Abstract

Despite the strong relationship between the rise in mass incarceration over the last forty years and racial inequality in employment and wages, few studies have examined the long-term consequences and spillover effects of criminal justice contact on the black-white wealth gap in the United States. In this paper, we investigate the mechanisms whereby the local and distal incarceration of a family member affects household wealth, focusing on wealth disparities by race and education. Using data from the Survey of Income and Program Participation (SIPP), the Current Population Survey, and the Survey of Inmates in State and Federal Correctional Facilities and Local Jails, we apply fixed-effects and probit models to estimate how a family member’s incarceration influences household assets and debt over panel waves. We find that having an incarcerated family member reduced household assets by 64.3 percent and debt by 85.1 percent after we adjusted for the underrepresentation of institutionalization in SIPP data. We also discuss these findings in the context of broader racial disparities in wealth and employment. Our findings demonstrate how contemporary patterns of mass incarceration contribute to the maintenance of social inequality in wealth and form barriers to economic security for other household members.

It is well established that the detrimental effects of incarceration extend into many areas of social life (Wakefield and Uggen 2010). Incarceration limits future employment prospects and earnings (Western and Pettit 2005; Western 2006; Pettit 2012), blocks political participation (Manza and Uggen 2006), and can lead to physical and mental health issues for former offenders (Schnittker, Massoglia, and Uggen 2011). These far-reaching effects have led some to characterize incarceration as a criminal credential or absorbing status that results in continuing disadvantage for former prisoners (Pager 2003, 2007).

The consequences of incarceration spread beyond the formerly incarcerated as well. Incarceration increases material hardship and familial stress, exacerbates marital instability by straining family ties, and is associated with a variety of adverse outcomes for children (Wildeman and Muller 2012). In this study we investigate the relationship between incarceration and the wealth profiles of ex-offenders and other family members, who include parents, romantic partners, and dependents.

Although researchers have shown that incarceration influences a variety of economic outcomes for former offenders and those around them, research on the relationship between incarceration and wealth accumulation is relatively new. The few studies on this topic indicate that incarceration is associated with decreased rates of homeownership and net worth for former offenders (Maroto 2015; Zaw, Hamilton, and Darity 2016); it is a particularly salient factor in explaining black-white disparities in homeownership (Schneider and Turney 2015). Additional research points to increasing debt for former offenders through the courts’ use of heavy pre- and post-conviction fines and fees that many individuals simply cannot afford to pay (Harris, Evans, and Beckett 2010, 2011).

Despite the growing research on mass incarceration and the importance of wealth for economic well-being, little is known about the long-term consequences of imprisonment for the wealth accumulation of former inmates and their families. We focus on how the negative effects of incarceration can infect households through economic disadvantage in the form of declining wealth. In doing so, we combine data from the 1996 to 2008 panels of the Survey of Income and Program Participation (SIPP), the Current Population Survey (CPS), the Survey of Inmates in State and Federal Correctional Facilities (SISFCF), and the Survey of Inmates in Local Jails (SILJ) to address the following research questions: How does the incarceration of one individual influence overall household wealth accumulation, as measured by total assets and debt? What happens to the racial wealth gap once we account for incarceration? And, on a more methodological level, does institutionalization in national household surveys provide a good proxy for incarceration?

In addition to demonstrating how the consequences of incarceration extend to families and household members, we also show how incarceration influences the racial wealth gap in the United States. With racial wealth disparities that greatly exceed income gaps, African Americans and Hispanics face continuing disadvantage in housing and credit markets (Conley 1999; Oliver and Shapiro 2006). Wealth inequality has also widened along racial lines since the recent economic downturn and its uneven recovery (Pfeffer, Danziger, and Schoeni, 2013; Wolff 2014), which further necessitates studies of the potential mechanisms behind racial inequality in wealth accumulation. Thus, this study offers a larger theoretical contribution in its investigation of incarceration’s place within a broader system of racial inequality by demonstrating incarceration’s contagious nature.

THEORETICAL FRAMEWORK AND BACKGROUND

We combine multiple conceptions of incarceration and its consequences within our theoretical framework. This framework highlights two key components related to incarceration’s negative effects. First, incarceration’s consequences are lasting and diffuse across the life course to implicate employment opportunities, educational attainment, and old-age dependency. Serving time in prison or jail acts as an absorbing status that feeds into a process of cumulative disadvantage. Second, incarceration influences more than just the formerly incarcerated individual; it harms families, children, friends, and even entire neighborhoods. Together, these components demonstrate incarceration’s contagious nature, which routinely disadvantages entire households in the United States within a broader system of inequality, hallmarked by discrimination (Lum et al. 2014; Reskin 2012).

The Consequences of Incarceration

By the end of 2013, almost 6.9 million adults were under correctional supervision, 2.23 million of whom were in prison or jail (Glaze and Kaeble 2014). Current estimates indicate that approximately 65 million Americans (27.8 percent) have a criminal record (Rodriguez and Emsellem 2011). The risk of incarceration is not uniform, given that young black men with little education are most likely to spend time behind bars (Pettit and Western 2004; Pettit, Sykes, and Western 2009; Pettit 2012; Western and Wildeman 2009). Among cohorts born in the late 1970s, 68 percent of African American men with less than a high school education served time in state or federal prison by the height of the prison boom in 2010 (Western and Travis 2014; Pettit, Sykes, and Western 2009). Although rates of incarceration are much lower for other racialized groups, 20 percent of less-educated Hispanic men and 28 percent of less-educated white men in this cohort had a record in the same period. These disproportionate rates of incarceration stem from the criminal justice system’s varying enforcement efforts, as well as the implementation of mandatory minimum sentencing, three strikes, and other laws in the 1980s and 1990s (Western and Travis 2014; Wacquant 2001).

The racial and educational disproportionality in incarceration is compounded by its numerous and well-documented social and economic consequences. In the labor market, incarceration acts a stigmatized status that creates barriers to employment and affects later earnings for former offenders, which furthers economic disadvantage (Pager 2003; Pager and Quillian 2005; Western and Pettit 2005; Western 2006; Pettit 2012). Although incarceration can shelter inmates from violence and provide them some access to health care (Patterson 2010), inmates have higher rates of certain diseases and psychological problems than the rest of the population (Schnittker, Massoglia, and Uggan 2011; Sykes, Hoppe, and Maziarka 2016; Wildeman and Muller 2012). Incarceration is also associated with increased morbidity, stress, and the risk of infectious disease, creating additional long-term health problems for former prisoners (Johnson and Raphael 2009; Massoglia 2008a, 2008b; Schnittker and John 2007; Sykes and Piquero 2009).

