Abstract

Using data from the 2008 and 2010 waves of the Health and Retirement Study to analyze the determinants of material hardship among individuals ages sixty-five and older, I look at five self-reported hardships: food insecurity, skipped meals, medication cutbacks, difficulty paying bills, and dissatisfaction with one's financial situation. One-fifth of the elderly report one or more of these hardships. Although hardship is more likely for those with low incomes, most older Americans experiencing hardship are not poor. I analyze whether alternative measures of resources do a better job of predicting hardship than does income relative to the federal poverty threshold. I find that spending relative to the poverty threshold does a worse job predicting hardship than does income relative to poverty. Subtracting out-of-pocket medical spending from income yields a measure that is an even better predictor of hardship. In multivariate models, I find that self-reported health, activity limitations, and disability are significant predictors of hardship. Having reliable children (as assessed by the respondent) or an able-bodied spouse reduces the likelihood of hardship. Poor health increases hardship through three channels: by lowering income, by increasing out-of-pocket medical spending, and through its direct effect on hardship. The first two of these—lower income and higher medical spending—are much less quantitatively important than the third; in a nutshell, poor health makes it harder to get by with less.

Social Security has enjoyed great success at reducing poverty and promoting independence among the elderly (Engelhardt, Gruber, and Perry 2005; Engelhardt and Gruber 2006). Indeed, the poverty rate among individuals age sixty-five or older was estimated at 9.5 percent in 2013, far lower than for children (19.9 percent) or for working-age adults (13.6 percent) (DeNavas-Walt and Proctor 2014). Poverty is an incomplete measure of material well-being, however, and is not synonymous with material hardship. A number of recent studies have analyzed hardship in the non-elderly population, particularly among single-mother families and former welfare recipients (Danziger et al. 2000; Iceland and Bauman 2007; Mayer and Jencks 1989; Meyer and Sullivan 2003; Rector, Johnson, and Youssef 1999; She and Livermore 2007; Sullivan, Turner, and Danziger 2008). Much less work has analyzed hardship among the elderly, perhaps because of their lower rates of official poverty.

The distinction between poverty and material hardship may be even more important for the elderly than it is for the non-elderly. Aging-related declines in physical and cognitive ability may visit material hardship even on individuals with relatively high incomes; at the same time, some elderly individuals with low income may have substantial assets that protect them from hardship. For both of these reasons, the relationship between income and hardship among the elderly is likely to be both complex and different from that for younger individuals. The recent development of an experimental poverty measure by the U.S. Census Bureau reflects some of these concerns. For example, one criticism of the official poverty measure is that it does not take into account the burden of high out-of-pocket medical spending, which is much more likely to be a problem for elderly households (Short 2014; Short and Garner 2002). Census Bureau estimates using an alternative poverty measure proposed by the National Academy of Sciences yield elderly poverty rates that are approximately twice the current official measure.1

At a time when pressure on the federal budget is giving rise to discussions of how entitlement programs benefiting the elderly might be restructured, understanding economic vulnerability among the elderly takes on new importance. How should the burden of any cuts in spending be distributed? Spending cuts can affect beneficiaries (for example, changing the formula for calculating Social Security cost-of-living increases; increasing beneficiary cost-sharing under Medicare), or they can affect health care providers (for example, cuts in Medicare reimbursement rates). For cuts that are borne by beneficiaries, policymakers must decide which beneficiaries will bear the brunt of these cuts and how to protect those who are most vulnerable.

In this article, I use data from the 2008 and 2010 Health and Retirement Study (HRS) to document patterns of material hardship among the elderly. I use five different measures of material hardship: food insecurity, skipped meals, cutting back on medications because of cost, difficulty paying bills, and dissatisfaction with one's financial situation. Overall, 21 percent of the elderly report one or more of these hardships. Among individuals in the lowest income quintile, the fraction is 37 percent, and even among those in the top income quintile, 11 percent report some hardship. Most elderly individuals who experience hardship are not poor. One alternative measure of resources that might be expected to predict hardship among older Americans better than income does, household spending, actually performs worse than income. To paint a fuller picture of why older individuals, including some with quite high incomes, experience hardship, I estimate multivariate models predicting hardship as a function of income and other characteristics, including health and cognition. In multivariate models, health status is a highly significant predictor of hardship: individuals who report being in worse health or who report more limitations on physical activity are much more likely to experience hardship. This result is robust to the inclusion of controls for income and out-of-pocket health spending, suggesting that poor health directly increases the risk of hardship, rather than only through its indirect effects on income or out-of-pocket medical spending. I also find that the risk of hardship is mitigated by having an able-bodied spouse; the risk of hardship is elevated for those with disabled spouses or very unreliable children.

These findings have important implications for public policy. First, since most of the elderly experiencing hardship are in fact not poor and therefore not eligible for means-tested transfer programs, increasing outreach with the goal of enrolling more eligible elderly in these programs has limited potential to reduce hardship. Similar logic suggests that while increasing benefit levels might reduce hardship among those who are already receiving benefits, its potential to reduce hardship is limited since transfer program recipients make up only about one-quarter of the elderly who experience hardship. Second, poor health's direct effect on hardship suggests that policy interventions that provide in-kind benefits—for example, congregate meal programs—could alleviate hardship more effectively than those that simply transfer cash.

PREVIOUS RESEARCH

A large literature considers the adequacy or optimality of retirement savings. A traditional approach to assessing the adequacy of retirement savings is to compare the income stream that would result from annuitizing wealth at the time of retirement to pre-retirement income (Mitchell and Moore 1998; Poterba, Venti, and Wise 2012). Retirement wealth is considered adequate if it yields an income stream that is not too much below one's income before retirement—regardless of how low this level may be. Numerous studies have noted that it is smooth consumption, rather than income, that reflects optimality, and a number of papers have tested this proposition (Engen et al. 1999; Hurd and Rohwedder 2006a, 2006b, 2008a, 2008b, 2011; Scholz, Seshadri, and Khitatrakun 2006). Again, the focus here is on smoothness over time rather than on the level of consumption; in particular, very low levels of consumption (so low as to result in food insecurity with hunger, for example) are not inconsistent with optimality in the economic sense.

A second relevant set of papers focuses on poverty among the elderly. Some of these extend the traditional approach to the adequacy of retirement wealth by comparing annuitized income streams to the poverty level or some other threshold level of expenditure required to meet basic needs; others compare actual income to the poverty level, while still others compare actual consumption to the poverty level (Brady 2010; Fisher et al. 2009; Haveman et al. 2003; Haveman et al. 2006; Haveman et al. 2007; Hungerford 2001; Johnson and Mermin 2009; Love, Smith, and McNair 2008; VanDerhei and Copeland 2010). An important subset of these papers focus on the high rate of poverty among elderly widows (Bound et al. 1991; Gillen and Kim 2009; McGarry 1995; McGarry and Schoeni 2005; Sevak, Weir, and Willis 2003; Weir and Willis 2000; Zick and Holden 2000).

An alternative approach to evaluating the economic well-being of the elderly is to analyze material hardship directly. Material hardship is operationalized in many different ways, depending on the population studied and the available data, and these methods are reviewed elsewhere (Beverly 2001; Federman et al. 1996; Ouellette et al. 2004). Some version of this approach has been applied to the non-elderly population, particularly to single-mother families and former welfare recipients (Danziger et al. 2000; Iceland and Bauman 2007; Mayer and Jencks 1989; Meyer and Sullivan 2003; Rector et al. 1999; She and Livermore 2007; Sullivan et al. 2008). Only one such study focuses on the elderly (Charles et al. 2006).

