Abstract

In this article, we assess the utility of the American Voices Project in supplementing more traditional sources of labor market data. To do so, we explore the effects of safety net program expansions on household financial stability and labor force participation during the COVID-19 pandemic. We find that despite the expanded safety net, employment loss was sometimes associated with declines in financial well-being. We find little evidence of the programs disincentivizing work, however. Pandemic relief programs helped cover essential living expenses, but implementation challenges muted their effects for some. Connections between employment loss and declines in mental well-being, as well as both the vulnerability and importance of gig work, emerged as prominent, if unexpected, themes. Our analysis suggests that, with improvements, an ongoing, large-scale qualitative data collection effort could be an invaluable asset in monitoring labor market conditions in low-income communities.

- American Voices Project

- pandemic labor market

- unemployment insurance benefits

- mental well-being

- gig work

The first known case of COVID-19 reached American shores in January 2020 (Centers for Disease Control and Prevention 2022), and by mid-March, the disease had set in motion both a public health epidemic and an economic recession. Many of those who were spared from the worst effects of the former were subjected to the widespread impacts of the latter. In the weeks and months following the onset of the pandemic, the federal government embarked on a series of efforts to mitigate the economic harm to workers and the households they supported as the country entered recession.

The economic impacts of the COVID-19 recession and subsequent policy responses to mitigate those impacts fed competing narratives about how expanded safety net programs impacted the financial stability and labor market decisions of low-income households. Articles and editorials in the popular press debated whether expanded unemployment benefits reduced worker participation in the labor force (Mulligan and Moore 2020; Iacurci 2021), or whether the missing workers were absent due to other COVID-related factors, such as fear of disease, school closures, or retirements (Chaney Cambon and Dougherty 2021). The perception that unemployment benefits were keeping workers on the sidelines of the labor market were among the reasons that roughly half of the states ended certain benefits prior to their federal expiration (Whittaker and Isaacs 2021). Simultaneously, research and public opinion, although not necessarily contradictory, were not always aligned on these topics and at times conveyed varying levels of impact; as an example, Economic Impact Payments (EIPs) and the refundable child tax credit lifted more than fourteen million people out of poverty in 2021 (Creamer et al. 2022), but the majority of recipients responding to one survey believed the funds helped them only “a little” (Marist Institute for Public Opinion 2021).

With these competing narratives as backdrop, we aimed to assess the potential of the American Voices Project (AVP) as an instrument for collecting policy-relevant labor market information that could supplement conventional survey and administrative data. As a first-of-its-kind data collection effort involving immersive interviews with more than two thousand households across the United States, we wondered whether the AVP as designed and executed could deliver the breadth and depth of qualitative data necessary to enrich, validate, or challenge conclusions reached with quantitative data while providing additional nuance around the complex decisions income-constrained households made during this period. To assess the AVP’s ability to do so, we leverage seventy-six interviews conducted between the fall of 2020 and the summer of 2021, focusing on low-income households most likely to be in the labor force and benefit from pandemic relief programs. We structured our exploration of the AVP data set around these policy-relevant research questions: How did interviewees experiencing negative employment effects describe the role that safety net programs played in stabilizing household finances? Is there evidence that these programs affected the employment or job-search behaviors of beneficiaries?

The AVP interviews in our sample offer a nuanced understanding of how low-income households were experiencing and responding to pandemic-induced economic shocks. Consistent with prior research, we find that for many low-income households, the pandemic and recession led to a loss of employment that took many forms, from a slight reduction in hours to a permanent layoff. However, the depth and prevalence of related financial hardships described in the interviews challenge the broader notion of households on firm financial footing, propped up by pandemic relief programs and disincentivized to return to work. Instead, interviewees’ experiences with acute financial difficulties during the pandemic were more aligned with quantitative research highlighting the financial distress that persisted despite these programs. Some interviewees described how pandemic relief funds, when delivered, and gig work activities, when not disrupted by the pandemic, were paramount to covering essential living expenses. Interviewees also highlighted the important connections between mental well-being and financial stability as they described heightened levels of stress, worry, and anxiety about making ends meet during the pandemic.

We view our analysis as a test-drive of sorts for how a data set such as the AVP could be used to contribute to policy-relevant research in the future. When we compare our findings with the literature, we consider none to be wholly novel. That is, research preceding ours and reviewed in this article also finds evidence of household-level financial distress and the problematic deployment of unemployment benefits during the pandemic, for example. However, the alignment between our findings and prior, mostly quantitative, work does not render AVP data redundant or superfluous. Instead, it is a testament to its validity. This article also deepens our understanding of the pandemic economy at the household level, giving robust insight into experiences that might otherwise be masked by averages and aggregate statistics. We conclude that with some improvements a generic, immersive-interviewing platform such as the AVP could serve as a valuable complement to the existing and emerging quantitative infrastructure in monitoring economic conditions in low-income communities.

BACKGROUND

The COVID-19 pandemic was an unprecedented shock to the U.S. economy.

Employment Disruption for Low-Income Households

Over two months in the spring of 2020, nonfarm payroll employment declined by almost 22 million jobs, roughly 17.million workers became unemployed, and the unemployment rate increased from 3.5 percent to 14.8 percent.1 Employment losses were concentrated in industries that relied on face-to-face interaction and services and, due in part to their higher representation in susceptible industries, Hispanic and Black, younger, and lower-income workers, as well as workers with less formal education, were more likely than others to experience job loss (FRB 2021; Despard et al. 2020; Karpman et al. 2020; Wardrip 2021; Cortes and Forsythe 2021; Horowitz, Brown, and Minkin 2021; Bartik et al. 2020; Bell et al. 2020), which took the form of reduced hours, the elimination of a position, and the loss of self-employment (FRB 2020; FRB 2021; Horowitz, Brown, and Minkin 2021).

The COVID-19 recession arrived quickly but lasted only two months, March through April of 2020 (NBER 2023). The early recovery was characterized by the recall of workers from temporary layoff and a subsequent rapid rebound in overall employment levels (Wolcott et al. 2020; Forsythe et al. 2020). The economic disruption proved to be longer lasting for some, however, given that only about half of the adults laid off because of the pandemic had returned or expected to return to their former job as of late 2020 (FRB 2021) and certain groups of workers (such as low-wage workers, Black workers) were less likely to regain employment than others (Cortes and Forsythe 2021; Bartik et al. 2020). The broader economic recovery continued into 2021 as unemployment steadily declined and payroll employment gradually increased, although at year end, they would remain above and below pre-pandemic levels, respectively.2

The Federal Safety Net

Acting quickly to support dislocated workers, the federal government created and enhanced a number of programs to blunt the economic effects of the pandemic and associated recession, including a major expansion of the unemployment insurance (UI) system. Passed in March 2020, the Coronavirus Aid, Relief, and Economic Security (CARES) Act and subsequent legislation modified the UI system along three dimensions to amplify its generosity and reach: benefit levels were increased; eligibility was expanded; and duration was extended. Between April and July 2020, UI claimants received a supplement of $600 in addition to their regular benefits through the Federal Pandemic Unemployment Compensation program; the supplement expired and in January 2021 was replaced by a $300 top-up. Further, through the Pandemic Unemployment Assistance (PUA) program, eligibility was extended to those not generally covered by the UI system, including self-employed workers, gig and contract workers, and those with a limited work history. Finally, the duration of benefits was extended through the Pandemic Emergency Unemployment Compensation program; with the exception of the five-month lapse and subsequent reduction of the supplement, these programs extended benefits through early September 2021 (BEA 2021). However, roughly half of the states terminated their participation in one or all of these programs in June or July 2021 for numerous reasons, including concern that programs were keeping potential workers out of the labor force and in light of the growing number of job openings (Whittaker and Isaacs 2021).