The Contagious Nature of Imprisonment

The consequences of incarceration are not limited to the formerly incarcerated individual. They are contagious and extend beyond the individual offender to disadvantage families, contacts, and communities (Lum et al. 2014; Wildeman and Muller 2012). As a result, families share in the social, economic, and health consequences of the former inmate. Parental incarceration is associated with increased material hardship and downward mobility for families (Geller, Garfinkel, and Western 2011; Schwartz-Soicher, Geller, and Garfinkel 2011; Sykes and Pettit 2015), along with child homelessness (Wildeman 2014) and a larger reliance on government programs (Sugie 2012; Sykes and Pettit 2015). For couples, incarceration is associated with an increased probability of single parenthood, separation, and divorce for current inmates (Apel et al. 2010; Lopoo and Western 2005), as well as repartnering (Turney and Wildeman 2013) and having children with multiple partners after incarceration (Sykes and Pettit 2014). Given that about half of all inmates are parents and approximately 2.6 million children under the age of eighteen have a parent in prison or jail, the collateral consequences of incarceration extend to children as well (Sykes and Pettit 2014; Western and Wildeman 2009).

Thus, previous research on the effects of incarceration for families, households, and communities shows how the consequences of incarceration are as contagious as incarceration itself. Many researchers have come to refer to these consequences as “collateral damage” (Foster and Hagan 2015; Hagan and Foster 2012) because the incarceration of one family member affects the economic well-being of other members through the loss of employment and income. However, wealth and asset ownership present another often-overlooked component of economic well-being. Wealth, in all of its many forms, creates more stability than income, particularly in times of economic distress (Keister and Moller 2000; Spilerman 2000). Wealth is associated with better outcomes for children (Keister 2000a), particularly when financial transfers fund and enable postsecondary educational attainment (Rauscher, this issue), and it is related to increased stability in romantic relationships (Eads and Tach, this issue). The benefits associated with assets, investments, and homeownership, the largest wealth component for most households, compound over time (Killewald and Bryan, this issue). Thus, the importance of wealth accumulation for many social, economic, and romantic outcomes requires an investigation into the relationship between incarceration and household assets and debt.

Incarceration and Household Wealth

Spending time in prison or jail creates a stigmatized legal status that limits access to and advancement within multiple areas of society, including credit markets. Recent studies on legal financial obligations (LFOs) show that former offenders face added debt burdens from heavy pre- and post-conviction fines and fees within the criminal justice system (Harris, Evans, and Beckett 2010, 2011). Payments can be particularly high because courts rarely consider offenders’ abilities to pay in assessing these fines and fees (Beckett and Harris 2011). The failure to pay fees on time can lead to accruing debts and even additional jail time for the former offender (Bannon, Nagrecha, and Diller 2010). In addition, county clerks can garnish the wages of a spouse and seize joint assets in cases of nonrepayment (Harris, Evans, and Beckett 2010).

Researchers have also found connections between wealth and incarceration. Using NLSY79 data and fixed-effects models to help account for selection, Michelle Maroto shows that the likelihood of homeownership declined by an additional 28 percentage points after incarceration, and an ex-offender’s net worth decreased by an average of $42,000 after incarceration. These declines compounded already low levels of wealth and coincided with additional labor market consequences that also limited ex-offenders’ abilities to earn income (Maroto 2015). Using state-level data from 1985 to 2005, Daniel Schneider and Kristin Turney (2015) also find that higher state-level incarceration rates are associated with decreased black homeownership rates, which leads to larger black-white wealth disparities. Khaing Zaw, Darrick Hamilton, and William Darity (2016) show that wealth is associated with lower rates of incarceration, but, when compared with whites, the likelihood of future incarceration was higher for blacks at every level of wealth. In light of incarceration’s effects on the wealth of former offenders, our framework is based in a contagion model of incarceration that leads to the expectation that the consequences of incarceration will spread to households, limiting both assets and debt.

Long before changes to American criminal justice policies resulted in the massive expansion of prisons and jails, sociological theory predicted the very relationship between penal practices, employment, and wealth. Michel Foucault (2015) shows that the origins of a punitive society rest on social beliefs about the nature of work, leisure, and power. These three elements converge to shape capital and household wealth, individual delinquency, and extra-juridical rules that maintain dominance over the poor and working class through penal codes. The “illegalisms” of idleness and employment irregularity during the early nineteenth century produced structural responses by government agents that resulted in “a de facto arrangement with the police that meant that a worker without a work record book was not arrested if he possessed a saving bank book,” thereby allowing the worker to escape further policing and institutionalization (Foucault 2015, 193). Thus the relationship between incarceration and household wealth has its antecedents in the modes of production and the structure of employment.

Just as multiple mechanisms help explain incarceration’s negative consequences on employment, multiple direct and indirect pathways tie incarceration and household wealth outcomes together. Incarceration limits a person’s ability to make payments, which can increase debt delinquency and negatively affect credit scores. Incarceration can then directly impede access to credit markets by making it more difficult for former offenders to access banks and lending, which leads to decreases in both assets and debt. Like employers, lenders may interpret a previous incarceration as a signal of untrustworthiness or instability, thereby limiting a previously incarcerated person’s access to investment and lending opportunities (Holzer, Raphael, and Stoll 2003; Pager and Quillian 2005). In addition, former offenders often also try to avoid mainstream financial institutions for fear of the extra surveillance (Brayne 2014; Goffman 2009).

A previous incarceration can also affect wealth through other indirect mechanisms. By limiting education, employment, and earnings, which are highly connected to wealth building (Bricker et al. 2014; Semyonov and Lewin-Epstein 2013), incarceration limits wealth for ex-offenders, along with their family members. Partners of incarcerated persons must also find ways to make up for a missing member of the household, which influences income flows and childcare options. These strains, along with changes in economic well-being and the physical and mental health of former offenders, can all lead to asset losses, less access to lending, and lower overall debt.

Connections to Racial Inequality

Given the overrepresentation of young black and Hispanic men in the criminal justice system, incarceration’s effects on wealth also factor into broader wealth disparities. Although imprisonment rates in the United States have declined slightly in recent years, racial wealth gaps, strengthened by differential returns to resources that largely benefit white households, have been increasing since the Great Recession (Kochhar, Fry, and Taylor 2011; Pfeffer, Danziger, and Schoeni, 2013; Wolff 2014). According to Survey of Consumer Finances data, the median net worth in 2013 for white non-Hispanic households was approximately 7.8 times greater than that of nonwhite or Hispanic households (Bricker et al. 2014). Even after accounting for variation in education and income, large racial wealth gaps remain in the United States (Oliver and Shapiro 2006). Black households are less likely to own their homes, have less net worth, and accumulate fewer assets over time than whites (Gittleman and Wolff 2004; Killewald 2013; Kuebler and Rugh 2013). Additional research has also shown significant disparities in wealth accumulation, home ownership rates, and home equity between white and Hispanic households (Campbell and Kaufman 2006; Flippen 2001, 2004; Krivo and Kaufman 2004). Yet, homeownership itself is a key marker of racial inequality: Killewald and Bryan (this issue) show that the wealth generating returns to homeownership are greatest for whites (at about $11,000 for each year of ownership) compared with Hispanics and blacks (about $9,000 and $5,000, respectively).