Finally, several studies have analyzed the determinants among the elderly of the two important outcomes that are treated as measures of hardship in the current analysis—food insecurity and medication cutbacks. One study using data from the Third National Health and Nutrition Examination Survey (1988–1994) and a much smaller 1994 survey of the elderly in New York State finds that low income, functional limitations, Hispanic ethnicity, younger age, and use of food stamps significantly predict food insecurity among the elderly (Lee and Frongillo 2001). In a related study, in-depth interviews were conducted with fifty-three elderly respondents about the causes of their food insecurity; this study concludes that, “although money is a major cause of food insecurity, elders sometimes have enough money for food but are not able to access food because of transportation or functional limitations, or are not able to use food (that is, not able to prepare or eat available food) because of functional impairments and health problems” (Wolfe, Frongillo, and Valois 2003, 2762).

A study of medication cutbacks among the elderly looked at medication restriction among seniors by using data on the approximately 5,000 respondents age seventy and older in the 1995–1996 wave of the HRS (the so-called AHEAD cohort) who regularly used prescription drugs (Steinman, Sands, and Covinsky 2001). This study finds that among the 1,911 of these respondents who had no drug coverage, poor health, nonwhite race-ethnicity, low education, low income, and high out-of-pocket drug costs are all significant predictors of medication restrictions. Finally, two studies of approximately 4,000 individuals age fifty and older with chronic illness find that younger age, lower income, and higher out-of-pocket costs all significantly predict medication restrictions (Heisler, Wagner, and Piette 2005; Piette, Heisler, and Wagner 2004).

This analysis updates and extends these studies by (1) looking at both types of cutbacks (medications and food) as well as two other self-reported measures of hardship in a common empirical framework; (2) linking the results to the more general literature on poverty; (3) using more recent data; (4) including more covariates; and (5) estimating individual fixed-effects models that eliminate time-invariant sources of unobserved heterogeneity.

DATA

Data for the analysis come from the Health and Retirement Study, a longitudinal study that has interviewed older adults since 1992. The HRS sample is described in detail elsewhere (Sonnega et al. 2014). Briefly, the HRS sample began with a cohort of approximately 12,600 respondents between the ages of fifty-one and sixty-one living in 7,700 households. Over time, the sample has been expanded and refreshed so that it is now nationally representative of the U.S. population over the age of fifty. Core interviews are conducted every two years either in person or over the phone with the full sample of respondents, querying them about their health, cognition, labor force status, income, and assets. For married couples, each member of the couple reports on his or her health, cognition, and labor force status, while household-level information, such as assets and income, are reported by a “financial respondent” on behalf of the household. Among married couples in our sample, husbands served as the financial respondent about two-thirds of the time. However, because single women outnumber single men in this age range, about half of all the financial respondents in our sample (including both singles and married couples) are female. Supplemental interviews on special topics are administered periodically to subsets of respondents. As described in more detail later in this article, this analysis relies on data from the 2008 and 2010 core surveys; from “leave-behind” surveys of psychosocial characteristics that were administered to half the sample in 2008 and the other half in 2010; and from the 2007 and 2009 waves of the Consumption and Activities Mailer Survey (CAMS), a supplemental survey of household spending patterns and time use administered to a random subsample of respondents.

Variables

The different variables used in the analyses are constructed as follows:

Measures of Hardship

The core HRS survey includes three yes or no questions that I use as measures of material hardship; individuals responding “yes” are coded as experiencing the hardship:

Food insecurity: “(Since your last interview/in the last two years), have you always had enough money to buy the food you need?”

Skipped meals: “At any time (since your last interview/in the last two years), have you skipped meals or eaten less than you felt you should because there was not enough food in the house?”

Medication cutbacks: “At any time (since your last interview/in the last two years) have you ended up taking less medication than was prescribed for you because of the cost?”

In addition, the psychosocial leave-behind questionnaire includes two questions about the respondent's financial situation:

Difficulty with bills: “How difficult is it for (you/your family) to meet monthly payments on (your/your family's) bills?” Response options are: “not at all difficult,” “not very difficult,” “somewhat difficult,” “very difficult,” and “completely difficult.” I code respondents as experiencing this hardship if they chose either “very difficult” or “completely difficult.”

Dissatisfaction with finances: “How satisfied are you with your present financial situation?” Response options are: “completely satisfied,” “very satisfied,” “somewhat satisfied,” “not very satisfied,” and “not at all satisfied.” I code respondents as experiencing this hardship if they chose either “not very satisfied” or “not at all satisfied.”

Economic Status

I use measures of family income and total household assets from the RAND HRS data file (version N, October 2014). A comparison of poverty rates among the elderly and near-elderly in HRS 2010 using this variable shows that they benchmark reasonably well to poverty rates for a similarly defined sample using data from the March 2010 Current Population Survey (CPS).2 Both income and assets are inflated to real 2010 values using the Consumer Price Index for All Urban Consumers (CPI-U) from the Bureau of Labor Statistics (BLS).

Total household spending: Information is available on total household spending for the subset of respondents included in the CAMS. I use the imputed version of this variable for 2007 and 2009 from the RAND data file (RAND CAMS, version D2, April 2015) and convert to real 2010 dollars using the CPI-U.

Out-of-pocket medical spending: I use measures of out-of-pocket medical spending for the respondent and spouse from the RAND HRS data file (version N, October 2014). The RAND measure is based on a question about respondents’ expenses during the previous two years. I convert this measure to 2010 dollars using the CPI-U and divide by two to get a measure of real annual out-of-pocket spending, which I subtract from annual income in some analyses.

Health: Respondents reported their overall assessment of their own health as “excellent,” “very good,” “good,” “fair,” or “or poor.”

Physical (Nagi) limitations: The HRS asks respondents whether they have difficulty because of a health problem with twelve different activities: walking several blocks, jogging a mile, walking a mile, sitting for two hours, getting up from a chair, climbing several flights of stairs, climbing a single flight of stairs, stooping, raising their arms above shoulder level, pulling or pushing large objects (the size of a living room chair), lifting or carrying weights over ten pounds (like a heavy bag of groceries), and picking up a dime from a table. From these responses I create an index of physical limitations by summing the number of positive responses to these items; the index takes on values from 0 (the healthiest, with no limitations) to 12 (the sickest, with the most limitations) (Fonda and Herzog 2004).

Number of medications taken regularly: The HRS asks respondents whether they take medications regularly for twelve different conditions: high blood pressure, diabetes, chronic lung disease, heart problems, conditions related to stroke, emotional, nervous, or psychiatric conditions, joint or muscle pain, asthma or allergies, stomach problems, sleep problems, anxiety, or depression. I use the number of medications taken regularly as a measure of the complexity of the respondent's medication regimen.

Cognitive ability: In the HRS core survey, interviewers read a list of ten words to respondents, who then recall as many words as they can. They are asked to recall the words immediately after hearing the list and also several minutes later. I use the sum of these from the 2006 survey, ranging from zero to twenty, as one indicator of cognitive ability. I also use respondents’ scores on the “Serial Sevens” test, in which they are asked to count backward from 100 by sevens up to five times. The score is the number of correct subtractions (from zero to five). Many respondents who have difficulty with these tasks refuse to complete them; I categorize those with missing data (about 15 percent for word recall and 7 percent for Serial Sevens) into the lowest performance category on each of these cognitive tests. Additional documentation on the HRS cognition measures is available elsewhere (Ofstedal, Fisher, and Herzog 2005).