The $600 supplement available to UI recipients in mid-2020 was designed to replace the earnings of the average worker (Bartik et al. 2020), but because pandemic job losses were concentrated in low-wage industries, the “replacement rate” (share of prior earnings replaced by benefits) for many UI recipients exceeded 100 percent. In fact, workers with the lowest wages were eligible for benefits that would have doubled their prior earnings, and the median replacement rate was estimated to be 145 percent (Ganong et al. 2020). A survey conducted in July 2020 suggests that among low-income households that received UI benefits, the vast majority reported that their income was higher than (56 percent) or about the same as (27 percent) their pre-layoff earnings (FRB 2020). The expiration of the $600 supplement in the summer of 2020 lowered the median replacement rate below 50 percent until the smaller $300 supplement was implemented in January 2021, raising the replacement rate again above 100 percent for the lowest-earning half of dislocated workers (Cortes and Forsythe 2021).

The apparent generosity of expanded and enhanced UI benefits must be considered alongside the ability of those experiencing job loss to access them. An analysis of Department of Labor data shows that only 28 percent of unemployed workers received regular UI benefits in 2019; at least in part due to the longer duration of benefits permitted during the pandemic, this share rose to 78 percent in 2020, even before factoring in the PUA program that expanded eligibility (Ganong et al. 2022). A simulation combining publicly available data to estimate individual eligibility with administrative data on actual payments suggests that the vast majority of those eligible for UI benefits received them, although the recipiency rate for the PUA program (76 percent) appears to have been lower than for standard UI (98 percent) (Forsythe 2023). Survey data tell a less optimistic story. Self-reported receipt of UI benefits among seemingly eligible workers was a much lower 36 percent, although benefit receipt in survey data is known to be underestimated (Forsythe and Yang 2021). Among those who applied for UI benefits between March and December 2020, roughly three-quarters (77 percent) reported being successful (Carey et al. 2021), but even successful applicants may have experienced delays in the delivery of their benefits (Bitler et al. 2020) because some state UI offices were suffering from well-documented backlogs in processing claims stretching weeks or months (DOL 2021). The rollout of the PUA program was notably problematic. Most states took more than thirty days to implement the program (DOL 2021), payments were subject to long delays (Greig et al. 2021), and some states initially paid recipients the minimum allowable benefit in order to expedite payments, with the expectation that recipients would be made whole retroactively (GAO 2020b).

Compounding their administrative and operational challenges, the UI programs did not provide relief equitably, cushioning the loss of earnings for some groups of workers more than for others. UI receipt varied dramatically—but not randomly—by state, as pandemic-era access to benefits was associated with the states’ UI policies and pre-pandemic coverage levels (Bell et al. 2021; Carey et al. 2021; Forsythe and Yang 2021). Among those who applied for UI benefits through the end of 2020, Black and Hispanic workers, younger workers, workers from lower-income households, and workers with less formal education were less likely to receive them (Carey et al. 2021). The lower recipiency rate for PUA-eligible individuals also likely disproportionately affected low-wage workers (Forsythe 2023).

In addition to UI benefits that directly targeted workers displaced by the pandemic, the federal government also approved more broadly targeted direct cash transfers. Between March 2020 and March 2021, Congress approved three rounds of EIPs ranging from $1,200 to $2,800 for each married couple and from $500 to $1,400 for each dependent child. Payments began phasing out for couples with an adjusted gross income of more than $150,000. Married parents earning less than $150,000 and supporting two children would have been eligible for a total of $11,400 (Treasury n.d.). Relative to the UI programs, the disbursement of EIPs went smoothly, relying as it did on information contained in previously filed federal tax returns. However, an assessment of the first round of EIPs found that nearly nine million eligible individuals had not received their funds several months after disbursement began, many because their low level of income did not require them to file a tax return. The assessment also uncovered issues related to underpayment as well as problems with the distribution of prepaid debit cards for recipients with no bank account information on file (GAO 2020a). A survey conducted in May 2020 indicated that, relative to higher-income and White respondents, individuals living below the poverty line and Black and Hispanic individuals were less likely to receive the initial EIP (Holtzblatt and Karpman 2020). Additional analyses of bank account and survey data suggest that individuals with lower balances and lower incomes were less likely to receive an EIP than those with greater resources (Ratcliffe et al. 2023).

Mixed Signals on Household Financial Stability

In the aggregate, the UI and EIP programs kept millions out of poverty, particularly in the early months of the pandemic (Han, Meyer, and Sullivan 2020; Parolin et al. 2020), and the UI program alone lowered the official count of the impoverished by 4.7 million in 2020 (Chen and Shrider 2021). Both safety net programs continued to lift millions above the poverty threshold into 2021 (Creamer et al. 2022), a year in which self-reported financial well-being reached its highest level in a national survey begun in 2013 (FRB 2022). Further, those making less than $30,000 annually saw a two percentage-point improvement in their financial health between 2020 and 2021 (Dunn et al. 2021). There is a vast body of evidence suggesting that those who received UI benefits had an economic advantage over those who applied for but did not receive such benefits (FRB 2020; Carey et al. 2021; Dunn et al. 2021); similar findings are associated with the receipt of EIPs (Dunn et al. 2021; Karpman and Acs 2020).

Evidence is clear that both EIPs and UI benefits provided needed financial support and promoted general economic security for those who received them (Whittaker and Isaacs 2022), with the benefits accruing to some types of households more than others. EIPs disproportionately supported the spending needs of lower-income and unemployed households (Armantier et al. 2021; Boutros 2020), as well as those living paycheck to paycheck, those with lower account balances and liquid wealth, and Black and Hispanic adults (Karger and Rajan 2021; Baker et al. 2020; Parker et al. 2021, 2022; Horowitz, Brown, and Minkin 2021). In addition to helping cover typical expenses, the receipt of both EIPs and UI benefits led to spending increases for low-income households (Chetty et al. 2020; Chetty, Friedman, and Stepner 2021; Greig, Deadman, and Noel 2021). Account balances declined more quickly for unemployed, younger, and lower-income account holders than for their counterparts, however (Farrell et al. 2020; Greig, Deadman, and Noel 2021). A study using checking account data shows that the lowest-income account holders had the highest percent increase in account balances (65 percent) in December 2021 relative to 2019 levels, but given their low starting points, this amounted to an increase of only around $500 (Greig, Deadman, and Sonthalia 2022).

Given the dramatic level of job loss and the temporary and episodic nature of the UI programs and EIP disbursement, to say nothing of the noted challenges with their administration, improvements in aggregate measures of well-being mask a fair amount of heterogeneity. In spite of the safety net programs, those who lost employment were much more likely than those who had not been laid off to struggle covering their expenses (FRB 2021; Holzer, Hubbard, and Strain 2021; Despard et al. 2020; Dua et al. 2021), with higher levels of financial distress observed both for those with lower levels of education and for Black and Hispanic adults (Dunn et al. 2021; FRB 2021). Financial stressors included difficulty covering food costs, medical expenses, and housing payments (Bitler et al. 2020; Dua et al. 2021; Despard et al. 2020; GAO 2020b; Karpman et al. 2020). Of note, according to a survey administered in early 2021, even among those using UI benefits to cover spending needs, nearly one-third had a very difficult time meeting usual household expenses, and nearly one-quarter of those also receiving SNAP benefits occasionally experienced food insecurity (Mohanty 2021). A reliance on earnings rather than benefits was far from a guarantee of financial stability, given that about half of those who experienced a pay cut after February 2020 reported earning less money in early 2021 than before the pandemic (Horowitz, Brown, and Minkin 2021).

Low-income households facing economic distress discussed a variety of coping strategies, including increased indebtedness, a reduction in spending, and the depletion of savings (Mattingly et al. 2021; Karpman et al. 2020). Some adults who experienced income volatility turned to gig work, a strategy that may have been only partially effective in smoothing earnings during the pandemic (FRB 2021; Liu 2020), but one that may have filled a desire to work and, in some cases, to receive income more quickly than UI claims could be processed (Ravenelle, Kowalski, and Janko 2021).