Multiple individual and structural mechanisms contribute to racial wealth disparities and general wealth inequality. On an individual level, these disparities stem from demographic differences contained in life cycle and microeconomic models (Addo and Lichter 2013; Keister 2004). In addition to family structure differences, lower levels of education, inadequate income, poor job prospects, and family poverty impede minorities’ transitions into homeownership and limit wealth accumulation (Bricker et al. 2014; Hall and Crowder 2011; Heflin and Pattillo 2006; Semyonov and Lewin-Epstein 2013). However, income and wealth are not perfectly correlated because other factors, particularly credit market access and behavior, also matter for wealth outcomes (Keister 2000a; McCloud and Dwyer 2011). Finally, differences in the incidence and amount of intergenerational transfers further work to maintain racial wealth gaps (Keister 2000b, 2003; Oliver and Shapiro 2006).

These mechanisms have all been supported by historical and contemporary discrimination in multiple markets, combined with residential segregation (Massey 2015; Massey and Denton 1993; Shapiro 2004). Although the process of redlining originally resulted in the greatest disadvantages to segregated minority communities through the denial of services, reverse redlining, where lenders target these communities for the sale of subprime loans, now leads to larger wealth disparities (Fisher 2009; Squires 2003; Williams, Nesiba, and McConnell 2005). This serial displacement of capital, as Jacob Rugh, Len Albright, and Douglas Massey (2015) describe it, very much played into the widening of racial wealth inequality since the recent economic downturn (Pfeffer, Danziger, and Schoeni 2013; Wolff 2014).

In the discussion of these broader mechanisms of racial wealth inequality, many researchers overlook a key explanation—the differential rates and experiences of incarceration that black and white households face. Although continuing racial wealth gaps likely remain due to direct discrimination, it is possible that the different rates of incarceration across groups (that is, racial minorities’ higher rates of incarceration) will also partially explain these lingering wealth disparities. When they are searching for housing and attempting to access lending markets, black and Hispanic former offenders likely face the double jeopardy of racial discrimination and prejudice against those with criminal records. Incarceration, therefore, provides us with an additional structural-level explanation for racial wealth inequality at the household level.

ESTIMATING THE EFFECTS OF INCARCERATION

Researchers often face certain challenges in studying the consequences of incarceration because our forms of recordkeeping, which generate knowledge, often undercount disadvantaged members of society. Although Michel Foucault states that “it is a society that links to this permanent activity of punishment a closely related activity of knowledge” through “a recording” of the individual (2015, 196), recent research suggests that such recordings are at best incomplete. Since the Great Recession, scholars have drawn increasing attention to the underestimation of program participation and markers of social disadvantage in household surveys. Even though the forms, specifics, and solutions vary across studies, the arguments and conclusions are broadly consistent: national household data, when compared with official statistics, underreport or exclude members of the population, thereby obscuring important metrics of social inequality. For instance, Bruce Meyer and his colleagues (2009) compare weighted household program estimates to administrative data to show how five major nationally representative household surveys underreport transfers in food stamps, Temporary Assistance for Needy Families, and worker’s compensation. They suggest a series of adjustment methods to address take-up rates—the fraction of eligible individuals or families that receive a given transfer.

Similarly, Becky Pettit (2012) finds that by excluding institutionalized populations, mainly those who are in prisons and jails, national surveys distort our understanding of racial inequality in employment, wages, educational completion, and political participation. As a solution to this problem, she includes inmates in the numerator or denominator of specific measures and then reestimates racial inequality in those social indicators to understand how sampling bias has grown in tandem with the rise in mass incarceration. Other scholars raise similar concerns and use alternative solutions (see Heckman and LaFontaine 2010; Neal and Rick 2014).

We propose a different, hybridized solution to these issues. We address the incorporation of the institutionalized population by constructing new weights for national surveys. Using data from a standard national survey that measures wealth and debt in the United States, we show how our incarceration-adjusted national weights for this survey track the overall penal representation when benchmarked to published statistics. Further, we estimate weighted models (unadjusted and adjusted for incarceration) to explore how institutionalization affects inequality in household assets and debt.

DATA

We use data from four sources to estimate the relationship between institutionalization and household wealth and debt. Our primary source is the Survey of Income and Program Participation. SIPP is a longitudinal, household-based survey that captures the non-institutionalized population through a continuous series of nationally representative panels. We rely on the 1996, 2001, 2004, and 2008 panels. Each includes a sample that captures information on the socio-demographic characteristics of household members, including measures of employment, wealth, program participation, and life-course transitions over multiple years. SIPP oversamples residences from high poverty areas to boost survey representation in places where household under-reporting is more prevalent. Every panel comprises an independent sample that interviewers followed for two to four years. The core data were retrospectively collected every four months during waves until the 2008 panel, when cost concerns led to a redesign that now contains annual recalls with an event history calendar.

Each SIPP wave contains four randomly selected rotation groups staggered across waves within panels. To minimize seam bias between reference months, we draw on data from the fourth reporting month in each panel wave when survey responses are most accurate (for more detail on seam issues in SIPP, see Ham, Li, and Shore-Sheppard 2016). Data on assets and liabilities are drawn from topical modules and matched to core data using a unique person identifier that indexes the panel, sampling unit (or household), and person number. Table A1 displays the household interview dates for the asset and liabilities topical modules across panel waves.

We then leverage periodic survey data from the SISFCF and the SILJ to measure institutionalization in the United States. These data are collected by the U.S. Census Bureau and distributed by the Bureau of Justice Statistics (BJS). Data for the SILJ were collected in 1972, 1978, 1983, 1989, 1996, and 2002, and for the SISFCF in 1974, 1979, 1986, and 1991. Inmates in federal facilities were surveyed in 1991, and state and federal data on inmates were jointly collected in 1997 and 2004. These surveys contain socio-demographic information that can be used to construct annual race, sex, age, and education specific incarceration rates.

We also draw on published correctional population totals from BJS. These data provide annual counts on the number of adult inmates in state, federal, and local (or jail) custody. Correctional totals are benchmarked using data from the National Prisoner Statistics Program, Annual Survey of Jails, Census of Jail Inmates, and the Annual Probation and Parole Surveys.

Additionally, we use data from the March Current Population Survey since 1972 to obtain population totals that will be used in the denominator of the incarceration rate. CPS data are collected by the Census Bureau and the Bureau of Labor Statistics (BLS) in March of each year, and the CPS samples approximately fifty thousand to sixty thousand non-institutionalized respondents attached to households. These data are used to generate the race, sex, age, and educational distribution of the civilian population.