Program use: I create dummy variables reflecting participation in three means-tested transfer programs: Medicaid, Supplemental Security Income (SSI), and food stamps. The Medicaid dummy indicates whether the individual reported having had Medicaid coverage at all during the two years since the previous interview. The SSI and food stamp dummies indicate whether the respondent—and spouse for married respondents—received any income from this source during the previous calendar year.

Labor force status: The core survey asks all respondents: “Are you working now, temporarily laid off, unemployed and looking for work, disabled and unable to work, retired, a homemaker, or what?” I use the responses to this question to create a labor force status indicator; the categories used in the multivariate analysis are “working,” “unemployed,” and “disabled,” with a residual category that includes retirees, homemakers, and respondents reporting “other” labor force status.

Demographics, education, and marital status: The analysis also includes controls for respondent age, race (white non-Hispanic, African American non-Hispanic, other non-Hispanic), ethnicity (Hispanic, not Hispanic), marital status, gender, and years of education.

The Sample

Because not all individuals are asked each question in each wave, the sample depends on the variables that are being analyzed. In 2008, 10,891 community-dwelling individuals ages sixty-five and older completed core interviews; in 2010, 10,423 did so. (The full HRS sample in each year, including individuals under the age of sixty-five, is around 17,000.) In 2008 and 2010, approximately 40 percent of the sample completed a leave-behind questionnaire, including two of my hardship measures (difficulty with bills and financial dissatisfaction) in each year. For the main analyses, which include the outcomes from the leave-behind questionnaire, this yields a sample of 8,738 individuals, with the data almost evenly split between those whose data are from 2008 and those whose data are from 2010. For panel analyses, which are possible only for outcomes from the core survey (food insecurity, skipped meals, and medication cutbacks), I have a sample of 9,078 respondents who are, for the most part, the same respondents in the sample used for the main analysis. Finally, for analyses including total spending and the leave-behind variables, I have a much smaller sample of 2,106 observations. All analyses use sampling weights unless noted otherwise.

RESULTS

Basic Descriptive Statistics

Table 1 presents basic descriptive statistics for the full sample and also by family income relative to poverty (less than 100 percent of the federal poverty level, 100 to 199 percent, 200 to 299 percent, 300 to 399 percent, 400 to 499 percent, and 500 percent or higher). Overall, 21 percent of the elderly reported some hardship; considering only the four hardships other than financial dissatisfaction (food insecurity, skipped meals, medication cutbacks, or difficulty paying bills), this figure is 13 percent. Seven percent reported medication cutbacks, 4 percent reported food cutbacks, and 2 percent reported skipping meals; 5 percent had difficulty paying bills, and 14 percent were dissatisfied with their financial situation. Among those who did experience some hardship, lower-income households were more likely to experience more than one hardship. Seven percent of the sample lived in poverty, and nearly one-quarter lived in a family with income less than 175 percent of the federal poverty level. Ten percent of the elderly reported using Medicaid, food stamps, SSI, or some combination of the three programs, with a much higher prevalence, not surprisingly, among lower-income households; half of all households in poverty reported some program use, while fewer than 2 percent of households with income higher than five times the poverty level (corresponding to approximately the top quartile of the income distribution) did. Most (84 percent) of the sample members were no longer working, and 26 percent reported that their health was only fair or poor.

Material Hardship and Sociodemographic Characteristics of Americans Age Sixty-Five and Older: Sample Means

How Well Does Income Explain Hardship Among the Elderly?