The Work Disincentives Debate

As discussed, whether and the extent to which workers opted out of the labor force in favor of enhanced UI benefits was a contested topic in the popular press, and it received a substantial amount of attention from the research community. The evidence is mixed.

Focusing on the effects of the $600 supplement, analyses of small business payroll data suggest that differences in states’ replacement rates had little to no effect on a worker’s likelihood of remaining unemployed or returning to work (Bartik et al. 2020; Finamor and Scott 2021). Likewise, states’ relative replacement rates were not found to be associated with job growth after the supplement ended (Dube 2021). Although one study suggests that the $600 supplement had a larger effect on job application activity (Marinescu, Skandalis, and Zhao 2021), the effect on recipients’ job-finding rates seems to have been only small to moderate (Ganong et al. 2023; Petrosky-Nadeau and Valletta 2023).

The decision made by some governors to end the $300 supplement in mid-2021 prior to its federal expiration provided another opportunity to test whether enhanced UI benefits were affecting workers’ decision to participate in the labor force. When states announced their intention to end the benefit early, their share of national online job postings clicks increased measurably but fleetingly (Kolko 2021). Comparing workers’ behavior in states that withdrew with those in states that retained the supplement, an analysis of bank transaction data finds a modest increase in the job-finding rate of workers in the former but attributes the finding to the exhaustion of UI benefits rather than the ending of the $300 supplement; this effect is characterized as being toward the lower end of what historical research on UI would suggest (Coombs et al. 2022). Other studies using a traditional labor market survey also find employment increases in states that ended the $300 supplement early (Arbogast and Dupor 2023; Holzer, Hubbard, and Strain 2021). With a few exceptions, the research generally suggests that even though the expansion of UI benefits had measurable impacts on the propensity to seek work, the impacts were relatively small (Ganong et al. 2022). The temporary nature of the pandemic-era supplements, the difficulty finding a job during a recession, and the prevalence of workers being recalled after a temporary layoff are offered as explanations for the relatively small employment effects associated with both supplements (Ganong et al. 2023), alongside health risks during the pandemic and the closure of schools and daycares (Ganong et al. 2022).

Workers themselves also shed light on the degree to which UI benefits and EIP receipt affected their decision to rejoin or remain in the labor force. In nationwide focus groups, noncollege workers generally suggested that support from these programs did not allow them to stop seeking employment altogether but, in some cases, gave them the flexibility to find better-paying work instead of accepting the first offer (Miller et al. 2023). In a survey administered to employees of small businesses in mid-2020, only 7 percent of those negatively affected by COVID said they would not look for work because it was not financially necessary to do so (Bartik et al. 2020). Another survey exploring the first round of EIPs found that the payments would not affect the labor force activity of the vast majority of respondents. Among unemployed respondents, more suggested they would begin looking for a job or put more effort into their existing search after receiving an EIP than said an EIP would reduce their job-search activity (Coibion, Gorodnichenko, and Weber 2020). Finally, in response to a survey administered in mid-2021, unemployed noncollege workers who were not urgently searching for a job suggested that the fear of contracting COVID was the primary reason for their lack of urgency. For these workers, the three most important milestones that would encourage a return to work were the availability of more job opportunities, increased vaccinations, and UI benefits or savings running out, in that order (Bunker 2021).

Existing research leaves no room for doubt that lower-wage and noncollege workers bore the brunt of the employment disruptions associated with COVID-19 pandemic and recession. Aggregate statistics indicate that the relatively generous expansion of UI benefits and the distribution of EIPs fortified household balance sheets in the wake of this employment shock, but there is also evidence that certain groups faced unequal access to these resources and persistent economic hardship. Complementing more traditional sources of survey and administrative data, the AVP offers a new source of in-depth information collected directly from scores of low-income households who shared their stories during this tumultuous period. As a first-of-its-kind, large-scale immersive-interviewing platform, we assess the utility of the AVP as a tool to monitor labor market conditions during a crisis by exploring these households’ experiences in the labor market, their efforts to balance a budget, their interactions with state UI offices, and their decisions surrounding labor force participation.

DATA AND METHODS

This analysis follows as closely as possible the consolidated criteria for reporting qualitative research (Tong, Sainsbury, and Craig 2007). Our three-person research team (two males, one female) includes members of the Community Development departments at the Federal Reserve Banks of Cleveland and Philadelphia. Our team generally focuses on issues related to workforce development and economic mobility for low- and moderate-income individuals. We are seasoned research professionals but less experienced with the type of full-scale qualitative research project undertaken in this analysis. Recognizing our inexperience, we sought out and benefited from the guidance and support of an experienced qualitative methodologist throughout this project. Eight Federal Reserve Banks, including our own, were among a coalition of AVP supporters, but the research team was not connected to the production of data.

Data

In this analysis, we rely exclusively on AVP interview transcripts. The AVP was a large-scale, qualitative data collection effort involving a representative sample of American households and led by the Stanford Center on Poverty and Inequality. The interview protocol included roughly two hundred questions spanning a wide range of topics such as life history, family, daily routines, and health; detailed demographic information was collected for each household member, as were data on living costs, income, and program participation, including the receipt of UI benefits. The interviews, which were conducted by current college students or college graduates who received intensive training in qualitative interviewing, lasted an average of 2.2 hours, and interviewees were compensated anywhere from $60 to $145 for their time (Stanford Center on Poverty and Inequality 2021). In total, more than 2,700 interviews were conducted between July 2019 and August 2021, with those prior to the onset of the COVID-19 pandemic conducted in person and the remainder by phone. In March 2020, questions exploring the impact of the pandemic were added to the interview protocol, including a question about the receipt of stimulus funds (that is, EIPs); additional questions about crossroads and turning points that tended to yield very rich responses were added in September 2020. Interviews were recorded, and transcripts were deidentified before being made available for research purposes. Additional information on the AVP data set can be found in the introduction to this issue (Edin et al. 2024).

Approach

We consider our approach to be aligned with thematic analysis as described in Virginia Braun and Victoria Clarke (2006). Our research questions were motivated by an interest in better understanding the COVID-19 pandemic and associated federal relief programs on low-income households—and specifically, how these relief programs affected household financial stability and labor force attachment. As is customary with secondary analysis, we underwent an inductive process to collect information relevant to our research questions, remaining flexible to allow the data to guide and refine our focus (Hinds, Vogel, and Clarke-Steffen 1997; Chatfield 2020). Doing so allowed us to not only address our specific research questions but also provide important, if unexpected, context on the employment and financial experiences of low-income households during this period.

Sample Selection

We use the second national sample of AVP interviews, conducted between September 2020 and August 2021 because it included new questions that yielded responses relevant to our inquiry. More than seven hundred interviews were completed as part of the second national sample, but only 490 had been transcribed at the time of our analysis. We limit our sample to households with earnings below 200 percent of the poverty level for the corresponding year, using Health and Human Services poverty guidelines for 2020 and 2021, adjusted for household size. We further restrict the sample to interviewees younger than fifty-five years old and exclude those who were disabled, retired, a seasonal worker, or a full-time student. We use household earnings to select our sample because research on the pandemic’s employment effects shows that low-wage workers absorbed the brunt of the job losses and received the greatest boost to their income through the expanded safety net programs. The other exclusions allow us to focus on those most likely to be in the labor force, which was critical to our research questions. Seventy-six interviewees satisfied these criteria.

