Abstract

Although a growing number of studies suggest that providing poor families with income supplements of as little as $1,000 per year will improve children’s well-being, many poor children miss important sources of income support provided through the tax system because their parents either do not work or do not file taxes. Accessing assistance through means-tested programs is also challenging. We propose replacing the complicated array of benefits provided through the tax system with a universal child benefit of $2,000 per child that would be available regardless of parents’ work status. Our reform would ensure that all children receive enough assistance to make a difference and it would be simpler and more equitable than the current array of child benefits that are provided through the tax code.

It is well known that children who live in poor families are at a substantially higher risk of growing up to be poor adults than those who grow up in more advantaged families. Wagmiller and Adelman for example, document that adults who experienced at least one year of poverty during childhood are more than ten times as likely to be poor at age thirty-five as those whose families were never poor (2009). Moreover, there are worrying signs that poor children’s chances for long-run success are worsening: recent studies indicate that educational achievement gaps between poor and non-poor children have been widening over time (Reardon 2011; Bailey and Dynarski 2011). For example, Sean Reardon documents that in the forty years between 1968 and 2008, the achievement gap between high- and low-income children increased by about 50 percent. Academic performance is an important predictor of future economic success, so these trends point toward higher levels of immobility in the future, particularly when coupled with the increases in income inequality that current generations of parents have experienced.

Although evidence is long-standing that family income during childhood predicts adult income, it is only recently that we have begun to understand the causal mechanisms behind this correlation. The increasing availability of large administrative datasets and the adoption of creative natural experiment analysis approaches have allowed social scientists to come closer to emulating randomized control experimental designs, which are the gold standard for causal inference but have been rare in the study of income disparities. These advances are critical to the development of effective anti-poverty policies: without them, it is impossible to know how much of the difference in children’s outcomes is driven by differences in monetary resources versus other family background characteristics or circumstances that are correlated with parental income. Careful quasi-experimental studies consistently show that providing low-income families with sustained financial aid improves both short-run measures of children’s well-being and their eventual labor market and health outcomes. The studies include analyses that exploit negative shocks to income, such as those precipitated by unanticipated job loss, and analyses that harness positive boosts to family income that are generated through the U.S. safety net and tax system.

The rapidly expanding evidence that “money matters” suggests that we may be able to improve poor children’s opportunities by increasing existing levels of cash assistance. Providing higher levels of cash assistance may also be an economically sensible investment because the ensuing improvements in children’s later labor market and health outcomes are likely to reduce later public expenditures on welfare and health care. Moreover, economic theory asserts that direct cash aid should dominate many other forms of government assistance because cash aid maximizes poor families’ flexibility in choosing child investments that will have the highest payoff to the family.

Twenty years after the passage of the Personal Responsibility and Work Opportunity Reconciliation Act (PRWORA), however, the majority of means-tested cash assistance to the nondisabled is delivered only to families in which an adult is employed. As discussed in the introduction to this issue, cash benefits provided through the Temporary Assistance for Needy Families (TANF) program have declined dramatically, and are now frequently tied to parental work effort. Furthermore, approximately half of the financial assistance that is available to able-bodied parents is generated through their tax returns, and tied to positive earnings. Children whose parents are unable or unwilling to find work cannot receive the refundable part of the Child Tax Credit (CTC) or the earnings subsidies that are provided through the Earned Income Tax Credit (EITC). Moreover, many low-income parents who do work and are eligible for these credits do not receive them because they have difficulties navigating the tax code or fail to file taxes altogether. Families who do not file taxes also fail to receive assistance that is available through the tax code’s dependent exemptions. In addition, many families who are eligible for near-cash benefits available through programs like the Supplemental Nutrition Assistance Program (SNAP) do not take them up because of difficulties or stigma associated with accessing welfare programs. Taken together, this means that a nontrivial number of children who would gain from additional monetary resources are not currently receiving them. For example, in data from the 2014 calendar year Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC), 10 percent of families with children under eighteen received no benefits from tax exemptions, the EITC, or the CTC. Six percent of families also did not get benefits through either the tax system or SNAP.

In this article, we review the rapidly expanding evidence on the causal relationship between family income and children’s short and long-term well-being. We then propose a new lump-sum child benefit that does not require a family to file taxes and would be available to all families with citizen children, regardless of their parents’ work status. Our proposal targets citizen children because they are easy to track through existing administrative systems.1 As we describe later, however, the child benefit could be extended to some noncitizen children through the same systems. Current research suggests that an annual benefit of approximately $2,000 per child would generate meaningful improvements in children’s well-being and life chances, and may have multiple advantages over the current array of cash assistance programs. It could also be implemented so as to be revenue neutral by replacing the child-related credits and exemptions that are part of the tax code. This would enable policymakers to avoid political economy challenges associated with funding new programs and would have the added benefit of separating the goals of equalizing children’s life chances from the goal of incentivizing adults’ participation in the labor market. One concern with our approach might be that a fixed grant would reduce work effort. Therefore, we discuss how variants of our proposal with different expected effects on parental work effort would be likely to affect the distribution of income across poor and near-poor children.

FAMILY INCOME AND CHILDREN’S SHORT- AND LONG-TERM WELL-BEING

Fifteen years ago, we knew that poor children were at relatively greater risk of experiencing a host of negative outcomes that include lower levels of educational attainment, higher rates of criminal involvement, and higher rates of mental illness (see, for example, Brooks-Gunn and Duncan 1997; Moore et al. 2009). We have also long known that poor children show notable compromises in the development of their cognitive and social-emotional skills (Bradley and Corwyn 2002; Brooks-Gunn and Duncan 1997; Farah et al. 2006; Noble, McCandliss, and Farah 2007; Evans and Cassells 2014; Yoshikawa, Aber, and Beardslee 2012). These outcomes in turn predict lower likelihood of labor market success and higher likelihood of poverty in adulthood. Consistent with these predictions, some studies have documented high rates of intergenerational income and poverty persistence (Solon 1992; Zimmerman 1992; Chetty et al. 2014). The article by Luke Shaefer and his colleagues in this issue (2018) also describes many other studies that have linked family income with a variety of measures of children’s short and longer-term well-being.

Until recently, however, we knew less about why these relationships existed. It has been unclear, for example, how much of the persistence in poverty across generations reflects the causal effect of growing up in a family with compromised monetary resources versus the effect of family background characteristics or neighborhood environments that are often correlated with low income. Fortunately, recent research developments have allowed social scientists to pinpoint important pathways that were previously difficult to identify with any clarity. Researchers have become increasingly adept at applying statistical and econometric methods that help separate causal effects from potentially confounding correlations. Moreover, improved access to large administrative datasets has provided opportunities to successfully apply these methods yet maintain statistical precision. Careful quasi-experimental and experimental studies harnessing these research advances show that changing the amount of money consistently available to families can directly affect child well-being and children’s later life success.

One set of studies uses unanticipated parental job displacements generated by mass layoffs and firm closures to examine the effects on children of a plausibly exogenous decline in family income. Mass layoffs are determined at the firm level, so job losses that are precipitated by such events are unlikely to be related to individual characteristics that independently affect children.2 Moreover, as is well known, these types of job displacements lead to substantial, persistent earnings declines (for a review of the literature, see von Wachter 2010). Steven Davis and Till von Wachter, for example, find that men with more than three years of prior job tenure at larger firms, who lose their jobs in a mass layoff, experience annual present value earnings reductions of about 12 percent in an average year (2011).3

Studies that compare children whose parents experienced an unanticipated job loss with similar children whose parents were able to maintain their jobs find that those with displaced parents have worse measures of early life health (Lindo 2010) and academic achievement (Coelli 2005; Stevens and Schaller 2011; Hilger 2016). Moreover, there is evidence that these impacts persist to later life labor market success. Using Canadian tax data, Philip Oreopoulos, Marianne Page, and Ann Stevens find that children whose fathers experienced a job displacement have adult earnings that are about 9 percent lower than children whose fathers did not experience an employment shock (2008). They are also more likely to receive social assistance. Importantly, these effects are driven by individuals whose parents were at the bottom of the income distribution: among those children whose father’s earnings were initially in the lowest quartile, subsequent earnings are 17 percent lower than predicted if their father had not been displaced.4

These impacts on short- and long-term measures of child well-being may result directly from parents’ compromised ability to invest in their children, but another potential pathway is through increases in family stress. Psychologists, neuroscientists, and economists have documented that economic stress has deleterious effects on mental health and family functioning, which may in turn affect children’s outcomes (Aizer, Stroud, and Buka 2016; Conger, Conger, and Elder 1997; Conger et al. 1994; Cutrona et al. 2003; McLoyd 1998; Conger 2011; Evans and Garthwaite 2014; Reeb, Conger, and Martin 2013; Santiago, Wadsworth and Stump 2011). Recent work by Mullainathan and Shafir 2013 also documents that income volatility combined with scarcity can have psychological impacts that make it difficult for parents to escape poverty and to parent effectively.

Fortunately, evidence is also strong that the negative effects of income deprivation can be counteracted by policies that provide cash or near-cash assistance. Leveraging variation in family income generated by the 1990s welfare-reform experiments, Greg Duncan, Pamela Morris, and Chris Rodriques find that a $1,000 increase in family income increases children’s achievement test scores by around 5 percent of a standard deviation (2011). Aletha Huston and her colleagues examine the New Hope experiment, which provided wage subsidies to full-time workers that were sufficient to raise family income above the poverty threshold along with childcare subsidies and health insurance (2001). They find that this combination of factors led to substantive improvements in both school performance and social outcomes that were concentrated among boys.

Perhaps most encouraging is what we have learned from careful quasi-experimental studies of the two primary cash and near-cash assistance programs currently available to children in the United States: the Earned Income Tax Credit, which provides cash refunds to working families through the tax system, and the Supplemental Nutrition Assistance Program formerly known as Food Stamps, which provides vouchers that can be redeemed for food.5 The EITC was created in 1975 and currently provides a refundable tax credit to low-income working families through the tax system. Adults twenty-five and older without children are eligible for a small transfer, but a larger credit is available to families with children. Following a substantial expansion that took effect from 1993 to 1995, the maximum value of EITC benefits roughly doubled. In 2013, the EITC reached more than 21.6 million families with children, providing over $66 billion in benefits. These transfers are substantive: the average EITC benefit received by a family with two children in 2013 was $3,667.6

Several studies exploit the mid-1990s expansions of the Earned Income Tax Credit to create treatment and control groups of children who were living in otherwise similar families but received different income boosts because of when and where they were living or the size of the family in which they lived. Hilary Hoynes, Douglas Miller, and David Simon find that a $1,000 increase in income reduces the probability that a newborn is below the low birth weight threshold (2,500 grams) by 2 to 3 percent (2015). Kate Strully, David Rehkopf, and Ziming Xuan find that in states that adopted EITCs during the 1990s, the average birthweight of infants born to unmarried women with a high school degree or less increased by about sixteen grams (2010). These findings are important in part because birthweight predicts later life economic success: Sandra Black, Paul Devereux, and Kjell Salvanes estimate that a 10 percent increase in birthweight increases later life earnings by 1 percent (2007). A related study using variation across years in predicted EITC income finds that a $1,000 increase in family income raises a child’s math and reading test scores by 6 percent of a standard deviation (Dahl and Lochner 2012.7 Test score increases of this magnitude are also associated with substantive improvements in later life labor market outcomes: based on their review of the literature on the returns to school achievement, Patrick Kline and Christopher Walters suggest that one standard deviation increase in test scores likely generates an increase in earnings of at least 10 percent (2016).8 Indeed, a related study finds that adolescent exposure to the EITC improves later life education, employment and earnings outcomes (Bastian and Michelmore 2016). In their article in this issue, Shaefer and his colleagues (2018) also provide a review of the EITC literature.

The SNAP program provides vouchers to families that can be used to purchase food in grocery stores. In 2014, vouchers were received by 46.5 million people at a cost of $74.1 billion and average monthly benefits were $257 per household (Hoynes and Schanzenbach 2016). The amount of the voucher is intentionally low enough that it does not fully cover food purchases in most households; as a result, many argue that it should be thought of as a program that effectively provides low-income families with near-cash assistance because most families would spend at least as much on food as their SNAP benefit.9

In a series of studies, Hoynes and Diane Schanzenbach (and often Douglas Almond) make use of geographic variation in the timing of the initial rollout of the Food Stamp Program in the 1960s and early 1970s to compare outcomes among similar children with differential exposure to the program because of when and where they were born. Almond, Hoynes and Schanzenbach find that prenatal exposure to the Food Stamp Program leads to higher average birth weight and lower neo-natal mortality (2011).10 Relative to infants who did not have prenatal access, the incidence of low birth weight among exposed infants was about 7 percent lower for whites and 5 to 11 percent lower for blacks. Using the same research design in a later study, Hoynes, Schanzenbach, and Almond also examined longer-term outcomes and find that disadvantaged children with full access to the Food Stamp program from conception to age five experienced a 0.3 standard deviation reduction in metabolic syndrome (2016).11 Disadvantaged girls who were fully exposed during the first five years of life were also 0.2 standard deviations more likely to be self-sufficient in adulthood than those who did not have access (p-value was .14). Hoynes and her colleagues conclude that the increase in self-sufficiency and decrease in metabolic syndrome are largely driven by the effect of early life Food Stamp access on educational attainment (2016). Using the Continuous Work History Sample and rollout dates from Hoynes and Schanzenbach (2009), Marianne Bitler and Theodore Figinski find that for women born between 1955 and 1980, early life exposure to Food Stamps leads to small but statistically significant increases in earnings at age thirty-two (2017).

Using more recent program variation, Chloe East exploits changes in immigrant parents’ eligibility for Food Stamps across states and over time that followed passage of PRWORA (2016). She focuses on U.S.-born children of immigrants whose mothers had at most a high school degree. She finds that an additional year of parental eligibility in early childhood reduces the chance that the child is reported to be in poor, fair or good health (versus very good or excellent health) by 6 percent.

These studies make it clear that the benefits of cash and near-cash assistance may go well beyond short-term improvements in early childhood well-being. The long-term benefits are also widespread and include improvements in both adult health and economic success. Cash assistance interventions may also have a higher return than a simple accounting exercise would suggest because the associated improvements in later life health and earnings will be associated with later reductions in public expenditures on health care and welfare.

CASH AND NEAR-CASH ASSISTANCE IN THE UNITED STATES

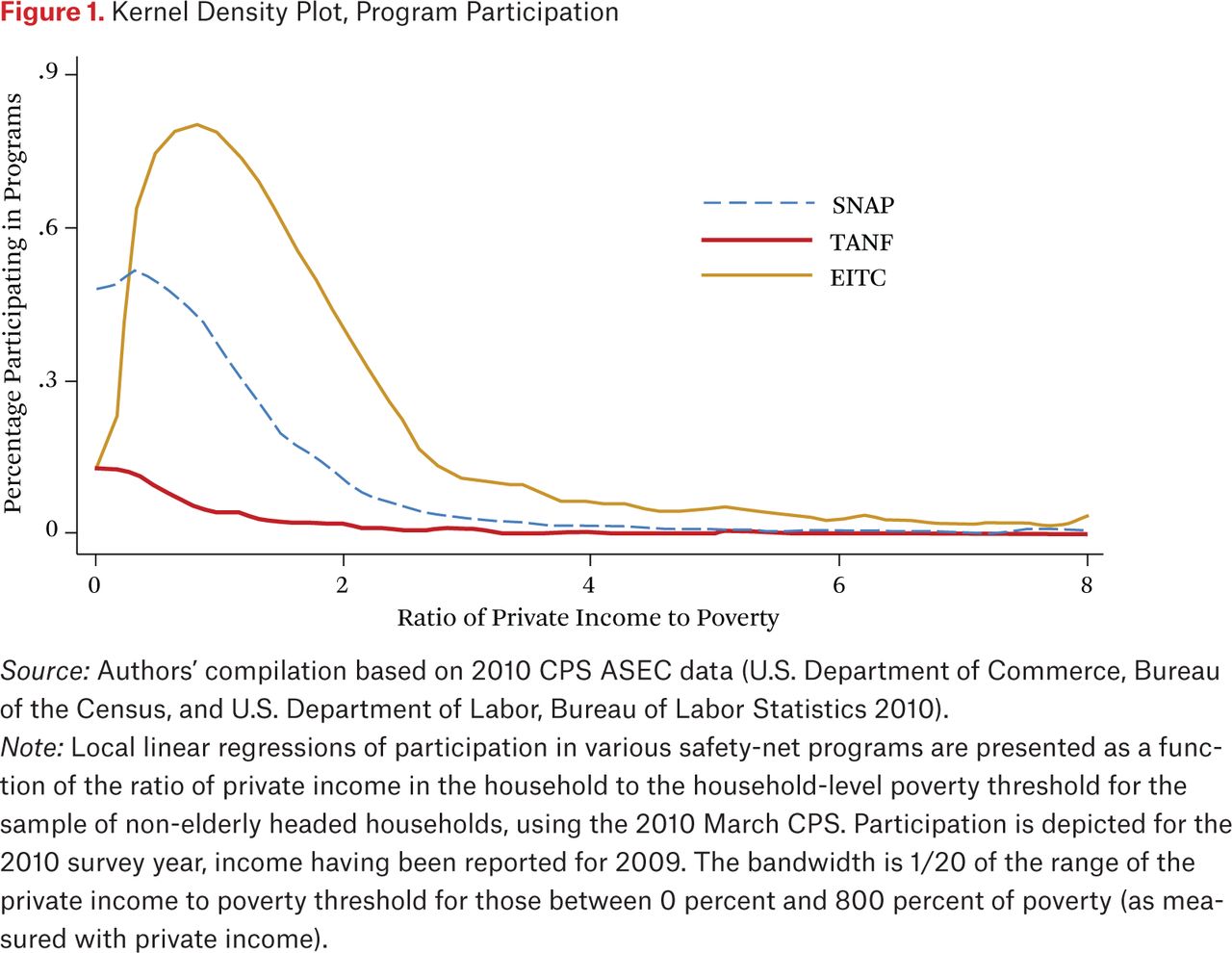

Despite evidence that cash and near-cash benefits that are provided through our existing safety net improve poor children’s outcomes, a significant number of poor children do not receive them. Figure 1 plots household participation in TANF, the EITC and SNAP as a function of the ratio of private income to poverty thresholds, using a sample of non-elderly families from the Current Population Survey.12 The figure makes clear that only families at the very bottom of the private income to poverty threshold distribution are getting cash assistance from TANF, and that even among the lowest income households, participation rates are very low: the TANF participation rate is below 15 percent in households with private income that is 50 percent of the poverty line, for example. SNAP and EITC participation rates are much higher and extend much further up the income to poverty distribution, yet even among the poorest households, SNAP participation rates do not exceed 60 percent.13 The EITC is the only program for which participation among families with incomes near the poverty threshold exceeds 60 percent. The EITC also reaches many near-poor households, including many with private income to poverty ratios that exceed 200 percent, but program benefits are largely missed by those at the very bottom of the income distribution.14

