Abstract

Since the end of the civil rights movement, the United States has not made meaningful progress toward closing the racial wealth gap. Without deliberate policy intervention, this gap will likely persist. Racial justice activists and policymakers, aiming in part to close this gap, have put forth various reparations programs. Others have proposed race-neutral wealth redistribution policies that also promise to address the gap, but as an indirect consequence of redistributing wealth in general. The potential impact of this second set of proposals on racial wealth inequality remains understudied. This article addresses this deficit through counterfactual historical simulation: By assessing the thirty-year impact of these race-neutral proposals, it finds significant reductions in the racial wealth gap over a generation. Yet these race-neutral programs have limitations vis-à-vis the broader goals of racial justice; this article concludes by emphasizing the unique capacities of reparations programs to address these limitations.

In 2014, Ta-Nehisi Coates published a fifteen-thousand-word essay in The Atlantic making the case for reparations. In the essay, he sought to move the discussion of reparations for Black Americans from something outside the Overton window to a serious policy proposal (Coates 2014). Since 2014, regardless of the unique contribution of Coates’s article, the discourse surrounding reparations for injustices committed against Black Americans has taken a prominent place in public and academic discourse.

During the 2020 Democratic presidential primary, for example, the vast majority of candidates pledged their support for a bill to create a commission to study reparations (Jamerson 2019). This bill, H.R. 40, draws its name from the unfulfilled Reconstruction-era promise of forty acres of land for the formerly enslaved. The late congressman John Conyers sponsored this legislation for nearly three decades before it garnered enough support to advance beyond the House Judiciary Committee in 2021 (Hodges, Brown, and Summers 2023). When it did, H.R. 40 had a record 215 congresspeople lending their support (Human Rights Watch 2022).

There are many ways to understand reparations and to characterize the social problem it seeks to address. Like H.R. 40, many cases for a reparations program identify a national reckoning with the history of oppression toward Black Americans as a first step (Coates 2014; Ogletree 2003; Robinson 2001). After recognition, however, and when it comes to redress, a wealth-centric conception of reparations is common. For example, General Sherman’s original 1865 promise to the formerly enslaved on the South Carolina coast—arguably one of the first reparations proposals—of forty acres and a mule was a land redistribution scheme and, therefore, a form of wealth redistribution (Sherman 2003, 325–27). A hundred years later, the Black Panthers’ Ten-Point Platform called for monetary reparations based on historical theft from Black Americans and Sherman’s unfulfilled promise (Newton 1995).

Many contemporary calls for reparations have focused on racial wealth inequality, particularly as measured by the racial wealth gap. For this contemporary camp, current-day racial wealth inequality represents racial injustices of today as well as the continuing legacy of past discrimination (Ogletree 2003) or, as Coates (2014, 23) puts it, the “multi-century plunder of black people in America.” In building his argument for reparations, for instance, Coates emphasizes the postwar exclusion of Black families from widespread homeownership afforded to White families as a particular instance of such discrimination. Exclusionary policies such as these have ripple effects on wealth accumulation over generations. Those who have centered the racial wealth gap in discussions of reparations argue that this gap expresses a whole lineage of discrimination.

However, even among reparations proposals that target racial wealth inequality, there exist important differences regarding what equality should look like and the form(s) restitution should take. For the 1966 Black Panthers’ reparations program, calls for monetary payments stemmed from the identification of a historical debt, but they were not intended to reduce racial wealth inequality through a direct transfer to Black individuals or families nor were they aimed at explicitly closing the racial wealth gap. Instead, as Robert Allen (1998, 3) summarizes, these payments “were to be used to fund a Southern land bank, independent media, training and organizing efforts, and educational initiatives.” In other words, these proposed funds were part of a more general strategy of Black empowerment.

In the decade after the Black Panthers’ proposal, the economist and director of the Black Economic Research Center, Robert Browne, argued for a reparations program consisting of a large transfer of wealth to the Black community (Browne 1971). Browne and colleagues made the case that even if ongoing racial discrimination and systemic oppression were to vanish, the legacy of past racial discrimination would intergenerationally continue in the form of wealth disparities. In 1998, Robert Allen, in crafting his own call for a targeted (or graduated) reparations scheme, argued that even though “struggles for civil rights are important … [they are] not sufficient. Transfers of capital resources into the African American community must also occur. Such transfers, to be most effective, must be class-based, aimed at benefitting first and foremost the black working class—those who have been most ravaged by the depredations of capitalism and who have benefitted least from … the civil rights era” (7).

This line of argument, which emphasizes racial wealth disparities as the central object of a reparations program, also animates this issue of RSF. The editors’ introduction, for instance, endorses Sandy Darity and Kirsten Mullen’s (2020) $15 trillion reparations program, a proposal designed to fully eliminate the racial wealth gap measured at the mean by distributing the difference between mean White and Black wealth—roughly $360,000 in 2019—to descendants of American slavery. This proposal is clearly more expansive, expensive, and ultimately bolder than the programs summarized earlier. In contrast, for instance, Allen’s (1998) proposals called for greater redistribution to poor Black Americans; the graduated design of this proposal would mean that the sheer scale of redistribution would be less than Darity and Mullen’s plan.

In the context of the current lively debate on reparations and the racial wealth gap, policymakers and scholars have also proposed that various universal tax and transfer policies, which are facially race-neutral, would also make steps toward closing the racial wealth gap. Examples include wealth taxation (Williamson 2020), reforms to capital gains taxation (Holtzblatt et al. 2023), income tax reform (Brown 2022), and baby bonds (Zewde 2020). This article extends this literature by simulating the long-term cumulative impact on the racial wealth gap of two prominent universal inheritance proposals financed by a steeply progressive wealth tax. The article demonstrates that these proposals—which would redistribute resources from predominantly White, affluent households to all children at birth—offer the potential to significantly reduce the racial wealth gap and, given adequate time and specific conditions, potentially even close it.

Moreover, this article further extends this literature by evaluating these universal proposals in light of the policy aims of reparations scholars, many of whom also call for closing the racial wealth gap, but importantly in the service of redressing historical injustice. Universal programs open up a rich set of questions for reparations scholars. Would universal proposals indeed eliminate racial wealth inequality? And if so, are equal wealth outcomes across race enough on their own, or should a reparations proposal do more? Who are the just recipients of reparations? And how does timing affect the integrity of social restitution? These questions have long roots in debates over reparations. They also touch on the relationship between policy design and processes of social trauma, grief, and healing in the wake of historical injustice.

This article concludes that the universal proposals studied, while substantially equalizing wealth across race, define the just recipients and time horizon needed for restitution differently than race-conscious reparations proposals, ultimately falling short of core policy aims of reparations, including social healing and atonement.

