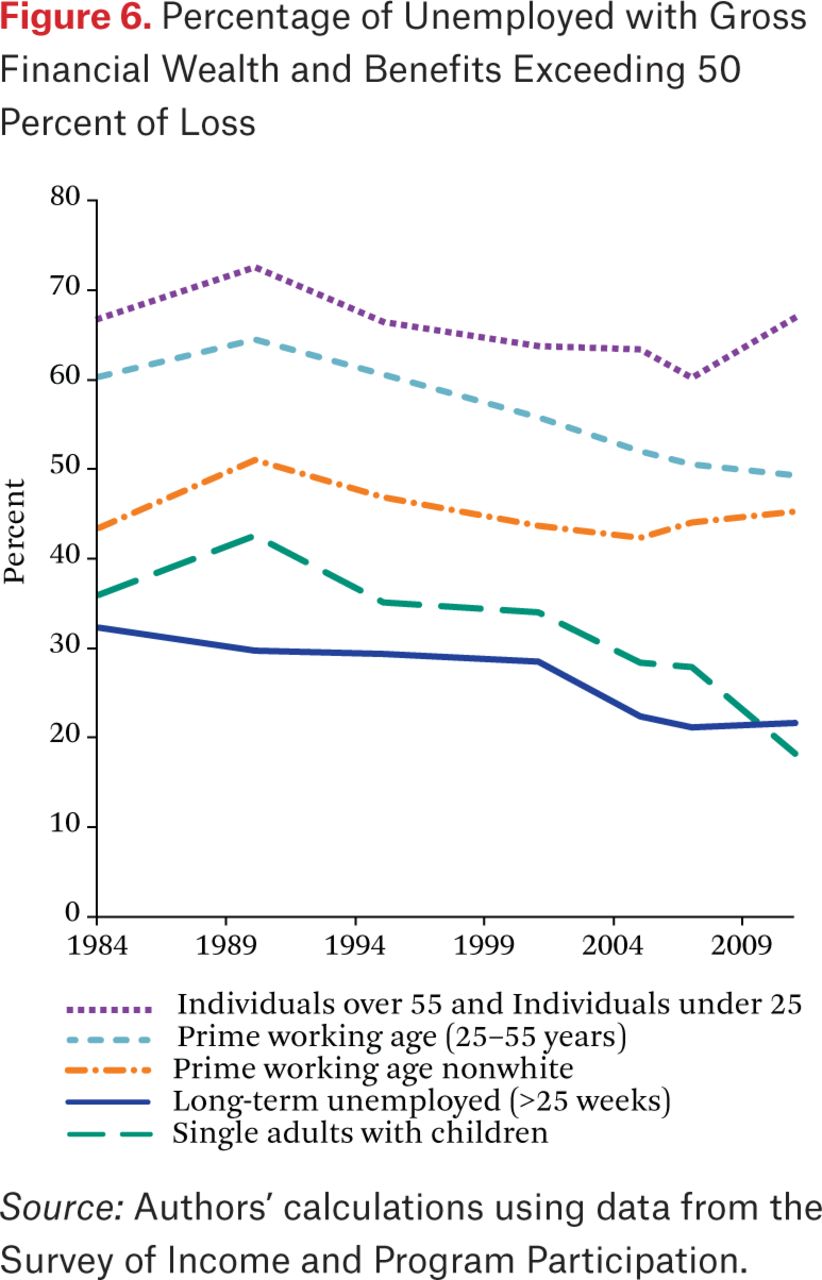

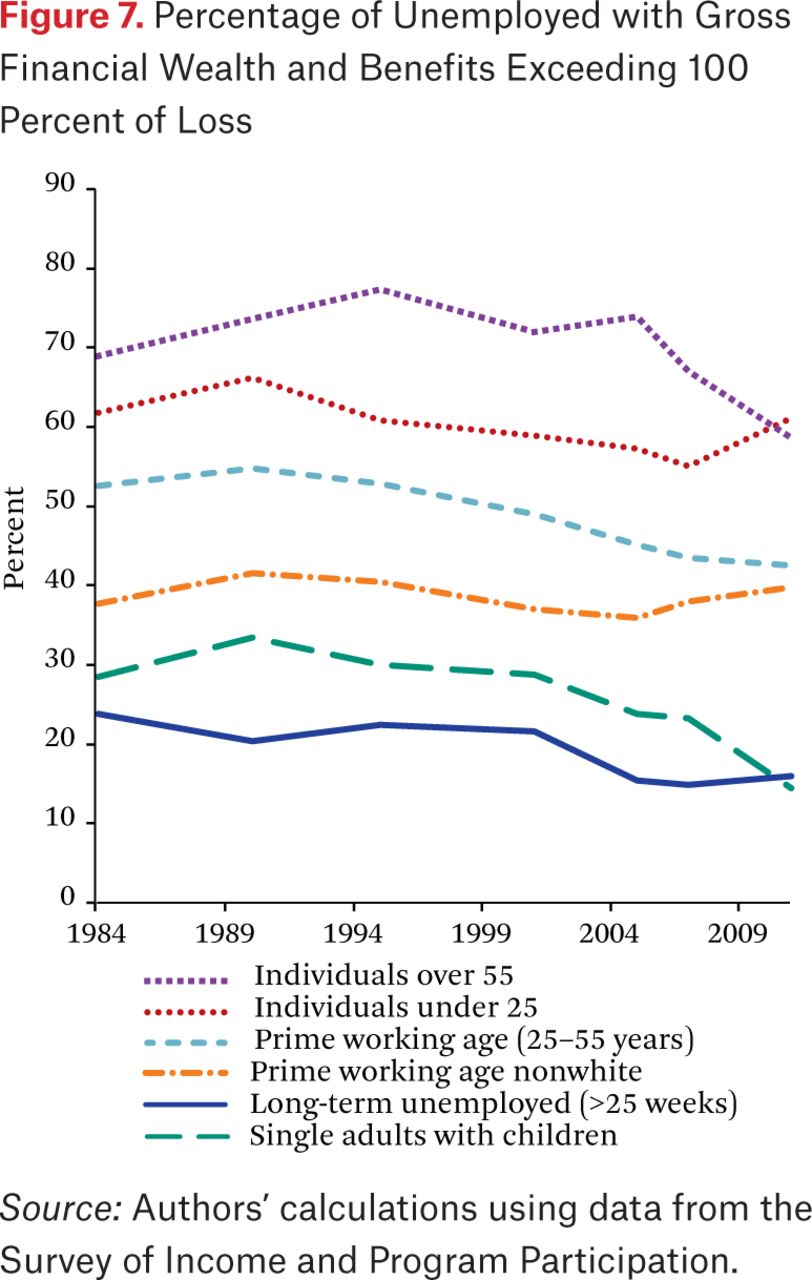

Further information on the role of transfer payments in covering earnings losses for the demographic and duration groups that we consider is shown in figures 2 through 7. Figures 2, 3, and 4 display the percentage of unemployment spells where at least 10 percent (figure 2), 50 percent (figure 3), and 100 percent (figure 4) of lost earnings could potentially be covered by gross financial wealth. Figures 5, 6, and 7 display the same information, but adds transfer payments to gross financial wealth in calculating the percentage of lost earnings potentially replaced.

Percentage of Unemployed with Gross Financial Wealth Exceeding 10 Percent of Loss

Percentage of Unemployed with Gross Financial Wealth Exceeding 50 Percent of Loss

Percentage of Unemployed with Gross Financial Wealth Exceeding 100 Percent of Loss

Percentage of Unemployed with Gross Financial Wealth and Benefits Exceeding 10 Percent of Loss

Percentage of Unemployed with Gross Financial Wealth and Benefits Exceeding 50 Percent of Loss

Percentage of Unemployed with Gross Financial Wealth and Benefits Exceeding 100 Percent of Loss

Figures 2 through 7 reinforce the findings from table 6 that single adults with children, prime-working-age nonwhite individuals, and those who experience long spells of unemployment are especially disadvantaged in replacing earnings lost during spells of unemployment. The figures also reinforce the finding that the percentage of lost earnings potentially replaced either by drawing down gross financial wealth or through the combination of transfer payment receipt and drawing down gross financial wealth has decreased over time.