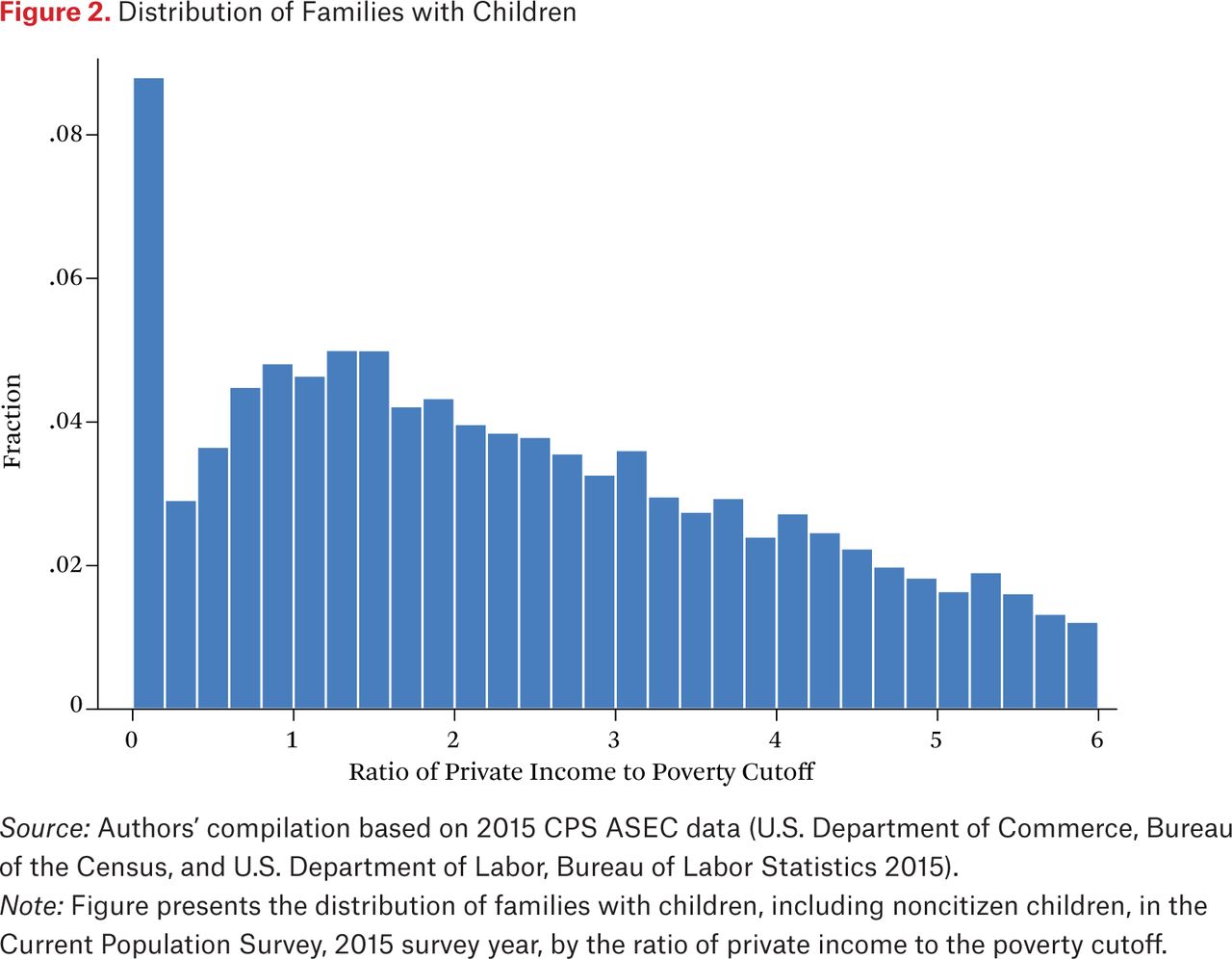

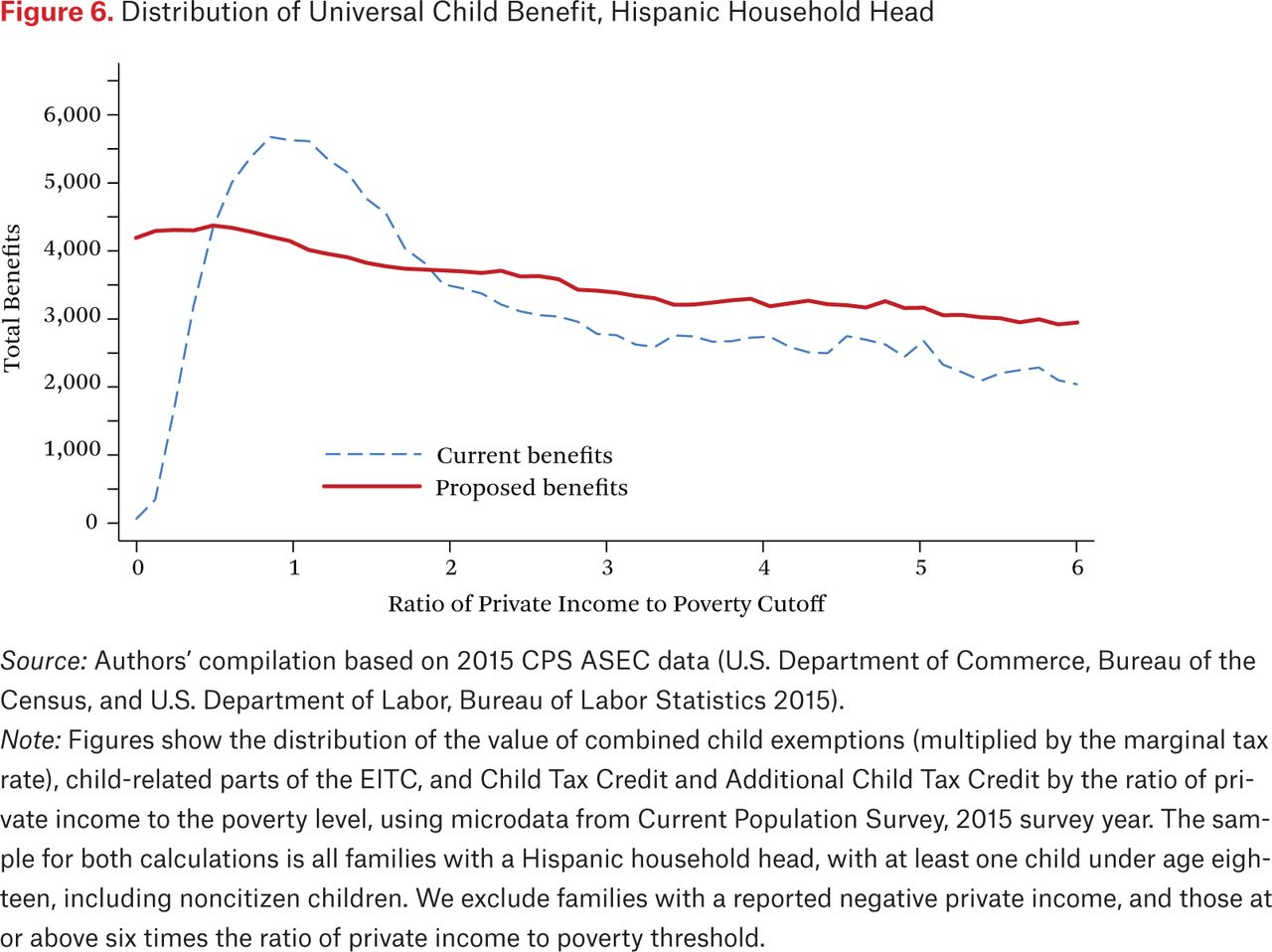

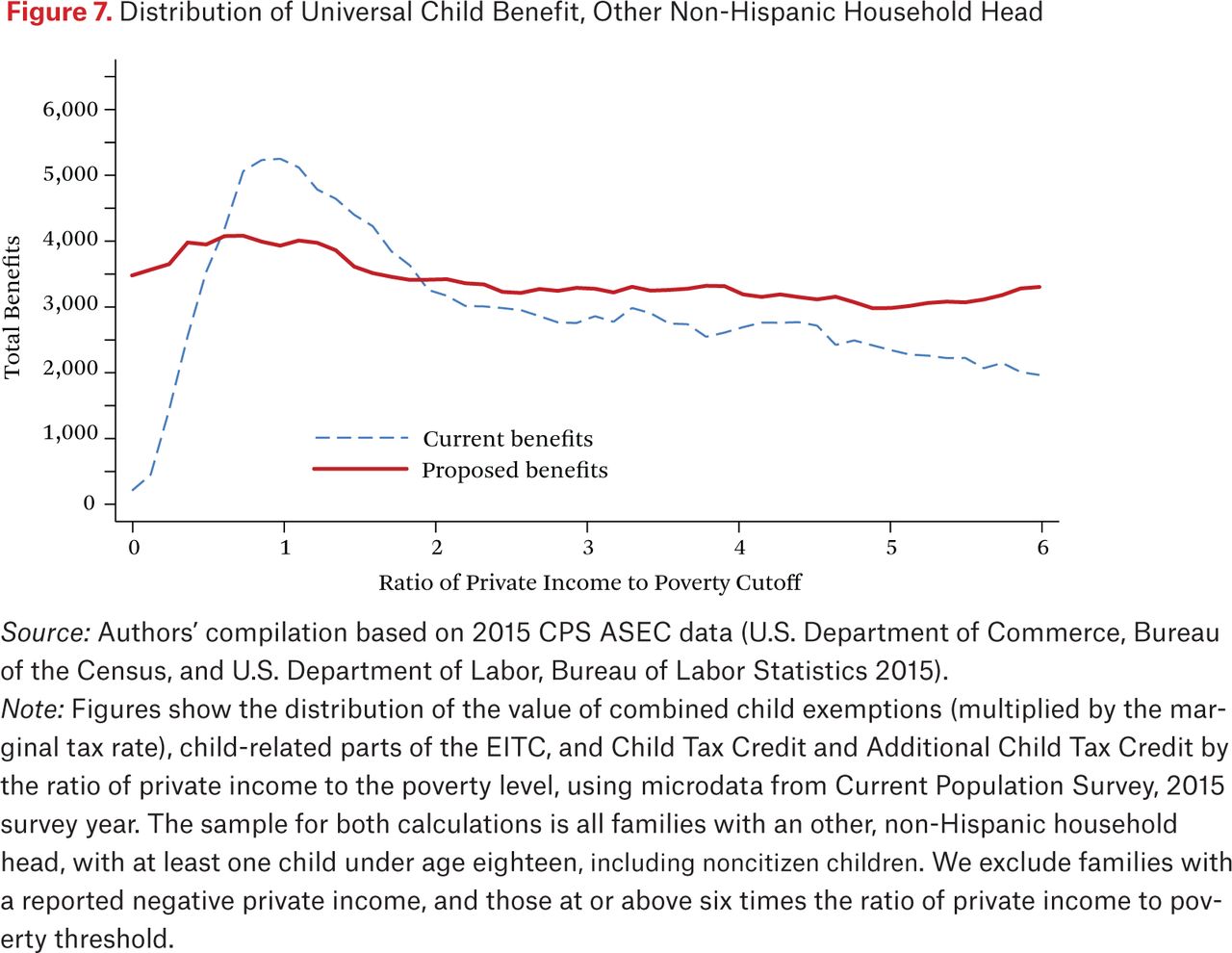

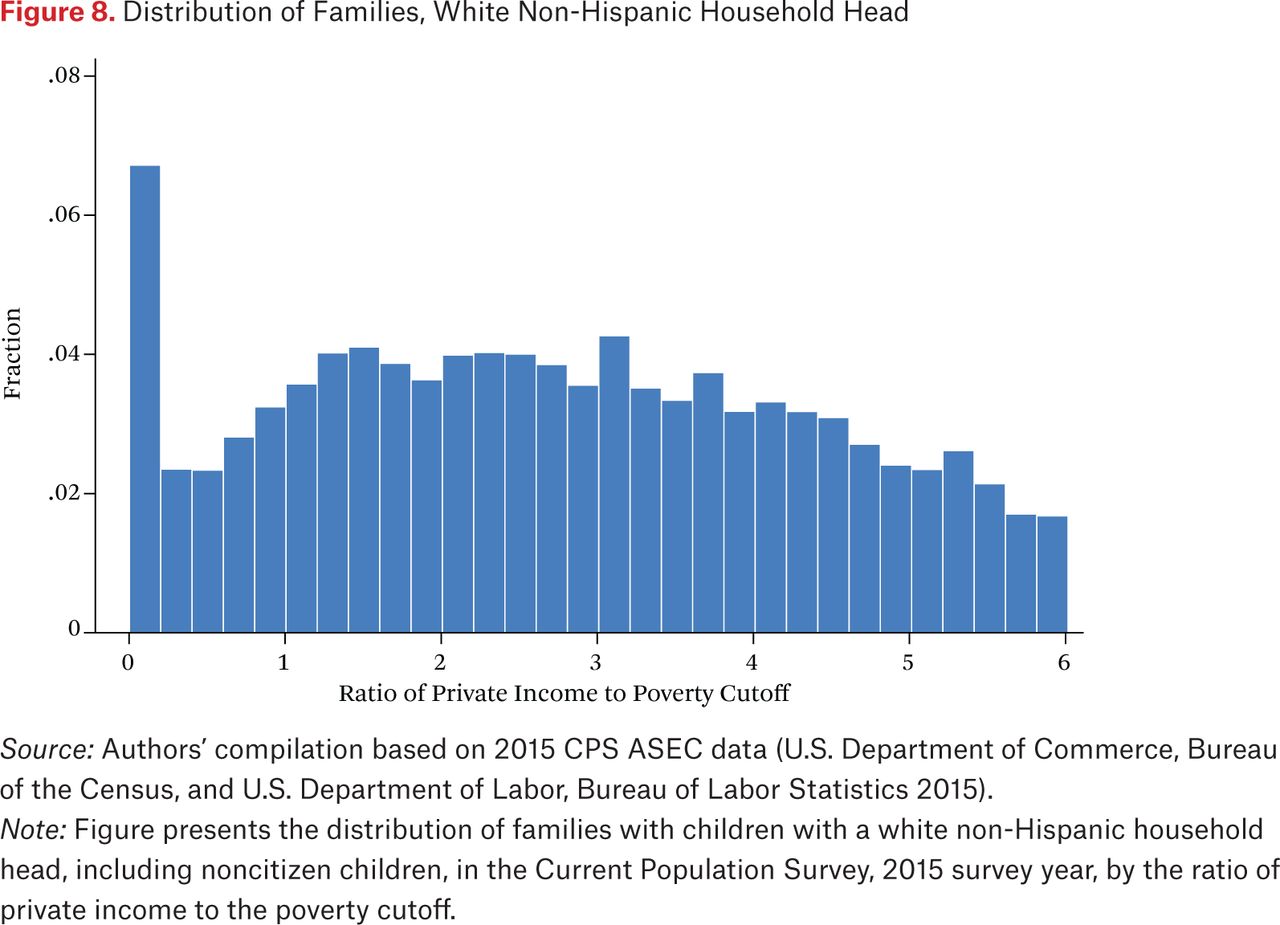

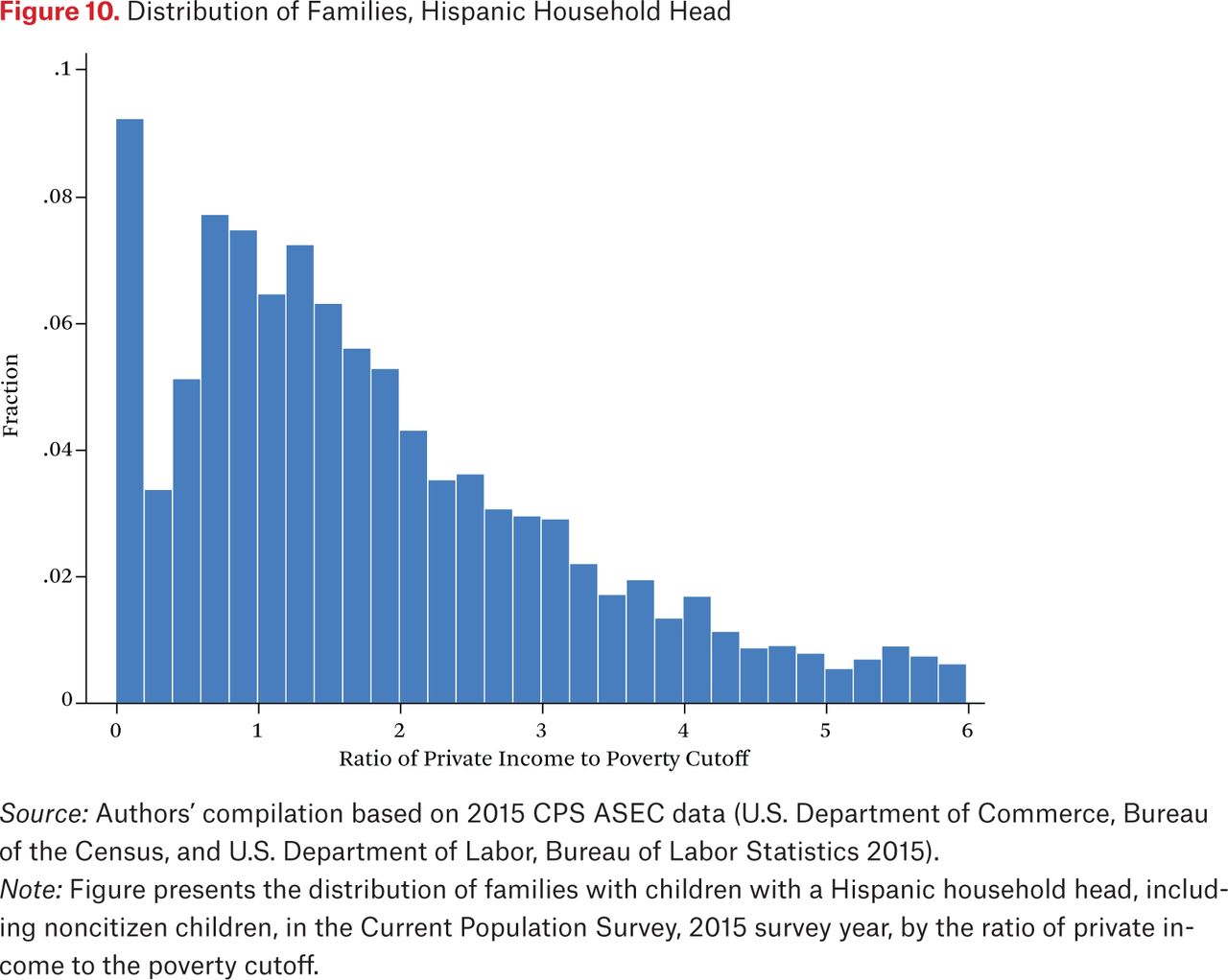

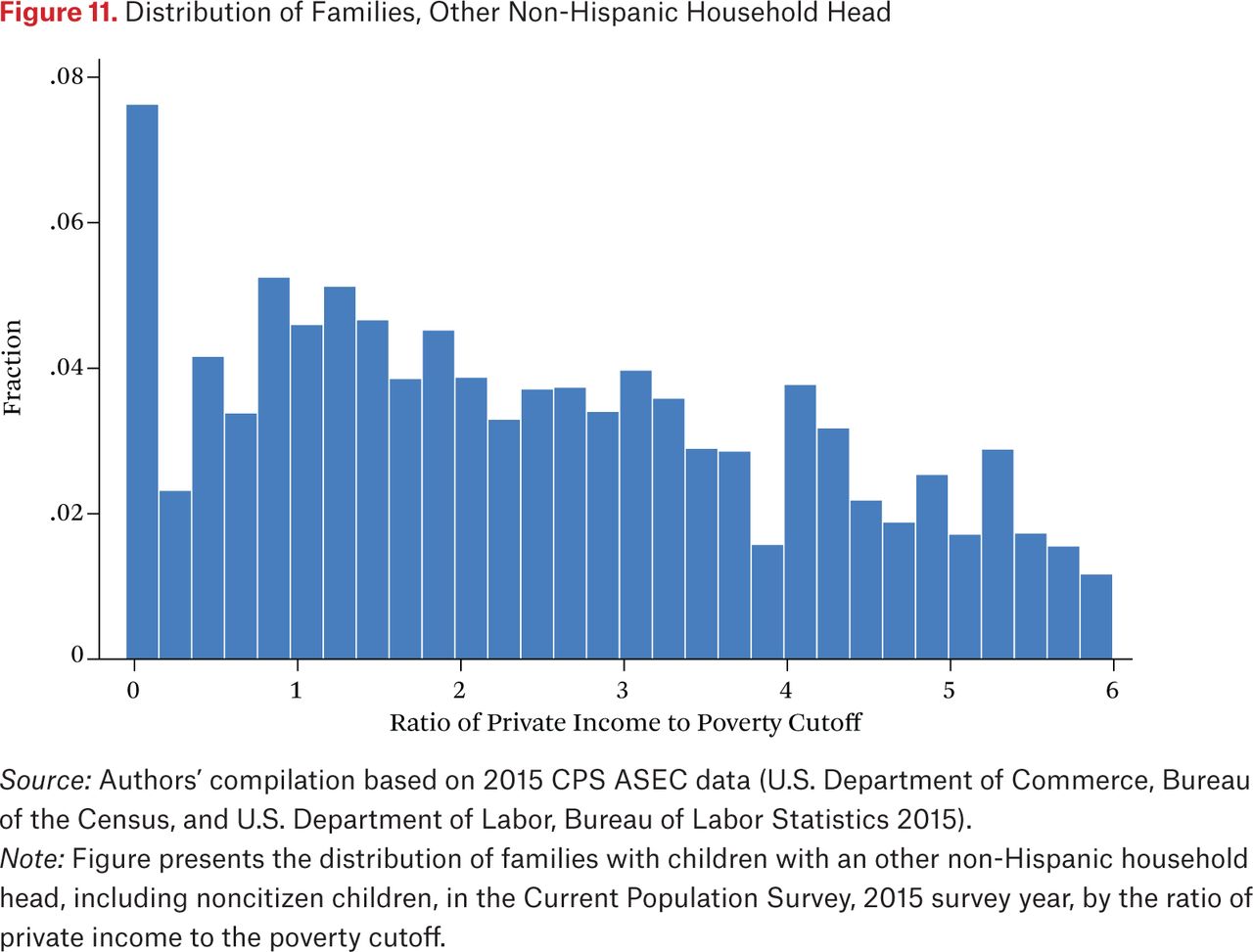

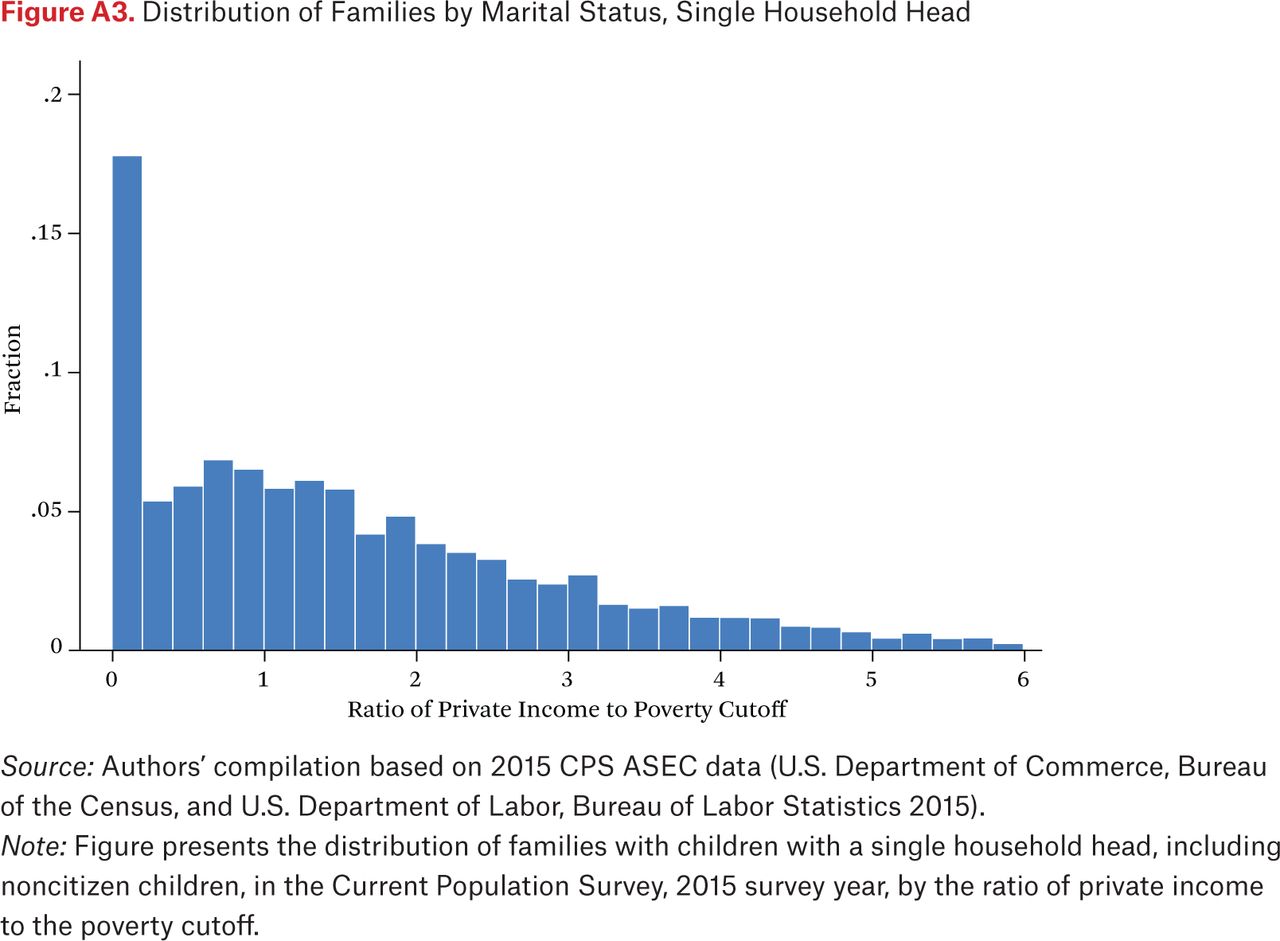

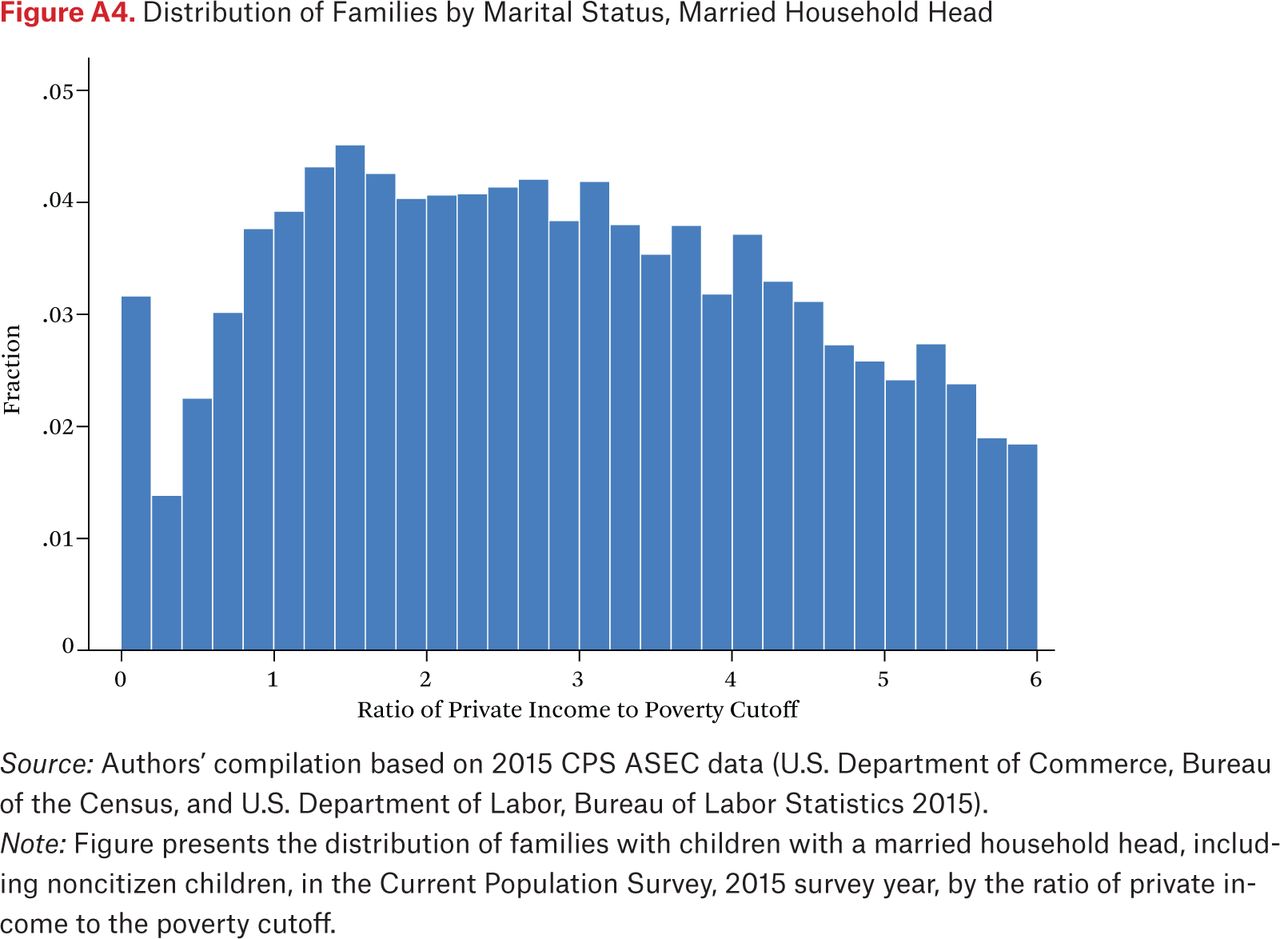

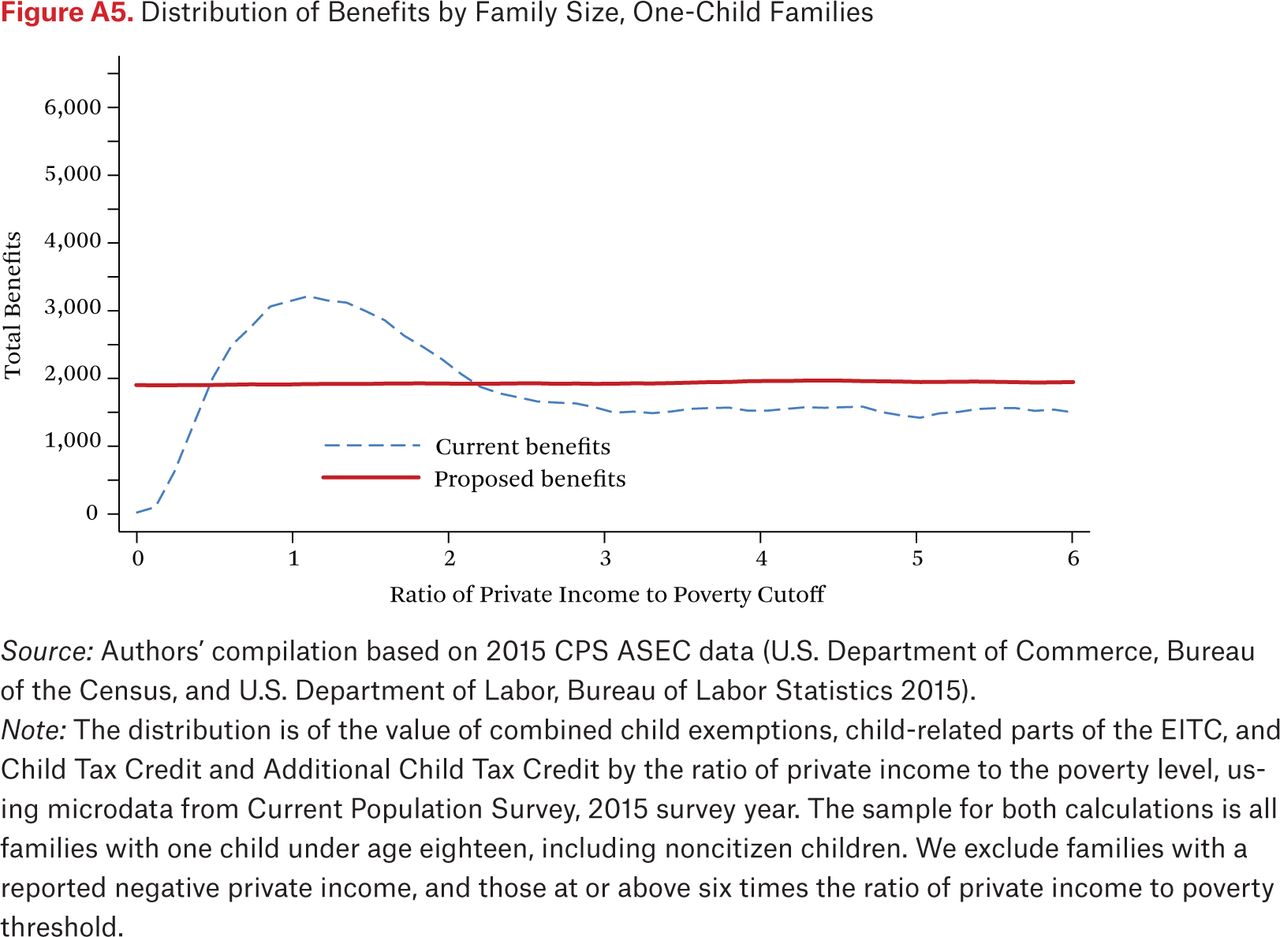

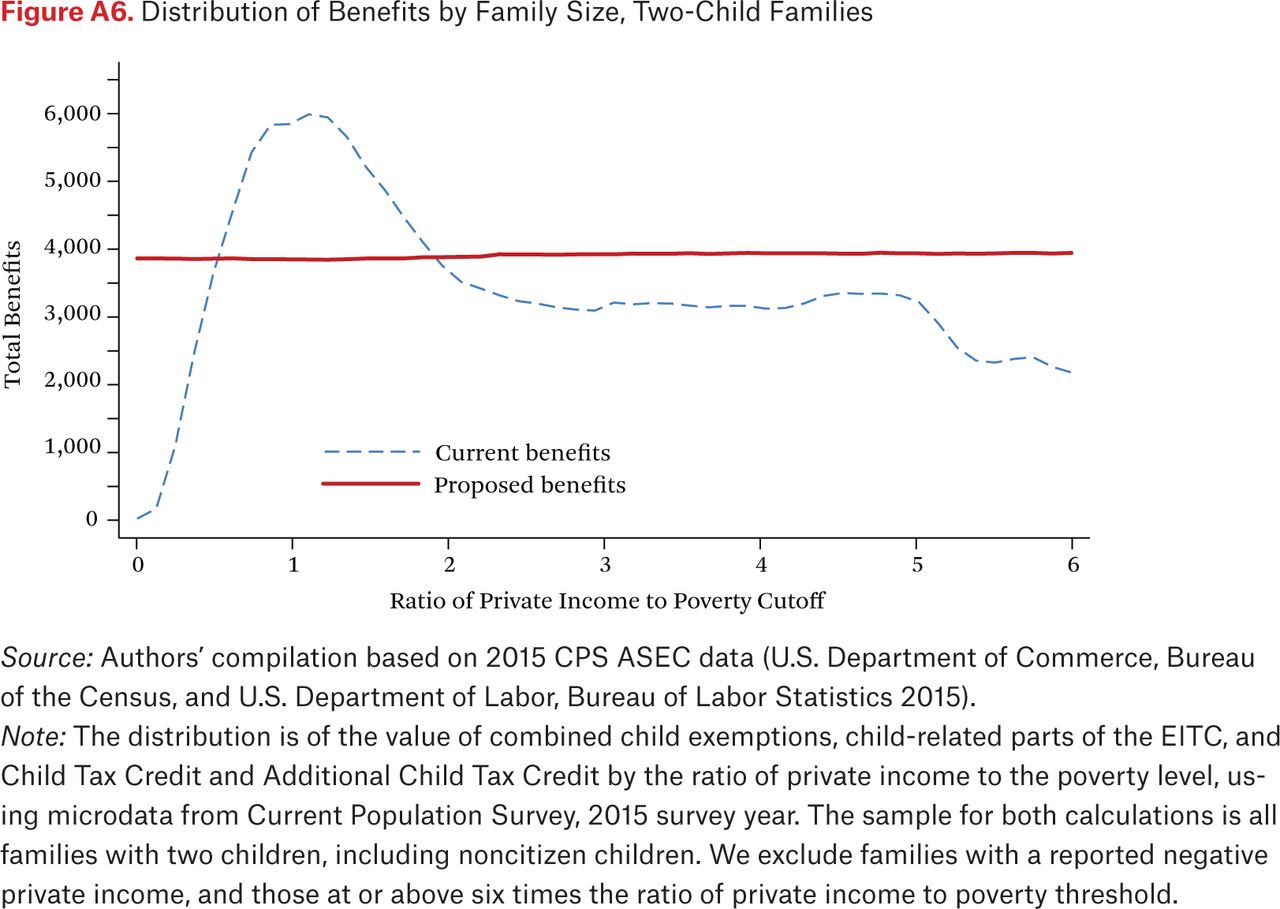

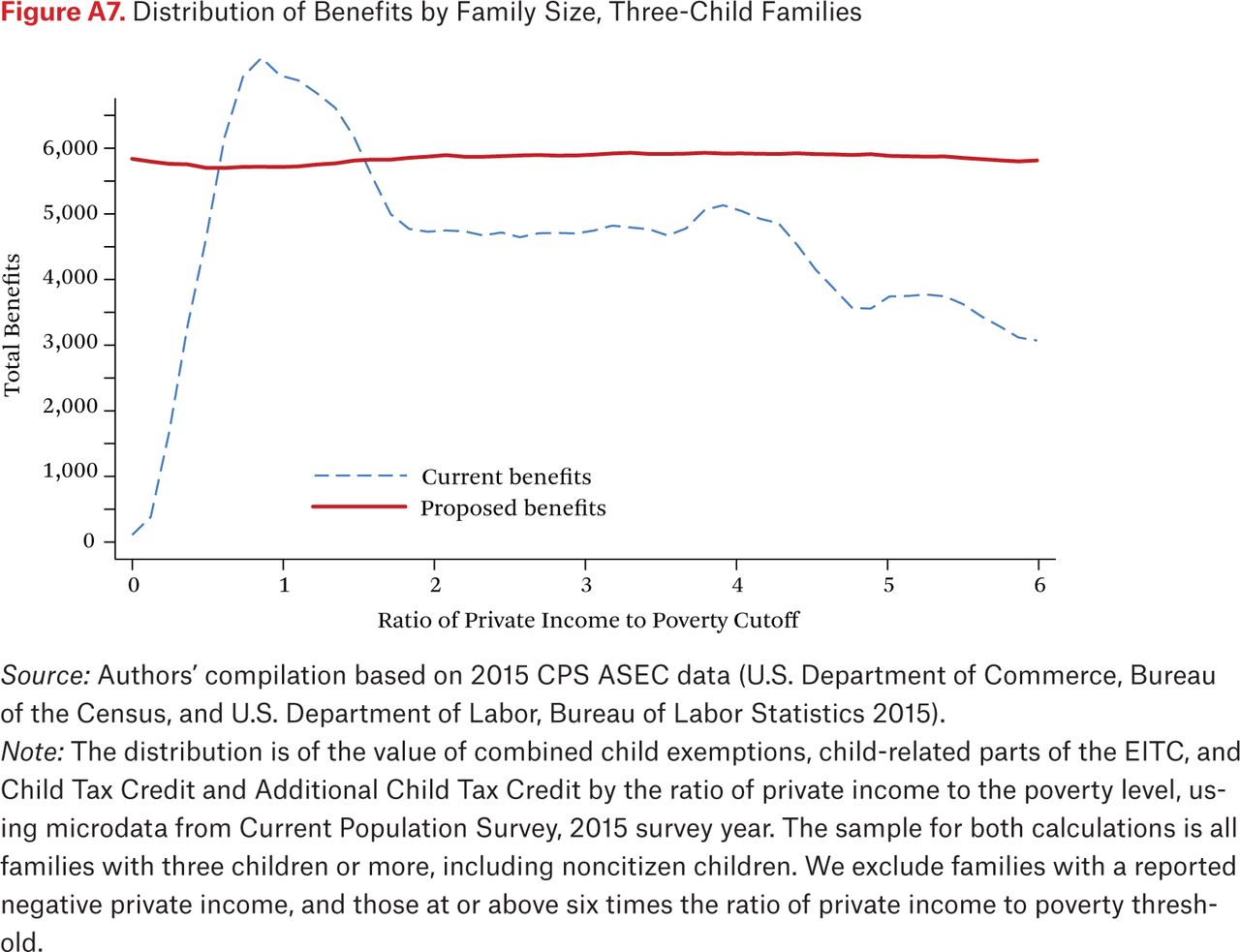

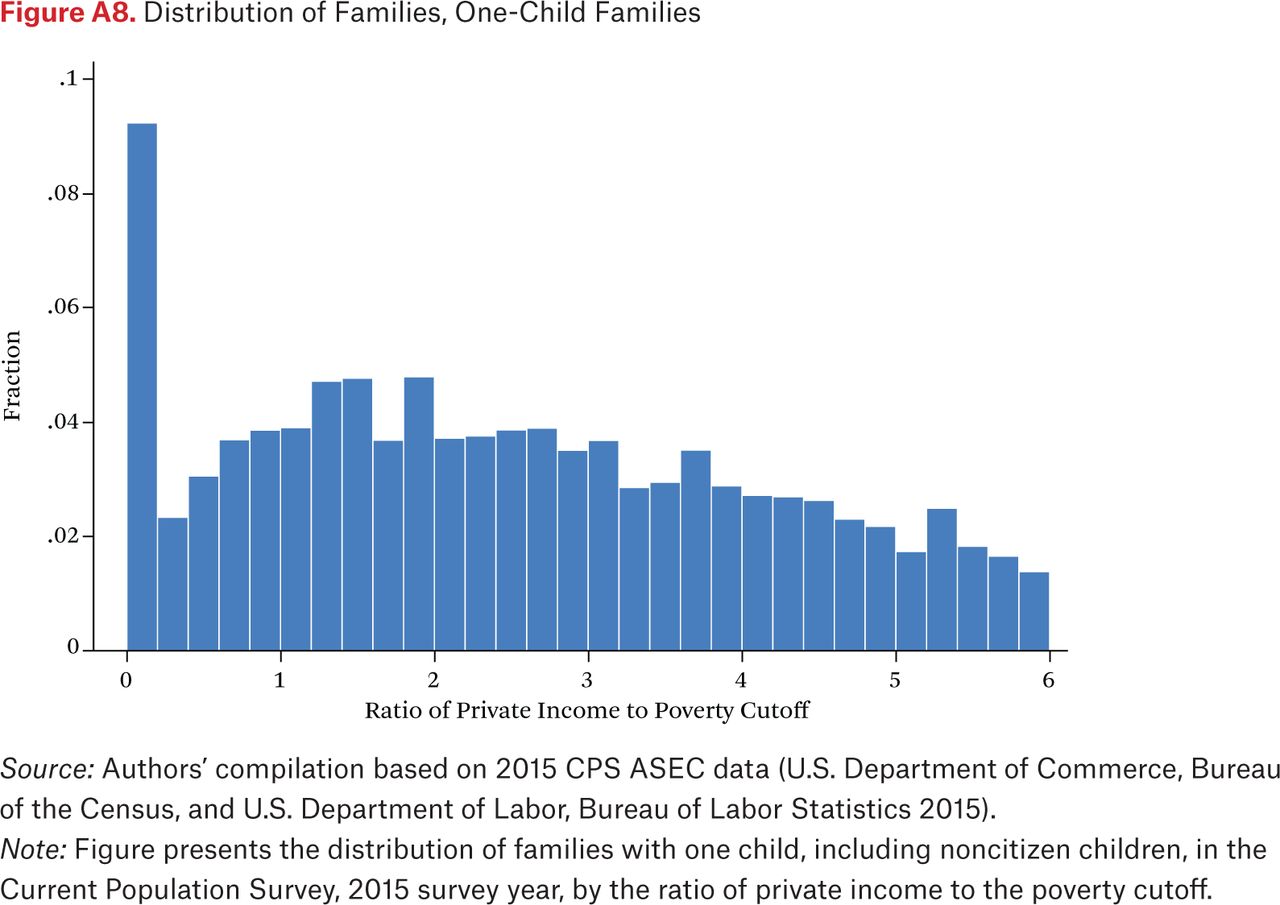

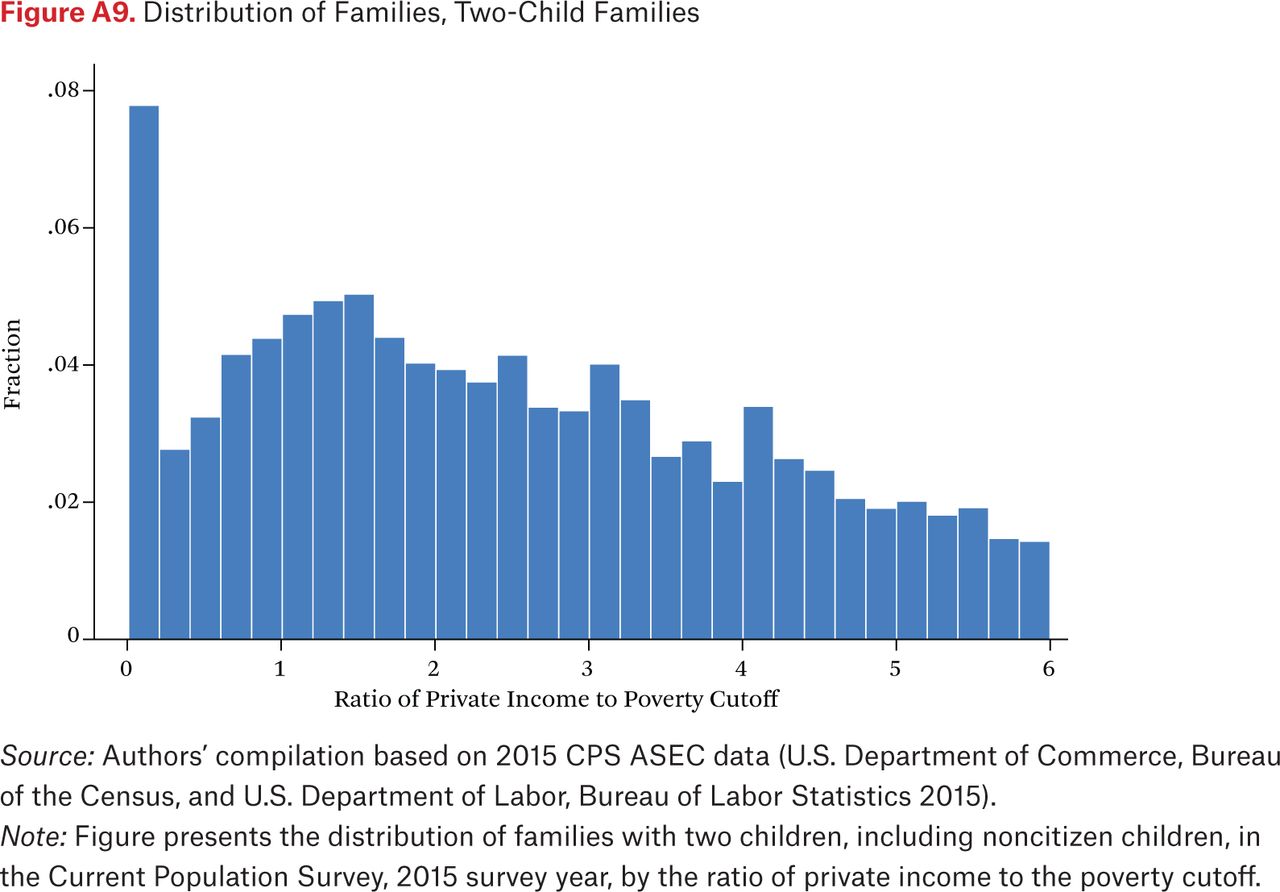

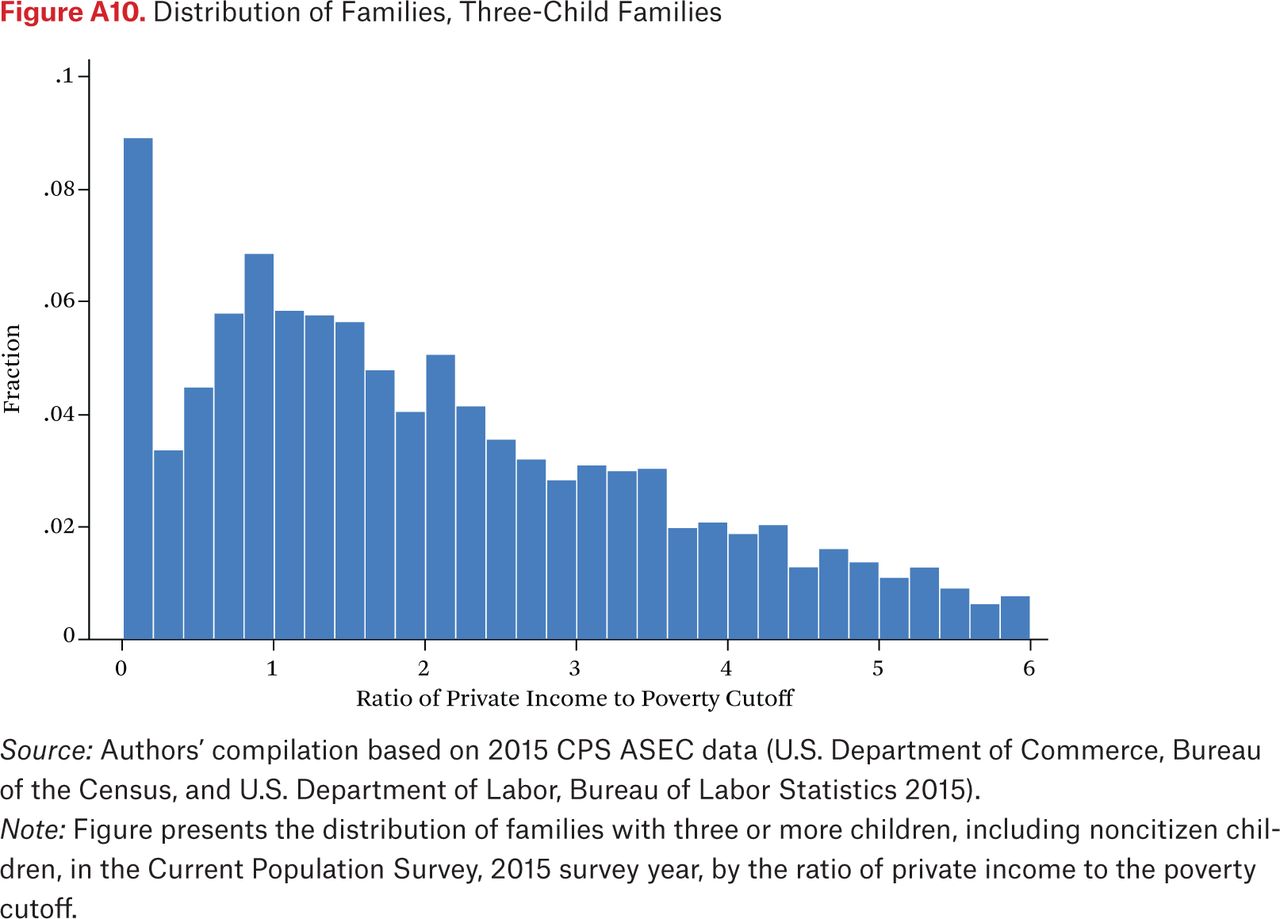