SIMULATED WEALTH REDISTRIBUTION PROGRAMS

Through counterfactual historical simulation, this article investigates the two chief race-neutral wealth redistribution proposals alive in political and academic discourse, models their generational effects, and evaluates the specifications necessary for these proposals to substantially reduce or even close the mean and median racial wealth gap. Both proposals are universal inheritance programs—both would endow all children with wealth at birth; but the two proposals differ in terms of their design. The first is a graduated program put forward by Darrick Hamilton and Sandy Darity (2010), termed baby bonds; it follows in the same tradition as Allen’s (1998) reparations proposal in that it would redistribute more to the children of poorer families, but of course unlike Allen’s reparations proposal, this program would apply to all U.S. resident children, regardless of race. The second is Thomas Piketty’s (2020) universal capital endowment; under this proposal, all young people would receive an equivalent and quite generous wealth transfer. This later program, bracketing its race-neutrality, is similar to Darity and Mullen’s (2020) reparations proposal in terms of its non-graduated design. The historical counterfactual simulation used, treats these proposals as financed by a revenue-neutral wealth tax on the top 1 percent of the household wealth distribution.1 Given that the top of the wealth distribution is overwhelmingly White, the wealth tax itself would reduce racial wealth stratification.2

Although the universal inheritance programs simulated in this article carefully build upon Hamilton and Darity’s (2010) and Piketty’s (2020) original proposals, particular characteristics of the policies simulated stray from their original design. This is done in order for the simulated programs to be equivalent along all dimensions other than their universal versus graduated design. The simulated programs contrast with their original proposals along the following axes: the sums distributed, the rate of return (RoR) that the wealth endowments garner, and the age at which children are granted the wealth transfer. For example, Piketty’s (2020) proposed capital endowment program would guarantee all twenty-five-year-olds a wealth transfer of roughly $125,000 financed by a highly progressive wealth tax; no particular RoR would be guaranteed on the wealth endowment. Hamilton and Darity (2010), in contrast, called for a progressively distributed, baby bonds program that would grant children at birth up to $50,000 and guarantee preadult recipients a 2 percent annual RoR.

The policies simulated share the following features: They are modeled as having begun in 1989. The last year for which the effects are analyzed is 2019. All children born in or after 1989 are provided a wealth endowment, such that in 1989 all children age one and younger are modeled to have received a wealth transfer. By 2019, all U.S. residents age thirty and younger would have received a wealth transfer under this counterfactual scenario.3 For the universal program, all eligible children receive the same transfer in 2019 dollars at birth. Under the graduated program, eligible children receive one of five transfers denominated in 2019 dollars as a function of their family’s net worth according to a schedule shared across all years.4

Simulated universal inheritance programs are financed by a revenue-neutral wealth tax on household net worth above the 99th wealth percentile threshold in each triennial Survey of Consumer Finances (SCF) year. The simulation dynamically incorporates the effects of the tax in previous years (that is, the stock of taxable wealth is reduced year-on-year according to the tax rate and threshold in prior years). Wealth tax thresholds are initially calculated in 1989, are last calculated in 2019, and are recalculated every three years between 1989 and 2019. Between triennial survey years (for example, 1990 and 1991), the wealth tax threshold is the same in real terms as the most recent previous survey year (for example, for 1990, the inflation-adjusted 1989 wealth tax threshold is used). Wealth tax thresholds are the same across all programs, although the wealth tax rates do vary as a function of the estimated annual aggregate cost of the transfer programs. The tax is modeled such that the wealth endowment and the returns from the endowment are fully excluded from the wealth tax. Like the decision to make the simulated programs equivalent along all dimensions other than their graduated and universal design, the wealth tax is modeled such that only the tax rate varies between simulations allowing the focus here to be on the relative impact of size and design of the transfer rather than on the design of the wealth tax program.

For each proposal type—the universal and graduated—a more and less generous version is simulated, for a total of four proposals: a universal program that guarantees an endowment at eighteen of $50,000; a universal program that guarantees an endowment at eighteen of $125,000; a graduated program that guarantees, depending on one’s family wealth at birth, an endowment at eighteen between $10,000 and $50,000; and a graduated program that guarantees, depending on one’s family wealth at birth, an endowment at eighteen between $25,000 and $125,000 (see table 1). Under the graduated versions of these programs, children born into a family with net worth in the lowest wealth quintile (as defined by 2019 quintiles) would be guaranteed the maximum value of the wealth transfer by eighteen—that is, $125,000 or $50,000. For each successive quintile of family net worth, the size of the endowment at eighteen would be reduced by one-fifth the monetary value of the maximum endowment.

Graduated Program Endowment at Eighteen by Family Net Worth at Birth

Rate of Return on the Capital Endowment

In Hamilton and Darity’s original 2010 baby bonds proposal, the federal government would guarantee a real annual RoR of 2 percent on the capital endowment from birth until age eighteen. This simulation, taking Hamilton and Darity as a starting point, assumes that the federal government would guarantee a real RoR of only slightly more, 3 percent, for endowment recipients from birth until age eighteen.5 It can be safely assumed that a guaranteed annual RoR may be slightly higher than 2 percent and remain revenue neutral (that is, the federal government would not subsidize the funds in order for them to reach a 3 percent RoR). Average real RoRs of a variety of investments were higher than 3 percent between 1989 and 2019—S&P 500 (9.27 percent), Baa corporate bonds (6.11 percent), and even ten-year treasury bonds (4.06 percent).6 In years when the market RoRs are greater than 3 percent, returns on investment would be greater than that needed to maintain a 3 percent RoR on the capital endowment; this extra capital would be used to insure against shortfalls in years when the real market RoR falls below 3 percent.

For the main simulation results, the capital endowment grows at a real 3 percent RoR for adults (when capital endowment recipients are older than eighteen and have autonomy over their capital account). To test the results’ sensitivity to this assumption, an alternative market-based RoR was modeled and the estimates under this specification are compared with the main results in appendix A; assuming a market-based RoR actually reduces the racial wealth gap to a greater extent than the fixed RoR in the baseline specification.

Both the baseline specification and the alternative market RoR specification treat the full endowment as growing at the specified RoR for all years. This effectively assumes that the principal and returns would be reinvested rather than consumed. Such an assumption is in line with the statutory requirements of many state-level baby bonds proposals and enacted state-level baby bonds programs that stipulate the endowment only be dedicated to wealth-generating purposes (Brown and Harvey 2022). Under the recently instituted Connecticut baby bonds program, for instance, recipients may only access these funds on turning eighteen; when the recipient is between eighteen and thirty, these funds may only be used for the following purposes: buying a home, starting or investing in a business, paying for education, and saving for retirement (Connecticut Office of the Treasurer 2023).

As with the Connecticut program, the oldest endowment recipient in this simulation is thirty, which is the age at which the Connecticut legislation no longer requires the endowment to be used for wealth-generating purposes. The results of this simulation can therefore be read as following the same requirements of the Connecticut program, that is, after thirty, the endowment does not need to be used for wealth-generating purposes. Alternatively, the simulation results do not need to be read as the consequence of requiring the endowment to be used for only wealth-generating purposes. Instead, these results may also be interpreted as an approximation of an upper bound. Any program that allows for the capital endowment and returns on the principal to be consumed rather than reinvested will likely tend to see the capital endowment accumulate at a slower pace and likely have a smaller effect on racial wealth inequality.

The baseline simulations explored in this article assume that endowments grow at the same rate for all recipients. However, if Black Americans tended to see lower annual average RoRs, this assumption would bias the simulated outcomes. For reasons related to existing lower levels of wealth ownership among Black families and other features of structural racism, Black Americans may, on average, be more likely to use the capital endowment to buttress economic shocks and may tend to see lower rates of capital accumulation (Shapiro, Meschede, and Osoro 2013; Bhutta et al. 2020). Relative to White Americans, for example, Black American endowment recipients may be more likely to use their endowment to pay for higher educational expenses in the absence of available family wealth (Addo, Houle, and Simon 2016). Investment in education may tend to be less wealth generating than investment in financial assets (at least before age thirty, the maximum age observed). With respect to noneducational investments, Black Americans may also see lower RoRs. For instance, although Black and White Americans saw highly similar mean returns on real estate from 2000 to 2019, during the Great Recession (2007–2010) Black homeowners saw sizably greater declines than their White counterparts (Aladangady and Forde 2021).