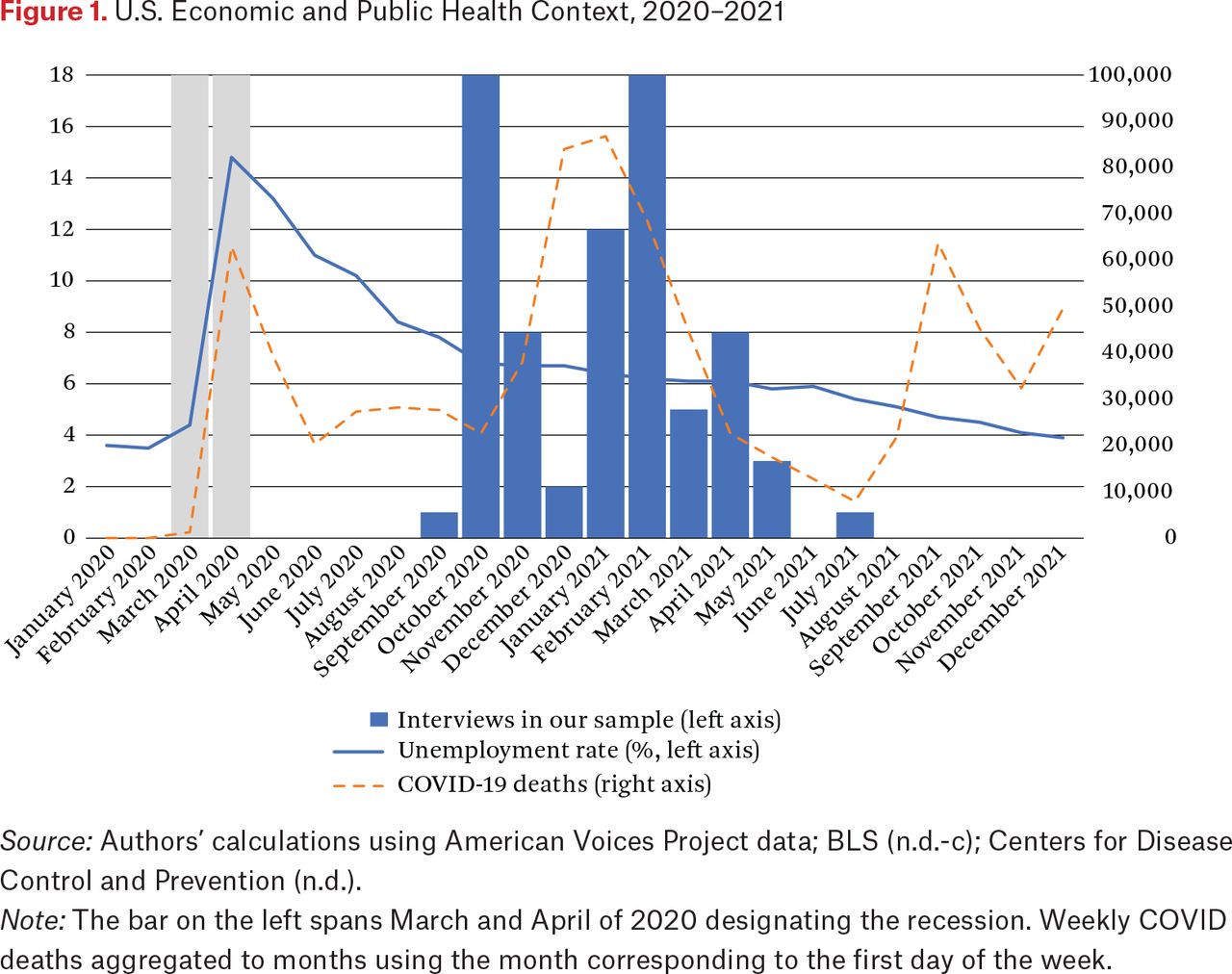

Relative to the second national sample and largely a product of our selection criteria, households in our sample had much lower earnings in the last year, were considerably younger, had lower levels of educational attainment, included more people per household, and were more likely to be employed or in the labor force (see table 1). Our sample also has broad geographic representation, including transcripts from twenty-one of the thirty-six states represented in the second national sample. These interviews were conducted during a period when COVID-19 presented significant health risks, and while the economy was improving, the unemployment rate was still above pre-pandemic levels (see figure 1).

Interviewee Characteristics

U.S. Economic and Public Health Context, 2020–2021

Source: Authors’ calculations using American Voices Project data; BLS (n.d.-c); Centers for Disease Control and Prevention (n.d.).

Note: The bar on the left spans March and April of 2020 designating the recession. Weekly COVID deaths aggregated to months using the month corresponding to the first day of the week.

Analysis

We used an inductive process to develop our codebook as we became familiar with the information contained in the transcripts. As mentioned, our initial reading of the transcripts allowed us to gain familiarity with content and develop our codebook. We refined our initial codebook through an iterative process of double and triple coding more than twenty transcripts, using NVivo (March 2020 version), a qualitative software program to facilitate the coding of passages, store results, and ensure coding consistency. During this process, we collectively discussed and settled discrepancies among coders, which helped us refine the definitions of our codes. To ensure a common and consistent understanding of the codebook throughout the analysis, we double-coded every fifth transcript and discussed and resolved any differences. After we finished coding the transcripts, we independently summarized what we viewed as the major themes associated with each code and then met as a team to discuss our interpretations and settle on what we consider to be our primary findings. As part of this process, we used the demographic information collected during the interviews to explore whether any themes were more or less prevalent across a variety of household characteristics, including the number of adults and children present, the ratio of last year’s earnings to the federal poverty guideline, residence in an urban, suburban, or rural area, and the race and ethnicity, education, age, and country of birth for adults in the household.3