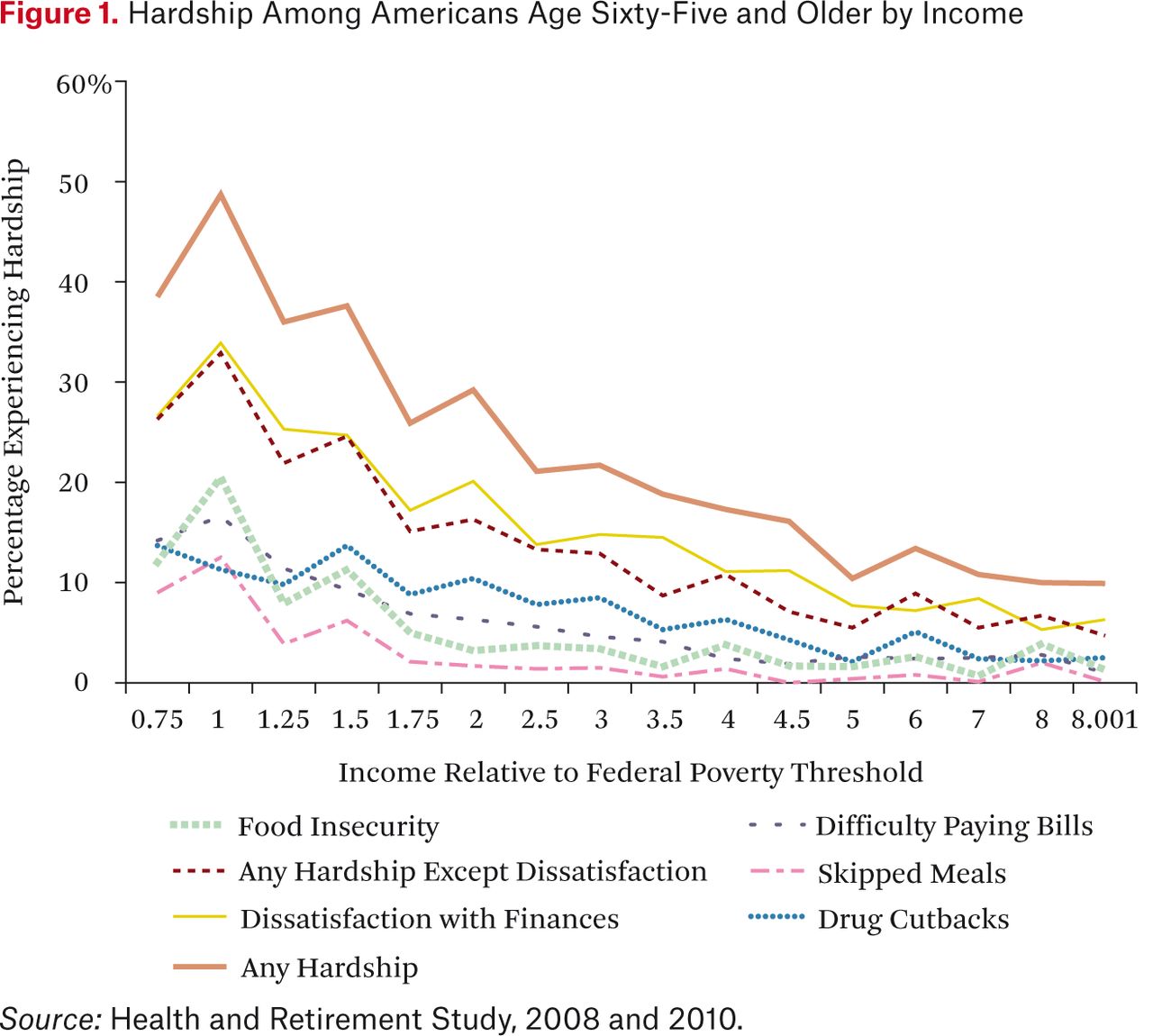

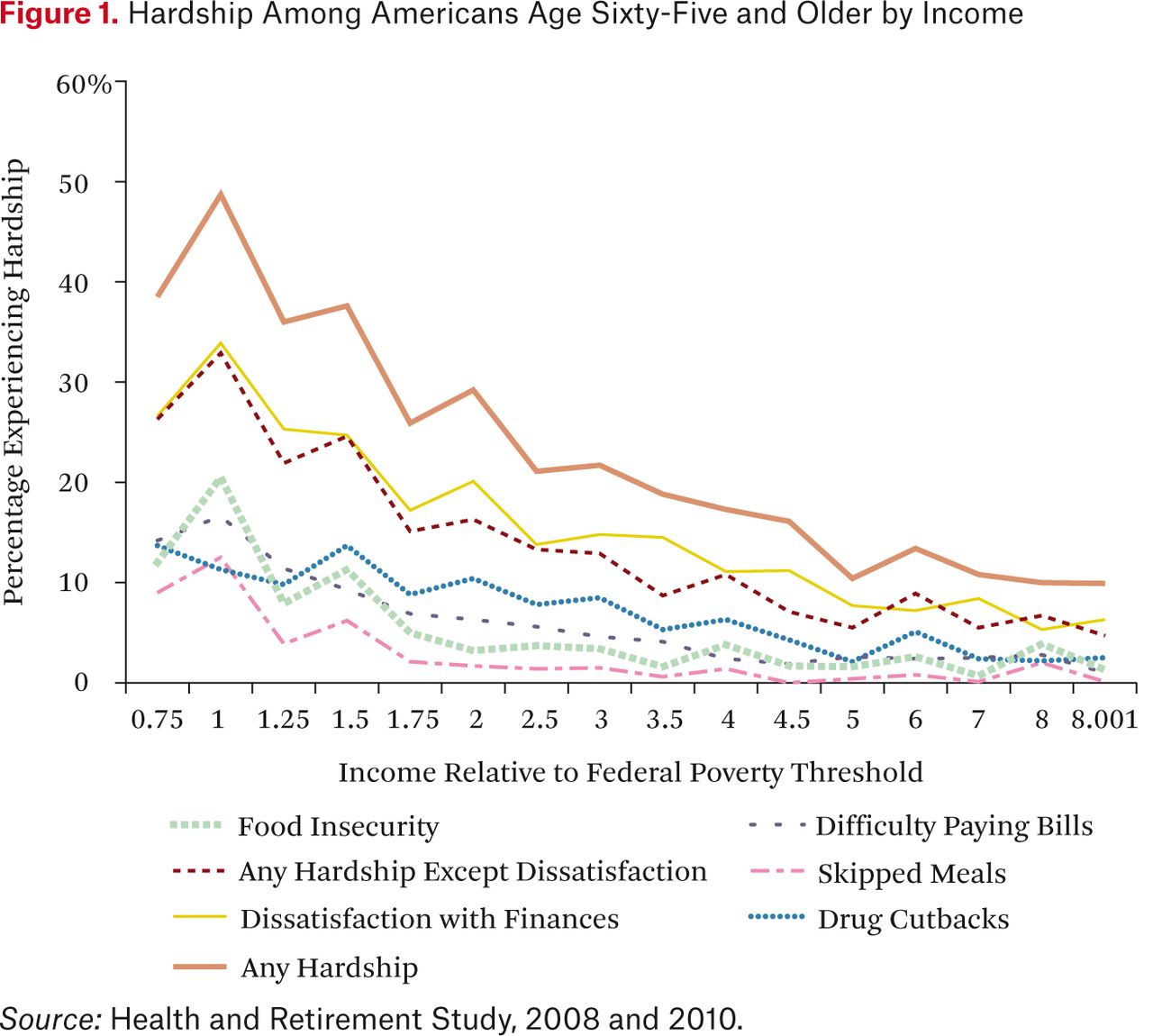

The prevalence of hardship declines as income increases, as shown in figure 1 (the data used to create this figure are in appendix table A1). There is a strong relationship between income and hardship: in the lowest income category—households with income below 75 percent of the poverty threshold, which account for about 3.4 percent of older Americans—38.5 percent experienced hardship. The prevalence of hardship increases slightly in the next income category, then declines slowly as income increases. At a certain point, which varies depending on which hardship is being analyzed, the relationship flattens out; additional income above this level does nothing to reduce hardship.

Hardship Among Americans Age Sixty-Five and Older by Income

The nonlinear relationship between income and hardship is not particularly surprising; what is surprising is how high income must be before additional income is no longer associated with lower hardship. Income must be about five times the poverty level before its effect on the probability of reporting any hardship fades out. This persistence of hardship is driven mostly by medication cutbacks, difficulty paying bills, and financial dissatisfaction; the income gradients associated with food insecurity and skipped meals fade out earlier, at about twice the poverty level. Also surprising is the fact that even at the highest levels of income, the prevalence of hardship is not zero. In families with incomes greater than five times the poverty level, about 5 percent of elderly individuals experienced some hardship. Hardship at higher levels of income consists mostly of medication cutbacks and dissatisfaction; only 1 or 2 percent of these individuals reported food insecurity or difficulty paying bills, and skipping meals was essentially unknown among families with income greater than three times the poverty level.