Due to these potential (and even likely) differential RoRs between Black and White endowment recipients, all simulated programs are tested for their sensitivity to equal RoRs. This analysis is conducted via depressing positive RoRs for Black recipients over eighteen by two-thirds and inflating negative RoRs by a factor of 1.33 for both the fixed and market-based RoR simulations. This analysis is explicated in appendix A. In short, though, lower returns for Black recipients tend to reduce the effects of these program on the racial wealth gap but only by a marginal extent; the key takeaways of the baseline analysis still hold when Black recipients garner lower RoRs than White recipients.

DATA AND METHODOLOGY

This article draws on data from the Federal Reserve’s SCF and the Panel Study of Income Dynamics (PSID).7 The SCF is the gold standard nationally representative surveys of U.S. household net worth. To protect the privacy of respondents, this stratified random sample employs a complex sample weighting scheme and excludes households in the Forbes 400—the wealthiest four hundred U.S. residents. To accurately capture wealth at the top of the wealth distribution, this article follows Emmanuel Saez and Gabriel Zucman (2019) in augmenting the SCF to include the Forbes 400.

In addition, this article follows Naomi Zewde’s (2020) example in using the PSID to simulate Hamilton and Darity’s (2010) baby bonds proposal. The PSID is an intergenerationally linked panel that allows for the simulated wealth endowments of children to be based on the net worth of their parents at birth. However, its design does not accurately capture the extraordinary skew of the wealth distribution. Therefore, the PSID cannot be reasonably used to simulate a wealth tax, particularly one that is applied solely to the top of the wealth distribution.

To simulate the revenue-neutral wealth tax and its effects, the SCF, augmented by the Forbes 400, is used exclusively. To simulate the transfer component of the graduated programs, the PSID is used; the results are scaled to match the SCF. For the universal programs, the SCF is used. The unit of observation for the PSID and SCF differ; the former uses the family and the latter the primary economic unit (PEU). The PEU is highly similar, but not completely identical to the concept of a family. However, the Federal Reserve typically refers to PEUs as families in its publications.8

The wealth concepts in the SCF and the PSID are approximately equivalent (Pfeffer et al. 2016); both surveys capture roughly the same assets and liabilities. Differences exist in the asset portfolios of respondents in the two surveys, but this is overwhelmingly the result of differences in survey questions and the fact that wealthier households are not as frequently surveyed by the PSID. Variation in asset composition between the surveys is not an issue for this analysis, given that the surveys’ overall wealth concepts are closely related. Last, net worth in both the PSID and the SCF+Forbes 400 is adjusted for inflation and is denominated in 2019 U.S. dollars.

The SCF and the PSID both collect information on race. The SCF has several race variables. This article uses the four-category race variable that is reported in the SCF Summary Extract. This variable contains information on the race of the reference person (or the spouse or partner) and takes on one of the following values: Hispanic, Black, White, or Other. Of course, many households are multiracial. The SCF does not allow for a rich evaluation of the incidence of such multiracial households. The PSID is similar to the SCF in that race information is collected for the reference person and the spouse. Future research should address multiracial households and how it affects measures of racial wealth inequality, but this important issue is outside the scope of this article (for more on the race and ethnicity in the SCF, see Bhutta et al. 2020).

Assignment of the Capital Endowment

The historical counterfactual simulation of these policies includes two components: a simulation of the universal inheritance programs and the wealth tax that would finance them. Each wealth tax and redistribution program is treated as having begun in 1989. The SCF is exclusively used to simulate the universal program and the wealth tax for both programs. The PSID—an intergenerational panel—is used to simulate the graduated program and the estimated results are scaled to match the SCF.9

For any year between 1989 and 2019, the maximum eligible age for transfer receipt (the age under which all U.S. residents are universal inheritance recipients) is simply a function of the current year, t, minus 1989 (that is, Max Aget = t – 1989). For those who are over the age of eighteen, the value of their capital endowment in year, t, is the value of the principal plus the compounded interest earned on the endowment in each year since they were eighteen. Given the structure of the SCF and the PSID, the value of the capital endowment is calculated at the household level. The cumulative value of the capital endowment, KE, for all members, i, of household, j, in each triennial survey year, t, is equal to the following:

In principle, the assignment of the capital endowment under the universal program is relatively straightforward. However, the SCF uses age categories, rather than a precise and continuous age variable such as the PSID, and these categories vary across survey periods. Appendix B outlines the process by which these coarse age categories were transformed to allow for a reasonably accurate assignment of the capital endowment.

Unlike the universal program, the endowment under the graduated programs is a function of the recipient’s family wealth at birth. The SCF, a cross-sectional survey, does not offer a way of ascertaining an individual’s family wealth when they were born; hence the PSID is used to simulate the graduated programs. Family net worth is available for PSID survey respondents in 1989, 1994, and biannually from 1999 to 2019. For children born in a year in which family net worth was not collected, the most recent previous year where net worth was collected is used. Following the schedule outlined in table 1, one of five endowments is assigned under the graduated programs.

As noted, unlike the SCF, the PSID does not capture the full distribution of household net worth. This is a large concern. In the absence of accounting for this downward bias in the PSID, differences in the simulated posttransfer wealth between the universal and the graduated program could be the result of either distinctive effects or disparities between the surveys. To correct for this, scaling factors are found for median and mean family net worth in each year for Black and White families. These scaling factors are the quotient of family net worth in the SCF over that in the PSID. For instance, after estimating posttransfer median Black wealth in the PSID, this result is scaled upward in each relevant year by the following term:

Dynamic Wealth Tax Simulation

To determine the distributional impacts of the revenue-neutral wealth tax in each year, t, between 1989 and 2019, the dynamic effect of the tax is modeled using the SCF such that the stock of taxable assets (assets owned by households above the wealth tax threshold) is successively reduced by the tax over each year. For each year, t, the wealth tax threshold is equal to the 99th percentile of the household net worth distribution in the triennial SCF survey year, t, or the most recent previous triennial survey year. Taxable wealth in each year, t, is defined as the sum of all household net worth greater than the tax threshold in that year for households with net worth above the tax threshold (that is, wj > tax threshold):

The wealth tax rate, τ, is equal to the rate that would be required to generate revenue equal to the annual cost of the universal inheritance program; meaning, it is recalculated for each year. For the universal program, the total program cost is the product of the number of children born in that year and the cost per child based on the present discounted value of the endowment at eighteen.10 This too holds for the graduated program, but the present discounted value of the endowment at eighteen varies depending on the family wealth of the child at birth. For all years, it is assumed that 30, 30, 20, 15, and 15 percent of all children are born into the first, second, third, fourth, and fifth quintiles, respectively. These figures are based on the number of children age one and younger by wealth quintiles per the SCF for the 1989 through 2001 triennial survey years. Across this twelve-year period, the relationship between the number of children born in each wealth quintile is relatively constant.11

In the program’s first year, 1989, the sum of taxable wealth is directly observed in the combined SCF and Forbes 400 data, allowing for the tax rate to be set trivially as follows:

In 1989, the wealth tax, τ, is applied to the sum of taxable wealth to simulate the sum of posttax taxable wealth in that same year.

Given that the SCF is triennial, the stock of taxable wealth in years between survey years (for example, 1990 and 1991) is found by annualizing the growth rate in aggregate net worth over the tax threshold between survey periods,  , and multiplying the simulated aggregate posttax wealth in the previous year by this annualized term.

, and multiplying the simulated aggregate posttax wealth in the previous year by this annualized term.