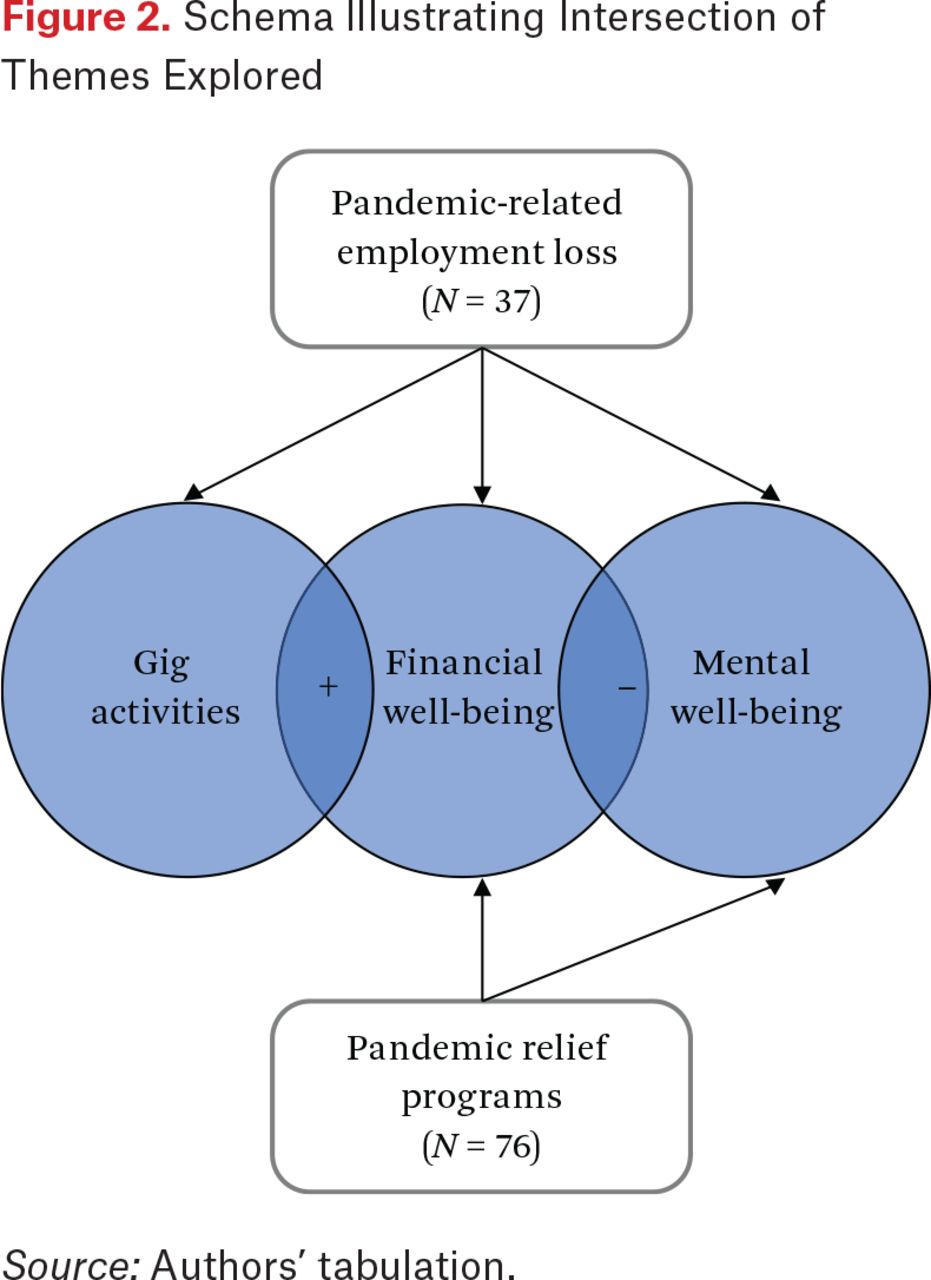

Figure 2 presents a visual oversimplification of our codebook and a preview of how we present our findings in the following section. It also clearly depicts how our exploration of the transcripts for information related specifically to household financial stability and the ways that pandemic relief programs might disincentivize work led to the discovery of our primary themes. Although the transcripts contained virtually no information suggesting safety net programs affected household members’ labor force participation, they were rich in information on the connection between employment loss and financial hardship. Further, we found that gig work was both a direct casualty of the pandemic and a common financial coping strategy. For some interviewees, employment loss and subsequent financial distress led to heightened levels of stress and anxiety, which we refer to broadly as negative impacts on interviewees’ mental well-being.4 Depending on their implementation, pandemic relief programs played a role in lessening these hardships for some and compounding them for others.

Schema Illustrating Intersection of Themes Explored

Source: Authors’ tabulation.

FINDINGS

The labor market disruption wrought by the COVID-19 pandemic has been well established, but interviewees’ accounts of this disruption provide important context for our findings. Given the economy-wide magnitude of job losses and their concentration at the lower end of the wage spectrum, it is perhaps unsurprising that we find evidence of pandemic-related employment loss for a subsample of thirty-seven of the seventy-six households (the subsample). Many of these interviewees, or those in their household, experienced a permanent layoff as a direct consequence of the COVID-19 recession, but reduced hours and temporary layoffs of weeks or months were more common.5

It is within the job loss subsample that we explore two primary themes emerging from our analysis. We discuss the impact of employment loss on the subsamples’ financial and mental well-being and then highlight the pandemic’s effects on gig work that played a critical role in stabilizing household finances. We neither searched for nor expected to find rich content on mental well-being and gig work as we reviewed interviewees’ discussions of employment loss and subsequent financial stability, but the importance of these issues was evident in the transcripts. Our final set of findings related to UI benefits and EIPs draws on the full sample to capture the widespread receipt of EIPs across low-income households in our sample.

In an effort to center the voices of those with lived experiences, quotes from fifteen interviewees residing in fourteen states and representing diversity along such dimensions as self-identified race and ethnicity, gender, and age are used throughout this section to support and describe the themes we discuss. The age category of the interviewee, whether the household’s earnings were below 100 percent or between 100 and 199 percent of the federal poverty guideline, the season and year of the interview, and general type of work are provided.6

Financial and Mental Well-Being

In spite of the short-term nature of the employment disruption for many households and the pandemic relief programs available during this period, interviewees from more than half of the households in our subsample described financial hardships or declining financial stability as a direct consequence of their pandemic-related employment loss. Interviewees discussed their difficulties making ends meet; falling behind on rent and utility payments was commonly reported and, in some cases, accompanied by references to subsequent housing instability.7 In the words of one health-care worker who was out of work for months due to the pandemic: “When my rent’s short, I would pay the rent that I’m short on with the next check and then catch up. I didn’t catch up really because I had other expenses like [inaudible]. I tried to catch up as much as I could” [age 35 to 54, below 100 percent, winter 2021].

“Ouch in My Pocket”

Even though none of the households in our sample earned more than twice the poverty level in the prior year, the financial hardship discussed by some interviewees seemed to mark a turning point toward instability. Reflecting on the swiftness of this transition, one worker who was also a student said, “all of a sudden, I don’t have my ducks in a row. And it’s not my fault.” Another remarked that as a result of the pandemic, their “income has changed tremendously” and they “barely make it.” The health-care worker lamented that after paying the rent on time for many years, they had fallen behind on payments and may have no choice but to move without paying what they owe, despite renting from landlords they considered to be good and patient. When asked to compare the last few months with the prior year, an interviewee who worked in the hospitality industry said, “Like, it’s totally different from last year. Last year, I was doing good. This time, the hours are short. We’re not getting paid what we were. So, it’s like been a big ouch in my pocket” [age 35 to 54, below 100 percent, fall 2020].

The apparent disconnect between the temporary bouts of under- or unemployment described by most of this subsample and the level of economic hardship described in the interviews may reflect the small margin for error in the financial conditions of households living in or near poverty. The most common strategy interviewees mentioned to make ends meet involved taking on debt, frequently by borrowing from family or friends but sometimes by using more formal lines of credit. Other strategies included reducing spending, negotiating with creditors, and prioritizing which bills to pay ahead of others. A few also described drawing down savings, but some households had little to no reservoir. When asked whether they would be able to cover an unexpected $400 expense, one construction worker replied,

No, I would not have the money. My bank account is at zero as of right now, so as far as how would I get the money, I might have to ask my mother for a couple of bucks, and then maybe go out to one of my old bosses and try to get a loan or something like that. I don’t really have a lot of resources on extra funds. We’re living day to day. [age 18 to 34, below 100 percent, fall 2020]

“Bad Days”

For some of the households in our subsample, the consequences extended beyond a weakened sense of financial well-being. During the course of their interviews, many also mentioned heightened levels of stress, worry, and anxiety; we refer to these instances collectively as negative effects on the mental well-being of interviewees or members of their household. Roughly one-fourth of these thirty-seven interviewees discussed the impact of their employment loss, or fear of such loss, on their mental well-being. Most associated declines in mental well-being with the financial hardships stemming from their loss of employment, such as the inability to pay rent or keep the lights on, but this laid-off worker’s response to a question about struggling with depression and anxiety suggests the loss of the job itself levied its own emotional toll:

Yeah, I have bad days. I get depressed especially, just not necessarily the lockdown, just not having a full-time job, not being able to, I’m used to paying for everything in the house and now, having to split a bill here and there with pop, I don’t like that just because he raised me and I owe him. He doesn’t owe me, so I mean, I get down on myself not a lot, but a few days here and there, I feel depressed and stuff like that. It’s not overwhelmingly depressed, but I know when it’s happening. I know the days that I’m depressed. I can just feel it, but it’s really more because of the full-time work thing than it is anything else. [age 35 to 54, 100–199 percent, fall 2020]

This quote is illustrative of the depth and acuity of most interviewees’ references to mental well-being—a heightened sense of concern, stress, and anxiety but one that does not pervade the interview. Others, however, conveyed a deeper level of distress. One interviewee who worked in the auto industry described being at their “wits’ end” as they contemplated a return to criminal activities to stay afloat financially. Several interviewees alluded to deep-seated concerns about the future and the uncertainty surrounding their employment and financial situations. Echoing the point made about rising financial instability, the worker-student noted, “Because it’s like, you never know what the next month is going to be like, and I’ve never had that uncertainty, ever in my life.” Describing their current financial situation, a former server said, “It scares me to death, that’s how I feel, I can’t get a job, I can’t get any help, and I don’t know what I’m going to do.”