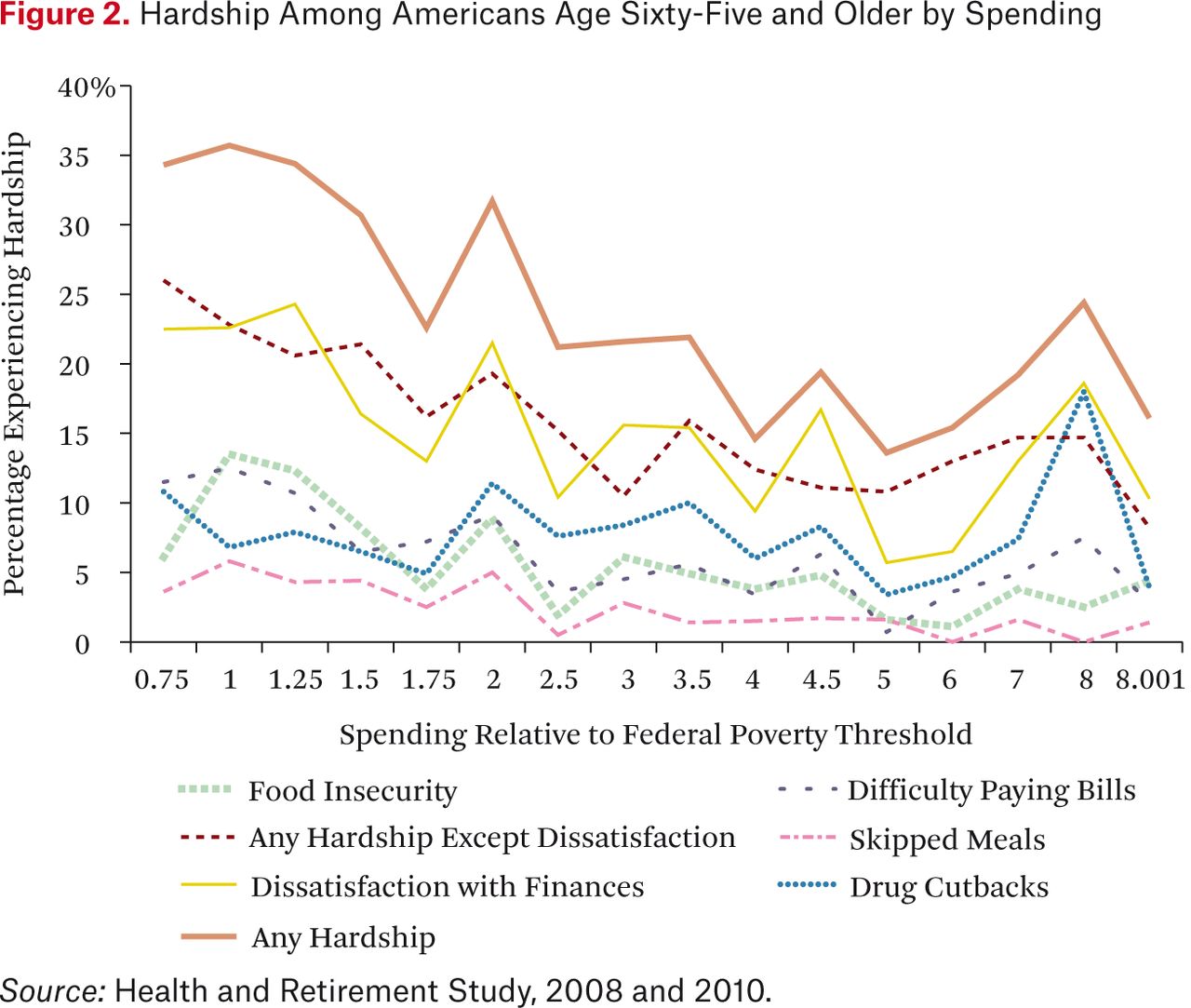

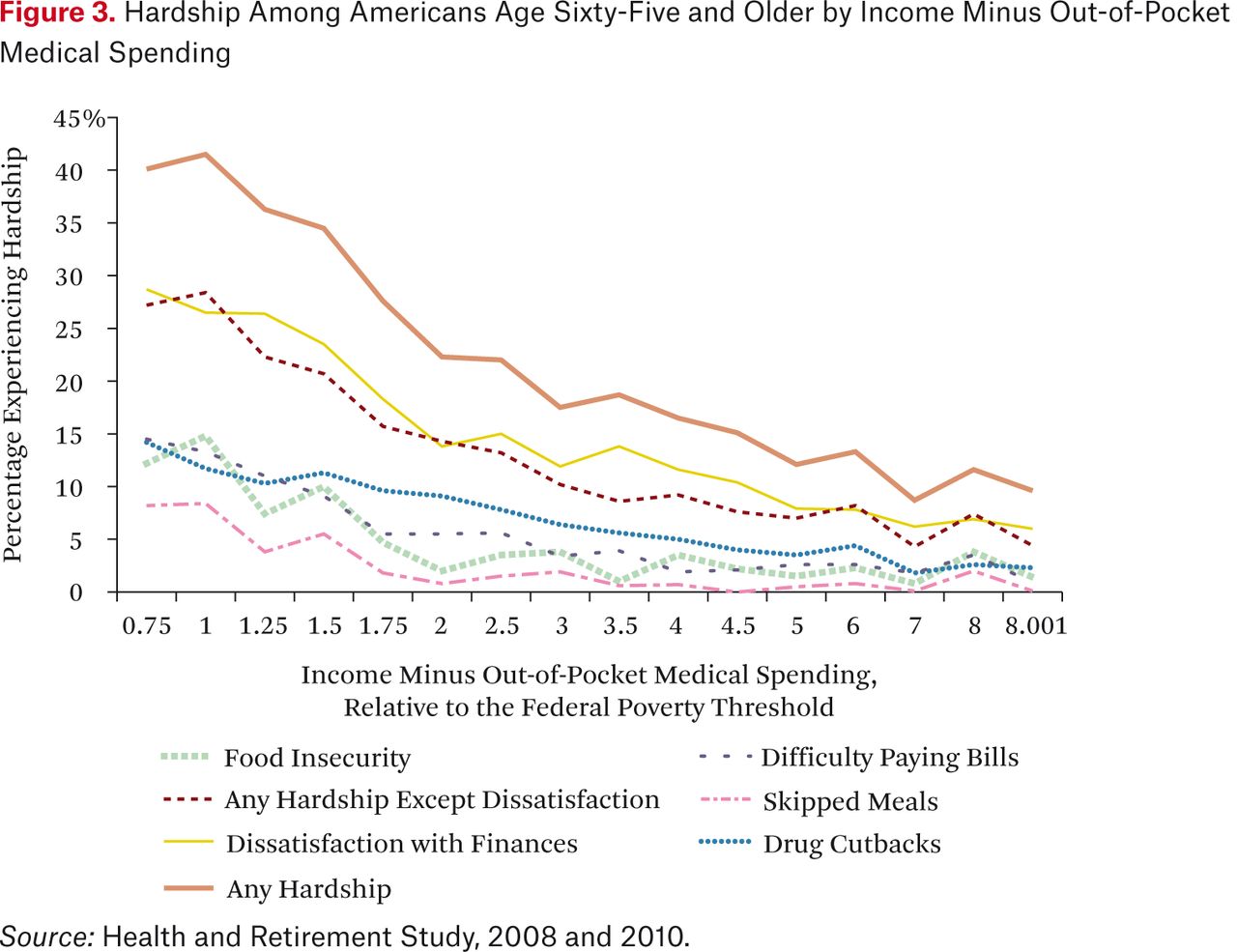

Would Alternative Measures of Resources Predict Hardship Among the Elderly More Accurately than Income Does?