To simulate taxable wealth in 1990 (the first relevant year not covered by the SCF), aggregate simulated posttax wealth above the wealth tax threshold in 1989 is multiplied by annualizing the growth rate term, r {1989, 1991}. Posttax taxable wealth in 1990 (simulated wealth exceeding the 1990 tax threshold, accounting for the reduction in taxable assets due to the 1989 wealth tax) is calculated using the following equation:

For all subsequent years (1991 through 2019), simulated posttax taxable wealth is successively calculated as follows:

Therefore, simulated taxable wealth at time t + 1 incorporates the reduction in the stock of assets above the tax threshold in all prior relevant years, and the tax rate correspondingly adjusts upward to account for the reduction in the volume of taxable assets.

The calculations thus far have focused on aggregates. However, distributional analysis at the household level is necessary to analyze the effects of the wealth tax on racial wealth inequality. Consequently, incorporating these macro-level effects at the micro level (household level) is essential. This entails determining the share of observed household assets exceeding the wealth tax threshold that the simulation estimates would have been directly taxed away or eliminated via the dynamic effects of the tax. This share, denoted as ρ, is the quotient of the simulated aggregate posttax taxable wealth over the observed taxable wealth in SCF survey years. Such analysis is exclusively conducted for SCF triennial survey years since household-level analysis is only reliable for those years.12 For each household, j, their posttax simulated net worth is the product of their observed net worth in excess of the tax threshold (for 99 percent of households this will be zero) times ρt , plus their net worth below the tax threshold:

RESULTS

This section provides a summary of the simulated effects of the universal inheritance and wealth tax proposals. First, it outlines budgetary cost and key characteristics of the wealth tax, providing necessary context. Second, it presents an analysis of the impact of these programs on the mean and median racial wealth gap from 1989 to 2019. Lastly, a closer examination of their effects specifically for the year 2019 is conducted.

Estimated Budgetary Program Characteristics

Table 2 provides estimates of key characteristics of the four simulated programs across all simulated years. The more universal and the greater the maximum endowment, the greater the cost per newborn. Mean costs per newborn vary between $21,853 and $72,844.13 The cost per child is lower than the amount of the child’s endowment at age eighteen because the initial endowments at birth are treated as being kept in a federally insured investment vehicle that would guarantee a 3 percent real RoR until age eighteen. Due to this feature, the inflation-adjusted budgetary cost of the endowment at birth would amount to approximately 60 percent of the accrued benefit to the recipient at age eighteen.

Estimated Program Budgetary Characteristics, 1989–2019

Under the least expensive program (that is, the graduated program with a $50,000 maximum), the cost per child is equivalent to two years of Head Start, which the Congressional Budget Office estimates at $10,000 per child per year—or, alternatively equivalent to four years of a Pell Grant, which was around $5,135 per year in 2018 (CBO 2018). The cost per newborn for the most expensive program is roughly equivalent to nine years of Medicaid for a nonelderly and nondisabled person (CBO 2018).

Average annual outlays required for these proposals would range between $82 and $315 billion. The estimated annual program cost for the $50,000 graduated program is in line with the annual cost estimates of Naomi Zewde’s (2020) simulation of the baby bonds program, who estimates that a national baby bonds program would cost around $80 billion annually. In terms of existing federal outlays, the more modest version of the graduated programs is comparable to the $91 billion in federal spending for the Supplemental Nutrition Assistance Program and child nutrition programs in 2018 (U.S. Office of Management and Budget 2023). The more expensive proposal—the $125,000 version of the universal scheme—is comparable to one-fifth the cost of Medicare and Medicaid in 2018. In 2019, U.S. GDP was $21.38 trillion; the cost of the least and most expensive of these proposals range between 0.4 percent and 1 percent of 2019 GDP, respectively.

Additionally, all programs are financed by a revenue-neutral wealth tax. The effect of this wealth tax is incorporated into the overall effect of these programs on racial wealth inequality. The revenue generation from a relatively small wealth tax on the top 1 percent of the family wealth distribution is sufficient to fund all proposed programs. The size of this wealth tax varies, by policy proposal and year, between 0.5 percent and 5.5 percent of all wealth over the tax threshold. Tax thresholds vary across years given that the programs are simulated such that the tax threshold is equal to the top 1 percent threshold in each triennial SCF survey year. Depending on the year, the tax would apply to the first dollar of family net worth over $4.11 million to $11.13 million. The estimated tax rates and thresholds are comparable to the wealth tax programs proposed by Bernie Sanders and Elizabeth Warren during their 2020 presidential campaigns (Saez and Zucman 2019).

Reduction in the Racial Wealth Gap over Time

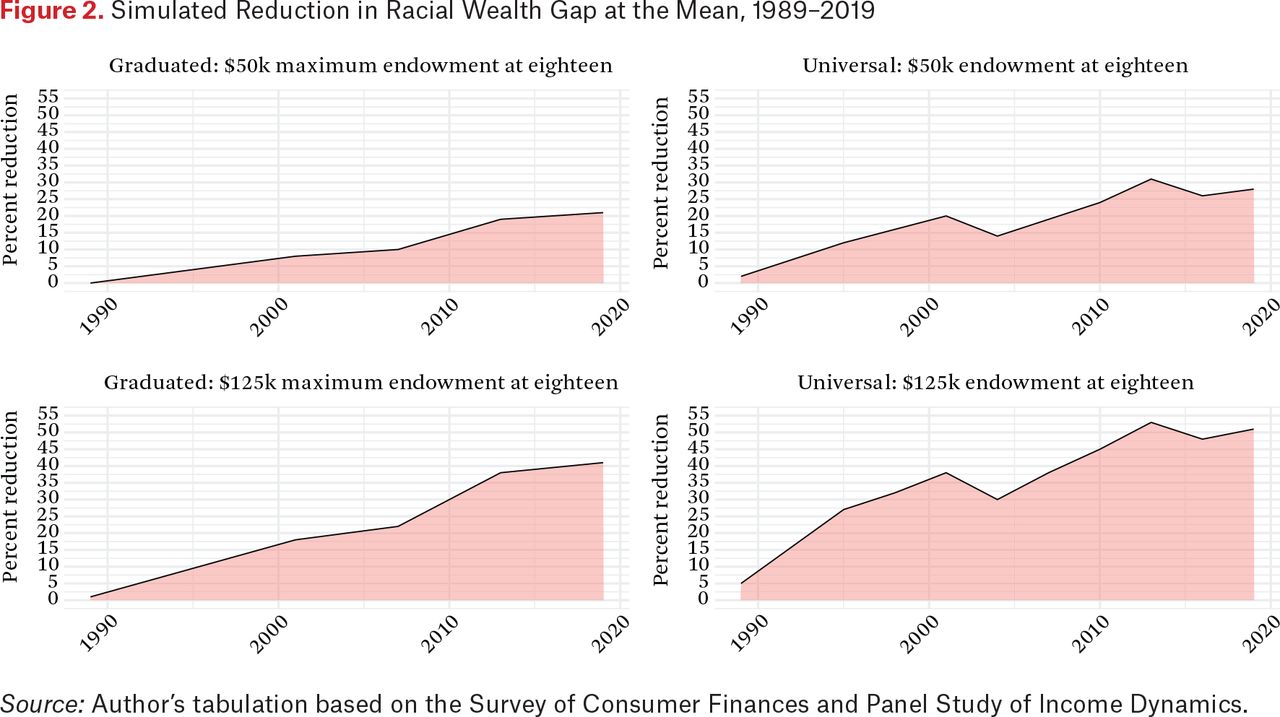

According to these simulations, over the course of a generation, all wealth redistribution programs analyzed would dramatically reduce the racial wealth gap, as measured at both the mean and the median. Figures 1 and 2 exhibit the percent change in the racial wealth gap at both the median and mean, respectively. Zero percent change would mean that none of the racial wealth gap would have been reduced; 100 percent would mean that the entire racial wealth gap would have been eliminated. The left two graphs in figures 1 and 2 display the results for the graduated programs;14 the right two graphs display the results for the universal programs.