Finally, we use BLS data to adjust wealth and debt dollars throughout the period. We standardize the buying power across panels and interview years using the consumer price index (CPI) inflation calculator. All income, wealth, and debt statistics are expressed in 2015 dollars.

CONCEPTUAL MEASURES

Table 1 displays the operationalization and coding of measures in our study. Our main variable, institutionalized, shows that 0.2 percent of all respondents in the 1996 SIPP panel report the institutionalization of a household member between December 1996 and March 2000. This percentage dips to 0.1 percent in the 2001 panel and returns to 0.2 percent during the 2004 and 2008 panels. Between the 1996 and 2004 panels, average monthly household income rose from $6,815 to $7,171. However, during the 2008 panel, average monthly household income declined to roughly $6,750 due to the onset of the Great Recession.

Variable Operationalization and Descriptive Statistics by Panel Year

Our two key outcome measures—total assets and total debt—present complementary measures of wealth. Like total household income, the Great Recession also eliminated a significant amount of household wealth. Total average household assets during the 1996 panel amounted to almost $189,000, rising to over $272,000 by the 2004 panel. The economic slowdown that began in December 2007 and ended in June 2009 had devastating consequences for household wealth. The 2008 panel shows that mean household assets had declined to almost $246,000. Average household debt, however, shows a steady increase across the four panels, going from almost $85,000 in 1996 to almost $116,000 by the close of 2011.

In our models, we also account for additional explanations of wealth inequality by using person- and household-level control variables related to demographic, family, education, and employment dynamics. We control for the respondent’s reported age, gender, marital status, number of children, and education. We measure age in years and include a quadratic age-squared term to account for any nonlinear relationships with wealth. We measure gender with an indicator variable of male or female and marital status with a variable indicating whether the respondent was never married. We incorporate a variable for the respondent’s race and ethnicity that includes four categories: non-Hispanic white (the referent), non-Hispanic black, Hispanic, and non-Hispanic other. Education is a categorical variable with three categories: less than high school, high school diploma, and some college or higher. We also control for labor market variables of employment status and monthly household income, along with measures of average household poverty and an indicator for whether the person lives in a metro area.

These other demographic and educational measures display considerable consistency across panels, although the percentage of non-Hispanic whites declines and that of Hispanic and non-Hispanic others increases. Additionally, over time, the sample has become more educationally advantaged, as the percentage of respondents with at least some college education increased from 53 percent during the 1996 panel to 62 percent during the 2008 panel.

METHODS

We merge population totals from the SISFCF, the SILJ, and the CPS by race, sex, age, and education to construct annual group-specific incarceration rates. Weighted group proportions from inmate surveys are linearly interpolated by facility type between survey years and applied to correctional population totals by facility type to construct national, group-specific incarceration counts. These aggregate inmate totals represent the numerator of the incarceration rate, while the denominator is obtained from non-institutionalized totals associated with the race-sex-age-education distribution of the civilian population. Further information on this method is provided in multiple published studies on mass incarceration (see Pettit, Sykes, and Western 2009; Pettit 2012; Sykes and Pettit 2014; Western and Beckett 1999; Western and Pettit 2005; Western 2006).

The 1996 SIPP panel contains entry and exit dates for each household member and the reason for departure or reentry. Consequently, subsequent panels do not include the month and day of entry or exit from the household. Therefore, we only leverage information on the reason for entering and departing the household. Respondents who report “institutionalization” as the explanation for household entry and exit are used to compare the race-sex-age-education distributions of adults currently institutionalized in American prisons and jails. We estimate race-sex-age-education group means for SIPP respondents who report institutionalization and match the incarceration rates to this socio-demographic distribution in SIPP. We calculate an institutionalization rate adjustment (IRADJ) factor that is the ratio of the incarceration rate derived from CPS and inmate data (IRCPS) relative to the institutionalized rate in SIPP (IRSIPP), as displayed in equation 1.1

Because SIPP contains multiple weights (for example, individual, household, and family weights), we elect to use the individual weights for our analysis because we are interested in the relationship between having a family member institutionalization and household wealth and debt. We then estimate a new, adjusted SIPP institutionalized weight (SIW) that accounts for national incarceration rates (in equation 2) by multiplying the adjusted institutionalization rate factor (IRADJ) with individual SIPP weights (SW) if the respondent reported being institutionalized during a specific month during that calendar year.

The unadjusted and adjusted SIPP weights are then benchmarked to published institutionalization rates (Pettit and Western 2004). We also apply these unadjusted and adjusted weights to our statistical models to understand how estimates of inequality change over time with growth in incarceration.

Because SIPP is a longitudinal dataset with multiple panels and waves, we use the fixed-effects estimator to measure the association between the institutionalization of a family member and household assets and debt. Jack Johnston and John DiNardo (1997, 399) show that fixed-effects estimation solves problems of omitted variable bias by “throwing away” parts of the variance that contaminate ordinary least squares or random-effects estimators. The Wu-Hausman test confirms that the error is correlated with our explanatory variables, indicating that the fixed-effects estimator is consistent, efficient, and preferred over the random-effects estimator.

We also estimate a series of probit models that quantify whether institutionalization affects having any household assets or debt between panel waves. We then report marginal effects—the rate of change in the dependent variable (that is, the predicted probability) relative to a unit change in an independent variable (Long 1997; Powers and Xie 2000)—with all models evaluated at their mean values.

FINDINGS

According to our results, the institutionalization of one family member is associated with declines in assets and debt and the household level. In addition to showing how institutionalization relates to wealth outcomes, these findings also demonstrate its contagious nature. The incarceration of one family member can have lasting consequences for the entire household.

Patterns of Institutionalization

Table 2 presents civilian institutionalization rates by race and education among U.S. men ages twenty to thirty-four in 1999. We compare published estimates of race and educational inequality in incarceration to institutionalization rates contained in SIPP using unadjusted SIPP weights and our incarceration-adjusted SIPP weights. The first horizontal panel presents published estimates from Becky Pettit and Bruce Western’s (2004) work on mass imprisonment and the life course; the middle panel displays estimates using normal SIPP weights; and the final panel displays our SIPP-incarceration weighted statistics.

Civilian Institutionalization Rates, 1999

First, the pattern of institutionalization in the unadjusted SIPP weighted data follows a racial and educational distribution similar to that of Pettit and Western (2004). However, racial and educational inequality is largely underestimated using unadjusted SIPP weights to measure institutionalization. For instance, whereas Pettit and Western find that 21 percent of young, black men with less than a high school diploma were institutionalized in 1999, unadjusted SIPP weights underestimate this group by almost sevenfold. The magnitude of this problem intensifies across levels of educational attainment. Sykes and Pettit (2014) observe similar racial and educational gradients when comparing parental incarceration estimates from the National Survey of Children’s Health with inmate surveys and official statistics. Overall, inequality in institutionalization is 2.7 times higher among blacks than among whites using unadjusted SIPP weights, versus the 8.5 factor difference in Pettit and Western (2004).