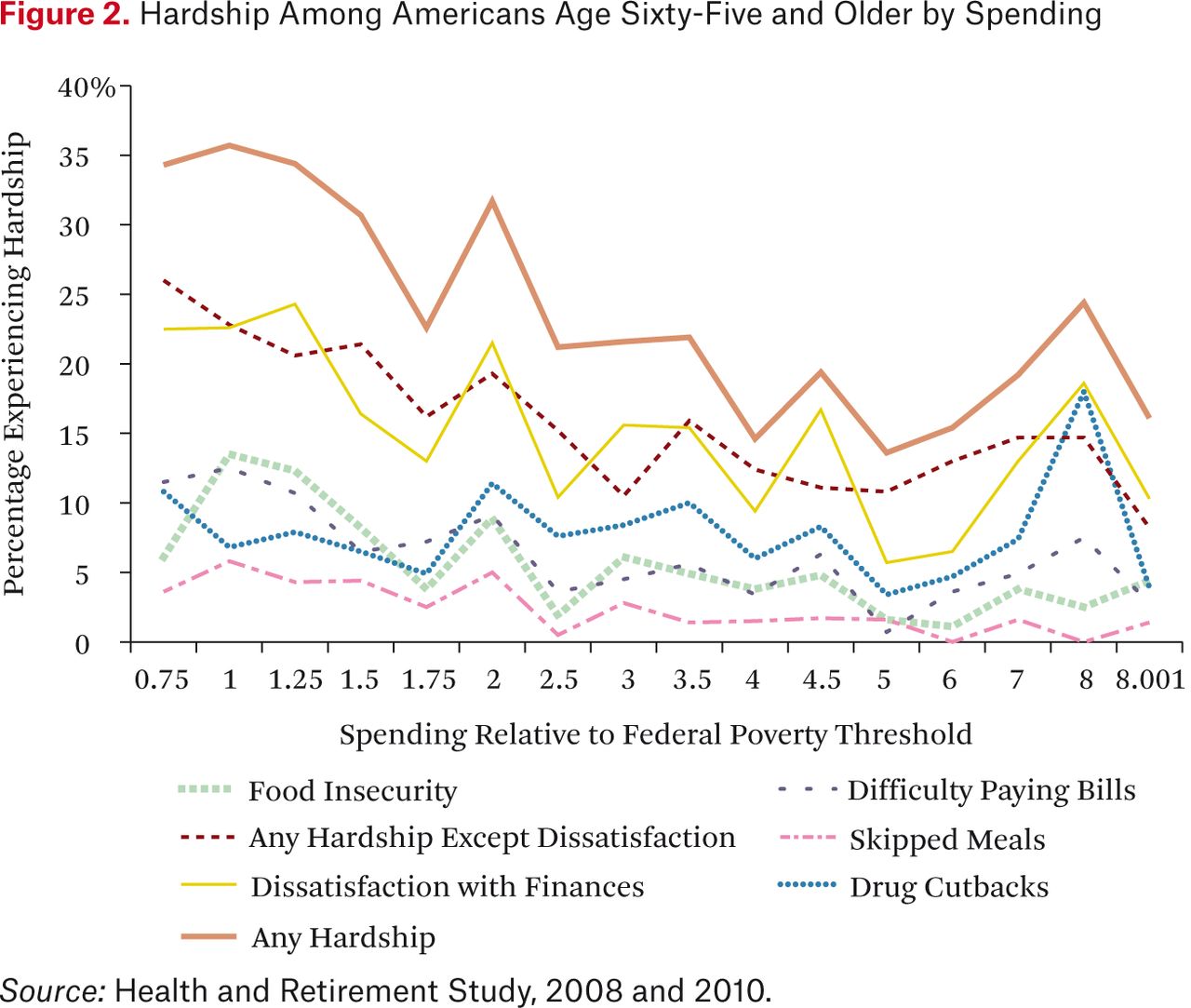

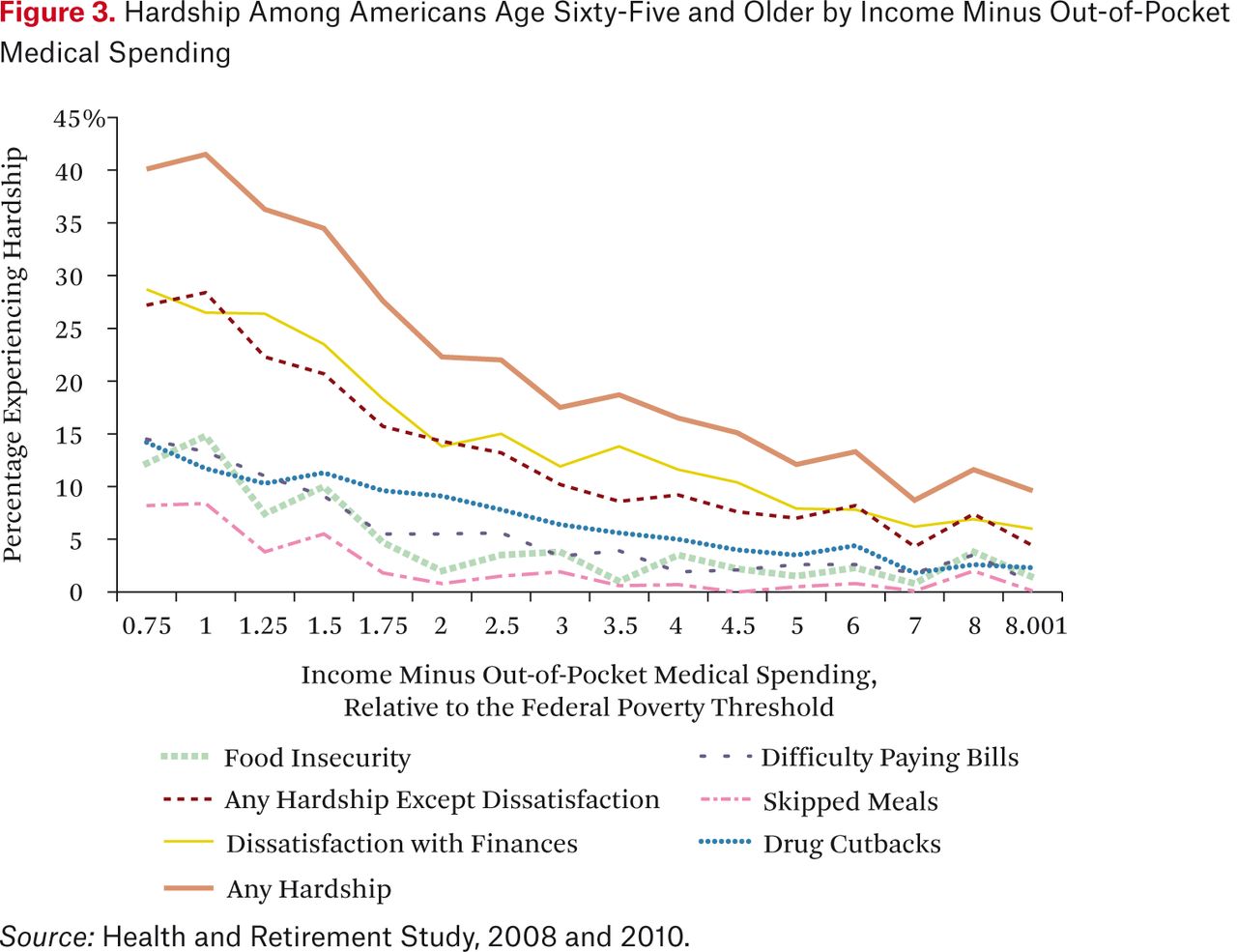

As already noted, other resource measures, such as consumption and disposable income, may target hardship more accurately than income does, particularly for the elderly. To test this possibility, I explore two other measures of resources: (1) total spending, using the subset of respondents for whom CAMS data are available, and (2) income minus household out-of-pocket medical spending. Figures 2 and 3 replicate figure 1 using these two alternative measures of resources. Figure 2 shows that total spending does not seem to do a better job than income of discriminating between those households that are likely to experience hardship and those that are not. This echoes the conclusion reached by Kerwin Kofi Charles and his colleagues (2006), who use somewhat different methods. In contrast, repeating the same tabulation using a measure of household income net of out-of-pocket medical spending (figure 3) does a somewhat better job than does income alone of identifying households at risk of hardship. That is, there is more mass in the left tail in figure 3 than in figures 1 or 2, and the probability of hardship declines more smoothly.

Hardship Among Americans Age Sixty-Five and Older by Spending

Hardship Among Americans Age Sixty-Five and Older by Income Minus Out-of-Pocket Medical Spending

While this eyeball test makes sense, it is not obvious how we could quantify the accuracy with which a resource measure identifies hardship. One way of doing this is to calculate how high up the resource distribution it is necessary to go before we have identified half (or some other chosen fraction) of those in hardship. Table 2 operationalizes this concept by calculating the median value of different resource measures for individuals experiencing each kind of hardship. A resource measure that more accurately identifies hardship will have lower values in table 2; that is, more of the population with hardship will be clustered at low resource levels. Table 2 confirms the intuition of figures 1, 2, and 3: total spending is inferior to income for targeting hardship, while income net of out-of-pocket medical spending is superior. There is still a lot of hardship, however, that is not explained by subtracting out-of-pocket medical spending from income; half of individuals reporting hardship were in households with income net of out-of-pocket medical spending greater than 170 percent of their federal poverty threshold.