Simulated Reduction in Racial Wealth Gap at the Median, 1989–2019

Source: Author’s tabulation based on the Survey of Consumer Finances and Panel Study of Income Dynamics.

Simulated Reduction in Racial Wealth Gap at the Mean, 1989–2019

Source: Author’s tabulation based on the Survey of Consumer Finances and Panel Study of Income Dynamics.

In the span of generation, had any one of these programs been in place, the median racial wealth gap would have been reduced by between 40 and 75 percent. The scale of this simulated effect is extraordinary. As would be expected, the less generous version of the graduated program has the most limited effect; however, limited is something of a misnomer. For later years, even this most modest program would nearly halve the median racial wealth gap.

The results at the mean are equally striking; the simulated programs would reduce the mean racial wealth gap by as much as 50 percent over the course of a generation. As the size of the endowment and the associated budgetary cost increases, the relative effect on the mean racial wealth gap increases more sharply than the median. The wealth tax is central to this difference. Wealth at the median is not impacted by the wealth tax, only the results at the mean are. As the cost of the programs increase so does the wealth tax rate and, thus, its effects on the racial wealth gap. Given the relative dearth of Black households in the top 1 percent, the incidence of the tax disproportionately falls on White households. Therefore, the greater the wealth tax, the greater the compound effect on the racial wealth gap over time. For example, the tax effect alone for the costliest program—the universal program that guarantees an endowment of $125,000—has an equivalent impact to the combined tax and transfer effects of the least costly program—the graduated $50,000 program. For all four simulated programs, the wealth tax effect accounts for roughly one-fourth of the reduction in the mean racial wealth gap. These results stand in quite sharp contrast to the dominant intuition summarized by Fabian Pfeffer and Robert Schoeni (2016, 16): “Emerging evidence suggests that taxation of wealth … may have limited redistributive effects.” Instead, over the course of a generation, the wealth taxes simulated could independently reduce the racial wealth gap by as much 15 or 20 percent.

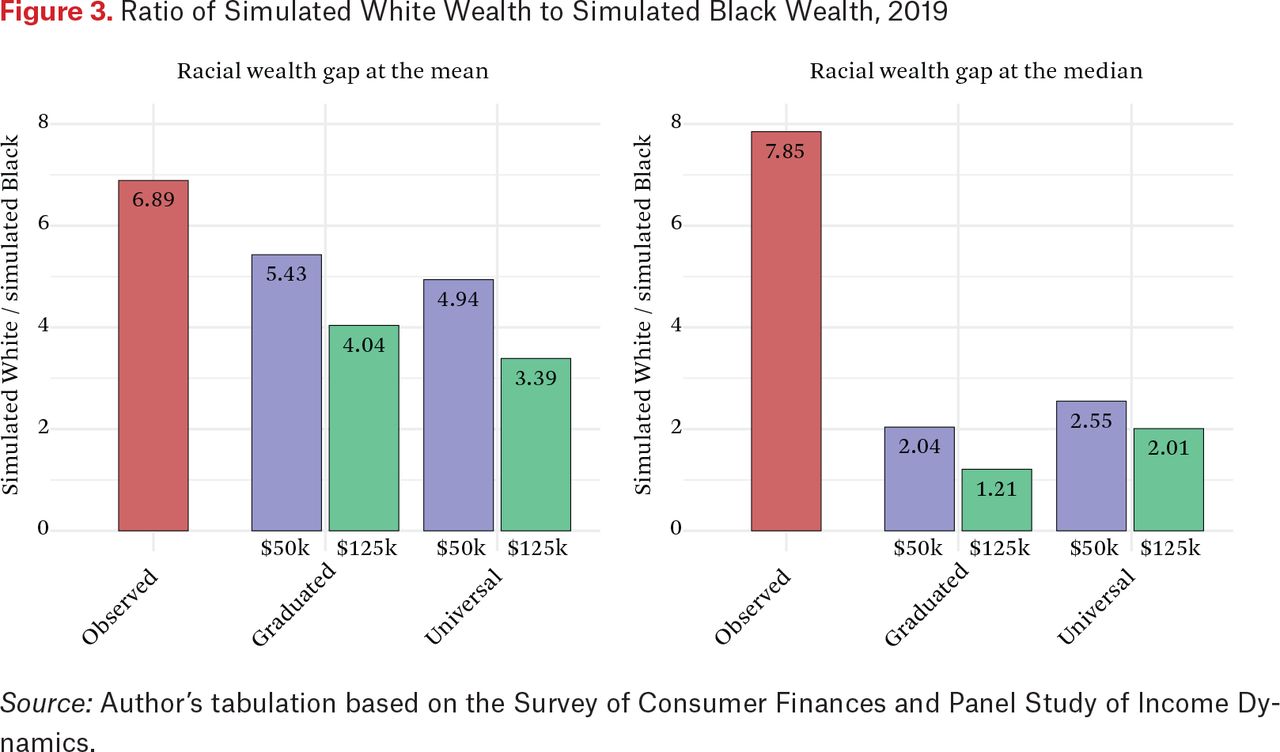

Effects on the Racial Wealth Gap in 2019

Figures 3 and 4 zoom in on the simulated racial wealth gap in 2019 under all four programs. Like figures 1 and 2, figure 3 displays the racial wealth gap in terms of simulated White posttax and transfer wealth to Black posttax and transfer wealth (at both the mean and the median). For reference, the observed racial wealth gap in 2019 is provided at the far left of each bar graph. The closer the ratio is to 1, the closer the results approximate racial wealth equality.

Ratio of Simulated White Wealth to Simulated Black Wealth, 2019

Source: Author’s tabulation based on the Survey of Consumer Finances and Panel Study of Income Dynamics.

Ratio of Observed White Wealth to Simulated Black Wealth, 2019

Source: Author’s tabulation based on Survey of Consumer Finances and Panel Study of Income Dynamics.

The simulated proposal capable of the deepest reductions in the mean racial wealth gap is the costliest: the universal program. But the program with the sharpest reductions in the gap at the median by 2019 is in fact a less costly program: the graduated version of the $125,000 program. As established, the more dramatic results at the mean are due to the tax effect. At the median, where tax effects are absent, the $125,000 graduated program—a program with a budgetary cost of roughly two-thirds of the equivalent universal—would actually have a greater effect.

Turning to figure 4, the ratio of observed White wealth to posttax and transfer Black wealth, the established relationship continues: at the median, graduated programs have a greater effect on racial wealth inequality than universal programs, whereas at the mean we see the opposite effect. When looking at the simulated results from this perspective, an important finding is uncovered: after thirty years, both the graduated and universal $125,000 programs would reduce racial wealth inequality by such a margin that simulated median Black wealth is estimated to be equivalent to median White wealth observed in 2019.