By contrast, estimates from SIPP-incarceration weighted data are much closer in the aggregate but highly variable by educational level. Among those with less than a high school diploma, our measure overshoots the estimates that Pettit and Western report (2004). One possibility for this discordance is that the age distribution of institutionalized respondents in SIPP does not perfectly align with the range of twenty to thirty-four reported in Pettit and Western, resulting in weighted averages that give greater weight to individuals closer to age thirty-four. Another possibility is that the educational distribution in SIPP overrepresents undereducated respondents during the 1996 panel, which may explain why estimates for respondents with a high school diploma and some college converge with statistics reported in Pettit and Western (2004). Nevertheless, our total estimates for institutionalization are much closer than the unadjusted SIPP weights.

Patterns in Assets, Debt, and Institutionalization

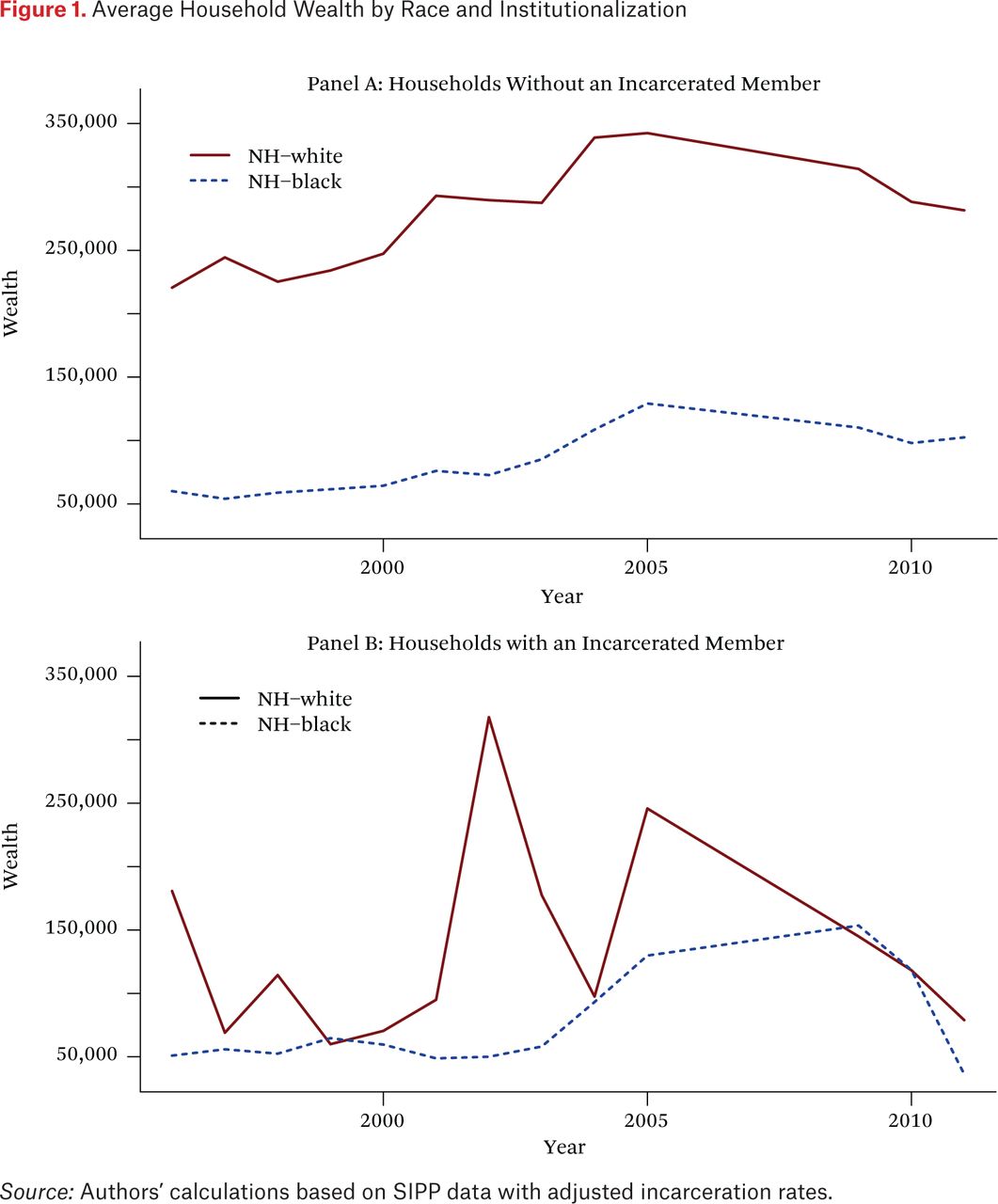

Figure 1 plots average household assets by race and institutionalization in the United States from 1996 to 2011. The top panel is for households without an incarcerated member; the bottom panel is for households with an incarcerated member.2 The top panel shows significant racial gaps in wealth among households without an incarcerated family member. In 1996, white households held nearly $221,000 in wealth at the mean versus $60,000 among blacks, resulting in a black-white gap of $160,000 in 1996. This gap in wealth reached its zenith at roughly $230,000 in 2004 and declined to $179,000 by the close of 2011.

Average Household Wealth by Race and Institutionalization

By contrast, households with an institutionalized family member are much closer and more volatile in their wealth patterns. In 1996, white households with an institutionalized member held approximately $183,000 in assets, versus the paltry $51,000 among similarly situated black households, resulting in a black-white wealth gap of almost $132,000, similar to that between households without an institutionalized family member. White assets fall below those of blacks in 1999, but the gap surges to almost $270,000 in 2002, stabilizes in 2009, and then settles at approximately $45,000 by 2011. The volatility between 2002 and 2009 could be the result of indictments and convictions following high-profile corporate crimes and malfeasance during this period, particularly for non-Hispanic whites.3