Median Resources Among Americans Age Sixty-Five and Older Who Experience Hardship

Is Hardship Related to Failure to Take Up Transfer Programs?

The role of transfer programs is particularly interesting because the existing literature mostly shows that hardships are more likely among recipients than among eligible nonrecipients. In particular, a number of studies find that food insecurity is more prevalent among food stamp recipients than among nonrecipients (Haider, Jacknowitz, and Schoeni 2003; Wilde and Nord 2005), presumably because the timing of enrollment, conditional on having income low enough to be eligible, is not random: people enroll in these programs when they have fallen on tough times. As a result, the partial correlation between program use and hardship reflects both self-selection into program use and any causal effect of program use on hardship, two factors that are likely to go in different directions (Haider, Jacknowitz, and Schoeni 2003; Wilde and Nord 2005). More recent studies relying on plausibly exogenous variation in program use to identify the effect of food stamps find mixed effects, which is probably related to variation in the validity of the instrumental variables strategy (Greenhalgh-Stanley and Fitzpatrick 2013; Schmidt, Shore-Sheppard, and Watson 2013).

Because I have no exogenous variation in program use, and also because public program use is not well measured in surveys (Meyer, Mok, and Sullivan 2009), I do not attempt to draw any causal inference about the relationship between take-up and hardship. Rather, my goal is to document how many of those experiencing hardship are not taking up public programs for which they may be eligible, in order to understand how much scope there is for reducing hardship by, for example, improving program outreach. Figure 4 (based on the data presented in appendix table A2) explores the relationship between hardship and transfer program use by categorizing the elderly experiencing hardship by income (collapsed into two categories: greater than or less than 175 percent of poverty) and the use of transfer programs (food stamps, Medicaid, and SSI). As already noted, about half of those experiencing hardship fell into the higher income category; about 10 percent of these (or 5 percent of the total) were programs users. In the lower-income group, most but by no means all of the elderly who experienced food insecurity or skipped meals were already using public programs. About half of low-income elders who had difficulty paying bills used public programs. For the other hardships—medication cutbacks and financial dissatisfaction—most of the elderly who experienced them did not use SSI, Medicaid, or food stamps. The fact that, overall, only 23 percent of those experiencing hardship were low-income individuals failing to take up any public programs suggests that improving outreach alone, without also expanding eligibility or increasing benefits, would have a limited effect in mitigating hardship.

Distribution of Americans Age Sixty-Five and Older Experiencing Hardship by Family Income and Use of Transfer Programs

Multivariate Results

The main result from this descriptive analysis is that while hardship is more likely among those with lower incomes, most of the elderly experiencing hardship are not poor. Why are so many nonpoor elderly experiencing hardship? To understand the determinants of hardship in a multivariate context, I estimate linear probability models predicting hardship as a function of economic resources, demographic characteristics, health, and cognition. I estimate the model separately for five hardships—(1) food insecurity, (2) skipped meals, (3) medication cutbacks, (4) difficulty paying bills, and (5) dissatisfaction with one's financial situation—and for two summary outcomes: (6) any of the above five hardships, and (7) any of the above five hardships except dissatisfaction with one's financial situation.

All models include controls for the natural log of real income net of out-of-pocket medical spending; the natural log of total real wealth; age; an indicator for fair or poor self-rated health; the number of Nagi limitations; the number of medications the respondent takes regularly (0 to 12); memory score (0 to 20); Serial Sevens score (0 to 5); gender and marital status dummies; an indicator for education less than high school; and race and ethnicity dummies. Regressions also include indicators of labor force status at the time of the interview (working, unemployed, or disabled), with the omitted group consisting mostly of respondents who were out of the labor force (homemakers, retirees) and a small number of respondents who reported “other” labor force status. The models reported here are parsimonious ones in which most variables (for example, education, cognition, and health status) are entered linearly or as a single dummy variable. More flexible models that include these variables as vectors of categorical dummies yield results that are very similar to the parsimonious models. Additional specification checks are discussed later.

Table 3 presents the basic multivariate results. Income and assets both significantly reduce the probability of all kinds of hardship. The coefficients imply that a 1 percent increase in income or assets translates, on average, into about a one-percentage-point reduction in the probability of food insecurity and about a two-percentage-point reduction in the probability of any of the hardships.

Multivariate Models Predicting Hardship Among Americans Age Sixty-Five and Older: Full Sample, OLS Estimates

Other than income and assets, the most striking predictors of hardship are measures of poor health, consistent with earlier studies (Lee and Frongillo 2001; She and Livermore 2007). Being in fair or poor health, having a greater number of Nagi limitations, or reporting one's work status as “disabled” all increase the probability of hardship substantially. Why is health so important? There are three plausible mechanisms through which poor health or disability may lead to hardship. First, poor health may reduce income directly by making it harder to work. Second, poor health may increase out-of-pocket medical spending, tying up income that could be used to meet other basic needs such as food. Third, poor health may affect one's ability to make do, as suggested by earlier qualitative work (Wolfe, Frongillo, and Valois 2003).

To test the importance of the first hypothesis, I reestimated the regressions both without any income controls and with more extensive controls for income (a set of fifteen dummies reflecting categories of income-to-needs). If income is an important channel through which poor health affects material hardship, dropping the income controls ought to increase the coefficient on the measures of poor health (self-reported health, Nagi limitations, number of medications taken regularly, and disability status). In fact, these coefficients are essentially unchanged by the exclusion of income controls or the inclusion of more detailed income controls. I conclude that, among the elderly at least, income is not the primary channel through which poor health translates into hardship.

The second channel through which health may affect hardship is through out-of-pocket medical spending. As already discussed in the context of figures 1 through 3 and table 2, out-of-pocket spending does seem to explain at least partly why apparently high-income individuals experience hardship. But reestimating the models in table 1 using income minus out-of-pocket spending rather than income changes the coefficients on the health variables very little. Thus, the regression results suggest that out-of-pocket medical spending explains relatively little of the effect of poor health on hardship; health has a strong independent effect on hardship regardless of income or out-of-pocket medical spending.

This leaves the third reason for why poor health could mean more hardship: it is simply harder to get by for someone who is in poor health, and it is especially difficult to make do with less. For example, an elderly person with activity limitations might have to purchase (more expensive) prepared meals, rather than cook from scratch, or have to shop at expensive convenience stores, being unable to shop around for lower prices.

Two supplemental analyses lend support to this story. The first explores the role of spouses and their physical limitations. It is evident from the results of the multivariate models in table 3 that being married may actually increase the risk of some hardships for men, while being married reduces hardship across the board for women. Table 4 presents coefficients from multivariate models that are the same as those presented in table 3 except that (1) the models are estimated separately for men and women, and (2) marital status is now measured using a complete set of dummies representing the spouse's level of physical limitations using the Nagi measures described earlier. The results for men in the top panel of table 4 show that having an able-bodied wife reduces the risk of hardship somewhat, but that having a disabled wife significantly increases the risk of food insecurity. For women, having a husband reduces the risk of hardship across the board, while having a husband with no physical limitations reduces hardship the most.