Work-related stressors evident among interviewees who lost employment were not limited to the financial implications of this loss. Other stressors, such as the fear of catching COVID-19 in the workplace and being overworked, arose but were discussed infrequently. In some cases, however, interviewees shared experiences that reflected the unique, cumulative effects of undergoing financial strain during a pandemic, as one employee working at a car wash stated: “The pandemic has affected my mental health with my anxiety because, I mean, my checks were cut up, so my bills were piling up, being around people and thinking, you know, they might have it has made my anxiety skyrocket to the point where I can’t be around other people or go to store or go to the restaurant, I don’t feel safe” [age 18 to 34, 100–199 percent, fall 2020].

Among the thirty-seven interviewees in the subsample, households with earnings below 100 percent of the federal poverty guideline and those with a lower level of formal education (no more than a high school diploma) were more likely to discuss negative impacts on both their financial and mental well-being than were their higher-income and more formally educated counterparts, respectively. These differences by educational attainment may be explained by the correlation in our sample between education and earnings.

Gig Work

As stated previously and as illustrated by the experiences of the thirty-seven households in our subsample, pandemic-related employment loss took many different forms, from a short-term reduction in hours to a permanent layoff. In some cases, the pandemic disrupted the earnings from a traditional employee-employer relationship (W-2 earnings), whereas in others, earnings from gig work, such as side jobs, freelance work, selling items of value, or temporary employment, were casualties of the pandemic.

“Blow into Our Finances”

The loss of earnings from gig work was described by roughly one-fifth of the subsample. Interviewees discussed experiences ranging from the loss of seasonal employment at an amusement park to the need to curtail babysitting “once COVID numbers started spiking up.” A chef discussed the opportunity to do private, in-home cooking demonstrations and the impact of the pandemic on this nascent entrepreneurial activity:

I do some stuff on the side here and there if people want — I had this one lady that [inaudible] but she wants me to do like a personal like a private cooking show for her, and her immediate friends and family. To where I would show up at her house with my equipment stuff like that, and actually just cook for them make something good for them let’s do a little dinner show. I can do stuff like that on the side I don’t get it very often like [inaudible] one of my first few that I’ve done, but I’ve never been able to get this one done yet, because it’s just this whole coronavirus thing threw me off. [age 18 to 34, below 100 percent, fall 2020]

For many of these interviewees, the loss of income from gig work was paired with—and compounded by—a reduction in earnings from their primary form of employment. In the words of one recent college graduate:

I did lose a lot of working hours. I worked 40 hours a week to maybe like 15 or 20. So I was still able to keep my job, which is great, and then I also made a lot of money selling [creative works] and when the pandemic hit, no one wanted to buy [creative works] because nobody wanted to spend extra money on something they couldn’t afford. And so that took a blow into our finances as well. [age 18 to 34, 100–199 percent, fall 2020]

“Got to Pay Bills”

Gig work was raised not only as a casualty of the pandemic but also as an important financial coping strategy. For some interviewees, it was difficult to discern whether these efforts predated the pandemic as part of an established system for making ends meet, but for most, they were clearly a direct response to the pandemic-related employment disruption. Illustrating a hybrid case, one stay-at-home mother of two suggested that while finding a side job to make ends meet was not atypical, “it’s been more frequently having to make ends meet with the COVID and everything” because a household member had their hours reduced at work. Among this group, very few references were made to jobs in the platform economy, such as food delivery or rideshare services (for an analysis of the app-based platform economy using AVP data, see Jackson 2024, this issue); instead, interviewees described more informal efforts to offer services for hire in the community. One interviewee described their daily routine as follows: “I wake up and I check my phone and emails and all that stuff to check for a job. … Hopefully, I have jobs. If I have jobs, then I plan my day according to them, but if there’s no work … then I got my own little room back here and I fill out job applications, play [video games], find something constructive to do” [age 35 to 54, 100–199 percent, fall 2020].

Other interviewees discussed selling goods rather than services. Examples included masks, digital content for video games, and making snacks distributed via both farmers markets and an online marketplace. Others discussed selling personal belongings for whatever cash they could generate after their hours were cut at their primary job:

I had to sell personal items that I didn’t want to sell, I had to sell things from my house that meant a lot to me, I had to sell other things that were worth a lot more money for less money just, because it’s like well I got to pay bills. … So we’ve lost a lot of things that we didn’t want to lose, but we’ve gotten through and we’ve come on the other end of it we’re starting to do better now due to my new job. [age 18 to 34, below 100 percent, fall 2020]

The Role of Pandemic Relief Programs

Shortly after the onset of the pandemic, an unprecedented number of federal, state, and local policies and programs were enacted to protect the U.S. economy and stabilize the labor market, particularly for vulnerable households. Because the AVP interview guide included direct questions about the receipt of UI benefits and stimulus payments (EIPs), and given the level of employment loss in our sample and widespread eligibility for EIPs, interviewees commonly discussed these programs in particular.8 In this section, we use the full sample of seventy-six households to explore interviewees’ use of these funds and views on program effectiveness.

“It Did Help a Lot”

Interviewees who elaborated on how UI benefits and EIPs were spent primarily discussed covering essential expenses. This included paying “the bills” (such as rent and utilities), and thus the funds helped offset some of the described financial hardships. A handful of interviewees suggested that these programs covered no more—and sometimes less—than their essential living expenses. One interviewee who was laid off from their job early in the pandemic put it plainly, stating “there’s nothing left over for anything” after using their unemployment check for basic needs. When asked how a temporary layoff affected their pay and benefits, a worker at a meat processing plant remarked, “They kind of affected it a lot. Meaning I had to make a lot of sacrifices, but at the same time, the unemployment did help. It did help a lot. If it wasn’t for that I don’t know how I probably would have made it through to be honest with you” [age 18 to 34, below 100 percent, fall 2020].

Rather than covering ongoing living expenses, a few interviewees allocated their EIPs, in particular, to large, unexpected spending shocks such as a veterinary bill, braces for their children, or compensation to another motorist for an automobile accident. Others discussed earmarking any surplus funds to cover future expenses. Households with earnings below 100 percent of the federal poverty guideline and households whose adults self-identified as Black were more likely than their counterparts to discuss using pandemic relief funds to cover essential living expenses. The latter observation may be explained by the fact that Black households in the sample had lower average earnings than households in the other race and ethnicity categories.

As might be expected in light of our focus on low-income households, only a handful in our sample suggested that they did not need the pandemic relief funds, spent them on discretionary items, or described a stronger household balance sheet as a result of their UI benefits or EIP receipt. One unemployed delivery worker mentioned how the “free money … helped us catch up on a lot of stuff” and expressed optimism that next year would be even better. This interviewee was the only one in our sample to make a clear connection between receipt of pandemic relief funds and labor force participation, stating that because “the government has given us free money, we don’t really have to work.”

Only one other interviewee even approximately suggested pandemic relief funds acted as a disincentive to work. After describing their partner’s ability to find informal work as being back and forth—consisting of anywhere between five and forty hours per week—the worker-student discussed the tension their partner felt between trying to earn income through gig work and maintaining their crucial, albeit unreliable, UI benefits:

Okay. So, like, when you’re on like unemployment, like if you make any additional money, like usually, like put that in, and so it comes off of what you get every week. So, like, when he gets his unemployment check, he just won’t work that week, just so we can keep that money coming in. Because when you do like too many weeks where you’re trying to pick up side jobs and claim unemployment, they’re like, cancel your claim. So, like, he’ll do like unemployment and then if like, they hold up his account for like identity verification for like a month, then he’ll like go and work for it’s like, it’s really inconsistent. Because I can’t even say, like he works as much a week, just because it’s not the same at all, every week is so different. But normally, he’ll be a full-time everyday worker. [age 18 to 34, below 100 percent, winter 2021]

Earlier in the interview, the same interviewee said “it’s like you’re not allowed to work” in reference to receiving their UI benefits.