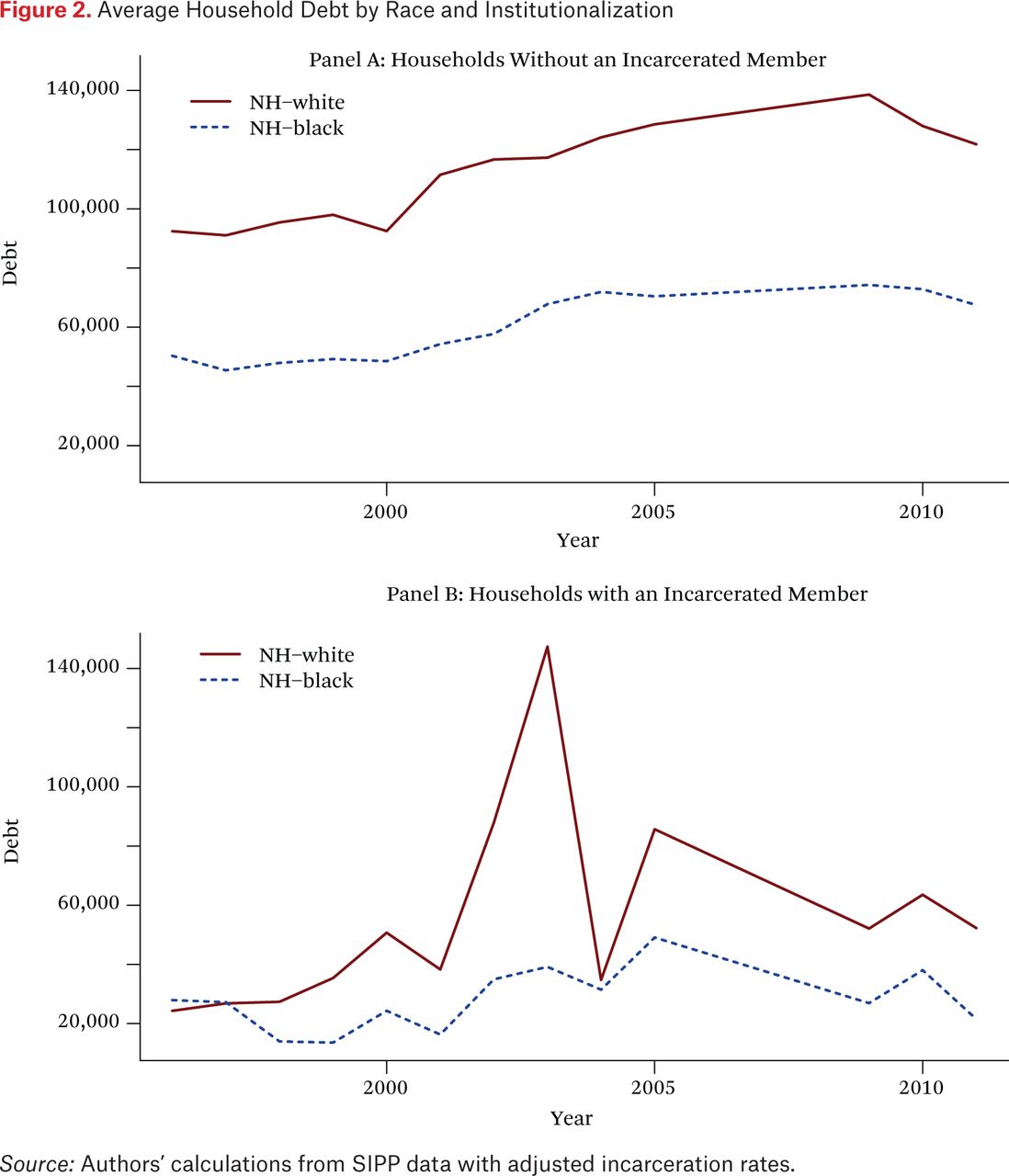

Figure 2 displays average household debt by race and institutionalization. Non-Hispanic whites without a family member institutionalized have greater debt than similar black households, as displayed in the top panel. In 1996, white families had around $92,400 of debt to the $50,300 of debt in black households, a debt gap of $42,100. The black-white debt gap climbs to almost $59,000 in 2002 and soars to nearly $64,300 in 2009.

Average Household Debt by Race and Institutionalization

Among households with an institutionalized family member (lower panel), black and white debt levels begin the series fairly even. However, by 1998, black household debt declined to about $14,000 as white debt levels rose. The slow increase in debt among black families with a household respondent institutionalized means that the debt gap remained fairly stable after 2005 and much smaller than the gaps for households without institutionalized family members.

Estimating Household Assets and Debt

Table 3 presents fixed-effects estimates of household wealth and debt by SIPP weighted and SIPP-incarceration weighted adjustments. Columns 1 through 4 present unlogged estimates of wealth and debt; columns 5 through 8 display logged differences. The institutionalization of a family member is not associated with lower assets or debt using either unadjusted or adjusted SIPP weights. However, the SIPP-incarcerated weights display larger differences for both assets and debt. Having any assets and debt in the previous wave is significantly related to having wealth and debt in the current wave. The estimated black-white wealth gap is almost $148,000 (column 2) and the debt gap about $45,200.

Estimated Household Wealth and Debt Levels

We also logged assets and debts to address data skewing and the nonlinear association between incarceration and components of household wealth.4 The unadjusted SIPP weights (column 5) indicate that, holding all other variables constant, having an institutionalized family member is moderately associated with a 57.3 percent reduction in total household assets.5 The SIPP-incarceration adjusted weights reveal a larger disparity; having a family member incarcerated reduces household assets by 64.3 percent using these weights.

Logged debt levels display greater magnitude differences. Even though unadjusted SIPP weights show that institutionalization is linked with lower household debt by 84.1 percent compared with households unexposed to institutionalization, the SIPP-incarceration weight adjustments (column 8) indicate a stronger association, at 86.1 percent. Thus, estimates of institutionalization in logged scales reveal how the SIPP-incarcerated weights correct for large differences in magnitude that result from undercounting and excluding inmates.

Racial gaps in assets and debt also appear in these models. We estimate that black household assets are 80.4 percent lower than white households, and household debt was approximately 74.6 percent lower among black households. In addition, Hispanic households held 64.3 percent less in assets and 66.7 percent less in debt than otherwise similar non-Hispanic white households. Together with the effects of institutionalization, these results indicate that institutionalization and race can both block access to credit markets, limiting wealth accumulation, as well as families’ abilities to borrow.

Table 4 presents marginal effects of current institutionalization on whether a household has any assets or debt. Although the SIPP unadjusted weights do not detect a significant association between institutionalization and the likelihood of having assets, the SIPP-incarcerated weight model shows that incarceration is moderately associated with a 2.7 percentage point reduction in the probability of having assets, holding all other variables at their mean values. When held at their mean values, non-Hispanic blacks, Hispanics, and other non-Hispanic racial groups are 5.4, 3.9, and 1.8 percentage points less likely to have assets than non-Hispanic whites, respectively.

Marginal Effects of Current Institutionalization on Whether a Household Has Any Assets or Debt

Households with an incarcerated family member are about 3.6 percentage points less likely to have debt when using the SIPP unadjusted weights. However, the SIPP-incarceration adjusted weights widen this disparity by 10 percent, resulting in the likelihood of having debt being 3.9 percentage points lower in households with a family member incarcerated. This association is likely driven by reduced access to credit markets among disadvantaged households.

Our first set of models shows that institutionalization is associated with lower assets and debt across households; however, the presence of assets and debt might also influence a household member’s likelihood of institutionalization. Table 5 presents the marginal effects of changes in household wealth and debt on changes in institutionalization between panel waves. Although having previous assets is associated with a reduced probability of institutionalization, the effect is too small to be meaningful. Furthermore, the SIPP-incarceration adjusted weights do not show any association between previous wealth affecting changes in institutionalization.