Effects of a Spouse's Physical Limitations on Experiences of Hardship Among Americans Age Sixty-Five and Older

The second supplemental analysis focuses on children. The top row of table 5 reports the coefficients from models similar to those in table 3 but augmented with a dummy for whether or not the respondent had children. Having children does not, on average, affect hardship, but this lack of an effect masks heterogeneity in the nature of the respondent's relationship with his or her children. The psychosocial leave-behind questionnaire asks respondents with children: “How much can you rely on them if you have a serious problem?” Possible responses are “a lot,” “some,” “a little,” and “not at all”; a small fraction of respondents with children (1 percent) did not respond to this question, and these nonresponses are treated as a separate category. When I estimate models similar to those in table 3 but augmented with a set of variables distinguishing between reliable and unreliable children, it is clear that the lack of an effect on average masks a significant increase of hardship among those with very unreliable children. (Fortunately, this type of children were quite rare: only 3 percent of parents reported having them. This explains the lack of any significant effect in the models with a simple indicator for whether or not the respondent had children.)3

Effects of the Presence and “Quality” of Their Children on Hardship Among Americans Age Sixty-Five and Older

Turning back to table 3 to look at other predictors of hardship, we see that better memory actually increases the probability of hardship slightly, possibly because these respondents were more likely to know or more likely to report that they had a problem. Respondents with higher scores on the Serial Sevens test, in contrast, were significantly less likely to report difficulty paying bills or financial dissatisfaction. Education is not a significant predictor of hardship in these models, since it is highly correlated with age, income, education, and cognition. In all models, older individuals were less likely to report hardship. Steven Haider, Alison Jacknowitz, and Robert Schoeni (2003) report a similar finding for food-related hardship (skipped meals) and speculate that the well-established fact that caloric needs decline with age may be responsible. On the other hand, a similar story cannot explain why medication cutbacks also decline with age, since medication use increases with age.

African Americans had significantly higher rates of food insecurity and medication cutbacks; rates for other nonwhites and Hispanics were similar to those for white non-Hispanics (the omitted group). Unmarried women, three-quarters of whom are widows, reported significantly higher rates of hardship than did single men, married men, or married women; much of this effect is due to their lower incomes. As already noted, the effect of marriage is different for men and women and depends, for men, on how healthy their wife is.

Individual Fixed-Effects Estimates

To address at least partially the concern that unmeasured individual-level factors correlated with the explanatory variables may actually be causing hardship, I also estimate models with an individual fixed effect (FE) using data from the 2008 and 2010 surveys. I cannot use fixed-effects models to analyze difficulty paying bills or financial dissatisfaction, since questions about these hardships are not asked every wave. Therefore, the FE models focus on food insecurity, skipped meals, and medication cutbacks. The FE models reported in table 6 confirm the central finding of the ordinary least squares (OLS) models reported in table 3: health measured using either Nagi limitations or self-reported disability status is an important predictor of hardship. Poor self-reported health status has a small and insignificant negative effect on hardship in the FE models. Income and assets remain significant predictors for some outcomes but not for others, and with smaller magnitudes than in the OLS models. Other explanatory variables that were significant in the OLS models, such as cognition, are no longer significant in the FE models, although it is difficult to say with certainty whether this is because these variables truly do not matter in determining hardship or because there was not much change in these characteristics over the two-year window from 2008 to 2010.

Multivariate Models Predicting Hardship Among Americans Age Sixty-Five and Older: Full Sample, Individual FE Estimates

DISCUSSION

The empirical analysis in this article yields two important results with implications for public policy and future research. First, I find that while hardship is more likely among poor individuals than among those with higher incomes, most older Americans experiencing hardship are neither poor nor using any transfer programs. Thus, the impact of efforts to reduce hardship by increasing outreach and enrollment among eligible nonparticipants, or by increasing benefit levels for those who already participate, is inevitably limited. Finding ways to target transfer programs more precisely to those experiencing hardship—which would probably involve rewriting the eligibility rules for the programs—could also be an important component of efforts to reduce hardship among the elderly.

Second, like a number of earlier studies cited here, I find that health status is an important predictor of hardship among the elderly: individuals in worse self-reported health or who report more limitations on their physical activity are significantly more likely to experience hardship. The persistence of this effect when controlling for income or for income net of out-of-pocket medical spending suggests that poor health has direct effects on hardship, not just that it affects income or expenditures. Simply put, poor health makes it harder to make do with less. Further research is needed to understand which interventions would do the most to reduce material hardship among the elderly.

Material Hardship Among Americans Age Sixty-Five and Older

Distribution of Americans Age Sixty-Five and Older Experiencing Hardship by Family Income and Use of Transfer Programs

Acknowledgments

I gratefully acknowledge helpful suggestions from Sanders Korenman, from Dean Lillard, from workshop participants at the Social Security Administration, Office of Research, Evaluation, and Statistics, and from participants in the Russell Sage Foundation “Severe Deprivation in America” conference. The Health and Retirement Study is sponsored by the National Institute on Aging (grant number NIA U01AG009740) and is conducted by the University of Michigan. I acknowledge financial support from the National Institute on Aging (grant number NIA K01AG034232). This project was also supported by a grant from the Social Security Administration through the Michigan Retirement Research Center. The findings and conclusions expressed are solely those of the author and do not represent the views of the Social Security Administration, any agency of the federal government, or the Michigan Retirement Research Center.

FOOTNOTES

↵1. U.S. Census Bureau, “Poverty: Experimental Measures,” available at: http://www.census.gov/hhes/www/povmeas/tables.html (last revised October 16, 2014). Another proposed measure of poverty based on data from the Luxembourg Income Study (LIS) would also yield higher poverty rates for the elderly (Brady 2004). Barbara Butrica, Dan Murphy, and Sheila Zedlewski (2010) demonstrate that a range of alternative measures of poverty yield higher poverty rates for the elderly.

↵2. Poverty rates for individuals ages fifty-six to sixty-four are 10.8 percent in HRS and 10.4 percent in CPS; for individuals ages sixty-five and older, the rates are 9.0 percent in HRS and 9.1 percent in CPS.

↵3. I also estimate models that distinguish between respondents with children who were coresident, who lived nearby (within ten miles), and who lived farther away. These models show higher rates of hardship among families with coresident children—almost certainly driven by selection into coresidence—and no differential effect of non-coresident children based on whether or not they lived nearby.

- Copyright © 2015 by Russell Sage Foundation. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Reproduction by the United States Government in whole or in part is permitted for any purpose. I gratefully acknowledge helpful suggestions from Sanders Korenman, from Dean Lillard, from workshop participants at the Social Security Administration, Office of Research, Evaluation, and Statistics, and from participants in the Russell Sage Foundation “Severe Deprivation in America” conference. The Health and Retirement Study is sponsored by the National Institute on Aging (grant number NIA U01AG009740) and is conducted by the University of Michigan. I acknowledge financial support from the National Institute on Aging (grant number NIA K01AG034232). This project was also supported by a grant from the Social Security Administration through the Michigan Retirement Research Center. The findings and conclusions expressed are solely those of the author and do not represent the views of the Social Security Administration, any agency of the federal government, or the Michigan Retirement Research Center. Direct correspondence to: Helen Levy at hlevy{at}umich.edu, Institute for Social Research, University of Michigan, 426 Thompson St., Ann Arbor, MI 48104.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.