DISCUSSION AND CONCLUSION

In the span of thirty years, a race-neutral universal inheritance program financed by a highly progressive wealth tax would substantially reduce the mean racial wealth gap and, under certain conditions, even eliminate the median racial wealth gap. From these results, answers can be offered (albeit tentative and partial) to the exploratory question posed at the beginning of this article and highly relevant to this issue of RSF: Are these race-neutral wealth redistribution schemes capable of adequately contending with the racial wealth gap and, depending on the answer to this question, what are the unique advantages (both economic and noneconomic) of a strict reparations program?

To answer these animating questions, the following points are discussed and evaluated. First, a summary is provided of the potential and shortcomings these wealth redistribution proposals may have for achieving racial wealth equality; their simulated outcomes are contextualized in question of whether closing the racial wealth gap at median is a sufficient goal or whether closing the gap at the mean is a more complete measure of racial wealth equality (particularly per the precepts animating the discourse over reparations). Next, the question is posed: Who pays for this wealth transfer? Overwhelmingly, wealthy White households do; this result is evaluated in terms of the normative principles of reparations. Then, the promises and shortfalls of designing a reparations program in the mold of the programs simulated here are considered; as part of this, the economic advantages of a strict reparations program for achieving racial wealth equality are discussed. This section concludes by discussing the ways—particularly noneconomic ways—in which these race-neutral proposals are incapable of achieving certain objectives of strict reparations programs, but also the ways in which these race-neutral proposals may open doors for imagining what reparations can look like.

Promises and Limitations for Achieving Racial Wealth Equality

Racial wealth inequality is shockingly persistent. Ellora Derenoncourt and her colleagues (2022) show that it has been stagnant since the end of the civil rights movement. How can this persistence desist? This article finds that one answer may be in a universal inheritance program financed by a wealth tax. As established, all four programs simulated would dramatically reduce racial wealth inequality within thirty years. However, differences between the programs are important. It is clear that the larger the size of the endowment (the larger the transfer payment), the greater the tendency toward racial equality. This is true for both universal and graduated programs as well as for both the racial wealth gap measured at the mean and the median.

Although this article unsurprisingly establishes the greater the endowment, the greater the effect, it does not provide an unambiguous answer as to whether a graduated or a universal program would be better at reducing racial wealth inequality. The universal program would be unambiguously more effective at reducing the mean racial wealth gap (figure 3); this is largely due to the mean capturing the effect of the wealth tax and the greater the program costs, the greater the tax burden. Over a generation, the simulated wealth taxes independently reduce the mean racial wealth gap by as much 20 percent. At the median by 2019, however, the graduated program would be even more effective (figure 3); however, this greater effectiveness comes at the cost of time. It would take thirty years for the graduated program to become more effective than the universal and substantial reductions would be immediate from the universal program. Weighing these pros and cons is outside the scope of this article. These differences, however, raise complicated normative and distributional questions. Future research should look into the effects of such proposals on other distributional dimensions beyond the racial wealth gap (for example, asset poverty, the share of families with negative net worth).

Although these proposals promise to dramatically reduce racial wealth inequality, they would not do so instantaneously (particularly in the case of the graduated proposals). If the simulations were to continue into the future, the effects would continue to compound and, conceivably, all proposals would tend to close the median racial wealth gap and, for some, the gap at the mean as well. However, this time horizon may be too sluggish. And, if the ultimate measure of racial wealth equality is White-Black parity at the mean, these programs’ pace may be of particular concerns. This, for instance, is the opinion of the editors of this issue, who write in the introduction that these “simulations demonstrate that race-neutral baby bonds cannot close the mean racial wealth gap over a reasonable time scale. They can, however, virtually close the median racial wealth gap” (Darity et al. 2024).

William Darity and Kirsten Mullen (2020) view the elimination of the mean racial wealth gap as a crucial normative objective, representing the culmination of cumulative intergenerational discrimination and oppression. Achieving closure at the mean within a single generation would require a distinct proposal. Alternatively, from perspectives such as those advocated in Robert Allen’s (1998) reparations program, which prioritize the economic empowerment of the most disadvantaged Black families, targeting the eradication of the median racial wealth gap might be considered a more fitting aim. Universal inheritance proposals could potentially contribute to this objective.

Who Would Pay for Wealth Redistribution?

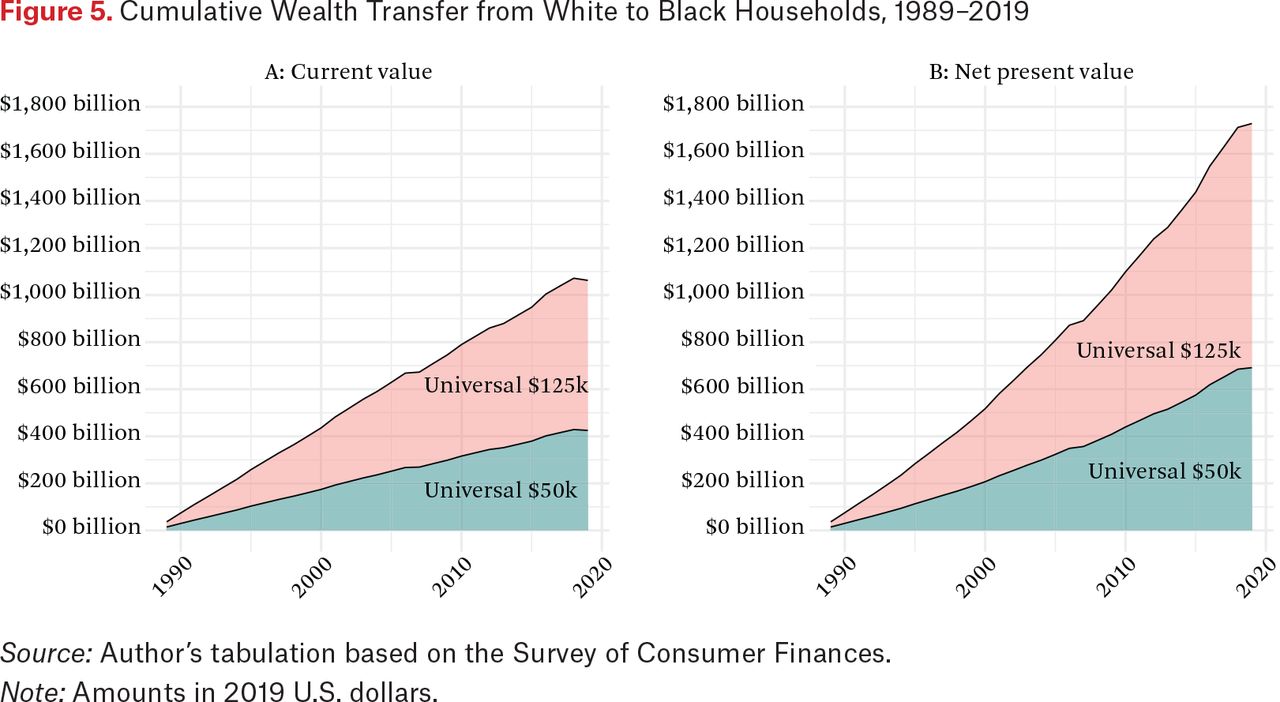

Like many reparations proposals, the programs simulated are fully federally financed by a revenue-neutral wealth tax on the top 1 percent. This tax reduces the wealth holdings of White families to such a greater degree than Black families that the financing itself mechanically reduces racial wealth inequality. For any year considered (1989–2019), more than 85 percent of assets above the simulated wealth tax threshold were held by White families; less than 1 percent were held by Black families. Figure 5 shows the cumulative transfer of wealth from White to Black households for the two universal programs simulated under both the current value and the net present discounted value (at a 3 percent discount rate). The cumulative transfer over thirty years ranges from $400 billion to a whopping $1.8 trillion. These ostensibly race-neutral taxes fall disproportionately on White households and redistribute wealth from White to Black families. Arguably much of this wealth was intergenerationally accumulated and often accumulated at the expense of Black families.