Comparison of figures 2 and 5 suggests that transfer payments reduce the variance over demographic groups in the percentage of spells where at least 10 percent of lost earnings can potentially be replaced. This phenomenon holds to a much lesser extent for the percentage of spells where at least 50 percent or 100 percent of lost earnings can potentially be replaced, especially for those with long unemployment spells. Social welfare and insurance benefits provide an important safety net, albeit one that provides only a small degree of insurance.

EMPLOYMENT AND EARNINGS INSTABILITY

Unemployment can continue to affect household finances even after an unemployment spell ends with reemployment in a new job. As previously discussed, earlier research has found that individuals often suffer a decrease in earnings relative to their pre-job loss level following an unemployment spell that ends in reemployment. In this section, we present new estimates showing that, on average, those leaving jobs involuntarily (that is, due to layoff or termination) during the Great Recession and its aftermath suffered very large reductions in earnings upon reemployment. The loss of earnings while unemployed is only part of the hit to household finances due to unemployment. The reduction in earnings upon reemployment is also a major source of financial stress, and may be longer-lasting than the spell of unemployment.

Table 7 displays the distribution of the percentage change in real monthly earnings between wave 1 and the first month with positive earnings following reemployment for individuals who were employed in wave 1, subsequently involuntarily lost their wave 1 job within the first two years of the SIPP panel, and were then reemployed before the end of the panel.1 We include only those losing a job within the first two years of each panel to reduce the problem of not observing the completion of spells of non-employment. The 2008 panel row indicates the consequences for earnings of losing a job during the Great Recession and its aftermath, the 2004 panel row indicates the consequences for earnings of losing a job during more normal labor market conditions, the 2001 panel row reflects the consequences of job loss and reemployment during the slow recovery from the 2001 recession, and the 1996 panel row reflects the experience of workers losing a job and becoming reemployed during the late 1990s economic boom.

Percentage Change in Earnings from Previous Employment to Initial Earnings in New Employment for Involuntary Job Changers

The percentage reduction in earnings for job losers is quite large both for those losing jobs during the Great Recession and for those losing jobs during the period of more normal labor market conditions preceding the Great Recession. The magnitude of the percentage drop in earnings upon reemployment is roughly the same for those losing jobs during the first two years of the 1996, 2001, and 2004 SIPP panels but earnings losses are substantially larger for those losing jobs during the first two years of the 2008 panel. For example, the median reduction in real monthly earnings for those losing jobs during the first two years of the 2004 panel is 24 percent in the first wave following reemployment, while the corresponding earnings reduction for those losing jobs during the first two years of the 2008 panel is 37 percent. This suggests that the Great Recession caused a large increase in the magnitude of job-loss-related earnings reductions relative to the pre-recession era, due to both the large increase in the percentage of workers losing jobs and also the substantial increase in the percentage reduction in earnings for workers who lost jobs. Members of the 2008 panel who involuntarily left jobs were also much more likely to experience a long period of non-employment than those who lost jobs in the pre–Great Recession era, implying that job loss during the Great Recession or its aftermath necessitated a need to stretch available financial resources over a longer period of joblessness than in the earlier era.

Table 8 is identical to table 7 except that it measures the percentage change in monthly earnings between that in the first-wave job and mean monthly earnings in all remaining months of the panel following the start of the first new job rather than just the first month following start of the new job. The percentage reduction in monthly earnings over the remainder of the panel relative to that immediately upon reemployment depends on the general strength of the labor market. In a tight labor market, such as that of the late 1990s, there are likely to be more favorable opportunities for job hopping and wage growth than in a slack labor market, such as that following the Great Recession. Non-employment spells following loss of an initial reemployment job are also likely to be longer in a slack labor market than in a tight labor market. For these reasons, one would expect earnings upon reemployment over the rest of the panel to be more favorable relative to that immediately upon reemployment in a tight labor market than in a slack labor market.

Percentage Change from Previous Earnings to Average Earnings Following Reemployment for Involuntary Job Changers

This prediction is supported by table 8. The distribution of the change in monthly earnings over the rest of the panel is more favorable for most of the distribution relative to the distribution of the change in earnings immediately upon reemployment for job losers in the tight labor market experienced by members of the 1996 panel. This is also true for the members of the 2004 and 2008 panels, who experienced weaker labor market conditions, but to a much lesser extent. A key conclusion that one can draw from the comparison between earnings losses upon reemployment and earnings losses measured over the rest of the panel is that earnings losses tend to be long lived, especially in a slack labor market.