Marginal Effects of Changes in Household Wealth and Debt on Changes in Institutionalization

Similarly, having previous debt is strongly associated with a lower probability of becoming incarcerated, and the model with adjusted SIPP-incarcerated weights confirms this association. However, like the wealth model, the effect is too small to be meaningful.

Employment and Institutionalization

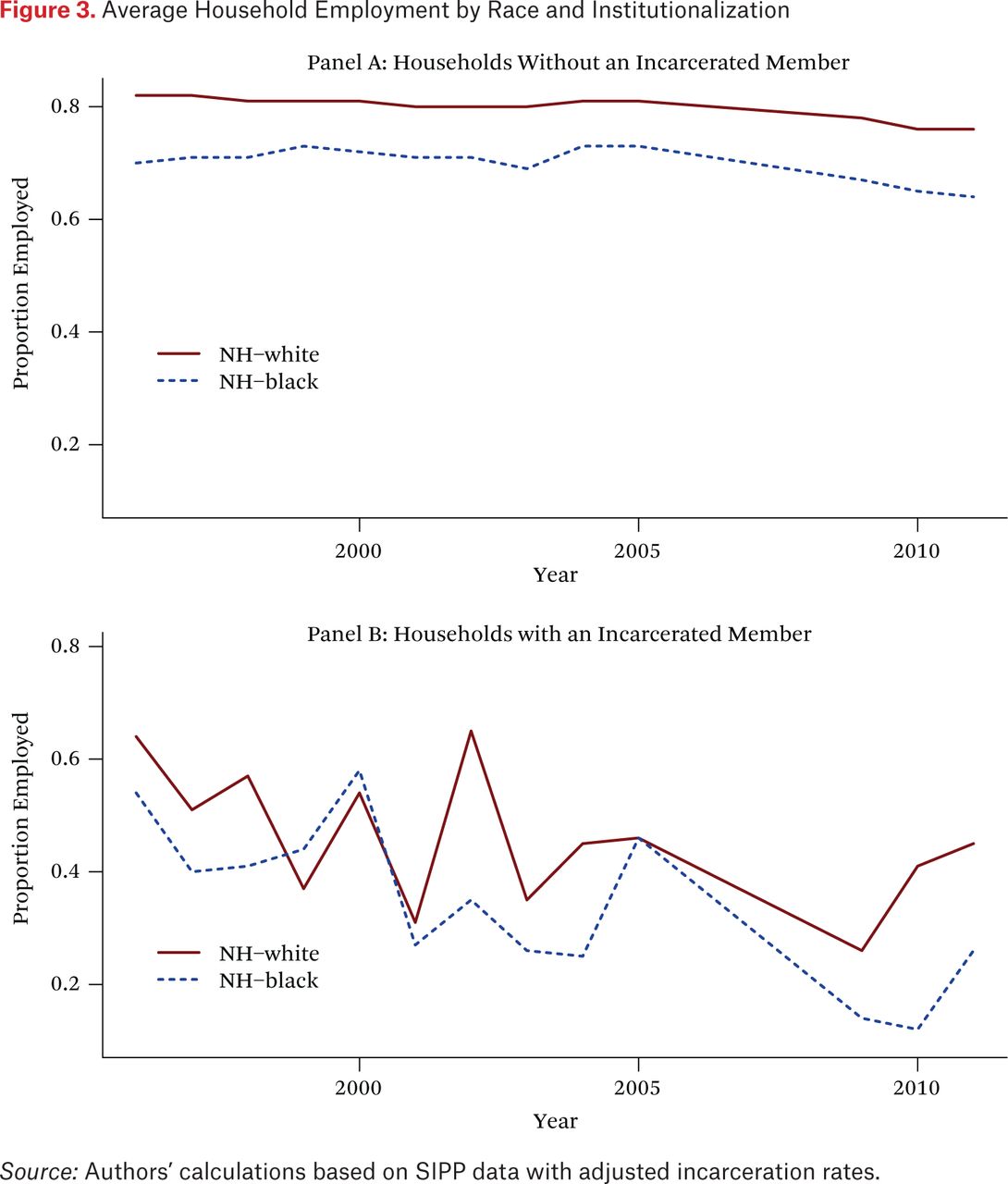

Figure 3 plots average household employment by race and institutionalization. In the first panel, nearly 82 percent of non-Hispanic whites without an institutionalized family member were employed in 1996. By the close of 2011, this figure had fallen 6 percentage points to 76 percent.6 In comparison, black households without an institutionalized family member saw their employment rates rise from 70 percent in 1996 to 73 percent in 2005. However, by the end of 2011, only 64 percent of respondents in black households without an incarcerated member were employed.

Average Household Employment by Race and Institutionalization

The lower panel shows the employment rates among households with an incarcerated family member. The employment rates are much lower among whites and blacks in residences exposed to incarceration. Between 1996 and 2011, white households with an incarcerated family member had an employment rate that fell from 64 percent to 45 percent over the period. Household employment is much more dire among blacks when a family member is incarcerated. In 1996, 54 percent were employed, but only 26 percent were employed by the close of 2011, a drop of nearly 28 percentage points.

Finally, table 6 presents marginal effects of changes in institutionalization on employment. A previous incarceration was not statistically associated with an increased probability of employment when the household held any assets. However, a comparison of estimates using the unadjusted SIPP weights and the adjusted SIPP-incarceration weights shows a large point-estimate change for previous institutionalization. The debt model confirms that this positive change is real, suggesting that perhaps a previous incarceration and increases in the probability of employment may be mandated by parole, probation, or court agents.

Marginal Effects of Changes in Institutionalization on Employment

CONCLUSIONS AND IMPLICATIONS

Recent statistics from a Gallup poll indicate that two-thirds of Americans are dissatisfied with the way income and wealth are distributed in the United States (Newport 2015). At the same time, concern is growing about the reach and pull of mass incarceration in America, particularly for measuring socioeconomic progress among families (Pettit 2012; Pettit and Sykes 2015; Sykes and Pettit 2014, 2015). However, no scholarship has linked these two disparate social problems to better understand the relationship between mass incarceration and household wealth over time. Our paper addresses this issue using longitudinal data on incarceration, assets, and debt among household members to explore the spillover effects of incarceration on wealth accumulation.

We find that incarceration not only influences the wealth and assets of the formerly incarcerated person but also spreads across households to affect the assets and debt of family members. The institutionalization of a family member was associated with a 64.3 percent decrease in asset levels and an 86.1 percent decrease in debt levels, as reported in our weighted models in table 3. Families with an institutionalized member were also 2.7 percentage points less likely to report owning any assets and 3.9 points less likely to report owning any debt, compared to otherwise similar households without institutionalized members (see table 4). With these findings, we provide additional evidence for the collateral damage associated with incarceration’s spillover effects for non-incarcerated household members, show support for incarceration’s contagious consequences for families, and bring together conversations of wealth inequality and mass incarceration.