Cumulative Wealth Transfer from White to Black Households, 1989–2019

Source: Author’s tabulation based on the Survey of Consumer Finances.

Note: Amounts in 2019 U.S. dollars.

Can these Programs Serve as a Model for Reparations?

Thus far, this article has explored whether these proposals may achieve comparable ends to those of wealth-focused reparations programs. Now, consider in what ways the organizational form of these proposals may serve as a model for strict reparations proposals (that is, non-race-neutral versions of the proposals considered).

The clearest answer to this question is the financing mechanism. A wealth tax on the top 1 percent would effectively transfer resources (largely, intergenerationally accumulated) from wealthy White households to Black households. For the highest tax rate simulated, the cumulative thirty-year net present discounted value of the wealth tax revenue would approach the budgetary cost of Darity and Mullen’s (2020) reparations proposal.

On the other hand, a shortfall of the proposals explored in this article is that, by design, only children and future generations benefit directly. Of course, families transfer resources between members, such that all family members may benefit indirectly. Regardless, though, a reparations program designed as a transfer at birth would not directly serve as redress for most living Black Americans and living ancestors of American slavery. If these important normative considerations could be bracketed, though, a transfer at birth has two important benefits: first, costs are spread, abrogating significant macroeconomic (inflationary) concerns, and, second, successive future generations of Black Americans or descendants of slaves would be guaranteed recipients of a wealth transfer.

An inheritance design is in line with Roy Brooks’s (2004) atonement model of reparations. Under this proposal, an atonement trust fund would be established for all Black children born for a certain period after the reparation program is enacted; Brooks suggested twenty-five years. The fund would transfer resources to these newborns. The results of this article show that such a time-limited fund may have strong effects depending on its design and the transfer allocated, but it would likely not bring forth full racial wealth equality; for this, more time would be needed. Additionally, as the editors remark in their introduction, a time-limited program would affect few Black Americans; a wealth inheritance entitlement that would continue in perpetuity would fall short of targeting adults, yet still would guarantee redress for future generations.

The Limits of Race-Neutral Programs and the Unique Capacities of Reparations

When asked what reparations should look like, Ta-Nehisi Coates remarked on what he saw as two keys aspects: documentation of the crimes committed to Black Americans—“You need the official imprimatur of the state: they say this actually happened”—and linking reparations to “specific acts” (New Yorker 2019). Coates’s comments point toward a tendency for reparations proposals to consist of both a case for redress and atonement, and the actual compensation that emanates from this.

In line with this tendency for reparations proposals to ask for both an account of past harms and material redress, Brooks’s (2004) reparations proposal calls for financial redress to Black Americans at birth, a formal apology, and a museum of slavery. Like Brooks, Kathryn Edwards and her coauthors (2024) argue that atonement for historical crimes and injustices are key features needed for a true reparations program. For Edwards and her colleagues, this atonement process ought to be ongoing and led by the victimized community. Echoing these positions, Coates argues, “Reparations—by which I mean the full acceptance of our collective biography and its consequences—is the price we must pay to see ourselves squarely” (New Yorker 2019).

The race-neutral programs considered here do not have the capacity to address historical crimes and certainly are not able to speak to atonement; this limitation points to one of the ways a race-neutral program cannot replace full reparations, no matter how transformative their consequences. However, if these race-neutral wealth redistribution proposals were in place and the forms of racial wealth inequality these programs could deal with were being addressed, would this open a door for forms of redress that could only be offered by a strict reparations program? And connected to this question, what alternative ways are on offer to “see ourselves squarely,” to quote Coates?

As explored at beginning of this article, not all calls for reparations have centered or even included the leveling of the wealth divide. In 1973, Yale Law professor Boris Bittker, for instance, argued in The Case for Black Reparations for a program to close the Black-White income gap. Randall Robinson, in his book The Debt: What America Owes to Blacks, argued for a reparations program that would create a need-based educational scholarship trust fund for Black Americans. Elizabeth Wrigley-Field (2024) makes a case for a health-based reparations program sourced in the shocking gap in Black-White life expectancy.

If race-neutral proposals were able to accomplish the individual redistributive goals of many reparations programs, namely, closing the racial wealth gap, would space open for alternative forms of redress? Such forms could include a health-based reparations program à la Wrigley-Field (2024), state and local reparations programs—many of which are reviewed in this issue—or other collective and institutional empowerment projects. Such a collective empowerment version of reparations was core to the Black Panthers’ 1966 reparations program, for instance. For them, financial reparations were sought as part of a general program of Black empowerment.

In sum, the revenue-neutral programs simulated here are not reparations; they are not capable of tackling many of the core issues raised in the debate over Black reparations in America. But, of course, these proposals are not designed for this. These proposals do have the capacity to strongly contend with racial wealth inequality, despite their shortcomings, which have been reviewed in this section. The shortcomings of these proposals point to where a strict reparations program can only offer answers; but the promise these proposals have for tackling racial wealth inequality may open doors for alternative versions and conceptions of reparations, many of which are discussed elsewhere in this issue.

APPENDIX A. SENSITIVITY ANALYSIS OF ESTIMATES TO VARYING RATES OF RETURN

The baseline estimates assume that the endowment grows at 3 percent per annum in real terms. This assumption, however, may bias estimates on two grounds.

First, the baseline estimates use a fixed RoR rather than a market RoR. To test the sensitivity of the baseline estimates to this assumption, an alternative market-based RoR is applied when the recipients are over eighteen. 15 Table A.1 shows that the use of a market-based RoR versus a fixed RoR of 3 percent has little effect. The estimated reduction in the racial wealth gap at the mean and the median is actually greater when assuming a market-based RoR versus a fixed 3 percent RoR.

Sensitivity of Estimated Reduction in Racial Wealth to Assumed Rate of Return on Endowments (2019 Simulated Results)

Second, the baseline estimates treat Black and White recipients as garnering the same RoR. To test the sensitivity of assuming equal RoRs for both Black and White recipients (termed homogenous RoR in table A.1), additional simulations are run that assume the RoR in adulthood for Black recipients is two-thirds that of White recipients (and one-third greater in absolute terms when market RoRs are negative). Under this assumption (termed heterogenous RoR in table A.1), estimated reductions in the racial wealth gap tend to be smaller; but, relative to the baseline estimates, the effects are minor and do not change the results and their implications in any meaningful ways.

APPENDIX B. TREATMENT OF AGES IN THE SCF ACROSS SURVEY PERIODS

The SCF Public Use File (PUF) includes household member ages for all survey years, with families (PEUs) capped at twelve members. However, the coding of children’s ages varies inconsistently over time. In 1989, ages are rounded to the nearest five years for most family members, except for one- and two-year-olds, and the reference person and spouse. From 1992 to 2001, ages are not rounded, except for children under one year, who are assigned a value of –1. In 1992 and 1998, a few children are assigned –1. To standardize, these children are coded as age 1.