Earnings losses upon reemployment are particularly severe for those who experience long spells of non-employment following their initial job loss, as shown in tables 9 and 10. These tables are similar to tables 7 and 8, but show the distribution of percentage earnings change for workers who are non-employed for at least eight full months following their initial job loss. These workers are especially unlikely to have had sufficient assets to maintain their consumption over their spells of non-employment, and one would expect that they would consequently be more likely to accept low-wage jobs than those who had not experienced as large a reduction in consumption expenditures. Overall, these tables strengthen the conclusion in the preceding section that households are not well positioned to insure their consumption spending against job loss. The loss of earnings during spells of unemployment is compounded by the reduction in earnings following reemployment. Both effects are especially severe during the Great Recession due to the increase in long unemployment spells and the elevated risk of further employment instability following initial reemployment.

Percentage Change in Earnings from Previous Employment to Initial Earnings in New Employment for Involuntary Job Changers with Long Non-employment Spells

Percentage Change in Earnings from Previous Employment to Average Earnings Following Reemployment for Involuntary Job Changers with Long Non-employment Spells

Many job changes occur for reasons other than layoff or termination. These job changes might result in increased earnings upon reemployment if the change is to a better job or to a better job match, or it may result in reduced earnings if the new job involves fewer hours of work or if the wage reflects the loss of rents or human capital specific to the previous job. In either case, the job change might put the worker at increased risk of future involuntary job loss due to the worker’s losing the protective effect of tenure on the previous job. These observations are borne out in tables 11 and 12, which are similar to tables 7 and 8 but pertain to job changes for reasons other than layoff or termination. The median worker experiences little change in earnings when changing jobs, but there is a large spread; some workers experience large percentage increases in earnings and others large decreases. For the 2008 panel, when monthly earnings are averaged over the remainder of the panel following employment in the first new job, the distribution of earnings changes shifts to the left (more negative) compared to when earnings are measured in the wave following employment in the first new job. This leftward shift does not occur in the earlier panels, suggesting that subsequent employment instability was a more important phenomenon for those switching jobs during the Great Recession than for those switching jobs in the pre-recession era.

Percentage Change in Earnings from Previous Employment to Initial Earnings in New Employment for Other Job Changers

Percentage Change in Earnings from Previous Employment to Average Earnings Following Reemployment for Other Job Changers

Finally, for comparison, table 13 shows the change in real monthly earnings over the first two years (through the beginning of the seventh four-month panel wave) of each panel for individuals who stayed in the jobs they held at the start of the panel. Real earnings changes tended to be quite small for the job stayers. By definition, the job stayers did not experience earnings disruptions associated with spells of non-employment. Table 13 shows that they also generally did not experience large reductions in real earnings while employed. It is surprising that even the 25th percentile of earnings change is only –8 percent (real) in the 2008 panel, which is slightly smaller in magnitude than the approximately 10 percent drop in the 1996 and 2001 panels, although larger than the 4 percent drop in the 2004 panel. This may reflect distressed firms being more likely to terminate workers rather than cut their inflation-adjusted compensation during the time span of the 2004 and 2008 panels. One reason for this may be the very low inflation rates of the later period, and the documented reluctance of firms to cut nominal wages. Table 13 also shows that earnings increases at the 50th and 75th percentiles are somewhat muted during the Great Recession era compared to the pre-recession period.

Percentage Earnings Changes for Job Stayers

CONCLUSION

For the last decade, most households have not had nearly enough financial wealth to smooth their consumption over more than a very short spell of unemployment. This situation compares unfavorably to the situation in the late 1980s and early 1990s. The reason for this is not clear, and will be an important topic for future research. Receipt of unemployment insurance benefits reduces the magnitude of this problem modestly, but still leaves most households vulnerable to experiencing a sharp drop in consumption expenditures during spells of unemployment.