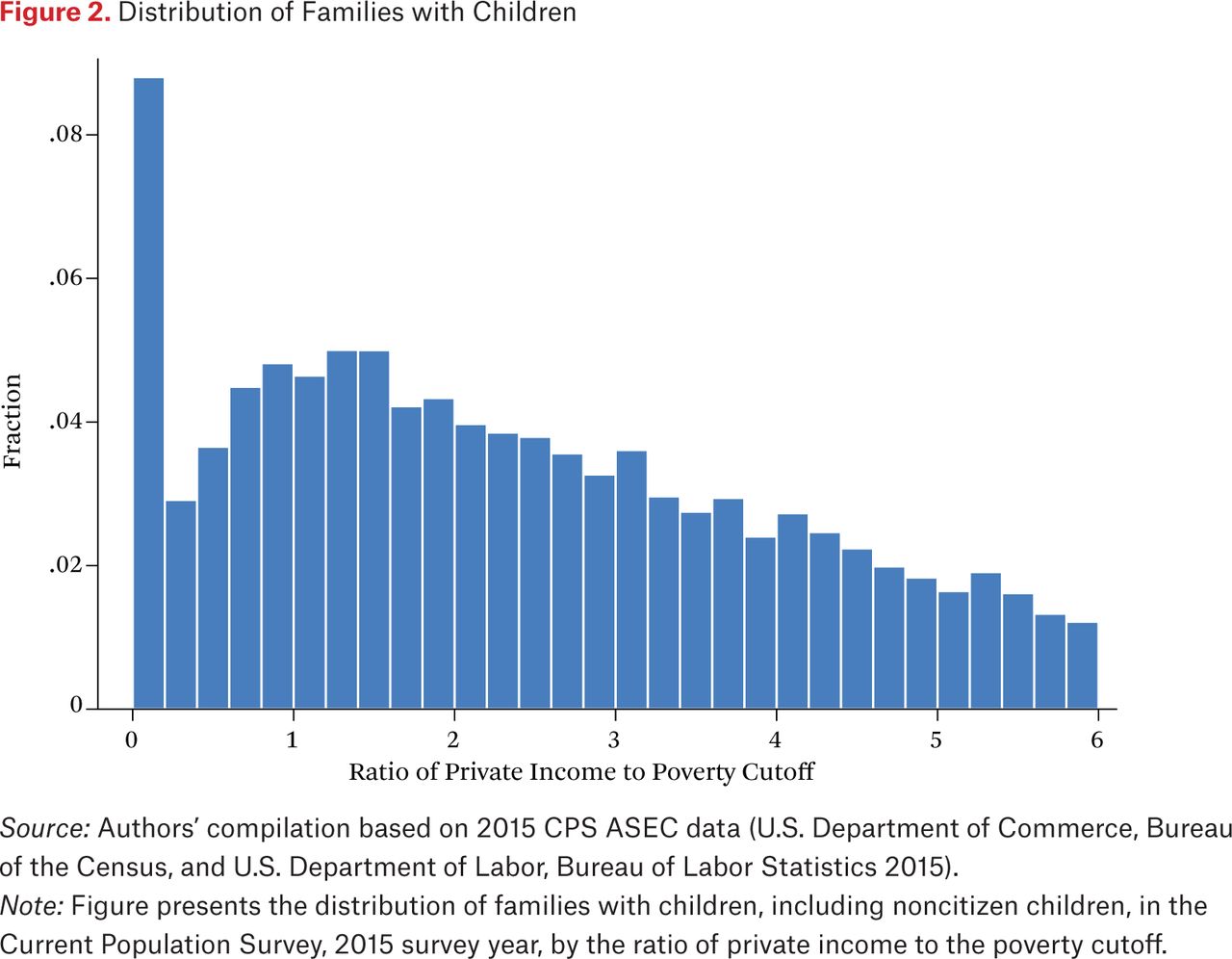

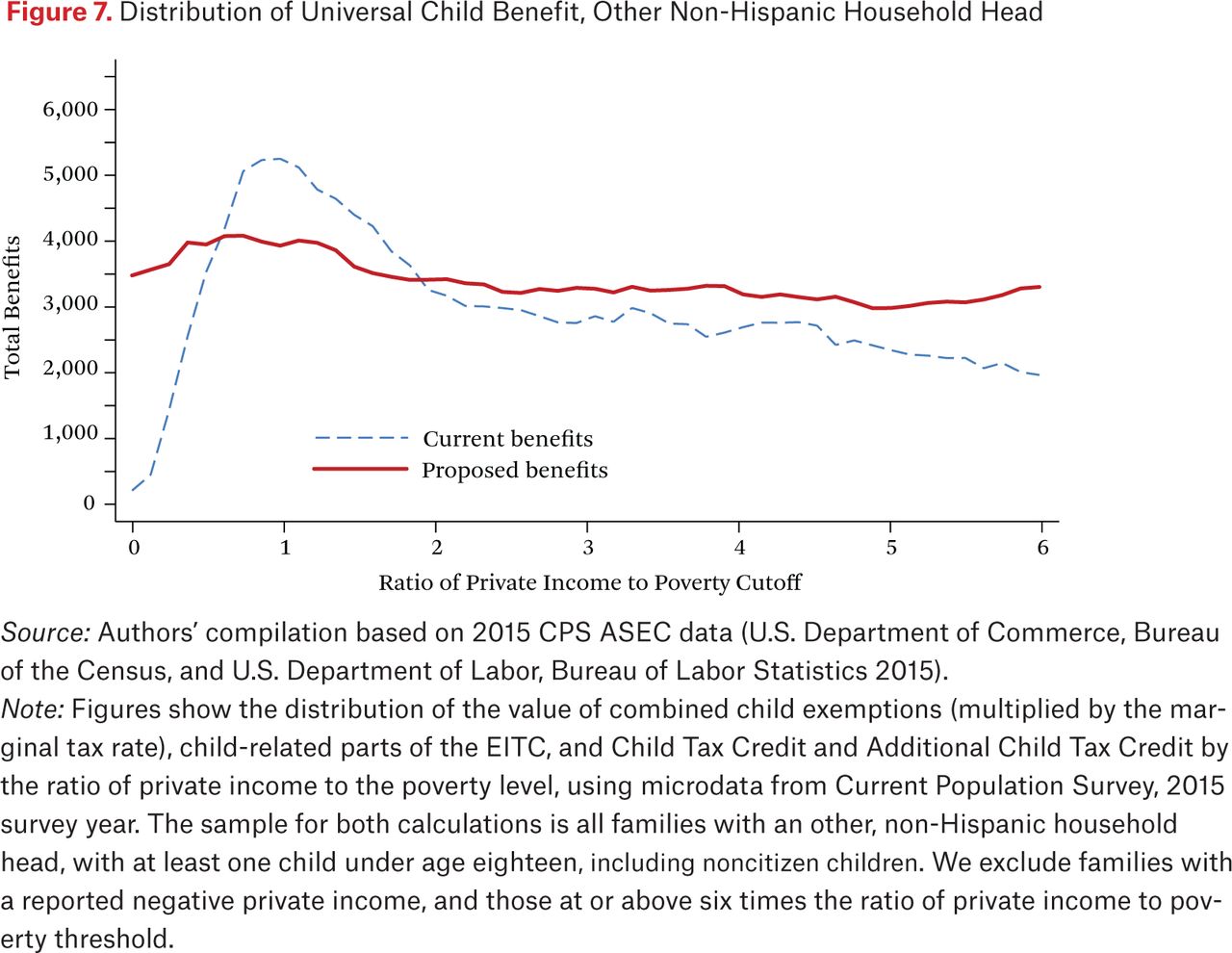

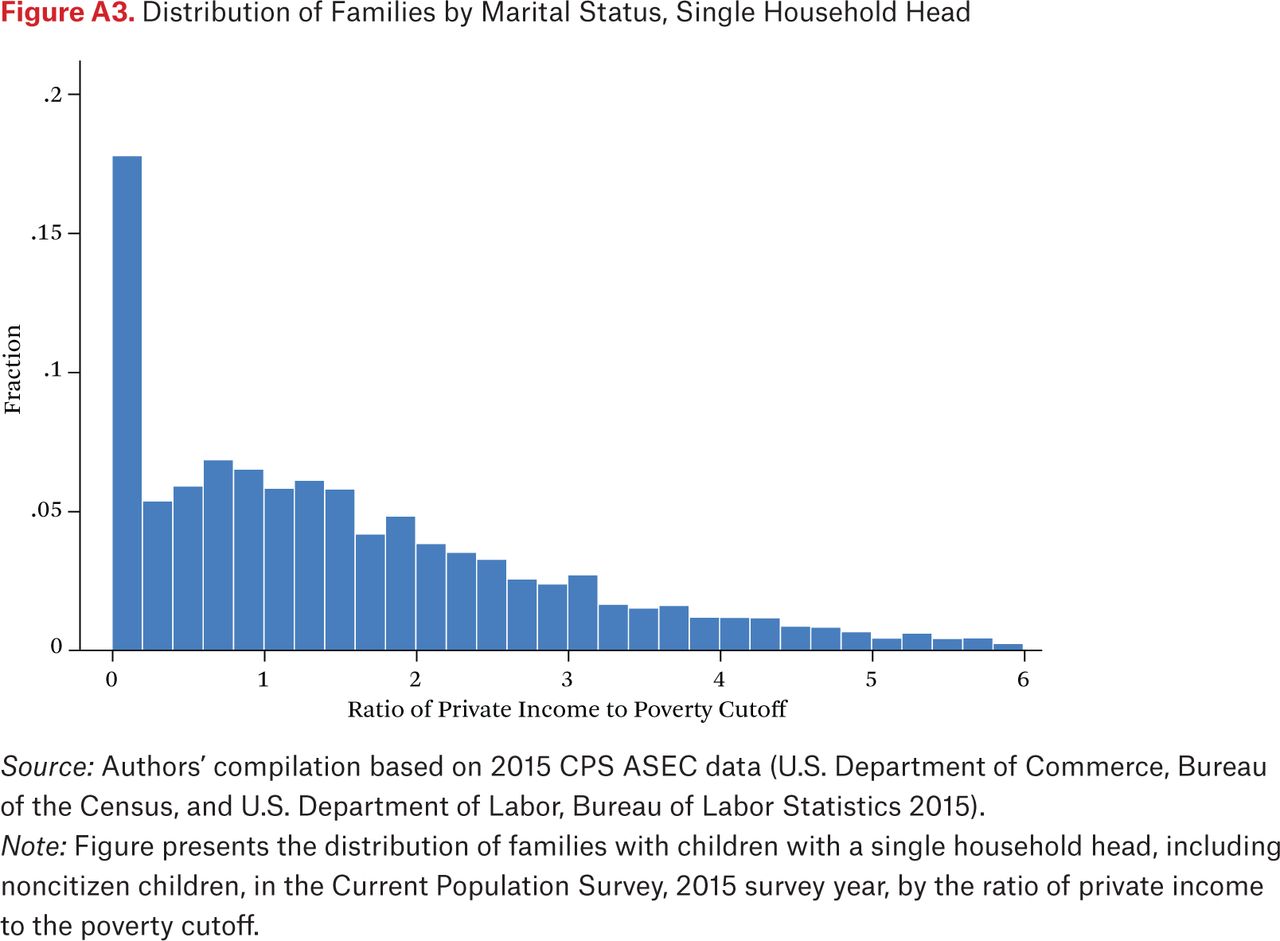

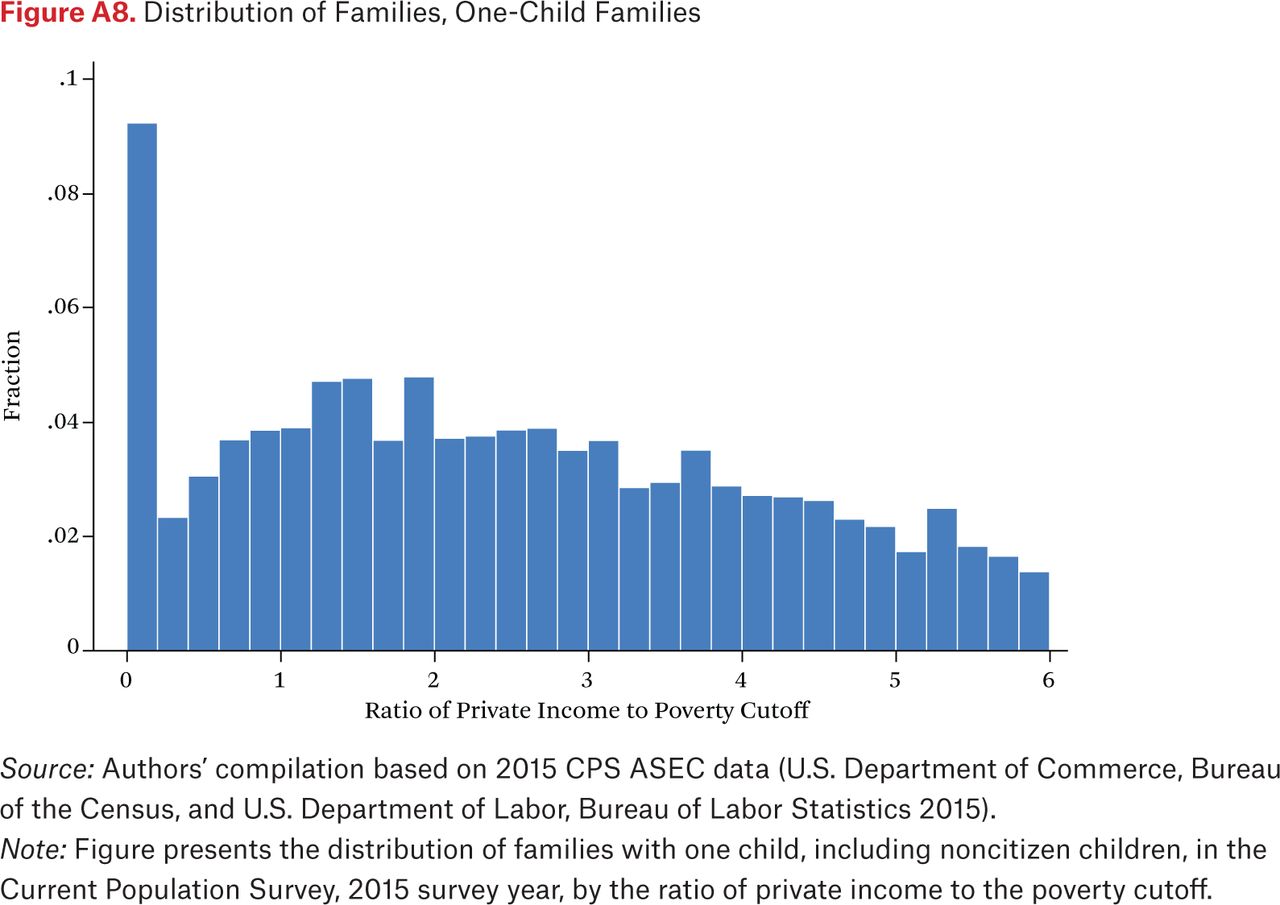

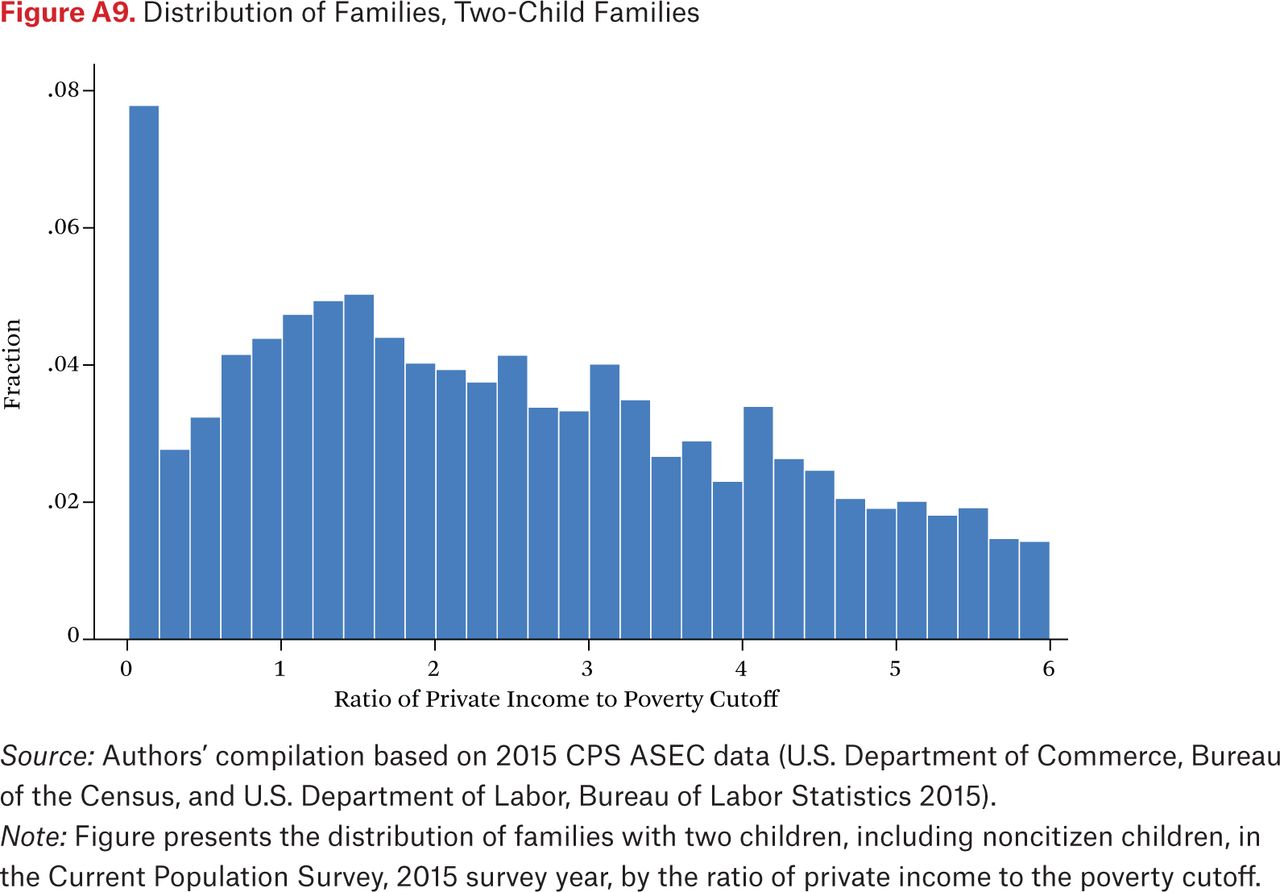

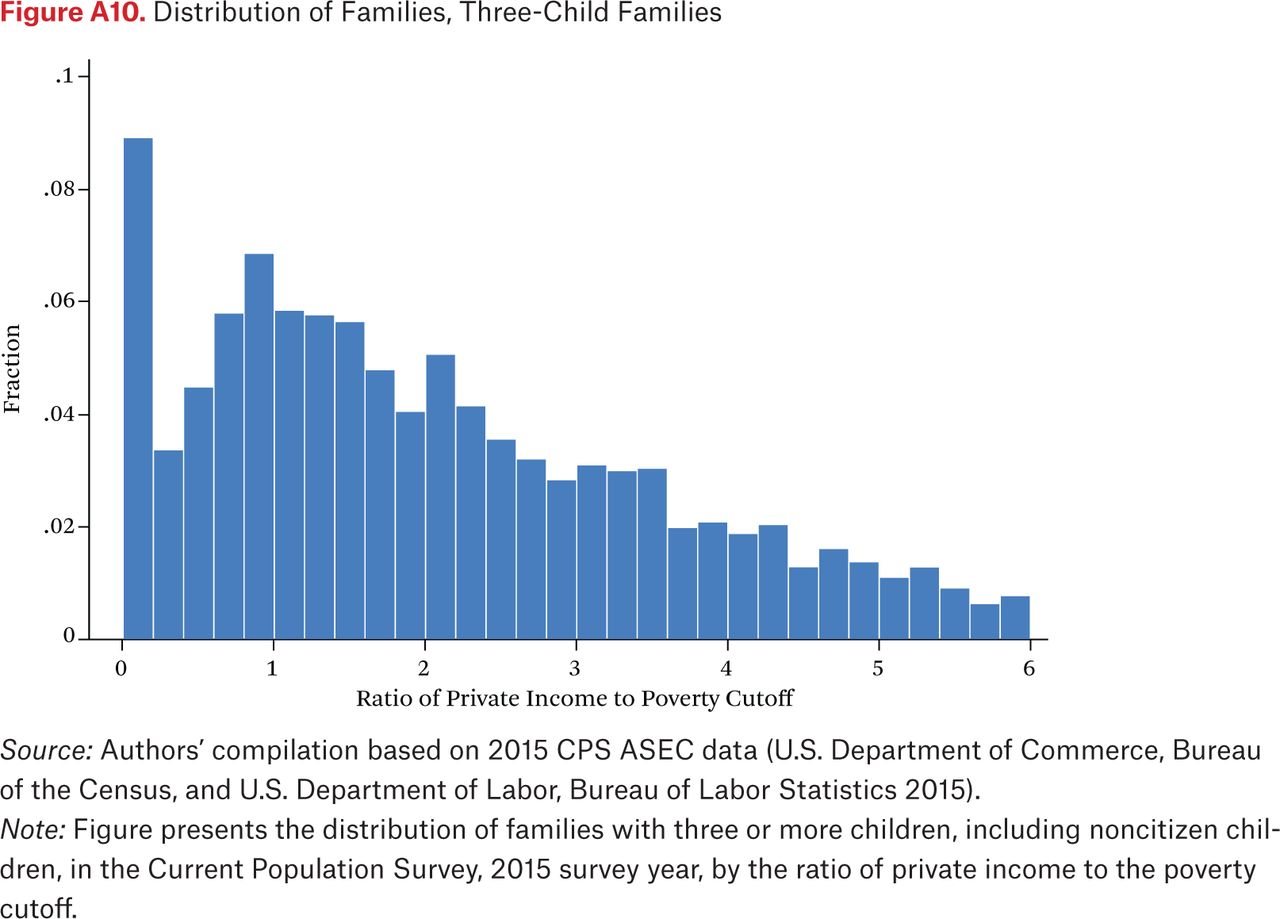

Figure 2 shows the distribution of families with children whose private income is below 600 percent of the poverty line, across the private income-to-needs distribution. When combined with figure 1, figure 2 makes clear that a nontrivial fraction of children live in families who are at substantial risk of falling through the cracks in our current safety net. In particular, more than 8 percent of these families have private incomes that are less than 20 percent of the poverty line, and almost 13 percent have incomes that are less than 50 percent. It is also important to notice that the distribution of families with children is not uniform across the distribution of income to needs, and there is a large point mass at zero. Figures 4 through 7 and figures A3 and A4 and A8 through A10 show similar distributions for subgroups defined by race of household head, family size, and parents’ marital status.