From 2003 to 2019, the ages of the reference person and spouse remain as reported. For other family members, ages are grouped nonlinearly: up to age 3 is coded as 3, 4–6 as 6, 7–12 as 12, 13–17 as 17, 18–25 as 25, 26–30 as 30, and incrementally by five years thereafter, with the maximum age capped at ninety-five for all years. For all coarse age groups, the capital endowment is multiplied by the midpoint of the age range. In the 1989 SCF PUF, few children have ages less than one. It appears that most children under one were recorded as one year old. Thus, ages equal to one are adjusted to half. For rounded age values, the midpoint of the category is used to calculate the capital endowment. For instance, children listed as age three in the survey years 2004 through 2019 could be under one, two, or three years old. The median value for this age group is two. Given minimal variation in aggregate births between neighboring years, this method is unlikely to significantly skew the simulation outcomes.

For survey years with age categories that don’t encompass all members eligible for a capital endowment, a reduced capital endowment is still allocated to all individuals. This reduced value is calculated by dividing the number of eligible ages in the category by the total number of ages. For example, in 2004, the maximum eligible age for a capital endowment is fifteen. Young adults aged thirteen to seventeen are grouped and assigned an age of seventeen. So, three-fifths of this group (ages thirteen, fourteen, and fifteen) are eligible for the endowment, while sixteen and seventeen are not. Each individual in this cohort is assigned the median eligible age (fourteen). The present discounted value of the capital endowment for a fourteen-year-old in 2004 is calculated and assigned to all observations in this age category, but it’s multiplied by three-fifths to adjust for the ineligible fraction. A mixture of eligible and non-eligible ages occur in five age categories for the survey years 2004 through 2016: (1) thirteen through seventeen in 2004, (2) eighteen through twenty-five in 2007, (3) eighteen through twenty-five in 2010, (4) eighteen through twenty-five in 2013, and (5) twenty-six through thirty in 2016.

After obtaining the fraction of ages eligible for the capital endowment in each survey year, the capital endowment, KE, for each individual, i, is estimated and multiplied by this eligible age term:

This procedure allows for the reasonable assignment of the capital endowment even when only coarse age categories are available.

FOOTNOTES

↵1. The wealth distribution is defined as the pretax (observed) distribution of household net worth as measured by the Survey of Consumer Finances (SCF) combined with the Forbes 400.

↵2. A progressive wealth tax, on its own, would engender greater racial wealth equality per certain metrics (such as the ratio of Black to White mean household net worth), but not for other important metrics (such as the racial wealth gap measured at the median).

↵3. Under this modeling strategy, U.S. residents who immigrated in adulthood would be assigned a wealth transfer. Neither policy proposal speaks at length about the relationship between the wealth transfer, citizenship, and immigration. However, given that the Black–non-Hispanic White household net worth ratio (the racial wealth gap) is the focus of this article, including or excluding immigrants and non-citizens would not meaningfully change this article’s key findings.

↵4. All monetary values in this article are denominated in 2019 U.S. dollars. Graduated programs could be organized such that the transfer schedule is calibrated to wealth thresholds in each survey year. For comparability across years, however, this modeling strategy was not used. By following a schedule set in terms of constant real 2019 dollars, rather than wealth quintile thresholds, the changing distribution of wealth over time has less of a relationship to the size of the wealth transfer program. Organizing the graduated program as such better facilitates comparison between simulated programs.

↵5. Eligible children at birth are given an initial endowment equal to what would ultimately accrue to the stipulated value at age eighteen under a 3 percent RoR—for example, $72,843 for the $125,000 endowment and $29,137 for the $50,000 endowment under the universal design or some value less than equal to this under the graduated design.

↵6. See Aswath Damodaran, “Historical Returns: Stocks, Bonds & T. Bills with Premiums,” New York University, 2024 (https://www.stern.nyu.edu/~adamodar/pc/datasets/histretSP.xls).

↵7. This article combines the SCF Public Use File (PUF) and Summary Extract Public Data (SCF Extract) to acquire select variables from both versions of the SCF. The SCF PUF contains most original variables from the survey, excluding those the Federal Reserve has deemed capable of identifying survey respondents. The SCF Extract contains a subset of survey variables included in the SCF PUF as well as variables constructed by the Federal Reserve, including household net worth. In lieu of reconstructing the Federal Reserve’s net worth measure, the SCF Extract, which includes net worth but not the age of all household members, is combined with the SCF PUF, which contains the ages of all household members but not their net worth. For each household, there are five replicates, each of which have different survey weights. Each household has a unique ID, as does each replicate. By merging on survey year, IDs, and survey weights, each observation in both versions of the SCF is matched.

↵8. The SCF 2016 codebook defines a PEU as consisting “of an economically dominant single individual or couple (married or living as partners) in a household and all other individuals in the household who are financially interdependent with that individual or couple.” Definitionally the PEU and the family are highly similar; however, due to the panel structure of the PSID, the units may differ slightly when members of a sampling unit break off from their family and form their own family.

↵9. Due to data limitations, Forbes 400 households are not assigned an endowment. Although the proposals do not exclude them from receiving an endowment, simulating it is not possible because Forbes does not provide sufficient information on household structure, including number of children. The effect of this is negligible.

↵10. Statistics on the number of children born are drawn from the United Nation’s World Population Prospects (2022).

↵11. The SCF is used instead of the PSID because the PSID is not fully representative of the wealth distribution; the number of children born in each wealth quintile may be biased toward the middle quintiles if the PSID were used.

↵12. For the simulations of the graduated programs, the PSID is used to calculate the transfer effects while the SCF is used to simulate the wealth tax effects. Mean wealth tax effects by race derived from this SCF based procedure are merely added to the PSID based estimated transfer effects to simulate the combined tax and transfer effect by race.

↵13. The range of average costs per newborn do not vary across years for either the graduated or universal programs. Consistency across years for the graduated program is a mere feature of the SCF’s data limitations (where only several years have information on newborns); in a real implementation scenario, the graduated programs would see marginal fluctuations across years in terms of the program cost per child.

↵14. For the graduated programs, results are provided for the following years: 1989, 2001, 2007, 2013, and 2019. Only this subset of years is analyzed because these are the only years in which the PSID and the SCF overlap.

↵15. The market RoR used is the real annual average RoR of defined contribution pension plans as reported on form 5500 and compiled by the U.S. Department of Labor. Defined contribution pension plans are an appropriate analogue for how capital endowments would be invested in the market; defined contribution plans are invested in a variety of financial assets, they typically allow for the plan owner to select different levels of risk (adding variability for risk preference), their returns reflect market conditions, and they are organized similarly to a child development account—a precursor to current baby bonds proposals (Sherraden 1991) and a potential model for large-scale wealth redistribution (see Shanks et al. 2024, this issue). These rates of returns are reported by the Department of Labor in table E20 in the publication “Private Pension Plan Bulletin Historical Tables and Graphs.”

- © 2024 Russell Sage Foundation. Dvir-Djerassi, Asher. 2024. “Closing the Racial Wealth Gap: A Counterfactual Historical Simulation of Universal Inheritance.” RSF: The Russell Sage Foundation Journal of the Social Sciences 10(3): 70–91. https://doi.org/10.7758/RSF.2024.10.3.04. This research was conducted with support from the Stone Center for Inequality Dynamics and a Eunice Kennedy Shriver National Institute of Child Health and Human Development training grant to the Population Studies Center at the University of Michigan (T32HD007339). The author thanks Davis Daumler for invaluable assistance with the Panel Study of Income Dynamics. The content is solely the responsibility of the author and does not necessarily represent the official views of the National Institutes of Health. Direct correspondence to: Asher Dvir-Djerassi, at asherd{at}umich.edu, Department of Sociology, University of Michigan, LSA Building, 500 South State Street, Ann Arbor, MI 48109-1382, United States.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.