“Unemployment Has Been a Nightmare”

Although relief programs were intended to ease the financial stress on vulnerable households brought on by the pandemic, challenges navigating the UI system in particular led to adverse outcomes for some interviewees and their household members. Interviewees described interacting with the UI system as the worst, stressful, and a battle. Criticisms of the system fell into four primary categories: being denied or failing to receive assistance, delays in benefit receipt, inconsistency of payments, and difficulties contacting program administrators. The first pertains to both UI benefits and EIPs; the last three were raised in connection with the UI system only.

Some interviewees felt they were unjustifiably denied benefits on applying, were deemed to be ineligible, or did not receive the assistance to which they felt entitled. The complexity of program eligibility renders it impossible to tell which denials were supported by fact and which were unjustified, but it is clear in the transcripts that some interviewees felt as if the programs were not administered equitably. For example, the construction worker explained that they had to take time off of work to supervise their children who were attending school virtually from home. Eventually, the worker was fired and later denied UI benefits: “So, I lost my job. … There wasn’t like kids going back to school, which meant I had to stay home with my kids. Which meant I had no … I lost my job because of it. But when I checked, when I tried to fill out unemployment, they said that wasn’t a reason” [age 18 to 34, below 100 percent, fall 2020].

Several interviewees also criticized the pandemic relief programs for the delays they experienced receiving benefits. For most, these objections were raised within the context of the described financial hardships, when relief funds were urgently needed. Administrative hiccups led to months of backpay in one case, and, in another, the post approval notification that a review specialist would need to get involved delayed the distribution of funds. A related but distinct concern with UI implementation was the inconsistent nature of payments even after they were approved. The former server described their frustration with interrupted or intermittent payments, as illustrated by these comments that also allude to delays that compounded the inconsistency: “So I started [serving] again, and I was making ends meet, and COVID hit, that took away the job, unemployment has been a nightmare, you can’t get it hardly, and if you do, they stop, they start it, they stop, they start it, there’s no, and it takes six months to even get it going, and then if it stops, takes another three to four months” [age 35 to 54, below 100 percent, spring 2021].

Finally, some interviewees found it difficult to get in contact with UI administrators when seeking more information about the program or their eligibility. As interviewees discussed this and other shortcomings in the UI system, feelings of stress and anxiety were shared, which serves as a testament to the criticality of funds for underresourced households. This passage from the worker-student encapsulates several of the broad categories of complaint highlighted in this section and illustrates how the program’s perceived flaws undermined both financial and mental well-being for those it was meant to serve:

I mean, I feel sick. Sometimes I get headaches just because of stress. And I mean that happens being a student and working but it’s all that stress of like, it’s serious like, I wonder like, “Okay, I have a bill due next month if I can’t pay it, what’s going to happen?” What am I going to have my lights on? Or am I gonna have my heat on what’s going to happen here? … And really, I mean, you get your unemployment so inconsistent when you call try to get help, no one answers. The lines are so busy. I mean, they add that extra $300 here in [state], no one’s seen it yet. I mean, it’s just, it’s stressful, and it’s stressful, and it’s negative. And day-to-day stuff right now it’s tough. [age 18 to 34, below 100 percent, winter 2021].

When delivered as expected, UI benefits and EIPs helped ameliorate the financial hardships that many households in our sample experienced during the COVID-19 pandemic and associated recession. Implementation and deployment challenges encountered by interviewees illustrate how the programs could also prove detrimental to both financial and mental well-being.

DISCUSSION

In this article, we present our analysis of transcripts from seventy-six in-depth interviews conducted with low-income households as part of the American Voices Project. We sought to learn whether and to what extent a large-scale qualitative data platform such as the AVP could contribute to public policy questions surrounding the federal response to the financial and employment disruptions brought about by the COVID-19 pandemic that were known to disproportionately affect low-income workers and households. Reflecting the direction of both quantitative research and active policy debates during this period, the research questions we used to guide our examination of the data set were: How did interviewees experiencing negative employment effects describe the role that safety net programs played in stabilizing household finances? And is there evidence that these programs affected the employment or job-search behaviors of beneficiaries? In this section, we begin by discussing our findings as they relate to our research questions. Shaped as they are by our experiences with the data, we end with our thoughts on how an immersive-interviewing platform such as the AVP could be a resource for monitoring labor market conditions and related policy responses.

We find that for many low-income households, the pandemic and recession led to a loss of employment that took many forms, from a slight reduction in hours to a permanent layoff. The depth and prevalence of related financial hardships described in the interviews challenge the broader notion of households on firm financial footing as a result of the pandemic relief programs. The experiences of many of the interviewees are more illustrative of prior quantitative studies highlighting some degree of household-level financial distress than of research suggesting a suppressed poverty rate or inflated checking account balances. Many of the interviewees who received pandemic relief funds described them as paramount to covering at least some essential living expenses, with fewer references to saving the proceeds or using the funds for discretionary expenses. Criticisms of the UI system, in particular, gave voice to the well-documented challenges to state offices facing unprecedented demand for their services.

We find little support for the position that expanded safety net programs acted as a disincentive to participating in the labor force. In our sample of thirty-seven interviewees with evidence of employment loss, in only one clear case did an interviewee describe UI benefits or EIPs in these terms. In only one other instance did an interviewee describe how UI rules and the irregular and inconsistent nature of benefit receipt affected their partner’s market decisions. An important caveat to our findings, however, is that the absence of evidence should not be confused with evidence of absence. Participants were not directly asked about how relief programs affected their employment decisions, so it is entirely possible that interviewees did not discuss “all aspects of their experiences” (GAO 2022, 57) during the semi-structured interview.

There is also reason to believe that both the study period and our sample selection criteria could have made it more likely that we would read transcripts describing financial distress rather than work disincentives. To leverage the rich responses to new questions added to the survey protocol in September 2020, we begin our study period in that month. Our sample therefore includes only interviews conducted after the expiration of the $600 UI supplement in July 2020, which may have ushered in a period of “material hardship for a multitude of UI recipients” (Cortes and Forsythe 2021, 25). Interviews conducted between spring and summer 2020 may have revealed a different level of financial distress or additional evidence of benefits affecting interviewees’ labor force participation. The same could be said for a study period that extended through the summer of 2021, when some states ended the $300 supplement early, but the last interviews available in the broader AVP database were conducted early that summer. Further, we intentionally constructed our sample to learn more about the experiences of the lowest-income households most likely to be affected by the pandemic-induced employment disruptions, but given their income levels, these same households were also most likely to face difficulty making ends meet generally. Even so, the AVP transcripts allowed us to burrow under the aggregate statistics and gave us a window into the financial stability of scores of low-income households during this period, and the view was not always as rosy as the top-line numbers would lead one to believe.

The interconnections between household financial stability and mental well-being highlight the opportunity for discovery that we view as an important strength of using qualitative data in spaces where quantitative analysis may be more customary. Consistent with pre-pandemic work illustrating unemployment’s negative implications for mental well-being (McKee-Ryan et al. 2005; Paul and Moser 2009; Singh and Siahpush 2016), research has found that households experiencing an income shock or employment loss during the pandemic were more likely than others to experience depression or anxiety (Donnelly and Farina 2021; Killgore et al. 2021; McDowell et al. 2021; Panchal et al. 2023; Parker, Igielnik, and Kochhar 2021; Singh, Lee, and Azuine 2021; Reading Turchioe et al. 2021; Guerin et al. 2021; Kelley et al. 2023). The connections between job loss or financial stress and reduced mental well-being have been shown to be strongest for low-income workers (Guerin et al. 2021; Prime, Wade, and Browne 2020). Regarding the association between UI receipt and mental well-being, our research appears to be aligned with recent work showing that UI benefits were effective in lessening the probability of anxiety and depressive symptoms for households receiving benefits (Berkowitz and Basu 2021; Donnelly and Farina 2021).9 In their coverage of the stress surrounding denied claims, breakdowns in communication, delayed payments, and the financial hardships that ensued, AVP interviews with disgruntled applicants testify to this association.