This phenomenon has potentially serious consequences for both aggregate economic activity and for household well-being. One of the distinguishing features of economic recessions is a sharp increase in involuntary job loss. Our findings suggest that a period of concentrated job loss would likely result in a drop in aggregate consumption, especially if the rate at which the unemployed find new jobs is relatively low and unemployment durations accordingly increase. Most households do not appear to be in a position to cover a prolonged loss in labor earnings through a combination of drawing down of financial assets and take-up of unemployment insurance benefits or other social welfare transfers. Absent a flow of money from another source, such as increased earnings of other household members, transfers from friends or family members, or increased borrowing, households would have little choice but to decrease their consumption expenditures. In a large economic contraction, such as the Great Recession, this has the potential to cause a substantial reduction in aggregate consumption expenditures.

The decrease in the ability of households to compensate for earnings lost due to unemployment through a combination of drawing down of financial assets and increased receipt of transfer payments since the late 1980s and early 1990s suggests that the consequences of an increase in layoffs and terminations for aggregate consumption has likely become more severe over the same period of time. The diminished ability of households to smooth consumption implies an increase in the amplification of economic shocks, and may make the economy more vulnerable to recessions. This suggests that reforms to the unemployment insurance system may be desirable to counter this effect. The unemployment insurance system is designed both to correct for market failures that leave households vulnerable to economic shocks and to provide an automatic stabilizer to macroeconomic activity. Unfortunately, our findings indicate that there has likely been a decrease over time in the effectiveness of the system in satisfying both of these objectives. Programs to increase the rate at which individuals collect benefits to which they are entitled may be desirable in this regard.

Compounding the problem of insufficient financial wealth to insure against earnings losses while unemployed, individuals are at high risk of earning much less than they did in their previous job upon reemployment following job loss. Even if households had financial assets adequate to cover the earnings lost while unemployed, they would likely still want to decrease their consumption expenditures to reflect their diminished earnings. The clustering of involuntary job separations during recessions amplifies the macroeconomic impact of this effect on aggregate consumption. Regardless of timing, the earnings loss upon reemployment reduces the welfare of affected households. Commercial insurance against this loss is not available because of moral hazard and adverse selection, and in practice households are not financially able to “self-insure” against long-term earnings reductions. Proposals for a new wage insurance program targeted to displaced workers who have suffered earnings reductions, such as that described by Robert J. LaLonde (2007), have the potential to at least partly correct this market failure. Although the primary motivation for wage insurance is to protect the economic welfare of displaced workers, it would also act as an automatic stabilizer of aggregate consumption and facilitate job matching after periods of concentrated layoffs and terminations.

Acknowledgments

We wish to thank Sam Richardson for expert research assistance. We are also grateful to participants at the Russell Sage Foundation conference, “The U.S. Labor Market During and After the Great Recession,” in particular Arne Kalleberg and Till von Wachter, participants at the Southern Economic Association annual conference, and two anonymous referees for very helpful comments and discussions. The views expressed in this paper are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Boston or the Federal Reserve System. All errors are our own.

FOOTNOTES

↵1. In each case, we measure monthly earnings by the mean reported within a wave.

- © 2017 Russell Sage Foundation. Dickens, Williams T., Robert K. Triest, and Rachel B. Sederberg. 2017. “The Changing Consequences of Unemployment for Household Finances.” RSF: The Russell Sage Foundation Journal of the Social Sciences 3(3): 202–21. DOI: 10.7758/RSF.2017.3.3.09. We wish to thank Sam Richardson for expert research assistance. We are also grateful to participants at the Russell Sage Foundation conference, “The U.S. Labor Market During and After the Great Recession,” in particular Arne Kalleberg and Till von Wachter, participants at the Southern Economic Association annual conference, and two anonymous referees for very helpful comments and discussions. The views expressed in this paper are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Boston or the Federal Reserve System. All errors are our own. Direct correspondence to: William T. Dickens at w.dickens{at}neu.edu, Department of Economics, Northeastern University, 360 Huntington Ave., Boston, MA 02115; Robert K. Triest at robert.triest{at}bos.frb.org, Research Department, Federal Reserve Bank of Boston, 600 Atlantic Ave., Boston, MA 02210; and Rachel B. Sederberg at sederberg.r{at}husky.neu.edu, Department of Economics, Northeastern University, 360 Huntington Ave., Boston, MA 02115.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.