Together, these figures make clear that our major cash and near-cash assistance programs miss a nontrivial number of poor children, particularly those children living in the poorest families. This results from several factors. First, the EITC is tied to employment, so children whose parents are unable (or unwilling) to work cannot receive the substantial income boost that it provides. Second, even children whose parents have positive earnings cannot receive EITC benefits unless their parents file a tax return. Previous studies indicate that approximately 16 percent of those who are eligible for the EITC may be in this nonfiler category, and that two-thirds of EITC-eligible nonparticipants do not file taxes (Plueger 2009). Low take-up of EITC benefits may result from lack of information regarding eligibility (Bhargava and Manoli 2015). Moreover, it is well known that the tax code is complicated and difficult to understand (Chetty, Friedman, and Saez 2013; Chetty and Saez 2013; Feldman, Katuscak, and Kowano 2016; Liebman and Zeckhauser 2004).

Without access to EITC benefits, the primary source of near-cash assistance available to poor children without disabled parents is SNAP, which provides an average monthly benefit of about $125 per person. As with the EITC, however, some eligible children do not receive SNAP benefits, at least in part because negative identity cues and stigma often accompany participation in means-tested programs (Bertrand, Mullainathan, and Shafir 2004; Moffitt 1983). Less than universal SNAP take-up may also result from the difficulties that low-income families face when they attempt to navigate the larger set of U.S. welfare programs and their varying rules, which in turn depend on different income concepts and family-unit definitions, and induce a dizzying host of marginal tax rates. There are also substantive “hassle” costs associated with participating in the safety net because families are often required to visit a variety of offices to register for different programs, and must know where to go and what information to bring along. Receipt of SNAP benefits sometimes requires fingerprints, and SNAP applications can be as long as thirty-six pages.15 Taken together, these factors may push the stress and cognitive-load limits of many would-be participants (Bertrand, Mullainathan and Shafir 2004). In the face of these challenges, individuals’ “bandwidth” for optimal decision making may be seriously constrained (Schilbach, Schofield, and Mullainathan 2016). Finally, as with the EITC, many families may simply be unaware that they are eligible for SNAP (Daponte, Sanders, and Taylor 1999).

A BROADER AND SIMPLER CASH ASSISTANCE PROGRAM

We propose a broader and simpler cash assistance program that reaches more children. Our program would track all citizen children under eighteen (through their Social Security numbers or birth certificates), and all of their families would automatically be sent a monthly, nontaxable, lump-sum benefit based on the number of children in the family.16 We focus on citizen children for administrative simplicity because noncitizen children are less easily identified and tracked with existing administrative systems. The universal child benefit would not depend on any other parameters and it would not be counted against other means-tested benefits. An income supplement of this type would be devoid of stigma because it would be provided to all citizen children, and would substantially reduce informational burdens and hassle costs.17 Families would not need to file a tax return or be evaluated for eligibility by a social worker. It would be vastly simpler than the current patchwork system of tax credits and deductions, making it easier for needy families to participate and would eliminate confusion associated with different definitions of children across credits. The lump-sum benefit would be distributed on a monthly basis to provide stability and help families accommodate unanticipated shocks that are far removed in time from the disbursement of one annual benefit.

Existing studies suggest than an annual benefit of $2,000 per child would be more than enough to provide meaningful impacts.18 This would also yield an increase in family income comparable to the average assistance currently provided to two-child families through the EITC. As described, a $1,000 increase in EITC income is associated with a 2 to 3 percent reduction in the probability that a newborn is below the low birth weight threshold (Hoynes, Miller, and Simon 2015). An additional $1,000 raises a child’s achievement scores by about 5 percent of a standard deviation (Duncan, Morris, and Rodrigues 2011; Dahl and Lochner 2012). Existing studies also find that improvements in children’s health and academic achievement of this magnitude are predictive of economically meaningful increases in later life economic success (for example, Kline and Walters 2016).

A frequent concern with government income transfers is that they reduce work incentives. Evidence suggests that a universal child benefit would be unlikely to generate large reductions in parental work effort, however. Recent work by Ben-Shalom, Moffitt, and Scholz 2012, for example, finds that most major means-tested transfer programs do not meaningfully reduce hours of work.19 Programs that do appear to reduce labor supply are generally associated with either a high earnings tax rate or with sharp discontinuities that cause complete elimination of benefits with an additional dollar of earnings. In contrast, Hoynes and Schanzenbach estimate quite modest earnings reductions in conjunction with rollout of the Food Stamp program, which had a nontrivial benefit reduction rate (2012).20 The universal child benefit would not impose an earnings tax. Moreover, as noted, many beneficiaries would be children whose parents are not currently working.

A $2,000 per child lump-sum benefit would cost the federal government approximately $142 billion per year and would reach the 24.5 percent of families with children under eighteen who have private incomes below the poverty line but currently receive no support through the tax system or from SNAP.21 The cost of providing this income supplement could be reduced by phasing it out among high-income families.

An income transfer of this magnitude could also be sustained without substantially increasing the level of government expenditures by repurposing funds currently devoted to the CTC (and Additional Child Tax Credit, ACTC), the child dependent exemption, and the child-related parts of the EITC.22 This would have the clear political advantage of maintaining revenue neutrality (and allow the Congressional Budget Office or Joint Committee on Taxation to score it accordingly), and would redirect government assistance from higher-income families toward children living in the most disadvantaged families. The long-standing child exemption—which currently provides families with approximately $600 per child, per year—is not available to non–tax filers, and largely benefits families with incomes above the poverty line.23 Moreover, the magnitude of the benefits received through the child exemption is larger for families who face higher marginal tax rates. The CTC (nonrefundable) and ACTC (refundable) jointly provide qualifying families with benefits of up to $1,000 per child under age seventeen. Like the child exemption, the CTC primarily benefits middle-income families.24 The ACTC and EITC do play a substantive role in poverty alleviation (Hoynes and Rothstein 2016), but for families with two children the maximum benefits allowed through these combined programs are comparable to the value of the lump-sum transfer that would replace it.

We document our proposal’s feasibility by leveraging 2013 Internal Revenue Service (IRS) Statistics of Income (SOI) tax data (2013a, 2013b). Details behind our calculations are described in the online appendix and shown in online table A1. Approximately $27.2 billion would be available from repurposing the CTC, and another $27.9 billion from the ACTC. We do not propose repurposing child exemptions that are currently available for disabled dependents or for older children away at college. Funds from the child exemptions would, therefore, yield about $42 billion. Together, funds repurposed from the CTC, the Additional CTC, and the child exemptions total $97 billion.

We also calculate how much would be available if we repurposed the child-related portion of the EITC without eliminating the part of the EITC earnings subsidy currently provided to families without children. This part of the EITC would continue to be available to all working adults. As before, our proposal would hold constant all EITC funds that go to families with disabled dependents or with older children in college. We calculate that the child-related part of the EITC would yield $54 billion of available funding. Combining these sources, the total amount repurposed for our child benefit would be $151 billion. We divide this estimated funding amount by the total number of children, and inflate to 2015 dollars, yielding an estimated annual benefit of approximately $2,000 per child. Our estimate of the average EITC benefit received by a family with two children is $3,667. Our estimate of the average EITC benefit received by a family with three or more children is $4,022. Thus, our alternative cash assistance program would provide all families with two children additional income similar to or larger than the amount they currently receive (on average) from the EITC. Families with more children would receive larger benefits. One-child families would, on average, receive less than they do under the current system. These static estimates are based on the assumption that there would be no accompanying changes in parents’ labor force participation or earnings.