In these relationships, incarceration directly and indirectly influences wealth. By reducing employment and increasing economic strain on families, incarceration can also limit any opportunities for asset accumulation. Institutionalization’s negative association with both assets and debt also indicates that it blocks access to credit markets and lending institutions. It can do so through its negative effects on credit scores, which most lenders use to make credit-based lending decisions, and the potential use of a household family member’s incarceration itself in a lender’s decision. Former offenders might also be choosing to avoid mainstream lending institutions, which further impedes their ability to build wealth.

In addition to highlighting incarceration’s relationship with household wealth, our findings also contribute to studies of racial inequality in wealth. Racial wealth disparities that continue after accounting for education and income are well documented in the United States. For instance, non-Hispanic black households held about 80.4 percent less in assets and 74.6 percent less in debts than similar non-Hispanic white households in our study (see table 3). Although these large disparities could be compounded by the institutionalization of a family member, we did not find support for this relationship, partly because most non-Hispanic black households held little wealth before the family member was institutionalized.7

In fact, because the association between institutionalization and assets was weaker than the associations for race, a non-Hispanic white household with an institutionalized member would actually hold more in assets than an otherwise similar black or Hispanic household without an institutionalized member. This finding mirrors that of Thompson and Conley (this issue), who show that white families facing health shocks still had greater wealth than black families who did not. Overall, by highlighting the associations across institutionalization, race, and wealth, we show that the disproportionate incarceration of young black men with limited education also helps explain these wealth disparities at a household level.

Our study has a few potential limitations. First, wealth estimates tend to be inconsistent because of the complexity of measuring the various components of wealth, a lack of standardization across surveys, and the difficulty many respondents have in estimating their wealth (Spilerman 2000). To help account for inconsistencies, SIPP includes questions about different types of assets and debt, regularly incorporates reinterview checks, and compares results with Flow of Funds and Survey of Consumer Finances data from the Federal Reserve Board (Czajka, Jacobson, and Cody 2003; Kalton et al. 1998). A second potential limitation is that we cannot control for selection into incarceration because measures of delinquency and low self-control—risk factors for future institutionalization—are not included in SIPP.

Despite these possible drawbacks, we provide a methodological contribution by using institutionalization as a proxy for incarceration in household surveys. National surveys, like SIPP, that report lower estimates of institutionalization may also underestimate the impact of incarceration on asset accumulation and debt reduction. We provide one possible solution for incorporating inmates into national surveys, but to do so requires at least one measure with which to benchmark incarceration statistics to official records. Foucault (2015, 196) highlights how the production of knowledge requires adequate record keeping (or “recordings”). Yet the social exclusion inherent in national surveys that render inmates invisible (Pettit 2012) and undercount families receiving government aid (Meyer, Mok, and Sullivan 2009) leads to what he calls the penalization of existence: “a diffuse, everyday penality, with para-penal extensions introduced into the social body itself, prior to the judicial apparatus” that shapes “rewards and punishments” (Foucault 2015, 193). We show that the penalization of existence conferred to former inmates is dispersed throughout the household, affecting the components of wealth for everyone in residence and further concentrating social disadvantage at a residential level.

Acknowledgments

An earlier version of this paper was presented at the Russell Sage Wealth Inequality Meeting in October 2015 and the 2016 Annual Meeting of the Population Association of America. We thank Fabian Pfeffer, Robert Schoeni, Sheldon Danziger, Robert Hauser, Alexandra Killewald, anonymous reviewers, and participants of the RSF Wealth Inequality Meeting for comments on previous versions of our paper.

Appendix

Interview Dates for Assets and Liabilities Topical Modules by SIPP Panel

FOOTNOTES

↵1. Although institutionalization is usually conceptualized to include respondents who exited and entered the home due to military enlistment and assisted-care living environments, our measure based on SIPP data does not include active military personnel, students living in dormitories, or old-age assisted group quarters.

↵2. The y-axes of these panels have been scaled similarly to facilitate comparisons of within-race and between-group differences in wealth (figure 1), debt (figure 2), and employment (figure 3) among households with and without a member institutionalized.

↵3. For instance, in 2003 one non-Hispanic white household with an institutionalized member actually held more than $3 million in assets, which skewed the results for this year. SIPP data limitations for measuring wealth, in combination with the low number of respondents institutionalized, may explain this variation.

↵4. Model fit improved considerably with the functional form transformation, even though this leads to a truncated distribution. To account for this, we also assess the relationship between institutionalization and the presence of any assets or debt in subsequent models.

↵5. Because many of these coefficients exceed 0.1, we use the following formula to determine the percentage change in assets and debt for a one-unit change in each predictor variable: %Δ(y) = 100*(eb – 1) (Gelman and Hill 2007; Wooldridge 2009, 190).

↵6. We benchmarked these estimates to employment to population ratios (EPR) presented in Becky Pettit, Bryan Sykes, and Bruce Western’s study (2009, table 17). Because 2008 is the last year in the report before the 2008 SIPP panel began interviewing respondents for wave 4 in 2009 (see table A1), we can only compare estimates of our SIPP-incarceration adjusted EPR with that in Pettit, Sykes, and Western for 2005. Pettit and her colleagues report an EPR of 80.6 in 2005 for men; our comparable EPR is 80.8 using the SIPP-incarcerated adjusted weights.

↵7. We are cautious in this conclusion because to test this proposition may require exogenous variation in exposure to incarceration at the household level. We used day of entry into the household, day of exit from the household, and job training and job seeking programs that were subsidized by welfare and social service agencies as instrumental variables for institutionalization within the 1996 panel (the only panel that had these variables) to assess this proposition. Despite various model specifications for institutional endogeneity, our instruments were not very strong. Douglas Staiger and James Stock (1997) recommend an F-value of 10 or greater for strong instruments; ours was 7.3.

- Copyright © 2016 by Russell Sage Foundation. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Reproduction by the United States Government in whole or in part is permitted for any purpose. An earlier version of this paper was presented at the Russell Sage Wealth Inequality Meeting in October 2015 and the 2016 Annual Meeting of the Population Association of America. We thank Fabian Pfeffer, Robert Schoeni, Sheldon Danziger, Robert Hauser, Alexandra Killewald, anonymous reviewers, and participants of the RSF Wealth Inequality Meeting for comments on previous versions of our paper. Direct correspondence to: Bryan L. Sykes at blsykes{at}uci.edu, 3317 Social Ecology II, University of California, Irvine, CA 92697; and Michelle Maroto at maroto{at}ualberta.ca, 6-23, Tory Building, University of Alberta, Edmonton, AB T6G 2H4, Canada.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.