Further underscoring the exploratory value of using qualitative data, the importance and vulnerability of gig work during this period emerged as integral to some interviewees’ financial experiences. Research suggests that although overall fewer people participated in gig work in 2020 than in 2019 (FRB 2021), some who lost a job or had their hours reduced during the pandemic turned to gig work for income (Reynolds and Kincaid 2023; Accenture 2021), and gig activity was almost twice as common for those saying it is hard to get by than for those living comfortably (FRB 2022). Earnings from gig work were often considered essential or important in meeting basic needs (Anderson et al. 2021) and provided a financial buoy for Black and Latinx families, before and during the pandemic (Fields-White et al. 2020). In some instances, income from gig work was a substitute for those who did not apply for, did not receive, or could not wait for UI benefits (Ravenelle, Kowalski, and Janko 2021). Gig work was far from immune to the economic disruption caused by the pandemic, however, as demand shifted away from ride-sharing and other services that required physical contact and toward delivery services and online platforms for selling goods (FRB 2021; Accenture 2021; Liu 2020; Greig and Sullivan 2021). Putting a finer point on this disruption, nearly all of the dozens of contingent workers interviewed for a qualitative study reported losing employment due to decreased demand or restrictions on in-person services (GAO 2022). Our findings broadly support the literature’s depiction of gig work during the pandemic as both a fallback source of income and a source of potential risk in the face of shifting demand during a public health crisis (Greig and Sullivan 2021).

Overall, our analysis suggests that with some improvements, an ongoing effort to collect in-depth, nationally representative, qualitative data could provide critical information to inform sound policy development in the future. Although it is true that our findings are largely aligned with prior research and that we claim nothing as wholly novel, it is also true that we did not gain access to the transcripts until more than eighteen months after the earliest interviews in our sample were conducted, a period during which a robust body of research was published. The value of the AVP, then, lies in the potential for more timely access to a repository of information collected with an interview protocol that can be modified to respond to the moment. For example, with dedicated resources and a process for timely transcription, coding, and analysis, specific challenges surrounding UI receipt for affected workers, which were evident in our sample and likely present in transcripts preceding our study period, could have been quickly and clearly identified. To be sure, these issues were raised in the press (Murphy Marcos 2020) and richly described in later qualitative analyses (Ravenelle, Kowalski, and Janko 2021; GAO 2022), but a more rigorous or more streamlined examination may have been possible if a nationally representative sample of immersive-interview transcripts had been readily available as problems with UI receipt emerged. A vast array of quantitative data sets that were not available or widely used during the Great Recession—for example, data on checking account balances (Greig, Deadman, and Noel 2021), online job applications and postings (Marinescu, Skandalis, and Zhao 2021), small business payroll data (Finamor and Scott 2021), and mobility tracking data (Bartik et al. 2020)—were used to monitor the COVID-19 recession as it unfolded. Ongoing, systematic interviews could be a qualitative complement to these data sets, mirroring their timeliness but improving on their depth and richness.

For any future efforts to create a large-scale, immersive-interviewing data platform, we make the following suggestions aimed at either improving access to these data or deepening the content. Regarding the former, transcripts should be made accessible to researchers on a rolling basis soon after interview completion, and the data set should be made publicly available. Both steps would drastically improve the platform’s ability to inform policy-relevant research. Further, with safeguards in place to ensure the anonymity of participants, granting access to the general public would not only broaden its reach and expand its utility as a tool for evidence-based policy development (Chetty et al. 2020), but it would also improve transparency by allowing the results of future research to be replicated.

To deepen the content collected, we recommend developing several topic-specific interview modules—with a labor market module among them—to be delivered alongside a standard set of core questions. Doing so would allow for the elicitation of richer content without extending an already lengthy interview protocol. Next, to address what we recognized as missed opportunities in the transcripts, we recommend additional interviewer training on how to ask probing follow-up questions, a practice that might be more natural in a topically focused, modular interview. Finally, we propose a process that makes supplemental data collection possible, potentially through a short survey or a tailored interview protocol targeting a specific subsample of interviewees. The ability to explore a topic of interest in more depth would leverage the existing strengths of the AVP’s design and overcome the difficulties we sometimes encountered in trying to interpret interviewee remarks that lacked depth, clarity, or context. We acknowledge that this process would need to ensure continued participant anonymity, be limited in scope so as not to overburden those involved, and include additional compensation for interviewees, but such a feature would allow researchers to better use these data for more directed analyses.

CONCLUSION

In this article, we analyze the transcripts from seventy-six interviews conducted with low-income households between the fall of 2020 and the summer of 2021 as part of the American Voices Project. We conducted this analysis because we saw the potential for the AVP as a new source of rich information on labor market experiences and wanted to assess the AVP’s ability to realize this potential. We did so by exploring the revealed experiences of households that lost employment during the COVID-19 pandemic and that ostensibly benefited from an expanded social safety net. In the transcripts, we find evidence of job loss for roughly half of our sample, and that, among these households, financial distress was not uncommon and was sometimes described in terms of the stress and anxiety that often accompany it. Although vulnerable to disruption during the pandemic, gig work was raised by some interviewees as an important economic lifeline, as were UI benefits and EIPs; administrative challenges associated with the UI system proved an independent source of stress for some households. We find little evidence that UI benefits or EIPs played a role in the labor market decisions of interviewees or their household members.

Our primary goal with this analysis was to assess the utility of a large-scale, immersive-interviewing platform such as the American Voices Project as a supplement to traditional market data. In comparing our findings with the literature, our conclusion is that although the experiences of our sample add depth and richness to the available quantitative analyses and are a good reminder of the heterogeneity that lies beneath averages and aggregates, we cannot claim any findings as wholly novel. We interpret the alignment of our findings with the vast body of relevant research as a testament to the quality and value of the AVP data set. Similarly ambitious data collection efforts in the future would benefit from several modifications to both improve timely access to the data and deepen its topical coverage. Given our experiences with the data and assuming these improvements, we believe a platform such as the American Voices Project could represent a powerful complement to the growing suite of real-time quantitative data available to inform both public policy and public opinion.

FOOTNOTES

↵1. Authors’ analysis of data from BLS (n.d.-a, n.d.-b, n.d.-c).

↵3. Because AVP interviews were intended to capture the experiences of all household members, using household—rather than interviewee—characteristics is more appropriate for identifying group differences. We developed separate categories for households with adults of different races or ethnicities or falling into different age bins. We used the highest educational attainment of adult members to classify households by education, and we classified any household with an adult born outside the United States as an immigrant household.

↵4. We are interested in aspects of financial and mental well-being that interviewees directly associated with pandemic-related employment loss.

↵5. We use permanent layoff to describe a permanent separation from the employer and temporary layoff to describe a layoff from a job to which a worker expects to be recalled.

↵6. The information provided is purposefully limited to protect the identity of interviewees.

↵7. For more on housing insecurity as seen through the lens of AVP interviews, see Max Besbris and colleagues (2024, this issue).

↵8. In addition to these programs, a handful of interviewees also discussed enhanced Supplemental Nutrition Assistance Program (SNAP) benefits and rent and utility assistance.

↵9. Although the negative association between difficulties with UI receipt and mental well-being is evident in our sample of transcripts, those who are highly affected by stress have lower UI recipiency rates than those who are not (Forsythe and Yang 2021).

- © 2024 Russell Sage Foundation. Fee, Kyle, Sloane Kaiser, and Keith Wardrip. 2024. “Catching Up and Coping in the COVID Economy.” RSF: The Russell Sage Foundation Journal of the Social Sciences 10(4): 34–59. https://doi.org/10.7758/RSF.2024.10.4.02. We thank Dr. Rosemary Frasso at Thomas Jefferson University for her methodological guidance. The views expressed here are those of the authors and do not necessarily represent the views of the Federal Reserve Banks of Cleveland or Philadelphia or the Federal Reserve System. Direct correspondence to: Kyle Fee, at kyle.d.fee{at}clev.frb.org, 1455 East 6th Street, Cleveland, OH 44114, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.