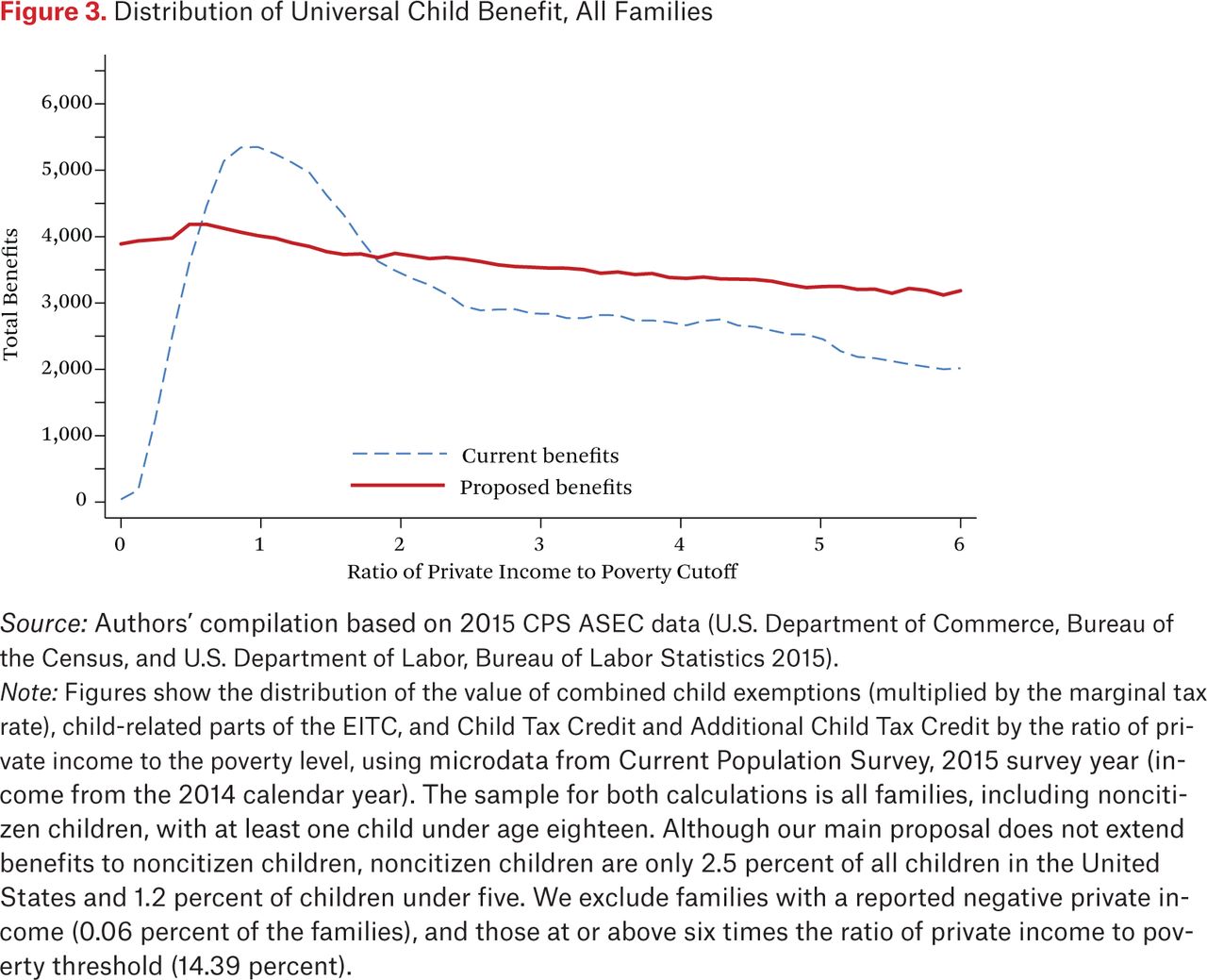

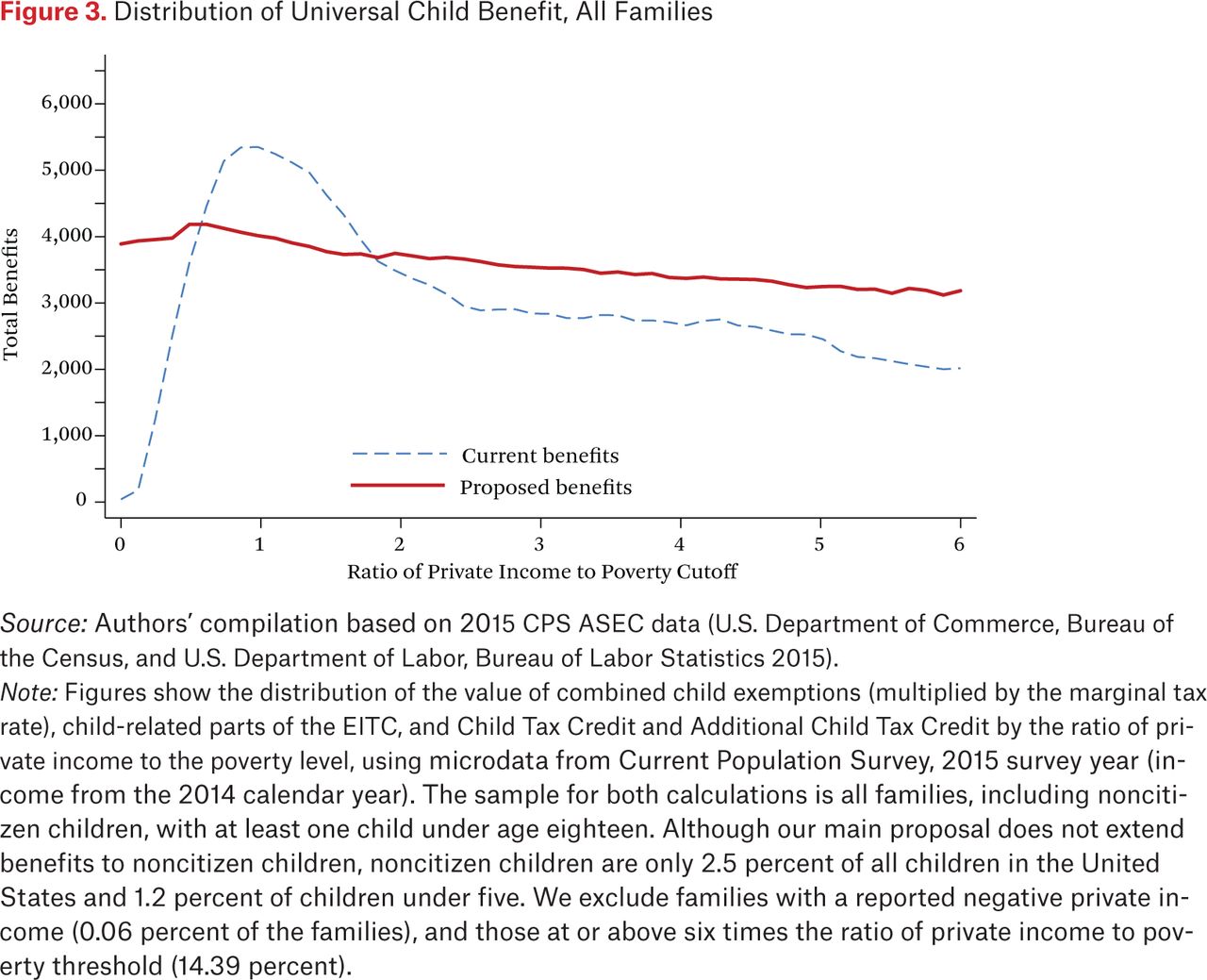

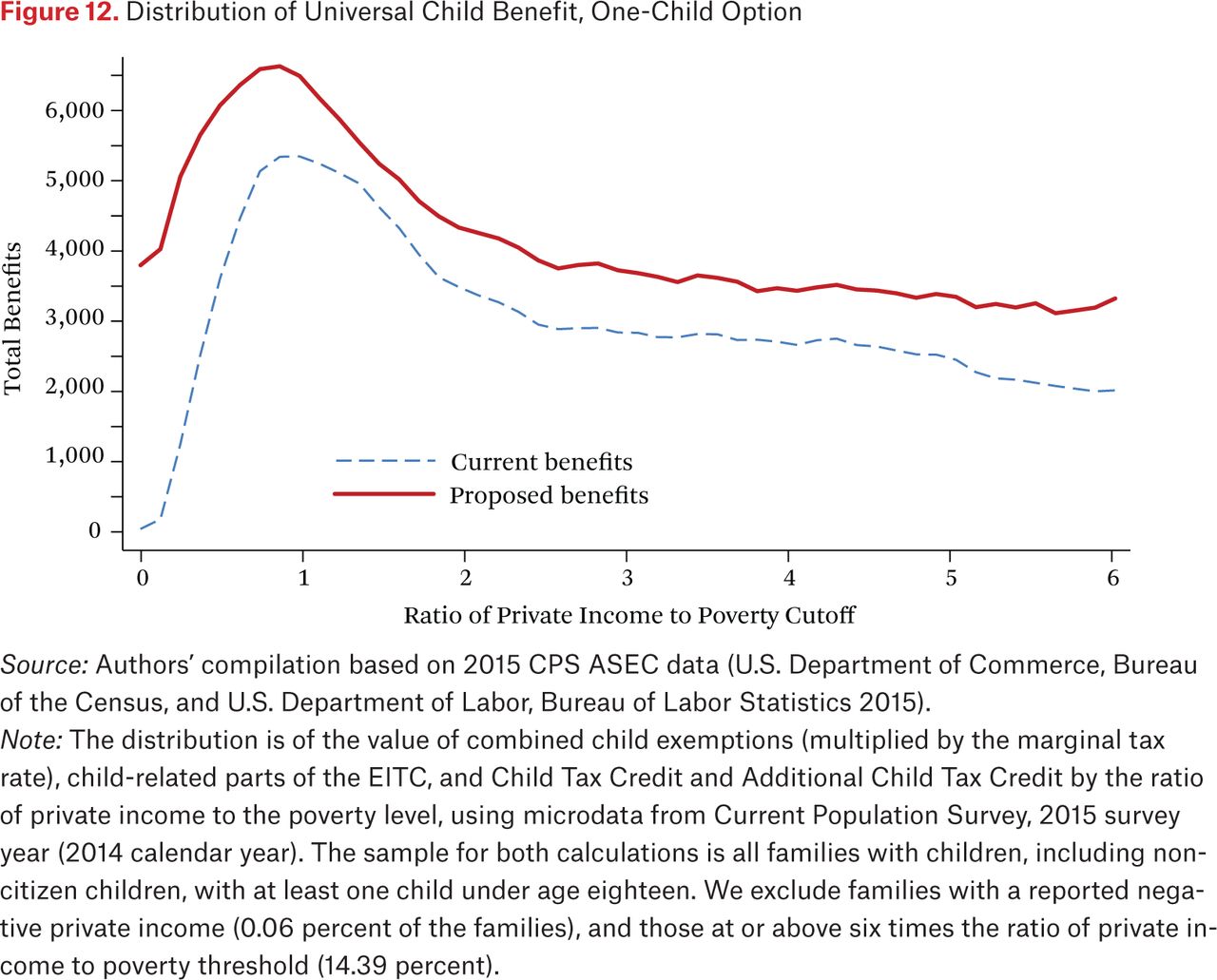

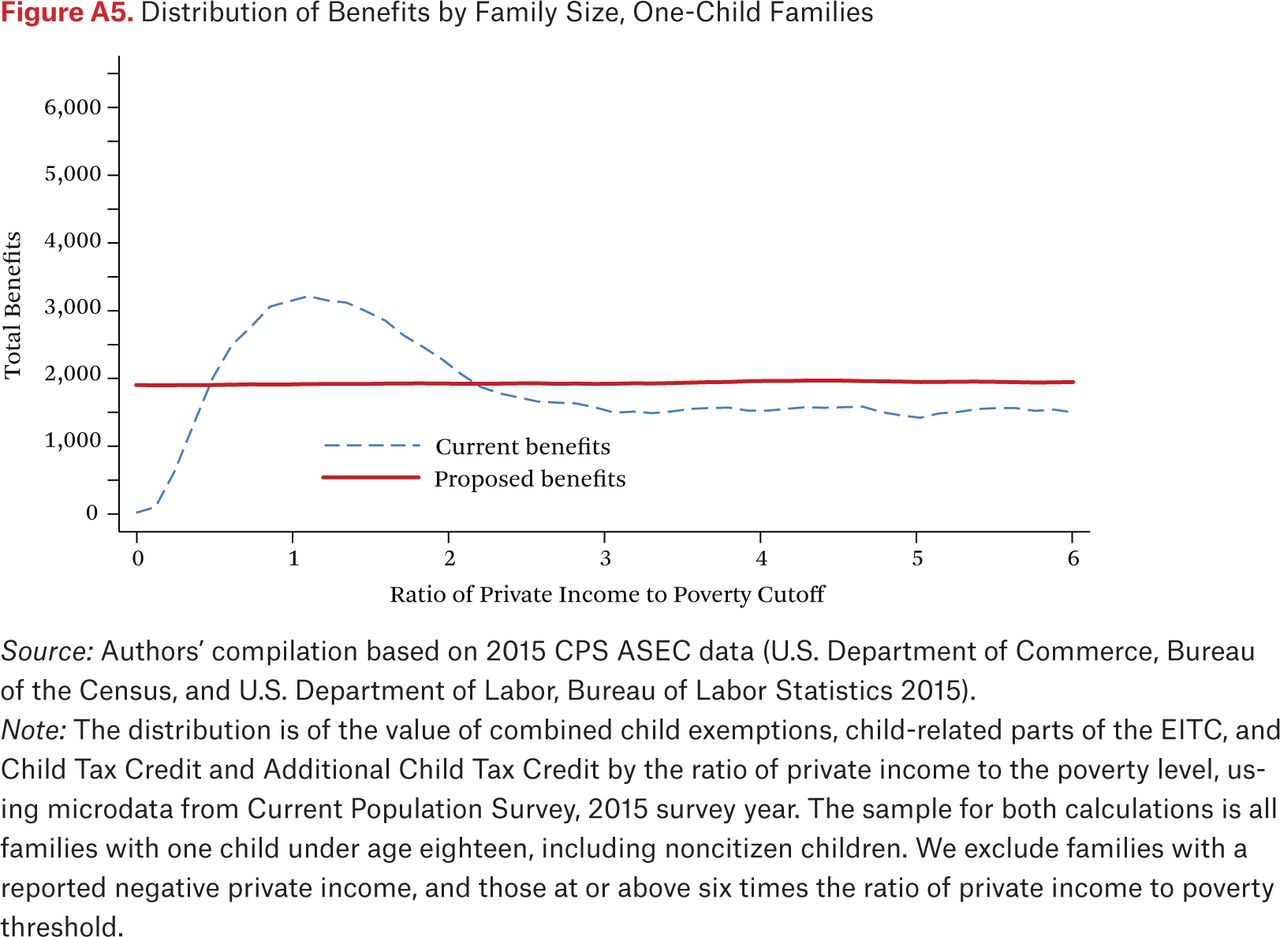

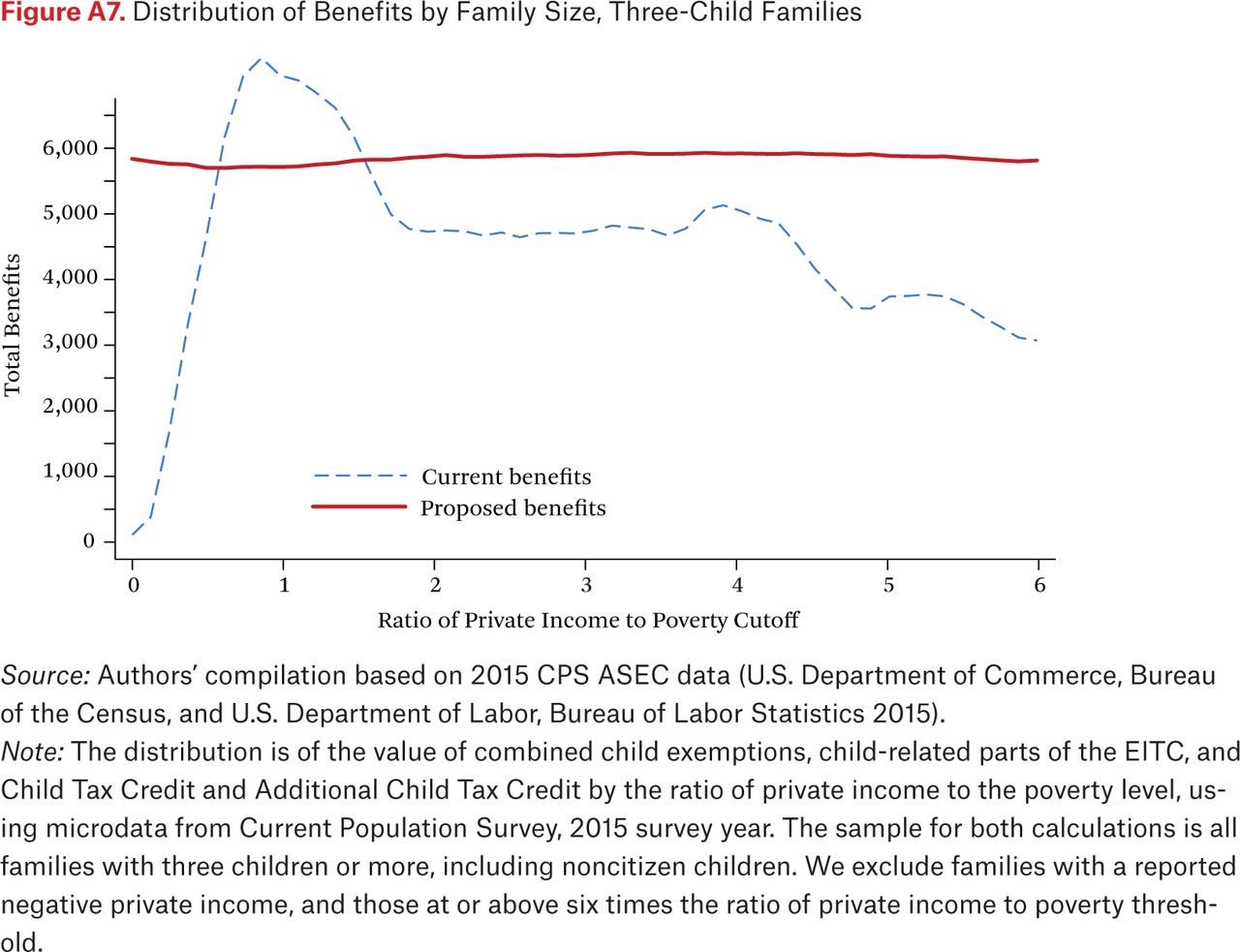

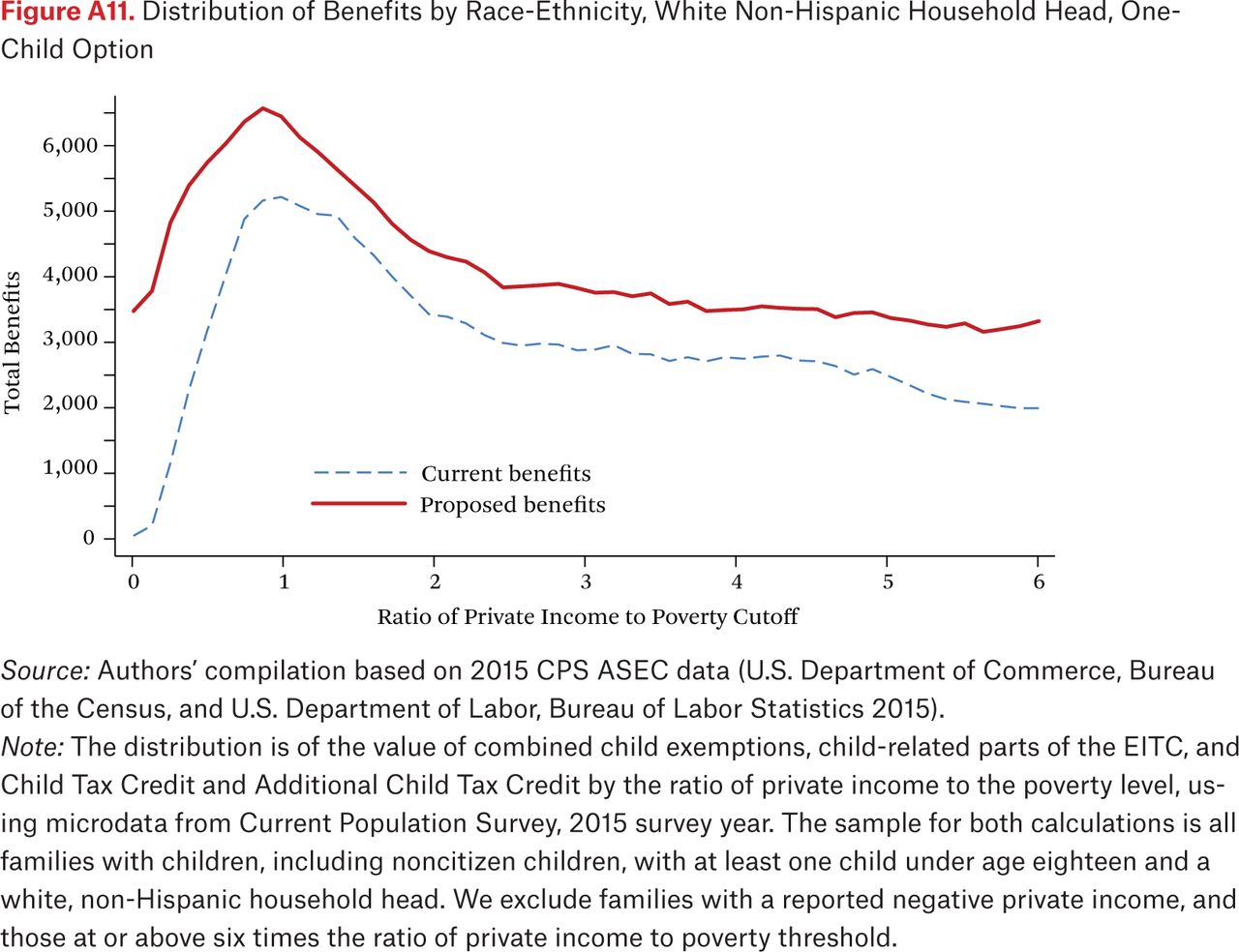

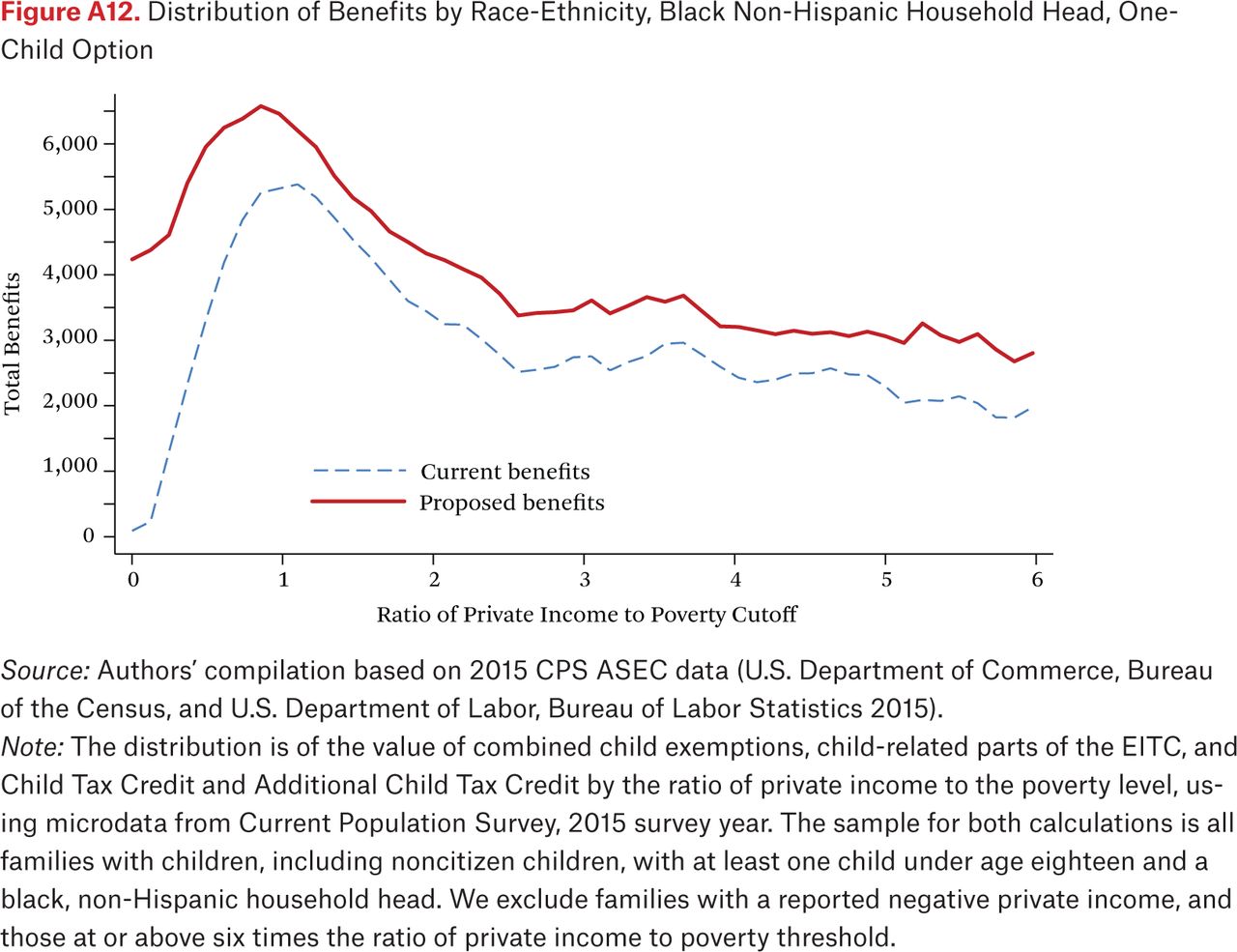

Figures 3 through 12 show how our revenue neutral proposal would change the distribution of government income support across families. The figures are based on data from the 2015 Current Population Survey ASEC, and plot the average benefit amount received by families with different (private) income-to-needs ratios under both the current system, and under our proposal. One can see immediately from figure 3 that repurposing funds from the EITC, CTC and child exemptions would increase government income support to children at the lowest end of the income distribution, and reduce support for many families with private incomes between 100 and 200 percent of the poverty line. Among those families (approximately 19 percent of those with children), the average cost of replacing the current array of tax benefits with a $2,000 universal benefit would be $1,203. This cost is balanced, however, by increases to families whose income is less than 50 percent of the poverty line (approximately 12 percent,). For very poor families, the average income gain would be $3,047.

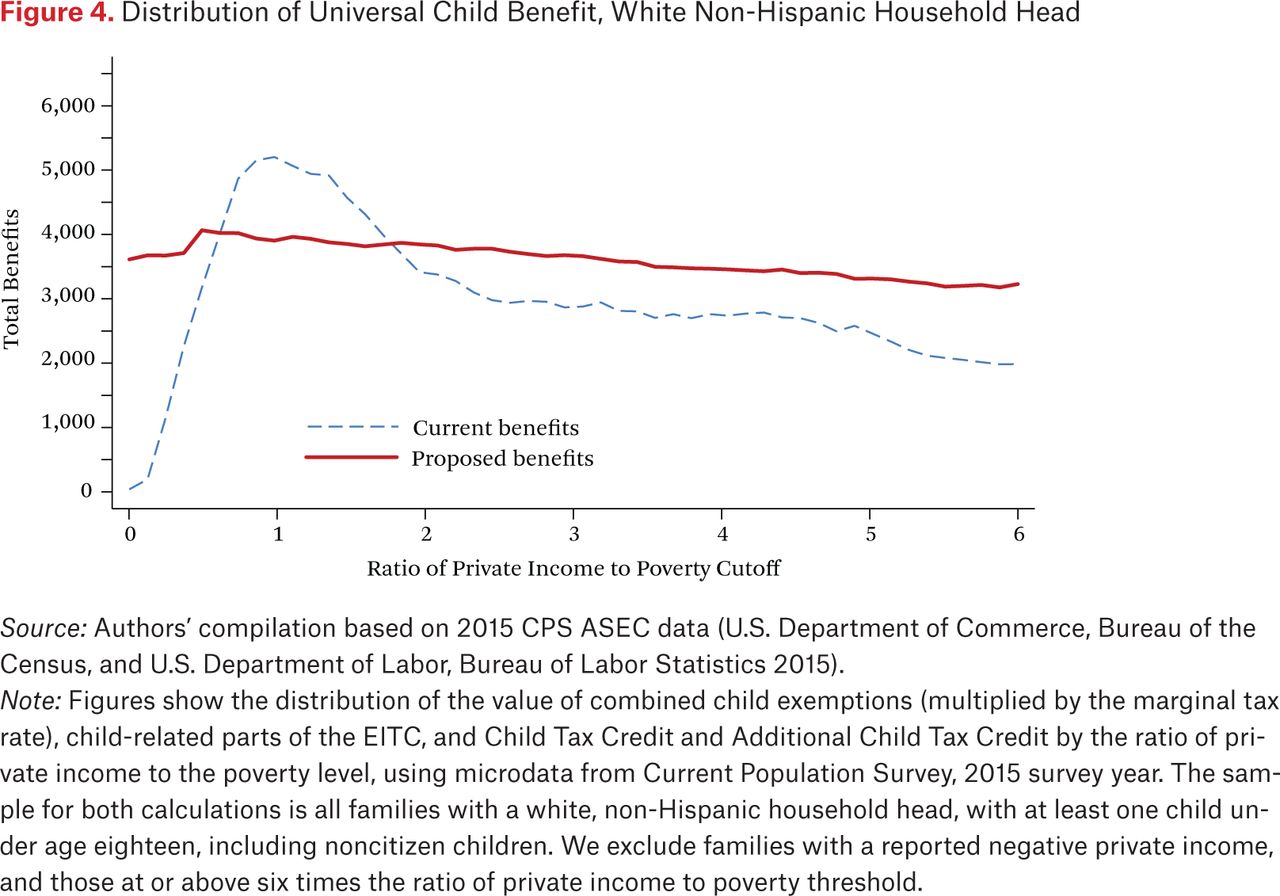

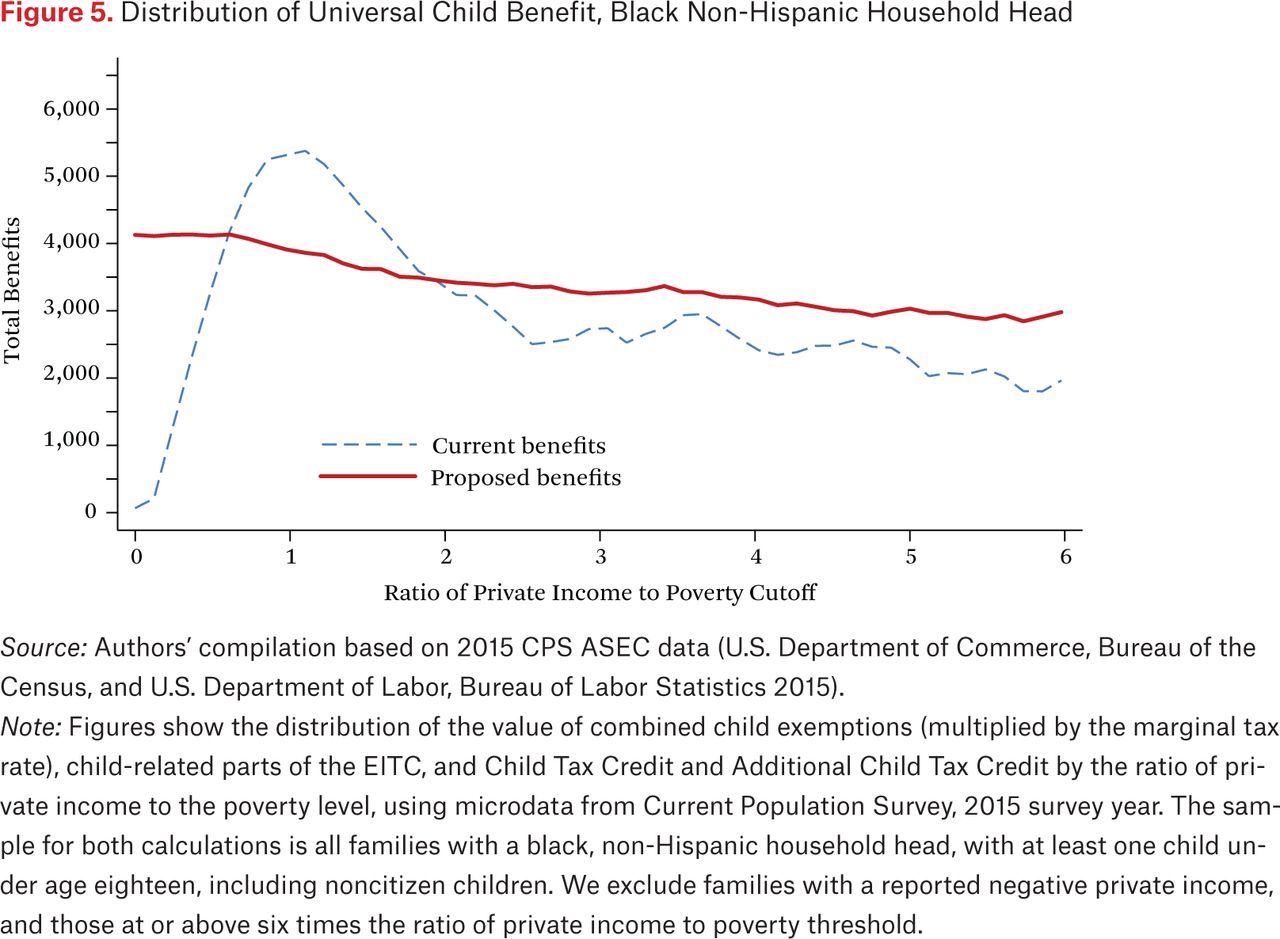

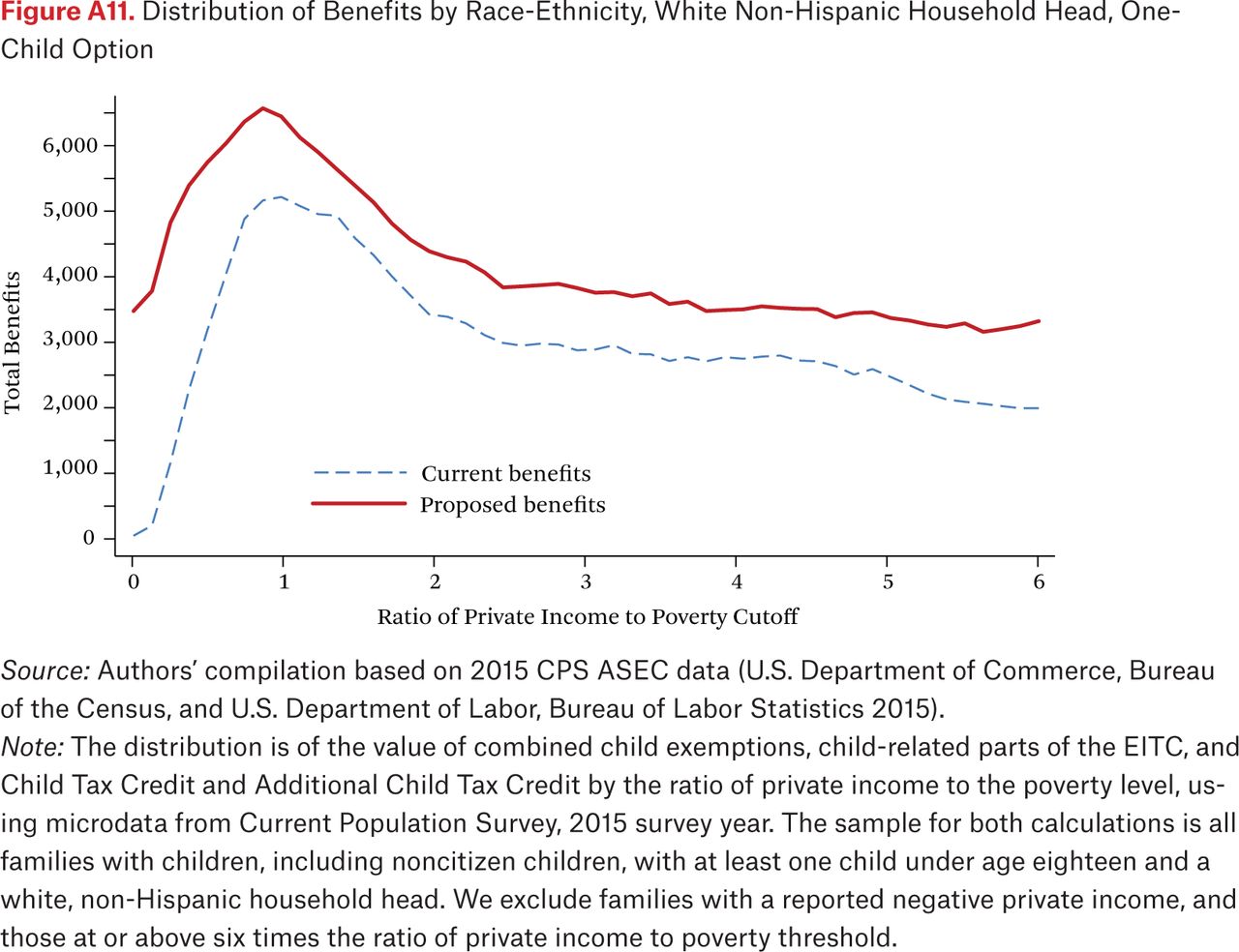

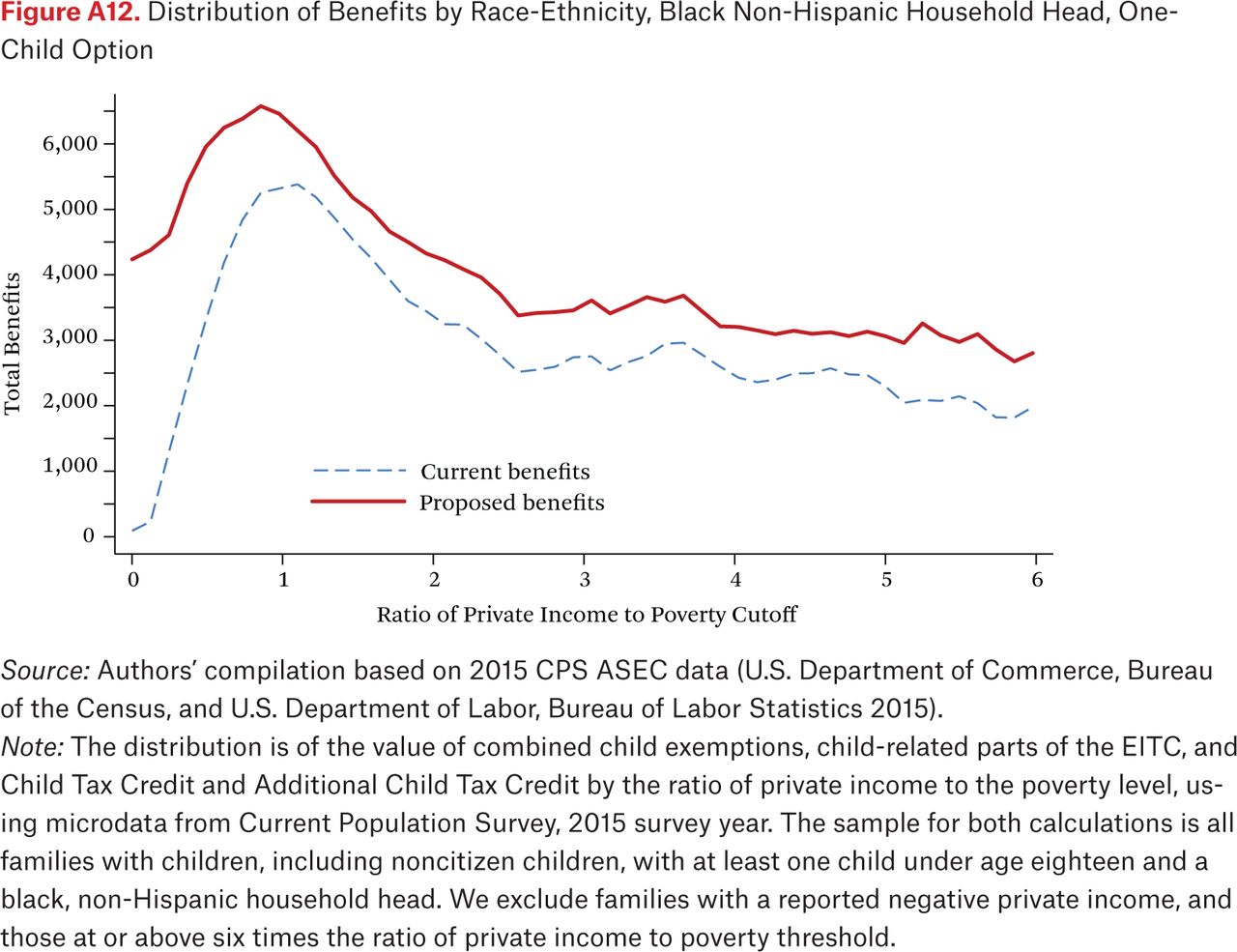

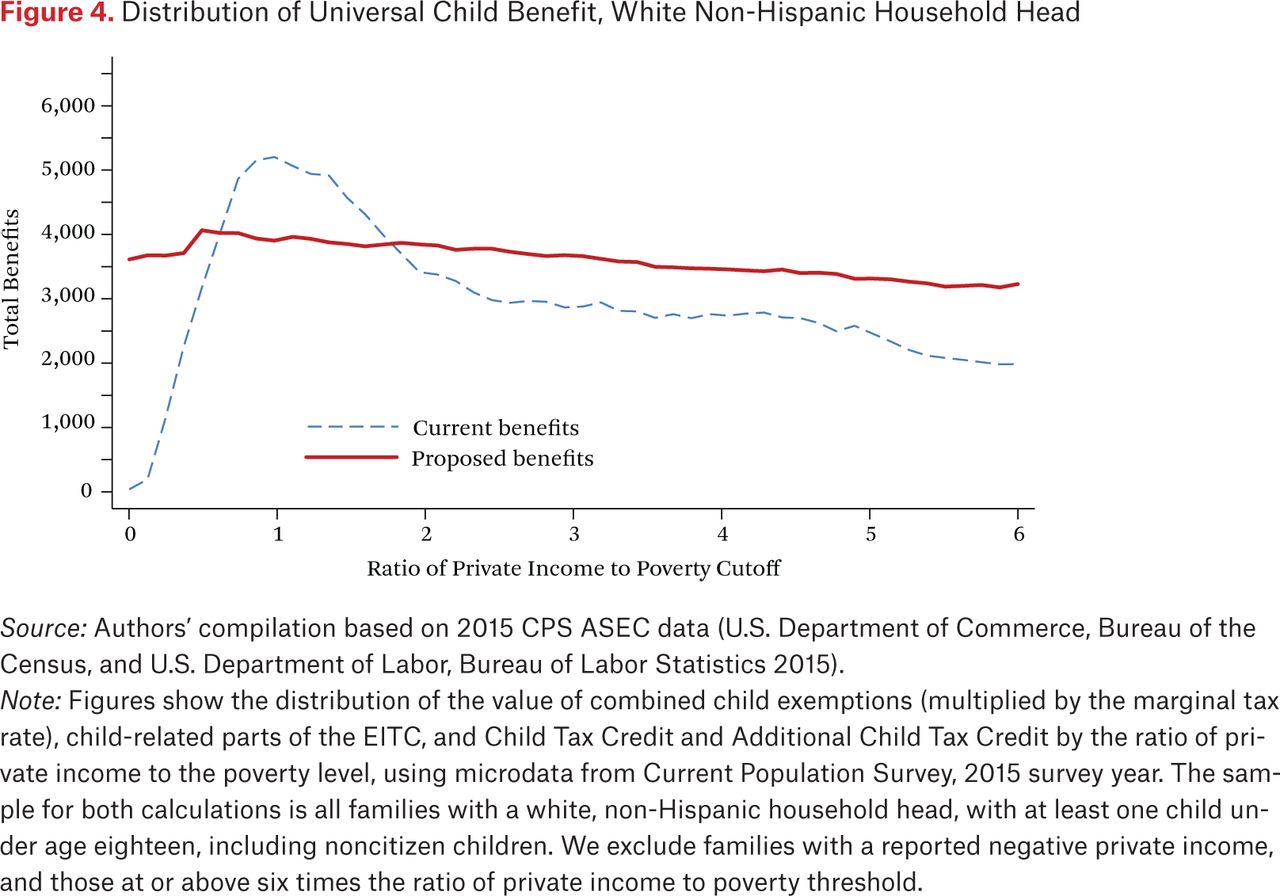

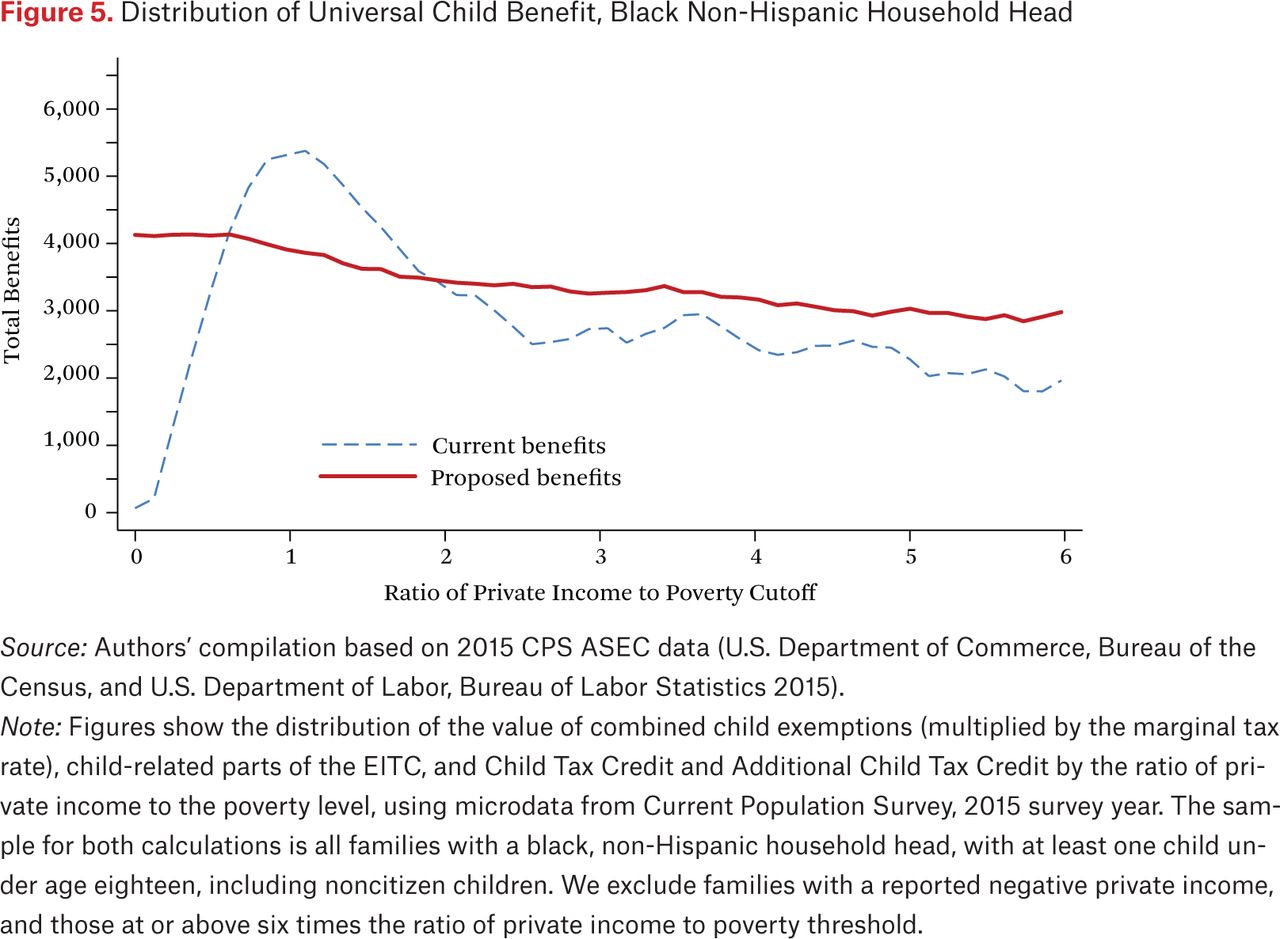

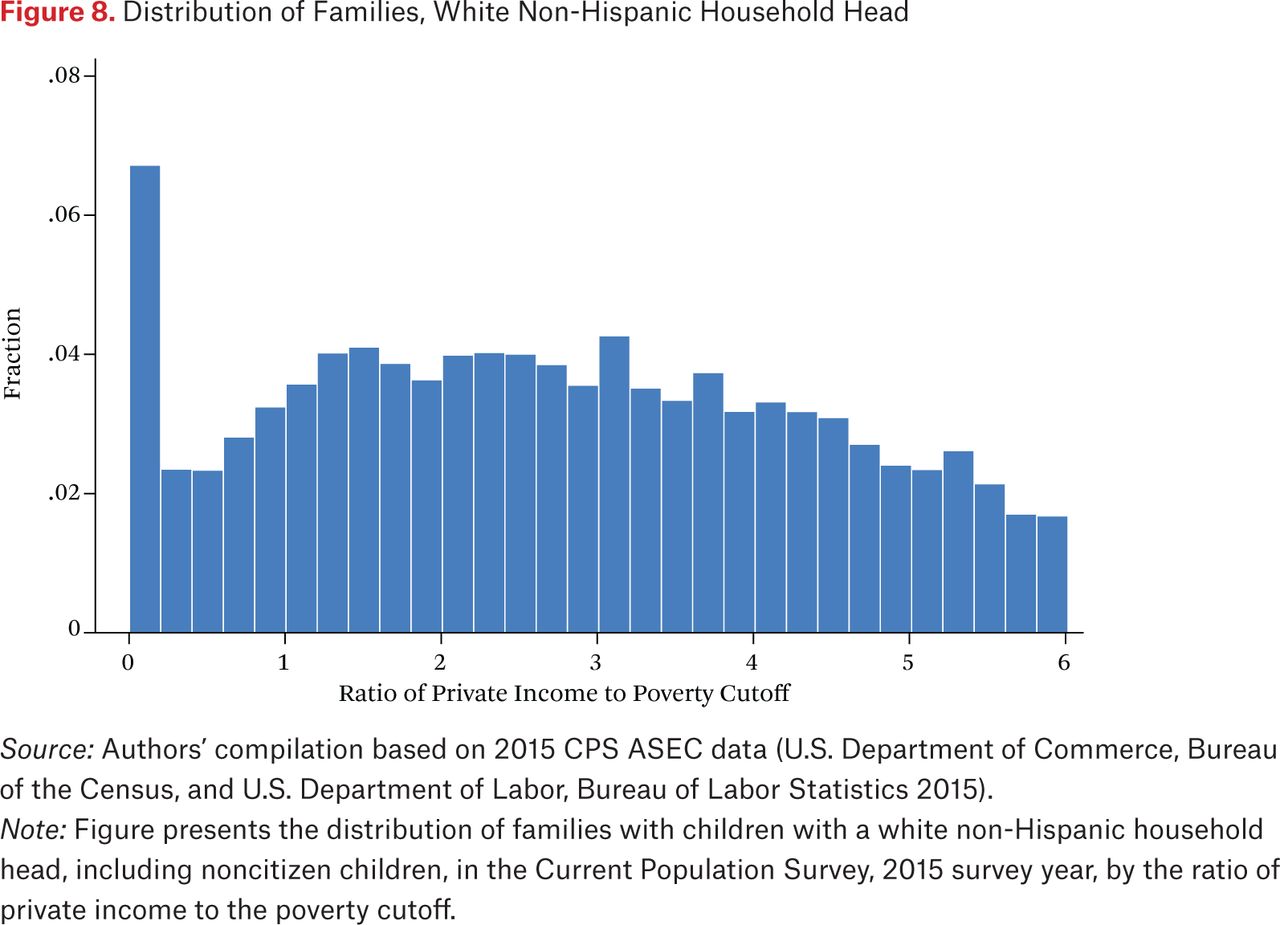

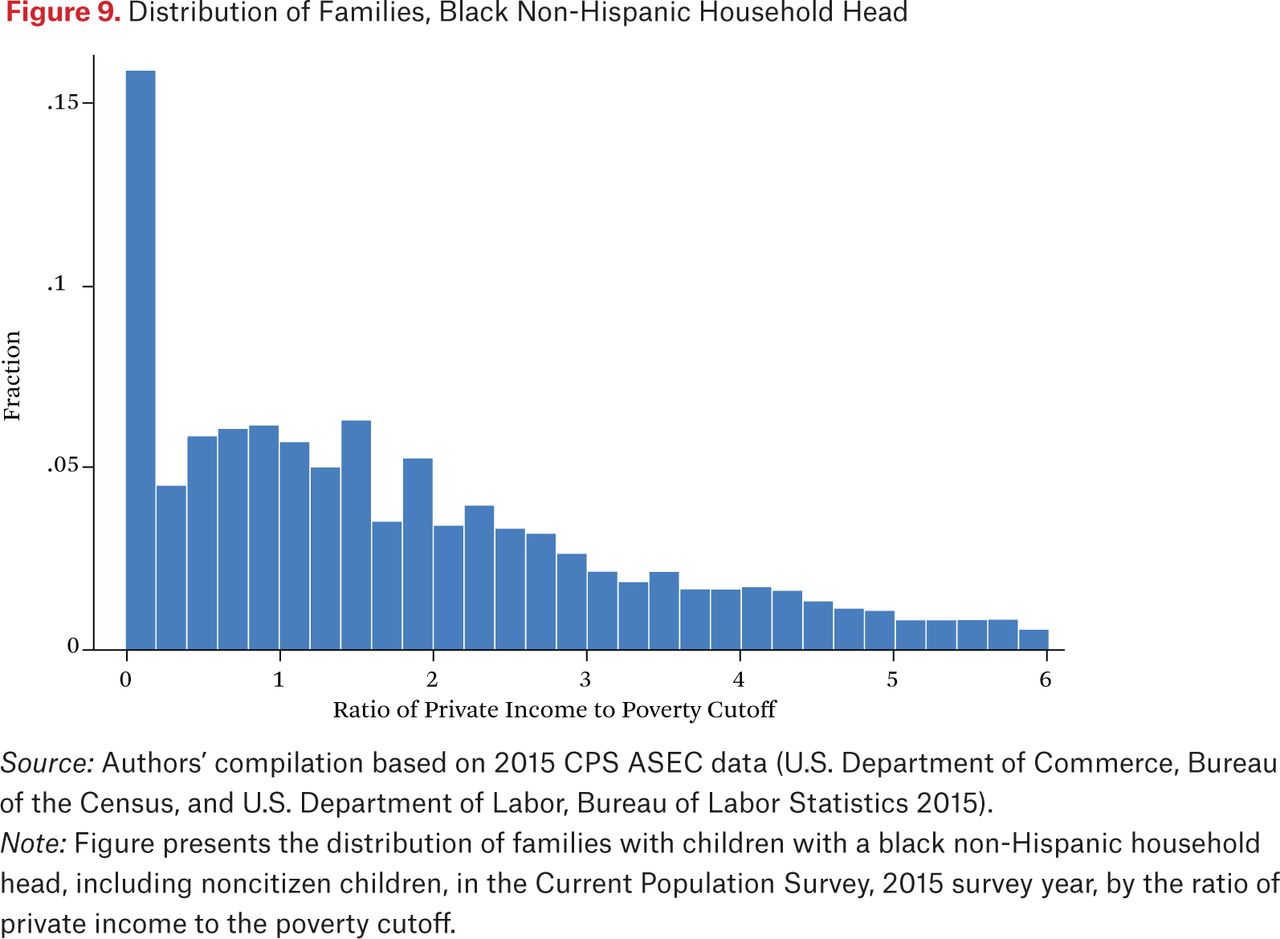

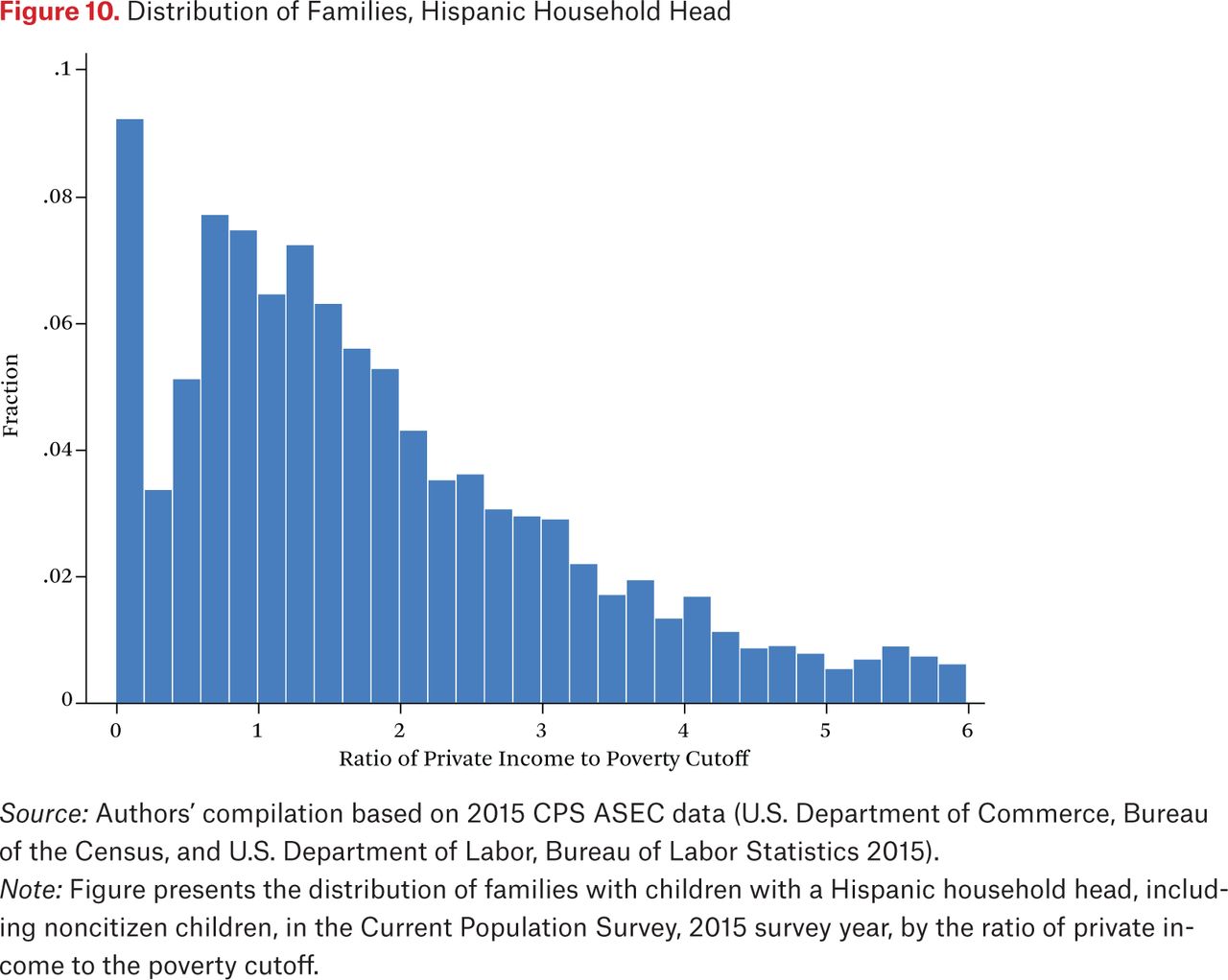

Figures 4 through 7 show that subsidizing the most economically disadvantaged children under our proposal would produce similar distributional effects within race and ethnic groups. What is not evident in the figures, however, is that children with different racial or ethnic identities tend to be located in different parts of the income-to-needs distribution. Figures 8 through 11 present histograms showing the fraction of families with different levels of income to needs by the race-ethnicity of the family head. It is clear that, relative to white non-Hispanic headed families, children in families headed by black non-Hispanics are much more likely to live in families with no private income. More than 15 percent of families with a black parent and a child under eighteen have no private income. The comparable statistic for the other demographic groups is 9 percent. Similarly, relative to non-Hispanic whites, many more Hispanic children live below the median of the private income-to-needs distribution.

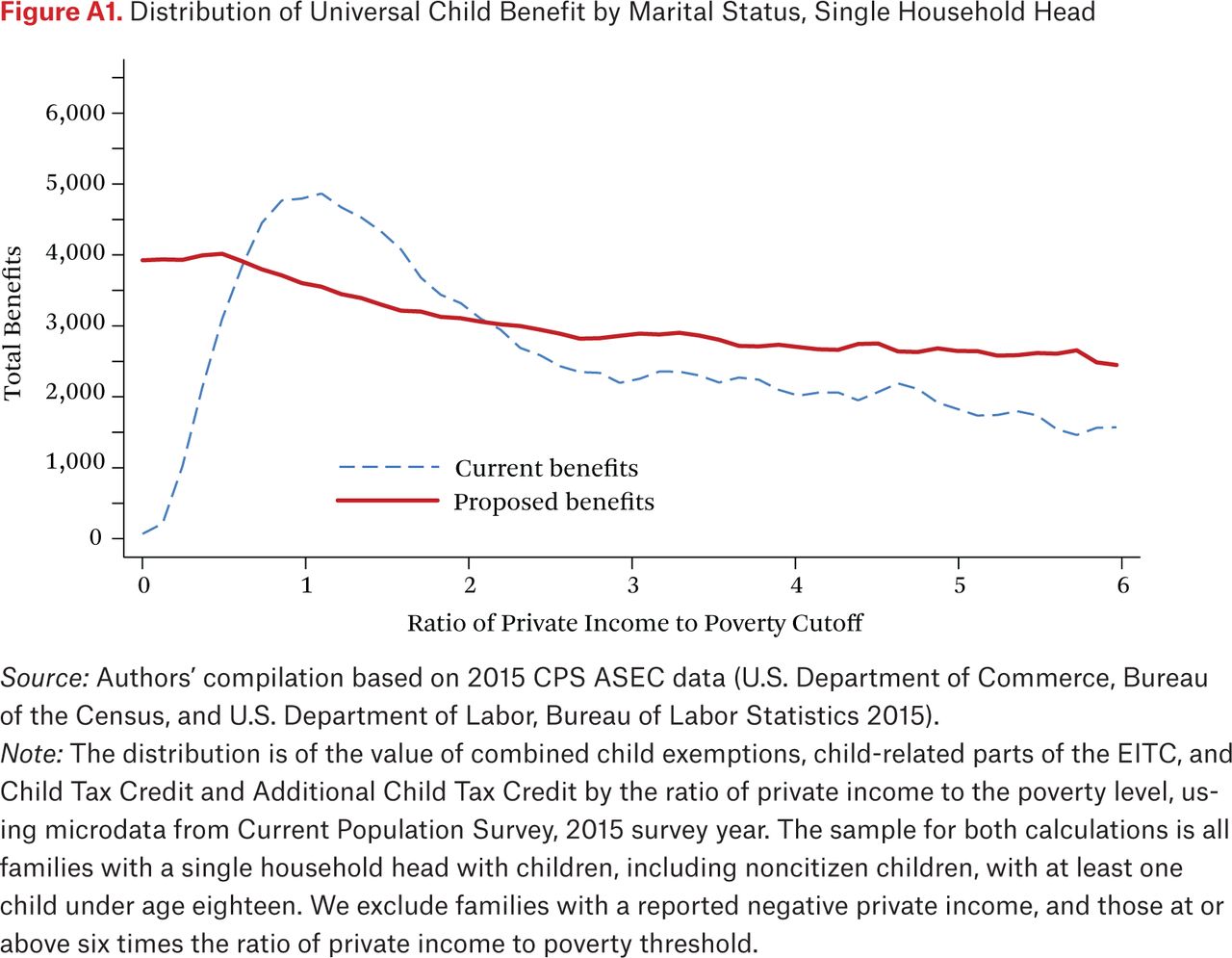

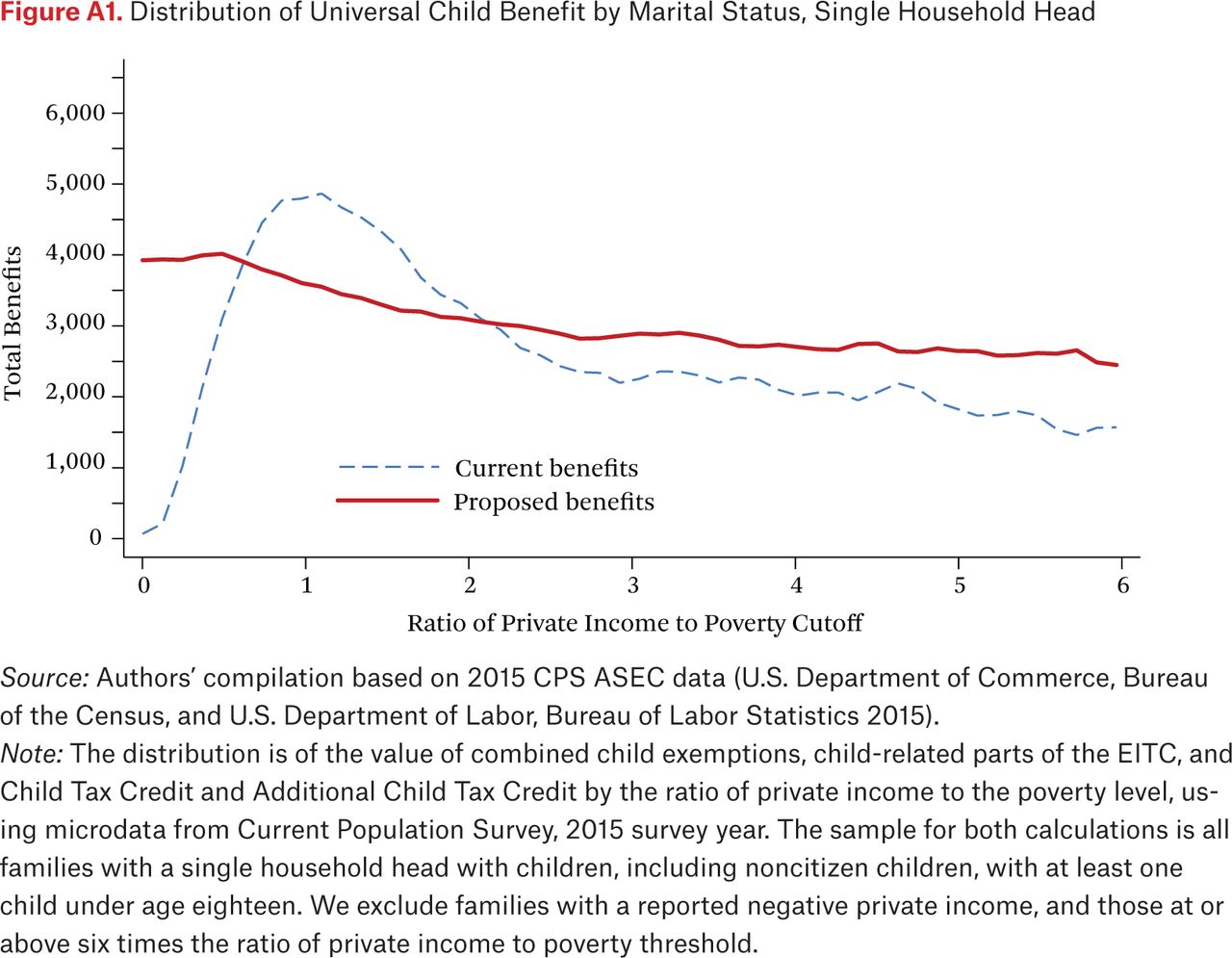

Thus, because black and Hispanic families are so much poorer than non-Hispanic white families, they are relatively more likely to gain from the repurposed funds. Figures A1 through A4 show that children living in single-parent-headed families would similarly benefit more than children in married-couple families: even though our proposal’s distributional effects are similar within marital groups, children living in single-parent families are disproportionately likely to have low income to needs.25 The first article in this issue also provides estimates, using a number of different metrics, of how our proposal would affect poverty.

Most of the income loss that near-poor families would experience under this revenue-neutral proposal is driven by our repurposing of the child-related parts of the EITC. If the feasibility of implementing a universal benefit requires that the government hold constant its current level of child-related tax expenditures, then we would support the replacement of the child-related component of the EITC with a universal child benefit because we believe that the cost to “less poor” children would be balanced by the gains to children whose families are even more disadvantaged. Rates of food insecurity, for example, are substantially higher among the very poor relative to the near-poor: nearly 25 percent of children living in families with incomes below 50 percent of the poverty line experience low food security, versus 16 percent of children whose family incomes are between 100 and 150 percent (Wight et al. 2014). Julie Siebens also documents a significant income gradient in material hardship (2013). As described earlier, the replacement of the current array of tax benefits with a universal child benefit would also ensure a fairer distribution of the government’s current monetary investment in children. Equality of opportunity cannot be achieved through government programs that tie the level of child benefits to the parents’ work effort.

Finally, among low-income families, the “churning” from one year to the next between states of near-poverty, poverty, and deep poverty is substantial, as is a concomitant churning in use of the EITC (Ackerman, Holtzblatt, and Masken 2009). Thus many of the families who would experience income losses because of a reduction in the EITC subsidy would do so only in some years. Our proposal would likely generate income gains to those same families in the years when they would not have been eligible for tax related benefits. Moreover, for families who experience high income volatility, the dependability of the income received through the universal child benefit could generate important psychological benefits.

Our cost estimates are based on the assumption that reducing the EITC earnings subsidy to the level currently available to childless adults would not affect parents’ labor force participation or earnings. A potential concern with any proposal that reduces the EITC subsidy is that the EITC is known to be effective at inducing individuals to either enter the labor force or to spend more time working. Because the EITC wage subsidy is substantially higher for families with children than for those without children, repurposing child-related EITC funds would likely reduce some parents’ incentives to work. This could be accommodated by altering the income span of the no-child EITC’s flat and phase-out ranges. It is also important that most studies that causally link income to poor children’s success are based on natural experiments that simultaneously alter parents’ labor force participation (for example, studies of job loss or of changes in EITC generosity). It may be that part of the documented resulting improvements in child well-being result from other changes in family dynamics that accompany changes in parental work.

To maintain the work incentives inherent in the current tax system, our preferred policy would be to simply divorce the government provision of child-related income support, which should be made on the grounds that all children are entitled to a basic standard of living, from government wage subsidies that are currently provided by the EITC but vary with family size. Figure 12 shows what would happen to the distribution of income support if we were to replace the child exemptions and and ACTC with our $2,000 universal child benefit, while maintaining the EITC for all families (including those without children) at the same subsidy and phase-out rates that are currently applied to families with one child (see also Shaefer et al. 2018). Under this proposal, average benefits would increase throughout the entire distribution. Using the CPS, we estimate that this proposal would cost an additional $74 billion.26 Approximately $9 billion would be recouped by repurposing the EITC benefits that currently go to families with more than one child, but it would cost an additional $83 billion to increase the small EITC wage subsidy currently provided to families with no children up to the level of the one-child EITC.27 The additional cost of this proposal could be covered by phasing out the universal child benefit for high-income families. The CTC currently phases out when families’ adjusted gross income exceeds $75,000.

Figures A11 through A16 show the distributional effects of this alternative proposal for different demographic groups. Once again, conditional on families’ income to needs, the effects across groups of providing the universal benefit plus the one-child EITC are similar, but because black, Hispanic, and single-head families are disproportionately at the bottom of the income-to-needs distribution, children in these families benefit more than white non-Hispanic children living with married parents. Obviously, providing low-income childless adults an EITC subsidy equivalent to the current one-child EITC would generate enormous gains for this group.

An alternative proposal that would preserve much of the EITC’s positive work incentives but would still cost less than the current system of benefits would be to provide all eligible families with dependents the one-child EITC wage subsidy, while maintaining the current EITC wage subsidy for those without dependents. This proposal would cost an additional $34 billion. From our perspective, a disadvantage of this proposal would be that it would continue to conflate the goal of providing work incentives with the goal of providing for children’s needs.

A few additional notes here are warranted. First, the simplest way of disbursing universal benefits would be through the Social Security system, because social security numbers are typically assigned to children shortly after birth. The only additional step that would be required would be to link parents’ information to their children. The Social Security Administration (SSA) already obtains address, employer, and earnings data from the IRS, which could be used to help track parents. It also currently distributes other benefits to children via the Social Security and Supplemental Security Income programs. We suggest that the mother (assuming one is present) be the default parental link to the child, because this would easily be determined at birth. When necessary, due to divorce or changes in custody, the reference parent could be changed at local SSA offices.

During the initial transition period, the tax system could be used to help identify eligible children and pass necessary information to the SSA. Eligibility for low-income children whose parents are nonfilers, or who are not in the Social Security system, could be determined via systems that assess eligibility for programs serving broad populations, such as Medicaid and SNAP. The provision of benefits to tax nonfilers could also be made automatically by providing information from state agencies and the IRS to the SSA, or by allowing families to register the link with their children at local SSA offices. Families who do not currently sign up for these programs or who file taxes could also obtain the benefit by voluntarily filing a tax return.28

SUMMARY

Although the United States provides cash assistance to low-income children through a variety of tax and transfer programs, the current system fails to reach many children. Income support for children whose parents are unable to work is particularly limited, yet children of poor, nonworking parents may be among our most vulnerable. Moreover, complexities associated with the current set of assistance programs that are available in the United States ensure that even many low-income children with working parents do not receive the support for which they are eligible. We propose that the United States should increase the financial resources available to poor children by providing an annual, universal, $2,000 per child benefit. We also argue that the case for a child benefit is distinct from that for incentivizing low-income adults’ labor supply: government investments in children should be made on the grounds of equality of opportunity, whereas programs such as the EITC should reward the same level of work effort equally across all adults irrespective of their family composition. The current system clearly mixes these goals while imposing many hurdles that make it difficult for low-income parents to make optimal investments. Our reform would address these challenges, and could be provided at limited cost by harnessing the dollars that are currently spent on the more complicated set of child benefits that are provided through the tax code.

APPENDIX

FOOTNOTES

↵1. Roughly 97 percent of children in the United States are citizens.

↵2. Recent work by Nathaniel Hilger questions this assumption (2016). Using an identification strategy that further accounts for individual characteristics, he still finds evidence that parental job loss has a small effect on children’s educational attainment, however.

↵3. Mass layoffs have also been found to negatively affect adult health (Sullivan and von Wachter 2009); parental health may in turn affect children’s outcomes.

↵4. Although Nathaniel Hilger does not find significant effects on later life earnings, his analyses focus on very young men, those under age twenty-five (2016).

↵5. Vouchers are currently provided through electronic benefit cards.

↵6. Our calculations are based on tables 2.3, 2.5 and 3.3 of the Statistics of Income Individual Tax Tables (2013a).

↵7. Samuel Lundstrom finds a coding error in their study; fixing this reduces the magnitude of their findings by one-third (2017).

↵8. For a list of studies and their associated estimates, see Kline and Walters 2016, table A.IV. Their numbers are based on these assumptions: childhood family income at the poverty line is about 26 percent of average family earnings, average discounted lifetime earnings are $522,000 in 2010 dollars (Chetty et al. 2014), and the discount rate is 3 percent.

↵9. Some studies suggest that the marginal propensity to consume food out of SNAP benefits is higher than it would be if cash benefits were increased. For example, Beatty and Tuttle 2015 examine the ARRA-funded increase in SNAP benefits and find that recipients do not respond to increases in benefits in the way the neoclassical model predicts. Using roll out of the Food Stamp program, however, Hilary Hoynes and Diane Schanzenbach find evidence that Food Stamp benefits are treated by recipients like cash (2009).

↵10. Neo-natal mortality estimates are not often statistically significant.

↵11. Their index of self-sufficiency is based on the individual’s levels of education, earnings, poverty status and participation in public-assistance programs. Their index of metabolic syndrome is based on measures of obesity, high blood pressure, diabetes, heart attack, and heart disease.

↵12. Estimates are based on the 2010 March CPS. Private income includes all earnings and unearned private income but excludes all government transfers and net taxes. Participation estimates are based on local linear regressions where an indicator for household participation is regressed on the ratio of private income to poverty. Bruce Meyer, Wallace Mok, and James Sullivan document that underreporting of transfers in the CPS and other household surveys has worsened over time (2009). As a result, the figure might understate true participation rates. However, unless underreporting is higher at lower levels of income, the figure should be informative about the distribution of program spending across the income to poverty distribution. If underreporting is higher at the bottom, the differences across the distribution should be even starker.

↵13. This participation estimate includes families who are not eligible for SNAP, and is therefore lower than estimates of take-up rates. It is also possible, given recent increases in underreporting, that these values are somewhat low. One study reports that for those eligible for SNAP, the participation rate among eligibles in 2011 was 77 percent (Cunnyngham, Sukasih, and Castner 2016).

↵14. It may seem strange that the EITC and SNAP are both received higher up in the income distribution than where their eligibility levels, as determined by poverty guidelines, end. But, the x-axis measures private income at the household level, divided by household poverty thresholds, and may accurately not represent the income and poverty thresholds of households with multiple family units. It also pools income across family units, and poverty is typically lower for big family units.

↵15. The literature on the administrative burden of public-benefit programs is extensive (see, for example, Aizer 2007; Brien and Swann 1999; Brodkin and Majmundar 2010; Heinrich 2016; Herd et al. 2013; Klerman and Danielson 2009; Moynihan, Herd, and Harvey 2015; Schanzenbach 2009; Schwabish 2012; Wolfe and Scrivner 2005).

↵16. For simplicity of design, we propose that the benefit be nontaxable. Taxing the universal child benefit would work against its main purpose by reducing its full value. Progressivity and cost savings could be built into the benefit by phasing it out for families with very high income.

↵17. Another body of literature shows that some children who are eligible for some government benefits but live in families with immigrant members do not participate in these programs because of concerns that claiming benefits will lead to difficulties with becoming naturalized citizens (for example, Watson 2014).

↵18. To maintain its real value over time, the universal benefit would be indexed using the CPI or PCE.

↵19. Exceptions are SSI, TANF, and housing assistance programs, which include significantly larger work disincentives. Of course, our universal credit might be expected to have negative effects on labor force participation in the range of the current EITC phase-in, but the magnitude of any negative effects would be reduced by leaving the current no-child EITC in place, or expanding the generosity of the no-child EITC credit.

↵20. The roll-out was associated with an annual reduction of about three hundred hours for participating households, but had no evident effect on family earnings (Hoynes and Schanzenbach 2012).

↵21. For comparability with estimates in Christopher Wimer, Sophie Collyer, and Sara Kimberlin’s article in this double issue (2018), our estimate is based on calculations from the Current Population Survey. We use the 2015 CPS because at the time of this writing, the imputed tax items in the 2016 CPS were not available. CPS estimates will differ somewhat from estimates elsewhere in this article that are based on the SOI data because the CPS does not survey all groups who file taxes (such as some military families). The SOI data also exclude nonfilers but may include individual claims that will later be disallowed (such as after an audit). Another difference between the datasets is that the CPS distinguishes citizens from noncitizens, which is relevant to our proposal. Citizenship status cannot be determined in the SOI, although filing for children lacking a SSN or Taxpayer Identification Number is not allowed.

↵22. Using funds from the CTC, Additional CTC and child-dependent exemption to fund a universal child benefit is similar to the proposal put forward by Shaefer and his colleagues in this issue (2018). A critical difference between our proposal and theirs is that our proposal would also harness funds from the EITC and comes closer to being revenue neutral.

↵23. The estimated value of the child exemption is based on the amount of the dependent exemption in 2013, which was $3,900. We multiply this amount by the average marginal tax rate of 14.7 percent.

↵24. For example, a married couple with two children and adjusted gross income of $150,000 is still eligible for the credit.

↵25. We also analyzed the proposal’s distributional effects by family size (see figures A5 through A7).

↵26. This assumes no increase in take-up among no-child families.

↵27. In contrast, if we provide all families with children the EITC wage subsidy currently available to families without children (as in our revenue-neutral proposal) then we are able to repurpose a net amount of $43 billion toward the universal child benefit using the SOI numbers.

↵28. Some challenges would be associated with distributing benefits to children whose parents split custody. One option would send the benefit to the parent the child is living with most of the time. Over time, however, benefits might be capitalized into child-support agreements.

- © 2018 Russell Sage Foundation. Bitler, Marianne P., Annie Laurie Hines, and Marianne Page. 2018. “Cash for Kids.” RSF: The Russell Sage Foundation Journal of the Social Sciences 4(2): 43–73. DOI: 10.7758/RSF.2018.4.2.03. We thank Hilary Hoynes and Elira Kuka for sharing code from joint work with Marianne P. Bitler related to use of SOI and CPS data (Bitler, Hoynes, and Kuka 2017). Direct correspondence to: Marianne P. Bitler at bitler{at}ucdavis.edu, Department of Economics, University of California, Davis, One Shields Ave., Davis, CA 95616; Marianne Page at mepage{at}ucdavis.edu, Department of Economics, University of California, Davis, One Shields Ave., Davis, CA 95616; and Annie Laurie Hines at ahines{at}ucdavis.edu, Department of Economics, University of California, Davis, One Shields Ave., Davis, CA 95616.

Open Access Policy: RSF: The Russell Sage Foundation Journal of the Social Sciences is an open access journal. This article is published under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

REFERENCES

In this issue

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.